ACA Changes for 2016 - CarePlus Benefits · ACA Changes for 2016 March 15, 2016 . 1 Employee...

56

ACA Changes for 2016 March 15, 2016

Transcript of ACA Changes for 2016 - CarePlus Benefits · ACA Changes for 2016 March 15, 2016 . 1 Employee...

0

Employee Benefits

ACA Changes for 2016 March 15, 2016

1

Employee Benefits

Susan Maley Rash Senior Vice President, Health Care Reform Practice Leader

Ken Johnson Senior Vice President, ERISA and EB Compliance Practice Leader

Anne Bach Vice President, ERISA and EB Consultant

Today’s Speakers

2

Employee Benefits

Guidance and interpretations relating to these matters are being released on a regular basis. BB&T Insurance Services is not providing legal or tax advice. To ensure compliance with requirements imposed by the IRS, any discussion of U.S. tax matters contained in this communication (including any attachments) is not intended and cannot be used by anyone to avoid IRS penalties. This material is for informational purposes only.

Disclaimer

Before we get started – March 15, 2016

Our presentations provide general information. This is not legal advice.

Guidance on many provisions of the Patient Protection and Affordable Care Act (ACA or PPACA) are outstanding. New guidance may be issued regarding the ACA, or more generally, changes to statutes, rules, or regulations may be forthcoming that change the content of this presentation or alter the answers to some questions. Keep this in mind as you review any recordings.

3

Employee Benefits

What We Will Cover Today

Recent Changes – Employer Reporting – Filing Extension – Cadillac Tax Delayed – Delays and Defundings – Marketplace Update

Notice 2015-87 Clarifications Employer Mandate Review Employer Reporting Review Resources for You Q & A

4

Employee Benefits

Recent Changes Employer Reporting – Filing Extension Cadillac Tax Delayed Delays and Defundings Marketplace Update

5

Employee Benefits

Recent Changes IRS Extends Employer Reporting Filing Deadlines

Source: IRS Notice 2016-4, issued Dec 28, 2015

Reporting Activity Old Deadline New Deadline

1095-C Form Furnished to Employees January 31, 2016 March 31, 2016

1095-C & 1094-C Forms Mailed to IRS for Submission February 29, 2016 May 31, 2016

1095-C & 1094-C Forms E-Filed to IRS for Submission March 31, 2016 June 30, 2016

Applies to B series and providers of MEC (§ 6055), such as Insurance Carriers, Medicare, Medicaid

March 31, 2016 May 31, 2016 June 30, 2016

6

Employee Benefits

Recent Changes Cadillac Tax Delayed Until 2020

Cadillac Tax – DELAYED for TWO years

The delay of the Cadillac/excise tax is effective for 2018 and 2019, meaning that without further legislative adjustment or repeal, the tax is scheduled to take effect beginning in January 2020

Language in the package also permanently makes the tax deductible to employers and calls for a study by the comptroller on appropriate age and gender adjustments in consultation with the National Association of Insurance Commissioners (NAIC)

Coalition of employers still working to achieve complete repeal – but remember, scored to raise $91 billion of revenue over 10 years

7

Employee Benefits

Recent Changes Cadillac Tax Delayed Until 2020 (cont.)

Cadillac Tax – DELAYED for TWO years

Once a tax is delayed, repeal may not be far behind. “The odds are high that will ultimately happen,” said Peter Orszag, a Citigroup executive who was the Office of Management and Budget director when the ACA was written

Signed into law by President Obama on Dec. 18, 2015 – Consolidated Appropriations Act of 2016

Remember – this affects ALL size employers

Obama proposals to modify – instead of single threshold

Source: Politico, How the White House Lost the Cadillac Tax, 12/16/15

8

Employee Benefits

Recent Changes What is the Cadillac Tax? § 4980I

Source: Title 25, Internal Revenue Code, page 2880

Tax on value in excess of thresholds:

Estimated – 2020:

$10,500 self-only

$28,300 family (not really that simple)

indexed by 2020

9

Employee Benefits

Recent Changes Cadillac Tax by State

First Year at Least 10% of Workers with Employer Coverage Affected by Cadillac Tax

■ Before 2020

■ 2020-2022

■ 2023-2025

■ After 2025

Source: Commonwealth Fund, Rethinking the ACA Cadillac Tax – Dec 18, 2015; Authors’ estimates based on data from the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC)

10

Employee Benefits

Recent Changes Cadillac Tax 2020: Employer Action Items

Start thinking and talking about a strategy now for 2020

Determine which benefits will be subject to tax (for planning purposes, not at an implementation point now)

Estimate tax exposure for 2020 and beyond – based on what we know, still tons unknown – 2020 will reflect increased dollar limits, delay did not affect indexing.

Consider political implications of next election

Watch for repeal news

11

Employee Benefits

Recent Changes Delays and Defundings

HIT (health insurance tax) – one-year moratorium – effectively delays the 2017 payments. Medical devise tax – two-year moratorium on this

2.3% tax; no tax on sales from 1/1/16 to 12/31/17 These, plus Cadillac tax, created a loss of $35 billion,

offset in budget Risk Corridors – restricted funds:

– One of the three Rs – Reinsurance, Risk Adjustment, and Risk Corridors – to ensure stability in the Marketplace

Funding for state-run exchanges defunded IPAB (Independent Payment Advisory Board) defunded: This was a

panel instructed to study ways to curtail Medicare spending; never convened – effectively defunded

Source: CIAB, NAHU Dec 2015

12

Employee Benefits

Recent Changes Marketplace Update

CBO sharply reduced estimates on Marketplace enrollment from 21 million to 13 million

11 million are expected to receive a subsidy (avg. enrollee has 72% of premium subsidized)

Concerns about carriers (UHC) withdrawing

CMS has begun to limit SEP (Special Enrollment Period) entry – SEP individuals are utilizing 55% more services than OE counterpart

State-run exchanges seeing large rate increases by BCBS plans – 47% in Minnesota, 36% in Tennessee

Employers are sticking with plans – in 2015, only 7% of employers with 50-499 said likely to terminate plans within five years (vs. 21% in 2013); 5% of employers with 500+ said likely to terminate

Source: I New York Times – Jan 9, 2016; WSJ Feb 1, 2016

13

Employee Benefits

Recent Changes Out-of-Pocket Maximums 2016

Out-of-Pocket Max (OOPM) for all non-GF plans – fully insured and self-funded – $6,850/$13,700 for 2016

– $7,150/$14,300 for 2017

– Take into account all non-premium cost sharing – deductibles, copays, and coinsurance

HDHP HSA compatible OOPM – $6,550/$13,100 for 2016

Embedded deductibles for family coverage effective 1/1/16 – legislative alert June 2015; non-GF plans must apply the ACA’s self-only OOPM to all individuals, regardless of whether they have self-only or family coverage

Penalty: 4980H penalty – $100 per participant

Source: HHS Fact Sheet Benefit and Payment Parameters for 2016, Nov 2014; for 2017, March 2016

14

Employee Benefits

Recent Changes ACA Political Updates

What to Watch for During the 2016 Elections

President Obama vetoed the Reconciliation Repeal of the ACA on Jan. 8, 2015 This is the first time a full repeal of the

ACA passed both chambers and reached the President’s desk Newly elected House Speaker Paul

Ryan and Senate Majority Leader Mitch McConnell worked together on repeal legislation Expect this to be a political hot topic of

2016 presidential elections

15

Employee Benefits

Notice 2015-87 Clarifications

16

Employee Benefits

IRS Notice 2015-87

Issued Dec. 16, 2015

Addresses how ACA provisions affect employer health coverage

Covers ACA market reforms and employer coverage rules

17

Employee Benefits

IRS Notice 2015-87 (cont.)

HRA integration with other group health plan coverage and employer payment plans (Q&As 1-6)

Affordability under § 4980H (Employer Mandate/“Play or Pay”) (Q&As 7-12)

– Employer contributions to HRAs (Q&A 7)

– Employer-provided flex credits (Q&A 8)

– Cash-outs/Opt-outs (Q&A 9)

– Davis Bacon Act and Service Contract Act employees (Q&A 10)

– Affordability indexed to 9.56% for 2015; indexed to 9.66% for 2016 (Q12)

Indexing of § 4980H penalty amounts.(Q&A 13)

§ 4980H – Hours of service, breaks in service for educational organizations, and rules offers to Tricare, AmeriCorps employees (Q&As 14-17)

Governmental entity/coverage issues (Q&A 18-20)

$500 health flexible spending account carryovers – including COBRA issues (Q&As 21-25)

Relief related to good faith and timely ACA reporting (Q&A 26)

Source: IRS Notice 2015-87, issued Dec 16, 2015

18

Employee Benefits

IRS Notice 2015-87 Employer Contributions

In the weeds: Employer contributions

Unconditional opt-out – May have affect of increasing contribution – Waiving: Choice of cash or coverage: $200/mo. required contribution or $100 in

wages to decline = $300 affordability (Q&A 9)

Flex Credits – Three examples (Q&A 8) – Will impact how we design future flex plans/exchanges. Transition relief for plans before 12/16/15

Service Contract Act (SCA) and Davis Bacon Act (Q&A 10)

Guidance generally applies for plan years beginning on or after Dec. 16, 2015

Source: IRS Notice 2015-87, issued Dec 16, 2015

19

Employee Benefits

IRS Notice 2015-87 Hours of Service

In the weeds: Hours of service

Does not include any hours after individual terminates employment with ALE

Does not include workers’ comp, unemployment

Does include: – LTD/STD payments trigger hours as long as the employer makes any

payment toward the cost of coverage (directly or indirectly) without regard to whether paid by the insurer or employer; payments under an employee pay-all after tax would not count as hours

Source: IRS Notice 2015-87, issued Dec 16, 2015

20

Employee Benefits

Hours of Service Determining Full-Time Status

Full-Time (FT) Employee: for any month, an employee who is employed, on average, at least 30 hours of service/week (130 hours per month)

Must calculate actual hours of service for hours recorded as worked, and hours for which payment is due: vacation, holidays, illness, incapacity (including disability, layoff, jury duty, and leave of absence)

ALE Status

• Look at hours of service for each calendar month (120 hours)

• FT status based on hours of service, not classification

Offering Coverage

• Monthly measurement method • Look-back measurement method • Employees in same category treated the

same

Source: Zywave Jan 20, 2015

21

Employee Benefits

Hours of Service – Recent News ERISA 510: Marin v. Dave & Busters

We are following this case – related to ACA, tracking hours, and offers of coverage

This is a class action lawsuit by an employee alleging the company interfered with her rights to benefits under ERISA

Federal District Judge in NY denied motion to dismiss

Claim is based on § 510 of ERISA

– Plaintiff is claiming the employer reduced her hours of work to below ACA definition of full-time

Caution: Litigation risks associated with workforce realignments

Source: McDermott Will and Emery, Feb 16, 2016

22

Employee Benefits

Employer Mandate Review

23

Employee Benefits

Employer Mandate Basics for 2016

Employers must offer medical coverage (“minimum essential coverage”) that meets certain standards to full-time equivalent employees (FTEs) and their dependent children up to age 26

Employer Size 2016 Plan Year and Beyond

Employer Reporting

50-99 ALEs Employers must offer coverage to

95% of FTEs Required

100+ ALEs Employers must offer coverage to

95% of FTEs Required

Source: IRS ESR final regs.

24

Employee Benefits

Employer Mandate Applicable Large Employer (ALE) Determination

ALE determination is based on the preceding calendar year: 2014 Determine if

ALE Count month by

month, if over 50 FTEs, ALE for next year

2016 File 1094-C with IRS and

1095-C to employees by March – June

2015 ALE and now subject to ALE

employer reporting

2015 Determine if

ALE Count month by

month

2016 ALE and now subject to ALE

employer reporting

2017 File 1094-C with IRS and

1095-C to employees by Jan – March

25

Employee Benefits

Employer Mandate Who is an ALE?

2015 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Full-Time (FT) Employees 48 40 40 40 41 40 39 62 63 60 61 55

Full-Time Equivalents (FTEs)

Hours paid: non-FT employee 1 120 120 0 0 0 0 0 60 70 120 90 95

Hours paid: non-FT employee 2 120 0 0 0 0 0 0 60 120 120 85 110

Hours paid: non-FT employee 3 35 0 0 0 0 0 0 30 90 120 75 120

Hours paid: non-FT employee 4 0 0 0 0 0 0 0 40 65 60 110 65

Total Hours Paid to non-FT employees 275 120 0 0 0 0 0 190 345 420 360 390

Total FTEs (Total Hours/120) 2.29 1.00 0 0 0 0 0 1.58 2.88 3.50 3.00 3.25

Employer Size (monthly) 50.29 41.00 40.00 40.00 41.00 40.00 39.00 63.58 65.88 63.50 64.00 58.25

Employer Size (for all months) 606.50

Average Employer Size/Month 50.54

Employer Size (Rounded) 51

For this calculation only, use maximum value of 120

hours per non-FT employee

Qs 4, 5, 12

New: Reduce ALE count by those enrolled on Tricare or

VA coverage (Surface Transportation Veterans Act)

26

Employee Benefits

Employer Mandate An ALE Meets Employer Mandate in 2016 If:

MEC Coverage is offered to: – At least 95% in 2016 of full-time employees and their children under

age 26 – Spouses are not dependents

9.66%

60%

An employer’s coverage is affordable if: – The employee’s share of the premium for self-only coverage is 9.66% or

less of household income – Safe harbor affordability computations can be:

1.9.66% of the employee’s W-2 wages 2.The employee rate of pay per month (hourly rate x 130 or monthly salary) 3.FPL = Federal Poverty Level for a single individual ($11,770/12 x 9.66% =

$94.74)

An employer offers coverage with minimum value (MV) if: – The proportion of cost of covered services paid by the plan is at least 60%

of the expected cost for a standard population

95% in 2016

Qs 19, 20,22, 34, 38 & 39

27

Employee Benefits

Employer Mandate Affordability Safe Harbor Percentages

• 9.50% 2014

• 9.56% 2015

• 9.66% ($94.74/mo.= FPL) 2016

• Adjustments to be posted on IRS.gov Future Years

28

Employee Benefits

Employer Mandate Employer Shared Responsibility: Penalty Amounts

• 4980H(a) = $2,000 • 4980H(b) = $3,000 2014

• 4980H(a) = $2,080 • 4980H(b) = $3,120 2015

• 4980H(a) = $2,160 (1/12 = $180) • 4980H(b) = $3,240 (1/12 = $270) 2016

• 4980H(a) = $2,260 Proposed • 4980H(b) = $3,390 2017

29

Employee Benefits

* Penalties are calculated and assessed monthly (1/12 of $2,160 will be $180//month, $3,240 is $270/month). The maximum penalty is the lesser of the two penalties.

Employer Mandate 2016 Pay or Play (50+)

P A Y Does the insurance pay more

than 60% of covered health care expenses? AND

Do all full-time employees pay less than 9.66% of income for

coverage? And offer to 100% of all FT

employees?

Does the employer offer MEC coverage to 95% of all full-time employees in 2016?

Do any full-time employees obtain

subsidized coverage on an Exchange?

No penalty for

small employers

YES

YES

YES

Do any full-time employees obtain

subsidized coverage on an Exchange?

NO

$3,000 PENALTY

“unaffordable”

YES

Start

$2,000 PENALTY “No offer” coverage

Does the employer have at least 50 full-

time equivalent employees in 2015?

Total Penalty* = $2,000 x (full-time EE count - 30)

for 2016

Total Penalty* = $3,000 x each full-time employee receiving

subsidized Exchange coverage

YES

Full-time = 30 or more hours/week Full-time equivalents =

full-time employees + (all part-time hours/120)

No penalty as affordable

coverage is offered

NO

NO

P L A Y IRC § 4980H(a) IRC § 4980H(b)

Q&A 18, 24, 25

Source: Employer Shared Responsibility Provisions under ACA, Department of the Treasury, Feb. 10, 2014

Indexed 2016: 1/12 $2,160 ($180) 1/12 $3,240($270)

30

Employee Benefits

Employer Reporting Review

31

Employee Benefits

Employer Reporting Challenges

Confusing FTE ALE Code Conundrums

Penalties AIR Burdensome Safe Harbors

Difficult LNAP Tax Assessments Forms

Disclosure Time Consuming Electronic Filing

Offer of Coverage Affordability Full Time

1094-C 1095-C § 6055 § 6056 IRS 2015 Instructions

32

Employee Benefits

Employer Reporting Checklist: Five Basic Steps

1. Double-check all full-time employees have been identified for ACA reporting purposes, paying close attention to special circumstances, such as staffing, temporary, short-term employees, etc.

2. Make sure you’re using the best calculation method – the monthly measurement method or the look-back method – for your particular workforce

3. Update all necessary plan documents and summary plan descriptions (SPDs) to reflect the measurement method your company uses to determine full-time status

4. Try to include specific date ranges (for measurement and stability periods), waiting periods for new employees, and detailed info on how to treat workers in special circumstances (e.g., employees shifted from part-time to full-time)

5. Select the appropriate safe harbor you’ll use for the ACA’s affordability calculation: – W-2 – Rate of pay (monthly) – Federal poverty line

Source: Penny Wofford, OgletreeDeakins, Dec 2015

33

Employee Benefits

Employer Reporting The A-B-Cs

Form 1095-A is a tax form sent to consumers enrolled in health insurance through the public Exchanges in 2015 Consumers will need to file this, along

with forms 1040 and 8962, for the premium tax credit (federal subsidy)

B forms – generally insurers and non- ALEs self-funded (under 50)

C forms – ALEs over 50 (self-funded must complete Part III of 1095-C for any employee enrolling or for non-employees enrolled; i.e., COBRA, retirees, etc.)

34

Employee Benefits

Employer Reporting Required Forms

ALEs sponsoring self-

insured plans

Form 1095-C: Part I, Part II, and Part III

Form 1094-C

ALEs sponsoring fully insured plans

Form 1095-C: Part I and Part II only

Form 1094-C

Non-ALEs sponsoring self-

insured plans

Form 1094-B

Form 1095-B

Source: Zywave July, 2015

Non-ALEs sponsoring insured plans are not required to report under either § 6055 or § 6056.

35

Employee Benefits

Employer Reporting Overview

Section 6055 Section 6056

Applies to: Self-funded plan sponsors and health insurance issuers Applicable large employers (ALEs)

Requires reporting entities to:

File information with the IRS and provide statements to covered

individuals (1094-B and 1095-B)

File information with the IRS and provide statements to FT

employees (1094-C and 1095-C)

Purpose: Help administer the individual mandate

Help administer the employer mandate and determine eligibility

for Exchange subsidies

2016 Deadlines: 2016 Deadlines Extended

Individual Statements: March 31 IRS Returns: May 31 (June 30 if filed electronically)

Self-funded plan sponsors that are ALEs must report under both sections, but will report using Forms 1094-C and 1095-C

36

Employee Benefits

Employer Reporting Final Forms 1094-C and 1095-C

1094-C Transmittal (3 pages)

1095-C Report/Statement (1 page plus recipient instructions)

Source: IRS September 17, 2015

Part I: Transmits 1095-Cs Part II: Identifies ALE and eligibility for

transition relief/simplified reporting Part III: Reports MEC offered to any FT

employees & transition relief USED to calculate the (a) penalties

Part I: Identifies employees and ALE Part II: Reports health coverage offered to

FT employees plus premium, employment info, and transition relief

USED to calculate the (b) penalties Part III: Reports enrollment by any employee

(FT or not), plus other covered individuals in ALE self-insured plans

Filed with IRS with 1095-C reports Copy to each employee

37

Employee Benefits

Employer Reporting 2015 FINAL 1095-C

Source: IRS Sept 17 2015

Reporting Basics: Added box Plan Start Month. Enter 2-digit month for the beginning of plan year – e.g., January = 01

01

Can truncate SSN on form distributed to employees, but NOT to IRS

Name of employer is not the plan; use entity name and EIN under which the employee is paid

38

Employee Benefits

Employer Reporting Basics

The IRS requires every ALE to provide a Form 1095-C to each employee who was a full-time employee for any month of the calendar year. Plus:

– Line 14: Select from 9 codes to indicate if there was an offer of coverage and type of offer

– Line 15: Calculate the employee’s share of the lowest cost of monthly premium offered

– Line 16: Select from 9 codes on why the employer would not owe a “tack hammer” penalty. Where line 16 is left blank, the employer will incur a penalty for the month if the employee qualified for a premium subsidy from the Marketplace/ Exchange.

– 2015 Final Instructions were issued Sept. 17, 2015

Source: IRS September 2015

39

Employee Benefits

Employer Reporting 1095-C: Deciphering the Codes

Line 14: Offer of Coverage 1A. Qualified Offer: Minimum Essential Coverage (MEC) providing

Minimum Value (MV) offered to full-time employee with employee contribution for self-only coverage equal to or less than 9.5% mainland single federal poverty line and MEC offered to spouse and dependent(s).

1B. MEC providing MV offered to employee only.

1C. MEC providing MV offered to employee and at least MEC offered to dependent(s) (not spouse).

1D. MEC providing MV offered to employee and at least MEC offered to spouse (not dependent(s)).

1E. MEC providing MV offered to employee and at least MEC offered to dependent(s) and spouse.

1F. MEC not providing MV offered to employee; or employee and spouse or dependent(s); or employee, spouse, and dependents.

1G. Offer of coverage to employee who was not a full-time employee for any month of the calendar year and who enrolled in self-insured coverage for one or more months of the calendar year.

1H. No offer of coverage (employee not offered any health coverage or employee offered coverage not providing MEC).

1I. Qualified Offer Transition Relief 2015: Employee (and spouse or dependents) received no offer of coverage, or received an offer of coverage that is not a Qualified Offer, or received a Qualified Offer for less than all 12 months.

Line 16: Safe Harbor Codes 2A. Employee not employed during the month.

2B. Employee not a full-time employee.

2C. Employee enrolled in coverage offered.

2D. Employee in a section 4980H(b) limited non-assessment period.

2E. Multiemployer interim rule relief.

2F. Section 4980H affordability Form W-2 safe harbor.

2G. Section 4980H affordability federal poverty line safe harbor.

2H. Section 4980H affordability rate of pay safe harbor.

2I. Non-calendar-year transition relief applies to this employee.

Source: EBIA & IRS 2014 Instructions for Forms 1094-C and 1094-C dated 2/4/15

40

Employee Benefits

Employer Reporting Form 1095-C: Commonly Asked Questions

Recognize there may be more than one code that is permissible

Vendors have taken some different interpretations of the IRS instructions

Remember, GOOD FAITH effort

41

Employee Benefits

1A Line 15 blank since using 9.66 FPL

Line 16 – ??? blank since using 9.66 FPL * note on IRS AIR webinar, not clear in instructions

1A. Qualified Offer: MEC providing MV offered to full-time employee with employee contribution for self-only coverage equal to or less than 9.66% mainland single federal poverty line (i.e., $94.74 per month 2016 – $11,770 FPL) and MEC offered to spouse and dependent(s). Note: $93.18 for 2015

Employer Reporting 1A vs. 1E – 2016

Source: EBIA & IRS 2014 Instructions for Forms 1094-C and 1094-C dated 9/15

1E. MEC providing MV offered to employee and at least MEC offered to dependent(s) and spouse. Premium greater than $94.74 per month. Must complete lines 15 and 16.

42

Employee Benefits

Employer Reporting 1095-C: Line 16, Code 2D = Limited Non-Assessment Period (LNP)

Regardless of hours, employees in 6different periods are effectively not treated as full-time employees and in an LNP: – First Year an ALE – January to March of first year employer is considered an ALE (if conditions met) – Waiting Period under Monthly Measurement (MM) – three-month calendar starting the first month the

employee is otherwise eligible for offer of coverage – Waiting Period under Look-Back Measurement (LBM) – initial three calendar months of employment for

a new employee reasonably expected to work full-time – Initial Measurement Period (IMP) & Associated Administrative Period under LBM – IMP plus initial

administrative period (IAP) of new part-time, variable-hour, or seasonal employee – Period following Change in Status – under LBM, permitted period after move by new part-time, variable-

hour, or seasonal employee to full-time position before IMP ends – First Calendar Month Employment – month in which employee is hired, if start date is other than first of

month

Source: EBIA & IRS 2014 Instructions for Forms 1094-C and 1094-C dated 9/15

Limited Non-Assessment Period (LNP). An LNP generally refers to a period during which an ALE member will not be subject to an assessable payment under § 4980H(a), and in certain cases § 4980H(b), for a full-time employee, regardless of whether that employee is offered health coverage during that period. The first five periods described above are LNPs only if the employee is offered health coverage by the first day of the first month following the end of the period, and are LNPs for § 4980H(b) only if the health coverage that is offered at the end of the period provides minimum value. For more information on LNPs and the application of section 4980H, see Regulations § 54.4980H-1(a)(26).

43

Employee Benefits

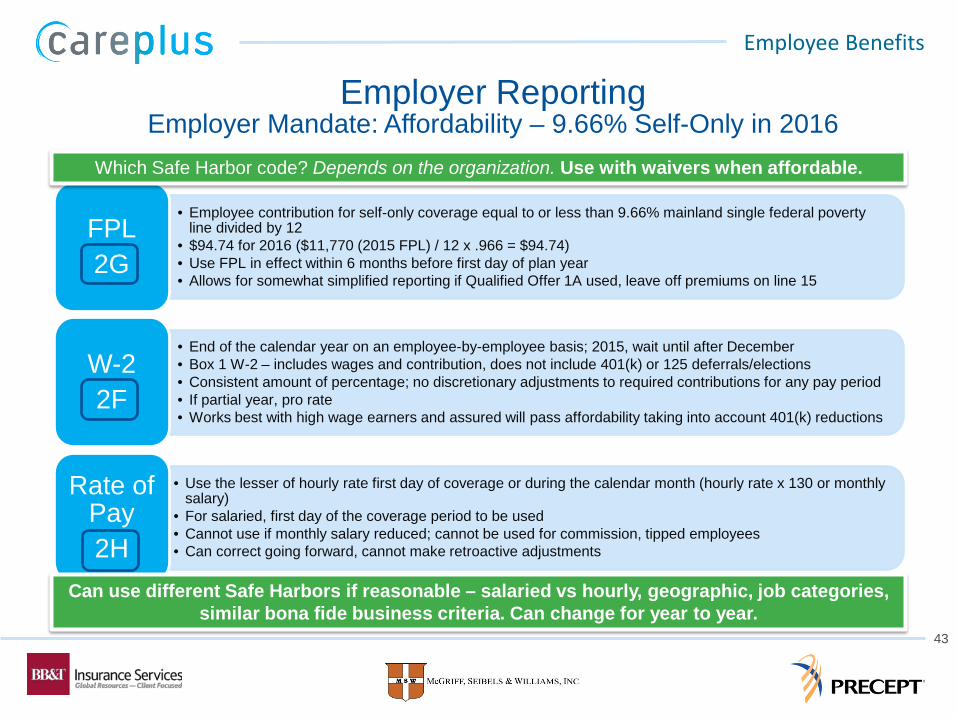

Employer Reporting Employer Mandate: Affordability – 9.66% Self-Only in 2016

• Employee contribution for self-only coverage equal to or less than 9.66% mainland single federal poverty line divided by 12

• $94.74 for 2016 ($11,770 (2015 FPL) / 12 x .966 = $94.74) • Use FPL in effect within 6 months before first day of plan year • Allows for somewhat simplified reporting if Qualified Offer 1A used, leave off premiums on line 15

FPL 2G

• End of the calendar year on an employee-by-employee basis; 2015, wait until after December • Box 1 W-2 – includes wages and contribution, does not include 401(k) or 125 deferrals/elections • Consistent amount of percentage; no discretionary adjustments to required contributions for any pay period • If partial year, pro rate • Works best with high wage earners and assured will pass affordability taking into account 401(k) reductions

W-2 2F

• Use the lesser of hourly rate first day of coverage or during the calendar month (hourly rate x 130 or monthly salary)

• For salaried, first day of the coverage period to be used • Cannot use if monthly salary reduced; cannot be used for commission, tipped employees • Can correct going forward, cannot make retroactive adjustments

Rate of Pay 2H

Which Safe Harbor code? Depends on the organization. Use with waivers when affordable.

Can use different Safe Harbors if reasonable – salaried vs hourly, geographic, job categories, similar bona fide business criteria. Can change for year to year.

44

Employee Benefits

Employer Reporting COBRA Codes Vary: Termination vs. Reduction in Hours

FINAL Instructions Changed Codes

Termination March 31, elects COBRA on April 1

Source: IRS September 17, 2015

2C 2C 2C

1E

$115 $115 $115

1E 1E

2A 2A

2A. Employee not employed during the month

1H 1H 1H 1H 1H 1H 1H

2A 2A 2A 2A 2A 2A 2A

NO premium listed

1H

1H. NO OFFER of coverage

1H

45

Employee Benefits

Source: IRS 2015

Employer Reporting 1095-C: Part III – Self-Funded Only: Covered Individuals

x x

x

1G

Example: COBRA divorced spouse enrolled, retirees

46

Employee Benefits

Employer Reporting 1094-C Transmittal to IRS

Form 1094-C: Transmittal to the

IRS – think in terms of a cover sheet to accompany all the forms of that ALE member

Four-part document

Submit one per ALE member – one per EIN as the authoritative transmittal

IRS uses the data in Part III to calculate the $2,000 (a) penalty

Source: IRS

47

Employee Benefits

Employer Reporting Transition Relief: Line 22

A = Qualifying Offer Method

B = Qualifying Offer Method Transition Relief

C = 4980H Transition Relief

D = 98% Offer Method

Reporting basics: Determine if “simplified” offer methods A, B or D make sense for your organization.

See pages 6-7 of instructions. A & B not useful if self-funded.

50-99 relief 100+ to get 30/80 subtraction for “sledgehammer.”

48

Employee Benefits

Employer Reporting Good Faith Effort

Good faith is distribution of the forms Good faith is the content of the forms (right codes) Good faith in the transmission to the IRS

Source: IRS Q & A on information on reporting by employers

49

Employee Benefits

Employer Reporting Penalty Amounts in 2015 & 2016

Penalty Type Per Violation Annual Maximum Annual Max for Small Employers*

Old New Old New Old New

General $100 $250 $1.5 million $3 million $500,000 $1 million

Corrected within 30 days $30 $50 $250,000 $500,000 $75,000 $175,000

Corrected after 30 days and before Aug. 1 $60 $100 $500,000 $1.5 million $200,000 $500,000

Intentional Disregard $250+ $500+ None N/A

*For purposes of the penalty maximum, a small employer is one with average annual gross receipts of up to $5 million for the three most recent taxable years.

50

Employee Benefits

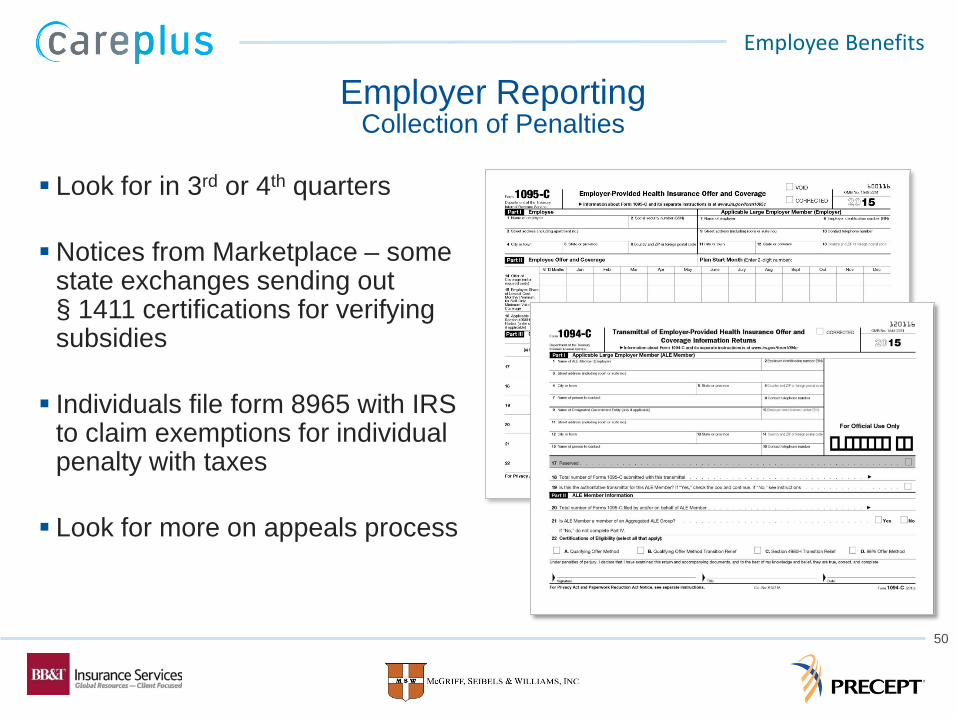

Employer Reporting Collection of Penalties

Look for in 3rd or 4th quarters

Notices from Marketplace – some state exchanges sending out § 1411 certifications for verifying subsidies

Individuals file form 8965 with IRS to claim exemptions for individual penalty with taxes

Look for more on appeals process

51

Employee Benefits

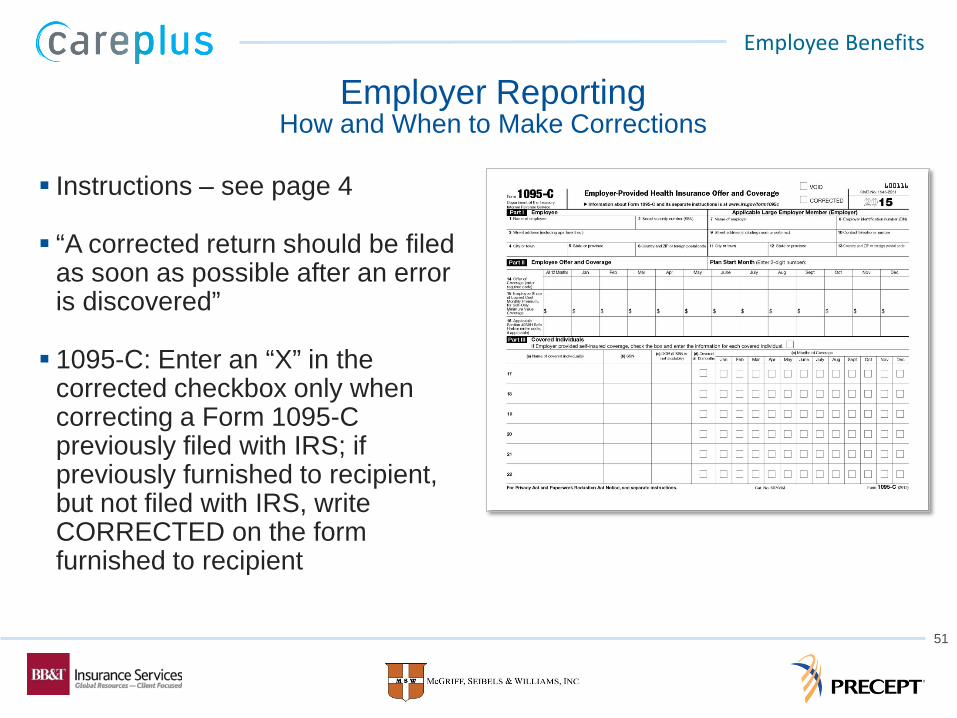

Employer Reporting How and When to Make Corrections

Instructions – see page 4

“A corrected return should be filed as soon as possible after an error is discovered”

1095-C: Enter an “X” in the corrected checkbox only when correcting a Form 1095-C previously filed with IRS; if previously furnished to recipient, but not filed with IRS, write CORRECTED on the form furnished to recipient

52

Employee Benefits

Employer Reporting Lessons Learned

Partner with compliance knowledge – start early in selecting a technology vendor Payroll/HRIS is clearly first choice Technology only goes so far –

data on COBRA, unions, retirees Test run early to review forms –

import and set-up problems are common this first year Switch early if moving to another

vendor…more out there now GOOD FAITH EFFORT!

53

Employee Benefits

Resources for You

54

Employee Benefits

Resources for You Webinar Series, Legislative Alerts, and Benefits News Clips

Weekly Webinar Series – http://insurance.bbt.com/business/employee-

benefits/education-center.asp

Rx for 401(k) Retirement Plans – March 17th – 12:00pm EDT/9:00am PDT

55

Employee Benefits

Any estimates presented here have been calculated prior to all regulations being issued for the Patient Protection and Affordable Care Act (ACA or PPACA). Future regulations may include clarifications, technical corrections, or guidance on complex calculations that may be required. As such, these estimates are not actuarial opinions. Financial and design decisions should only be made after careful consideration and not only on the estimates presented here. Additionally, financial and design decisions are the sole responsibility of the company or client attending this presentation.

CarePlus is a suite of employee benefit services, including SHDR, offered by BB&T Insurance Services

Insurance products are offered by BB&T Insurance Services, Inc., BB&T Insurance Services of California, Inc., F.B.P. Insurance Services, LLC dba Precept Insurance Solutions, LLC and dba ProView Advanced Administrators, LLC, and McGriff, Seibels & Williams, Inc., all subsidiaries of BB&T Insurance Holdings, Inc. BB&T Insurance Services, Inc., CA Lic #0C64544; BB&T Insurance Services of California, Inc., CA Lic #0619252; F.B.P. Insurance Services, LLC, CA Lic #0747466; McGriff, Seibels & Williams, Inc., CA Lic #0E83682.

BB&T Insurance Services is not providing legal or tax advice. To ensure compliance with requirements imposed by the IRS, any discussion of U.S. tax matters contained in this communication (including any attachments) is not intended and cannot be used by anyone to avoid IRS penalties. This material is for informational purposes only.

©2016, Branch Banking and Trust Company. All rights reserved. Insurance.BBT.com