Accounting & Financial Analysis 1 Lecture 2 Specialised journals General journal Specialised...

27

Accounting & Financial Analysis 1 Lecture 2 Specialised journals General journal

-

Upload

basil-samson-thompson -

Category

Documents

-

view

219 -

download

2

Transcript of Accounting & Financial Analysis 1 Lecture 2 Specialised journals General journal Specialised...

Accounting & Financial

Analysis 1

Lecture 2

Specialised journals

General journal

JournalsJournals

All information relating to the transactions of a company are processed through journals into the general ledger.

There are two types of journals :

1. Specialist journals (Subsidiary books, day books)

2. General journal

All information relating to the transactions of a company are processed through journals into the general ledger.

There are two types of journals :

1. Specialist journals (Subsidiary books, day books)

2. General journal

What is a specialist journal? What is a specialist journal?

Limited function nowadays, due to modern computer accounting systems

A chronological summary of similar transactions that occur regularly, recorded in a day book with the column totals summarised and posted to the general ledger at the end of a specified period usually 1 month.

Limited function nowadays, due to modern computer accounting systems

A chronological summary of similar transactions that occur regularly, recorded in a day book with the column totals summarised and posted to the general ledger at the end of a specified period usually 1 month.

7 Specialist Journals7 Specialist Journals

There are seven specialist journal books:1. Sales journal (Day book which records all the credit sales)2. Sales returns journal (Day book which records credit sale

returns)3. Purchases journal (Day book which records credit

purchases of stock)4. Purchase returns journal (Day book which records the

returns of stock purchased on credit)5. Cash receipts journal (Day book which records all cash

receipts)6. Cash payments journal (Day book which records all cash

payments)7. Petty cash journal (Day book which records all petty cash

payments and the receipt of replenishment)

There are seven specialist journal books:1. Sales journal (Day book which records all the credit sales)2. Sales returns journal (Day book which records credit sale

returns)3. Purchases journal (Day book which records credit

purchases of stock)4. Purchase returns journal (Day book which records the

returns of stock purchased on credit)5. Cash receipts journal (Day book which records all cash

receipts)6. Cash payments journal (Day book which records all cash

payments)7. Petty cash journal (Day book which records all petty cash

payments and the receipt of replenishment)

General Journal General Journal

The general journal is the subsidiary book in which we record the details of any transaction that cannot be recorded in any other subsidiary book. (Specialist journals)

The general journal is the subsidiary book in which we record the details of any transaction that cannot be recorded in any other subsidiary book. (Specialist journals)

General Journal - 2General Journal - 2

It has the following characteristics:1. Provides a record of details in date

order2. Indicates the general ledger

accounts to be debited or credited.3. Indicates the $ amount to be

processed to each general ledger account.

4. Gives the reason for the transaction being processed.

It has the following characteristics:1. Provides a record of details in date

order2. Indicates the general ledger

accounts to be debited or credited.3. Indicates the $ amount to be

processed to each general ledger account.

4. Gives the reason for the transaction being processed.

General Journal - 3General Journal - 3

The general journal is generally used to process transactions/activities that are not recorded in any of the specialised journals.

The general journal is generally used to process transactions/activities that are not recorded in any of the specialised journals.

General Journal - 4General Journal - 4

These transactions generally relate to the following activities:

1. Start-up business entries2. Correction of posting errors3. End of month entries: depreciation charge,

bank interest & charges, provision for bad debts, bad debts write-off etc.

4. Accrual of expenses5. Adjustments for prepayments6. Purchase of fixed assets on credit7. Adjustment entries on sale of assets8. Contra entries, inter-account transfers

These transactions generally relate to the following activities:

1. Start-up business entries2. Correction of posting errors3. End of month entries: depreciation charge,

bank interest & charges, provision for bad debts, bad debts write-off etc.

4. Accrual of expenses5. Adjustments for prepayments6. Purchase of fixed assets on credit7. Adjustment entries on sale of assets8. Contra entries, inter-account transfers

JOURNALS ARE BOOKS JOURNALS ARE BOOKS

Each journal is a separate ledger book with analysis columns (up to 25 columns, each column for a separate account with the last column for any uncommonly used accounts). The first column is for the total $ value of the transaction.

Each journal is a separate ledger book with analysis columns (up to 25 columns, each column for a separate account with the last column for any uncommonly used accounts). The first column is for the total $ value of the transaction.

JOURNAL EXAMPLESJOURNAL EXAMPLES

Sales (Credit Sales/Trade Debtors) Sales returns (Credit Sales returns) Purchases (Credit Purchases/Trade

Creditors Purchases returns (Credit Purchase

returns) Cash receipts Cash payments Petty cash General journal.

Sales (Credit Sales/Trade Debtors) Sales returns (Credit Sales returns) Purchases (Credit Purchases/Trade

Creditors Purchases returns (Credit Purchase

returns) Cash receipts Cash payments Petty cash General journal.

Credit terms Credit terms

Credit terms is the agreement made with the customers which specifies the time in which the account has to be paid, and sometimes

the discount allowed if the account is paid earlier.

Every business tries to collect the money owing as quickly as possible as this will help the business cash flow.

In order to get the trade debtors (accounts receivable) to pay their account quicker a discount may be offered for quick settlement.

The discount could be 3% if paid within 10 days, if not, the full amount within 30 days. The discount will be documented as follows: Terms

3/10, net 30.

Credit terms is the agreement made with the customers which specifies the time in which the account has to be paid, and sometimes

the discount allowed if the account is paid earlier.

Every business tries to collect the money owing as quickly as possible as this will help the business cash flow.

In order to get the trade debtors (accounts receivable) to pay their account quicker a discount may be offered for quick settlement.

The discount could be 3% if paid within 10 days, if not, the full amount within 30 days. The discount will be documented as follows: Terms

3/10, net 30.

Credit terms - 2Credit terms - 2

For accounting purposes Discount allowed = Debit entry Discount received = Credit entry

For accounting purposes Discount allowed = Debit entry Discount received = Credit entry

The sales returns journal – see attachment 1

The sales returns journal – see attachment 1

The sales returns journal is the subsidiary day book which records all the RETURNED CREDIT SALES (of trading stock) that have taken place during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

The sales returns journal is the subsidiary day book which records all the RETURNED CREDIT SALES (of trading stock) that have taken place during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

Example: Sales returns journal

Example: Sales returns journal

Date Description Credit.Note Value GST Total

5/7/07 Goods sold on credit returned by Tuan

15 $40 $4 $44

12/7/07 Goods sold on credit returned by Barath

16 $30 $3 $33

TOTAL $70 $7 $77

Purchase journal – see attachment 1

Purchase journal – see attachment 1

The purchase journal is the subsidiary day book which records all the CREDIT PURCHASES (of trading stock) that have taken place each day during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

Purchases of other items such as office computer is not recorded in the purchases journal only trading stock (for resale) purchased on credit is recorded in the purchases journal.

The purchase journal is the subsidiary day book which records all the CREDIT PURCHASES (of trading stock) that have taken place each day during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

Purchases of other items such as office computer is not recorded in the purchases journal only trading stock (for resale) purchased on credit is recorded in the purchases journal.

Example: Purchases journalExample: Purchases journal

Date Description Inv.No. Value GST Total 4/2/07 Purchased goods on credit from

Supplies Ltd 2356 $1,420 $142 $1,562

10/2/07 Purchased goods on credit from Co-Op Ltd

4257 $2,420 $242 $2,662

12/2/07 Purchased goods on credit from Easton Ltd

1258 $860 $86 $946

18/2/07 Purchased goods on credit from Uncle Toby

687 $440 $44 $484

Total $5,140 $514 $5,654

The purchases returns journal – see attachment 1

The purchases returns journal – see attachment 1

The purchases returns journal is the subsidiary day book which records all the RETURNED CREDIT PURCHASES (of trading stock) that have taken place during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

The purchases returns journal is the subsidiary day book which records all the RETURNED CREDIT PURCHASES (of trading stock) that have taken place during the month.

At the end of the month the columns are totalled (added up) and ONLY the total of each column is posted to the General Ledger.

Example: Purchases returns journal

Example: Purchases returns journal

Date Description Credit.Note

Value GST Total

14/2/07 Purchases returned to Co-Op Ltd

246 $180 $18 $198

20/2/07 Purchases returned to Easton Ltd

316 $80 $8 $88

Total $260 $26 $286

The Cash Payments and receipts journals – see attachment 2

The Cash Payments and receipts journals – see attachment 2

The cash journals (payments and receipts) are the journals into which we record all the cash transactions that take place during the month.

All cash receipts are recorded in the CASH RECEIPTS JOURNAL and

All cash payments are recorded in the CASH PAYMENTS JOURNAL.

The cash journals (payments and receipts) are the journals into which we record all the cash transactions that take place during the month.

All cash receipts are recorded in the CASH RECEIPTS JOURNAL and

All cash payments are recorded in the CASH PAYMENTS JOURNAL.

The cash payments journalThe cash payments journal

A business will have various cash payments to record during the month, some of which will be the payment of wages, rent, telephone, electricity, purchase of goods for cash, payments to trade creditors, GST payments etc. etc.

Each one of these payments will be recorded in the cash payments journal and

at the end of each month the columns will be totalled (added up) and ONLY the total of each expense account will be posted to the General Ledger.

The sundry column will be used to record all the payments for which there is no specific column.

A business will have various cash payments to record during the month, some of which will be the payment of wages, rent, telephone, electricity, purchase of goods for cash, payments to trade creditors, GST payments etc. etc.

Each one of these payments will be recorded in the cash payments journal and

at the end of each month the columns will be totalled (added up) and ONLY the total of each expense account will be posted to the General Ledger.

The sundry column will be used to record all the payments for which there is no specific column.

Example: Cash Payments Journal

Example: Cash Payments Journal

Debit Credit Date Details Chq.

No. Dis. Rec.

Creditors

Cash Purchases

Inp Tax Cr

Wages Sundry Bank

4/2 Wages 46 $1,800 $1,800 6/2 Trade Creditors -

Co-Op Ltd 47 $1,500 $1,500

8/2 Cash purchase 48 $1,200 $120 $1,320 10/2 Rent 49 $90 $900 $990 12/2 Wages 50 $1,880 $1,880 16/2 Trade Creditors

– Easton Ltd 51 $600 $600

18/2 Cash purchase 52 $860 $86 $946 20/2 Insurance – M.V. $40 $400 $440

Total $2,100 $2,060 $336 $3,680 $1300 $9,476

Use of Cash Payments Journal

Use of Cash Payments Journal

Therefore if we want to confirm that an expense has been paid by the business we would have to refer to the Cash Payments Journal for detail of all payments.

Therefore if we want to confirm that an expense has been paid by the business we would have to refer to the Cash Payments Journal for detail of all payments.

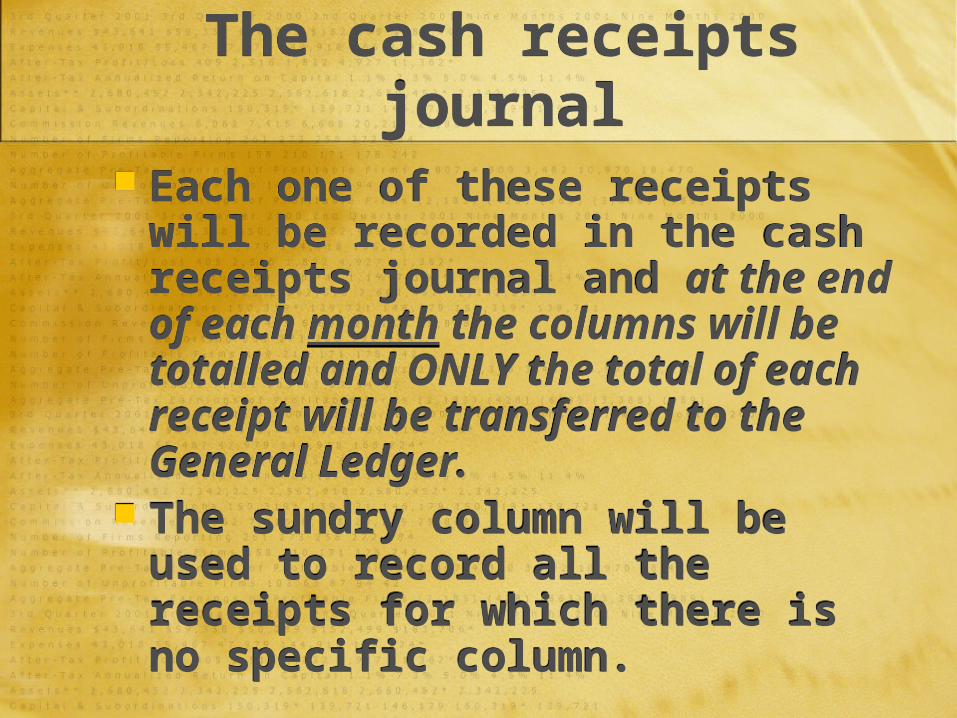

The cash receipts journalThe cash receipts journal

A business will have various cash receipts to record during the month, most of which will be receipts from

trade debtors (accounts receivable), and cash sales, GST payments etc. Each one of these receipts will be recorded in

the cash receipts journal and at the end of each month the columns will be totalled and ONLY the total of each receipt will be transferred to the General Ledger. The sundry column will be used to record all the receipts for which there is no specific column.

A business will have various cash receipts to record during the month, most of which will be receipts from

trade debtors (accounts receivable), and cash sales, GST payments etc. Each one of these receipts will be recorded in

the cash receipts journal and at the end of each month the columns will be totalled and ONLY the total of each receipt will be transferred to the General Ledger. The sundry column will be used to record all the receipts for which there is no specific column.

The cash receipts journalThe cash receipts journal

Each one of these receipts will be recorded in the cash receipts journal and at the end of each month the columns will be totalled and ONLY the total of each receipt will be transferred to the General Ledger.

The sundry column will be used to record all the receipts for which there is no specific column.

Each one of these receipts will be recorded in the cash receipts journal and at the end of each month the columns will be totalled and ONLY the total of each receipt will be transferred to the General Ledger.

The sundry column will be used to record all the receipts for which there is no specific column.

Example: Cash Receipts Journal

Example: Cash Receipts Journal

Credit Debit Date Details Inv.

No. GST Adj

Dis. Exp.

Debtors Cash Sales

GST Pay

Rent Sundry Bank

4/2 Cash sale $250 $25 $275 6/2 Trade Debtor –

John Smith $583 $583

8/2 Cash sale $90 $9 $99 10/2 Rent $60 $600 $660 12/2 Trade Debtor –

Monica Borg $715 $715

16/2 Cash sale $760 $76 $836 18/2 Commission $6 $60 $66 20/2

Total $1,298 $1,100 $176 $600 $60 $3,234

Cash Receipts Journal -2 Cash Receipts Journal -2

Therefore if we want to confirm receipt of income we would have to refer to the Cash Receipts Journal for detail of all receipts.

Example: If a debtor (credit sales) claims to have paid an account we would have to check the Cash Receipts Journal to see if the payment is recorded.

Therefore if we want to confirm receipt of income we would have to refer to the Cash Receipts Journal for detail of all receipts.

Example: If a debtor (credit sales) claims to have paid an account we would have to check the Cash Receipts Journal to see if the payment is recorded.

Have a go!Have a go!

CLASS EXERCISE 2 At the back of your handouts

CLASS EXERCISE 2 At the back of your handouts

![celasin ( Cumhuriyet...Dayang Journal System (DJS) Digital Journals Database Directory of Acadonic Resources Directory Of Research Journal Indexing (DRJI) DOA] Index Electronic Journals](https://static.fdocuments.us/doc/165x107/5e18b7fdd61f2c13c66695c0/celasin-cumhuriyetdayang-journal-system-djs-digital-journals-database-directory.jpg)