ACCOUNTING FOR PARTNERSHIPS

23

INTERMEDIATE ACCOUNTING Partnership Accounts By Juma Bananuka Makerere University Business School Department Of Accounting [email protected]

-

Upload

juma-bananuka -

Category

Business

-

view

169 -

download

0

Transcript of ACCOUNTING FOR PARTNERSHIPS

INTERMEDIATE ACCOUNTING

Partnership Accounts By

Juma BananukaMakerere University Business School

Department Of Accounting

DEFINITION OF PARTNERSHIP

A partnership is an agreement between two or

more people who enter into business with a

view of earning profits. A partnership includes at

least two individuals (partners). In certain

jurisdictions, there may be an upper limit to the

number of partners.

Definition continued………..

It is a relationship between persons competent

of entering into a contract or an agreement

according to their own management or

dictation by law. Partnerships may be

established formally by means of a partnership

agreement / deed or a partnership may be

presumed to exist from the actions of

individuals.

Contents of a partnership deed

A partnership agreement / deed is a written agreement in which partners among others set out the terms of the partnership.

The contents of the partnership include the following;

The names of the partners

Capital to be contributed by each partner

Interest on capital if any

Drawings to be made by the partners

Contents of a partnership deed

cont………..

Interest on drawings if any

Salaries to be paid to active partners

Nature and kind of business

Contractual duties of the partners

Valuation of goodwill in case of changes in the partnership

Preparation and auditing of accounts

Procedure of admission and retirement of partners

Duration of the partnership business

Advantages of Partnership

Partnerships are relatively easy to establish.

The ability to raise funds is increased, either because two or

more partners may be able to contribute more funds and/or

their borrowing capacity may be greater.

Benefit from the combination of complementary skills of two or

more people. There is a wider pool of knowledge, skills and

contacts.

Partnerships can be cost-effective as each partner specializes

in certain aspects of the business.

Advantages continued…….

Business can be easily expanded since new partners can beadmitted and there is a pool of talent to draw from to supportbusiness growth.

Partnerships provide moral support and may allow for morecreative brainstorming.

In case of difficulties, discussions among partners are likely toyield solutions.

Losses and liabilities are shared, hence reducing on theburden placed on an individual.

Proper accounting and other systems.

Disadvantages of partnership

Partners are jointly and individually liable for the

actions of the other partners. If one partner makes a

mistake all the others partners will be affected.

Profits must be shared with others, hence reducing

the potential amount receivable by an individual.

Partners may have difficulties in deciding on how

they value each other’s time and skills. Partners with

better skills and more hardworking may not be

appropriately rewarded for their input in the business.

Disadvantages cont……………..

Since decisions are shared, disagreements can occur

hence slowing down the decision making process.

The partnership may have a limited life; it may end

upon the withdrawal, death or bankruptcy of a

partner.

A major disadvantage of a partnership is unlimited

liability. General partners are liable without limit for all

debts contracted and errors made by the

partnership.

Characteristics of partnerships

Association of two or more persons: Partnership is formed by the

association of two or more persons. However, the maximum number of

partners cannot exceed ten in case banking business and twenty in

case of other business, otherwise it will be illegal.

Contractual relationship: Partnership arises from contract as the partners

enter into agreement to carry on a business. The contract may be oral

or written. To become a partner must be of the age of majority and is of

sound mind. A minor cannot be a partner but can admitted to the

partnership for benefits only with the consent of all the partners.

Characteristics continued……..

Existence of lawful business: Partnership is formed for the purpose of

carrying on lawful business only. The term business is very wide and

includes every trade, occupation or profession. But when the purpose is

to do some charitable work or to share the income of property held in

joint ownership, it will not constitute partnership.

Sharing of profits on agreed basis: Sharing of profits is one of the essential

characteristics of partnership. The partners share the profits as per

agreement. This implies at the partnership must have the motive to earn

profit. Therefore, business carried on with philanthropic motive or only

one partner entitled to the entire profit of the business shall 3t be

considered as a partnership.

Characteristics continued………

Principal-agent relationship: In partnership, there is existence of

principal-agent relationship. Every partner is entitled to take part in the

management of the business. When one or few partners do manage

the business they represent the firm and other partners. As gents, they

can bind the firm and the other partners for their action in the ordinary

course of business. The principal-agent relationship is a real test of the

existence of partnership.

Unlimited liability: The liability of the partners is unlimited. This implies that

the private properties of the partners are at risk as these can be used to

meet the obligations of tie firm when the assets of the firm are not

sufficient for the purpose. Each partner is jointly id severally liable for the

debts and obligations of the business.

Characteristics continued………….

Restriction on transfer of shares: A partner cannot transfer his

share in the business an outsider without the consent of all

other partners. When there is transfer of share, a new

partnership comes into existence even though the same

business is continued. Every addition pr deletion of a partner

changes the entire partnership deed.

Utmost good faith: There is mutual trust and confidence

among the partners. Therefore, every partner must be just

and faithful to one another render true and proper accounts

and provide full information concerning the business.

Partnership concepts

Capital –is the amount of money required to start partnership business. it

is contributed by every partner according to the deed

Profit and loss sharing ratios –it states how each partner should share in

profit or loss i.e. proportion of profit or loss a partner takes

Interest on capital –this guaranteed on partners capital contributed i.e.

on capital, a partner contributes him or she has to get interest.

Interest on drawings - is charged on the amount withdrawn by a

partner for private use. This is charged to deter partners from

withdrawing money any how (not to steal)

Salaries – a salary is paid to an active partner who takes daily work.

Types of partners

Sleeping / dormant partner

Is one who does not actively participate in partnership activities.

A dormant partner shares profits and has a right to access all

the partnership books of accounts and is liable to third parties

who deal with him on behalf of the partnership.

Nominal partner

Is a person whose name is used as if he or she was a member of

the firm, but in actual sense is not a partner. He is liable to third

parties who give credit to the firm on the strength of his being a

partner.

Types continued…..

Minor

A person who is under the age of majority according to the law to which

he or she is subject may be admitted to the benefits of partnership but

cannot be made personally liable for any obligation of the firm; but the

share of that minor in the property of the firm is liable for the obligation of

the firm. A person who has been admitted to the benefits of partnership

under the age of majority becomes, on attaining that age, liable for all

obligations incurred by the partnership since he or she was so admitted,

unless he or she gives public notice within a reasonable time of his or her

repudiation of the partnership.

Types cont……

Sub partners

Is one who gets a share of profits through one of the partners. Is

not liable against the firm and is not liable to third parties of the

firm.

Partners in profits only

Is one who shares profits only and does not share losses.

THE DOUBLE ENTRY SYSTEM UNDER PARTNERSHIP

In case of capital contribution

Dr Cash / Bank A/C

Cr Capital A/C

When partners are entitled to interest on capital

Dr Profit & loss appropriation A/C

Cr Current / Capital A/C

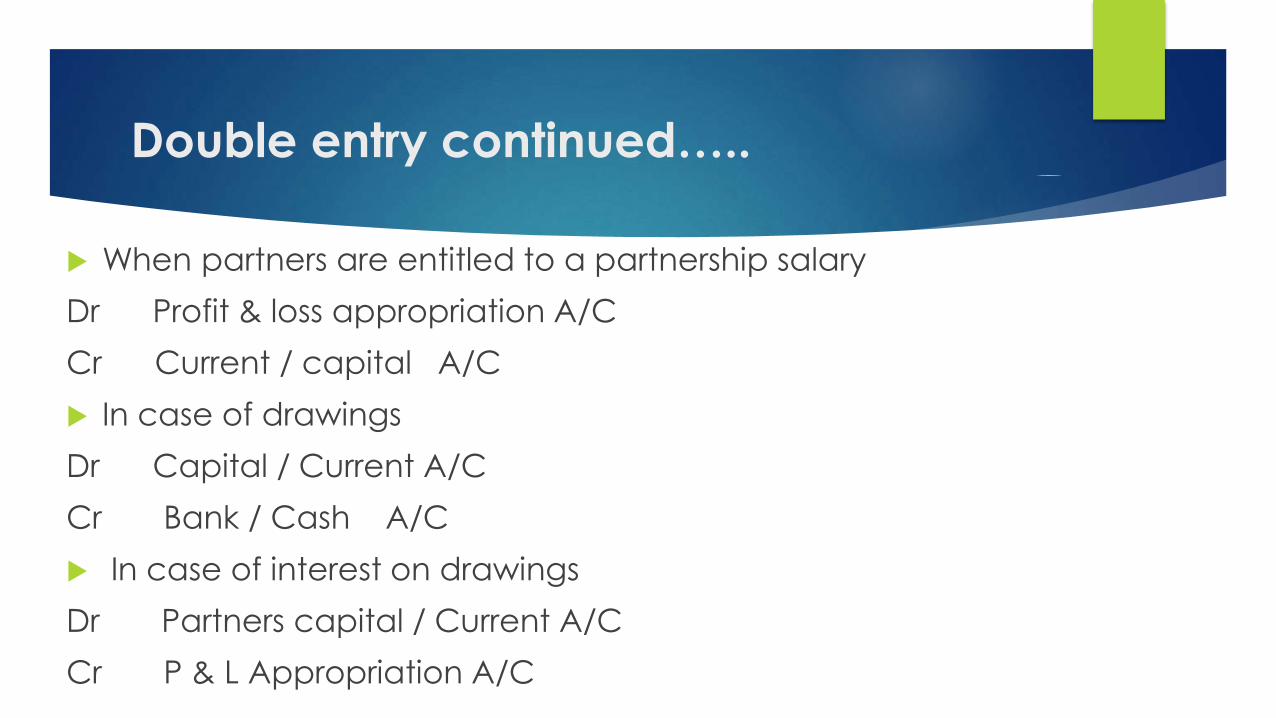

Double entry continued…..

When partners are entitled to a partnership salary

Dr Profit & loss appropriation A/C

Cr Current / capital A/C

In case of drawings

Dr Capital / Current A/C

Cr Bank / Cash A/C

In case of interest on drawings

Dr Partners capital / Current A/C

Cr P & L Appropriation A/C

Double entry continued…..

In case of sharing profits

Dr P & L Appropriation A/C

Cr Current / Capital A/C

In case of a loss,

Dr Partners capital / Current A/C’s

Cr P & L Appropriations A/C

Note

Interest on a loan is a business expense and treated asbusiness expenses in the profit and loss account.

If a partnership gives out a loan in return for interest, theinterest received is treated as miscellaneous income.

If a partner extends a loan to the partnership, interestcharges on the loan is a business expense and chargedagainst the profits.

The place to be