Accounting and Auditing Update - schneiderdowns.com and... · • Opening and closing balances ......

49

Accounting and Auditing Update Nick D. Lombardo

Transcript of Accounting and Auditing Update - schneiderdowns.com and... · • Opening and closing balances ......

Accounting and Auditing Update

Nick D. Lombardo

Agenda

2

• ASU 2014-09: Revenue from Contracts with

Customers

• Leases

• Other Highlights

― Recently issued/Newly effective ASUs

― Other projects/initiatives of interest

• Going Concern

• Financial Statement Project for NFP Entities

• OMB’s Uniform Grant Guidance

Revenue From Contracts With Customers (ASU 2014-09)

3

Objective: single, principle-based revenue standard

• Improve accounting for contracts with customers ― More robust framework for recognizing revenue

― Increased comparability across industries & capital markets

― Better disclosures

• Excludes contributions and collaborative arrangements

Substantially converged on major decisions

Final standard issued on May 28, 2014

Core Principle and Application

Core Principle: Recognize revenue to depict the transfer of promised goods or

services to customers in an amount that reflects the consideration to which the

entity expects to be entitled in exchange for those goods or services

4

ASU 2014-09: Disclosure Requirements*

• Disaggregate revenue into categories that depict how

revenue and cash flows are affected by economic

factors

• Explain the relationship with segment disclosures

• Opening and closing balances

• Amount of revenue recognized from contract liabilities

• Explanation of significant changes in contract balances

• Transaction price allocated to remaining performance

obligations

• Quantitative or qualitative explanation of when amounts

will be recognized as revenue

• All quantitative disclosures in annual and interim

(Public entities only)

5

Disaggregation of

Revenue

Information

about Contract

Balances

Remaining

Performance

Obligations

Interim

Requirements

*Most quantitative disclosures optional for nonpublic entities

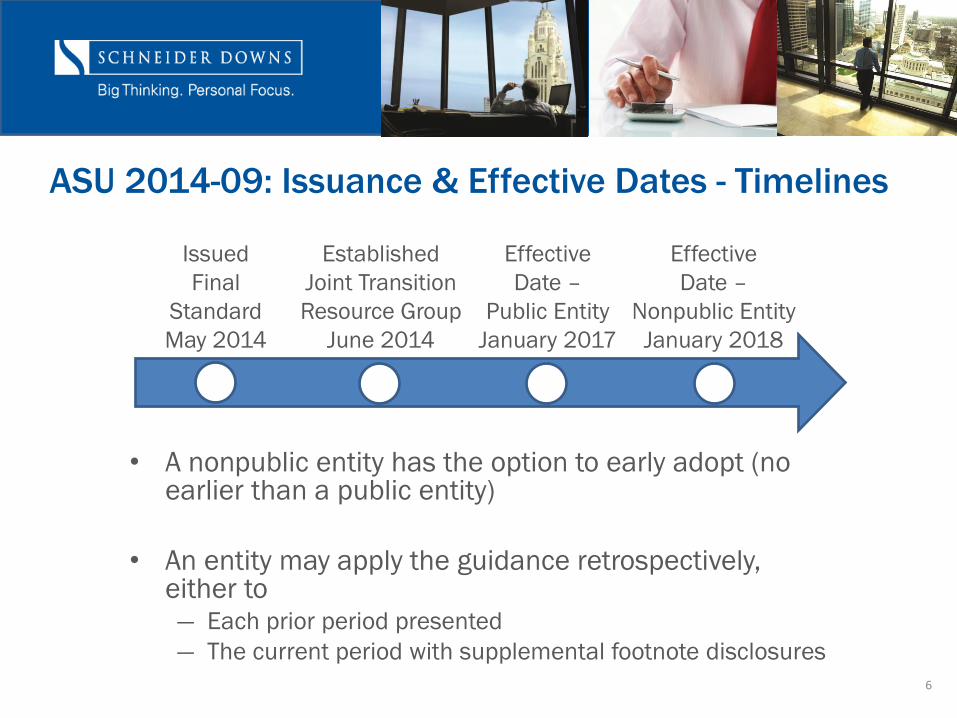

ASU 2014-09: Issuance & Effective Dates - Timelines

• A nonpublic entity has the option to early adopt (no earlier than a public entity)

• An entity may apply the guidance retrospectively, either to ― Each prior period presented

― The current period with supplemental footnote disclosures

6

Issued

Final

Standard

May 2014

Established

Joint Transition

Resource Group

June 2014

Effective

Date –

Public Entity

January 2017

Effective

Date –

Nonpublic Entity

January 2018

ASU 2014-09: Implementation

7

Significant effort likely to be expended as the U.S. moves from the current industry‐specific guidance to this new, broader, principles‐ based approach

• FASB’s formation of a Joint Transition Resource Group ― To identify and discuss broader issues, including those that may

warrant follow-up standard-setting activity by the FASB ― Similar to what we’ve done in the past following issuance of FAS 157

(Valuation Resource Group) and certain other broad standards

• AICPA’s formation of various industry-focused groups ― Includes one for Health Care and one for NFPs

Leases

8

Proposed Right-of-Use Model

A lease contract conveys the right to use an asset (the underlying asset) for

a period of time in exchange for consideration

9

Lessee Model Approach

All leases (more than 12 months) are recognized on the lessee’s balance

sheet

10

Current U.S.

GAAP (IFRS) IASB FASB

Capital (Finance)

Leases

Type A Type A

Operating Leases Type A Type B

All leases are

the same

Not all leases are the same

Classification is

based on IAS 17

(similar to FAS 13)

Lessee Accounting Overview

11

Right-of-use

asset

Lease liability

Amortization

expense

Interest

expense

Cash paid for

principal and

interest

payments

Right-of-use

asset

Lease liability

Single lease

expense on a

straight-line

basis

Cash paid for

lease

payments

Balance Sheet

Income

Statement

Cash Flow

Statement

Type

A

Type

B

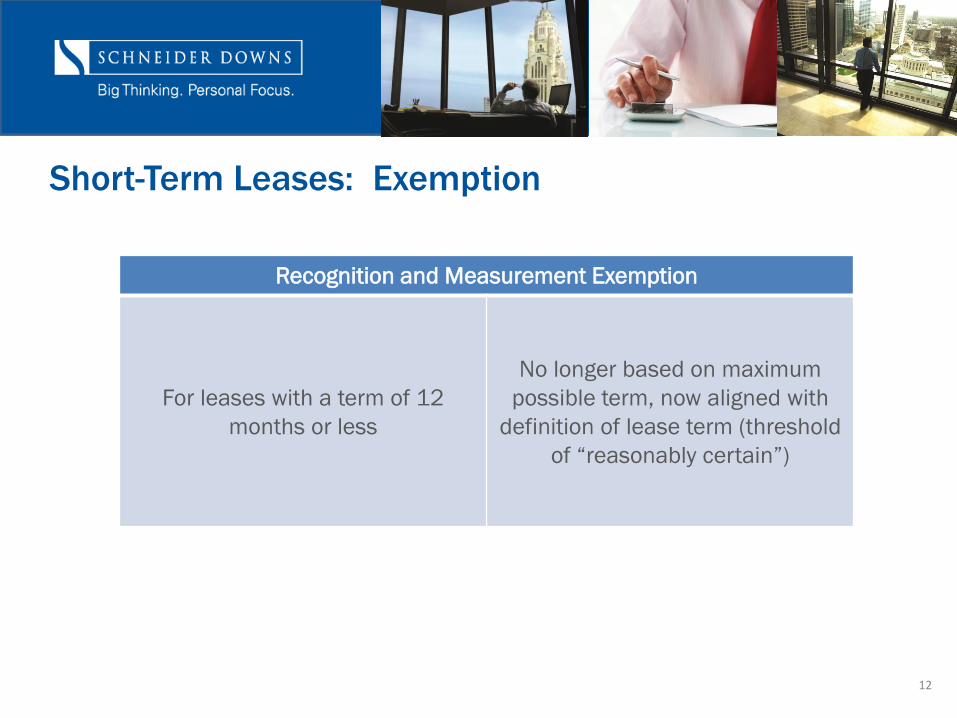

Short-Term Leases: Exemption

12

Recognition and Measurement Exemption

For leases with a term of 12

months or less

No longer based on maximum

possible term, now aligned with

definition of lease term (threshold

of “reasonably certain”)

Other Topics Discussed by Boards

13

• Lease term • Lease modifications/Contract combinations • Variable lease payments • In-substance fixed payments • Discount rate

• Definition of a lease • Separating lease and non-lease components • Initial direct costs and lease incentives

March/April

2014

May 2014

Next Set of Topics for Board Discussion

14

• Subleases • Presentation – Balance sheet • Presentation – Cash flows

• Sale and leaseback transactions • Lessee disclosures • Lessor disclosures • Leases of small assets

June 2014

July 2014

Future topics include: Related party leases, Leveraged leases, Transition, Effect date, etc.

Recently Issued/

Newly Effective ASU’s

15

ASU 2013-06: Services Received from Personnel of

an Affiliate

• Personnel services received from affiliate (parent/sub or common

control) for which affiliate doesn’t charge recipient NFP should be

recognized in recipient NFP’s financials, measured at actual costs

incurred by the affiliate

― Contributed services criteria no longer applicable

― FV practicability exception if cost will significantly over-state or

understate the value of the services received

― Entities under Topic 954 (healthcare) would report as equity transfer

• Effective for f/y beginning after 6-15-2014. Modified retrospective

application; early adoption permitted

16

ASU 2013-04: Obligations Resulting from Joint and

Several Liability Arrangements

• Requires entity to measure such obligations for which total amount of

obligation is fixed at reporting date as the sum of:

a) amount the entity agreed to pay on the basis of its arrangement among its

co-obligors, and

b) any additional amount the entity expects to pay on behalf of its co-obligors

• Also requires disclosures about nature and amount of obligation and

other information about those obligation

• Effective date:

― Nonpublic entities: f/y ending after 12-15-2014

― Retrospective application; early adoption permitted

17

Two Other Recent ASUs

• Liquidation Basis of Accounting (ASU 2013-07)

a) Defines when it should be used, how assets and liabilities should be

valued under it, and what should be disclosed

b) Effective for f/y beginning after 12-15-2013; applied prospectively

• Reporting Discontinued Operations and Disclosures of

Disposals of Components of an Entity (ASU 2014-08)

a) Only disposals involving major strategic shifts (e.g., geographic area, line

of business) henceforth will be reported as discontinued operations;

others will merely be disclosed

b) Effective for disposals in f/y beginning after 12-15-2014; applied

prospectively

18

ASU 2012-05: Newly Effective: Classification of Sales

Proceeds of Donated Financial Assets

• NFP should classify cash receipts from sale of financial assets that

upon receipt are (1) directed for sale and (2) converted nearly

immediately into cash, as operating or financing activities in statement

of cash flows, rather than as investing activities

― Operating unless restricted to a long-term purpose, e.g., endowment or

plant, then classified as financing activities

― Consistent with cash contributions

• Effective for f/y beginning after 6-15-2013. Retrospective application,

early adoption permitted

19

Going Concern: Single-Threshold Model

In May 2014, the Board directed the staff to draft a final Accounting Standards

Update.

20

Summary of

Board’s

Decisions

Single threshold model similar in principle to current

auditing standards (AU 341)

Disclosures required when there is substantial doubt, or

when…

Substantial doubt has been alleviated primarily by

management plans

Substantial doubt exists when it is probably that entity will

not meet obligations…

…for a period of one year from the financial statement

issuance date

Applies equally to both public and nonpublic entities

Effective prospectively for annual periods beginning after

December 15, 2015 and interim periods thereafter

Financial Statements Project

for NFP Entities

21

Net asset classification

Financial Performance

Reporting of Expenses

Cash Flow Statement

Liquidity NFP Note

Disclosures

Financial Statements of Not-for-Profit Entities:

Topics

22

Net Assets – Issues

• UPMIFA and PRNA/TRNA distinction

– Ability to spend from donor-restricted endowments even if underwater

– Board action required to appropriate investment returns for spending

• TRNA considered by many to be “Hodgepodge”

– Need for better disclosure of the nature and availability (timing) of

donor restricted resources

• URNA open to misinterpretation

– Better disclosure surrounding availability/liquidity would be helpful,

including limits imposed by an entity’s governing board

23

Net Assets – Two Approaches Approach 1 –

Restrictions as primary cut

Without Restrictions

Operating Endowment Plant

Approach 2 – Purpose as primary cut

Operating

Without restrictions

With restrictions

With Restrictions

Operating Endowment Plant

Endowment

Without restrictions

With restrictions

Plant

Without restrictions

With restrictions

24

Net Assets

• Can we streamline and make more meaningful?

Unrestricted Temp. Restricted Perm. Restricted

Without Donor Restrictions

With Donor Restrictions

Amount and purpose of board

designations

Nature and amount of donor restrictions

Current

GAAP

Proposed

GAAP

Disclosures

+

25

26

Financial Performance: Statement Approach

2 Statement

Greater emphasis on the operating measure

Facilitates multi-year comparison

Some may ignore the second statement

Incorrectly equate the operating measure to net income

1 Statement

Ability to present total revenue and contributions

Effect of transfers easier to identify

Too much information in one statement

Labeling of totals difficult Retain Flexibility

Without Donor

Restrictions

With Donor

RestrictionsTotal

Revenue and support:

Fees for services 495$ 495$

Bequests 600 600

Other contributions 425 1,500 1,925

Restricted support released for current period 1,375 (1,375)

Total revenue and support 2,895 125 3,020

Expenses:

Total expenses 1,950 - 1,950

Excess/(Deficit) before appropriations/transfers 945 125 1,070

Board appropriations/transfers to/(from) operations:

Investment returns appropriated from donor endowment 60 a 60

Investment returns appropriated from quasi-endowment 90 b 90

Bequests transferred to quasi-endowment (500) c (500)

Total appropriations/transfers to/(from) operations: (350) - (350)

Excess/(deficit) from operations 595$

Investment return, net 170 445 615

Board appropriations/transfers from/(to) operations:

Investment returns appropriated from donor endowment (60) a (60)

Investment returns appropriated from quasi-endowment (90) b (90)

Bequests transferred to quasi-endowment 500 c 500

Total appropriations/transfers from/(to) operations: 410 (60) 350

Total change in net assets 1,175 510 1,685

Net assets at the beginning of the period 1,500 2,100 3,600

Net assets at the end of the period 2,675$ 2,610$ 5,285$

One Statement Approach Statement of Activities

27

Operating Revenue and Support:

Fees for services 495$

Bequests 600

Other contributions 425

Restricted support released for current period 1,375

Total Operating Revenue and Support 2,895

Operating Expenses:

Total Operating Expenses 1,950

Excess/(Deficit) before appropriations/transfers 945

Board appropriations/transfers to/(from) operations:

Investment returns appropriated from donor endowment 60 a

Investment returns appropriated from quasi-endowment 90 b

Bequests transferred to quasi-endowment (500) c

Total Board transfers to/(from) operations: (350)

Excess/(deficit) from operations 595$ d

Two Statement Approach Statement of Operations

28

Two Statement Approach (cont’d) Statement of Changes in Net Assets

Without

Donor

Restrictions

With Donor

RestrictionsTotal

Excess/(deficit) from operations 595$ d $ 595$

Nonoperating activities

Contributions 1,500 1,500

Restricted support released for current period (1,375) (1,375)

Investment return, net 170 445 615

Board designated transfers from/(to) operations:

Investment returns appropriated to operations from donor endowment (60) a (60)

Investment returns appropriated to operations from quasi-endowment (90) b (90)

Bequests transferred to quasi-endowment 500 c 500

Changes in Net Assets 1,175 510 1,685

Net assets at the beginning of the period 1,500 2,100 3,600

Net assets at the end of the period 2,675$ 2,610$ 5,285$ 29

Cash Flow Statement – Issues

#1 •Understandability/Utility

#2 •Relation to Statement of Activities

(and any operating measure therein)

30

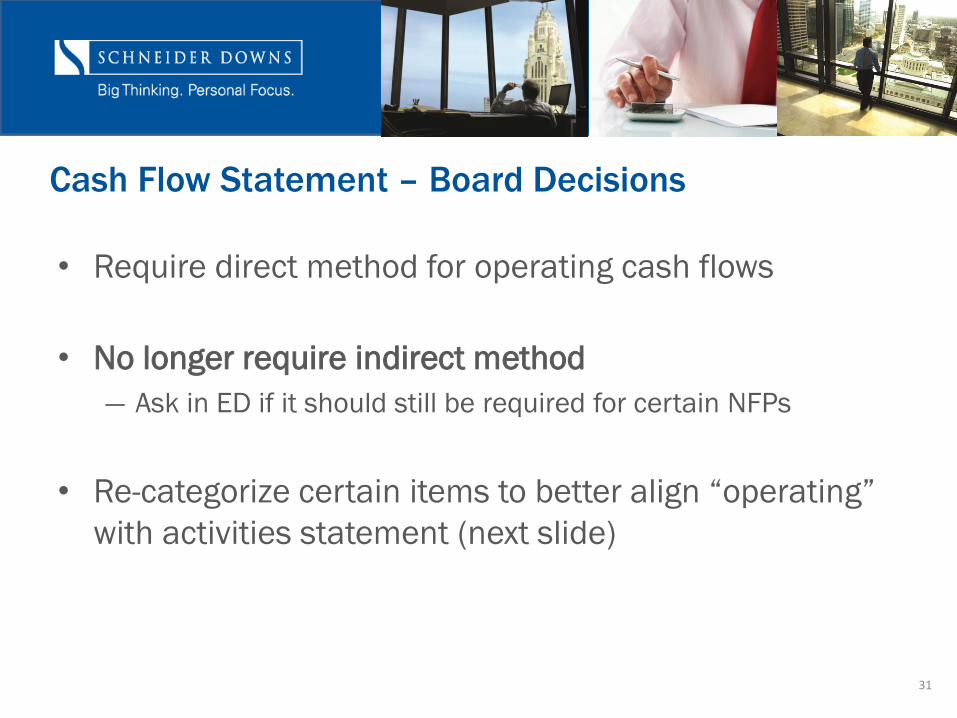

Cash Flow Statement – Board Decisions

• Require direct method for operating cash flows

• No longer require indirect method

― Ask in ED if it should still be required for certain NFPs

• Re-categorize certain items to better align “operating”

with activities statement (next slide)

31

32

Cash Flow Statement Cash Flows from Operating Activities

Cash received from service recipients

Cash received from donors

Cash paid to employees

Cash paid to vendors

Purchase of property and equipment

Contributions restricted for property and equipment

Net cash from operating activities

Cash Flows from Investing Activities

Cash received from interest and dividends

Purchase of investment assets

Proceeds from sale of investment assets

Net cash from investing activities

Cash Flows from Financing Activities

Payments of principal on long-term debt

Interest paid on long-term debt

Contributions restricted for endowment

Net cash from financing activities Net increase in cash

Cash at the beginning of year

Cash at end of year 32

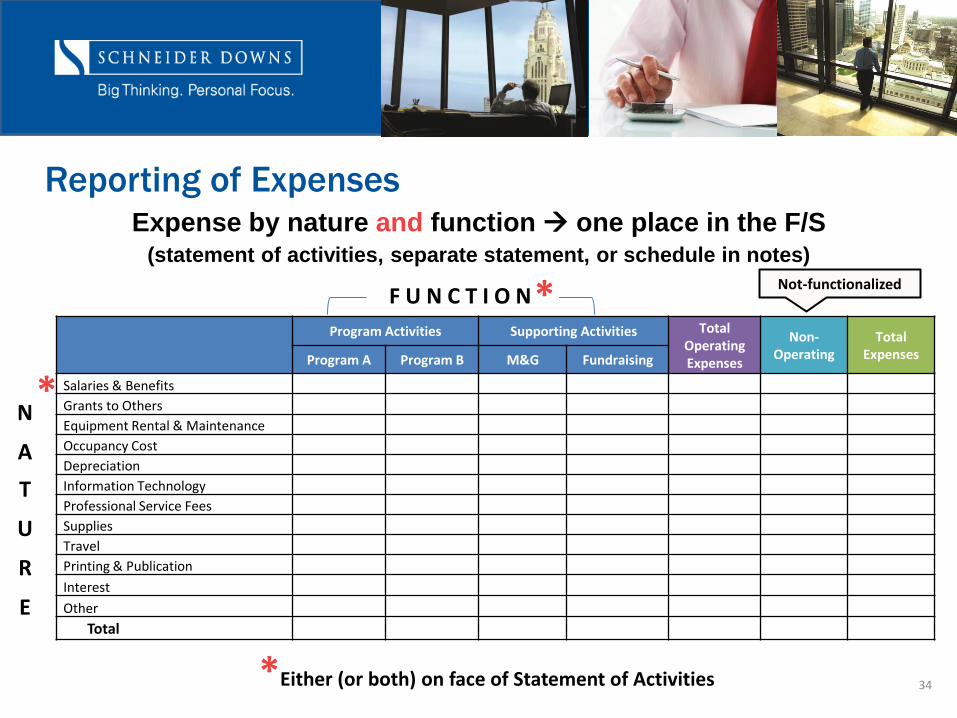

Reporting of Expenses – Issues

• AICPA Issue

― Who should be required to present a Statement of Functional

Expenses?

• FASB Deliberations

― Should natural expenses be required?

― Should functional expenses still be required?

― Should both be required together?

― Which breakout on the Statement of Activities?

― Should investment /other nonoperating expenses be

functionalized?

33

Expense by nature and function one place in the F/S (statement of activities, separate statement, or schedule in notes)

Reporting of Expenses

Program Activities Supporting Activities Total

Operating Expenses

Non- Operating

Total Expenses Program A Program B M&G Fundraising

Salaries & Benefits

Grants to Others

Equipment Rental & Maintenance

Occupancy Cost

Depreciation

Information Technology

Professional Service Fees

Supplies

Travel

Printing & Publication

Interest

Other

Total

F U N C T I O N

N

A

T

U

R

E

*

*

*Either (or both) on face of Statement of Activities

Not-functionalized

34

• Reporting of investment expenses (Board discussion

begun)

• Liquidity and financial flexibility (Board discussion begun)

• NFP-specific notes (in-process)

• Expiration of capital restrictions and other display issues

concerning capital transactions

35

Remaining Topics

Board Deliberations

First half 2014

Q3 2014

Exposure Draft

Comment Period

Q4 2014 – Q1 2015

2015

Final ASU

36

Project Timeline

OMB’s Uniform Grant

Guidance

37

Agenda

• Introduction to OMB’s Uniform Grant Guidance

(Super Circular)

• Subpart A – Acronyms and Definitions

• Subpart B – General Provisions

• Subpart C – Pre-Award Requirements

• Subpart D – Post-Award Requirements

• Subpart E – Cost Principals

• Subpart F – Audit Requirements

38

What Is the Super Circular?

• OMB’s Uniform Administrative Requirements, Cost

Principles and Audit Requirements for Federal

Awards

― Project to streamline Circulars A-21, portion of A-50, A-

87, A-89, A-102, A-110, A-122, and A-133

― Eliminate duplicative and conflicting guidance

― Consistent and transparent treatment of costs

― Effective for f/y that begin on or after December 26,

2014

― Guidance reviewed at least every 5 years

39

Subpart F – Audit Requirements

• The final guidance strengthen oversight and focuses audits where there is the greatest risk of waste, fraud, and abuse of taxpayer dollars

• Improves transparency and accountability by providing on-line access to complete single audit reports

• Encourages Federal agencies to take a more cooperative approach to resolve weaknesses in internal controls

• Reinforces risk-based approach to determining Major Programs

• The basic structure of the Single Audit process is unchanged

40

Subpart F – Audit Requirements

• COFAR has provisions throughout the Uniform Guidance to

strengthen the level of oversight for non-Federal entities that fall

below the new threshold

• Audit threshold increases from $500,000 to $750,000

• Major Program determination focuses on internal control

deficiencies identified as material weaknesses

• Type A/B programs minimum threshold will also be $750,000

41

Subpart F – Audit Requirements

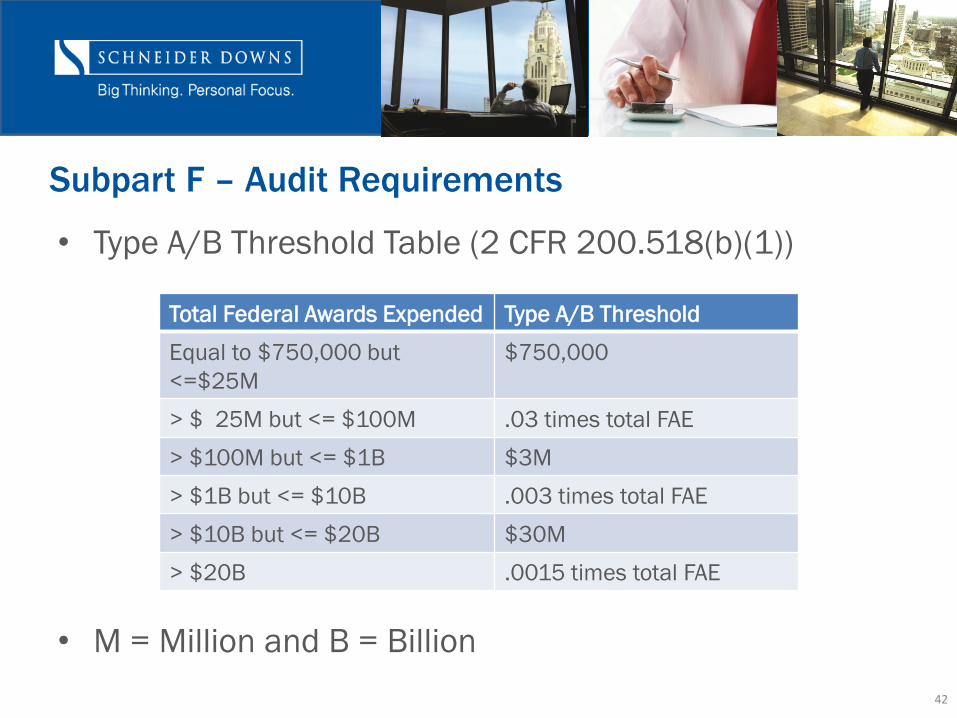

• Type A/B Threshold Table (2 CFR 200.518(b)(1))

• M = Million and B = Billion

42

Total Federal Awards Expended Type A/B Threshold

Equal to $750,000 but

<=$25M

$750,000

> $ 25M but <= $100M .03 times total FAE

> $100M but <= $1B $3M

> $1B but <= $10B .003 times total FAE

> $10B but <= $20B $30M

> $20B .0015 times total FAE

Subpart F – Audit Requirements High-Risk Type A

Program

Current A-133 Criteria New Uniform Guidance

Not audited as major program in 1 of 2

most recent audit periods

Unchanged

In most recent period had ANY audit

finding

• Provided for limited auditors

judgment

• Oversight exercised by Federal

agencies or pass-through entities,

audit follow-up, or changes in

personnel or systems that

significantly increased risk

In most recent period had a HIGH-RISK

AUDIT FINDING

• Modified opinion

• Material weakness in internal control

• Known or likely questioned costs

more than 5% of program

expenditures

• Auditors judgment basically

unchanged

43

Subpart F – Audit Requirements High-Risk Type B

Program

Current A-133 Criteria Uniform Guidance

Two Type B risk assessment options: Perform risk assessments on Type B

programs until high-risk Type B

programs have been identified UP TO

at least 25% of the number of low-risk

Type A programs.

• Option 1 – Perform risk assessment of

ALL Type B programs and select 50% of

Type B programs identified as high risk

up to the number of low-risk Type A

programs

• Option 2 – Perform risk assessments on

all Type B programs until as many high-

risk Type B programs have been

identified as there are low-risk Type A

programs

44

Subpart F – Audit Requirements

• Uniform Guidance reduces the minimum audit

percentage of coverage of total SEFA programs as

follows:

45

Type of Auditee Current New

Not low-risk 50% 40%

Low-risk 25% 20%

Subpart F – Audit Requirements Low-Risk Auditee

Current Criteria (2 prior years) Uniform Guidance (2 prior years)

Annual single audits Unchanged

Unmodified opinion on financial

statements in accordance with GAAP

Unmodified opinions on GAAP

statements or basis of accounting

required by state law

Unmodified SEFA in relation to opinion Unchanged

No GAGAS material weaknesses Unchanged

No Type A programs had:

• Material Weaknesses

• Material noncompliance

• Questioned costs > 5%

Unchanged

Timely filing with FAC Unchanged

Auditor reporting going concern does

not preclude low-risk

No audit reporting of going concern

Waivers No waivers 46

Subpart F – Audit Requirements

• All auditees must submit the complete reporting package and Data Collection Form (DCF) electronically to the Federal Audit Clearinghouse (FAC)

• FAC will be responsible to make the reports available on a website

• Subrecipient is only required to submit report to FAC

• Pass-through entity not required to retain copy of subrecipient report

47

Subpart F – Audit Requirements

• The threshold for reporting know and likely questioned costs increases from $10,000 to $25,000

• Requires that questioned costs be identified by CFDA number and applicable award number

• Requires report on status of prior year audit finding(s) in the Summary Schedule of Prior Audit Findings

• Audit finding numbers must be formatted as prescribed by the DCF

• Requires disclosure of population and number of cases examined, quantified in terms of dollar value and whether the sampling was statistically valid for the finding

48

49

QUESTIONS