ACCTG 414 Final Exam review Jocelyn’s Office hours – All...

24

ACCTG 414 Final Exam review Jocelyn’s Office hours – All students in 414 are welcome Tuesday Dec 10 Noon – 2 pm Wednesday Dec 11 Noon – 3 pm Thursday Dec 12 Noon – 3 pm Friday Dec 13 Noon – 2 pm Or you can use the discussion board. For the final exam

Transcript of ACCTG 414 Final Exam review Jocelyn’s Office hours – All...

ACCTG 414 Final Exam review

Jocelynrsquos Office hours ndash All students in 414 are welcomeTuesday Dec 10 Noon ndash 2 pmWednesday Dec 11 Noon ndash 3 pmThursday Dec 12 Noon ndash 3 pmFriday Dec 13 Noon ndash 2 pmOr you can use the discussion board

For the final exam

o Time Dec 14 2013 Saturday 1400 ndash 1700 (Consolidated exam 3 hours)

o Location Pavilion Rows 2468o Arrive at least 30 minutes before the start time of the exam

o Bring a non- programmable calculator

o Please bring Your One Card or a piece of government issued picture ID with you

o Read each question Carefully ndash answer all parts

o Budget your time

Rough Split of pre midterm versus post midterm questionsCh 1-5 appendix Approx 25 Ch 6-11 Approx 75But remember that much of the new material builds on material from earlier chapters

Note

This document is not an exhaustive summary of all materials covered this term but this quick review may be helpful to you in studying It is not a replacement for reading the text and doing the assigned questions

You may wish to add your own notes into this document

Ch 1 and 2 Objectives of Financial Accounting

To communicate financial information to parties outside the business organization

1 Equity Investors 4 Suppliers2 Creditors 5 Customers etc3 Employees

Financial StatementsThe four basic financial statements Statement of Financial position Income Statement statement of comprehensive income Statement of Cash Flows Statement of Retained earningsshareholdersrsquo equity Most companies prepare financial statements at the end of each year (called annual reports) and at the end of each quarter (called quarterly reports)

General justification for ASPE GAAP vs IFRS

Cash Basis vs Accrual Basis Recognition Criteria

Accrual basis Cash basisRevenue When earned When cash is receivedExpense When incurred When cash is paid

Review the conceptual framework

What type of questions would you ask

Appendix - The accounting cycle

The Recording Process Journal entries Unadjusted trial balance Adjusting entries Adjusted Trial Balance Financial statement preparation Closing entries Post closing trial balance Reversing entries are optional ndash not required in this course

The Journal EntriesTransactions recorded using double entry bookkeeping

Debits Dr Credits Cr

Journal Entries and T-accounts

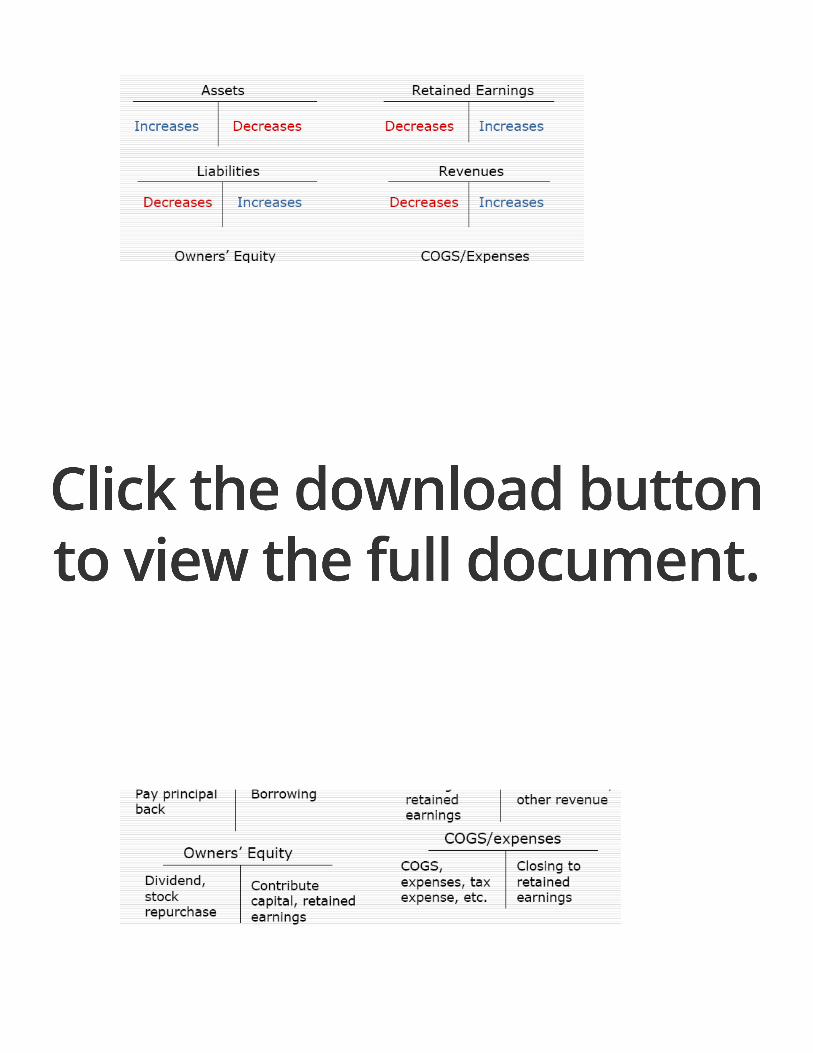

Increases in assets are debited and recorded on the left side of the T-account

Increases in liabilities are credited and recorded on the right side of the T-account

Increases in revenues are credited and recorded on the right side of the T-account

Increases in expenses are debited and recorded on the left side of the T-account

Remember that the balances of the permanent accounts carry over to the next year

Remember that the income statements accounts (revenues and expenses) will be closed through closing entries by the end of each reporting period

T-Accounts You can use balances from T-accounts to prepare financial statements at the end of a fiscal period

Basic Accounts

Adjusting EntriesAdjusting entries record activities that have taken place but which have not yet been recorded Four scenarios1 Cash first expenses later eg Prepaid expense office supplies purchased for later use PPampE purchased2 Expenses first cash later eg Wages accrued but not paid purchases of inventory on credit3 Cash first revenues later eg Unearned revenues 4 Revenues first cash later eg Interest revenues accrued credit sales

Involve at least one temporary account (revenue expense) and at least one permanent account (asset liabilities) They NEVER involve cash

Trial BalancesPurpose To ensure both sides on an entry recorded at the same amount ndash do not guarantee that your entries are correct but do reduce errors

Closing EntriesBridge the Income Statement and Statement of Financial Position ( through) Retained EarningsClose Revenue into RE by

Dr Revenues Cr Retained earnings

Close COGSExpenses into RE byDr Retained earnings

Cr COGSExpensesWhat about dividends Ensure that any dividends declared are closed to retained earnings You can use the income summary if you wish

Sub-ledgers and special journals

What questions might you ask

Ch 3 - The Income Statement and Comprehensive Income

The income statement measures firm performance regardless of when cash is exchanged Key principle

Single step vs Multi stepSingle step

Revenues + gainsLess Expenses and losses=Net income before taxesless Taxes ndash as these mush be shown separately=Net Income

Multi stepRevenues( from operations only)Less COGS=Gross Profitless Operating expenses= operating incomeless Non operating expenses=Net income before taxesless Taxes=Net Income

Function vs Nature

Function- Sort by functional area of the business eg sales admin engineering RampD etc You need to have the costs split by function in order to do thisNature ndash Sort expenses by type eg Utilities office professional fees etcLook at the accounts you are given and use this to determine the better approach Smaller businesses generally sort by nature bigger organizations with more separation by departments may use function

Income statement Equations

Revenue ndash Cost of Goods Sold = gross profitNet Income + - Other comprehensive income = comprehensive income

Components(IFRS and ASPE GAAP)

o Heading ndash for the [year] ended [date] or other period coveredo Revenues -Sales or service revenueo Gains -eg selling an equipment for cash greater than its net book valueo Expenses -Cost of goods sold operating expenses etco Losses eg selling an equipment for cash less than its net book valueo Other revenues and expenses

o Interest revenue dividend income interest expense

Income from Continuing Operationso Discontinued Operations

o Income or Loss from Discontinued Operations net of taxo Gain or Loss on Disposal of Discontinued Operations net of tax

Net income

IFRS onlyo +- Other comprehensive income

Comprehensive income

Differences between IFRS and ASPE

Accounting for discontinued operations and intra-period tax allocation

Earnings management

Typical Questions

Ch 4 - The Statement of Financial Position Statement of Retained Earnings Changes in Shareholdersrsquo Equity and Disclosure

STATEMENT OF FINANCIAL POSITION

Equation Assets = Liabilities + Shareholdersrsquo equity

Components of the Statement - Heading ndash as at [date]- Assets Economic benefits owned by the business as a result of

past transactions - Liabilities Debt and other obligations of the business that result

from past transactions - Shareholdersrsquo equity Residual claim of and financing provided by

the owners of the business- Current vs Non Current- Major categories

o Review major categories for presentation- Order of accounts

o Assets- liquidityo Liabilities ndash time to maturityo Sh Equity - permanence

STATEMENT OF RETAINED EARNINGSThis is reported as a solo statement under ASPE GAAP onlyOpening Retained Earnings + Net Income - Dividends = Closing Retained Earnings

STATEMENT OF CHANGES IN SHAREHOLDERSrsquo EQUITYIFRS OnlyA continuity schedule of opening balances +- changes = closing balance for each component of shareholders equity including retained earnings

Financial statements - Note DisclosurePurpose to provide supplementary information about the financial condition of the company

- Describe accounting policies followed by the company - Provide additional detail about an item on the financial statements- Provide additional information about an item not on the financial

statements- Subsequent events consider the difference in treatment of the two

types of subsequent event

Typical Questions

Ch 5 ndash CASH FLOW STATEMENT ndash indirect method only

Cash and Cash equivalentsbull Cash on hand Bank balancesbull Bank overdraftsbull Short term risk free investments with maturity dates within 3 months

Reports the changes to other accounts that affect a change in cash and cash equivalents on the SFP The change in the cash account is usually not equal to net income

Revenues reported do not always equal cash collected (credit sales)Expenses reported do not always equal cash paid (prepaid expenses)

In relation to the SFP The sum of cash flows from operations cash flows from investing and cash flows from financing must equal to the change in cash and cash equivalents on the SFP

Statement of Cash Flows reports operating cash flow as well as other cash flow information

Provides important information to investors and creditors In particular information about differences in the timing of revenue and

expense recognition under GAAP and the associated cash inflows and outflows

Preparing a cash flow statement Heading - for the [year] ended [date] or other period covered

Cash flow provided by (used in) operating activities (Indirect method)Net IncomeAdjust for Non-Cash Changes in non-cash WC accounts

- Subtract increase in assets- Add decreases in asset- Add increase in liabilities- subtract decreases in Liabilities

Adjust for non cash items included in net incomeAdd Depreciation amp AmortizationAdd Loss on Sale of AssetsSubtract Gain on Sales of Assets

Cash flows provided by (used in) investing activitiesCash paid for long-term assetsCash proceeds from the sale of long-term assets

Cash flows provided by (used in) financing activitiesCash dividends paidCash received on issuing debt ndash ie borrowingCash paid for retirement of debt

Cash received from issuance of common shares Ch 6 - Revenue and Expense RecognitionWhy do we care about revenue recognitionRevenue has a BIG impact on bottom-line profitability managers may be tempted to manage revenue

Criteria for revenue recognition ndash existing standardA firm recognizes revenue when it has

bull Performance achievedbull Measurability of the revenues and associated remaining costsbull Collectability is reasonably assured

Revenue is most often recognized at the time of sale as long as- Reasonable estimate of uncollectible amount - Reasonable estimate of sales returns - Reasonable estimation of all other material expenses representing

uncertain future outflows (eg warranty costs) - Most common in retail wholesale amp manufacturing - Even when right of return exists as long as the company has

booked reasonable allowance for sales return we can still recognize revenues at the point of sale

If there is uncertainty in the three criteria then wait until the uncertainty is resolved

Criteria for revenue recognition ndash proposed standardIFRS

1 Identify the contract(s) with the customer ndash May be explicit or implicit

2 Identify the separate performance obligations ndash may be one or many

3 Determine the transaction price ndash using either weighted probabilities method or most likely amount You must determine an amount for revenue This is very different from the existing approach

4 Allocate the transaction price to the performance obligations

5 Recognize revenue when a performance obligation is satisfied

Review the two cases covered in the lectures

MethodsPercentage of completion method - Recognize revenue and profit as contract progresses Extent of completion at any one point in time is determined by the costs incurred to date divided by the total estimated costs of the contract If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Completed contract method - Recognize revenue and profit when the contract is complete If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Percentage of completion methodReview profitable contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Given

Gross profit I - A

AND Loss contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Plug this

Total estimated Loss Calc this

(Profit) Loss previously recognized Prior yrs

Gross profitTypical Questions

Ch 7 ndash Financial Instruments Cash Receivables and Payables

CashCash and Cash Equivalents ndash Identifying amounts to be included in cash equivalents ndash See chapter 5 material

Accounts Receivable

Relevant Formulae

1 Ending AR = Beg Bal AR + Credit Sales ndash Cash Received ndash Write-off + 0 Recovery of previous write-off2 Ending Allowance for doubtful accounts (ADA) = Beg Bal AFDA + Bad

Debt Expense ndash Write-off + Recovery of previous write-off

Two approaches to determining Allowance for Bad Debts

1 Percentage of (Credit) Sales (Income statement approach)2 minus Focuses on calculating the Bad Debt Expense recorded for the year

Aging Method (Balance sheet approach)3 minus Focuses on calculating the Ending Balance of Allowance for Bad

Debts 4 minus Bad Debt Expense is a ldquoPlugrdquo

Accounts Receivable Relevant entries 0 Credit sales Dr Accounts receivable

Cr Revenue 2 Record bad debt expense 0 Dr Bad debt expense 0 Cr AFDA 3 When bad debt happens (when we are sure a specific customer

defaults) Dr AFDA 4 Cr Accounts receivable5 Recovery of bad debt 6 Dr Accounts receivable7 Cr AFDA 0 Dr Cash1 Cr Accounts receivable

Notes receivablePayable- Notes written promises- May be at a market rate of interest ndash no discounting needed- May be at a low rate on interest ndash discount the face value of the

note and the interest payments at the market rate- May be at no interest ndash discount the face value at the market rate

of interest

Other items

Sales discounts- Account for sales discounts by recording ldquoallowance for sales

discountsrdquo o A contra account for sales revenue on Income statement

Customer return merchandise- Debit to ldquoSales returns and allowancesrdquo

o A contra account for sales revenue on Income statement

Year-end adjusting entry to account for an estimated amount of sales return and merchandise return

- Credit to Allowance for sales return and allowance - A balance sheet contra account attached to accounts receivables

Transfers of ARIdentify if the transaction is to be accounted for as a sale or a borrowing transaction

Sale transactionsJournal entries to remove the AR any associated AFDA record the receipt of cash the residual obligation if any and a loss on disposal

Borrowing transactionsJournal entries to record the new debt and interest costs fees The AR and associated AFDA remain on the books

Types of Questions

Ch 8 Inventory12 INVEB = INVBB + Purchase ndash COGS

Inventory is recorded on the SFP at the lower of the cost or the net realizable value of the inventory

Key equation Beginning Inv+ Purchases - COGS = Ending Inv

IssuesConsignment inventory - Consignment inventory on the firm premises owned by others should be excluded Consignment inventory of the firm held elsewhere should be included in the inventory of the firm

Goods in transit at period end - Items shipped FOB shipping point are considered to have been sold when shipped Items shipped FOB destination are not considered to have been sold until they have arrived at their destination

Cut-off Errors - A cut-off error occurs with respect to ending inventory if items owned at period end are incorrectly excluded from the physical inventory count or if items already sold are incorrectly included in the period end inventory count

SystemsPerpetual system tracks units sold continuously

More accurate more timely potentially more costlyPeriodic system infer quantities sold by using purchasesproduction beginning and ending inventories

Units sold = Beg Units + Production ndashEnd Units Harder to detect inventory ldquoshrinkagerdquo (eg theft spoilage)

Cost flow assumptions Specific identification Costs of the specific item sold are included in cost of goods sold Costs of specific items on hand are included in inventory (Perpetual inventory systems)

Weighted average cost Inventory is priced on the basis of average cost of goods available for sale during the period Thus the same cost per item is assigned to cost of goods sold and to ending inventory (This method is used for periodic inventory systems)

Moving average cost Cost of goods sold is determined by calculating the average cost of goods available at the time a sale is made (This method is used for perpetual inventory systems)

FIFO assumption about the physical flow of inventory used to determine cost of goods sold and the ending inventory account balance The actual physical flow of inventory need not correspond to these assumptions FIFO shows SFP at relatively current values but income statement cost of goods sold at stale values

Inventory estimation methods

The Gross Profit Method

The gross profit method of inventory estimation relies on the knowledge of opening inventory net purchases net sales at retail prices and the historical gross profit margin

The Retail Inventory Method

The retail inventory method is a method of estimating the dollar amount of ending inventory using the current relationship between cost and selling price This is commonly used by retail stores for the preparation of interim financial statements

IFRS vs ASPEIFRS covers biological assets in a separate sectionIFRS requires the capitalization of interest on inventory that must be manufactured in large quantities ASPE GAAP gives companies the option

Types of Questions

Ch 9- 10 - Accounting for capital assetsPPampE

1 PPEEB = PPEBB + Acquisitions ndash Disposals 2 Straight-line depreciation = (Purchase price ndash salvage value) Useful

life 3 Declining balance methods = (Purchase cost- sum of all prior yearsrsquo

depreciation) X rate4 Units of Production = (Purchase price ndash salvage value) Useful life in

units annual depreciation = rate X of units5 Accumulated DepEB = Accumulated DepBB + Depreciation ndash

AccDepDisposal

Capitalize vs expense Capitalizing costs means to show them as an asset on the SFP (assets have future economic benefits)

We expense (ie not capitalize) when (a) benefits are immediate (b) or future benefits are too uncertain or immaterial (eg RampD)

Accounting for tangible assetsWhat is the acquisition cost

o Include all costs required to bring the asset into usable condition and location

o Purchased assets purchase price plus cost to prepare the asset for use (installation transportation testing)

o Self-constructed assets direct cost of construction (direct material direct labour pro-rata allocation of overhead costs) financing costs (interest on funds specifically borrowed to finance construction can be capitalized)

o Basket purchase ndash the best way to allocate the purchase price of the assets to the individual assets is based on the relative fair market values of the assets acquired

o Deferred payment contracts ndash recorded at the present value of the consideration exchanged between the contracting parties at the date of acquisition

o Non-monetary transactions recorded at the fair value of the assets received or the fair value of the asset given up whichever is more easily determined ASPE GAAP

o Check page 636 and 637 on how IFRS is differento

Measurement after acquisition Cost model vs Revaluation Model

How to account for costs subsequent to acquisition- Additions capitalize the costs to the existing capital asset account and

revise the service life and residual value as needed

- Betterments and replacements capitalize the costs to the existing capital asset account Distinguish the expenditures from normal repair costs o The appropriate accounting treatment depends on whether or not

we know the carrying value of old assets o If Costs are known then remove the old cost and accumulated

depreciation record a loss on disposal and then capitalize the new costs

o If costs are not known then add the new costs into the cost pool and revise the service life and residual value as needed

- Rearrangement and reinstallation capitalize the costs to the existing capital asset account

The appropriate accounting treatment depends on whether or not we know the carrying value of old assets

If Costs are known then remove the old cost and accumulated depreciation record a loss on disposal and then capitalize the new costs

If costs and Accum Amortization not known then expense the full amount

o Repairs ndash always expensed as incurred

Accounting for Intangible Assets

Specific assets - Patents Trademarks Customer lists FranchisesResearch and development Goodwill etc See notes below under Chapter 11 for calculation of Goodwill

o Goodwill is the expected value of future above-normal financial performance

What is the acquisition costPurchased assets - Include all costs required to bring the asset into usable condition and location Goodwill is only recorded if purchased

Six Criteria for capitalization of internally generated intangible assets

Costs to be included ndash Materials and servicesndash Direct labour and other payroll costsndash Interest and borrowing costs ndash if specifically related

Costs excluded ndash Selling administration and general overhead costs

Measurement after acquisition Cost model vs Revaluation Model ndash general understanding of the differences in the two models only

Amortization of Capital assets - What is the expected useful life

o The time period over which the asset will be used

- What is the Residual value o To determine residual value of an asset it requires managerial

judgment o Residual value is the estimated amount a company would receive

today on disposal of an asset net of related disposal costs

- What amortization should we use to allocate expense over the useful life

o What does GAAP allow Straight-line method

bull Annual Depreciation Expense = depreciable basisservice life (in years) = (Acquisition Cost -SV) Useful Years

bull Common for tangible assetsbull Uniform amortization charges over time

Activity methodbull Input methods ndash eg Depreciation cost per machine-

hour = depreciable basisservice life (in machine-hours)

bull Depr Expense = Actual hours used hourly ratebull Common for manufacturing firms bull Output methods- eg units producedbull Depr Expense = Actual units produced rate per unit bull Common for natural resources companybull Unequal amortization charges over time

Decreasing charge (declining balance CCA double declining balance)

bull Higher amortization expense is recognized in the earlier years of an assetrsquos useful life

bull Constant amortization rated applied to reducing book value of assets

Increasing chargebull Lower amortization expense in earlier years and

higher amortization in later years Donrsquot need to calculate this

Land is the never amortized

What accounts does depreciation affect Tangible assets - Accumulated depreciation account Intangible assets ndash The asset account directly Retained earnings account Depreciation expense

Which financial statements are affected SFP and income statement

Does depreciation affect cash NEVER

Amortization for partial periods amortization charges for the periods in which when assets are purchased and disposed Follow the company policy if given

Impairment in Value of Capital Assets IFRS requires impairment test for intangible and tangible assets be

conducted at least once a year Use the rational entity impairment model

Impairment = Carrying value minus (the greater of FV in use and FV less costs to sell)

Impairment loss can be reversed if value recovers in future years

ASPE GAAP requires impairment test for tangible and intangible assets only when circumstances change such that there might be a permanent impairment in the assetsrsquo carrying value Once impairment loss is recorded it cannot be recovered later

Use the cost recovery impairment model - Tangible Assets

Two steps Step 1 compare the assets carrying value to sum of the

Undiscounted cash flowsbull If sum of the undiscounted cash flows gt carrying

value no impairment loss is recorded and impairment test stops

bull If sum of the undiscounted cash flows lt carrying value go to step 2

Step 2 Determine the assetsrsquo fair market value bull If there is an active market for the assets then use

the quoted market price as the fair market value bull If there is no active market for the assets then

calculate the intrinsic value (theoretical value) of the assets by discounting all future cash flows to be resulted from the assets to current period

Impairment loss = carrying value ndash fair market value

Goodwill is not amortized but written down if impaired in value Two steps

bull Step 1 compare fair value of each reporting unit to the total net book value (including goodwill)

o If fair value gt book value no impairment loss is recorded and impairment test stops

o Otherwise go to the second stepbull Step 2

o Determine the fair value of reporting unito Subtract the fair value of all net identifiable

assets of that unit and allocates the remainder to goodwill implied goodwill

o Carrying value of goodwill ndash implied goodwill impairment loss to be recognized

Disposition of Capital assets- Remove the cost from the capital asset account and the accumulated

amortization related to disposed capital assets - Once a long-term assets is determined to be disposed

o Reclassify to assets held for sale

o Determine the net realizable value the lower of carrying value and fair value less cost to sell

o Not amortized any more o When sold record gainloss from disposal

Review Basket purchases and Non-monetary transaction

Ch 11 - Investments

Passive investmentsWhen the investor company does not have significant influence over the investee company

Choices are costamortized cost FVTPL or FV-OCIo ASPE allow only costamortized cost and FVTPL o ASPE GAAP ndash Companies must use FVTPL when active market for

shares existso ASPE GAAP allows companies to choose to use FVTPL if they so

designate at time of initial recognition

Investments other than bonds being held to receive their contractual cash flows will be adjusted to market value at year end

o SFP effects are the same ie FV reported

What is different o Income statement effects o For investments FVTPL gains or losses recognized in Income in

the current periodo For investments FV-OCI gains or losses are recorded in

ldquocomprehensive incomerdquo and accumulated in AOCI until securities are sold

Investments FVTPL (debt and equity) Purchased for short-term profit potential Year-end adjustment to the market value Changes in market value (holding lossgain) reported in the income

statement of the current period

Investment Amortized Cost (debt) Purchased with ability and intention to hold to maturity No adjustment to market value Carried at amortized cost on the SFP

Investments FV-OCI (debt and equity) Securities not classified as either of above Changes in market value (holding lossgain) reported in comprehensive

income On the SFP donrsquot forget to report accumulated comprehensive gainloss

under Shareholdersrsquo equity

Investment revenue is recognized at the point when the investee company declares and pays dividends

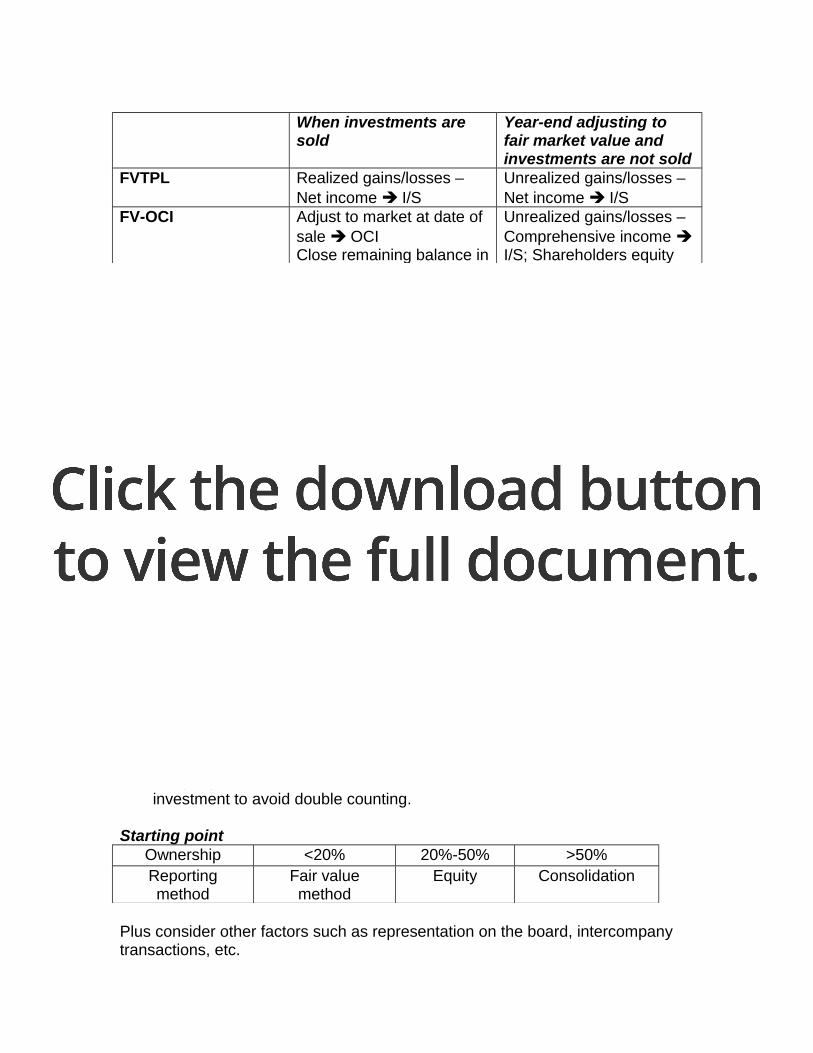

When investments are sold

Year-end adjusting to fair market value and investments are not sold

FVTPL Realized gainslosses ndash Net income IS

Unrealized gainslosses ndash Net income IS

FV-OCI Adjust to market at date of sale OCIClose remaining balance in AOCI for the investments sold to RE

Unrealized gainslosses ndash Comprehensive income IS Shareholders equity

Bonds ndash Intent to hold until maturity

NA No year- end adjustment to FV Record at amortized cost

Bonds - Terminology

1 1048697 Principal (Par Value) face value of the bond the amount due at maturity

2 1048697 Coupon Rate the rate used to determine the periodic cash payments (coupon payment) if any

3 1048697 Coupon Payment Cash Payment = face value x Coupon Rate

4 1048697 Market Interest Rate the rate used to determine the current market value of the bond

Bonds - ParDiscountPremium

Bonds Sells Market Rate at issuance

Market Value at issuance

Coupon Payment

At Par = Coupon rate = Par value =Interest expenseAt a Discount gt Coupon rate lt Par value ltInterest expenseAt a Premium lt Coupon rate gt Par value gtInterest expense

Active investmentsUsed when significant influence exists- Under the equity method investment revenue is recognized as soon as the

investee company reports a net income or net loss - When the investee company declares and pays dividends the investor

company does not record as investment revenue but as a decrease of investment to avoid double counting

Starting pointOwnership lt20 20-50 gt50Reporting method

Fair value method

Equity Consolidation

Plus consider other factors such as representation on the board intercompany transactions etc

Equity method - investeersquos announcement of earnings increases investorrsquos Investment

account - Investeersquos announcement of dividends decreases investorrsquos

Investment account - Calculation of equity Income

ASPE vs IFRS - IFRS must use Equity method for investments with significant influence APSE Can use Equity method or Cost( if Shares are not actively traded) If shares actively traded then the choice is Equity or FVTPL

Purchase premiums- Purchase premiums arise for two reasons

o Fair market value differentials the FV of assetsliabilities of the investee are different from BV of those assetsliabilities

Fair market value differentials are amortized and the amortization expenses will be included in net income

bull Inventory fair market value differentials is usually amortized in the first period after acquisition

bull Fixed assets fair market value differentials are usually amortized over the expected remaining service life of the assets

o Goodwill is the expected value of future above-normal financial performance

- Calculation of Goodwill and FV differentials to be amortized

Goodwill CalculationPurchase priceLess percentage share of BV acquiredEquals Purchase PremiumMinus FV differences where FVgtBVAdd FV differences where FVgtBVRemainder equals Goodwill

- Revenue recognized to date G

- Revenue recognized to date G

- Inventory estimation methods

- The Gross Profit Method

-

Ch 1 and 2 Objectives of Financial Accounting

To communicate financial information to parties outside the business organization

1 Equity Investors 4 Suppliers2 Creditors 5 Customers etc3 Employees

Financial StatementsThe four basic financial statements Statement of Financial position Income Statement statement of comprehensive income Statement of Cash Flows Statement of Retained earningsshareholdersrsquo equity Most companies prepare financial statements at the end of each year (called annual reports) and at the end of each quarter (called quarterly reports)

General justification for ASPE GAAP vs IFRS

Cash Basis vs Accrual Basis Recognition Criteria

Accrual basis Cash basisRevenue When earned When cash is receivedExpense When incurred When cash is paid

Review the conceptual framework

What type of questions would you ask

Appendix - The accounting cycle

The Recording Process Journal entries Unadjusted trial balance Adjusting entries Adjusted Trial Balance Financial statement preparation Closing entries Post closing trial balance Reversing entries are optional ndash not required in this course

The Journal EntriesTransactions recorded using double entry bookkeeping

Debits Dr Credits Cr

Journal Entries and T-accounts

Increases in assets are debited and recorded on the left side of the T-account

Increases in liabilities are credited and recorded on the right side of the T-account

Increases in revenues are credited and recorded on the right side of the T-account

Increases in expenses are debited and recorded on the left side of the T-account

Remember that the balances of the permanent accounts carry over to the next year

Remember that the income statements accounts (revenues and expenses) will be closed through closing entries by the end of each reporting period

T-Accounts You can use balances from T-accounts to prepare financial statements at the end of a fiscal period

Basic Accounts

Adjusting EntriesAdjusting entries record activities that have taken place but which have not yet been recorded Four scenarios1 Cash first expenses later eg Prepaid expense office supplies purchased for later use PPampE purchased2 Expenses first cash later eg Wages accrued but not paid purchases of inventory on credit3 Cash first revenues later eg Unearned revenues 4 Revenues first cash later eg Interest revenues accrued credit sales

Involve at least one temporary account (revenue expense) and at least one permanent account (asset liabilities) They NEVER involve cash

Trial BalancesPurpose To ensure both sides on an entry recorded at the same amount ndash do not guarantee that your entries are correct but do reduce errors

Closing EntriesBridge the Income Statement and Statement of Financial Position ( through) Retained EarningsClose Revenue into RE by

Dr Revenues Cr Retained earnings

Close COGSExpenses into RE byDr Retained earnings

Cr COGSExpensesWhat about dividends Ensure that any dividends declared are closed to retained earnings You can use the income summary if you wish

Sub-ledgers and special journals

What questions might you ask

Ch 3 - The Income Statement and Comprehensive Income

The income statement measures firm performance regardless of when cash is exchanged Key principle

Single step vs Multi stepSingle step

Revenues + gainsLess Expenses and losses=Net income before taxesless Taxes ndash as these mush be shown separately=Net Income

Multi stepRevenues( from operations only)Less COGS=Gross Profitless Operating expenses= operating incomeless Non operating expenses=Net income before taxesless Taxes=Net Income

Function vs Nature

Function- Sort by functional area of the business eg sales admin engineering RampD etc You need to have the costs split by function in order to do thisNature ndash Sort expenses by type eg Utilities office professional fees etcLook at the accounts you are given and use this to determine the better approach Smaller businesses generally sort by nature bigger organizations with more separation by departments may use function

Income statement Equations

Revenue ndash Cost of Goods Sold = gross profitNet Income + - Other comprehensive income = comprehensive income

Components(IFRS and ASPE GAAP)

o Heading ndash for the [year] ended [date] or other period coveredo Revenues -Sales or service revenueo Gains -eg selling an equipment for cash greater than its net book valueo Expenses -Cost of goods sold operating expenses etco Losses eg selling an equipment for cash less than its net book valueo Other revenues and expenses

o Interest revenue dividend income interest expense

Income from Continuing Operationso Discontinued Operations

o Income or Loss from Discontinued Operations net of taxo Gain or Loss on Disposal of Discontinued Operations net of tax

Net income

IFRS onlyo +- Other comprehensive income

Comprehensive income

Differences between IFRS and ASPE

Accounting for discontinued operations and intra-period tax allocation

Earnings management

Typical Questions

Ch 4 - The Statement of Financial Position Statement of Retained Earnings Changes in Shareholdersrsquo Equity and Disclosure

STATEMENT OF FINANCIAL POSITION

Equation Assets = Liabilities + Shareholdersrsquo equity

Components of the Statement - Heading ndash as at [date]- Assets Economic benefits owned by the business as a result of

past transactions - Liabilities Debt and other obligations of the business that result

from past transactions - Shareholdersrsquo equity Residual claim of and financing provided by

the owners of the business- Current vs Non Current- Major categories

o Review major categories for presentation- Order of accounts

o Assets- liquidityo Liabilities ndash time to maturityo Sh Equity - permanence

STATEMENT OF RETAINED EARNINGSThis is reported as a solo statement under ASPE GAAP onlyOpening Retained Earnings + Net Income - Dividends = Closing Retained Earnings

STATEMENT OF CHANGES IN SHAREHOLDERSrsquo EQUITYIFRS OnlyA continuity schedule of opening balances +- changes = closing balance for each component of shareholders equity including retained earnings

Financial statements - Note DisclosurePurpose to provide supplementary information about the financial condition of the company

- Describe accounting policies followed by the company - Provide additional detail about an item on the financial statements- Provide additional information about an item not on the financial

statements- Subsequent events consider the difference in treatment of the two

types of subsequent event

Typical Questions

Ch 5 ndash CASH FLOW STATEMENT ndash indirect method only

Cash and Cash equivalentsbull Cash on hand Bank balancesbull Bank overdraftsbull Short term risk free investments with maturity dates within 3 months

Reports the changes to other accounts that affect a change in cash and cash equivalents on the SFP The change in the cash account is usually not equal to net income

Revenues reported do not always equal cash collected (credit sales)Expenses reported do not always equal cash paid (prepaid expenses)

In relation to the SFP The sum of cash flows from operations cash flows from investing and cash flows from financing must equal to the change in cash and cash equivalents on the SFP

Statement of Cash Flows reports operating cash flow as well as other cash flow information

Provides important information to investors and creditors In particular information about differences in the timing of revenue and

expense recognition under GAAP and the associated cash inflows and outflows

Preparing a cash flow statement Heading - for the [year] ended [date] or other period covered

Cash flow provided by (used in) operating activities (Indirect method)Net IncomeAdjust for Non-Cash Changes in non-cash WC accounts

- Subtract increase in assets- Add decreases in asset- Add increase in liabilities- subtract decreases in Liabilities

Adjust for non cash items included in net incomeAdd Depreciation amp AmortizationAdd Loss on Sale of AssetsSubtract Gain on Sales of Assets

Cash flows provided by (used in) investing activitiesCash paid for long-term assetsCash proceeds from the sale of long-term assets

Cash flows provided by (used in) financing activitiesCash dividends paidCash received on issuing debt ndash ie borrowingCash paid for retirement of debt

Cash received from issuance of common shares Ch 6 - Revenue and Expense RecognitionWhy do we care about revenue recognitionRevenue has a BIG impact on bottom-line profitability managers may be tempted to manage revenue

Criteria for revenue recognition ndash existing standardA firm recognizes revenue when it has

bull Performance achievedbull Measurability of the revenues and associated remaining costsbull Collectability is reasonably assured

Revenue is most often recognized at the time of sale as long as- Reasonable estimate of uncollectible amount - Reasonable estimate of sales returns - Reasonable estimation of all other material expenses representing

uncertain future outflows (eg warranty costs) - Most common in retail wholesale amp manufacturing - Even when right of return exists as long as the company has

booked reasonable allowance for sales return we can still recognize revenues at the point of sale

If there is uncertainty in the three criteria then wait until the uncertainty is resolved

Criteria for revenue recognition ndash proposed standardIFRS

1 Identify the contract(s) with the customer ndash May be explicit or implicit

2 Identify the separate performance obligations ndash may be one or many

3 Determine the transaction price ndash using either weighted probabilities method or most likely amount You must determine an amount for revenue This is very different from the existing approach

4 Allocate the transaction price to the performance obligations

5 Recognize revenue when a performance obligation is satisfied

Review the two cases covered in the lectures

MethodsPercentage of completion method - Recognize revenue and profit as contract progresses Extent of completion at any one point in time is determined by the costs incurred to date divided by the total estimated costs of the contract If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Completed contract method - Recognize revenue and profit when the contract is complete If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Percentage of completion methodReview profitable contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Given

Gross profit I - A

AND Loss contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Plug this

Total estimated Loss Calc this

(Profit) Loss previously recognized Prior yrs

Gross profitTypical Questions

Ch 7 ndash Financial Instruments Cash Receivables and Payables

CashCash and Cash Equivalents ndash Identifying amounts to be included in cash equivalents ndash See chapter 5 material

Accounts Receivable

Relevant Formulae

1 Ending AR = Beg Bal AR + Credit Sales ndash Cash Received ndash Write-off + 0 Recovery of previous write-off2 Ending Allowance for doubtful accounts (ADA) = Beg Bal AFDA + Bad

Debt Expense ndash Write-off + Recovery of previous write-off

Two approaches to determining Allowance for Bad Debts

1 Percentage of (Credit) Sales (Income statement approach)2 minus Focuses on calculating the Bad Debt Expense recorded for the year

Aging Method (Balance sheet approach)3 minus Focuses on calculating the Ending Balance of Allowance for Bad

Debts 4 minus Bad Debt Expense is a ldquoPlugrdquo

Accounts Receivable Relevant entries 0 Credit sales Dr Accounts receivable

Cr Revenue 2 Record bad debt expense 0 Dr Bad debt expense 0 Cr AFDA 3 When bad debt happens (when we are sure a specific customer

defaults) Dr AFDA 4 Cr Accounts receivable5 Recovery of bad debt 6 Dr Accounts receivable7 Cr AFDA 0 Dr Cash1 Cr Accounts receivable

Notes receivablePayable- Notes written promises- May be at a market rate of interest ndash no discounting needed- May be at a low rate on interest ndash discount the face value of the

note and the interest payments at the market rate- May be at no interest ndash discount the face value at the market rate

of interest

Other items

Sales discounts- Account for sales discounts by recording ldquoallowance for sales

discountsrdquo o A contra account for sales revenue on Income statement

Customer return merchandise- Debit to ldquoSales returns and allowancesrdquo

o A contra account for sales revenue on Income statement

Year-end adjusting entry to account for an estimated amount of sales return and merchandise return

- Credit to Allowance for sales return and allowance - A balance sheet contra account attached to accounts receivables

Transfers of ARIdentify if the transaction is to be accounted for as a sale or a borrowing transaction

Sale transactionsJournal entries to remove the AR any associated AFDA record the receipt of cash the residual obligation if any and a loss on disposal

Borrowing transactionsJournal entries to record the new debt and interest costs fees The AR and associated AFDA remain on the books

Types of Questions

Ch 8 Inventory12 INVEB = INVBB + Purchase ndash COGS

Inventory is recorded on the SFP at the lower of the cost or the net realizable value of the inventory

Key equation Beginning Inv+ Purchases - COGS = Ending Inv

IssuesConsignment inventory - Consignment inventory on the firm premises owned by others should be excluded Consignment inventory of the firm held elsewhere should be included in the inventory of the firm

Goods in transit at period end - Items shipped FOB shipping point are considered to have been sold when shipped Items shipped FOB destination are not considered to have been sold until they have arrived at their destination

Cut-off Errors - A cut-off error occurs with respect to ending inventory if items owned at period end are incorrectly excluded from the physical inventory count or if items already sold are incorrectly included in the period end inventory count

SystemsPerpetual system tracks units sold continuously

More accurate more timely potentially more costlyPeriodic system infer quantities sold by using purchasesproduction beginning and ending inventories

Units sold = Beg Units + Production ndashEnd Units Harder to detect inventory ldquoshrinkagerdquo (eg theft spoilage)

Cost flow assumptions Specific identification Costs of the specific item sold are included in cost of goods sold Costs of specific items on hand are included in inventory (Perpetual inventory systems)

Weighted average cost Inventory is priced on the basis of average cost of goods available for sale during the period Thus the same cost per item is assigned to cost of goods sold and to ending inventory (This method is used for periodic inventory systems)

Moving average cost Cost of goods sold is determined by calculating the average cost of goods available at the time a sale is made (This method is used for perpetual inventory systems)

FIFO assumption about the physical flow of inventory used to determine cost of goods sold and the ending inventory account balance The actual physical flow of inventory need not correspond to these assumptions FIFO shows SFP at relatively current values but income statement cost of goods sold at stale values

Inventory estimation methods

The Gross Profit Method

The gross profit method of inventory estimation relies on the knowledge of opening inventory net purchases net sales at retail prices and the historical gross profit margin

The Retail Inventory Method

The retail inventory method is a method of estimating the dollar amount of ending inventory using the current relationship between cost and selling price This is commonly used by retail stores for the preparation of interim financial statements

IFRS vs ASPEIFRS covers biological assets in a separate sectionIFRS requires the capitalization of interest on inventory that must be manufactured in large quantities ASPE GAAP gives companies the option

Types of Questions

Ch 9- 10 - Accounting for capital assetsPPampE

1 PPEEB = PPEBB + Acquisitions ndash Disposals 2 Straight-line depreciation = (Purchase price ndash salvage value) Useful

life 3 Declining balance methods = (Purchase cost- sum of all prior yearsrsquo

depreciation) X rate4 Units of Production = (Purchase price ndash salvage value) Useful life in

units annual depreciation = rate X of units5 Accumulated DepEB = Accumulated DepBB + Depreciation ndash

AccDepDisposal

Capitalize vs expense Capitalizing costs means to show them as an asset on the SFP (assets have future economic benefits)

We expense (ie not capitalize) when (a) benefits are immediate (b) or future benefits are too uncertain or immaterial (eg RampD)

Accounting for tangible assetsWhat is the acquisition cost

o Include all costs required to bring the asset into usable condition and location

o Purchased assets purchase price plus cost to prepare the asset for use (installation transportation testing)

o Self-constructed assets direct cost of construction (direct material direct labour pro-rata allocation of overhead costs) financing costs (interest on funds specifically borrowed to finance construction can be capitalized)

o Basket purchase ndash the best way to allocate the purchase price of the assets to the individual assets is based on the relative fair market values of the assets acquired

o Deferred payment contracts ndash recorded at the present value of the consideration exchanged between the contracting parties at the date of acquisition

o Non-monetary transactions recorded at the fair value of the assets received or the fair value of the asset given up whichever is more easily determined ASPE GAAP

o Check page 636 and 637 on how IFRS is differento

Measurement after acquisition Cost model vs Revaluation Model

How to account for costs subsequent to acquisition- Additions capitalize the costs to the existing capital asset account and

revise the service life and residual value as needed

- Betterments and replacements capitalize the costs to the existing capital asset account Distinguish the expenditures from normal repair costs o The appropriate accounting treatment depends on whether or not

we know the carrying value of old assets o If Costs are known then remove the old cost and accumulated

depreciation record a loss on disposal and then capitalize the new costs

o If costs are not known then add the new costs into the cost pool and revise the service life and residual value as needed

- Rearrangement and reinstallation capitalize the costs to the existing capital asset account

The appropriate accounting treatment depends on whether or not we know the carrying value of old assets

If Costs are known then remove the old cost and accumulated depreciation record a loss on disposal and then capitalize the new costs

If costs and Accum Amortization not known then expense the full amount

o Repairs ndash always expensed as incurred

Accounting for Intangible Assets

Specific assets - Patents Trademarks Customer lists FranchisesResearch and development Goodwill etc See notes below under Chapter 11 for calculation of Goodwill

o Goodwill is the expected value of future above-normal financial performance

What is the acquisition costPurchased assets - Include all costs required to bring the asset into usable condition and location Goodwill is only recorded if purchased

Six Criteria for capitalization of internally generated intangible assets

Costs to be included ndash Materials and servicesndash Direct labour and other payroll costsndash Interest and borrowing costs ndash if specifically related

Costs excluded ndash Selling administration and general overhead costs

Measurement after acquisition Cost model vs Revaluation Model ndash general understanding of the differences in the two models only

Amortization of Capital assets - What is the expected useful life

o The time period over which the asset will be used

- What is the Residual value o To determine residual value of an asset it requires managerial

judgment o Residual value is the estimated amount a company would receive

today on disposal of an asset net of related disposal costs

- What amortization should we use to allocate expense over the useful life

o What does GAAP allow Straight-line method

bull Annual Depreciation Expense = depreciable basisservice life (in years) = (Acquisition Cost -SV) Useful Years

bull Common for tangible assetsbull Uniform amortization charges over time

Activity methodbull Input methods ndash eg Depreciation cost per machine-

hour = depreciable basisservice life (in machine-hours)

bull Depr Expense = Actual hours used hourly ratebull Common for manufacturing firms bull Output methods- eg units producedbull Depr Expense = Actual units produced rate per unit bull Common for natural resources companybull Unequal amortization charges over time

Decreasing charge (declining balance CCA double declining balance)

bull Higher amortization expense is recognized in the earlier years of an assetrsquos useful life

bull Constant amortization rated applied to reducing book value of assets

Increasing chargebull Lower amortization expense in earlier years and

higher amortization in later years Donrsquot need to calculate this

Land is the never amortized

What accounts does depreciation affect Tangible assets - Accumulated depreciation account Intangible assets ndash The asset account directly Retained earnings account Depreciation expense

Which financial statements are affected SFP and income statement

Does depreciation affect cash NEVER

Amortization for partial periods amortization charges for the periods in which when assets are purchased and disposed Follow the company policy if given

Impairment in Value of Capital Assets IFRS requires impairment test for intangible and tangible assets be

conducted at least once a year Use the rational entity impairment model

Impairment = Carrying value minus (the greater of FV in use and FV less costs to sell)

Impairment loss can be reversed if value recovers in future years

ASPE GAAP requires impairment test for tangible and intangible assets only when circumstances change such that there might be a permanent impairment in the assetsrsquo carrying value Once impairment loss is recorded it cannot be recovered later

Use the cost recovery impairment model - Tangible Assets

Two steps Step 1 compare the assets carrying value to sum of the

Undiscounted cash flowsbull If sum of the undiscounted cash flows gt carrying

value no impairment loss is recorded and impairment test stops

bull If sum of the undiscounted cash flows lt carrying value go to step 2

Step 2 Determine the assetsrsquo fair market value bull If there is an active market for the assets then use

the quoted market price as the fair market value bull If there is no active market for the assets then

calculate the intrinsic value (theoretical value) of the assets by discounting all future cash flows to be resulted from the assets to current period

Impairment loss = carrying value ndash fair market value

Goodwill is not amortized but written down if impaired in value Two steps

bull Step 1 compare fair value of each reporting unit to the total net book value (including goodwill)

o If fair value gt book value no impairment loss is recorded and impairment test stops

o Otherwise go to the second stepbull Step 2

o Determine the fair value of reporting unito Subtract the fair value of all net identifiable

assets of that unit and allocates the remainder to goodwill implied goodwill

o Carrying value of goodwill ndash implied goodwill impairment loss to be recognized

Disposition of Capital assets- Remove the cost from the capital asset account and the accumulated

amortization related to disposed capital assets - Once a long-term assets is determined to be disposed

o Reclassify to assets held for sale

o Determine the net realizable value the lower of carrying value and fair value less cost to sell

o Not amortized any more o When sold record gainloss from disposal

Review Basket purchases and Non-monetary transaction

Ch 11 - Investments

Passive investmentsWhen the investor company does not have significant influence over the investee company

Choices are costamortized cost FVTPL or FV-OCIo ASPE allow only costamortized cost and FVTPL o ASPE GAAP ndash Companies must use FVTPL when active market for

shares existso ASPE GAAP allows companies to choose to use FVTPL if they so

designate at time of initial recognition

Investments other than bonds being held to receive their contractual cash flows will be adjusted to market value at year end

o SFP effects are the same ie FV reported

What is different o Income statement effects o For investments FVTPL gains or losses recognized in Income in

the current periodo For investments FV-OCI gains or losses are recorded in

ldquocomprehensive incomerdquo and accumulated in AOCI until securities are sold

Investments FVTPL (debt and equity) Purchased for short-term profit potential Year-end adjustment to the market value Changes in market value (holding lossgain) reported in the income

statement of the current period

Investment Amortized Cost (debt) Purchased with ability and intention to hold to maturity No adjustment to market value Carried at amortized cost on the SFP

Investments FV-OCI (debt and equity) Securities not classified as either of above Changes in market value (holding lossgain) reported in comprehensive

income On the SFP donrsquot forget to report accumulated comprehensive gainloss

under Shareholdersrsquo equity

Investment revenue is recognized at the point when the investee company declares and pays dividends

When investments are sold

Year-end adjusting to fair market value and investments are not sold

FVTPL Realized gainslosses ndash Net income IS

Unrealized gainslosses ndash Net income IS

FV-OCI Adjust to market at date of sale OCIClose remaining balance in AOCI for the investments sold to RE

Unrealized gainslosses ndash Comprehensive income IS Shareholders equity

Bonds ndash Intent to hold until maturity

NA No year- end adjustment to FV Record at amortized cost

Bonds - Terminology

1 1048697 Principal (Par Value) face value of the bond the amount due at maturity

2 1048697 Coupon Rate the rate used to determine the periodic cash payments (coupon payment) if any

3 1048697 Coupon Payment Cash Payment = face value x Coupon Rate

4 1048697 Market Interest Rate the rate used to determine the current market value of the bond

Bonds - ParDiscountPremium

Bonds Sells Market Rate at issuance

Market Value at issuance

Coupon Payment

At Par = Coupon rate = Par value =Interest expenseAt a Discount gt Coupon rate lt Par value ltInterest expenseAt a Premium lt Coupon rate gt Par value gtInterest expense

Active investmentsUsed when significant influence exists- Under the equity method investment revenue is recognized as soon as the

investee company reports a net income or net loss - When the investee company declares and pays dividends the investor

company does not record as investment revenue but as a decrease of investment to avoid double counting

Starting pointOwnership lt20 20-50 gt50Reporting method

Fair value method

Equity Consolidation

Plus consider other factors such as representation on the board intercompany transactions etc

Equity method - investeersquos announcement of earnings increases investorrsquos Investment

account - Investeersquos announcement of dividends decreases investorrsquos

Investment account - Calculation of equity Income

ASPE vs IFRS - IFRS must use Equity method for investments with significant influence APSE Can use Equity method or Cost( if Shares are not actively traded) If shares actively traded then the choice is Equity or FVTPL

Purchase premiums- Purchase premiums arise for two reasons

o Fair market value differentials the FV of assetsliabilities of the investee are different from BV of those assetsliabilities

Fair market value differentials are amortized and the amortization expenses will be included in net income

bull Inventory fair market value differentials is usually amortized in the first period after acquisition

bull Fixed assets fair market value differentials are usually amortized over the expected remaining service life of the assets

o Goodwill is the expected value of future above-normal financial performance

- Calculation of Goodwill and FV differentials to be amortized

Goodwill CalculationPurchase priceLess percentage share of BV acquiredEquals Purchase PremiumMinus FV differences where FVgtBVAdd FV differences where FVgtBVRemainder equals Goodwill

- Revenue recognized to date G

- Revenue recognized to date G

- Inventory estimation methods

- The Gross Profit Method

-

Appendix - The accounting cycle

The Recording Process Journal entries Unadjusted trial balance Adjusting entries Adjusted Trial Balance Financial statement preparation Closing entries Post closing trial balance Reversing entries are optional ndash not required in this course

The Journal EntriesTransactions recorded using double entry bookkeeping

Debits Dr Credits Cr

Journal Entries and T-accounts

Increases in assets are debited and recorded on the left side of the T-account

Increases in liabilities are credited and recorded on the right side of the T-account

Increases in revenues are credited and recorded on the right side of the T-account

Increases in expenses are debited and recorded on the left side of the T-account

Remember that the balances of the permanent accounts carry over to the next year

Remember that the income statements accounts (revenues and expenses) will be closed through closing entries by the end of each reporting period

T-Accounts You can use balances from T-accounts to prepare financial statements at the end of a fiscal period

Basic Accounts

Adjusting EntriesAdjusting entries record activities that have taken place but which have not yet been recorded Four scenarios1 Cash first expenses later eg Prepaid expense office supplies purchased for later use PPampE purchased2 Expenses first cash later eg Wages accrued but not paid purchases of inventory on credit3 Cash first revenues later eg Unearned revenues 4 Revenues first cash later eg Interest revenues accrued credit sales

Involve at least one temporary account (revenue expense) and at least one permanent account (asset liabilities) They NEVER involve cash

Trial BalancesPurpose To ensure both sides on an entry recorded at the same amount ndash do not guarantee that your entries are correct but do reduce errors

Closing EntriesBridge the Income Statement and Statement of Financial Position ( through) Retained EarningsClose Revenue into RE by

Dr Revenues Cr Retained earnings

Close COGSExpenses into RE byDr Retained earnings

Cr COGSExpensesWhat about dividends Ensure that any dividends declared are closed to retained earnings You can use the income summary if you wish

Sub-ledgers and special journals

What questions might you ask

Ch 3 - The Income Statement and Comprehensive Income

The income statement measures firm performance regardless of when cash is exchanged Key principle

Single step vs Multi stepSingle step

Revenues + gainsLess Expenses and losses=Net income before taxesless Taxes ndash as these mush be shown separately=Net Income

Multi stepRevenues( from operations only)Less COGS=Gross Profitless Operating expenses= operating incomeless Non operating expenses=Net income before taxesless Taxes=Net Income

Function vs Nature

Function- Sort by functional area of the business eg sales admin engineering RampD etc You need to have the costs split by function in order to do thisNature ndash Sort expenses by type eg Utilities office professional fees etcLook at the accounts you are given and use this to determine the better approach Smaller businesses generally sort by nature bigger organizations with more separation by departments may use function

Income statement Equations

Revenue ndash Cost of Goods Sold = gross profitNet Income + - Other comprehensive income = comprehensive income

Components(IFRS and ASPE GAAP)

o Heading ndash for the [year] ended [date] or other period coveredo Revenues -Sales or service revenueo Gains -eg selling an equipment for cash greater than its net book valueo Expenses -Cost of goods sold operating expenses etco Losses eg selling an equipment for cash less than its net book valueo Other revenues and expenses

o Interest revenue dividend income interest expense

Income from Continuing Operationso Discontinued Operations

o Income or Loss from Discontinued Operations net of taxo Gain or Loss on Disposal of Discontinued Operations net of tax

Net income

IFRS onlyo +- Other comprehensive income

Comprehensive income

Differences between IFRS and ASPE

Accounting for discontinued operations and intra-period tax allocation

Earnings management

Typical Questions

Ch 4 - The Statement of Financial Position Statement of Retained Earnings Changes in Shareholdersrsquo Equity and Disclosure

STATEMENT OF FINANCIAL POSITION

Equation Assets = Liabilities + Shareholdersrsquo equity

Components of the Statement - Heading ndash as at [date]- Assets Economic benefits owned by the business as a result of

past transactions - Liabilities Debt and other obligations of the business that result

from past transactions - Shareholdersrsquo equity Residual claim of and financing provided by

the owners of the business- Current vs Non Current- Major categories

o Review major categories for presentation- Order of accounts

o Assets- liquidityo Liabilities ndash time to maturityo Sh Equity - permanence

STATEMENT OF RETAINED EARNINGSThis is reported as a solo statement under ASPE GAAP onlyOpening Retained Earnings + Net Income - Dividends = Closing Retained Earnings

STATEMENT OF CHANGES IN SHAREHOLDERSrsquo EQUITYIFRS OnlyA continuity schedule of opening balances +- changes = closing balance for each component of shareholders equity including retained earnings

Financial statements - Note DisclosurePurpose to provide supplementary information about the financial condition of the company

- Describe accounting policies followed by the company - Provide additional detail about an item on the financial statements- Provide additional information about an item not on the financial

statements- Subsequent events consider the difference in treatment of the two

types of subsequent event

Typical Questions

Ch 5 ndash CASH FLOW STATEMENT ndash indirect method only

Cash and Cash equivalentsbull Cash on hand Bank balancesbull Bank overdraftsbull Short term risk free investments with maturity dates within 3 months

Reports the changes to other accounts that affect a change in cash and cash equivalents on the SFP The change in the cash account is usually not equal to net income

Revenues reported do not always equal cash collected (credit sales)Expenses reported do not always equal cash paid (prepaid expenses)

In relation to the SFP The sum of cash flows from operations cash flows from investing and cash flows from financing must equal to the change in cash and cash equivalents on the SFP

Statement of Cash Flows reports operating cash flow as well as other cash flow information

Provides important information to investors and creditors In particular information about differences in the timing of revenue and

expense recognition under GAAP and the associated cash inflows and outflows

Preparing a cash flow statement Heading - for the [year] ended [date] or other period covered

Cash flow provided by (used in) operating activities (Indirect method)Net IncomeAdjust for Non-Cash Changes in non-cash WC accounts

- Subtract increase in assets- Add decreases in asset- Add increase in liabilities- subtract decreases in Liabilities

Adjust for non cash items included in net incomeAdd Depreciation amp AmortizationAdd Loss on Sale of AssetsSubtract Gain on Sales of Assets

Cash flows provided by (used in) investing activitiesCash paid for long-term assetsCash proceeds from the sale of long-term assets

Cash flows provided by (used in) financing activitiesCash dividends paidCash received on issuing debt ndash ie borrowingCash paid for retirement of debt

Cash received from issuance of common shares Ch 6 - Revenue and Expense RecognitionWhy do we care about revenue recognitionRevenue has a BIG impact on bottom-line profitability managers may be tempted to manage revenue

Criteria for revenue recognition ndash existing standardA firm recognizes revenue when it has

bull Performance achievedbull Measurability of the revenues and associated remaining costsbull Collectability is reasonably assured

Revenue is most often recognized at the time of sale as long as- Reasonable estimate of uncollectible amount - Reasonable estimate of sales returns - Reasonable estimation of all other material expenses representing

uncertain future outflows (eg warranty costs) - Most common in retail wholesale amp manufacturing - Even when right of return exists as long as the company has

booked reasonable allowance for sales return we can still recognize revenues at the point of sale

If there is uncertainty in the three criteria then wait until the uncertainty is resolved

Criteria for revenue recognition ndash proposed standardIFRS

1 Identify the contract(s) with the customer ndash May be explicit or implicit

2 Identify the separate performance obligations ndash may be one or many

3 Determine the transaction price ndash using either weighted probabilities method or most likely amount You must determine an amount for revenue This is very different from the existing approach

4 Allocate the transaction price to the performance obligations

5 Recognize revenue when a performance obligation is satisfied

Review the two cases covered in the lectures

MethodsPercentage of completion method - Recognize revenue and profit as contract progresses Extent of completion at any one point in time is determined by the costs incurred to date divided by the total estimated costs of the contract If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Completed contract method - Recognize revenue and profit when the contract is complete If it becomes apparent that a loss is expected on a contract recognize the total amount of the expected loss immediately

Percentage of completion methodReview profitable contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Given

Gross profit I - A

AND Loss contracts

Calc Year 1 Year 2Costs incurred to date (B) given

Total estimated costs (D) given

Percentage complete (E) BD

Contract Value (F) Given

Revenue recognized to date G F X E

Less revenue already recognized H

Annual revenue ( I) G-H

Construction costs incurred (A) Plug this

Total estimated Loss Calc this

(Profit) Loss previously recognized Prior yrs

Gross profitTypical Questions

Ch 7 ndash Financial Instruments Cash Receivables and Payables

CashCash and Cash Equivalents ndash Identifying amounts to be included in cash equivalents ndash See chapter 5 material

Accounts Receivable

Relevant Formulae

1 Ending AR = Beg Bal AR + Credit Sales ndash Cash Received ndash Write-off + 0 Recovery of previous write-off2 Ending Allowance for doubtful accounts (ADA) = Beg Bal AFDA + Bad

Debt Expense ndash Write-off + Recovery of previous write-off

Two approaches to determining Allowance for Bad Debts

1 Percentage of (Credit) Sales (Income statement approach)2 minus Focuses on calculating the Bad Debt Expense recorded for the year

Aging Method (Balance sheet approach)3 minus Focuses on calculating the Ending Balance of Allowance for Bad

Debts 4 minus Bad Debt Expense is a ldquoPlugrdquo

Accounts Receivable Relevant entries 0 Credit sales Dr Accounts receivable

Cr Revenue 2 Record bad debt expense 0 Dr Bad debt expense 0 Cr AFDA 3 When bad debt happens (when we are sure a specific customer

defaults) Dr AFDA 4 Cr Accounts receivable5 Recovery of bad debt 6 Dr Accounts receivable7 Cr AFDA 0 Dr Cash1 Cr Accounts receivable

Notes receivablePayable- Notes written promises- May be at a market rate of interest ndash no discounting needed- May be at a low rate on interest ndash discount the face value of the

note and the interest payments at the market rate- May be at no interest ndash discount the face value at the market rate

of interest

Other items

Sales discounts- Account for sales discounts by recording ldquoallowance for sales

discountsrdquo o A contra account for sales revenue on Income statement

Customer return merchandise- Debit to ldquoSales returns and allowancesrdquo

o A contra account for sales revenue on Income statement

Year-end adjusting entry to account for an estimated amount of sales return and merchandise return

- Credit to Allowance for sales return and allowance - A balance sheet contra account attached to accounts receivables

Transfers of ARIdentify if the transaction is to be accounted for as a sale or a borrowing transaction

Sale transactionsJournal entries to remove the AR any associated AFDA record the receipt of cash the residual obligation if any and a loss on disposal

Borrowing transactionsJournal entries to record the new debt and interest costs fees The AR and associated AFDA remain on the books

Types of Questions

Ch 8 Inventory12 INVEB = INVBB + Purchase ndash COGS

Inventory is recorded on the SFP at the lower of the cost or the net realizable value of the inventory

Key equation Beginning Inv+ Purchases - COGS = Ending Inv

IssuesConsignment inventory - Consignment inventory on the firm premises owned by others should be excluded Consignment inventory of the firm held elsewhere should be included in the inventory of the firm

Goods in transit at period end - Items shipped FOB shipping point are considered to have been sold when shipped Items shipped FOB destination are not considered to have been sold until they have arrived at their destination

Cut-off Errors - A cut-off error occurs with respect to ending inventory if items owned at period end are incorrectly excluded from the physical inventory count or if items already sold are incorrectly included in the period end inventory count

SystemsPerpetual system tracks units sold continuously

More accurate more timely potentially more costlyPeriodic system infer quantities sold by using purchasesproduction beginning and ending inventories

Units sold = Beg Units + Production ndashEnd Units Harder to detect inventory ldquoshrinkagerdquo (eg theft spoilage)

Cost flow assumptions Specific identification Costs of the specific item sold are included in cost of goods sold Costs of specific items on hand are included in inventory (Perpetual inventory systems)

Weighted average cost Inventory is priced on the basis of average cost of goods available for sale during the period Thus the same cost per item is assigned to cost of goods sold and to ending inventory (This method is used for periodic inventory systems)

Moving average cost Cost of goods sold is determined by calculating the average cost of goods available at the time a sale is made (This method is used for perpetual inventory systems)

FIFO assumption about the physical flow of inventory used to determine cost of goods sold and the ending inventory account balance The actual physical flow of inventory need not correspond to these assumptions FIFO shows SFP at relatively current values but income statement cost of goods sold at stale values

Inventory estimation methods

The Gross Profit Method

The gross profit method of inventory estimation relies on the knowledge of opening inventory net purchases net sales at retail prices and the historical gross profit margin

The Retail Inventory Method

The retail inventory method is a method of estimating the dollar amount of ending inventory using the current relationship between cost and selling price This is commonly used by retail stores for the preparation of interim financial statements

IFRS vs ASPEIFRS covers biological assets in a separate sectionIFRS requires the capitalization of interest on inventory that must be manufactured in large quantities ASPE GAAP gives companies the option

Types of Questions

Ch 9- 10 - Accounting for capital assetsPPampE