AC 508 Company Study (CMI)

38

A Company Study Presented to the culty of the Department of Accountancy University of San Carlos Cebu City, Philippines _____________________________ In Partial Fulfillment of the requirements for the course C508: Accounting Information Systems _____________________________ March 14,2015

-

Upload

patricia-mae-amores -

Category

Education

-

view

151 -

download

1

Transcript of AC 508 Company Study (CMI)

A Company StudyPresented to the

Faculty of the Department of AccountancyUniversity of San CarlosCebu City, Philippines

_____________________________

In Partial Fulfillment of the requirements for the course

AC508: Accounting Information Systems_____________________________

March 14,2015

Revenue Cycle

Sales Order Processing SystemRevenue Cycle

Sales Warehouse Sales and Marketing Department Accounting and Finance Department

Architectural Plan

Prepare contract

quotation

Contract Quotation

Signed Contract

Purchase Order

Request signature for Sales Order

Contract

Signed Sales Order Contract

Estimate of

products needed

Clear product available

Signed Contract Quotation

Prepare Sales Order

Contract

Sales Order Contract 1

Sales Order Contract 2

Sales Order Contract 3

Issue Sales Invoice

Sales Invoice

Input

Auto-entry to General Ledger

A

Customer

Customer

Product Specialist

Product Specialist

Sales and Marketing Officer

Inventory Control Staff

Quantity Engineer

Architectural Plan

Customer

Original Copy Sales Order Contract

Customer File

Folder

Accounting and Finance Officer

General Ledger

Accounting and Finance Officer

Confirmation of payment

SALES ORDER PROCESSING SYSTEM

Accounting and Finance Department Warehouse General LedgerSales

Coordinate for delivery

and schedule

for delivery

Inform Administration

officerProcess Pull-out Slip and Delivery

Slip

Pull-out Slip

Delivery SlipSummary of SOC

Summary of SI

Summary of PR

Summary of DS

Summary of POSSummary of

Inventory

Review

ACustomer

Product Specialist

Administration Officer

Accounting and Finance Officer

Prepare the

goods

Input

Auto-entry to General Ledger

Product Specialist

Warehouse-In-Charge

Deliver prepared

goods

Delivery Personnel

Customer

Delivery Slip

Stock Release

Stock Release

General Ledger

Administration Officer

Product Specialist

Confirms the status of the account of the

customer from the Accounting &

Finance Department

SALES ORDER PROCESSING SYSTEM

Deliver Goods

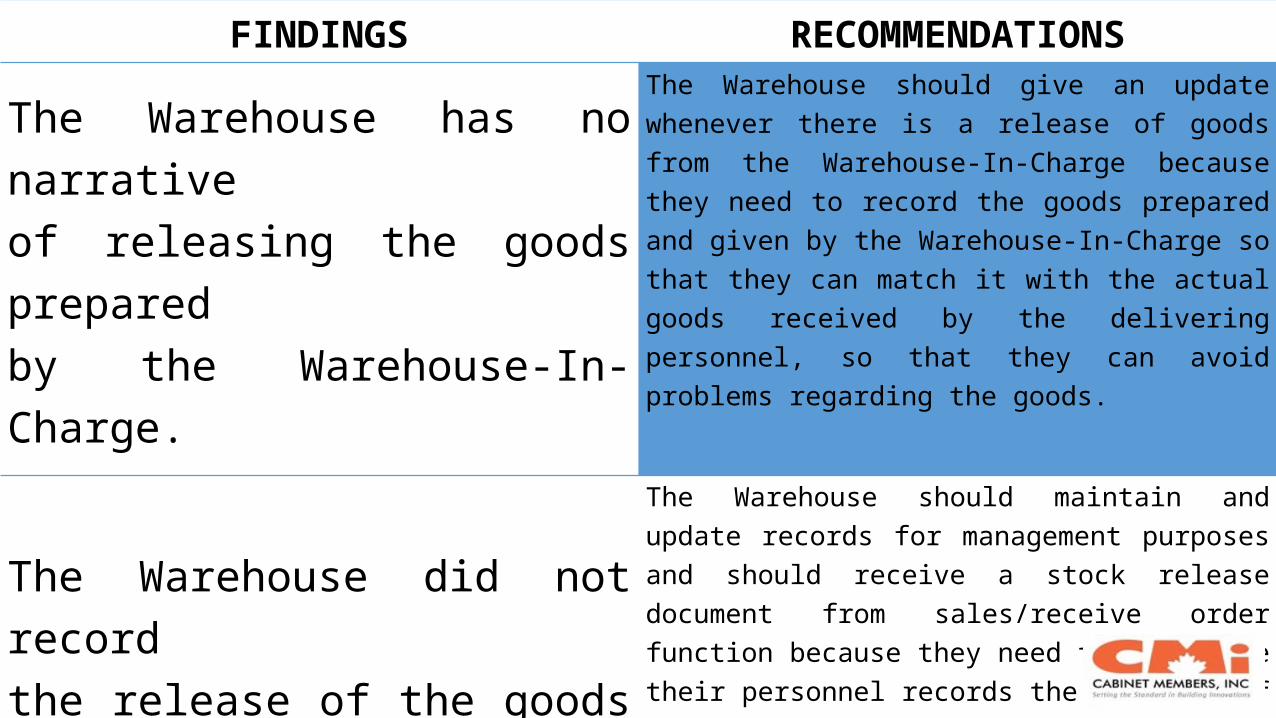

Findings and RecommendationsSales Order Processing System

FINDINGS RECOMMENDATIONS

The Warehouse has no narrative of releasing the goods prepared by the Warehouse-In-Charge.

The Warehouse should give an update whenever there is a release of goods from the Warehouse-In-Charge because they need to record the goods prepared and given by the Warehouse-In-Charge so that they can match it with the actual goods received by the delivering personnel, so that they can avoid problems regarding the goods.

The Warehouse did not record the release of the goods in the stock records.

The Warehouse should maintain and update records for management purposes and should receive a stock release document from sales/receive order function because they need to make sure their personnel records the delivery of goods and they would not be held liable for any problems regarding the delivery and so that they will have a record of their current inventory.

Internal Controls and RecommendationsSales Order Processing System

Internal Control Existing Comment Recommendation

1. Transactions Authorization

The company does not have a credit check process to check the credit-worthiness of their customers.

The company should incorporate a credit check process to check the credits of their customers.

Internal Control Existing Comment Recommendation

2. Segregation of Duties

1. The transaction is separate from the transaction processing.

2. There is no clear narrative that separates the asset custody and asset record keeping.

3. There is no clear structure that

prevents perpetration of fraud.

The company should incorporate a credit check process to check the credits of their customers.

Internal Control Existing Comment Recommendation

3. Supervision None

They can keep this current way, but if their company continues to grow then they should employ someone to supervise the departments.

Internal Control Existing Comment Recommendation

4. Accounting Records

1. Their documents are already pre-numbered.

2. They have special journals which provides a concise record of the entire class of events.

3. They have subsidiary ledgers for checking the different accounts.

4. They have general ledger which contains all information needed to make a financial statement.

Their internal controls for accounting records is OK.

Internal Control Existing Comment Recommendation

5. Access

The Warehouse-In-Charge is in-charge of the warehouse inventory but has two people assisting him in the process, so there is a prevention of illegal and unauthorized access.

Their current system is OK.

Internal Control Existing Comment Recommendation

6. Independent Verification

1. There is no indication of checking of the goods before they are sent to the customer.

2. There is no indication of a billing function that reconciles the original sales to verify and ensure that the customer only pays for their order.

1. They should indicate in their narratives the checking of the goods before they are sent in and out of their warehouse.

2. They should indicate in their narratives of the reconciliation of the sales order and the actual goods that are sent to the customer.

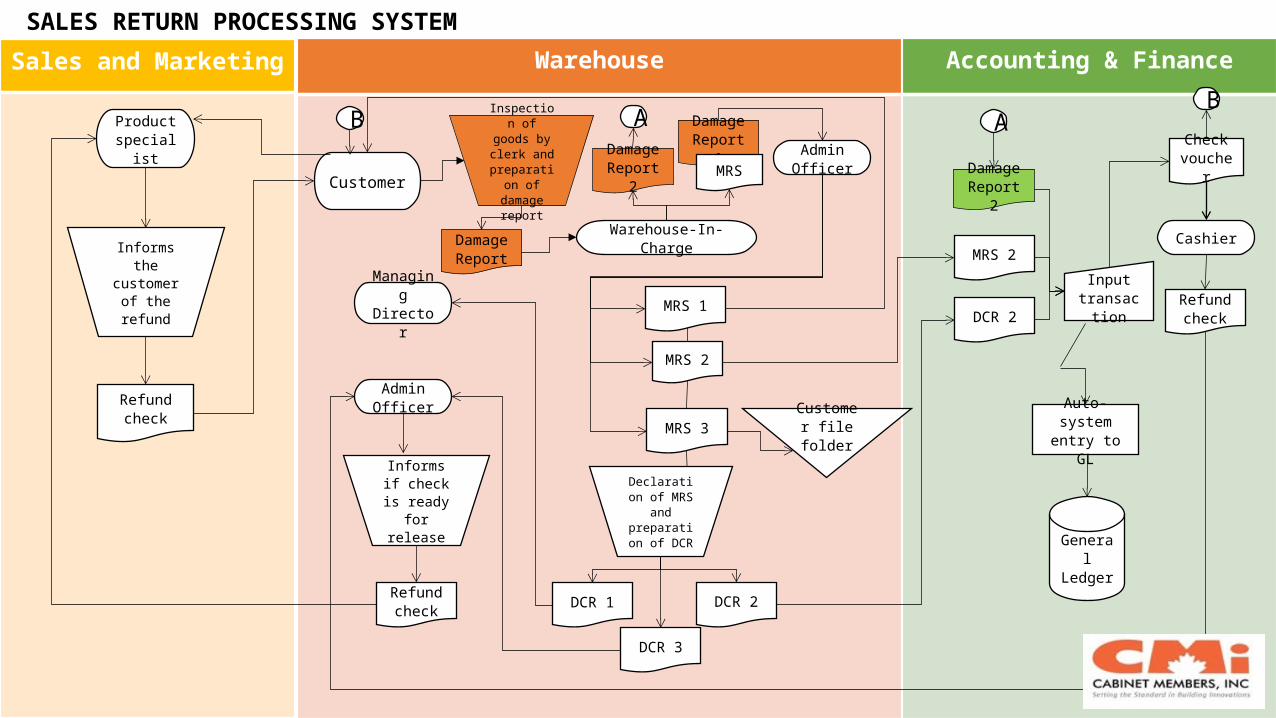

Sales Return Processing SystemRevenue Cycle

Sales and Marketing Warehouse Accounting & Finance

Customer

Product specialist

Inspection of goods by clerk and

preparation of damage

report

Admin Officer

MRS 3Customer file folder

Declaration of MRS and preparation

of DCR

DCR 1 DCR 2

DCR 3

Managing Director DCR 2

Admin Officer

Input transaction

Cashier

Refund check

Informs if check is

ready for release

Refund check

Informs the customer of the refund

Refund check Auto-system

entry to GL

General Ledger

Damage Report

Warehouse-In-Charge

MRS 1

Check voucher

Damage Report 1

MRS

MRS 2

Damage Report 2

MRS 2

Damage Report 2

A AB

B

SALES RETURN PROCESSING SYSTEM

Findings and RecommendationsSales Return Processing System

FINDINGS RECOMMENDATIONS

Warehouse-In-Charge is the one who inspects returned goods, approves the return, and at the same time prepares the MRS.

A Warehouse Clerk should be the one to receive, and to initially check the damages of the goods. He should prepare a damage report to be forwarded to the Warehouse-In-Charge. The Warehouse-In-Charge should reconcile this report with the actual damages of the goods 1-2 working days from receipt of the damage report. This control is needed since this is one problem the company is currently experiencing. A customer sometimes bribes or persuades the Warehouse-In-Charge into accepting and approving the refund for returned goods even though the goods do not qualify for such.

Internal Controls and RecommendationsSales Return Processing System

Internal Control Existing Comment Recommendation

1. Transactions Authorization

Approval of return and refund is based on the company’s policies and required qualifications

Effective

Internal Control Existing Comment Recommendation

2. Segregation of Duties

1.No separation of deciding authority between the receipt of goods and approval for return.

2.Preparation of refund check is separate from the release of the check.

1. Inspection of damaged goods shall be done by an employee other than the one who approves the return.

2. Effective

Internal Control Existing Comment Recommendation

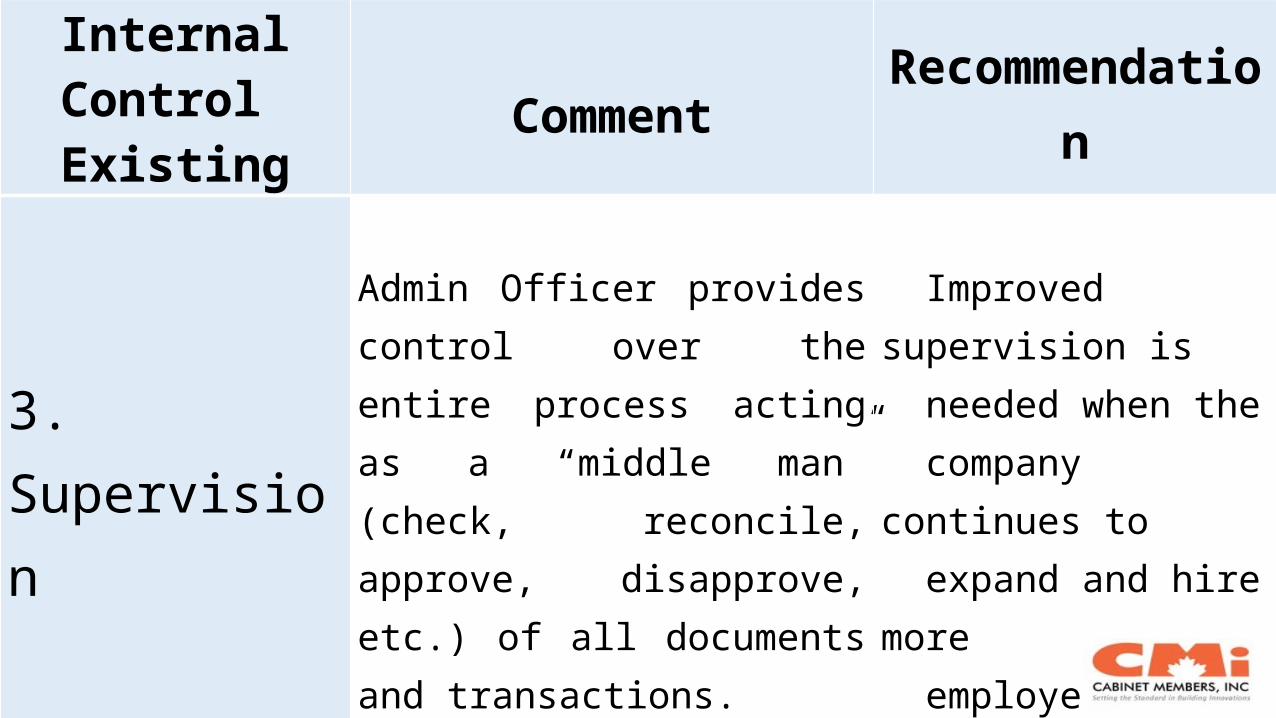

3. Supervision

Admin Officer provides control over the entire process acting as a “middle man” (check, reconcile, approve, disapprove, etc.) of all documents and transactions.

Improved supervision is needed when the company continues to expand and hire more employees.

Internal Control Existing Comment Recommendation

4. Accounting Records

1. Computerized system

2. Slips, vouchers and other documents are released in copies.

Effective

Internal Control Existing Comment Recommendation

5. Access

As the “middle man”, Admin Officer has access to master file of all documents.

Sufficient and effective access controls.

Internal Control Existing Comment Recommendation

6. Independent Verification

1. Inspection of goods before approval for return and refund

2. Refund check reconciles with check voucher

Effective

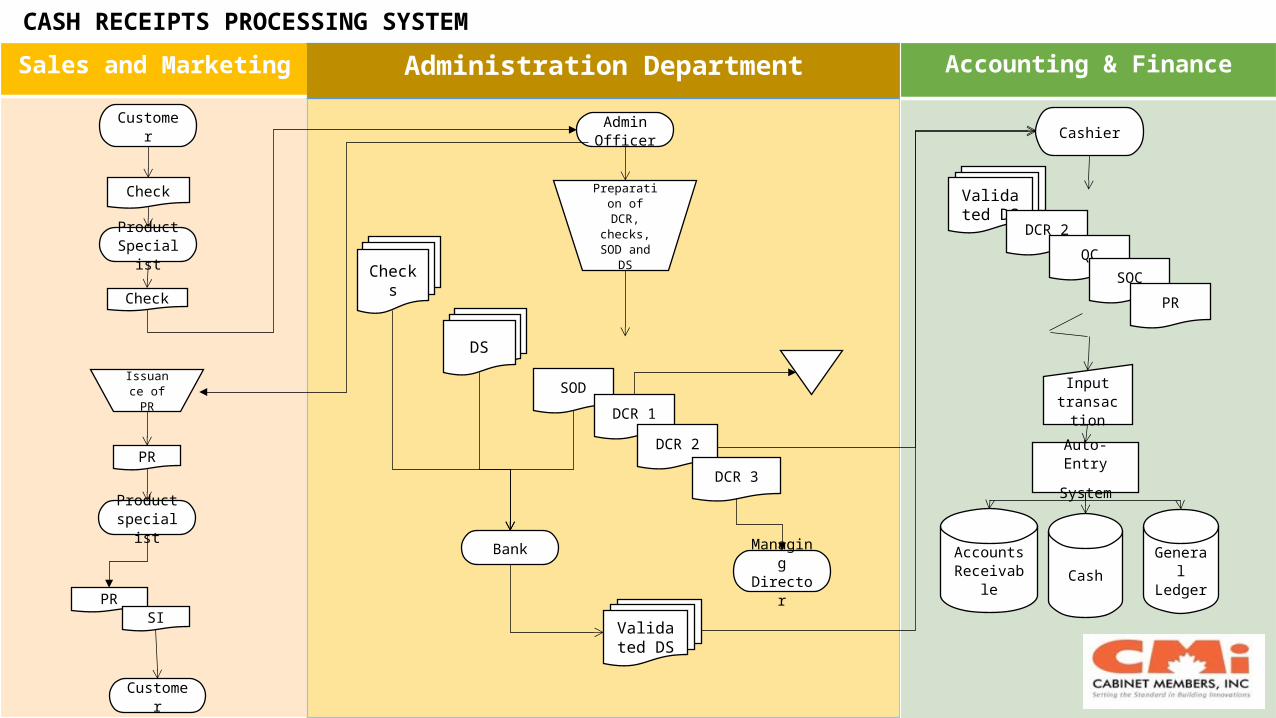

Cash Receipts Processing SystemRevenue Cycle

Sales and Marketing Administration Department

Accounting & Finance

Customer

Bank

Preparation of DCR,

checks, SOD and DS

Managing Director

Admin Officer

Input transaction

Check

Auto-Entry

System

General Ledger

Cashier

Product Specialist

Check

Issuance of PR

PR

Product specialist

Customer

Checks

DS

SOD

DCR 1

DCR 2

DCR 3

Validated DS

Validated DS

DCR 2

QC

SOC

PR

CashAccounts

Receivable

CASH RECEIPTS PROCESSING SYSTEM

PRSI

Findings and RecommendationsCash Receipts Processing System

FINDINGS RECOMMENDATIONS

The Admin receives all the checks, prepares the deposit slips, issues the PR, prepares the daily collection report and prepares the summary of deposits.

There should be strict supervision applied by the Admin Officer and segregation of duties to avoid potential employee fraud and to boost employee performance.

Internal Controls and RecommendationsCash Receipts Processing System

Internal Control Existing Comment Recommendation

1. Transactions Authorization

The company policies, like cash before delivery and check clearance before installation provide adequate internal control.

The company policies must be strictly implemented

Internal Control Existing Comment Recommendation

2. Segregation of Duties

There is inadequate separation of duties because there is a relatively fewer number of employees.

Closer supervision is recommended.

Internal Control Existing Comment Recommendation

3. Supervision

Admin Officer provides control over the entire process acting as a “middle man” (check, reconcile, approve, disapprove, etc.) of all documents and transactions.

Improved supervision is needed when the company continues to expand and hire more employees.

Internal Control Existing Comment Recommendation

4. Accounting Records

There is adequate amount and quality of documents to support the audit trail for the system.

Effective

Internal Control Existing Comment Recommendation

5. AccessThere is sufficient amount of access control to prevent and detect unauthorized access to records.

Effective

Internal Control Existing Comment Recommendation

6. Independent Verification

Cash receipt, general ledger and bank reconciliation functions are sufficiently verified independently to allow effective detection of irregularities.

Effective

Evaluation