Accounting of Inventories

54

Accounting of Inventories www.Afzalur.com Accounting of Inventories Slide 1 of 48 www.afzalur.com

-

Upload

afzalur-rahman -

Category

Education

-

view

467 -

download

0

Transcript of Accounting of Inventories

Accounting of Inventories

www.Afzalur.com

Accounting of Inventories

Slide 1 of 48www.afzalur.com

Accounting of Inventories

Meaning of Inventory

Inventory Valuation - Methods

Effect of Incorrect Inventory Valuation

Store (or Material) Record

Preparation of Trading Account

Treatment of Shortage / Surplus of Material

Pricing of Material Returned to store

Pricing of Material Returned to Vendor.

CHAPTER AT A GLANCE

Slide 2 of 48www.afzalur.com

Accounting of Inventories

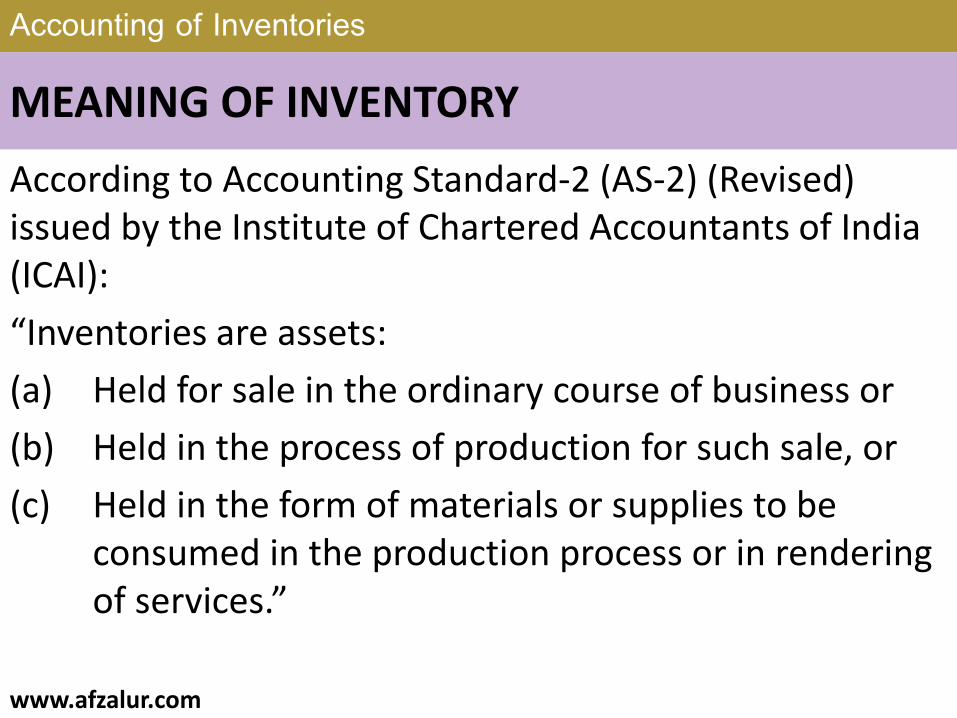

MEANING OF INVENTORY

According to Accounting Standard-2 (AS-2) (Revised) issued by the Institute of Chartered Accountants of India (ICAI):

“Inventories are assets:

(a) Held for sale in the ordinary course of business or

(b) Held in the process of production for such sale, or

(c) Held in the form of materials or supplies to be consumed in the production process or in rendering of services.”

Slide 3 of 48www.afzalur.com

Accounting of Inventories

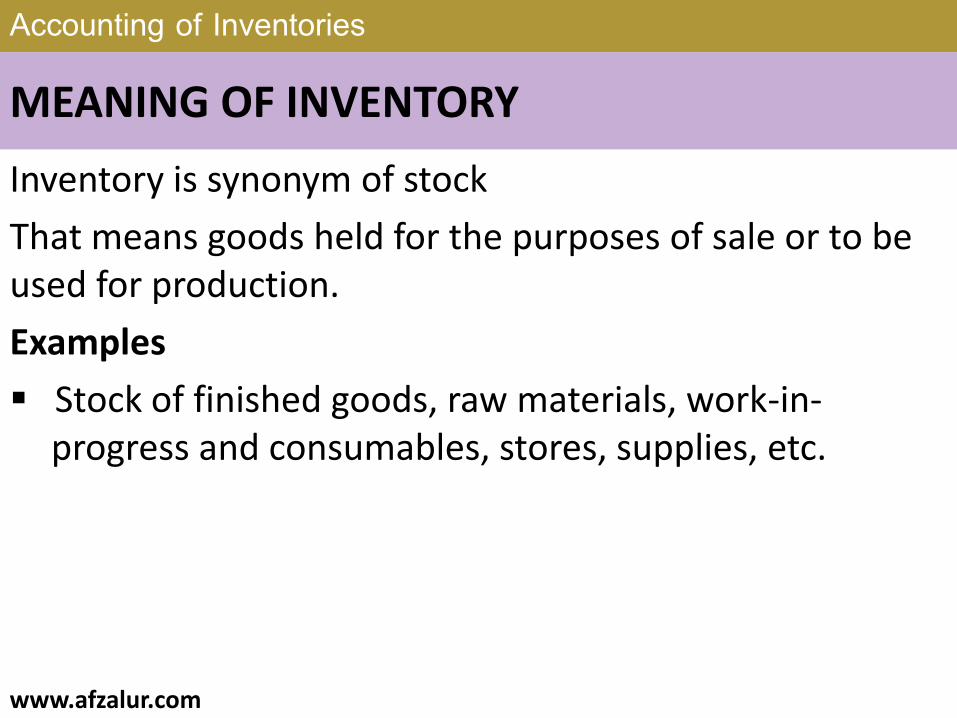

MEANING OF INVENTORY

Inventory is synonym of stock

That means goods held for the purposes of sale or to be used for production.

Examples

Stock of finished goods, raw materials, work-in-progress and consumables, stores, supplies, etc.

Slide 4 of 48www.afzalur.com

Accounting of Inventories

MEANING OF INVENTORY

At the end of an accounting period, an enterprise may have unsold goods in hand.

A manufacturing enterprise may have stock of finished goods, stock of raw materials, stores and work-in-progress.

Similarly, a trading enterprise may have stock of finished goods.

The quantities of goods held at the end of the year are known as Closing Inventory or Closing Stock which is carried forward to the next year as Opening Stock.

Slide 5 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Closing Inventory or Closing Stock is taken, valued and credited to the Manufacturing Account, in case of manufacturing enterprises or When drawing manufacturing account and

to the Trading Account, in case of other enterprises to arrive at the correct cost of goods sold and thus correct profit earned or loss incurred for the accounting period is ascertained.

Closing Inventory being an asset is shown in the Balance Sheet as a current asset. Thus, correct financial position at the year end is ascertained.

Slide 6 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Inventory is always valued at cost or net realisable value, whichever is lower following the method regularly adopted by the enterprise.

Accounting Standard – 2 (Revised) on Inventory Valuation issued by ICAI is a mandatory accounting standard.

AS – 2 (Revised) permits three methods for inventory valuation namely

1) Specific Identification Method, 2) FIFO Method and 3) Weighted Average Cost Method.

Slide 7 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Specific Identification Method.

Under this method, units in inventory are specifically identified and each unit cost is identified with a particular invoice.

Thus, the method tracks the actual physical flow of goods available whether for sale or for production. The method gives the advantage that cost charged to jobs is actual not notional.

Slide 8 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Inventory valuation method in which the actual cost of the purchased and issued (used or sold) items is identified by purchase date, serial number or particular code.

This method is suitable when cost of items forming part of inventory are not ordinarily interchangeable

and goods or services produced are segregated for specific projects and valued according to this method.

This method is applied when materials are purchased and set aside for a specific job or work order.

Slide 9 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

The method is particularly suitable for automobiles, jewellery, antiques and custom made merchandise.

Thus, the method tracks the actual physical flow of goods available whether for sale or for production.

The method gives the advantage that cost charged to jobs is actual not notional.

The method is not suitable when items are many and also interchangeable.

Slide 10 of 48www.afzalur.com

Accounting of InventoriesIllustration M/s MR Fabricators Ltd. is in the business of

manufacturing and installing windmills.

M/s BR Enterprises entered into contract with M/s MR Fabricators Ltd. for installing a windmill as per the designs supplied by it.

M/s MR Fabricators Ltd. manufactured the parts for the windmill as per the designs received.

The project was not completed at the year end and thus, inventory had to be carried forward.

Which method of inventory valuation should be applied to value the inventory?

Slide 11 of 48www.afzalur.com

Accounting of Inventories

The parts have been manufactured for the project of M/s BR Enterprises as per the design supplied by it.

It therefore, cannot be used in any other project.

It is a case of inventory being for a specific project.

Thus, M/s MR Fabricators Ltd. should adopt Specific Identification Method to value the closing inventory.

Solution

Slide 12 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

First In First Out Method (FIFO)

Method of inventory valuation based on the assumption that goods are sold or used in the same chronological order in which they are bought.

Hence, the cost of goods purchased first (first-in) is the cost of goods sold first (first-out).

Slide 13 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

It means, items in the Opening Stock are issued first,

then from the first purchase , and so on.

Items in the Closing Stock of materials are from the last purchases and thus, valued at the latest cost of purchases.

Issue of material is priced in the sequence of purchases received and this flow continues until that lot is exhausted.

Thereafter, the next lot is taken.

Slide 14 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

The effects of the method are

The issue is priced at the cost of material used because the material used is the oldest stock in hand.

Closing Stock is valued at the latest cost of purchases. Thus, the closing stock or inventory represents the current value.

Slide 15 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

FIFO Method is most suitable in times of falling prices because the issues are priced at the earliest prices which are higher. It means, cost of sales is higher and thus profit is lower.

Since the Closing Stock is valued at the latest cost of purchases, which are lower, the Profit and Loss Account shows the correct profit.

Slide 16 of 48www.afzalur.com

Accounting of Inventories

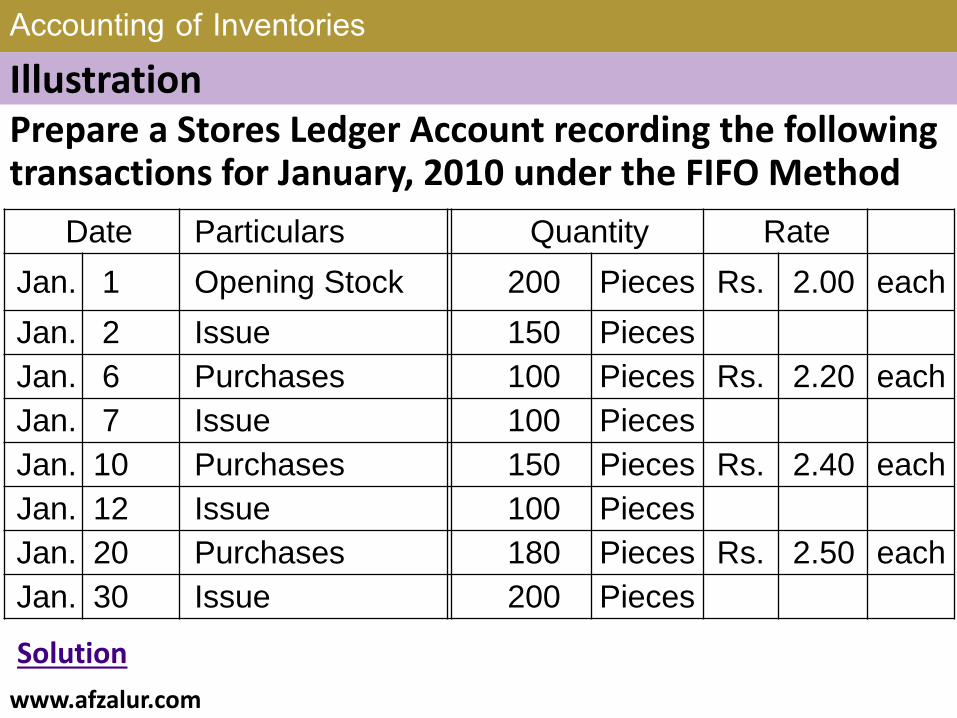

Prepare a Stores Ledger Account recording the following transactions for January, 2010 under the FIFO Method

Illustration

Date Particulars Quantity Rate

Jan. 1 Opening Stock 200 Pieces Rs. 2.00 each

Jan. 2 Issue 150 Pieces

Jan. 6 Purchases 100 Pieces Rs. 2.20 each

Jan. 7 Issue 100 Pieces

Jan. 10 Purchases 150 Pieces Rs. 2.40 each

Jan. 12 Issue 100 Pieces

Jan. 20 Purchases 180 Pieces Rs. 2.50 each

Jan. 30 Issue 200 Pieces

Solution

Slide 17 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

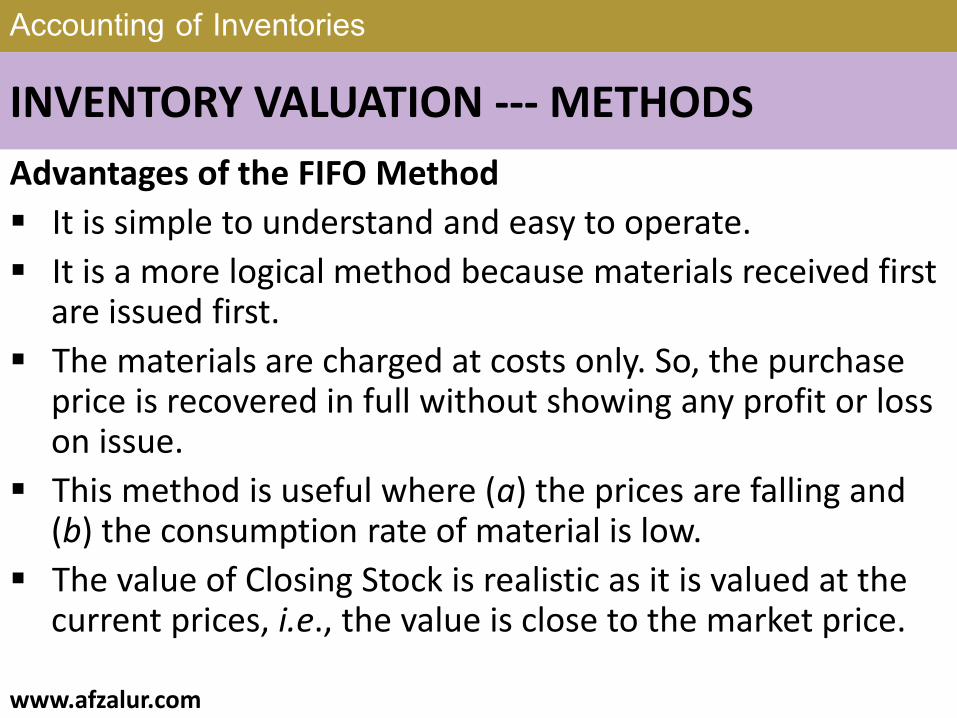

Advantages of the FIFO Method

It is simple to understand and easy to operate.

It is a more logical method because materials received first are issued first.

The materials are charged at costs only. So, the purchase price is recovered in full without showing any profit or loss on issue.

This method is useful where (a) the prices are falling and (b) the consumption rate of material is low.

The value of Closing Stock is realistic as it is valued at the current prices, i.e., the value is close to the market price.

Slide 18 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

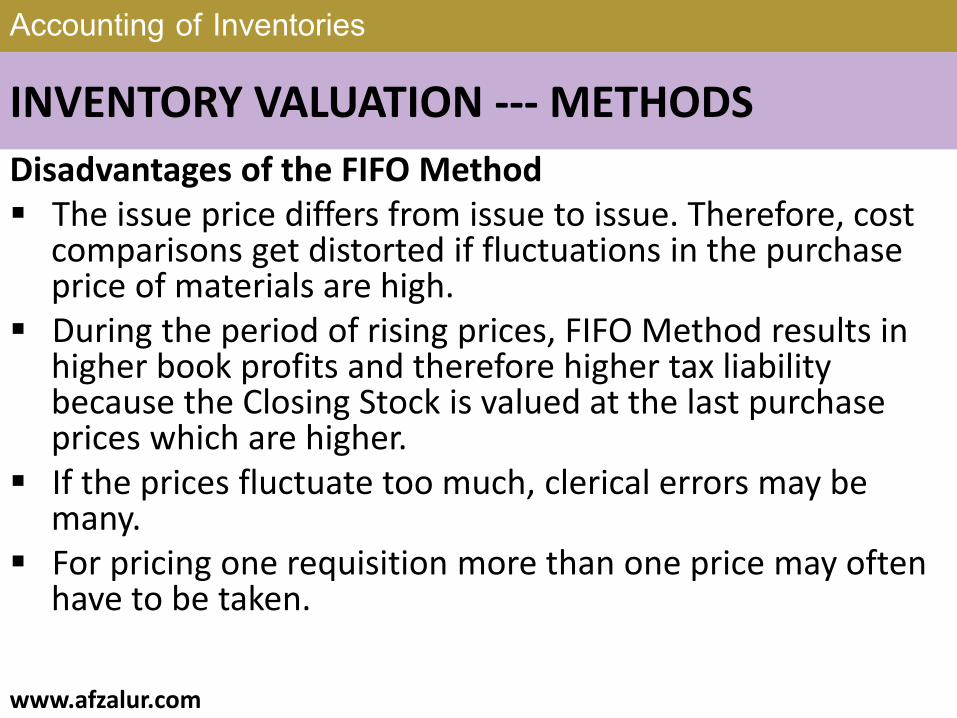

Disadvantages of the FIFO Method The issue price differs from issue to issue. Therefore, cost

comparisons get distorted if fluctuations in the purchase price of materials are high.

During the period of rising prices, FIFO Method results in higher book profits and therefore higher tax liability because the Closing Stock is valued at the last purchase prices which are higher.

If the prices fluctuate too much, clerical errors may be many.

For pricing one requisition more than one price may often have to be taken.

Slide 19 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

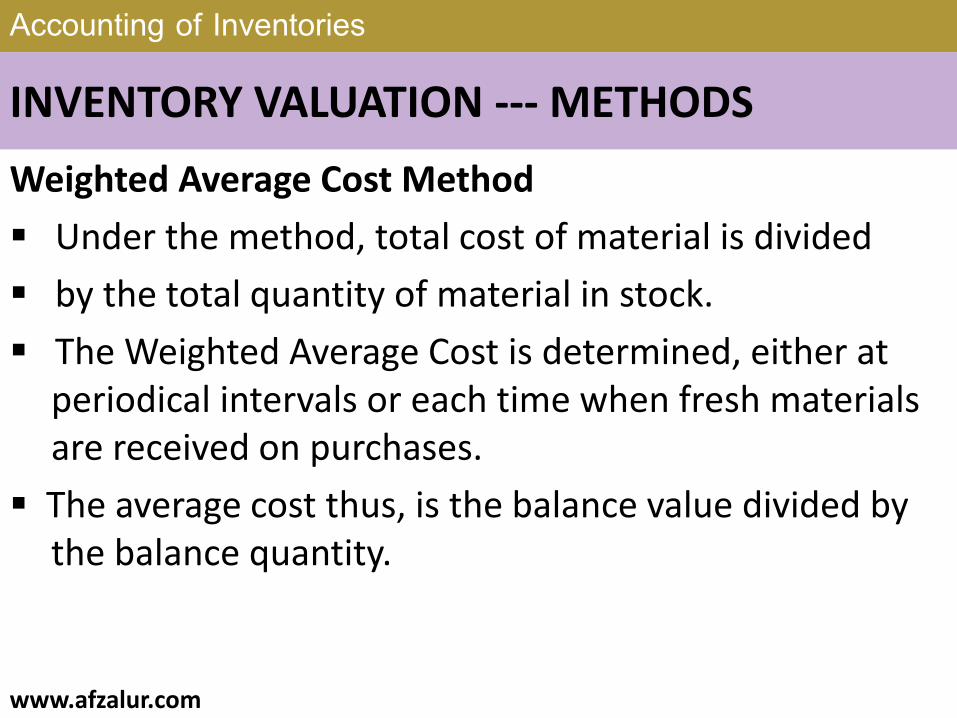

Weighted Average Cost Method

Under the method, total cost of material is divided

by the total quantity of material in stock.

The Weighted Average Cost is determined, either at periodical intervals or each time when fresh materials are received on purchases.

The average cost thus, is the balance value divided by the balance quantity.

Slide 20 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

AS – 2 further permits use of either

Standard Cost Method or

Retail Inventory Method,

if it results in estimating cost of inventory that approximates actual cost.

Slide 21 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Standard Cost Method

It is the predetermined cost based on attainable efficiency standards for a given volume of output.

Slide 22 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Retail Inventory Method.

The method is not based on actual cost but aims at ensuring that the value of inventories being a close approximation to cost.

The method is used by retail stores which has numerous items having small values. It is difficult to keep track of physical flow of goods.

Slide 23 of 48www.afzalur.com

Accounting of Inventories

INVENTORY VALUATION --- METHODS

Thus, a simple method is adopted to value the inventory. But, to make the method effective, near accurate information must be available on retail prices and likely margins.

This method involves three steps

Determining value of end inventory at retail price i.e. price at which they are likely to be sold.

Establishing gross margin based on current year’s data.

Applying the gross margin to retail price of each inventory.

Slide 24 of 48www.afzalur.com

Accounting of Inventories

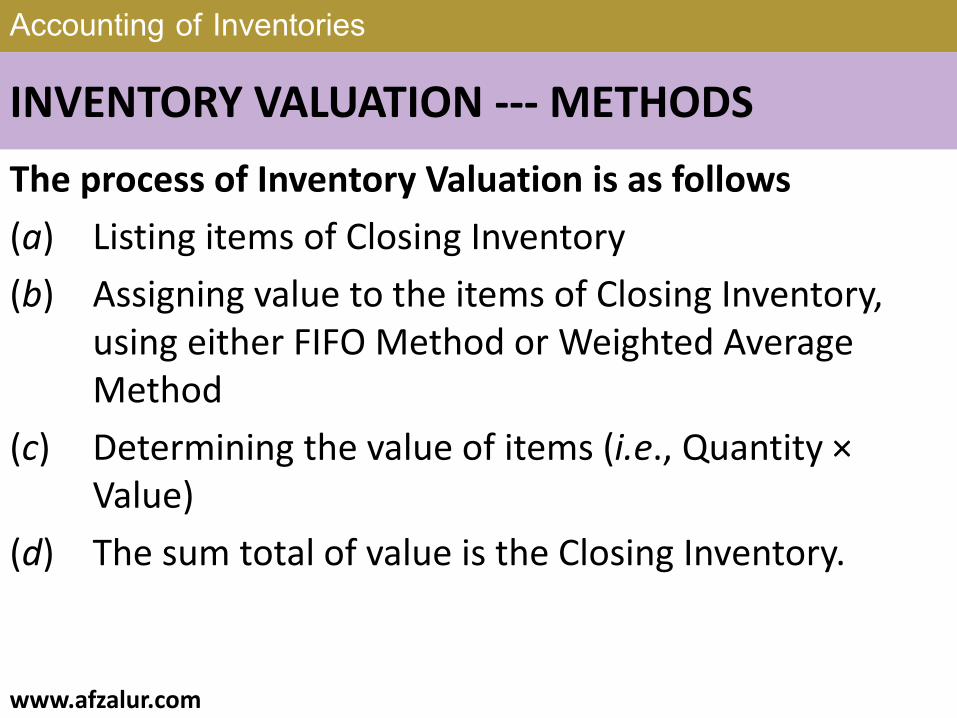

INVENTORY VALUATION --- METHODS

The process of Inventory Valuation is as follows

(a) Listing items of Closing Inventory

(b) Assigning value to the items of Closing Inventory, using either FIFO Method or Weighted Average Method

(c) Determining the value of items (i.e., Quantity ×Value)

(d) The sum total of value is the Closing Inventory.

Slide 25 of 48www.afzalur.com

Accounting of Inventories

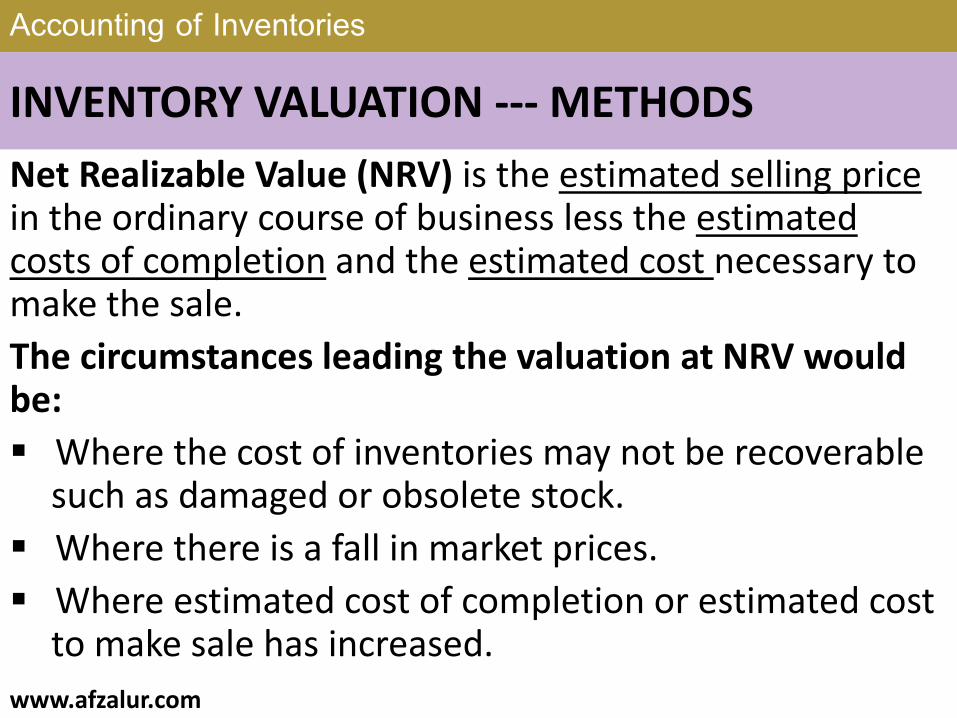

INVENTORY VALUATION --- METHODS

Net Realizable Value (NRV) is the estimated selling pricein the ordinary course of business less the estimated costs of completion and the estimated cost necessary to make the sale.

The circumstances leading the valuation at NRV would be:

Where the cost of inventories may not be recoverable such as damaged or obsolete stock.

Where there is a fall in market prices.

Where estimated cost of completion or estimated cost to make sale has increased.

Slide 26 of 48www.afzalur.com

Accounting of Inventories

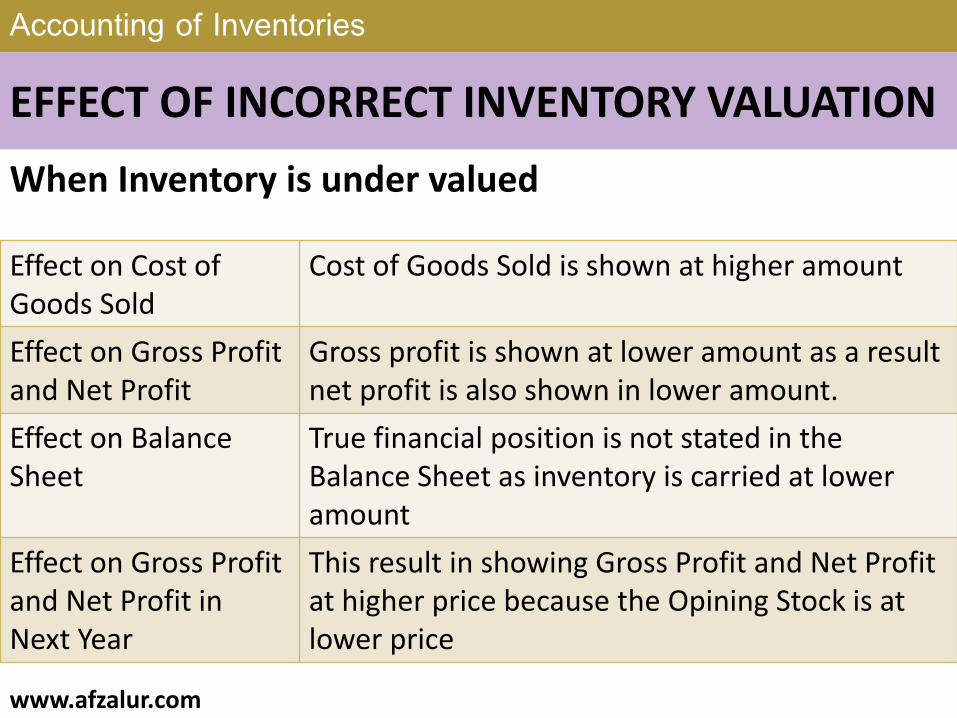

EFFECT OF INCORRECT INVENTORY VALUATION

When Inventory is under valued

Effect on Cost of Goods Sold

Cost of Goods Sold is shown at higher amount

Effect on Gross Profit and Net Profit

Gross profit is shown at lower amount as a result net profit is also shown in lower amount.

Effect on Balance Sheet

True financial position is not stated in the Balance Sheet as inventory is carried at lower amount

Effect on Gross Profit and Net Profit in Next Year

This result in showing Gross Profit and Net Profit at higher price because the Opining Stock is at lower price

Slide 27 of 48www.afzalur.com

Accounting of Inventories

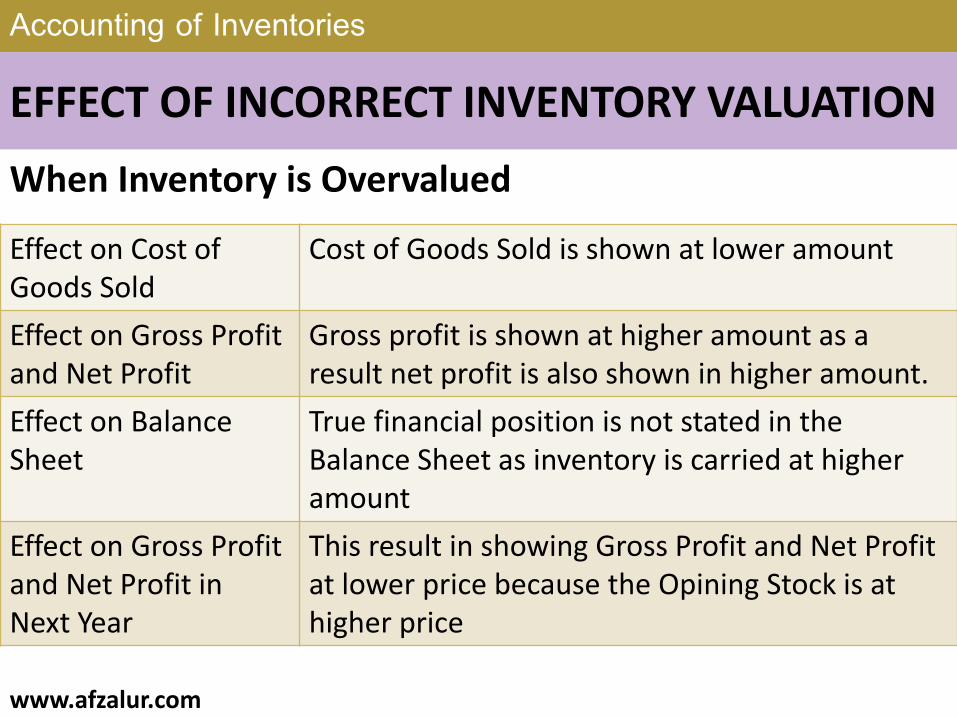

EFFECT OF INCORRECT INVENTORY VALUATION

When Inventory is Overvalued

Effect on Cost of Goods Sold

Cost of Goods Sold is shown at lower amount

Effect on Gross Profit and Net Profit

Gross profit is shown at higher amount as a result net profit is also shown in higher amount.

Effect on Balance Sheet

True financial position is not stated in the Balance Sheet as inventory is carried at higher amount

Effect on Gross Profit and Net Profit in Next Year

This result in showing Gross Profit and Net Profit at lower price because the Opining Stock is at higher price

Slide 28 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Stores (or Material) Records are the records maintained with a purpose to have effective control on materials besides knowing the quantity of material in hand and its location.

Stores Ledger and Bin Cards are two important stores records maintained for inventory.

Apart from them, goods received note, Store Requisition Note, Materials Returned Note and Materials Transfer Note are also important.

Slide 29 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Stores Ledger

Stores Ledger is a record of individual items maintained by the Stores Department

Here receipts and Issues both are recorded in term of quantity

Specimen of Stores Ledger in next slide

Slide 30 of 48www.afzalur.com

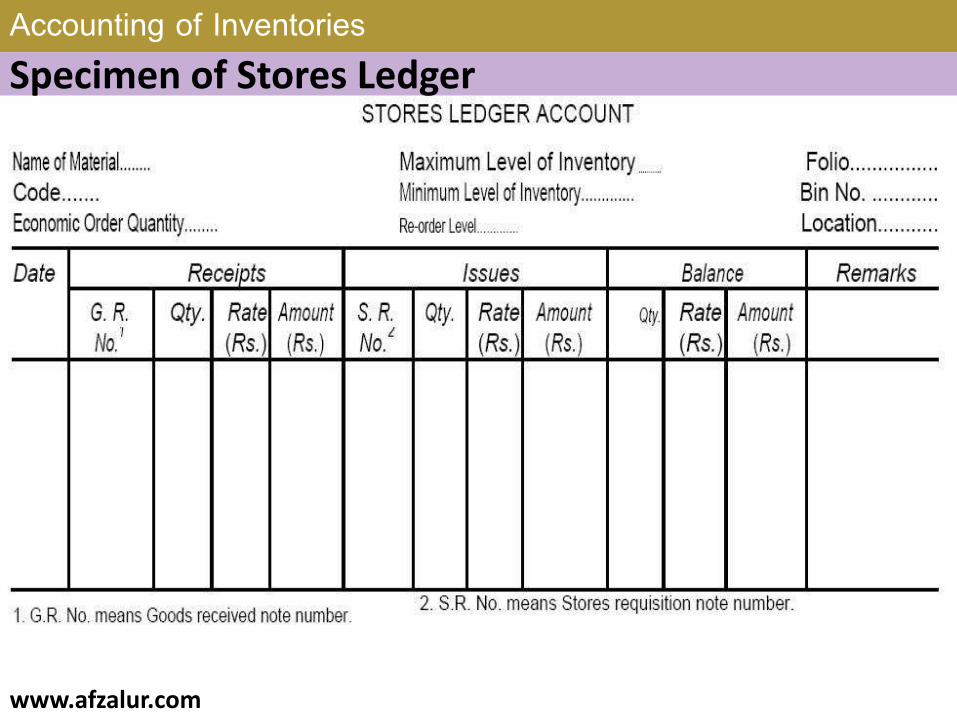

Accounting of InventoriesSpecimen of Stores Ledger

www.afzalur.com Slide 31 of 48

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Bin Card

The term ‘Bin’ refers to the space where the material is stored.

It may be an almirah, rack or an open space.

In addition to the Stores Ledger, a Bin Card is also maintained for each item or material by the Stores Department.

A Bin Card is attached to the bin, where the material is stored.

Slide 32 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

At the time of each receipt or issue an entry is recorded in the Bin Card and the new balance of stock is ascertained.

The entries of receipts and issues of materials are supported by documents such as Goods Received Note, Materials Returned Note, Store Requisition Note, etc.

The Bin Card balance at any time should agree with the physical balance in the bin and also with the balance in Stores Ledger.

Slide 33 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

A Bin Card is a quantitative record of receipts, issues and the balance of materials for individual item of stores;

it also has minimum and maximum quantity levels and the re-ordering quantity.

Slide 34 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

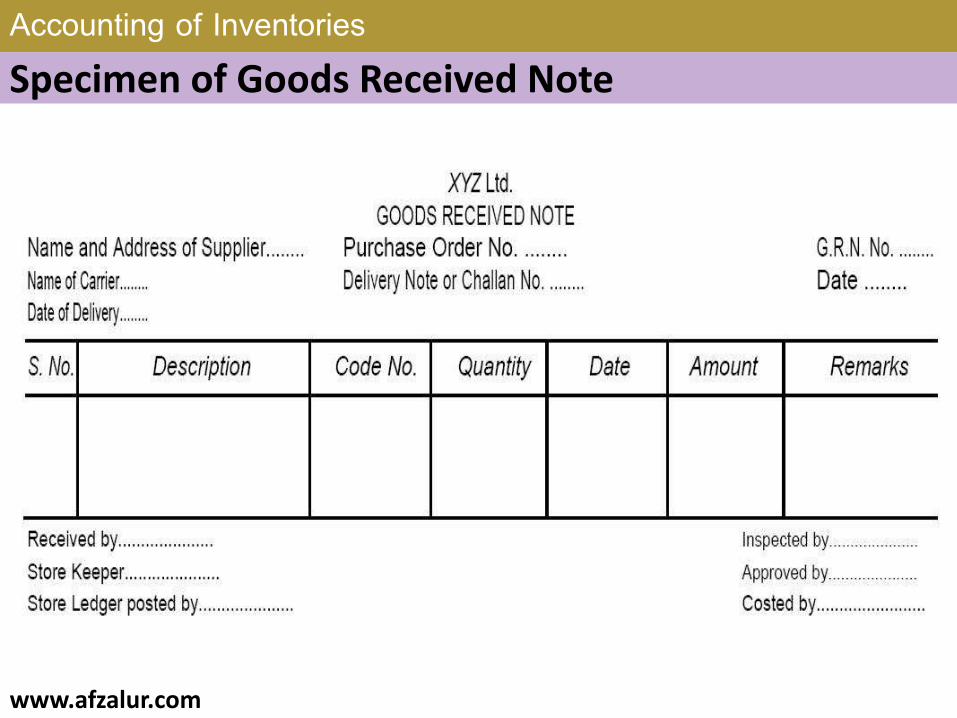

Goods Received Note (GRN) or Materials Received Note (MRN)

Goods Received Note or Materials Received Note is prepared by the Receiving Section of the enterprise.

It prepares the Goods Received Note after verifying that the goods received are in accordance with the Purchase Order, i.e.,

quantity and rate; and quality report approving the goods.

Specimen of Goods Received Note in next slide

Slide 35 of 48www.afzalur.com

Accounting of InventoriesSpecimen of Goods Received Note

www.afzalur.com Slide 36 of 48

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Four copies of the Goods Received Note are prepared and distributed as

One copy is retained by the Receiving Department.

Purchase Department for information regarding the delivery of materials.

Accounts Department for passing supplier’s bills.

Store Department for comparing the type and quantity of materials with the note.

Slide 37 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

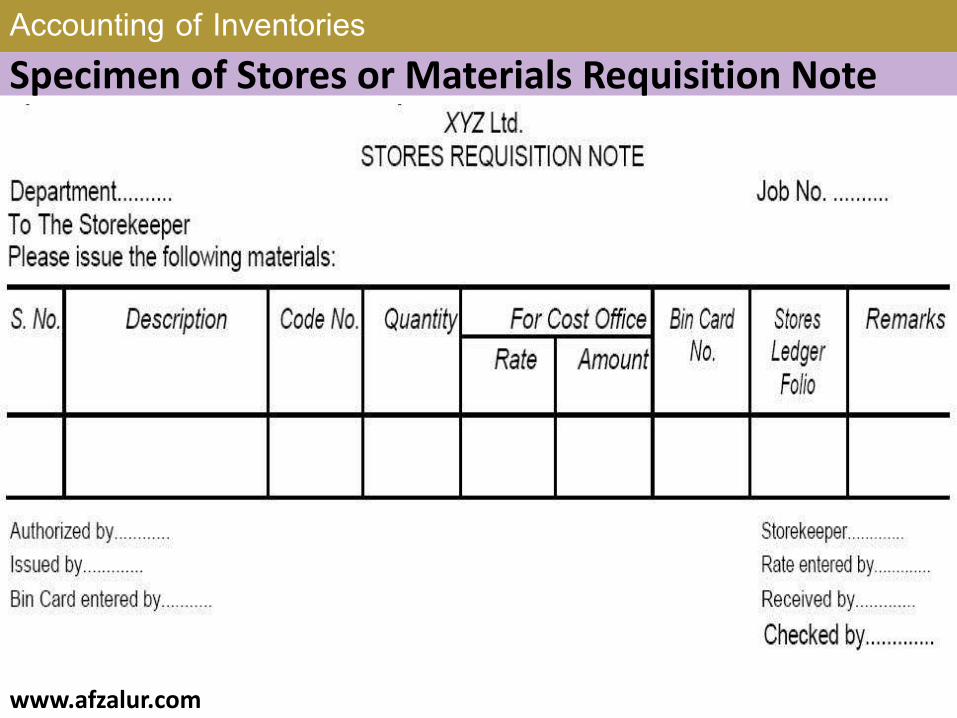

Stores Requisition Note (SRN) Stores Requisition Note is a written requisition for

material by the Production (user) Section to the Storekeeper duly signed by an authorized officer.

The Stores Department issues material to the user section on the basis of Stores Requisition Note.

SRN contains the relevant information such as, the name of the section making the requisition for the material, job for which it is required, Code No. and description of materials required and signature of the authorized officer.

Specimen of Stores or Materials Requisition Note in next slide

Slide 38 of 48www.afzalur.com

Accounting of InventoriesSpecimen of Stores or Materials Requisition Note

www.afzalur.com Slide 39 of 48

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

MRN is prepared in triplicate.

The Storekeeper signs all copies and distributes them as

(i) One copy is returned to the Requisitioning Department together with the issued material. It is a proof with the Receiving Department for material received.

(ii) One copy is sent to the Accounts Department as a basis for debiting the Requisitioning Department.

(iii) One copy is retained by the Storekeeper. This copy is a supporting evidence and authorization for issue of materials.

Slide 40 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Materials Returned Note

The Production Department may get excess materials due to wrong estimate of requirement or any other reasons

Excess materials are returned to the stores along with the Materials Returned Note.

Materials Returned Note contains particulars similar to that of Materials Requisition Note.

Specimen of Materials Returned Note in next slide

Slide 41 of 48www.afzalur.com

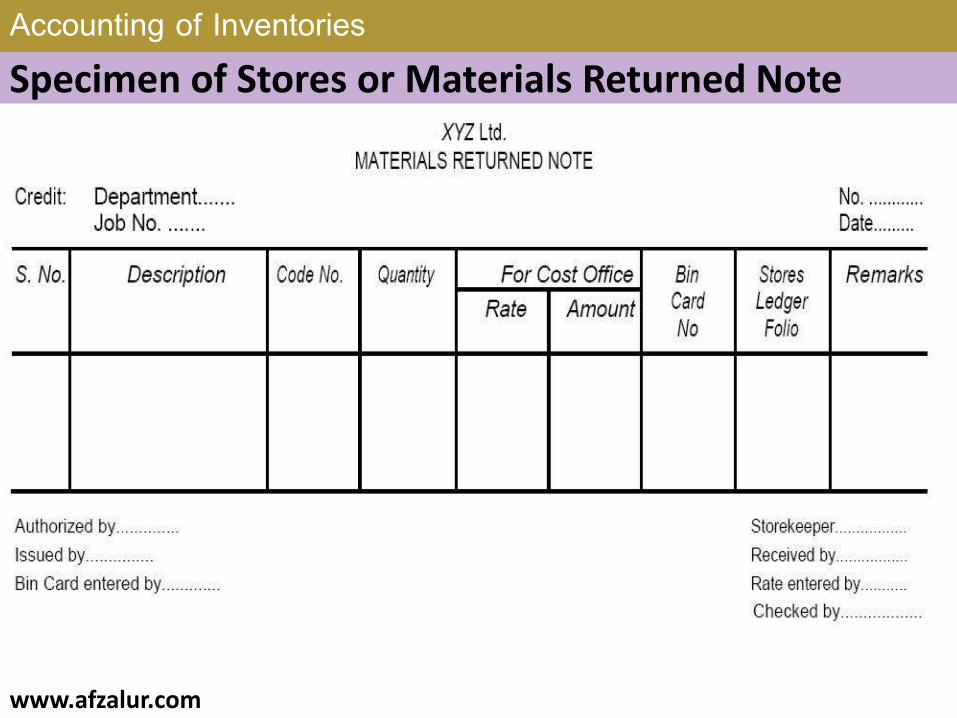

Accounting of InventoriesSpecimen of Stores or Materials Returned Note

www.afzalur.com Slide 42 of 48

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Three copies of the note are prepared and distributed as:

(i) One copy duly signed is returned by the Storekeeper to the Returning Department;

(ii) One copy is sent to the Accounts Department as a basis for giving credit to the Returning Department.

(iii) The third copy is retained by the Storekeeper for completing store records.

Slide 43 of 48www.afzalur.com

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Materials Transfer Note

Materials if transferred from one department (or job) to another department (or job) are transferred by preparing a Materials Transfer Note.

Such transfers take place normally when urgent orders are executed.

Specimen of Materials Transfer Note in next slide

Slide 44 of 48www.afzalur.com

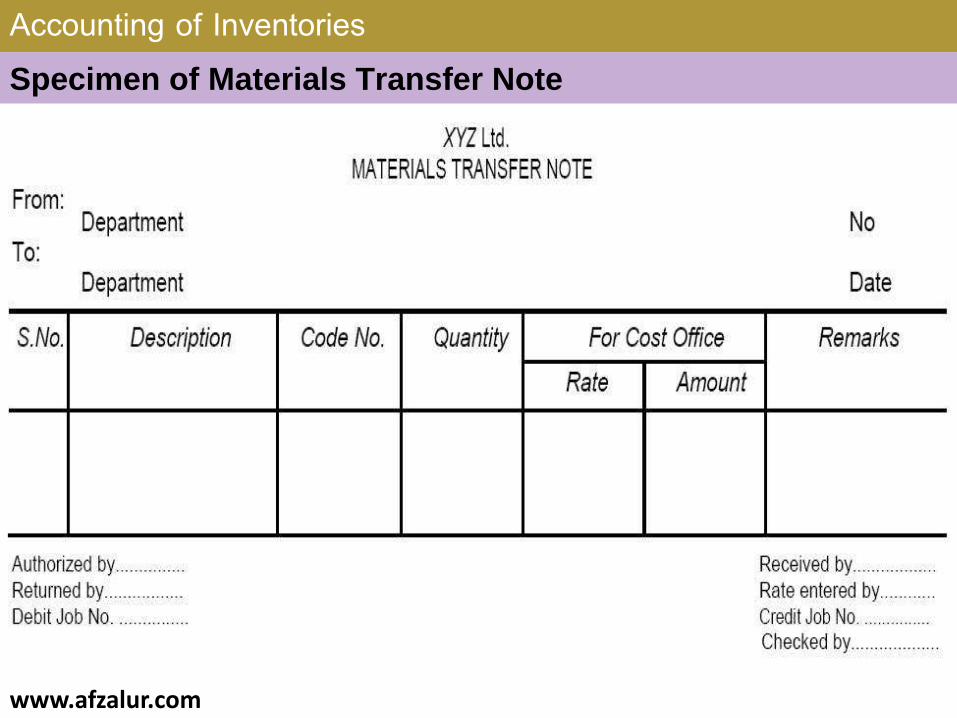

Accounting of InventoriesSpecimen of Materials Transfer Note

www.afzalur.com Slide 45 of 48

Accounting of Inventories

STORES (OR MATERIAL) RECORDS

Materials Transfer Note is prepared in triplicate by the Transferring Department giving complete details of materials transferred. It is distributed as

One copy is retained by the Transferring Department.

A copy is sent along with the goods to the department to which goods are sent;

Third copy is sent to Accounts Department on the basis of which Transferring Department/job is credited and Transferee department/job is debited.

Storekeeper does not record the transfer of materials in the store records.

Slide 46 of 48www.afzalur.com

Accounting of InventoriesVALUATION OF INVENTORY AND PREPARATION OF TRADING ACCOUNT Accounting for inventory involves valuation of materials

received (Incoming Materials) and materials issued (Outgoing Materials).

Valuation of Materials Received or Purchased (Incoming Materials): The materials received are valued at invoice price plus expenses incurred for bringing the materials to the stores. These expenses include—(a) freight and duty, (b) insurance and storage costs, (c) cost of containers and (d) sales tax, etc.

Valuation of Materials Issued (Outgoing Materials): Materials are issued for different jobs or work orders from the stores. These jobs or work orders are charged with the value of materials issued to them.

Slide 47 of 48www.afzalur.com

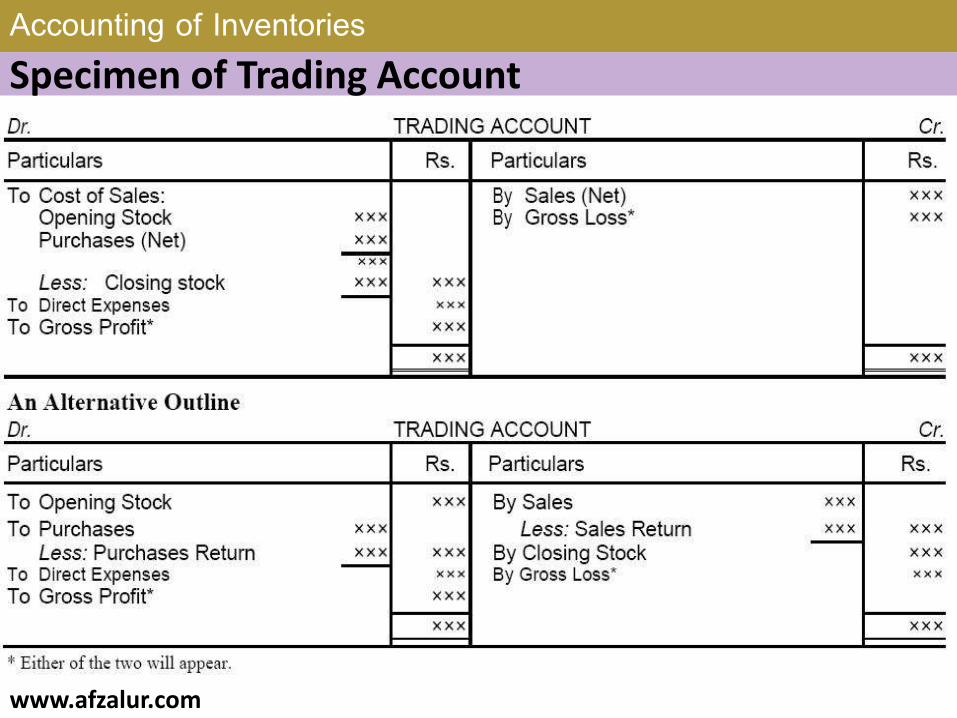

Accounting of InventoriesVALUATION OF INVENTORY AND PREPARATION OF TRADING ACCOUNTPreparation of Trading Account when FIFO Method is followed

Trading Account is an account that determines the gross profit or gross loss. It is debited with Cost of Goods Sold (Opening Stock + Purchases (Net of Returns) + Direct Expenses – Closing Stock) and credited it with the amount of Sales (Net of Returns).

Specimen of Trading Account in next slide

Slide 48 of 48www.afzalur.com

Accounting of InventoriesSpecimen of Trading Account

www.afzalur.com Slide 49 of 48

Accounting of Inventories

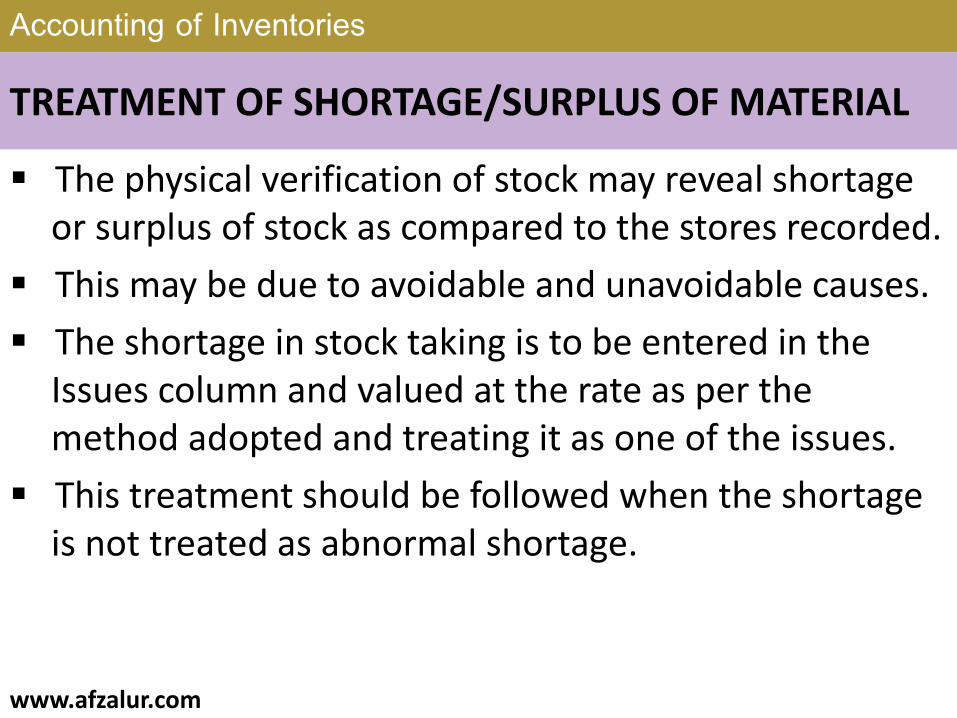

TREATMENT OF SHORTAGE/SURPLUS OF MATERIAL

The physical verification of stock may reveal shortage or surplus of stock as compared to the stores recorded.

This may be due to avoidable and unavoidable causes.

The shortage in stock taking is to be entered in the Issues column and valued at the rate as per the method adopted and treating it as one of the issues.

This treatment should be followed when the shortage is not treated as abnormal shortage.

Slide 50 of 48www.afzalur.com

Accounting of Inventories

TREATMENT OF SHORTAGE/SURPLUS OF MATERIAL

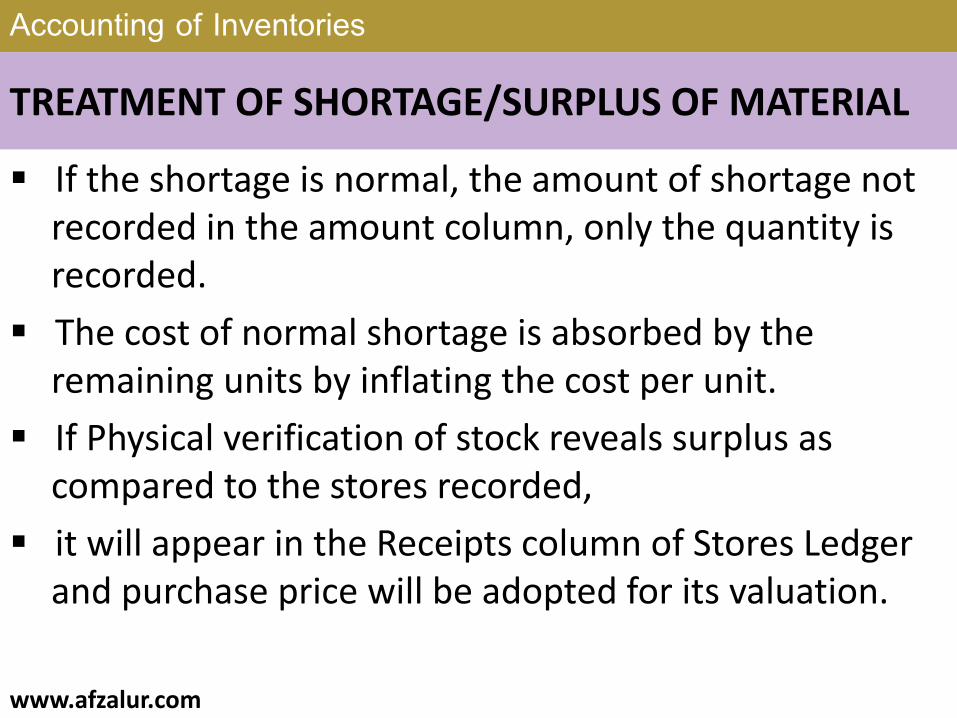

If the shortage is normal, the amount of shortage not recorded in the amount column, only the quantity is recorded.

The cost of normal shortage is absorbed by the remaining units by inflating the cost per unit.

If Physical verification of stock reveals surplus as compared to the stores recorded,

it will appear in the Receipts column of Stores Ledger and purchase price will be adopted for its valuation.

Slide 51 of 48www.afzalur.com

Accounting of Inventories

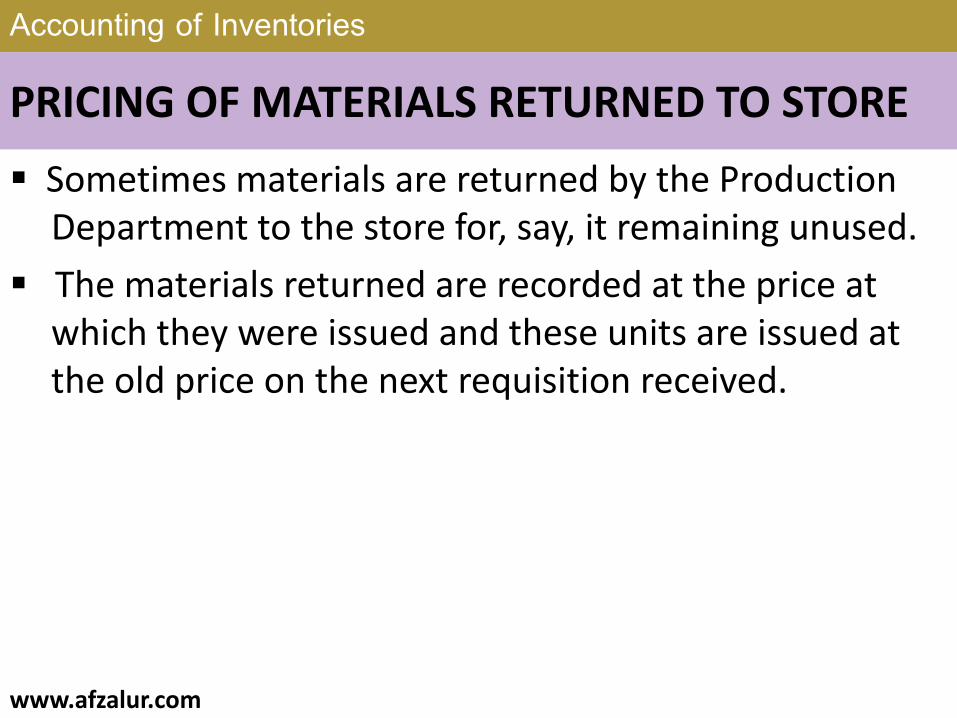

PRICING OF MATERIALS RETURNED TO STORE

Sometimes materials are returned by the Production Department to the store for, say, it remaining unused.

The materials returned are recorded at the price at which they were issued and these units are issued at the old price on the next requisition received.

Slide 52 of 48www.afzalur.com

Accounting of Inventories

PRICING OF MATERIALS RETURNED TO VENDOR

Sometimes materials received do not conform to specifications and they are returned to vendor.

If the material has not yet been issued, it is credited to stores ledger at its purchase price and no other adjustment is necessary.

Slide 53 of 48www.afzalur.com

Accounting of Inventories

www.afzalur.com

Slide 54 of 48www.afzalur.com