Accounting Standards for Private Entete p ses a d ...adamsmil/files/ASPEPresentation9_24... ·...

102

Accounting Standards for Private Enterprises and Not-for-Profits September 24, 2013

Transcript of Accounting Standards for Private Entete p ses a d ...adamsmil/files/ASPEPresentation9_24... ·...

Accounting Standards for Private Enterprises and Not-for-Profitste p ses a d ot o o ts

September 24, 2013

Although the presentation and related gmaterials have been carefully prepared, neither the presentation authors, firm, nor any persons involved in the preparation and/or instruction of the materials accepts any legal responsibility for its contents or for any consequences arising from its use.

ASPE and ASFNPO Updates; Common challenges with Accounting Standards Financial instruments Prepaids R Revenue Inventory I i t Impairments

Not-for-Profit Corporations Act

Good news – no new significant changes to the standards yetchanges to the standards – yet

Bad news – big changes to ASFNPO may be on the waymay be on the way

2013 Annual Improvements Minor in nature Business combinations – contingent considerations Subsidiaries – change in ownershipg p Non-controlling interests – minor clarifications Financial instruments – minor clarifications Accounting Handbook Part II to be updated Accounting Handbook Part II to be updated

October 2013 Effective for year-ends commencing after Jan.1

20142014 Also affect any NPO’s using relevant sections

updated

2013 Major Handbook change Employee future benefits (defined benefit pensions

alert!)alert!) Deferral of gains/losses no longer allowed Balance sheet now shows true assets and liabilities at

year end May cause significant volatility in Net Income

Effective for years commencing after Jan.1 2014 A different standard is proposed for NPO’s

Active Exposure Drafts Consolidations V i bl l i i i Variable control entities - improvements to

presentation of assets and liabilities controlled by the enterprise

Joint ArrangementsJoint ventures – increased clarity of the nature of

interest in a JV Effective dates – no earlier than years beginning

Jan.1 2016

Active Exposure Draft Employee future benefits D f l f i /l l ll d Deferral of gains/losses no longer allowed Balance sheet now shows true assets and liabilities at

year end Gains/losses recognized directly as changes in net

assets – gain/losses are not included in the statement of

operations

Statement of Principles – NPO way forward(?)Principles open for public comment Fi t t l f f i l t tiFirst step only - we are far from implementationAffects both private and public sector NPO’s

Main features of Statement of Principles Recognition of contributions D f l h d d ld f hi i Deferral method removed – old concept of matching is

gone – Ex. recognize revenue used to purchase capital assets

Capital assets Capitalization exemption based on organization’s size

is removed (previously<$500K revenue)p y Impairment – recognize partial loss of service

potential even if still in use (applies to intangibles also) Other areas Other areas

Financial Instruments Prepaids Revenue Inventory

Impairments

Financial InstrumentsFinancial Instruments

Back to Basics (s3856)Back to Basics (s3856) Definitions Initial Measurement (Day 1) Subsequent Measurement (Day 2)

Transaction costs and financing fees Transaction costs and financing fees

Redeemable preferred shares Redeemable preferred shares

Loans at non-market interest rates

Exercise Classification of Financial Exercise – Classification of Financial Instruments

Classify the items on the following Classify the items on the following slide into the appropriate categories Financial asset Financial asset Financial liability Equity instrumentq y NOT a financial instrument

Exercise (cont’d) Exercise (cont d)• Cash

A t bl

• Investment property

Li f dit• Accounts payable

• Demand loan payable

• Line of credit

• Income taxes payable

• Inventory

• Demand loan receivable

• Preferred shares (non-redeemable)

• Bond payable• Demand loan receivable

• Warranty obligation

• Bond payable

• Common shares

Key definitionsKey definitions

Financial instrument Financial instrument

Contract that creates financial asset for one Contract that creates financial asset for one entity and financial liability or equity instrument of another entity

Financial assetFinancial asset

cashcas contractual right to ...

(i) receive cash(ii) receive another financial asset from

another party(iii) exchange financial instruments with(iii) exchange financial instruments with

another party under conditions that are potentially favourable to the entity

Financial liabilityFinancial liability

contractual obligation to ...co t actua ob gat o to(i) deliver cash(ii) deliver another financial asset to another

party(iii) exchange financial instruments with

another party under conditions that areanother party under conditions that are potentially unfavourable to the entity

Equity instrument

contract that results in a residual interest in assets of an entity after deducting all of its liabilities

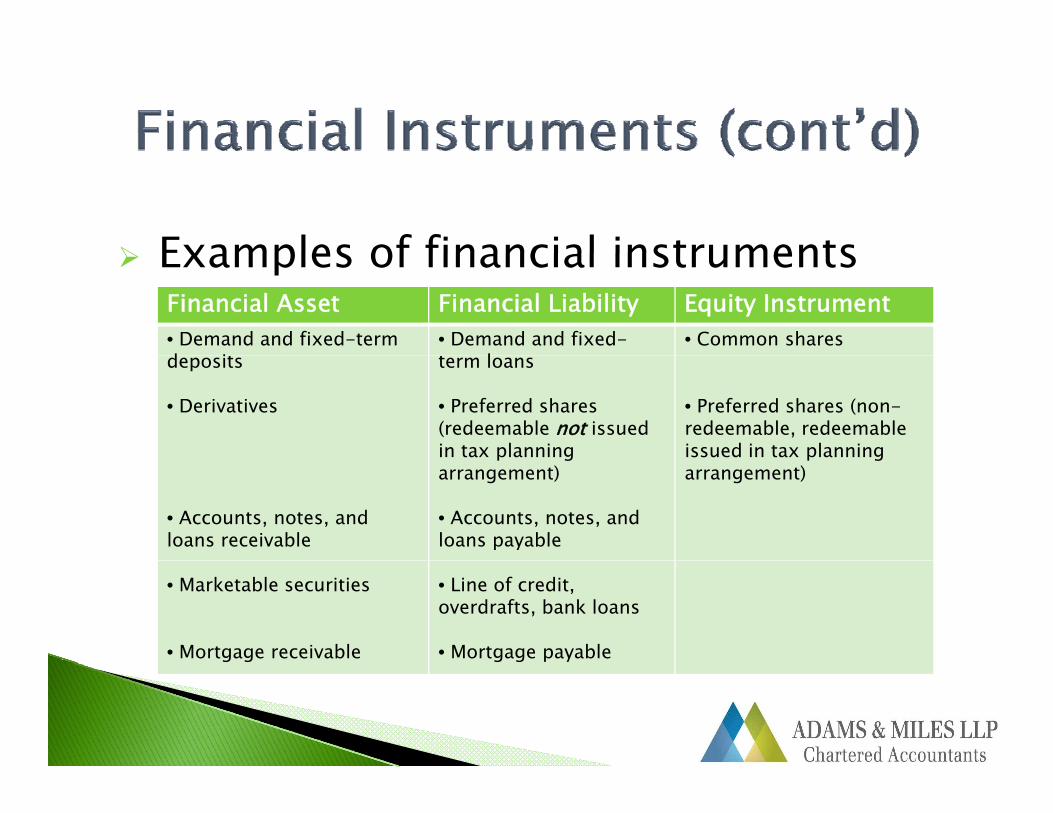

Examples of financial instruments Examples of financial instrumentsFinancial Asset Financial Liability Equity Instrument• Demand and fixed-term d i

• Demand and fixed-l

• Common sharesdeposits

• Derivatives

term loans

• Preferred shares (redeemable not issued in tax planning

• Preferred shares (non-redeemable, redeemable issued in tax planning

• Accounts, notes, and loans receivable

p garrangement)

• Accounts, notes, and loans payable

p garrangement)

• Marketable securities

• Mortgage receivable

• Line of credit, overdrafts, bank loans

• Mortgage payable

Initial measurement (Day 1) Initial measurement (Day 1)

ALWAYS at fair value ALWAYS at fair value The question is which components are included in

fair value A ti f t ti t d fi i f Accounting for transaction costs and financing fees

depends on... how the financial instrument will be measured subsequently

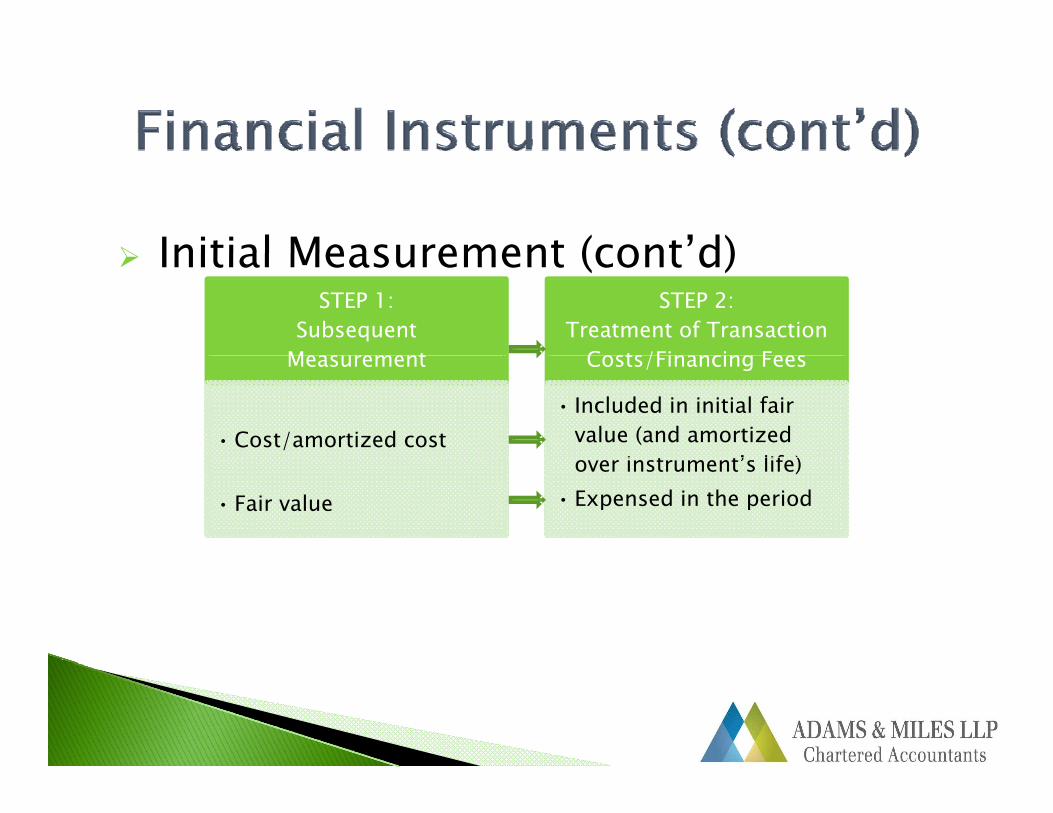

Initial Measurement (cont’d) Initial Measurement (cont d)STEP 1:

Subsequent Measurement

STEP 2:Treatment of Transaction

Costs/Financing FeesMeasurement

• Cost/amortized cost

Costs/Financing Fees

• Included in initial fair value (and amortized

i ’ lif )

• Fair value

over instrument’s life)• Expensed in the period

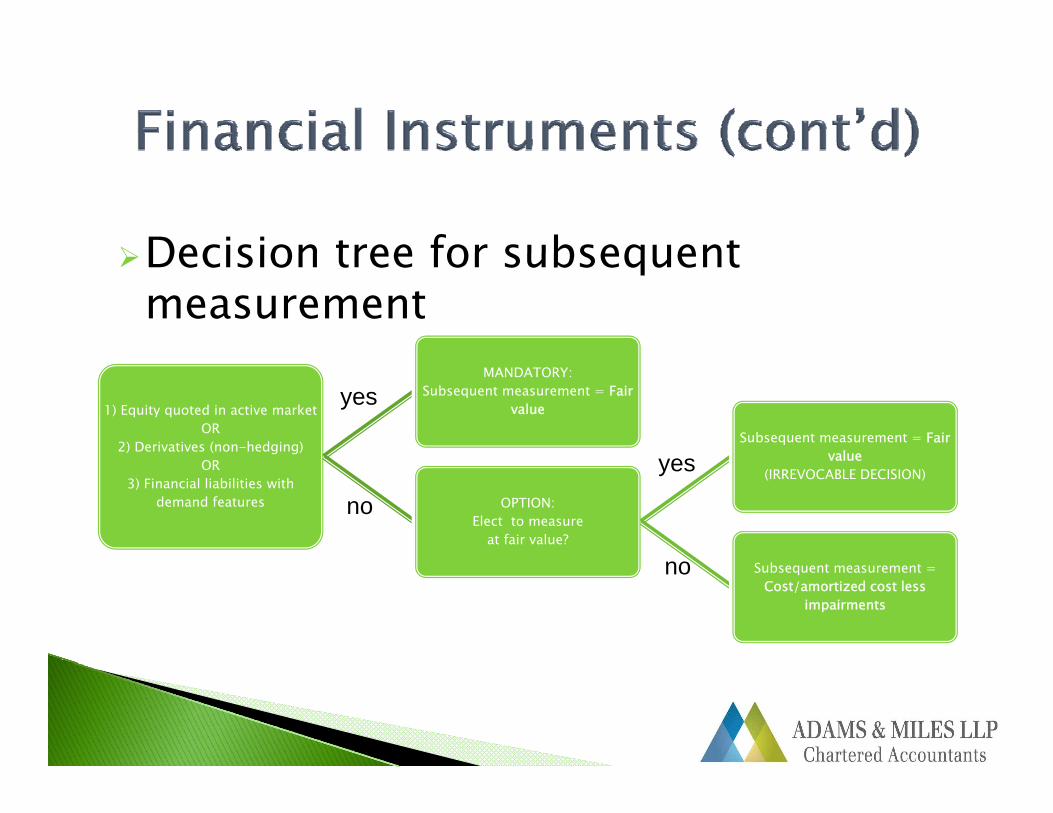

Decision tree for subsequentDecision tree for subsequent measurement

1) Equity quoted in active market OR

2) Derivatives (non-hedging)

MANDATORY:Subsequent measurement = Fair

value

Subsequent measurement = Fair value

yes

OR3) Financial liabilities with

demand features OPTION:Elect to measure

at fair value?

value(IRREVOCABLE DECISION)

no

yes

Subsequent measurement = Cost/amortized cost less

impairments

no

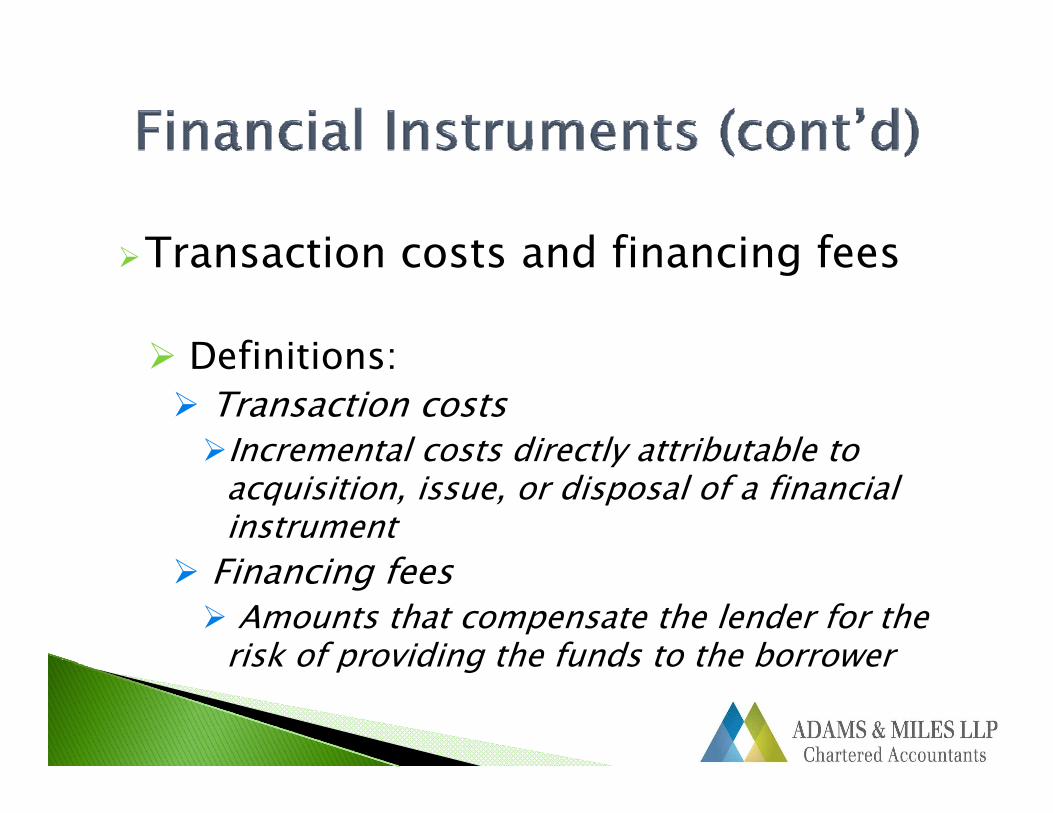

Transaction costs and financing feesTransaction costs and financing fees

Definitions: Definitions: Transaction costsIncremental costs directly attributable toIncremental costs directly attributable to

acquisition, issue, or disposal of a financial instrument

Fi i f Financing fees Amounts that compensate the lender for the

risk of providing the funds to the borrowerrisk of providing the funds to the borrower

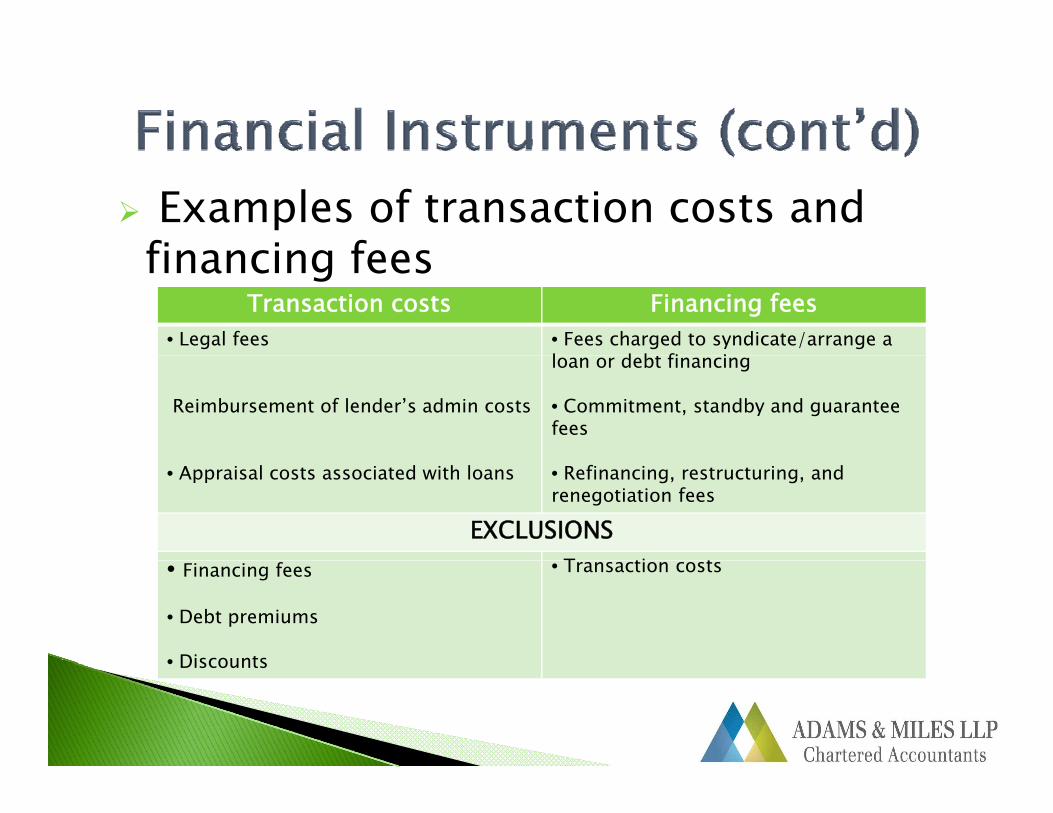

Examples of transaction costs and financing feesfinancing fees

Transaction costs Financing fees• Legal fees • Fees charged to syndicate/arrange a

l d b fi i

Reimbursement of lender’s admin costs

loan or debt financing

• Commitment, standby and guarantee fees

• Appraisal costs associated with loans • Refinancing, restructuring, and renegotiation fees

EXCLUSIONST ti t• Financing fees

• Debt premiums

• Discounts

• Transaction costs

• Discounts

Transaction costs and financing fees –Transaction costs and financing fees Example Problem

ABC Limited obtains a ten yearloan for ABC Limited obtains a ten yearloan for $500,000. There are financing fees of $25,000 incurred to arrange the loan. No elections have been made by ABC Limitedelections have been made by ABC Limited related to the subsequent measurement of this loan. What is the initial carrying amount of the What is the initial carrying amount of the

loan that is recognized in the books of ABC Limited?

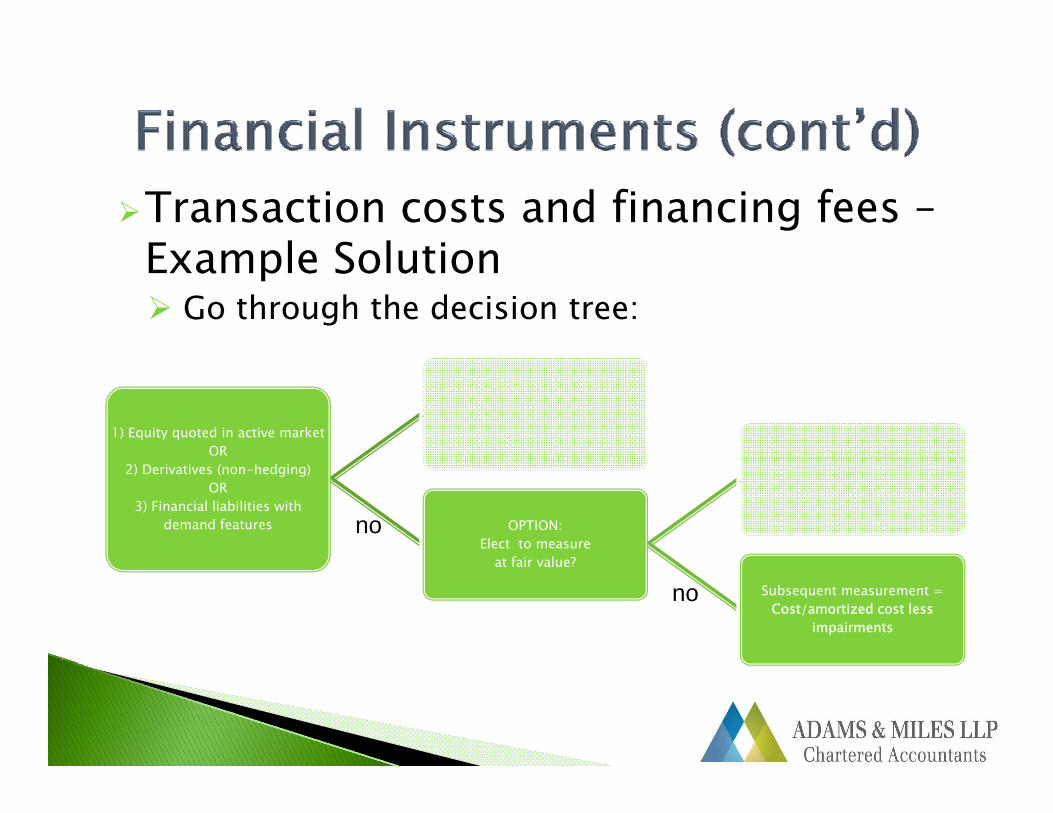

Transaction costs and financing fees –Example SolutionExample Solution Go through the decision tree:

1) Equity quoted in active market OR

2) Derivatives (non-hedging)OR

3) Financial liabilities with demand features OPTION:

Elect to measure at fair value?

noat fair value?

Subsequent measurement = Cost/amortized cost less

impairments

no

Transaction costs and financing feesTransaction costs and financing fees –Example Solution

Now determine day 1 accounting (initial carrying amount): Since subsequently measured at cost/amortized cost

less impairments => financing fees must be included in the fair value of the loan, i.e., netted against cost of th lthe loan

Initial carrying amount = $500,000 gross loan proceeds minus $25,000 financing fees = $475,000

Transaction costs and financing fees –Transaction costs and financing fees Example Solution – Journal Entry

Initial recognition: DR Cash 475,000 (= 500k-25k)CR Loan payable 475 000CR Loan payable 475,000

Subsequent annual entries:DR Financing fees exp 2,500 (=25k/10 yrs)C bl 2 00CR Loan payable 2,500

* Assumed financing fees recognized evenly over the term

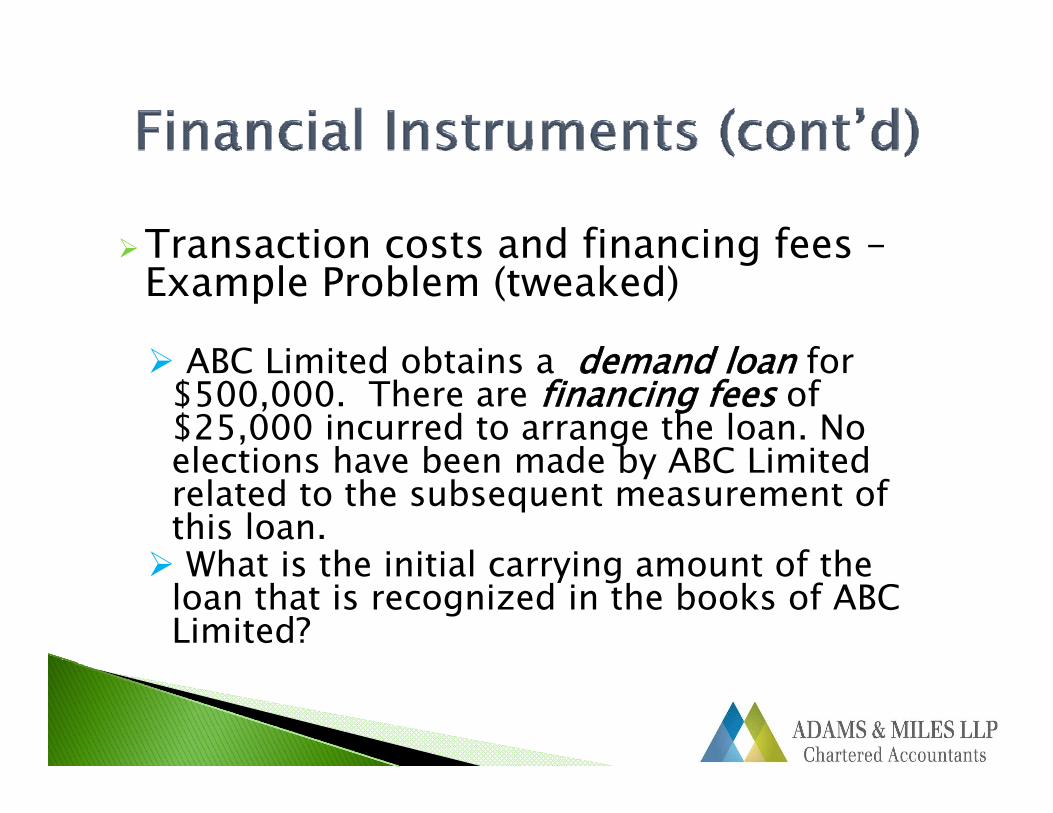

Transaction costs and financing fees –Transaction costs and financing fees Example Problem (tweaked)

ABC Limited obtains a demand loan for ABC Limited obtains a demand loan for $500,000. There are financing fees of $25,000 incurred to arrange the loan. No elections have been made by ABC Limitedelections have been made by ABC Limited related to the subsequent measurement of this loan. What is the initial carrying amount of the What is the initial carrying amount of the

loan that is recognized in the books of ABC Limited?

Transaction costs and financing fees –Example Solution (tweaked)Example Solution (tweaked) Go through the decision tree

1) Equity quoted in active market OR

2) D i i ( h d i )

MANDATORY:Subsequent measurement = Fair

valueyes2) Derivatives (non-hedging)

OR3) Financial liabilities with

demand features

Transaction costs and financing feesTransaction costs and financing fees –Example Solution (tweaked)

Now determine day 1 accounting (initial carrying amount): Since subsequently measured at fair value =>

financing fees must be expensed in the period the fee is incurred

Initial carrying amount = $500,000 gross loan

Transaction costs and financing feesTransaction costs and financing fees –Example Solution (tweaked) – Journal EntryEntry

Initial recognition: Initial recognition: DR Cash 475,000DR Financing fees exp 25,000CR Loan payable 500,000

Transaction costs and financing feesTransaction costs and financing fees –Final Summary

In order to determine the proper accounting treatment, you should know what the features of the credit facility/other financial liability are as well as what types of fees are being charged

Redeemable preferred sharesRedeemable preferred shares

Liability or equity? Liability or equity? Decision tree in CICA HB s3856 – Appendix A

(29)

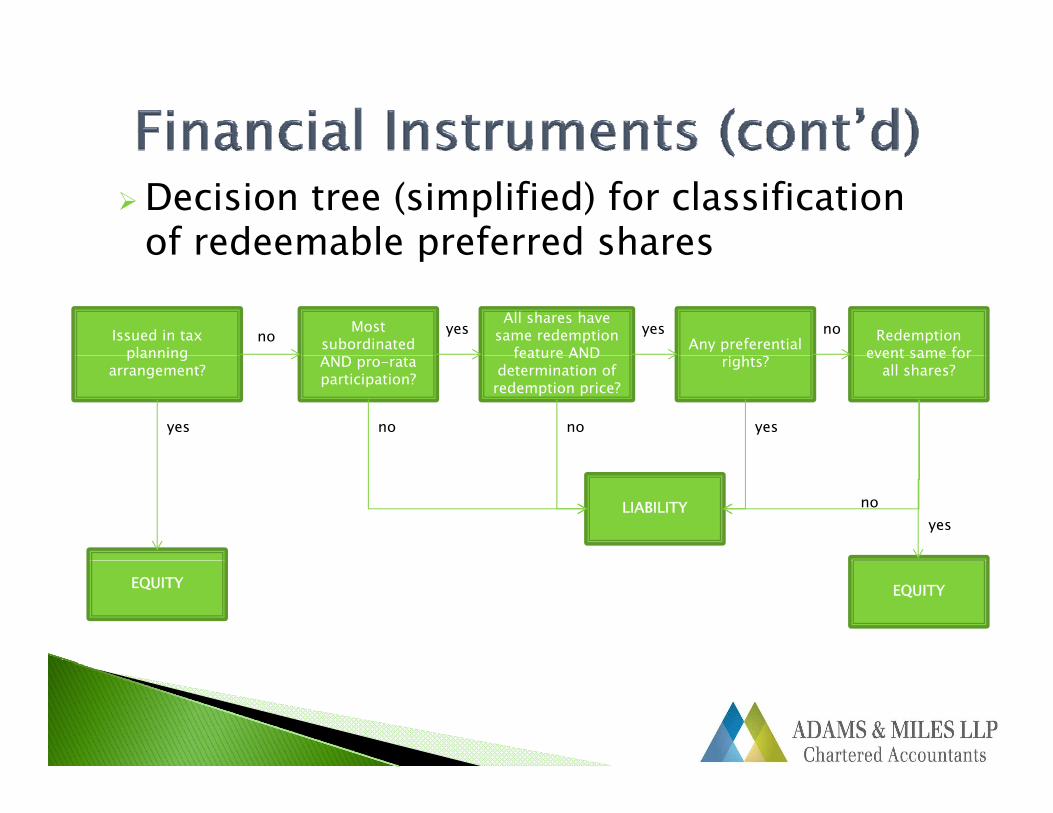

Decision tree (simplified) for classificationof redeemable preferred sharesof redeemable preferred shares

Issued in tax planning

Most subordinated

All shares have same redemption

feature ANDyes

Any preferential h

yes Redemption event same for

nonoplanning

arrangement? AND pro-rata participation?

yes

feature AND determination of redemption price?

rights? event same for all shares?

no no yes

LIABILITYyes

no

EQUITY EQUITY

Financial Instruments - LoansFinancial Instruments Loans

Example On January 1, 2013, Seller Inc. finances Buyer

Co’s purchase of a $18,000 vehicle. Terms of repayment includes monthly repayment of $300repayment includes monthly repayment of $300 for 5 years with no interest.

Discussion – How to record initial measurement?

Loans at non-market interest rate Indication – more than a pure

lending/borrowing relationship The present value difference between the rate The present value difference between the rate

on the loan and fair market lending rate may represent part of the price of an asset

Example On January 1, 2013, Seller Inc. finances Buyer

Co’s purchase of a $18,000 vehicle. Terms of repayment includes monthly repayment of $300repayment includes monthly repayment of $300 for 5 years with no interest.

The market rate of interest for a similar loan based on Buyer Co’s credit rating is 5%.

What do we need to do?

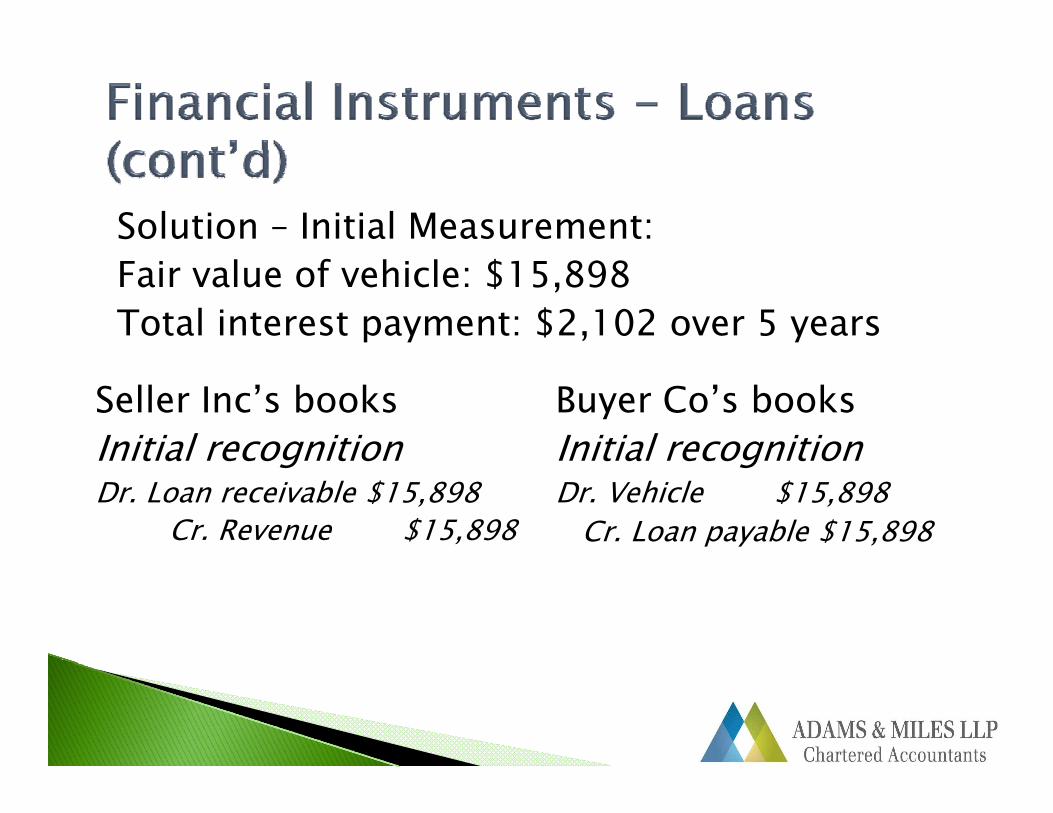

Solution – Initial Measurement:Fair value of vehicle: $15,898Total interest payment: $2,102 over 5 years

Seller Inc’s booksInitial recognition

Buyer Co’s booksInitial recognitionInitial recognition

Dr. Loan receivable $15,898Cr. Revenue $15,898

Initial recognitionDr. Vehicle $15,898

Cr. Loan payable $15,898

Solution – Subsequent recognition Effective Interest Method (Seller Inc’s perspective)(S p p )◦ Dec. 31, 2013 Dr. Cash $3,600

Cr. Loan receivable $2,870Cr. Interest income 730

◦ Dec. 31, 2014 Dr. Cash $3,600C L i bl $3 017Cr. Loan receivable $3,017Cr. Interest income 583

◦ Dec. 31, 2015 Dr. Cash $3,600Cr. Loan receivable $3,172Cr Interest income 428Cr. Interest income 428

◦ Dec. 31, 2016 Dr. Cash $3,600Cr. Loan receivable $3,334Cr. Interest income 266

◦ Dec. 31, 2017 Dr. Cash $3,600Cr. Loan receivable $3,504Cr. Interest income 96

Note: Buyer Co’s entries would mirror those of Seller Inc’s.

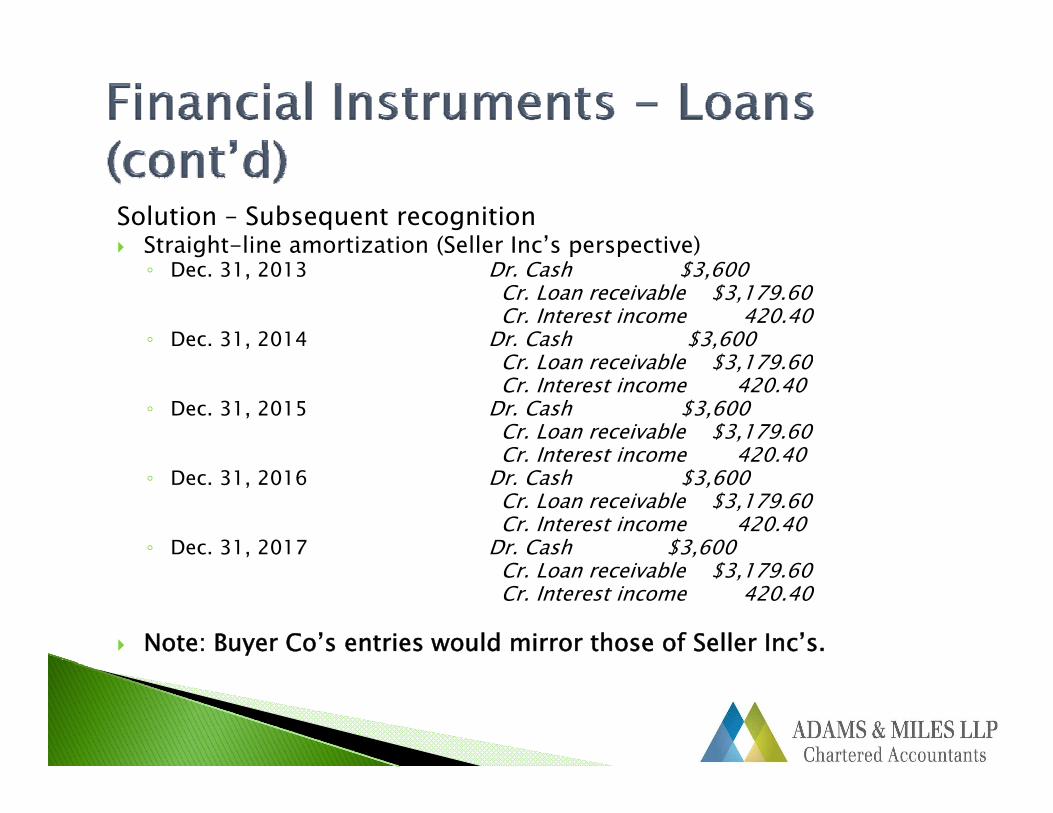

Solution – Subsequent recognition Straight-line amortization (Seller Inc’s perspective)S g (S p p )◦ Dec. 31, 2013 Dr. Cash $3,600

Cr. Loan receivable $3,179.60Cr. Interest income 420.40

◦ Dec. 31, 2014 Dr. Cash $3,600C L i bl $3 179 60Cr. Loan receivable $3,179.60Cr. Interest income 420.40

◦ Dec. 31, 2015 Dr. Cash $3,600Cr. Loan receivable $3,179.60Cr Interest income 420 40Cr. Interest income 420.40

◦ Dec. 31, 2016 Dr. Cash $3,600Cr. Loan receivable $3,179.60Cr. Interest income 420.40

◦ Dec. 31, 2017 Dr. Cash $3,600Cr. Loan receivable $3,179.60Cr. Interest income 420.40

Note: Buyer Co’s entries would mirror those of Seller Inc’s.

CICA HB s3856, 3064, Chapter 45 – www cica ca Chapter 45 www.cica.ca

PrepaidsPrepaids

Back to BasicsBack to Basics Definition (s3064)

Common Examples NPOs NPOs Profit-oriented enterprises

Prepaids fall under category ofPrepaids fall under category of... Intangible assets (s3064 of Part II of the HB)the HB)

4 major components in definition of 4 major components in definition of Intangible assets

Definition and Recognition of Definition and Recognition of Intangible asset (s3064) Identifiability Identifiability Control over a resource Existence of future economic benefits Cost of asset can be measured reliably

If criteria are not met the item MUST be If criteria are not met, the item MUST be expensed when incurred

Identifiability Identifiability

Identifiable whenIdentifiable when... separable OR arises from contractual or other legal rightsarises from contractual or other legal rights

Control Control

Power to Power to ... obtain future economic benefits from underlying

resourcerestrict access of others to those future economic

benefits

Future economic benefits Future economic benefits

Management should assess this probability Management should assess this probability ... using reasonable and supportable assumptions May include ... y revenue from sale of products/services cost savings h b fi l i f f b other benefits resulting from use of asset by

entity

Examples – NPOsExamples NPOs

NPO Org hosts an annual fundraising gala every June. It’s year end is March 31 2013 Tickets are bookedIt s year end is March 31, 2013. Tickets are booked and paid for in advance of the gala– mainly in January and February of each year. Sponsorships are also received in those months. Significant costs incurred b f d i f h d i hbefore year end comprise of the deposits on the banquet hall and catering services, deposit on entertainment band, and time spent by staff organizing the event. Historically, revenues haveorganizing the event. Historically, revenues have exceeded expenditures for this gala. Should any of these costs be classified as a prepaid

or expensed?

Examples – NPOs (cont’d)p ( )

Are the costs identifiable? relate specifically to a single event...YES

Does NPO Org have control over the asset? NPO Org is the only entity who will receive cash flows from the

fundraiser...YES

Are there future economic benefits that will flow to NPO Org? Are there future economic benefits that will flow to NPO Org? the gala has generated revenues that exceed expenditures historically and

significant tickets and sponsorships have been received this year as well...YES

Can the costs be reliably measured? invoices supporting cost for deposit on banquet hall, catering,

entertainment...YES Support for time spent by staff on the event?

Examples NPOs (cont’d)Examples – NPOs (cont d)

If the costs meet all of the criteria (including If the costs meet all of the criteria (including supporting the time spent by staff on the fundraiser), all of the costs may be classified as a prepaid (current asset) on the balance sheet

The costs will be expensed when the fundraising The costs will be expensed when the fundraising gala is held in June 2013 (i.e., after year end)

Examples – NPOs (tweaked)Examples NPOs (tweaked)

NPO Org will host its first annual fundraising NPO Org will host its first annual fundraising gala in June 2013. It’s year end is March 31, 2013. NPO Org has struggled to generate ticket revenue and sponsorships. Significant costsrevenue and sponsorships. Significant costsincurred before year end comprise of the deposits on the banquet hall and catering services, deposit on entertainment band, andservices, deposit on entertainment band, and time spent by staff organizing the event. Should these costs be classified as a prepaid or

expensed?expensed?

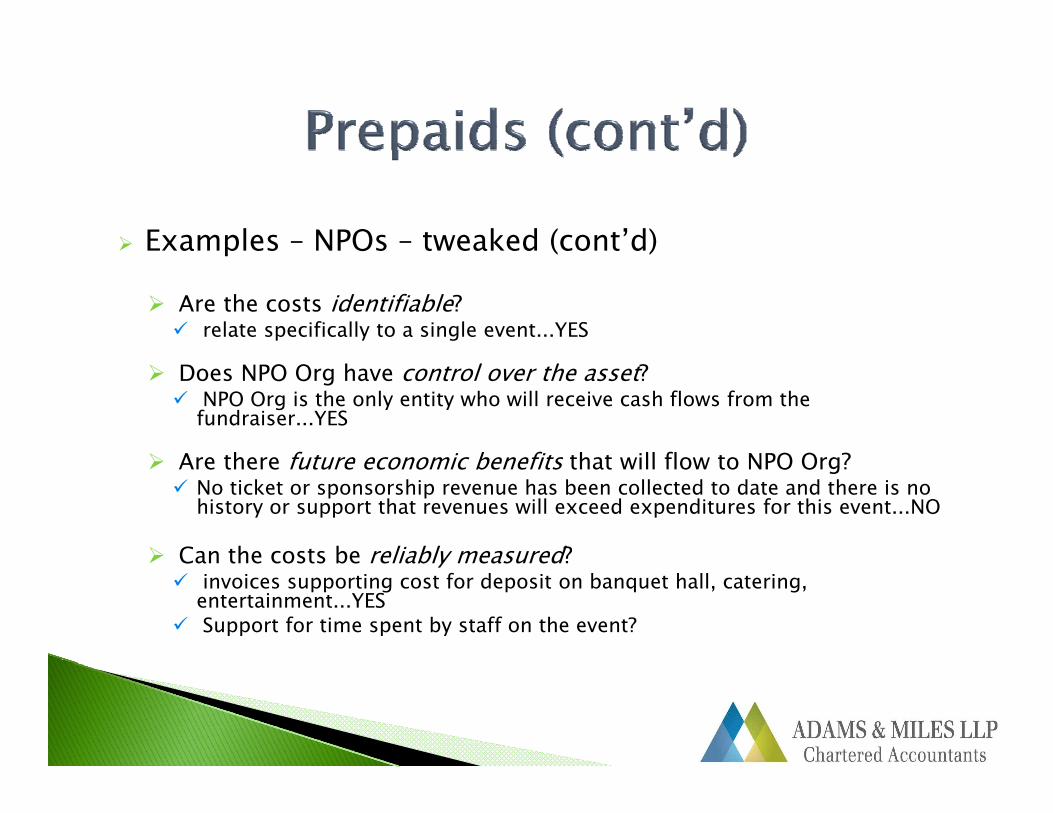

Examples – NPOs – tweaked (cont’d)p ( )

Are the costs identifiable? relate specifically to a single event...YES

Does NPO Org have control over the asset? NPO Org is the only entity who will receive cash flows from the

fundraiser...YES

Are there future economic benefits that will flow to NPO Org? Are there future economic benefits that will flow to NPO Org? No ticket or sponsorship revenue has been collected to date and there is no

history or support that revenues will exceed expenditures for this event...NO

Can the costs be reliably measured? Can the costs be reliably measured? invoices supporting cost for deposit on banquet hall, catering,

entertainment...YES Support for time spent by staff on the event?

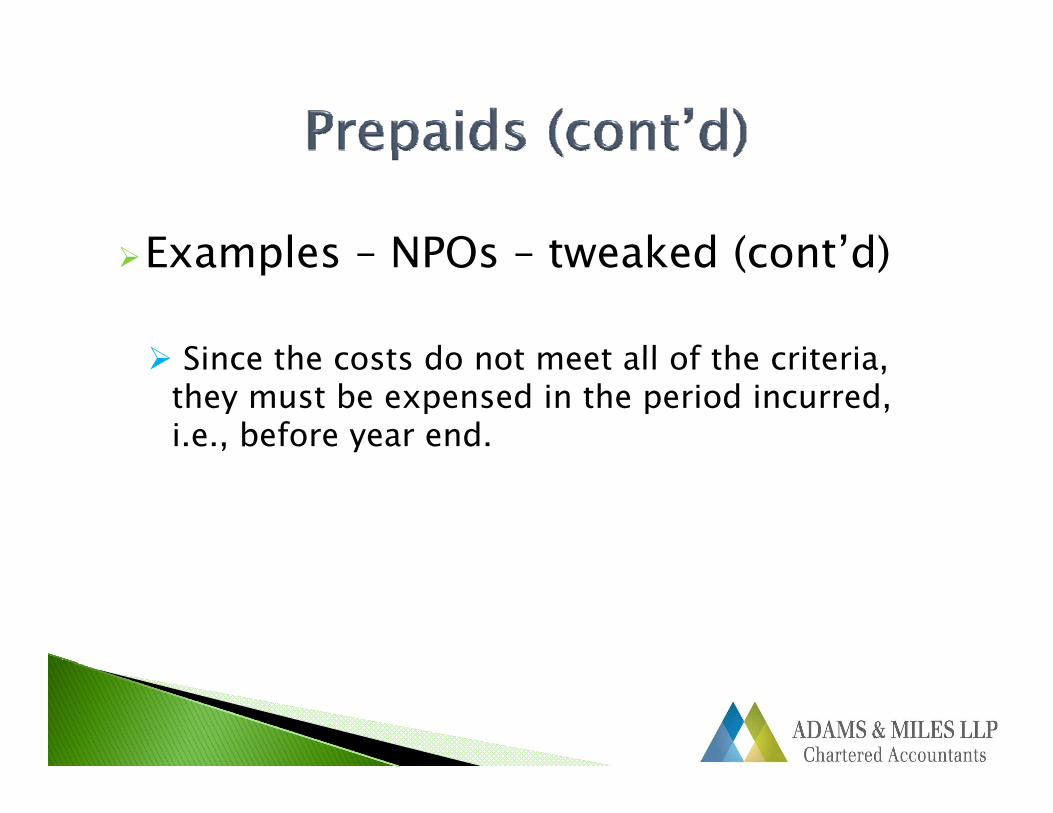

Examples NPOs tweaked (cont’d)Examples – NPOs – tweaked (cont d)

Since the costs do not meet all of the criteria Since the costs do not meet all of the criteria, they must be expensed in the period incurred, i.e., before year end.

Examples Profit OrientedExamples – Profit Oriented (Discussion) Should the following items be recorded as Should the following items be recorded as

prepaids? Rent paid in advance Promotional catalogues (paid for and received) Printing paper on hand at year end

Revenue RecognitionRevenue Recognition

Determining when revenue should beDetermining when revenue should be recorded?

If in doubt refer to section 3400 in Part II of the handbook.

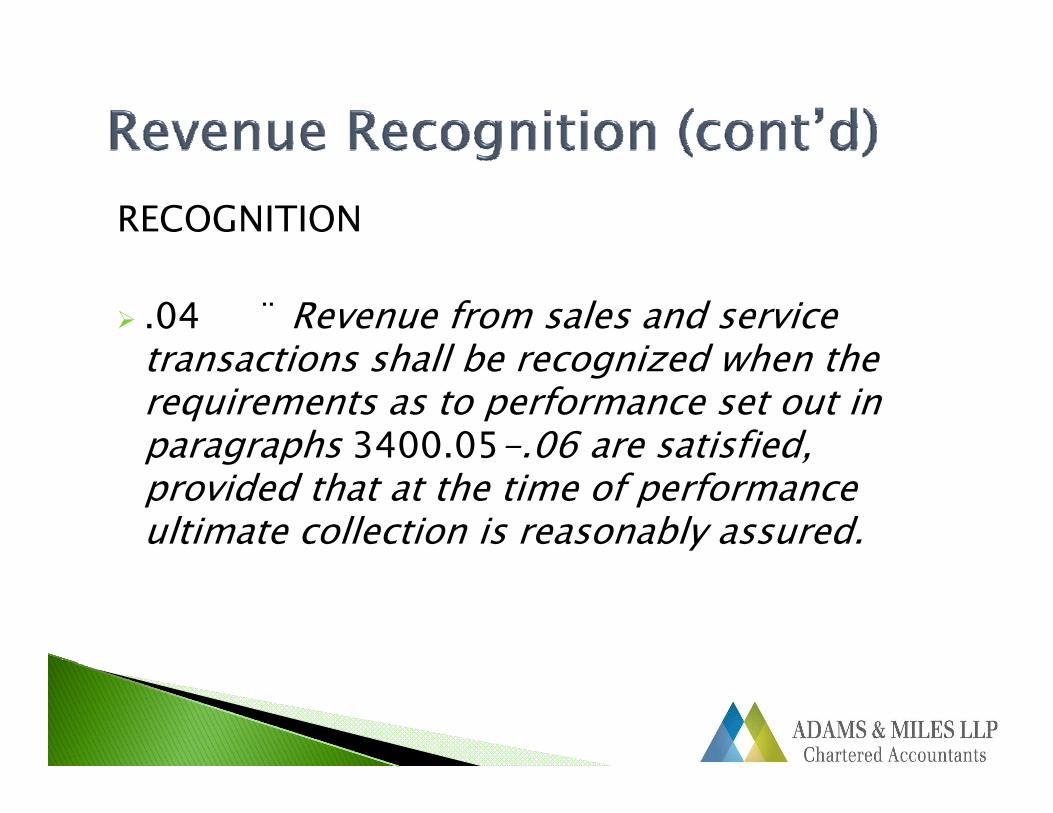

RECOGNITION

.04 ¨ Revenue from sales and service transactions shall be recognized when thetransactions shall be recognized when the requirements as to performance set out in paragraphs 3400.05-.06 are satisfied, p g p 3 00 05 06 ,provided that at the time of performance ultimate collection is reasonably assured.

.05 ¨ In a transaction involving the sale of goods, performance shall be regarded as having been achieved when the following conditionsbeen achieved when the following conditions have been fulfilled:

◦ (a) the seller of the goods has transferred to the buyer the significant risks and rewards of ownership, in that all significant acts have been completed and the seller retains no continuing managerial involvement in orretains no continuing managerial involvement in, or effective control of, the goods transferred to a degree usually associated with ownership; and

◦ (b) reasonable assurance exists regarding the measurement of the consideration that will be derived from the sale of goods, and the extent to which goods g , gmay be returned.

Performance is complete when the following three criteria are metfollowing three criteria are met.

Persuasive evidence Delivery hasPersuasive evidence of an arrangement

exists

Delivery has occurred or services

been rendered

Th ll ’ iThe sellers’ price to the buyer is fixed or

determinable

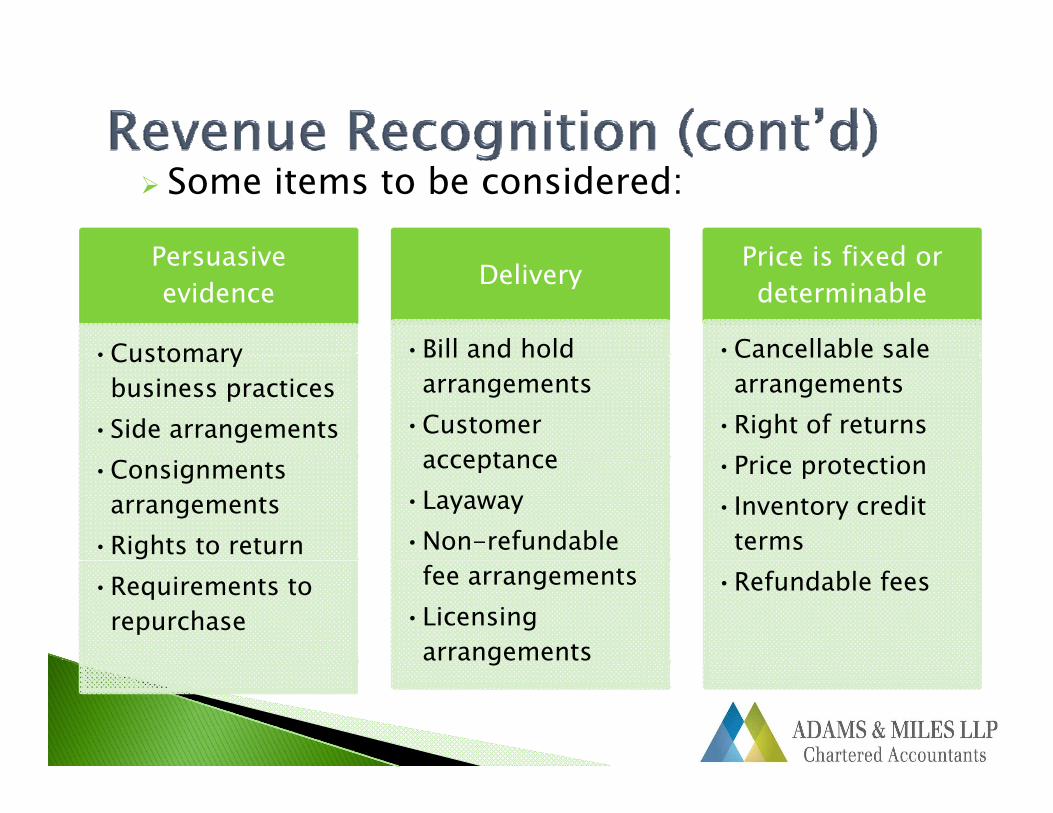

Some items to be considered:

Persuasive Price is fixed orPersuasive evidence

•Customary

Delivery

•Bill and hold

Price is fixed or determinable

•Cancellable sale•Customary business practices

•Side arrangements

Bill and hold arrangements

•Customer acceptance

Cancellable sale arrangements

•Right of returnsP i t ti•Consignments

arrangements•Rights to return

acceptance•Layaway•Non-refundable

•Price protection•Inventory credit

terms•Requirements to

repurchasefee arrangements

•Licensing arrangements

•Refundable fees

g

The tough situations:

What to do with long term contracts?What to do with long-term contracts? Percentage of Completion or Completed Contractp

Percentage of completion is used when f i f h i fperformance consists of the execution of more

than one act, and revenue would be recognized proportionately by reference to the performance of each act.

Completed contract generally only Completed contract generally only appropriate when there is a single act or estimation of progress towards completion cannot be madecannot be made.

What to do with sales with multiple deliverables? Section 3400 is usually applied separately to

each transaction. Th b i h h h i l There may be times though that a single transaction may involve multiple deliverables. The key is to determine if the sale is one or more thanThe key is to determine if the sale is one or more than

one transaction. Examples of single transactions with multiple

d li bl ld b i t h ithdeliverables would be equipment purchases with a maintenance contract or servicing contract.

Example 1:

Company A is a distributor of picture frames. It is currently selling a high-end frame that it

has never sold before, however, the product is similar to another that Company A usually sellssimilar to another that Company A usually sells.

The Company is selling 15 frames at a price of $30,000. Normal 30 day return period. For$30,000. Normal 30 day return period. For COD.

When should Company A recognize revenue?

Example 1 – Answer:p Persuasive evidence of an arrangement exists

– no unusual arrangements and no continual i l dmanagement involvement noted

Delivery – the product has been delivered to the customerthe customer

Price is determinable – the price is set at $30,000. The only question is if an estimate$30,000. The only question is if an estimate for returns can be made?

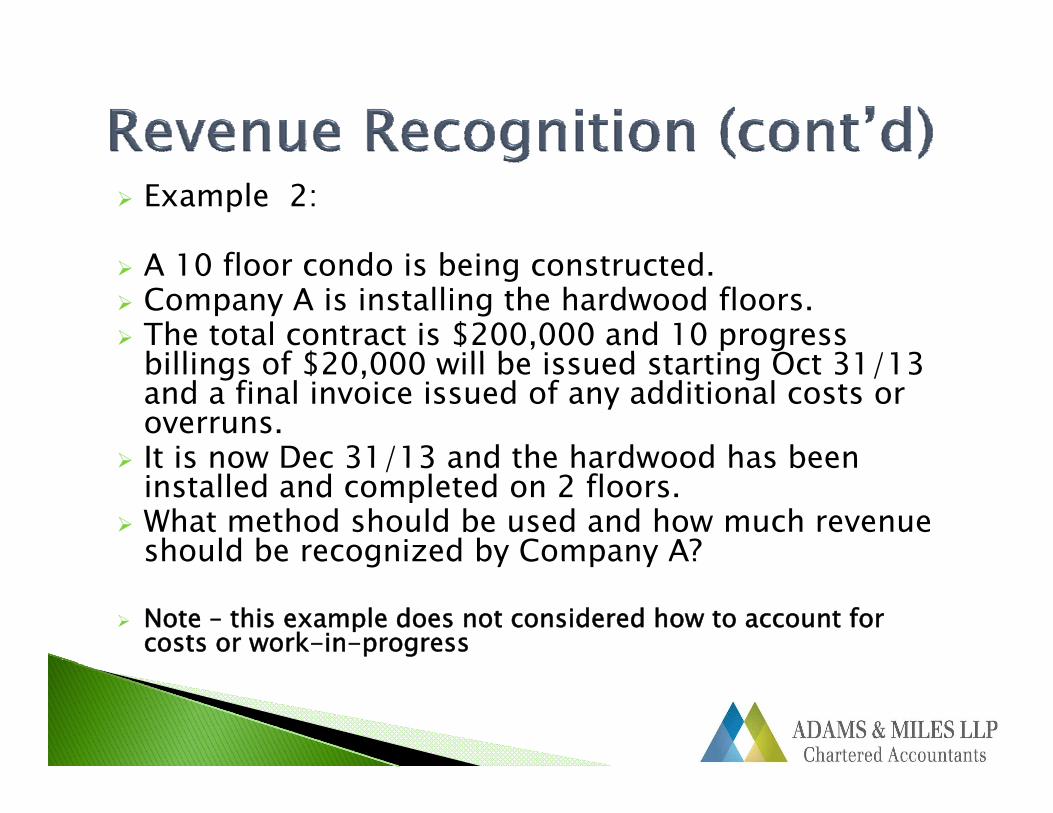

Example 2:

fl d b d A 10 floor condo is being constructed. Company A is installing the hardwood floors. The total contract is $200,000 and 10 progress

billi f $20 000 ill b i d t ti O t 31/13billings of $20,000 will be issued starting Oct 31/13 and a final invoice issued of any additional costs or overruns.

It is now Dec 31/13 and the hardwood has been It is now Dec 31/13 and the hardwood has been installed and completed on 2 floors.

What method should be used and how much revenue should be recognized by Company A?should be recognized by Company A?

Note – this example does not considered how to account for costs or work-in-progress

Example 2 – Answer: There is a series of acts/milestones completion There is a series of acts/milestones – completion

of individual floors We are told that 2 floors are completed thus

progress of the milestone can be estimatedprogress of the milestone can be estimated As of Dec 31/13 – 3 progress bills have been

issued for a total of $60,000 (3 x $20,000)2 floors completed which represents 20% of the 2 floors completed which represents 20% of the total project of 10 floors or $40,000 of contract price (20% x $200,000)

$40 000 revenue should be recorded as of Dec $40,000 revenue should be recorded as of Dec 31/13. Based on performance/completion of work and not the billings issue.

Example 3:

Company A sells photocopiers. Company A also includes an option for

customers to buy an extended service plan. Company Z purchased the elite model copierCompany Z purchased the elite model copier

for $20,000 and purchased the extended service plan (3 years) for an additionalservice plan (3 years) for an additional $3,000.

When should Company A record revenue?

Example 3 - Answer: Example 3 Answer: The sale on the photocopier should be

recorded when delivered. Risks and rewards have transferred. Nothing to indicate otherwise. S l t d d i t t Sale on extended service contract With initial sale of photocopierOver three year period (contract term)

The answer is – over the three year period. H bl k d hi

Over three year period (contract term)At the end of the service contract (after three years)

However, not black and white

InventoryInventory

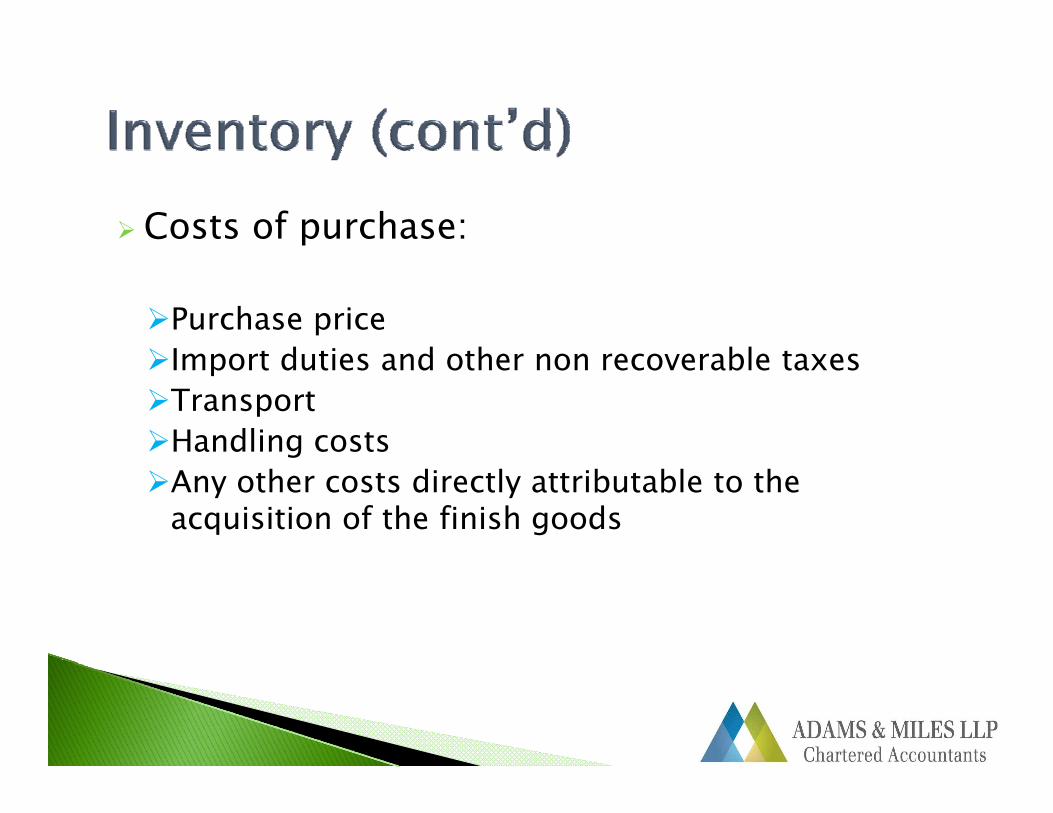

Per Section 3031.11;

“The cost of inventories shall comprise all f h f i dcosts of purchase, costs of conversion and

other costs incurred in bringing the inventories to their present location andinventories to their present location and condition.”

Costs of purchase:

Purchase priceImport duties and other non recoverable taxesImport duties and other non recoverable taxesTransportHandling costsAny other costs directly attributable to the

acquisition of the finish goods

Cost of conversion must include the following:Costs directly attributable to the units of

production such as direct labourproduction, such as direct labourA systematic allocation of fixed and variable

production overheads incurred in converting the t i l i t fi i h d d S lmaterial into finished goods. Some examples are:AmortizationMaintenance of building and equipmentCost of factory management and administration

Are these costs to be included or excluded from inventory?Storage costsOffice admin costsOffice admin costsCost of wasted materialsSelling costs

Impairmentsp Inventory Investments

bl Accounts Receivable Long-Lived Assets

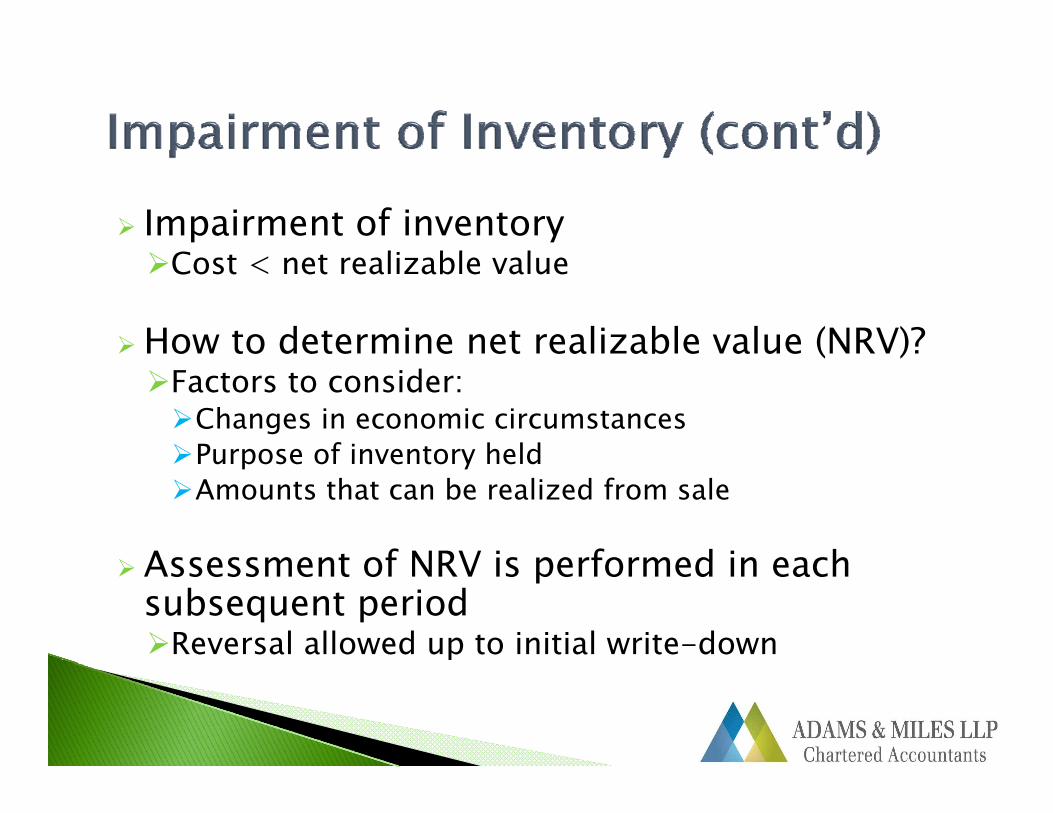

Per Section 3031.27, there is impairment of inventory when:

“Th t f i t i t b bl if“The cost of inventories may not be recoverable if those inventories are damaged, if they have become wholly or partially obsolete, or if their selling prices have declined.”

Impairment of inventory C li bl lCost < net realizable value

How to determine net realizable value (NRV)?( )Factors to consider:Changes in economic circumstancesPurpose of inventory heldPurpose of inventory heldAmounts that can be realized from sale

Assessment of NRV is performed in eachAssessment of NRV is performed in each subsequent periodReversal allowed up to initial write-down

This section applies to investments except:

Subsidiaries or interest in joint ventures that are consolidated or reported on the proportionateconsolidated or reported on the proportionate consolidation basis (Section 3055);

Financial instruments (3856);

Investments held by investment companies (AcGInvestments held by investment companies (AcG-18)

Test for impairment:

At the end of each reporting period, an entity shall assess whether there are any indications that anassess whether there are any indications that an investment may be impaired. And;

A tit h ll d t i h th i ifi tAn entity shall determine whether a significant adverse change has occurred during the period in the expected timing or amount of future cash flows from the investment.

Indicators of impairment include:significant financial difficulty of the investee;it becoming probable that the investee will enter

bankruptcy or other financial reorganization;bankruptcy or other financial reorganization;the disappearance of an active market for shares of

the investee because of financial difficulties; and i ifi t d h i th t h l i la significant adverse change in the technological,

market, economic or legal environment in which the investee operates, or in the market to which an asset is dedicated (for example, a sharp decline in the price of a commodity that may cause economic instability in the investee's industry).y y)

When there is an indication of impairment, the carrying amount should be reduced to the higher ofcarrying amount should be reduced to the higher of the following:

(a) the present value of the cash flows expected to be ( ) p pgenerated by holding the investment, discounted using a current market rate of interest appropriate to the asset; and

(b) the amount that could be realized by selling the asset (b) the amount that could be realized by selling the asset at the balance sheet date.

The carrying amount of the investment shall be y greduced – and the amount recognized as an impairment should be recorded in net income.

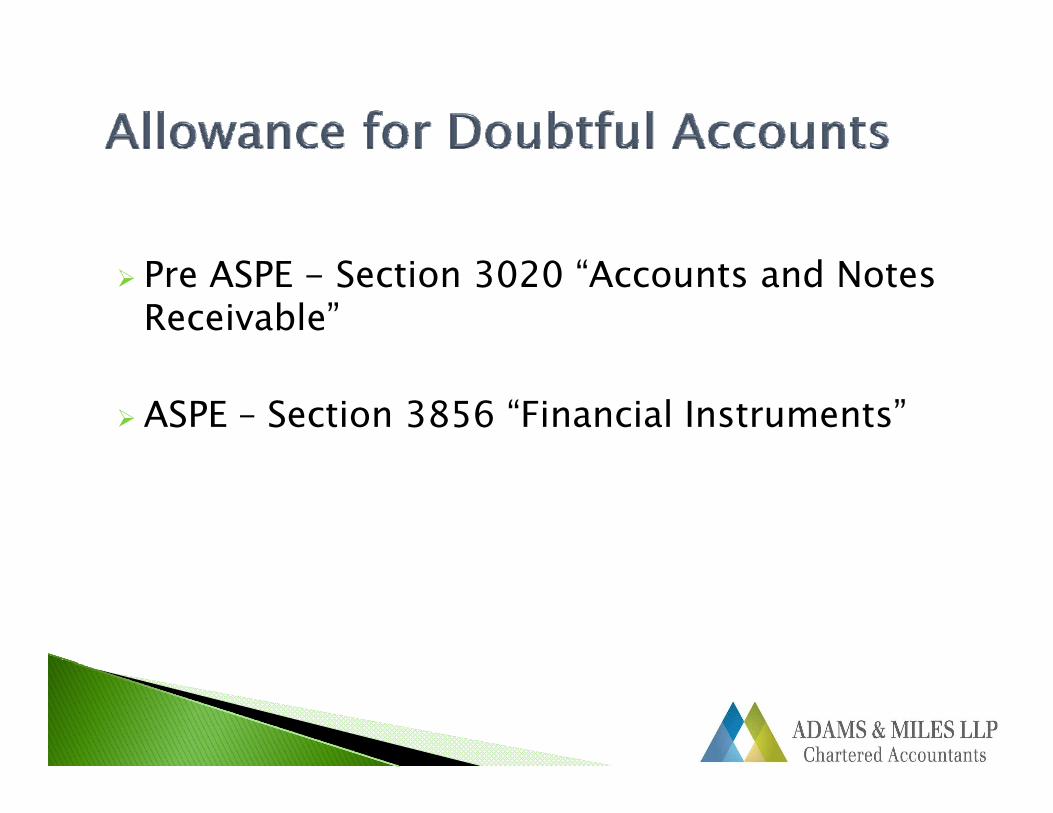

Pre ASPE - Section 3020 “Accounts and Notes Receivable”

ASPE – Section 3856 “Financial Instruments”

Main guidance in previous standards was Section 3020.10;

“A i bl h ld b“An account or note receivable should be written off as soon as it is known to be uncollectable or should be written down to itsuncollectable or should be written down to its estimated realizable value as soon as it is known that it is not collectible in full.”

Under new section 3856.17

When an entity identifies a significant adverse change in the expected timing or amount of future cash flows from a financial asset, it shall reduce the carrying amount of the

t t th hi h t f th f ll iasset, to the highest of the following:

(a) the present value of the cash flows expected to be generated by holding the asset, discounted using a current market g y g , grate of interest appropriate to the asset;

(b) the amount that could be realized by selling the asset, at the balance sheet date; and

(c) the amount the entity expects to realize by exercising its right to any collateral held to secure repayment of the asset, net of all costs necessary to exercise those rights.

Property Plant Intangible assetsProperty, Plant and Equipment

Intangible assets with finite useful

lilives

Long-term Prepaid assets

When to recognize?

An impairment loss shall be recognized when the carrying amount of a long-lived asset is not recoverable and exceeds its fair valuerecoverable and exceeds its fair value.

The carrying amount of a long-lived asset is not recoverable if the carrying amount exceeds therecoverable if the carrying amount exceeds the sum of the undiscounted cash flows expected to result from its use and eventual disposition. This assessment is based on the carrying amount ofassessment is based on the carrying amount of the asset at the date it is tested for recoverability, whether it is in use or under development.

If an impairment is recognized the adjusted i b h icarrying amount becomes the new carrying

amount.

For property, plant and equipment the impairment loss recognized cannot be reversed.

A long-lived asset shall be tested for recoverability whenever events or changes inrecoverability whenever events or changes in circumstances indicate that its carrying amount may not be recoverable.

Cash flow test for recoverability

.18 “Estimates of future cash flows used to test the recoverability of a long-lived asset shall y ginclude only the future cash flows (cash inflows less associated cash outflows) that are directly associated with, and that are expected to arise asassociated with, and that are expected to arise as a direct result of, its use and eventual disposition. These cash flows include the principal amount of any liabilities included in theprincipal amount of any liabilities included in the asset group, but not interest that will be recognized as an expense when incurred.”

Grouping of assets:

For purposes of recognition and f i i l lmeasurement of an impairment loss, a long-

lived asset shall be grouped with other assets and liabilities to form an asset group at theand liabilities to form an asset group at the lowest level for which identifiable cash flows are largely independent of the cash flows of other assets and liabilities.

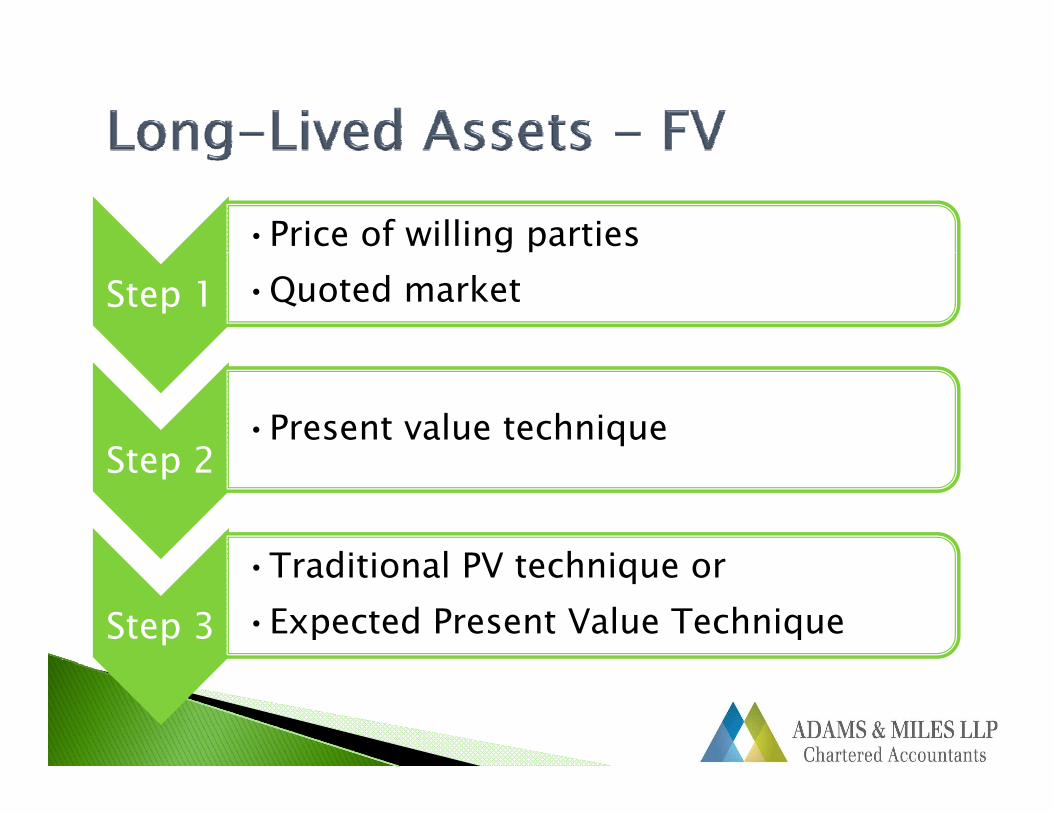

•Price of willing partiesStep 1 •Quoted market

Step 2•Present value technique

Step 2

Traditional PV technique orStep 3

•Traditional PV technique or•Expected Present Value Technique

A ll iActually, its two acts: Federal (“CNCA”) Provincial (“ONCA”) Provincial ( ONCA )

Where was your NPO incorporated?New Acts better address NPO’s needs simplify incorporation clarify Directors’ responsibilities d d ti d f ll titi reduced reporting needs for smaller entities

CNCA in force since Oct.17, 2011 Three years to transition to CNCA Three years to transition to CNCA If certificates of continuance are not filed by Oct.17, 2014 – corporation may be dissolved, p y Action items

Review letters patent, articles and by-laws Submit certificate of continuance by Oct.17 2014

ONCA anticipated in force sometime in 2014 Three years to transition to ONCA Three years to transition to ONCA Any provisions under old OCA deemed to be amended to comply with ONCA after the three p yyear period Action itemsReview and amend letters patent, articles and by-laws

ONCA Ministry of Consumer Servicesy CA/CPA NPO Director Alert May 2013

CNCACNCA Industry Canada CA/CPA NPO Director Alert December 2011

Charities Canada Revenue AgencyCa ada e e ue ge cy