ACC 221 Tax Accounting Ch 1

37

Income Tax Fundamentals 2009 edition Gerald E. Whittenburg Martha Altus-Buller 1 2009 Cengage Learning

-

Upload

angela-cipriano -

Category

Documents

-

view

2.022 -

download

2

description

Transcript of ACC 221 Tax Accounting Ch 1

Income Tax Fundamentals 2009 edition Gerald E. Whittenburg

Martha Altus-Buller

12009 Cengage Learning

Since 1913 - adoption of 16th amendment - the constitutionality of income tax has never been questioned

Income taxes serve a multitude of purposes

22009 Cengage Learning

Raise revenue

Tool for social and economic policies

• Social policy encourages desirable activities and discourages undesirable activities

Can’t deduct penalties

Can deduct charitable contributions

Credits for higher education expenses

• Economic policy as manifested by fiscal policy

Encourage investment in capital assets

• Both economic and social

Exclude gain on sale of personal residence up to $250,000 ($500,000 if married)

32009 Cengage Learning

Individual• Taxable income includes wages, salary, self-

employment earnings, rent, interest and dividends• An individual may file simplest tax form qualified for

1040EZ 1040A 1040

• If error made on one of the three above forms, can amend with a 1040X

4

See next slide

2009 Cengage Learning

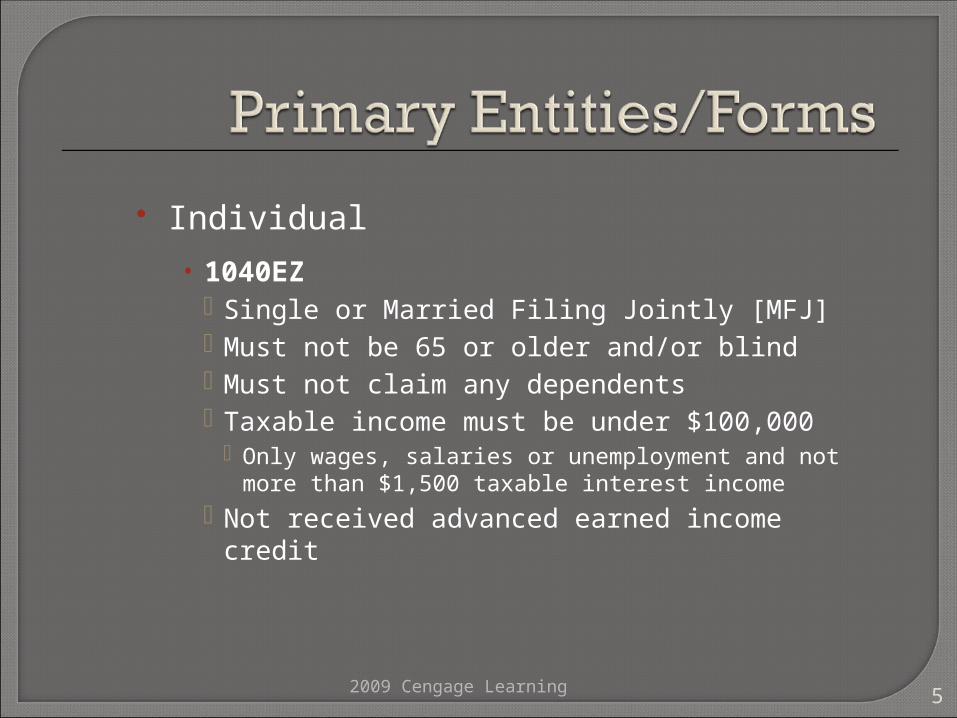

Individual

• 1040EZ Single or Married Filing Jointly [MFJ] Must not be 65 or older and/or blind Must not claim any dependents Taxable income must be under $100,000

Only wages, salaries or unemployment and not more than $1,500 taxable interest income

Not received advanced earned income credit

52009 Cengage Learning

Individual [continued]• 1040A

Generally used by taxpayers who are not self-employed and don’t itemize deductions

• 1040 If taxpayer doesn’t qualify to use 1040EZ or 1040A should

complete a 1040 with possible schedules attached: Schedule A to itemize deductions Schedule B to report dividends/interest income > $1500 Schedule C to report trade/business income Schedule D to report capital gains/losses Schedule E to report rental/royalty income Schedule F to report farm/ranch activities

62009 Cengage Learning

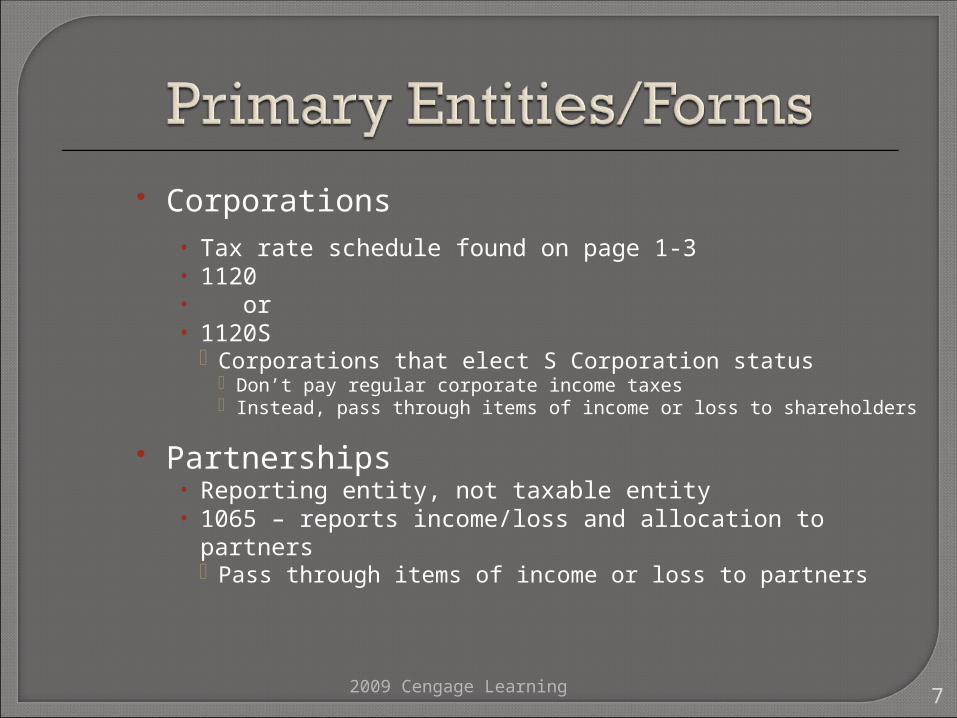

Corporations• Tax rate schedule found on page 1-3• 1120 • or• 1120S

Corporations that elect S Corporation status Don’t pay regular corporate income taxes Instead, pass through items of income or loss to shareholders

Partnerships• Reporting entity, not taxable entity• 1065 – reports income/loss and allocation to partners

Pass through items of income or loss to partners

72009 Cengage Learning

This model follows Form 1040

Gross Income

less: Deductions for Adjusted Gross Income [AGI]

AGI

less: Greater of Itemized or Standard Deduction

less: Exemptions

Taxable Income

times: Tax Rate (using tax tables or rate schedules)

Gross Tax Liability

less: Tax Credits and Prepayments

Tax Due or Refund

82009 Cengage Learning

9

2008 standard deductionSingle $ 5,450

Married Filing Joint [MFJ] $10,900Qualifying Widow(er) $10,900 also known as Surviving Spouse

Head of Household [HOH] $ 8,000

Married Filing Separate [MFS] $ 5,450

*Taxpayers 65 or older and/or blind get an additional amount$1050 if MFJ, MFS or SS$1350 if HOH or Single

2008 exemption $3500 – personal & dependency

10

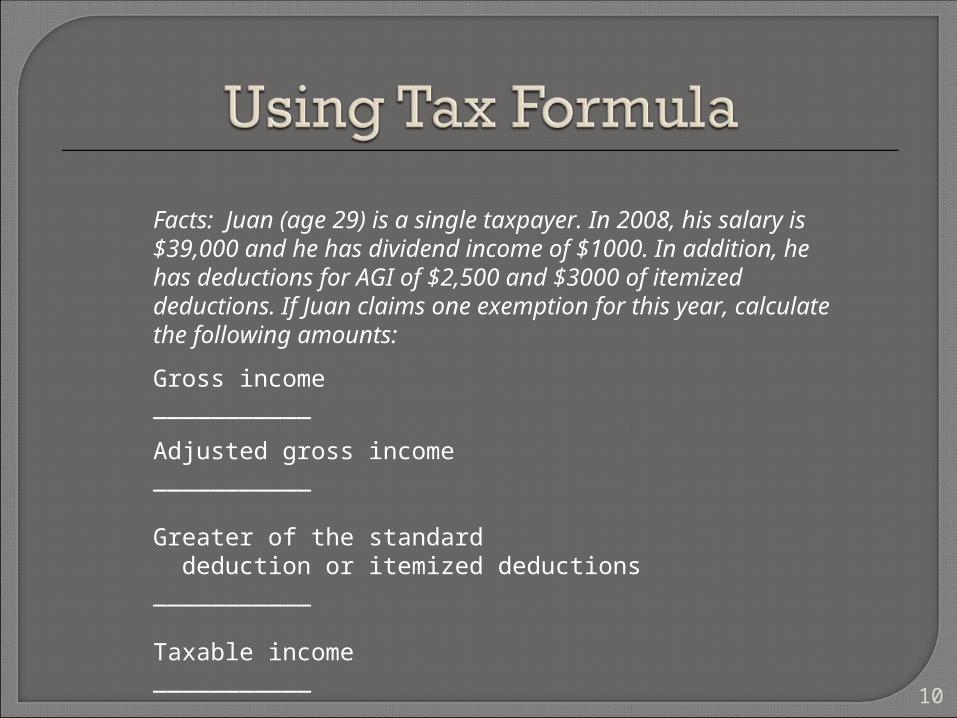

Facts: Juan (age 29) is a single taxpayer. In 2008, his salary is $39,000 and he has dividend income of $1000. In addition, he has deductions for AGI of $2,500 and $3000 of itemized deductions. If Juan claims one exemption for this year, calculate the following amounts:

Gross income ___________

Adjusted gross income ___________

Greater of the standard deduction or itemized deductions ___________

Taxable income ___________

11

Gross income $40,000

Adjusted gross income ___________

Greater of the standard deduction or itemized deductions ___________

Taxable income ___________

Gross income = $39,000 + 1,000

12

Gross income $40,000

Adjusted gross income 37,500

Greater of the standard deduction or itemized deductions ___________

Taxable income ___________

AGI = $40,000 – 2,500

13

Gross income $40,000

Adjusted gross income 37,500

Greater of the standard deduction or itemized deductions 5,450

Taxable income ___________

The standard deduction of $5450 exceeds itemized deductions of $3000

2009 Cengage Learning

14

Gross income $40,000

Adjusted gross income 37,500

Greater of the standard deduction or itemized deductions 5,450

Taxable income $28,550

Taxable income = $37,500 – 5,450 – 3,500 exemption

2009 Cengage Learning

Based on filing status and gross income• Generally, if exemptions plus greater of

standard or itemized deductions exceed income, then filing is not necessary

• If taxpayer is claimed as a dependent on another’s return, dependent’s standard deduction is: Greater of $900

or Earned income + $300 But never more than standard deduction

152009 Cengage Learning

Taxpayer must file if• Owe any special taxes (See Chart C)

• Received Advanced Earned Income Credit payments from employer

• Had self-employment [SE] income >= $400

• Had wages of $108.28 or more from a church that is exempt from paying social security and Medicare taxes

• Other situations outlined on Chart C

162009 Cengage Learning

Note: Must analyze each independent situation to determine if the taxpayers are required to file a return for 2008

Taxpayer [age 45] is a single waiter and has unreported tips of $1510; is the taxpayer required to file?

Yes, because taxpayer owes social security taxes on unreported tips

172009 Cengage Learning

Taxpayer is single [age 31] and blind and has income of $9,250; is the taxpayer required to file?

No, because standard deduction = $6800 [$5450 + 1350]; exemption= $3500. These amounts total to $10,300 and exceed income.

182009 Cengage Learning

Husband [age 67] and wife [age 69] have income of $19,180 and MFJ; are the taxpayers required to file?

No, because standard deduction = $12,800 [10,900+ 1050 + 1050]; exemptions = $7000. These amounts total to $20,000 and exceed income.

192009 Cengage Learning

Taxpayer is a single full time college student, age 21, with wages from a part-time job of $6340. He is claimed as a dependent by his parents; is the taxpayer required to file?

Yes, because standard deduction = $5450; exemption = 0 [as he’s claimed by parents]. Income exceeds these amounts.

202009 Cengage Learning

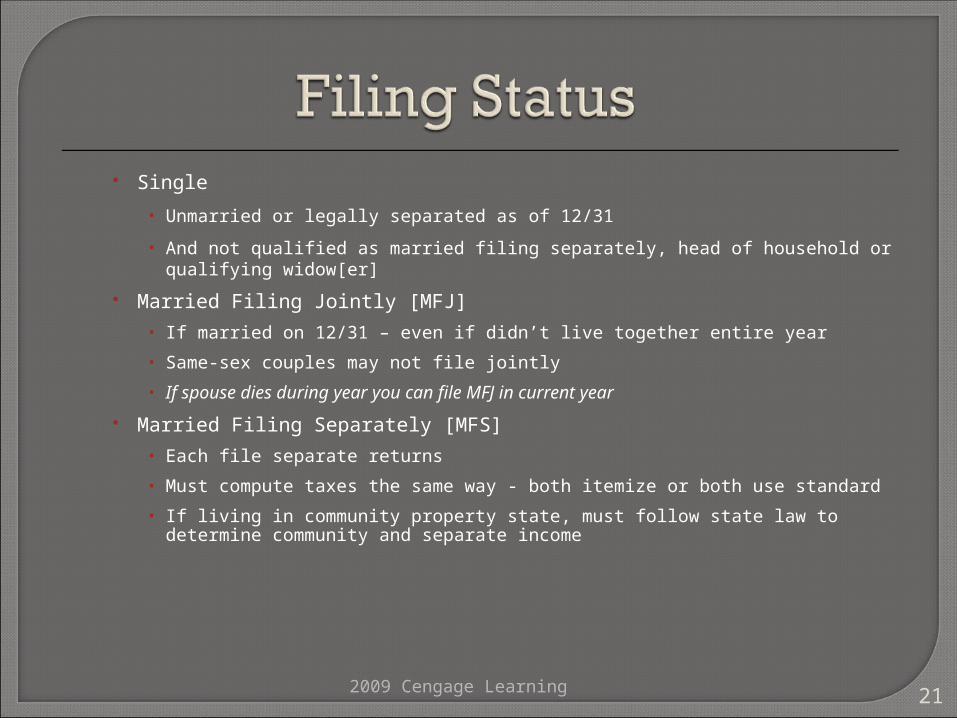

Single

• Unmarried or legally separated as of 12/31

• And not qualified as married filing separately, head of household or qualifying widow[er]

Married Filing Jointly [MFJ]

• If married on 12/31 – even if didn’t live together entire year

• Same-sex couples may not file jointly

• If spouse dies during year you can file MFJ in current year

Married Filing Separately [MFS]

• Each file separate returns

• Must compute taxes the same way - both itemize or both use standard

• If living in community property state, must follow state law to determine community and separate income

212009 Cengage Learning

Head of Household [HOH]

• Tables have lower rates than single or MFS

• Taxpayer can file as HOH if: Unmarried or abandoned* as of 12/31 Paid > 50% of cost of keeping up home that was

principal residence of dependent child or other qualifying dependent relative

There is one exception to principal residence requirement: if dependent is taxpayer’s parent, he/she doesn’t have to live with taxpayer

22

*See p. 1-10 for requirement for abandoned spouse

2009 Cengage Learning

Surviving Spouse [SS]• Also known as qualifying widow or widower

• Available in year of spouse’s death and for

two subsequent years Must pay over half the cost of maintaining a

household where a dependent child, stepchild, adopted child or foster child lives

232009 Cengage Learning

Six brackets (in Appendix)• 10%, 15%, 25%, 28%, 33%, 35%• Tax rate schedules for different filing types in

Appendix A• Marginal rate may exceed 35% when taxpayers are

required to phase out exemptions and deductions Qualifying dividends and net long-

term capital gains may be taxed at lower rates

242009 Cengage Learning

Personal exemptions may be taken for self/spouse

Additional exemptions may be taken for individuals who are either • Qualifying child

or

• Qualifying relative For 2008 each exemption = $3500 Exemption phased out to $2333 when AGI

exceeds thresholds found on p. 1-12

252009 Cengage Learning

Six tests must be met for a child to be claimed as a dependentRelationship Test - child must be taxpayer’s child,

stepchild, adopted child or taxpayer’s sibling, half- or step-sibling, or a descendant of any of these. Foster child may also qualify.

Domicile Test- child must have same principal place of abode as taxpayer for more than ½ the year.

Age Test – child must be under 19 or a full-time student under 24 [enrolled at least 5 months of year].

262009 Cengage Learning

Joint Return Test – child may not file joint return with spouse [exception: if it’s only to claim refund, then considered to have passed this test].

Citizenship Test – dependent must be a US citizen, a resident of the US, Canada or Mexico, or an alien child adopted by and living with a US citizen.

Self-Support Test – child who provides more than ½ of his/her own support cannot be claimed as a dependent of someone else. Funds received by students as scholarships are excluded from support test.

272009 Cengage Learning

Five-part test must be met for a qualifying relative [who is not a qualifying child] to be claimed as a dependent.

Note: A taxpayer’s child who does not meet qualifying child test may meet qualifying relative test!!

282009 Cengage Learning

Relationship or Member of Household Test – list of relatives that qualify is available at IRS web site A member of household [even if unrelated] for entire year

meets the relationship test Gross Income Test – individual may not have gross

income in excess of $3500 Support Test – dependent must receive over ½ of

his/her support from taxpayer Joint Return Test – dependent may not file a joint return

unless it’s solely to claim refund Citizenship Test – dependent must meet the citizenship

test identified in the qualifying child slide

292009 Cengage Learning

Certain taxpayers may not use standard deduction, instead must use itemized:• Married individual filing separately and whose

spouse itemizes• Nonresident aliens• Individual filing a short-period tax return

302009 Cengage Learning

31

The special rule for standard deduction for dependents is “deduction = greater of $900 or earned income + $300 but only up to basic standard deduction”

Example 1: Jaime is 23 and a full time student and her folks claim her as a dependent; she earned $2,000 in 2008.

2,000 earned income(2,000) standard deduction $0 taxable income

Example 2: Tia is 18 and has dividend income of $1,500 [not earned]

1,500 dividend income( 900) standard deduction$ 600 taxable income

32

Basic Gain/Loss Model

Amount Realized*

- Adjusted Basis**

Realized Gain/Loss

*Sales Price - Sales Expenses

**Cost - Accumulated Depreciation

A capital asset is any property [personal or investment] held by a taxpayer, with certain exceptions as listed in the tax law

• Examples: stocks, bonds, land, cars and other items held for investment

• Gains/losses on these assets are subject to special rates

Holding period of asset determines treatment • Long term is held >12 months (taxed at capital rates)

• Short term is held <= 12 months (taxed at ordinary rates)

332009 Cengage Learning

Long term capital gain

• Special rates depending upon taxpayer’s bracket

Ordinary Tax Bracket Capital Gains Tax Rate

10% or 15% 0%

All other brackets 15%

Long term capital loss

• Only allowed $3,000 net capital loss per year against ordinary income

• Carry-forward any unused balance

342009 Cengage Learning

35

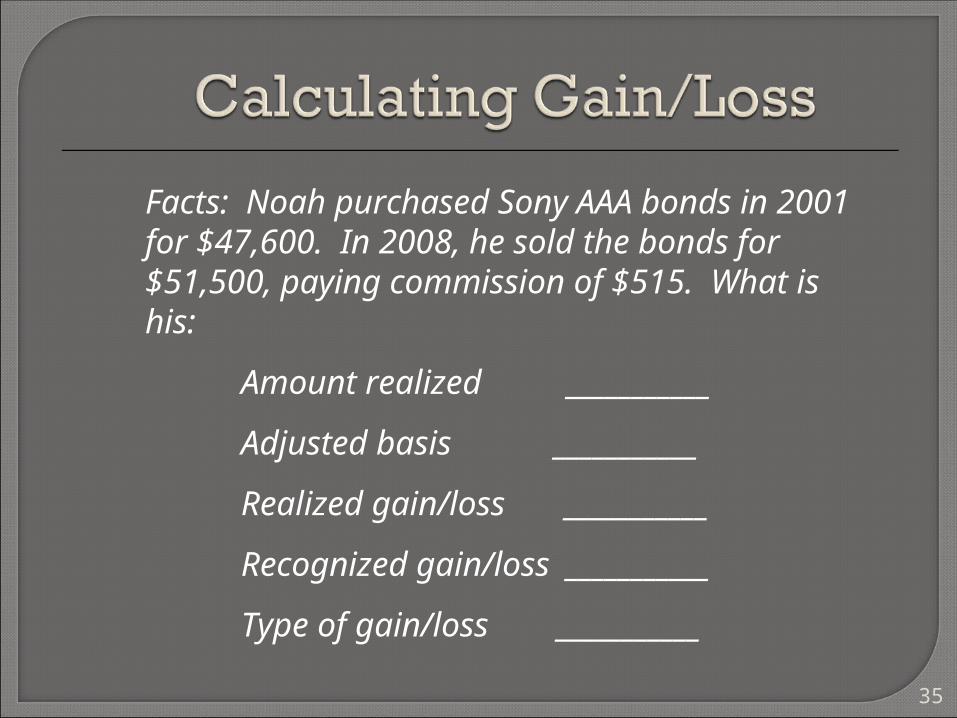

Facts: Noah purchased Sony AAA bonds in 2001 for $47,600. In 2008, he sold the bonds for $51,500, paying commission of $515. What is his:

Amount realized ___________

Adjusted basis ___________

Realized gain/loss ___________

Recognized gain/loss ___________

Type of gain/loss ___________

36

Amount realized * $50,985

Adjusted basis 47,600

Realized gain/loss 3,385

Recognized gain/loss 3,385

Type of gain/loss Long term capital gain

*$51,500 – 515 = 50,985

37