Accessing the US Capital Markets from Outside - Latham & Watkins

170

Alexander F. Cohen Dana G. Fleischman Antti V. Ihamuotila Jeffrey H. Lawlis IFLR international Financial Law Review Accessing the US capital markets from outside the United States An overview for foreign private issuers and their advisors 2013 Update

Transcript of Accessing the US Capital Markets from Outside - Latham & Watkins

Alexander F. Cohen

Dana G. Fleischman

Antti V. Ihamuotila

Jeffrey H. Lawlis

IFLRinternational Financial Law Review

Accessing the US capitalmarkets from outside theUnited StatesAn overview for foreign privateissuers and their advisors2013 Update

IFLRA

ccessing the US

capital markets from

outside the United S

tatesA

n overview for foreign private issuers and their advisors

2013 UP

DATE

About us

Latham & Watkins is a global powerhouse in both the debt and equity capital markets.With more than 300 capital markets lawyers located in offices in the world’s majorfinancial, business and regulatory centers, we advise on the market’s largest and mostcomplex securities offerings. Latham couples the resources of a truly international firmwith an on-the-ground understanding of local markets and deep industry and productexpertise in order to provide our clients with unparalleled service and commercialadvice.

Latham has ranked #1 in US IPOs since the year 2000, and no firm ranks higher inrepresenting both issuers and investment banks in high yield debt issuances.* Lathamalso received more Top 10 rankings than any other law firm in The American Lawyer’s2013 Corporate Scorecard.

Our lawyers have extensive experience navigating the US securities regulatorylandscape, which includes the US securities laws, SEC rules and regulations (includingfinancial reporting requirements), stock exchange rules and the rules of variousself-regulatory organizations. In addition to our expertise advising US issuers and theirinvestment banks, we routinely advise clients on securities offerings by non-US issuersin Europe, Asia, Latin America and the Middle East. In many of these transactions, theissuer’s securities are sold in concurrent offerings in the United States.

We take pride in our efforts to explain and demystify complex legal issues in the capitalmarkets in a lively, plain-English manner. You can find our industry-leading thoughtleadership pieces on our website, www.lw.com, and on our Words of Wisdom blog,www.wowlw.com. For a glossary of more than 1200 terms used in capital-raisingtransactions, visit the iTunes App store to download two of our most popular apps: TheBook of Jargon™ – US Corporate and Bank Finance and The Book of Jargon™ –European Capital Markets and Bank Finance.

* Sources: IPO Vital Signs and Bloomberg.

** In association with the Law Office of Salman M. Al-Sudairi

lw.com

Latham & Watkins operates worldwide as a limited liability partnership organized under the laws of theState of Delaware (USA) with affiliated limited liability partnerships conducting the practice in the UnitedKingdom, France, Italy and Singapore and as affiliated partnerships conducting the practice in Hong Kongand Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’ associated office in the Kingdomof Saudi Arabia. In Qatar, Latham & Watkins LLP is licensed by the Qatar Financial Centre Authority. © Copyright 2013 Latham & Watkins. All Rights Reserved.

Abu DhabiBarcelonaBeijingBostonBrusselsChicagoDohaDubai

DüsseldorfFrankfurtHamburgHong KongHoustonLondonLos AngelesMadrid

MilanMoscowMunichNew YorkOrange CountyParisRiyadh**Rome

San DiegoSan FranciscoShanghaiSilicon ValleySingaporeTokyoWashington, D.C.

Alexander F. CohenPartner, Washington

Dana G. FleischmanPartner, New York+1-212-906-1220

Antti V. IhamuotilaPartner, London

Jeffrey H. LawlisPartner, Milan and London

Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors i

2013 EDITION

Accessing the US capital markets from outside theUnited States: an overview forforeign private issuers andtheir advisors

Editors

Alexander F. Cohen Dana G. Fleischman Antti V. Ihamuotila Jeffrey H. Lawlis

Latham & Watkins LLP

September 2013

Latham & Watkins operates worldwide as a limited liability partnership organized under the lawsof the State of Delaware (USA) with affiliated limited liability partnerships conducting the practicein the United Kingdom, France, Italy and Singapore and as affiliated partnerships conducting thepractice in Hong Kong and Japan. The Law Office of Salman M. Al-Sudairi is Latham & Watkins’associated office in the Kingdom of Saudi Arabia. In Qatar, Latham & Watkins LLP is licensed bythe Qatar Financial Centre Authority.

© Latham & Watkins and Euromoney Institutional Investor 2013. All rights reserved.

All or part of this document has been or may be used in other materials published by the authorsor their colleagues at Latham & Watkins and may be updated or changed in other materials. Theinformation contained in this document is published by Latham & Watkins as a service to itsclients and should not be construed as legal advice. Should further analysis or explanation of thesubject matter of this document be required, please contact any of the authors or the Latham &Watkins attorney with whom you normally consult.

ii Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

About the editors Alexander F. Cohen is a partner in the Washington, D.C. office of Latham & Watkins and Co-Chairof Latham’s national office, a central resource for clients and Latham lawyers facing complex issuesarising under the US securities laws. Mr. Cohen is a former senior official of the US Securities andExchange Commission. He joined the SEC Staff in 2006 as Deputy General Counsel for LegalPolicy and Administrative Practice and later served as Deputy Chief of Staff. His practice coverscapital markets, registration and reporting with the SEC, corporate governance, accountingrestatements, investigations by the SEC and related issues. Mr. Cohen was a partner in Latham’sLondon and Hong Kong offices from 2001 to 2006, and has particular expertise advising non-UScompanies on US securities law matters.

Dana G. Fleischman is a partner in the New York office of Latham & Watkins and is a member ofLatham’s Capital Markets and Financial Regulatory Practices and the firm’s Financial InstitutionsGroup. Ms. Fleischman’s practice focuses on matters involving the regulation of broker-dealers andsecurities markets. Her clients consist primarily of major investment banks, leading financial tradeassociations, electronic trading platforms, investment advisers, exchanges, clearing organizations,and non-US banks and bank holding companies. Ms. Fleischman advises clients on a wide range ofcorporate and regulatory compliance matters, including in connection with mergers and acquisitionsand cross-border transactions. She also has extensive experience representing US and non-UScorporate and investment banking clients in public offerings and private placements and assistsclients in connection with internal investigations and enforcement matters.

Antti V. Ihamuotila is a partner in the London office of Latham & Watkins. He practices corporatelaw with an emphasis on capital markets, mergers and acquisitions and securities regulation. Mr.Ihamuotila has advised on public and private offerings of equity and debt securities and public andprivate mergers and acquisitions. He also advises clients in venture capital investments and ongeneral corporate matters, including compliance with US federal securities laws.

Jeffrey H. Lawlis is a partner in the London and Milan offices of Latham & Watkins. Mr. Lawlis’practice focuses on corporate finance, including leveraged finance and high yield transactions andother debt and equity capital markets offerings and liability management transactions, companyrepresentation and general securities matters as well as mergers and acquisitions. Mr. Lawlis hasextensive international experience representing companies, sponsors and investment banks in avariety of industries on a wide range of both public and private cross-border transactions, with aparticular focus on the Italian and Spanish markets.

Editor Danielle Myles

Sub-editor Phil Taylor

Production editor Richard Oliver

Associate publisher Denny Squibb

Managing director Tim Wakefield

Divisional director Danny Williams

Image setting and printing by Buxton Press, Buxton, UK.

This report states the law as at the beginning of September 2013. It is not a substitute fordetailed legal advice.

© Latham & Watkins and Euromoney Institutional Investor 2013.

For additional copies of this publication and more information on International Financial LawReview, including a sample copy, call Denny Squibb, on Tel: +852 2842 6945 or e-mail:[email protected]

Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors iii

About the other contributing authors

Alan W. Avery is a partner in the New York office of Latham & Watkins and a member of the firm’sFinancial Institutions Group. He concentrates his practice in federal and state regulation of bankingorganizations, advising domestic and foreign banking institutions concerning the impact of USfederal and state banking laws on their global operations. Additionally, he advises domestic andforeign banks on regulatory issues, including Bank Secrecy Act and anti-money laundering issuesand investigatory matters, as well as related corporate and litigation matters. Mr. Avery also advisesdomestic and foreign financial institutions and other parties on a wide range of matters related toUS financial regulatory reform.

Witold Balaban is a partner in the New York office of Latham & Watkins and a member of the firm’sCapital Markets and Derivatives Practices. He specializes in equity derivatives and equity-linkedproducts, including convertible and exchangeable bond offerings (both optional and mandatory)and related equity derivatives products (such as call spread overlays and issuer or affiliate borrowfacilities), fixed and variable share forward sales and related equity offerings, issuer share repurchasetransactions, hedging and monetization transactions (including equity-based finance transactions)and structured products distributed publicly and privately.

Richard Brown is a partner in the London office of Latham & Watkins. He has wide experience inboth public and private mergers and acquisitions transactions as well as both primary and secondaryequity capital markets work both in the UK and internationally. Mr. Brown advises both issuers andunderwriting banks on equity capital markets transactions.

Les P. Carnegie is a partner in the Washington, D.C. office of Latham & Watkins and a member ofthe firm’s Export Controls and Economic Sanctions Practice. He specializes in a wide variety ofinternational trade and national security matters. Mr. Carnegie’s practice focuses on legal, policy andenforcement issues arising under US export controls, trade and economic sanctions, anti-boycottrestrictions, national security reviews of foreign investments in the United States and compliancewith the Foreign Corrupt Practices Act. With a particular focus on leading complex internalinvestigations, preparing disclosures to the US government and developing compliance programs,Mr. Carnegie has specialized expertise in the aerospace, defense, life sciences, energy, financial andhigh technology industries.

Barton B. Clark is a partner in the Washington, D.C. office of Latham & Watkins and is Co-Chairof the firm’s Investment Funds Practice Group. Mr. Clark represents private equity funds and theirsponsors and advisers, as well as other market participants, both internationally and in the UnitedStates. His practice addresses fund formation, portfolio investment structuring, sponsor equity andgovernance arrangements, as well as joint ventures and other strategic transactions. As part of hispractice, Mr. Clark advises sponsors of private investment funds on registration and compliancematters under the Investment Advisers Act of 1940 and the Investment Company Act of 1940.

Kirk A. Davenport II is a partner in the New York office of Latham & Watkins, Co-Chair of the firm’snational office and a former member of the firm’s Executive Committee. His practice centers oncapital markets and securities law matters as well as all aspects of debt and equity financings. Mr.Davenport’s clients include US and international investment banks, New York Stock Exchange andNasdaq-listed companies, foreign private issuers, leveraged buyout funds and mezzanine investmentfunds.

Bryant B. Edwards is a partner in the Hong Kong office of Latham & Watkins. Mr. Edwardsrelocated to Hong Kong after four years in Dubai where he led the opening of the firm’s four MiddleEast offices and served as Chair of the firm’s Middle East Practice. Before Dubai, Mr. Edwards spenteight years in the firm’s London office, where he was Chair of the Corporate Department andfocused on the development of the firm’s European high yield bond practice. He previously servedas Chair of the Los Angeles Corporate Department. Mr. Edwards’ practice includes representationof companies and investment banking firms in merger and acquisition transactions and in publicand private offerings of securities, with a particular emphasis on issuances and restructurings of debtsecurities. He has advised issuers and underwriting banks in more than 100 bond offerings.

iv Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

Rafal Gawlowski is a partner in the New York office of Latham & Watkins and a member of the firm’sCapital Markets, Derivatives and Structured Finance & Securitization practices. Mr. Gawlowski’spractice focuses on derivatives, particularly equity derivatives and equity-linked capital marketstransactions. Those transactions most prominently include derivatives products relating to equity-linked capital markets transactions (call spread overlays), structured repurchase transactions(accelerated forward and forward issuer repurchases), issuer forward issuance transactions, variousmonetization and hedging transactions and derivative financing transactions. In addition toderivatives, Mr. Gawlowski has practiced in the areas of cross-border corporate finance, privateequity, structured finance, investment management and banking, both in New York and in London.

Lene Malthasen is a partner in the London office of Latham & Watkins and Co-Chair of the firm’sglobal Capital Markets Practice. Her practice focuses primarily on equity and debt capital markets,where she has acted for underwriters, issuers, arrangers and trustees on debt issues; MTN and ECPprograms; GDR and other equity offerings; convertible, exchangeable, subordinated, high-yield, andcross-over bonds; as well as sovereign and municipal bonds and tender offers, consent solicitationsand bond restructurings. Ms. Malthasen has considerable experience in listing debt, equity andstructured finance products on the London Stock Exchange, AIM, the PSM, the Luxembourg StockExchange, Euro MTF and the Irish Stock Exchange.

William M. McGlone is a partner in the Washington, D.C. office of Latham & Watkins. Mr.McGlone is one of the leading US practitioners in the field of export controls and economicsanctions. His practice focuses on legal, policy and enforcement issues arising under United Statesexport controls, trade and economic sanctions, and other laws governing cross-border transactions.Mr. McGlone counsels and represents clients on legal and policy issues arising under various legalregimes that govern international trade, technology transfers, investment and cross-border businessactivities. His areas of expertise include sanctions administered by the Treasury Department’s Officeof Foreign Assets Control, the International Traffic in Arms Regulations, the Export AdministrationRegulations, US anti-boycott laws, the Foreign Corrupt Practices Act and multilateral trade controls.

Gregory P. Rodgers is a partner in the New York office of Latham & Watkins and a member of thefirm’s Capital Markets, Derivatives and General Corporate Representation Practices. In corporatefinance matters, Mr. Rodgers represents issuers, investors and investment banks in public and privateequity, debt and hybrid capital markets transactions, commercial lending transactions, restructuringsand other financing transactions, with a particular focus on convertible securities and high yieldsecurities.

Nabil Sabki is a partner in the Chicago office of Latham & Watkins. Mr. Sabki’s practice focuses onthe representation of financial service companies, such as registered investment advisers, privateequity and hedge fund managers, private investment funds, registered mutual funds and businessdevelopment companies. He has significant experience forming and representing various privatefunds and their sponsors, including both domestic and offshore hedge funds.

Mark A. Stegemoeller is a partner in the Los Angeles office of Latham & Watkins. He was a partnerin the firm’s London office from 1998 through 2002. Mr. Stegemoeller practices corporate law withsignificant expertise in capital markets and securities matters. He has handled a wide variety of cross-border public and private debt and equity securities offerings for investment banking and corporateclients (including initial public offerings and registered, Rule 144A, Regulation S, Regulation D andhigh yield debt offerings). Mr. Stegemoeller is also experienced in debt tender and exchange offers,consent solicitations and restructuring transactions, and advises corporate clients concerningcompliance with registration and reporting provisions of the US Securities Act of 1933 and the USSecurities Exchange Act of 1934.

Michael W. Sturrock is a partner in the Singapore office of Latham & Watkins and Vice Chair of thefirm’s global Corporate Department. His practice focuses on corporate finance and mergers andacquisitions. Mr. Sturrock represents both issuers and underwriters in corporate financings and bothbuyers and sellers in public and private merger and acquisition transactions. He has extensiveexperience in Asia having advised on more than 200 completed financing and mergers andacquisitions transactions in the region. Mr. Sturrock is consistently recognized as one of the region’sleading lawyers for corporate and capital markets transactions.

Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors v

Joel H. Trotter is a partner in the Washington, D.C. office of Latham & Watkins. He is the globalCo-Chair of the firm’s Public Company Representation practice group, Deputy Chair of theCorporate Department in the firm’s Washington, D.C. office and Co-Chair of the firm’s nationaloffice. His practice focuses on capital markets, mergers and acquisitions, securities regulation andgeneral corporate matters. Mr. Trotter represents major New York Stock Exchange and Nasdaqcompanies and counsels issuers and underwriters in the public offering process and in other SEC-related matters. He also serves as special counsel for boards of directors, audit committees and specialcommittees on governance issues, corporate crises and business combination proposals. Inconnection with his service as one of two lawyers on the IPO Task Force, Mr. Trotter served as aprincipal author of the IPO-related provisions of the JOBS Act of 2012.

Eric S. Volkman is a partner in the Washington, D.C. office of Latham & Watkins. He primarilypractices in the areas of white collar criminal defense, internal corporate investigations, trade andeconomic sanctions and complex civil litigation. Mr. Volkman has represented clients facinggovernment investigations into alleged violations of the Foreign Corrupt Practices Act, exportcontrols and trade sanctions, federal securities laws (including insider trading) and a variety of otherregulatory regimes in the government contracting, energy and financial sectors. In addition togovernment-facing investigations, a significant aspect of Mr. Volkman’s practice involves counselingfinancial institutions, institutional investors and other companies on these issues in connection withcross-border M&A and capital markets transactions, as well as third-party diligence. He also assistsclients in designing and implementing compliance programs on these and other topics, both in theUS and abroad.

John D. Watson, Jr. is a partner in the London office of Latham & Watkins and Vice Chair of thefirm’s global Corporate Department. In this role, Mr. Watson is responsible for coordination,resource allocation and strategic development of the firm’s transactional practice in Europe. Mr.Watson’s practice focuses on capital markets transactions, representing issuers and underwriters inRule 144A financings and registered public offerings of common stock and high yield debt. Sincemoving to Europe in 2001, Mr. Watson has focused on the representation of issuers andunderwriters in leveraged finance transactions. He has also represented underwriters in US-registeredIPOs of several European issuers.

Lawrence A. West is a partner in the Washington, D.C. office of Latham & Watkins. His practicefocuses on representing individuals and entities in SEC, Public Company Accounting OversightBoard, and other securities-related enforcement matters, conducting internal investigations, andcounseling corporations and their officers regarding disclosure and corporate compliance issues.Before joining Latham & Watkins in 2006, Mr. West was an Associate Director of the Division ofEnforcement at the SEC, where he worked for 12 years.

Stephen P. Wink is a partner in the New York office of Latham & Watkins and a member of the firm’sCapital Markets, Financial Regulatory, Investment Funds and Mergers & Acquisitions Practices. Hispractice focuses on advising a wide range of market players including investment banks, hedge funds,private equity firms, exchanges, alternative trading platforms and other financial institutions onmatters involving the regulation of broker-dealers and investment advisers, market regulation, andcompliance and enforcement matters.

Chapter 1 Background 1

US Securities Act of 1933; US Securities Exchange Act of 1934 1

JOBS Act 1

Foreign private issuers 1

What is a foreign private issuer? 1

How is US ownership of record determined? 1

When is foreign private issuer status determined and what are the consequences of gaining or losing that status? 1

What are some of the benefits of being a foreign private issuer? 2(i) Ability to use US GAAP, IFRS or local GAAP 2(ii) Quarterly reporting not required; current reporting on Form

8-K not required 2 (iii) Financial information goes “stale” more slowly 2(iv) Ability to submit IPO registration statements confidentially 2(v) Exempt from proxy rules 2(vi) Exempt from Regulation FD 2(vii) Affiliates, directors and officers are exempt from beneficial

ownership reporting and short-swing profit recapture rules 3 (viii) Have more time to file annual reports 3(ix) Exempt from certain aspects of the Sarbanes-Oxley Act 3

Registered and unregistered offerings 3

Chapter 2 Unregistered global offerings – Regulation S, Rule 144A and traditionalprivate placement transactions 5

Regulation S – background 5

Regulation S safe harbor for sales by an issuer, underwriter or affiliate 5(i) Category 1 5(ii) Category 2 5(iii) Category 3 6

Violation of Regulation S safe harbor conditions 6

Rule 144A transactions 6(i) Rule 144A requirements 7(ii) Definition of QIB 7(iii) A/B exchange offers 7

Section 4(a)(2) – traditional private placements 7

Regulation D private placements – Rule 506 safe harbor 7

Regulation D private placements – deviations from Regulation D 8

Title II of the JOBS Act 8

vi Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

CONTENTS

Repealing the ban on general solicitation in Rule 144A and Rule 506 offerings 8

The SEC’s proposed Regulation D rules 9

“Bad actor” disqualification from Rule 506 offerings 9

Restrictions on communications in connection with unregistered global offerings 10

(i) Securities Act Rule 135e – offshore press activity 10(ii) Securities Act Rule 135c – limited notices of unregistered offerings 10(iii) Research reports 10

Use of the internet for unregistered global offerings 11(i) Offshore offering with no concurrent US offering 11(ii) Offshore offering with concurrent US unregistered offering 11

State blue sky issues in unregistered global offerings 11

FINRA filing requirements for private placements 11

Chapter 3 Unregistered resales of Regulation S and privately placed securities 13

Resales of securities 13

Regulation S safe harbor for offshore resales 13

“Section 4(1-1/2)” resales 13

Rule 144 resales 13

Chapter 4 SEC registered offerings 16

Issues to identify before registration 16

Available registration forms 16

ADRs and ADSs 17

NYSE and Nasdaq listing requirements 17

Confidentiality 18

FINRA’s Corporate Financing Rule and related requirements 18

Chapter 5 SEC registered offerings by EGCs under the JOBS Act 20

What is an EGC? 20

Changes to the IPO process 20

Research 20

Elements of the IPO on-ramp 21

Contents vii

Chapter 6 Restrictions on communications in connection with SEC registered offerings 23

Testing the waters by EGCs 23

Restrictions on communications during the quiet period 23

Securities Act Rule 135e – offshore press activity 24

Securities Act Rule 163A – the 30-day bright line safe harbor 24

Securities Act Rule 135 – pre-filing public announcements of a planned offering 24

Securities Act Rule 168 – factual business communications by reporting companies 24

Securities Act Rule 169 – factual business communications by non-reporting companies 25

Rule 163 – pre-filing offers by WKSIs 25(i) Definition of WKSI 25

Restrictions on communications during the waiting period 25

Securities Act Rule 134 – limited post-filing communications 25

Preliminary prospectus (red herring) 26

Road shows 26

Free writing prospectuses 26(i) Overview 26(ii) Securities Act Rule 164(a) – why are FWPs permitted? 26(iii) Securities Act Rule 433(b) – use of FWPs 26(iv) Securities Act Rule 433(f) – media FWPs 27(v) Securities Act Rule 433(c) – what can be in an FWP? 27(vi) Securities Act Rule 433(d) – when must FWPs be filed? 27(vii) Securities Act Rule 164 – certain failures to file and failures

to include the required legend 27

Restrictions on communications after effectiveness of the registration statement; prospectus delivery 28

(i) Prospectus-delivery requirements 28

Research reports 28(i) Definition of research report 28(ii) Rule 137 – publication of research by non-participating

broker-dealers 28(iii) Rule 138 – publication of research by an underwriter on

other securities of an issuer 29(iv) Rule 139 – publication of research about the securities being

offered by an underwriter 29

Chapter 7 Issuer financial statements 31

Background to financial statement requirements 31

What financial statements must be included in public offerings? 31

When does financial information go stale? 33

viii Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

MD&A 34

Using IFRS without reconciliation 34

Reconciliation to US GAAP 35(i) Annual audited and interim unaudited financial statements 35(ii) Selected financial information 35(iii) MD&A 35

Audit reports 35

Currency translation; exchange rates 35

Recent and probable acquisitions 36(i) Overview 36(ii) What is a “business?” 36(iii) What is “probable?” 36(iv) Significance tests 36(v) Summary of financial statement requirements 37(vi) Exceptions to the financial statement requirements for

acquired businesses 38(vii) Industry roll-ups and operating real estate 38(viii) MD&A for acquisitions 38(ix) Pro forma financial information 38(x) Pro forma financial information – certain key content requirements 39

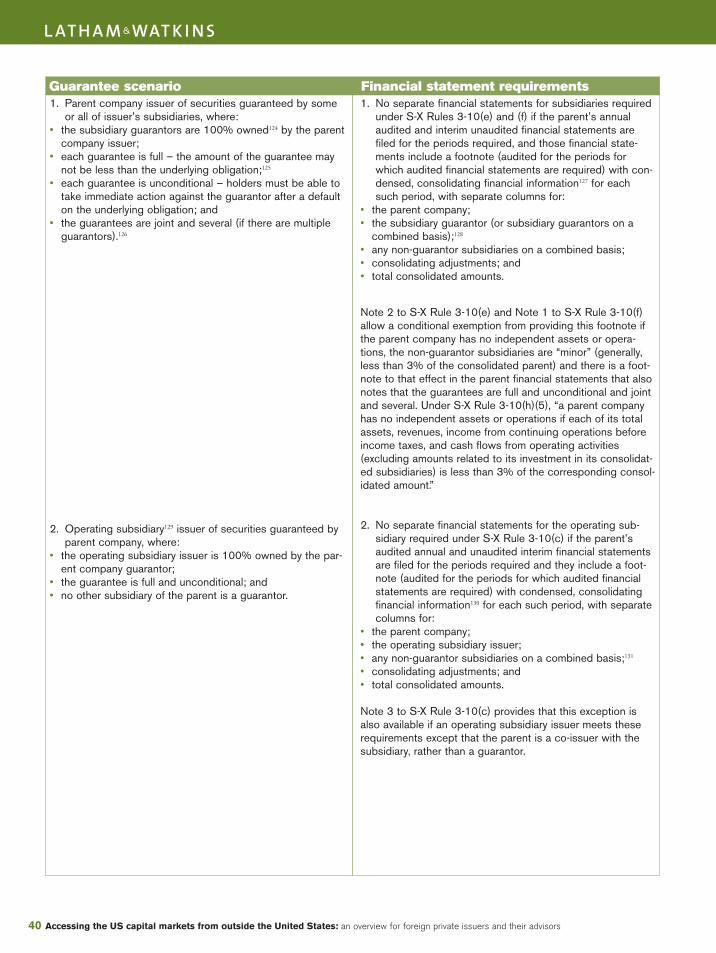

Guarantor financial statements 39

Secured offerings 42

Investments accounted for under the equity method 42

Segment reporting 42

Supplemental schedules for certain transactions 43

Industry guides 43

Quantitative and qualitative disclosure about market risk 44

Item 18 versus Item 17 44

Additional financial information that is typically included 44(i) Other financial data 44(ii) Recent financial results 44(iii) Recent developments 44

Non-GAAP financial measures 45(i) Regulation G 45(ii) S-K Item 10(e) 45(iii) Updated SEC Staff guidance 45

Interactive data 46

Special considerations in Rule 144A transactions 46

Contents ix

Chapter 8 Equity derivatives 53

Examples of corporate equity derivatives transactions 53(i) Structured share repurchases 53(ii) Convertible/exchangeable bond hedge transactions 53(iii) Margin loans 54(iv) Equity swaps 54(v) Variable share forwards and collars 54

Common regulatory issues 54(i) Registration under the 1933 Act 54(ii) Insider trading rules and safe harbor 55(iii) Market manipulation 55(iv) Exchange Act Section 13 reporting requirements 55(v) Regulation M 55(vi) Margin regulations 55(vii) Anti-takeover/antitrust and state takeover regulations 55(viii) The Dodd-Frank Act 55

Conclusion 56

Chapter 9 Cross-border tender and exchange offers—the Tier I and Tier II exemptions; Rule 802 57

The regulatory scheme 57

The Tier I exemption – relief granted 57

The Tier I exemption – requirements 57(i) Foreign private issuer 57(ii) 10% limit 57(iii) Equal treatment of US securities holders 57(iv) Informational documents in the United States 58(v) Limitation on investment companies 58

The Tier II exemption – relief granted 58

The Tier II exemption – requirements 58

Rule 14e-5 – restrictions on purchases outside the tender offer 58(i) Tier I offers 58(ii) Tier II offers 59(iii) All tender offers 59

Rule 802—securities issued in cross-border M&A transactions 59(i) General 59(ii) Requirements of Rule 802 59(iii) State blue sky issues in Rule 802 transactions 60

Chapter 10 Rights offerings under Rule 801 and employee equity compensation plans under Rule 701 63

Securities Act Rule 801 rights offerings 63(i) Background 63(ii) Requirements of Rule 801 63

Securities Act Rule 701—compensatory benefit plans 63(i) Eligible issuers 63(ii) Eligible transactions 63(iii) Eligible plans and participants 64

x Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

(iv) Amounts that may be offered and sold 64(v) Disclosure requirements 64(vi) No integration 64(vii) Resale limitations 64

State blue sky issues in Rule 701 and Rule 801 transactions 64

Chapter 11 Exchange Act registration, reporting and deregistration for foreign private issuers 66

Rule 12g3-2(b) exemption 66

Exchange Act reporting 66(i) Annual report on Form 20-F 66(ii) Current reports on Form 6-K 67(iii) Other consequences of Exchange Act reporting 67

Deregistration under the Exchange Act and termination of reporting 67(i) Alternative 1: 5% average daily trading volume test 67(II) Alternative 2: 300 holder test 67(iii) Additional conditions 67(iv) Terminating Exchange Act reporting for debt securities 67(v) Implications for M&A transactions 68(vi) Interaction with Rule 12g3-2(b) exemption 68(vii) Interaction with Rule 13e-3 68

Reporting by shareholders – obligations of major shareholders to file Schedule 13D or 13G reports 68

(i) Schedule 13D 68(ii) Schedule 13G 68(iii) Amendments to Schedule 13D or 13G reports 68

Filing electronically 69

Chapter 12 The US Sarbanes-Oxley Act of 2002 71

Who is subject to Sarbanes-Oxley? 71

Section 404 – internal control over financial reporting 71

Disclosure controls and procedures 71

Certification requirements – Sections 302 and 906 71

Listed company audit committees – Rule 10A-3 71

Loans to executives – Section 402 72

Forfeiture of bonuses – Section 304 72

Audit committee financial expert 72

Attorney conduct – Part 205 73

Regulation BTR 73

Contents xi

Chapter 13 Selected issues under the Dodd-Frank Act 75

Conflict minerals 75(i) What are conflict minerals and where are they found? 75(ii) What does manufacture or contract to manufacture mean? 75(iii) What is the meaning of necessary to the functionality or

production of a product? 75(iv) Form SD – due date 75(v) Form SD – Conflict Minerals Disclosure and Conflict Minerals Report 75(vi) Form SD – transitional relief 76

Payments by resource extraction issuers 76(i) “Commercial development of oil, natural gas, or minerals” 76(ii) Required disclosures 76(iii) Disclosures on Form SD 77(iv) Compliance date 77

Compensation committee listing standards 77(i) Exemptions for foreign private issuers 77(ii) Compensation committee independence 77(iii) Authority to retain and compensate compensation consultants,

independent legal counsel and other compensation advisers 77(iv) Independence of compensation consultants and other advisers 77(v) Compliance date 77

Chapter 14 Liability under the US federal securities laws for foreign private issuers 79

Registration—Section 5 of the Securities Act 79

Anti-fraud 79(i) What is material? 79(ii) Rule 10b-5 – fraud in connection with the purchase or sale

of securities 80a. Elements of a claim under Rule 10b-5 80b. Scope of Rule 10b-5 80c. Insider trading 80d. Damages under Rule 10b-5 80e. Extraterritorial application of Section 10(b) and Rule 10b-5 81

(iii) Section 11 of the Securities Act—registered offerings 81(iv) Section 12(a)(2) of the Securities Act—registered offerings 81

a. Rule 159—timing of the investment decision under Section 12(a)(2) 82

Liability considerations in connection with pending M&A transactions 82

Controlling person liability 82

PSLRA safe harbor 83

Enforcement 83(i) Background 83(ii) Enforcement against foreign private issuers and non-US nationals 83

Chapter 15 Activities of non-US broker-dealers in the United States 87

Background 87

What is a “broker-dealer?” 87

The Rule 15a-6 safe harbor 87

xii Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

Permitted activities under Rule 15a-6 – without a Chaperoning Arrangement 88(i) Unsolicited transactions 88(ii) Activities with certain specified counterparties 88 (iii) Provision of research reports to major US institutional investors 88

Permitted activities under Rule 15a-6 – with a Chaperoning Arrangement 89(i) Contacts with major US Institutional Investors from outside

the United States 89(ii) Contacts with US Institutional Investors (non-majors) from outside

the United States 89(iii) In-person US visits 89(iv) Access to screen-based quotations 89

Key requirements with respect to the establishment of a Chaperoning Arrangement 89

(i) Certain requirements applicable to the Non-US BD and its personnel 89

(ii) Certain responsibilities of the chaperoning broker-dealer under the Chaperoning Arrangement 89

Chapter 16 US restrictions on interactions between investment banking personnel and research analysts 92

Background 92

Regulation AC 92

FINRA Rules – NASD Rule 2711 and incorporated NYSE Rule 472 92(i) Restrictions on research analyst compensation 92(ii) Prohibition of quid pro quo research and participation in

sales meetings 93(iii) Chaperone provisions 93(iv) Restrictions on publishing research reports and making public

appearances following certain offerings 93(v) Disclosure requirements 94

Global Research Analyst Settlement 94

Chapter 17 The Prospectus Directive (Directive 2003/71/EC) 97

When the PD applies 97

Exemptions 97

Basic disclosure regime 97

Divergence from US requirements 100

Approval of the prospectus and passporting within the EEA 100

Chapter 18 The US Investment Company Act of 1940 102

Background 102

Can an operating company be an investment company? 102

Investment company definition; the 40% test 103(i) 40% test – what is an investment security? 103(ii) 40% test – value 103(iii) 40% test – cash items 103

Contents xiii

Rule 3a-1 safe harbor; 45% tests 103

Additional exceptions and exemptions 104

Exceptions and exemptions based on characteristics of the issuer 104(i) Issuers primarily engaged in non-investment activity –

Sections 3(b)(1) and 3(b)(2) 104(ii) Broker-dealers – Section 3(c)(2) 104(iii) Banks and insurance companies – Section 3(c)(3) and Rule 3a-6 104(iv) Transient investment companies – Rule 3a-2 105(v) Finance subsidiaries – Rule 3a-5 105(vi) Research and development companies – Rule 3a-8 105

Exceptions and exemptions based on transaction structure 106(i) 100 holders – Section 3(c)(1) 106(ii) Qualified purchasers – Section 3(c)(7) 106

Exemptive orders 106

Chapter 19 Some additional relevant laws; self-regulatory organizations 109

Foreign Corrupt Practices Act 109

OFAC; US sanctions 109

Anti-money laundering; PATRIOT Act 109

Investment Advisers Act of 1940 110

Self-regulatory organizations; FINRA membership 110

US federal tax laws; passive foreign investment companies 110

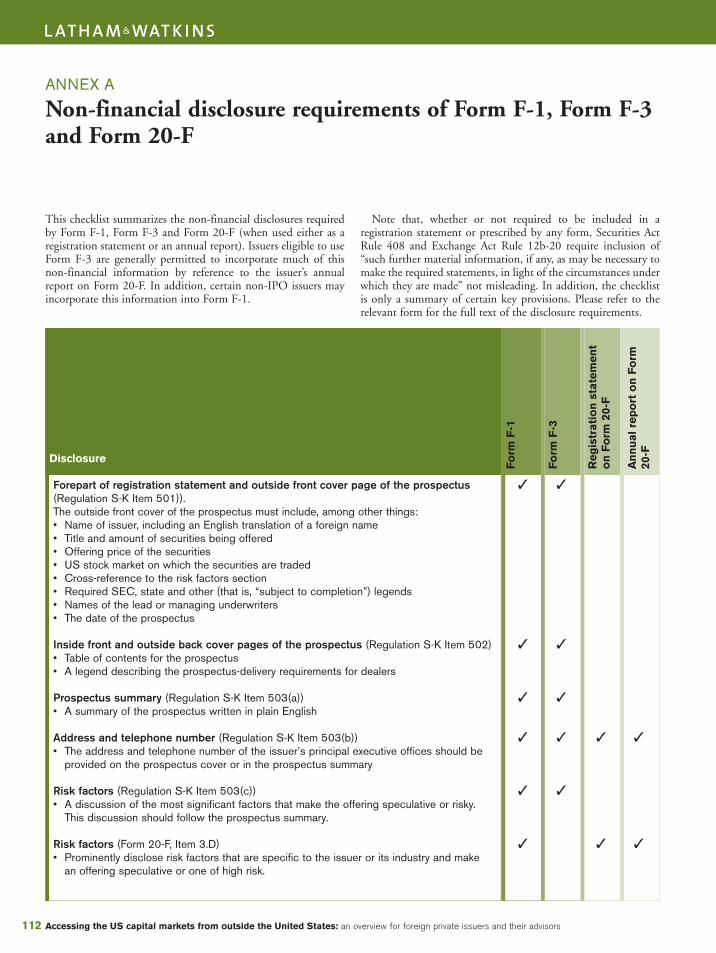

Annex A Non-financial disclosure requirements of Form F-1, Form F-3 and Form 20-F 112

Annex B NYSE quantitative listing criteria and corporate governance standards 133

Annex C Nasdaq quantitative listing criteria and corporate governance standards 141

Annex D MD&A 151

xiv Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

2013 EDITION

Accessing the US capital markets from outside theUnited States: an overview forforeign private issuers andtheir advisors

Fabry-Pérot Interferometer, SA is a highly successful non-US company known to the world as FPI.FPI is considering doing a debt or equity offering in the United States. What are the key legal issuesit, and its underwriters or financial advisors, are likely to face?This book was written to help answerthat question. Our aim is to help the FPIs of the world and their investment bankers understandbetter the regulatory regime applicable to capital-raising activities in the United States.

US regulation of securities offerings is quite complex, and may appear overwhelming to an issueraccessing the US capital markets for the first time. In order to make the maze of US regulations abit more manageable, we have chosen in this book to focus only on those aspects of US law that, inour experience, are most relevant to US capital markets transactions involving non-US companies.Taking this approach means we have had to be selective – for example, we do not address the separateregimes that apply to offerings by certain Canadian-domiciled issuers, non-US governments andregistered investment companies. And, we do not attempt to provide a detailed analysis of every legalissue or every regulatory regime (such as, for example, those that may apply to companies engagedin business in highly regulated areas like banking, communications or utilities) a non-US companymay face. But we think our approach strikes the appropriate balance between a simple issues outlineand a typical multi-volume treatise and, as such, hope you will find this book to be a useful – andmore user-friendly – resource for those wishing to enter and navigate these waters.

Before we delve further into our topic, just an additional word about format. We have includedvarious “Practice Points” throughout the book to highlight certain key items we think are helpful tokeep in mind as the proposed transaction takes shape and you begin to formulate your strategy. Asa necessary evil, we have also included extensive endnotes, which include references to the primarysource materials and are quite handy when trying to recall the basis for, or evolution of, a particularposition. (Of course, the underlying statutes, rules, regulatory interpretations and the like are subjectto change and should always be consulted anew for each proposed transaction, and this book shouldnot be relied on as providing definitive advice with respect to any particular transaction or situation.)

Preface xv

US Securities Act of 1933; US SecuritiesExchange Act of 1934The starting place for understanding the US regulatory regimegoverning capital markets transactions is two US federalstatutes: the US Securities Act of 1933 (the Securities Act or1933 Act) and the US Securities Exchange Act of 1934 (theExchange Act or the 1934 Act). The Securities Act generallygoverns the initial offer and sale of securities in the UnitedStates, while the Exchange Act generally regulates the post-issuance trading of securities, the activities of certain marketparticipants such as underwriters and broker-dealers andongoing public reporting and merger and acquisition (M&A)transactions such as exchange offers and tender offers.

The US Securities and Exchange Commission (the SEC orthe Commission) has issued a comprehensive body of rules andregulations under the Securities Act and the Exchange Act thathave the force of law. The SEC and its Staff have also providedinterpretive guidance on a wide range of questions under thesecurities laws.

JOBS ActIn April 2012, the Jumpstart Our Business Startups Act (JOBSAct) became law. The JOBS Act made significant changes to theUS securities laws in a wide variety of areas. Above all, it createda new category of issuer, called an emerging growth company(EGC). EGCs benefit from a various accommodations designedto make the initial public offering (IPO) process more attractiveand to ease the transition from private to public company. Non-US companies can be EGCs, and we discuss the JOBS Act inmore detail below.

Foreign private issuersThe US securities laws draw a key distinction between domesticand non-US companies, and in particular a category of non-UScompanies known as “foreign private issuers” (FPIs). Thereference to “issuer” means an issuer of securities (presumablyin the US capital markets) while the reference to “private” isonly designed to draw a distinction with foreign governments –it has nothing to do with the difference between publicly tradedand privately traded companies. Importantly, a non-UScompany that is publicly traded can still be a foreign privateissuer.

We’ll start with some basic concepts – what is a foreignprivate issuer and how does it differ from its US domesticrelative?

What is a foreign private issuer?A foreign private issuer is an entity (other than a foreigngovernment) incorporated or organized under the laws of ajurisdiction outside of the US unless1:• more than 50% of its outstanding voting securities are

directly or indirectly owned of record by US residents; and• any of the following applies:

- the majority of its executive officers or directors are US

citizens or residents;- more than 50% of its assets are located in the United

States; or- its business is administered principally in the United

States.

How is US ownership of record determined?In order to determine the percentage of outstanding votingsecurities held “of record” by US residents, a company shouldbegin with a review of the addresses of its security holders in itsrecords.2 But the inquiry does not end there. In particular, thecompany first needs to look past institutional custodians (such asthe Depository Trust Company, or DTC, and its nominee, Cede& Co.) and other commercial depositories (such as Euroclear andClearstream) to identify participants in those systems (such asbroker-dealers, banks and nominees). Then, it must drill downbeyond certain “street name” accounts – that is, accounts held ofrecord by a broker-dealer, bank or nominee located in3:• the United States;• the company’s jurisdiction of incorporation; and • the jurisdiction that is the company’s primary trading market

for its voting securities (if different than the jurisdiction ofincorporation).In the case of these securities, the number of separate accounts

for which the securities are held should be counted.4

A company may rely in good faith on information as to thenumber of these separate accounts supplied by the broker-dealer,bank or nominee.5 If, after reasonable inquiry, the company isunable to obtain information about the amount of securitiesrepresented by accounts of customers resident in the UnitedStates, it may assume that these customers are residents of thejurisdiction in which the nominee has its principal place ofbusiness.6

When is foreign private issuer status determined and what are the consequences ofgaining or losing that status?Under Exchange Act Rule 3b-4, for a company that is registeringwith the SEC for the first time, the determination of whether anissuer qualifies as a foreign private issuer is made as of a datewithin 30 days prior to the filing of the initial registrationstatement. Thereafter, it must test its status annually, at the endof its most recently completed second fiscal quarter.

Once a company qualifies as a foreign private issuer, it isimmediately able to use the forms and rules designated forforeign private issuers. For example, a company that reports as a

An issuer that has more than 50% US ownership can stillbe a foreign private issuer. To fail to qualify as a foreign pri-vate issuer, a company needs to be both majority owned byUS residents and meet any one of the three additional testsnoted above.

PRACTICE POINT

Background 1

CHAPTER 1

BackgroundAlexander F. Cohen, Dana G. Fleischman, Antti V. Ihamuotila and Jeffrey H. Lawlis

domestic US issuer but subsequently determines that it qualifiesas a foreign private issuer as of the end of its second fiscal quarterwould no longer need to continue making Form 8-K and Form10-Q filings for the remainder of that fiscal year. Instead, it couldimmediately begin furnishing reports on Form 6-K and wouldfile an annual report on Form 20-F (rather than Form 10-K).

By contrast, if an issuer does not qualify as a foreign privateissuer at the end of its second fiscal quarter, it nonethelessremains eligible to use the forms and rules for foreign privateissuers until the end of that fiscal year – in other words, it doesnot lose its status as a foreign private issuer until the first day ofthe next fiscal year. Once an issuer fails to qualify as a foreignprivate issuer, it will be treated as a domestic US issuer unless anduntil it requalifies as a foreign private issuer as of the last businessday of its second fiscal quarter.

Take the example of a calendar year company that does notqualify as a foreign private issuer as of the end of its second fiscalquarter in 2013. It would not become subject to quarterlyreporting on Form 10-Q during 2013. However, it would berequired to file its annual report on Form 10-K in 2014 in respectof its 2013 fiscal year on the same timetable as a domestic UScompany. It would also become subject to the proxy rules,reporting of beneficial ownership of securities by officers,directors and beneficial owners of more than 10% of a class ofequity securities of the issuer, and reporting on Form 8-K andForm 10-Q as of the first day of 2014.7

What are some of the benefits of being a foreign private issuer?Foreign private issuers are allowed a number of key benefits notavailable to domestic US issuers, including the following:

(i) Ability to use US GAAP, IFRS or local GAAP Domestic US issuers must file financial statements with the SECin accordance with US generally accepted accounting principles(US GAAP).8 The financial statements of foreign private issuers,however, may be prepared using US GAAP, InternationalFinancial Reporting Standards (IFRS), or local home-countrygenerally accepted accounting principles (local GAAP).9 In thecase of foreign private issuers that use the English-languageversion of IFRS as issued by the International AccountingStandards Board (IASB IFRS), no reconciliation to US GAAP isneeded.10 By contrast, if local GAAP or non-IASB IFRS is used,the consolidated financial statements (both annual and interim)must include a note reconciliation to US GAAP.11

(ii) Quarterly reporting not required; current reportingon Form 8-K not required Unlike domestic US issuers, foreign private issuers are notrequired to file quarterly reports (including quarterly financialinformation) on Form 10-Q.12 They also are not required to useForm 8-K for current reports, and instead furnish (not file)current reports on Form 6-K with the SEC.13 Some foreignprivate issuers, however, choose (or are required by contract) tofile the same forms with the SEC that domestic US issuers use. Inthat case, they must comply with the requirements of the formsfor domestic issuers (and would file quarterly reports on Form10-Q and current reports on Form 8-K, in addition to annualreports on Form 10-K).14

(iii) Financial information goes “stale” more slowly The SEC’s rules also allow a foreign private issuer’s registrationstatement to contain financial information that is of an earlierdate than that allowed for domestic US issuers. In particular,foreign private issuers can omit interim unaudited financialstatements if a registration statement becomes effective less thannine months after the end of the last audited fiscal year (unlessthe issuer has already published more current interim financialinformation).15 After that time, a foreign private issuer mustprovide interim unaudited financial statements (which may beunaudited) covering at least the first six months of the fiscal year,together with comparative financial statements for the sameperiod in the prior year.16

(iv) Ability to submit IPO registration statementsconfidentially Certain foreign private issuers that are registering for the firsttime with the SEC may submit draft registration statements on aconfidential basis to the SEC Staff. In particular, a foreign privateissuer may submit its IPO registration statement on aconfidential basis if it: • qualifies as an EGC;• is listed or is concurrently listing its securities on a non-US

securities exchange – i.e., a foreign private issuer that is notsolely listing in the United States;

• is being privatized by a foreign government; or • can “demonstrate that the public filing of an initial registration

statement would conflict with the law of an applicable foreignjurisdiction.”17

By contrast, domestic US issuers that are not EGCs must fileregistration statements publicly.

Confidential submission can be a significant advantage becausethe procedure allows the complicated issues often encountered inan initial SEC review to be resolved behind closed doors. Aforeign private issuer will still be required to file its initialregistration statement and all amendments publicly prior beforegoing on a road show or selling its securities.18 A confidentialsubmission to the SEC with respect to an offering in the UnitedStates will trigger filing requirements under the CorporateFinancing Rule, Rule 5110, of the Financial Industry RegulatoryAuthority, Inc. (FINRA) unless the offering satisfies an exceptionfrom filing under that Rule, as discussed in more detail below.

(v) Exempt from proxy rulesThe US proxy rules – which specify the procedures and requireddocumentation for soliciting shareholder votes – are notapplicable to foreign private issuers.19

(vi) Exempt from Regulation FDRegulation FD provides that when a domestic US issuer, orsomeone acting on its behalf, discloses material non-publicinformation to certain persons (including securities analysts,other securities market professionals and holders of the issuer’ssecurities who could reasonably be expected to trade on the basisof the information), it must make simultaneous public disclosureof that information (in the case of intentional disclosure) orprompt public disclosure (in the case of non-intentionaldisclosure). Foreign private issuers are expressly exempt fromRegulation FD.20

2 Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

(vii) Affiliates, directors and officers are exempt frombeneficial ownership reporting and short-swing profitrecapture rules Under Section 16(a) of the Exchange Act, anyone who ownsmore than 10% of any class of equity security registered underthe Exchange Act, or who is an officer or director of an issuer ofsuch a security, must file a statement of beneficial ownershipwith, and report changes in beneficial ownership to, the SEC.Similarly, Section 16(b) requires any such shareholder, officer ordirector to disgorge to the issuer profits realized on purchases andsales within any period of less than six months. Securities offoreign private issuers are exempt from Section 16.21

(viii) Have more time to file annual reportsAnnual reports on Form 10-K by domestic US issuers are duewithin 60, 75 or 90 days after the end of the issuer’s fiscal year,depending on whether the company is a “large accelerated filer,”“accelerated filer” or a non-accelerated filer.22 By contrast, foreignprivate issuers may file annual reports on Form 20-F within fourmonths after the end of their fiscal year.23

(ix) Exempt from certain aspects of the Sarbanes-Oxley ActThe Sarbanes-Oxley Act of 2002 (the Sarbanes-Oxley Act orSarbanes-Oxley) made broad revisions to the US federalregulation of public companies and their auditors. Although theact itself generally did not distinguish between domestic USissuers and foreign private issuers, the SEC has, in its rulesimplementing Sarbanes-Oxley, made a number of significantexemptions for the benefit of foreign private issuers.

Registered and unregistered offeringsThe Securities Act requires registration with the SEC of anytransaction involving the offer or sale of a security, unless thesecurity is of a type that is exempt from registration or thetransaction is structured to take advantage of an availableexemption from registration. The terms “offer,” “sale” and“security” are very broadly defined.

As we discuss in more detail below, registered transactionsinvolve filing a registration statement with the SEC and meetingdetailed and specific disclosure and financial statementrequirements. In addition, registered transactions trigger thewide-ranging provisions of the Sarbanes-Oxley Act and acomprehensive liability scheme.

By contrast, the requirements of unregistered transactions aregenerally – but not invariably – less demanding. A foreign privateissuer will not typically become subject to Sarbanes-Oxley merelyby issuing securities in an unregistered transaction, and theliability regime governing unregistered transactions is morecircumscribed.

The decision whether to issue securities in a registered orunregistered transaction involves balancing business and legalobjectives. Broadly speaking, registered transactions are morecomplex, time-consuming and carry greater liability risks.However, not all securities issuances can take the form of anunregistered transaction. For example, if a foreign private issuerwishes to list its securities on a US securities exchange, or to makea public offering of securities to retail investors in the US, thetransaction will have to be registered.

Foreign private issuers that file reports with the SEC typi-cally choose to comply with Regulation FD (at least in part),particularly since the restrictions in their home jurisdictionsin many cases overlap with Regulation FD’s requirements.

PRACTICE POINT

Regardless of the exemption from Regulation FD, foreignprivate issuers remain exposed to potential liability fromselective disclosure, for example from “tipping” securitiesanalysts or selected shareholders.

PRACTICE POINT

Background 3

1. Securities Act Rule 405; Exchange Act Rule 3b-4.2. Instruction to paragraph (c)(1) of Exchange Act Rule 3b-4;

Instructions to paragraph (1) of the definition of “Foreignprivate issuer” in Securities Act Rule 405. Note that theseinstructions send the reader to Exchange Act Rule 12g3-2(a),which in turn refers to Exchange Act Rule 12g5-1.

3. Instruction to paragraph (c)(1) of Exchange Act Rule 3b-4;Instructions to paragraph (1) of the definition of “Foreignprivate issuer” in Securities Act Rule 405.

4. Exchange Act Rule 12g3-2(a)(1).5. Id.6. Instruction (i) to paragraph (c)(1) of Exchange Act Rule 3b-4;

Instruction (b) to paragraph (1) of the definition of “Foreignprivate issuer” in Securities Act Rule 405. Cf. Final Rule:International Disclosure Standards, Release No. 33-7745(September 30, 2000) at II.E (issuer may rely on a presumptionthat customer accounts are held in the nominee’s principal placeof business if the nominee’s charge for supplying theinformation would be unreasonable).

7. See SEC Division of Corporation Finance, Financial ReportingManual, Section 6120.2 [Financial Reporting Manual].

8. See Regulation S-X Rule 4-01(a)(1) [S-X] (financial statementsof domestic US issuers not prepared in accordance with“generally accepted accounting principles” are presumed to bemisleading or inaccurate); see also Financial Reporting Manual,Section 1410.1 (US domestic issuers must follow Regulation S-X and US GAAP).

9. S-X Rule 4-01(a)(2).10. Final Rule: Acceptance from Foreign Private Issuers of Financial

Statements Prepared in Accordance with International FinancialAccounting Standards Without Reconciliation to US GAAP,Release No. 33-8879 (December 21, 2007) [IFRS ReconciliationRelease]; see also Financial Reporting Manual, Section 6310.1. Inthis case, the accounting policy footnote must state compliancewith IASB IFRS and the auditor’s report must opine oncompliance with IASB IFRS. Financial Reporting Manual,Section 6310.2.

11. See Form 20-F, Items 17(c), 18.12. Exchange Act Rule 13a-13(b)(2).

13. See Exchange Act Rule 13a-11(b); see also Exchange Act Rule13a-16(c) (reports on Form 6-K are furnished, not filed).

14. See Exchange Act Rule 13a-16(a)(3); see also Financial ReportingManual, Section 6120.1 (if a foreign private issuer elects to doso, “it must comply with all the requirements of the ‘domesticcompany’ forms”).

15. See Form 20-F, Item 8(a)(5); Financial Reporting Manual,Sections 6220.1, 6220.6.

16. See Form 20-F, Item 8(a)(5).17. See Staff of the Division of Corporation Finance, Non-Public

Submissions from Foreign Private Issuers (December 8, 2011,updated May 30, 2012).

18. A foreign private issuer that submits its IPO registrationstatement on a confidential basis as an EGC may not commenceits IPO road show until at least 21 days after publicly filing theinitial confidential submission and all confidentially submittedamendments. A foreign private issuer that is not an EGC but isotherwise eligible to submit its IPO registration statementconfidentially does not need to comply with this 21-dayrequirement but is still required to publicly file its previousconfidential submissions prior to its road show. A foreign privateissuer that qualifies as an EGC and would also be entitled tosubmit its draft registration statement for confidential review ifit were not an EGC does not need to comply with the 21-dayrequirement, so long as the issuer does not take advantage of anybenefit available to EGCs under the JOBS Act. Staff of theDivision of Corporation Finance, Jumpstart Our BusinessStartups Act Frequently Asked Questions: Generally ApplicableQuestions on Title I of the JOBS Act, Question 9 (April 16, 2012,updated May 3, 2012 and September 28, 2012).

19. Exchange Act Rule 3a12-3(b).20. Regulation FD, Rule 101(b)(ii).21. Exchange Act Rule 3a12-3(b). These securities remain subject to

the beneficial ownership reporting requirements of Sections13(d) and 13(g).

22. See Form 10-K, General Instruction A(2); see also Exchange ActRule 12b-2 (defining the terms “large accelerated filer” and“accelerated filer”).

23. Form 20-F, General Instruction A(b)(2).

4 Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

ENDNOTES

Global offerings that are not registered in the UnitedStates with the SEC are typically structured to takeadvantage of a combination of exemptions. Theportion of the transaction sold to investors outside the

United States will be designed to comply with the safe harbor foroffshore transactions provided by Securities Act Regulation S. At thesame time, the portion sold to US investors will be structured tocomply with the safe harbor of Securities Act Rule 144A for resalesto certain large US institutional investors known as qualifiedinstitutional buyers (QIBs), or (generally for smaller transactions),the private placement exemptions of Section 4(a)(2) of theSecurities Act or Securities Act Regulation D.

We discuss these exemptions below.

Regulation S – background Regulation S provides a safe harbor from Securities Act registrationrequirements for certain offerings outside the United States andoffshore resales of securities. If the conditions of Regulation S aremet, the transaction is deemed to take place outside the UnitedStates and hence does not trigger the registration requirements ofSection 5 of the Securities Act.1

All Regulation S transactions start with the same basicrequirements, set out in Rule 903. Then, Regulation S layers onadditional restrictions depending on the nature of the issuer.

The basic requirements are that:• the offer or sale must be made in an “offshore transaction;” and• there must be no “directed selling efforts” in the United States.

We refer to these below as the Regulation S Basic Conditions.An “offshore transaction” is defined as an offer that is not made

to a person in the United States, and either:2

• at the time the buy order is originated, the buyer is outside theUnited States or the seller (and any person acting on the seller’sbehalf) reasonably believes that the buyer is outside of the UnitedStates;

• for purposes of the issuer safe harbor, the transaction is executedin, on or through the physical trading floor of an establishedforeign securities exchange located outside of the United States;or

• for purposes of the resale safe harbor, the transaction is executedin, on or through the facilities of a designated offshore securitiesmarket and neither the seller (nor any person acting on the seller’sbehalf) knows that the transaction has been prearranged with abuyer in the United States.The term “directed selling efforts” is broadly defined to include

any activities that have, or can reasonably be expected to have, theeffect of conditioning the market in the United States for thesecurities being offered in reliance on Regulation S.3 Prohibited

efforts include mailing offering materials into the United States,conducting promotional seminars in the United States, grantinginterviews about the offering in the United States (including bytelephone), or placing advertisements with radio or televisionstations broadcasting in the United States.4 Importantly, sellingactivities in the United States in connection with concurrent USofferings – whether registered or private – do not constitute directedselling efforts.5 More generally, offshore transactions in compliancewith Regulation S are not integrated with registered or exempt USdomestic offerings.6

Regulation S safe harbor for sales by an issuer,underwriter or affiliateRule 903 of Regulation S provides a safe harbor for sales by issuers,“distributors” (essentially, entities that act as underwriters for theissuer) and most affiliates of the issuer (other than certain officersand directors). Bear in mind that the term “affiliate” is defined verybroadly, and it is not always simple to determine precisely who isand who is not an affiliate.

Under Rule 903, there are three levels or “categories” ofrequirements, with Category 1 being the least burdensome andCategory 3 being the most restrictive.

(i) Category 1Category 1 has no requirements other than the Regulation S BasicConditions. It is available for:• securities offered by foreign issuers7 who reasonably believe at the

commencement of the offering that there is no “substantial USmarket interest”8 in the securities offered;

• securities offered and sold in an “overseas directed offering;”9

• securities backed by the full faith and credit of a foreigngovernment; or

• securities offered and sold pursuant to certain employee benefitplans established and administered under the laws of a foreigncountry.

(ii) Category 2Category 2 covers securities that are not eligible for Category 1 andthat are either (1) equity securities10 of a foreign issuer that is areporting company under the Exchange Act or (2) debt securities11

of Exchange Act reporting issuers (domestic or foreign) and non-

Even if Category 1 is available, market practice for debtofferings is often to follow Category 2 restrictions wherethere is a concurrent Rule 144A offering.

PRACTICE POINT

Unregistered global offerings 5

CHAPTER 2

Unregistered global offerings –Regulation S, Rule 144A and traditionalprivate placement transactionsAlexander F. Cohen, Bryant B. Edwards, Mark A. Stegemoeller, Michael W. Sturrock and John D. Watson, Jr.

reporting foreign issuers. Issuers in this category may take advantageof the safe harbor if the following conditions are met along with theRegulation S Basic Conditions:• Certain “offering restrictions”12 must be adopted, including:

- Each distributor must agree in writing that all offers and salesduring a 40-day distribution compliance period may be madeonly in accordance with safe harbors under Regulation S,pursuant to registration under the Securities Act or anexemption from registration.

- Prospectuses, advertisements, and all other offering materialsand documents (other than press releases) used in connectionwith offers and sales during the distribution compliance periodmust disclose that the securities are not registered under theSecurities Act and cannot be sold in the United States or to USpersons (other than distributors) unless so registered or anexemption from registration is available.13

- During the 40-day distribution compliance period, offers andsales of the security cannot be made to a US person other thana distributor.

- Any distributor selling securities to another distributor, dealer,or person receiving a selling commission must deliver, duringthe 40-day distribution compliance period, a confirmation ornotice to the purchaser stating that the purchaser is subject tothe same resale restrictions as the distributor.

The 40-day distribution compliance period begins on the later ofthe date of the closing or the date on which securities were firstoffered to persons other than distributors (generally, the pricingdate).14

(iii) Category 3Category 3 is a catch-all and has the most restrictive conditions. Itincludes all securities that are not eligible for Category 1 or 2, suchas any securities of a voluntary filer or a non-reporting domestic USissuer, equity securities of a reporting domestic US issuer and equitysecurities of a non-reporting foreign issuer (with substantial USmarket interest in the equity securities of that issuer). In addition tothe Regulation S Basic Conditions, an issuer must also meet thefollowing requirements:• Each of the offering restrictions described above for Category 2

must be met,15 except that a one-year distribution complianceperiod (or six-month distribution compliance period forreporting issuers) applies to offerings of equity securities and a40-day distribution compliance period applies to offerings ofdebt securities.

• During the applicable distribution compliance period, offers orsales cannot be made to a US person other than a distributor(although exempt sales, such as those pursuant to Rule 144A,may be made) and, in the case of equity securities:- the purchaser (other than a distributor) must certify that it is

not a US person;- the purchaser must agree to resell the securities only in

accordance with Regulation S, pursuant to registration underthe Securities Act or an exemption from registration; and

- certain other restrictions must be satisfied, including aprohibition against corporate registration of transfers not madein accordance with Regulation S.

• Debt securities generally must be represented upon issuance by atemporary global security not exchangeable for definitivesecurities until the expiration of the 40-day distributioncompliance period and, for persons other than distributors, untilcertification of beneficial ownership by a non-US person.

• Any distributor selling the securities to another distributor,

dealer, or person receiving a selling commission must deliver,during the applicable distribution compliance period, a notice orconfirmation to the purchaser stating that the purchaser is subjectto the same resale restrictions as the distributor.

Violation of Regulation S safe harbor conditionsThe consequences of a breach of the conditions for use ofRegulation S could be significant, since this would potentially allowbuyers of the securities to rescind their purchases.21 If an issuer,distributor, any of their respective affiliates or any person acting ontheir behalf fails to comply with the Regulation S Basic Conditions,then the issuer safe harbor will not be available to any person inconnection with the offer or sale of the securities. However, if anyof these persons fails to comply with any of the other issuer safeharbor requirements (in other words, other than the Regulation SBasic Conditions), then only the party who fails to comply (as wellas its agents and affiliates) will be unable to rely on the issuer safeharbor exemption. In that case, the fact that there may have been abreach on the part of the issuer, distributor, their affiliates or agents(other than certain officers or directors relying on the resaleexemption) does not generally negate a resale safe harbor exemptionfor an unaffiliated person.22

Rule 144A transactionsAlthough market participants often refer to Rule 144A offerings, asa technical matter most Rule 144A transactions involve two steps.These are sales to initial purchasers under an exemption such asRegulation S or Regulation D (discussed below), followed by resalesto QIBs under Rule 144A. As a result, Rule 144A transactionsfollow various limitations not found directly in Rule 144A itself aswell as the explicit requirements of Rule 144A.

Equity securities issued by a domestic US issuer (whetherreporting or non-reporting) pursuant to Regulation S areconsidered “restricted securities”16 subject to limitations onresale, and they remain restricted securities even after anexempt resale pursuant to Regulation S.17 As a practicalmatter, these restrictions have limited the use of RegulationS for exempt sales of equity securities by domestic USissuers.

PRACTICE POINT

A foreign private issuer that is a reporting issuer with theSEC may be required to furnish a copy of an offering mem-orandum relating to a Regulation S offering on Form 6-K (if,for example, it files that offering memorandum with a stockexchange on which its securities are listed, and theexchange makes the offering memorandum public). This willgenerally not constitute directed selling efforts.18

PRACTICE POINT

The safe harbors of Regulation S are not exclusive and par-ties may use any other applicable exemptions provided bythe Securities Act.19 Regulation S only applies to the regis-tration requirements of the Securities Act and does not limitthe applicability of the US federal anti-fraud laws or anystate laws relating to securities offerings.20

PRACTICE POINT

6 Accessing the US capital markets from outside the United States: an overview for foreign private issuers and their advisors

(i) Rule 144A requirementsThe requirements for a valid Rule 144A transaction include:• Sales to QIBs: the securities must be offered and sold only to

QIBs or to a person who the seller (and any person acting on itsbehalf) “reasonably believes” is a QIB;

• Notice to buyers: the seller (and any person acting on its behalf)must take “reasonable steps” to ensure that the buyer is aware thatthe seller may be relying on Rule 144A (generally by so noting inthe offering memorandum, or in the trade confirmation in thecase of an undocumented offering);

• Fungibility: the securities must not be, when issued, of the sameclass as securities listed on a US national securities exchange (or,in the case of convertible or exchangeable securities, have aneffective conversion premium of 10% or more); and

• Information delivery: if the issuer is a reporting company underthe Exchange Act or is exempt from reporting under ExchangeAct Rule 12g3-2(b), a seller wishing to resell the securities is notobligated to furnish the purchaser with information concerningthe issuer. However, if the issuer is not a reporting company andis not exempt under Exchange Act Rule 12g3-2(b), a holder orthe purchaser must have the right to obtain from the seller or theissuer, upon request, certain minimal “reasonably current”information concerning the business of the issuer and its financialstatements.

(ii) Definition of QIBA QIB is defined in Rule 144A to include any of the followingentities acting for its own account or the account of other QIBs thatin the aggregate owns and invests on a discretionary basis at least$100 million in securities of issuers that are not affiliated with theQIB:• US-regulated insurance companies;• investment companies registered under the US Investment

Company Act of 1940 (the Investment Company Act);• small business investment companies licensed by the US Small

Business Administration;• certain employee benefit plans;• certain trusts;• certain tax-exempt organizations and corporations;• certain registered investment advisers;• certain registered broker-dealers; and• US banks and savings and loan associations, and non-US banks,

savings and loan associations, and equivalent institutions.

(iii) A/B exchange offersRule 144A is particularly popular for global offerings of debtsecurities, in part because of a line of SEC Staff no-action letters thatpermits issuers who have sold debt securities to QIBs pursuant toRule 144A subsequently to register an exchange offer of identicalsecurities for the Rule 144A securities.24 This procedure allowsQIBs, subject to limited exceptions, to obtain freely tradableregistered securities in exchange for the restricted, legendedsecurities they obtained in the Rule 144A offering. Because theexchange offer will go through the SEC registration process, most

issuers and underwriters seek to conform the original Rule 144Aoffering memorandum as closely as possible to the requirements ofa full registration statement.

The availability of this exchange procedure allows issuers andunderwriters to complete transactions quickly under Rule 144Ato take advantage of market conditions, but with the expectationthat the issuer will promptly register an exchange of identicalsecurities. As a result, purchasers generally do not require theliquidity discount they would otherwise demand if the securitieswere to remain private (though there is typically an interest ratebump in the event the issuer does not effect the registeredexchange within the specified time frame). In addition topromising public registration under the Securities Act, the issueralso typically agrees to file periodic reports with the SEC underthe Exchange Act, thereby enhancing public information andliquidity.

Section 4(a)(2) – traditional private placementsSection 4(a)(2) of the Securities Act exempts “transactions by anissuer not involving any public offering.” The term “public offering”is not defined in the Securities Act and the scope of the Section4(a)(2) exemption has largely evolved through case law, SECpronouncements and market practice.

The core issue is whether the persons to whom securities areoffered need the protection of the Securities Act – that is, whetherthey are sufficiently sophisticated so as to be able to fend forthemselves.25 In determining whether a transaction is a publicoffering, relevant factors include the number of offerees and theirrelationship to each other and the issuer, the number of securitiesbeing offered, the size of the offering and the manner in which theoffering is conducted.26 All of the surrounding circumstances mustbe considered in this analysis.27

Private placements under Section 4(a)(2) typically consist of,among other things:• a non-public offering (that is, an offering without any form of

general solicitation or advertising);• to a limited number of offerees;• who are buying for investment and not with a view to

distribution; and• who are sophisticated investors and have been provided with or

have access to information about the issuer.28

In addition, the securities issued in a private placement generallyinclude restrictions on resales by the purchasers (such as through theuse of stop-transfer orders, restrictive legends and the like).29

Regulation D private placements – Rule 506 safeharborAs you can see, it is not possible to map the borders of Section4(a)(2) with precision. Securities Act Regulation D helps give somecertainty in this area, and it also establishes various safe harbors fromSecurities Act registration.

Foreign private issuers are most likely to look to Rule 506 ofRegulation D, which is not limited to offering amount (other partsof Regulation D are limited to offerings of up to $1 million or $5million, for example). If the conditions of Rule 506 are met, the

Securities purchased under Rule 144A are deemedrestricted securities and can only be resold pursuant toRule 144A or another exemption (including the RegulationS resale safe harbor described above).23

PRACTICE POINT