Accounting equation

19

Accounting Equation www.afzalur.com Accounting Equation This topic is on the demand of the students as a separate chapter.

-

Upload

afzalur-rahman -

Category

Education

-

view

184 -

download

0

Transcript of Accounting equation

Accounting Equationwww.afzalur.com

Accounting Equation

This topic is on the demand of the students as a separate chapter.

Accounting EquationChapter at a Glance• Basic Accounting Equation• Assets• Liabilities• Owner’s Equity• Investment• Drawing • Revenue • Expenses• Explanation of the transaction

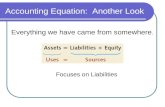

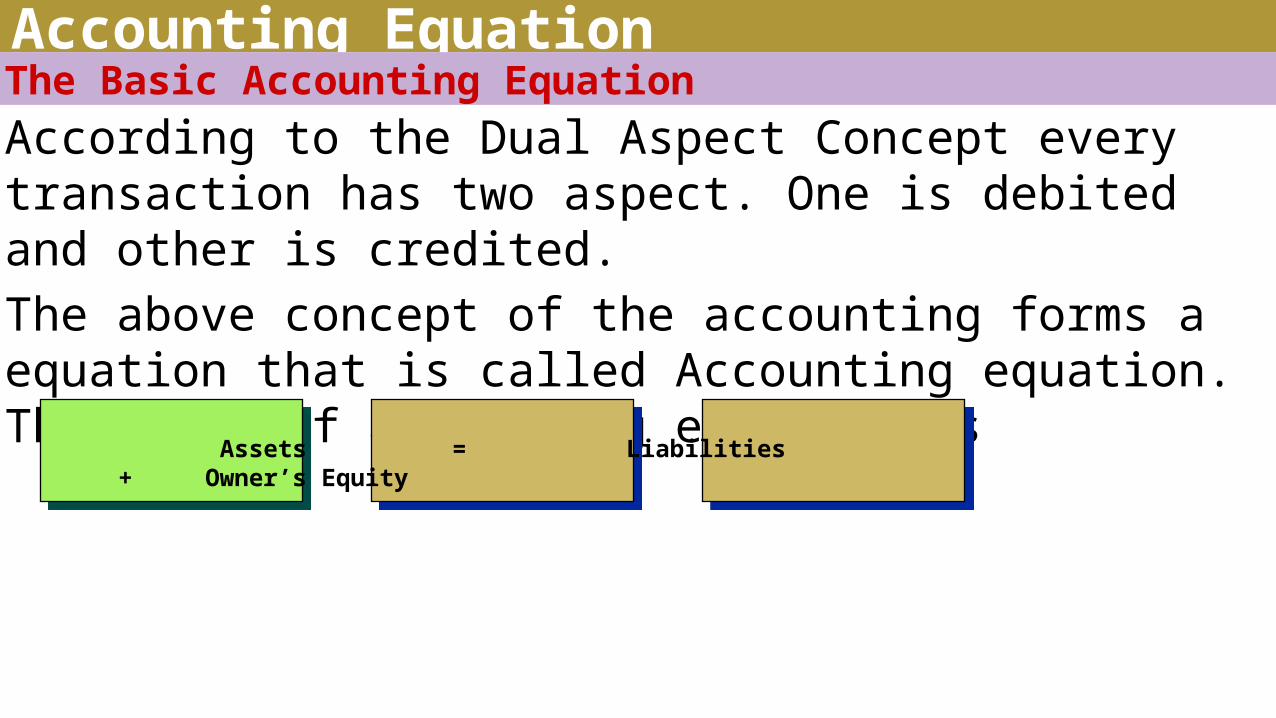

Accounting EquationThe Basic Accounting EquationAccording to the Dual Aspect Concept every transaction has two aspect. One is debited and other is credited. The above concept of the accounting forms a equation that is called Accounting equation. The basis of accounting equation is

Assets = Liabilities + Owner’s Equity

Accounting EquationAssets• Assets are resources owned by a business.• They are things of value used in carrying out such activities

as production and exchange.

To recognize the assets quickly we can say that Cash is an asset and all the things that could be convert into cash or have some future value and benefit is an assets.

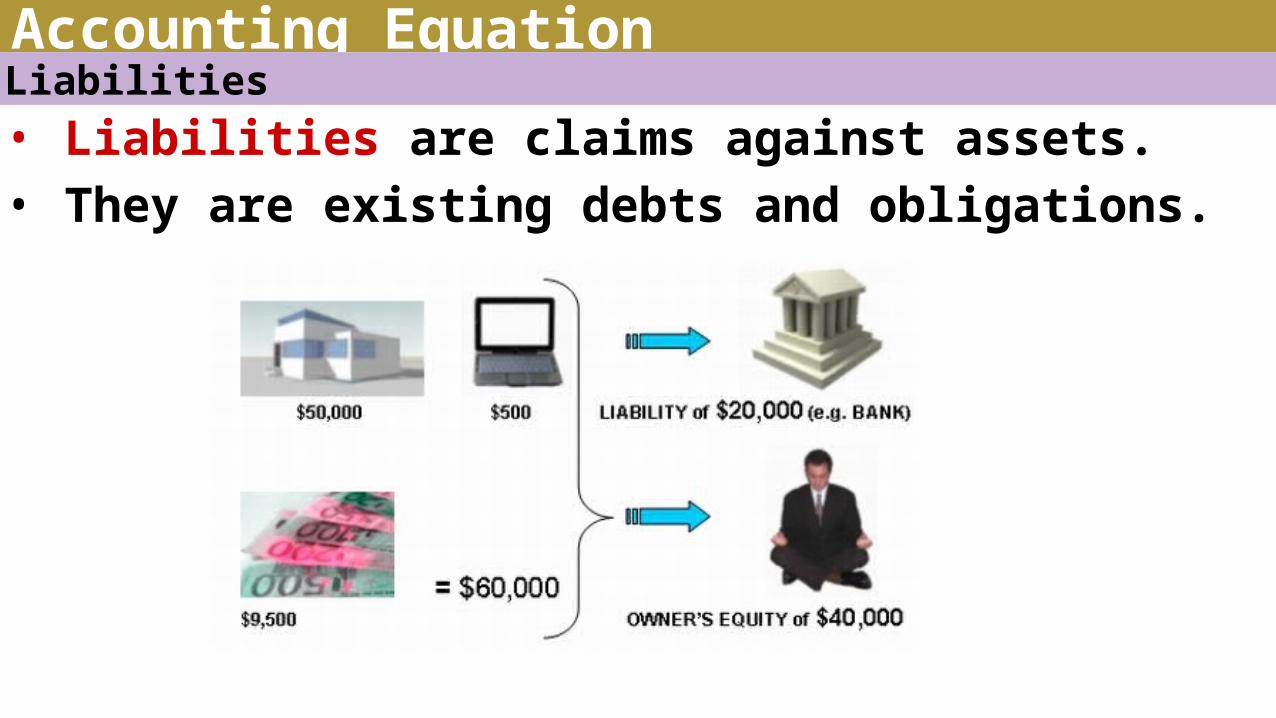

Accounting EquationLiabilities• Liabilities are claims against assets.• They are existing debts and obligations.

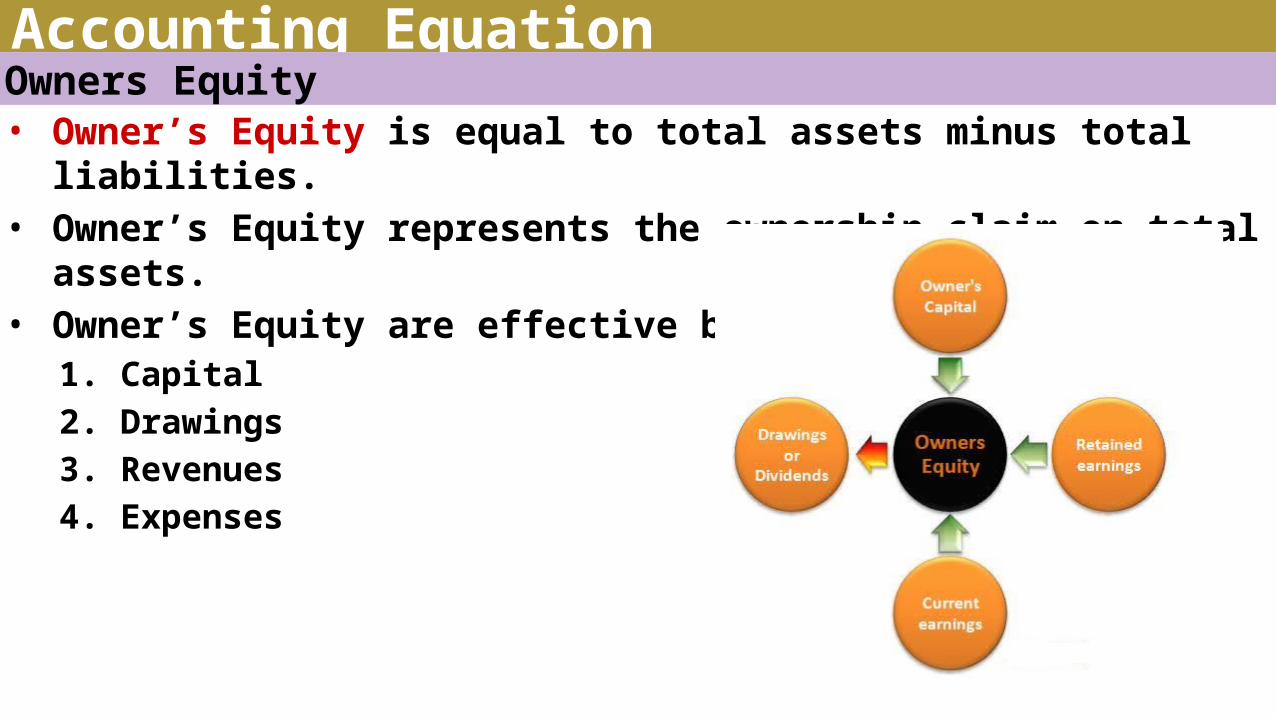

Accounting EquationOwners Equity• Owner’s Equity is equal to total assets minus total liabilities.• Owner’s Equity represents the ownership claim on total assets.• Owner’s Equity are effective by:

1. Capital2. Drawings3. Revenues4. Expenses

Accounting EquationInvestment • Investments by owner are the assets put into the business

by the owner.• These investments in the business increase owner’s equity.

It also has the following meaning. Deployment of funds with the intention and expectation that it

will earn a return. In common parlance, it refers to shares

and debentures of companies or mutual funds or bonds issued by the financial institutions or by the Government.

Accounting EquationDrawings• Drawings are withdrawals of cash or other assets by the

owner for personal use.• Drawings decrease total owner’s equity.

Accounting EquationRevenues• Revenues are the gross increases in owner’s equity resulting

from business activities entered into for the purpose of earning income.

• Revenues may result from sale of merchandise, performance of services, rental of property, or lending of money.

• Revenues usually result in an increase in an asset.

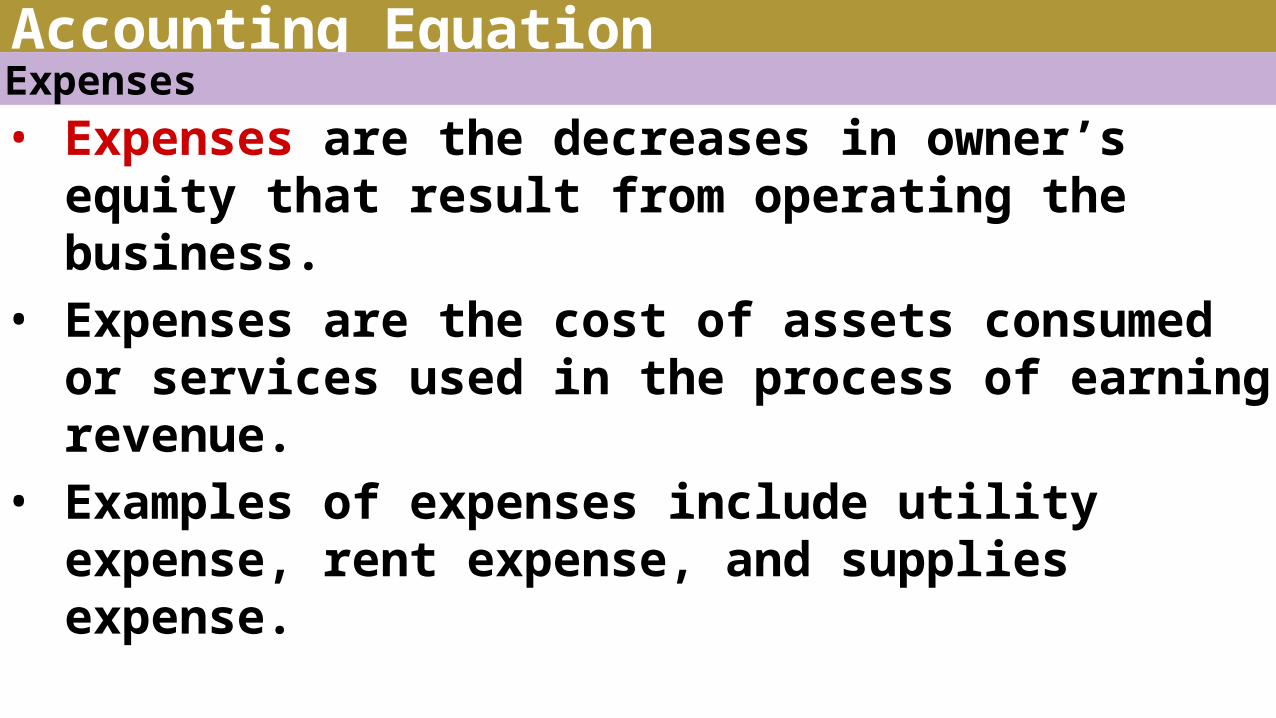

Accounting EquationExpenses• Expenses are the decreases in owner’s equity that result

from operating the business.• Expenses are the cost of assets consumed or services used in

the process of earning revenue.• Examples of expenses include utility expense, rent expense,

and supplies expense.

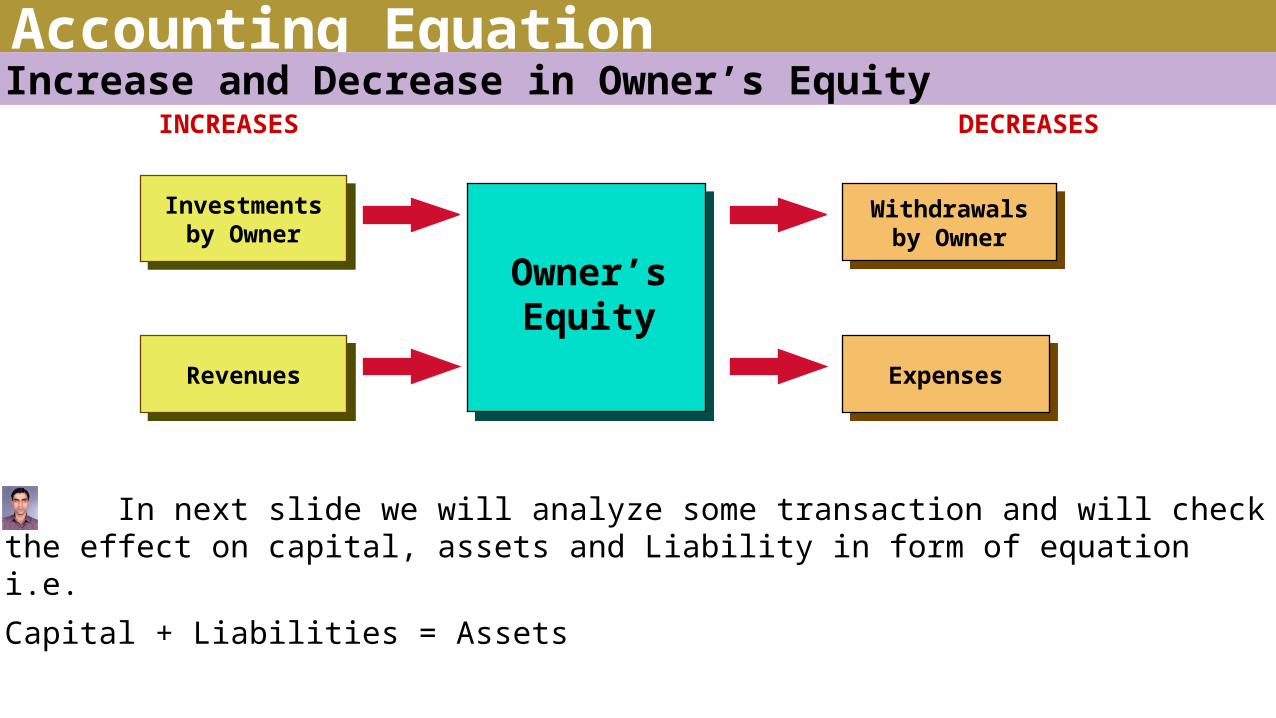

Accounting EquationIncrease and Decrease in Owner’s Equity

In next slide we will analyze some transaction and will check the effect on capital, assets and Liability in form of equation i.e.Capital + Liabilities = Assets

INCREASES DECREASESInvestments by

Owner

Revenues

Withdrawals by Owner

Expenses

Owner’s Equity

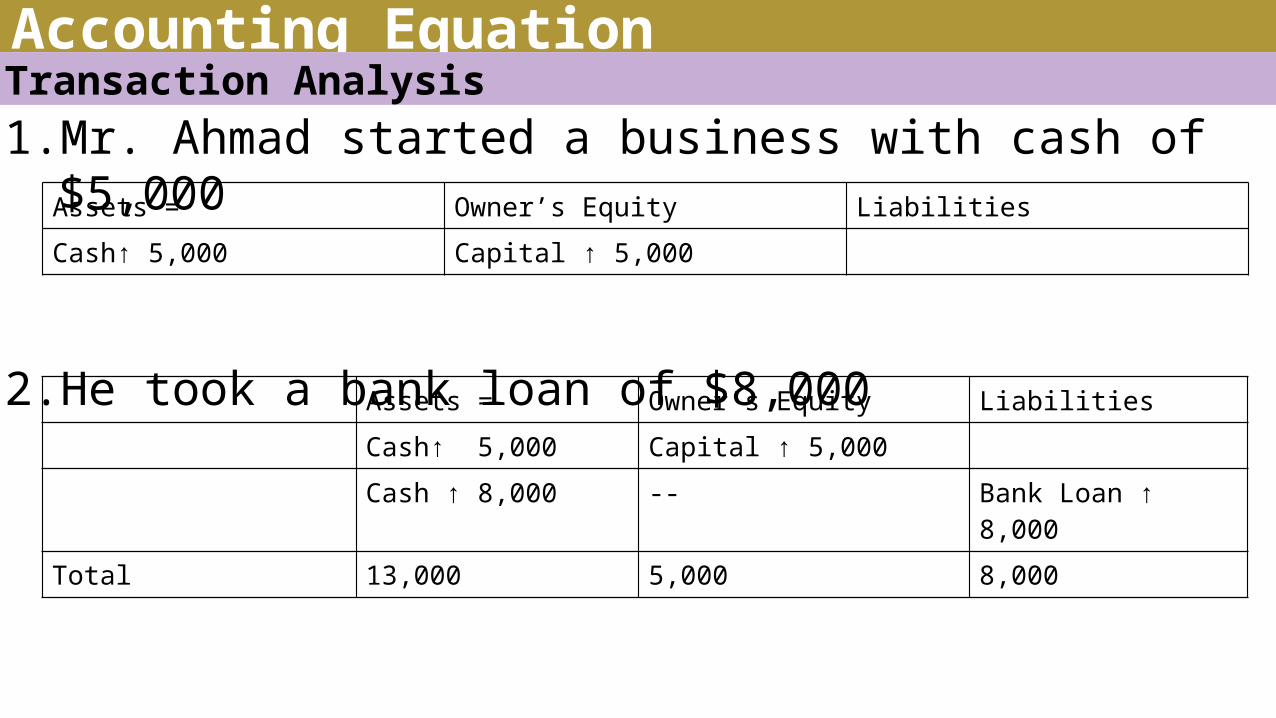

Accounting EquationTransaction Analysis1. Mr. Ahmad started a business with cash of $5,000

2. He took a bank loan of $8,000

Assets = Owner’s Equity LiabilitiesCash↑ 5,000 Capital ↑ 5,000

Assets = Owner’s Equity LiabilitiesCash↑ 5,000 Capital ↑ 5,000Cash ↑ 8,000 -- Bank Loan ↑ 8,000

Total 13,000 5,000 8,000

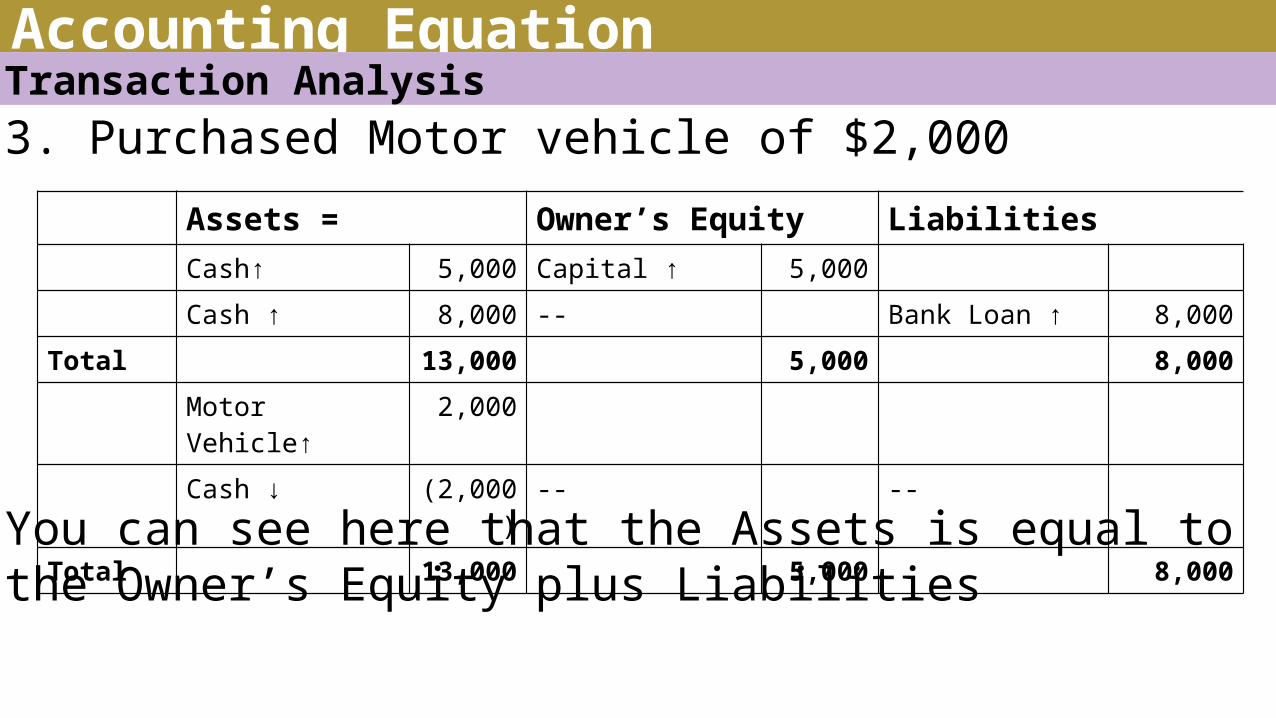

Accounting EquationTransaction Analysis3. Purchased Motor vehicle of $2,000

You can see here that the Assets is equal to the Owner’s Equity plus Liabilities

Assets = Owner’s Equity LiabilitiesCash↑ 5,000 Capital ↑ 5,000Cash ↑ 8,000 -- Bank Loan ↑ 8,000

Total 13,000 5,000 8,000Motor Vehicle↑ 2,000Cash ↓ (2,000) -- --

Total 13,000 5,000 8,000

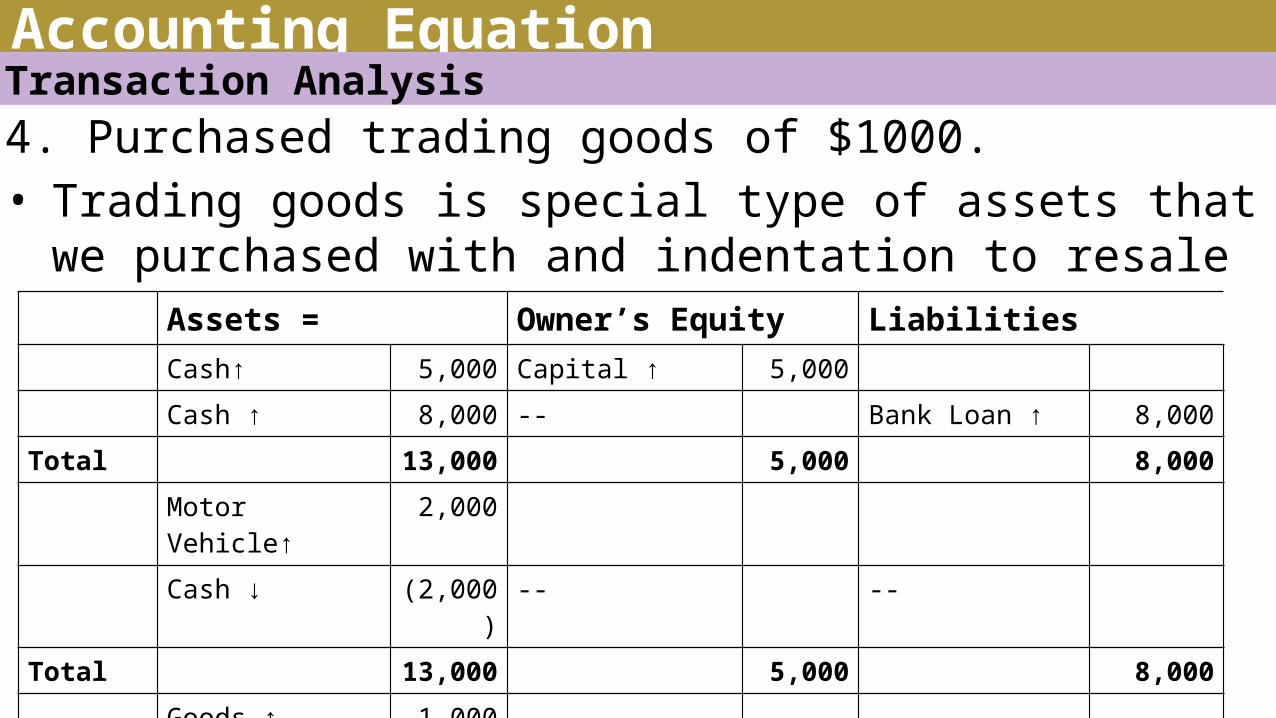

Accounting EquationTransaction Analysis4. Purchased trading goods of $1000.• Trading goods is special type of assets that we purchased with

and indentation to resaleAssets = Owner’s Equity LiabilitiesCash↑ 5,000 Capital ↑ 5,000Cash ↑ 8,000 -- Bank Loan ↑ 8,000

Total 13,000 5,000 8,000Motor Vehicle↑ 2,000Cash ↓ (2,000) -- --

Total 13,000 5,000 8,000Goods ↑ 1,000 -- --Cash ↓ (1,000)

Total 13,000 5,000 8,000

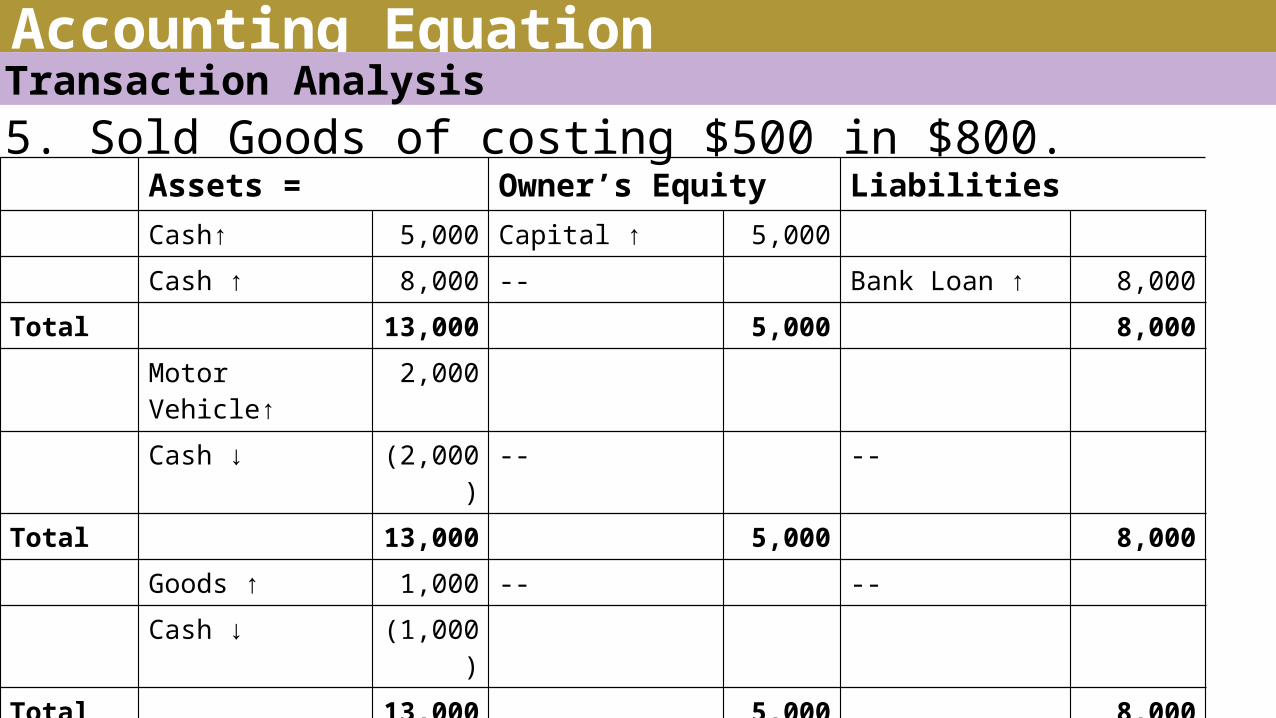

Accounting EquationTransaction Analysis5. Sold Goods of costing $500 in $800.

Assets = Owner’s Equity LiabilitiesCash↑ 5,000 Capital ↑ 5,000Cash ↑ 8,000 -- Bank Loan ↑ 8,000

Total 13,000 5,000 8,000Motor Vehicle↑ 2,000Cash ↓ (2,000) -- --

Total 13,000 5,000 8,000Goods ↑ 1,000 -- --Cash ↓ (1,000)

Total 13,000 5,000 8,000Goods ↓ (500) Profit ↑ 300Cash ↑ 800

Total 13,300 5,300 8,000

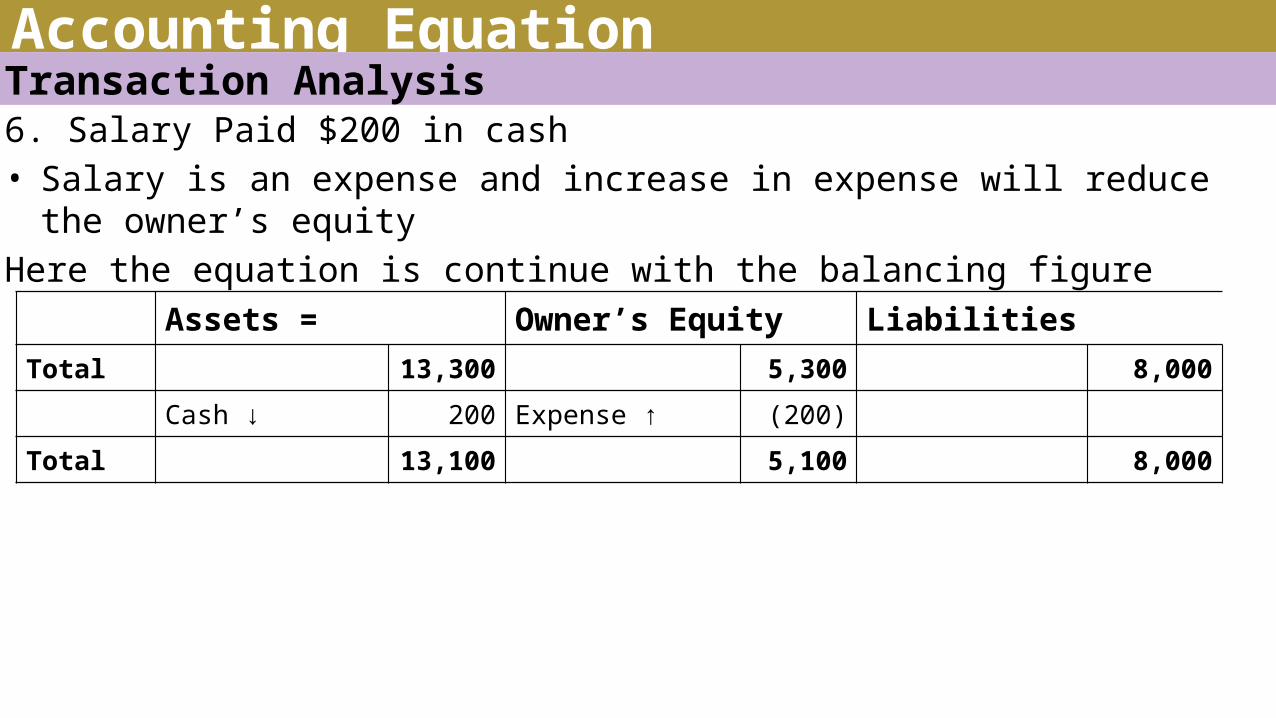

Accounting EquationTransaction Analysis6. Salary Paid $200 in cash• Salary is an expense and increase in expense will reduce the owner’s equityHere the equation is continue with the balancing figure

Assets = Owner’s Equity LiabilitiesTotal 13,300 5,300 8,000

Cash ↓ 200 Expense ↑ (200)Total 13,100 5,100 8,000

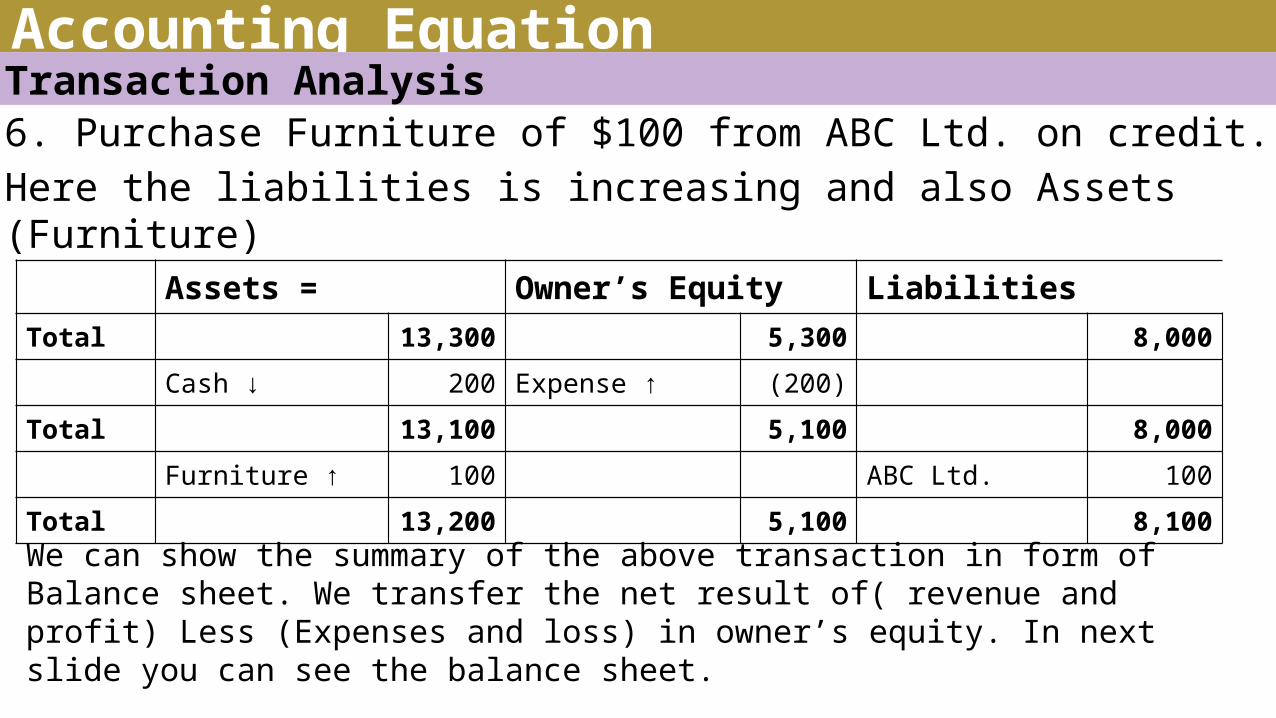

Accounting EquationTransaction Analysis6. Purchase Furniture of $100 from ABC Ltd. on credit.Here the liabilities is increasing and also Assets (Furniture)

Assets = Owner’s Equity LiabilitiesTotal 13,300 5,300 8,000

Cash ↓ 200 Expense ↑ (200)Total 13,100 5,100 8,000

Furniture ↑ 100 ABC Ltd. 100Total 13,200 5,100 8,100

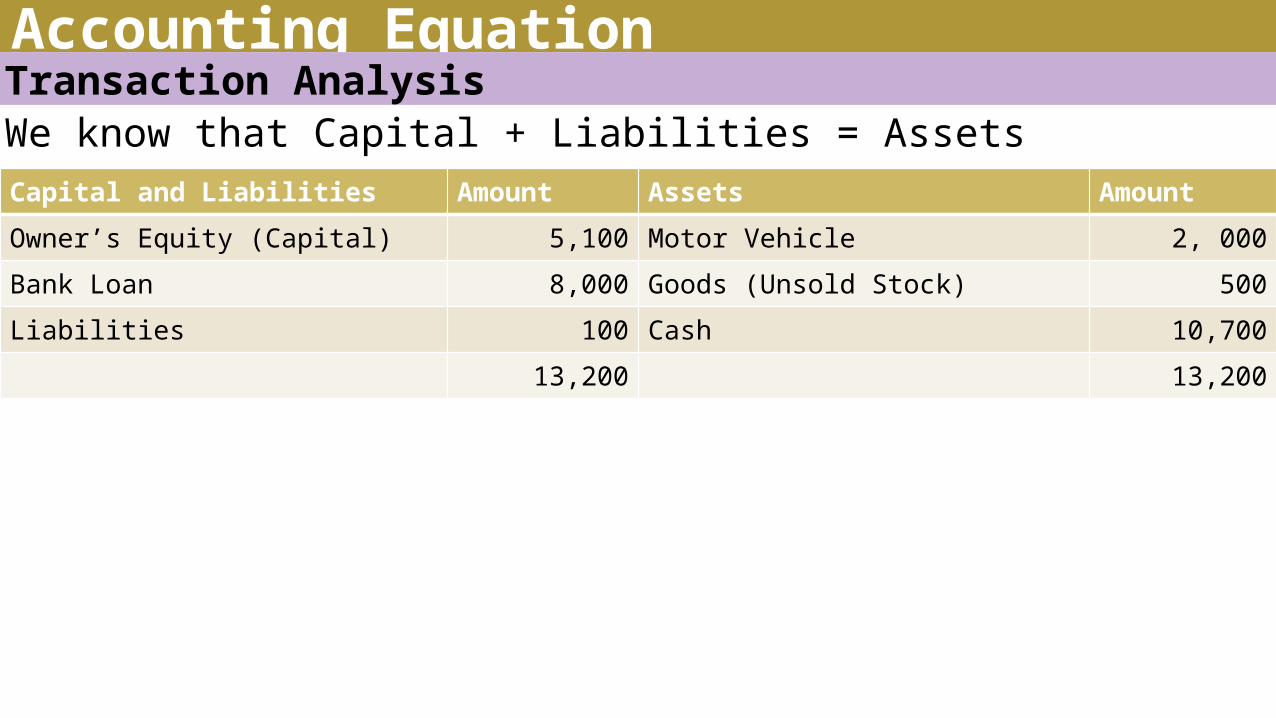

We can show the summary of the above transaction in form of Balance sheet. We transfer the net result of( revenue and profit) Less (Expenses and loss) in owner’s equity. In next slide you can see the balance sheet.

Accounting EquationTransaction AnalysisWe know that Capital + Liabilities = AssetsCapital and Liabilities Amount Assets AmountOwner’s Equity (Capital) 5,100 Motor Vehicle 2, 000Bank Loan 8,000 Goods (Unsold Stock) 500Liabilities 100 Cash 10,700

13,200 13,200

Accounting EquationFor more content visit www.afzalur.com

Appear in the quiz and many more on www.afzalur.com

Thank You