_Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

32

Journal of Accounting Research Vol. 36 Supplement 1998 Printed in U.S.A. The Value Relevance of Intangibles: The Case of Software Capitalization DAVID ABOODY* AND BARUCH LEVf 1 . Introduction We examine the relevance to investors of information on the capitali- zation of software development costs, in accordance with the Financial Accounting Standards Board's Statement N o . 86 {SFAS N o. 86).^ Software capitalization, the only exception in the United States to the full ex- pensing rule of R &D {SFAS No . 2 ), pertains to the development com- ponent of R&D. It therefore provides a laboratory experiment for an accounting treatment of intangibles that differs from the nearly univer- sal full expensing of intangible assets.^ Our examination of the ten-year record of SFAS N o. 8 6 is also motivated by the 1996 petition from the Software Publishers Association {SPA) to abolish the standard. The FASB has indicated (in an "Action Alert," dated August 28, 1996) that it will consider the petition. The major claim put forward by the S P A is that, given industry changes since 1986, capitalization of software development costs does not benefit investors: *LIniversity of California, Los Angetes; fNew York University. We acknowledge the helpful comments of Brad Barber, Daniel Bens, Garry Biddle, Robert Herz, Bertrand Horwitz, Robert Holthausen, James Leisenring, Ed Maydew, Krishna Palepu, Michael Williams, and Paul Zarowin. ' The essence of this statement is presented in Appendix A. 2 Software capitalization starts upon the establishment of technological feasibility of the product under development. The preceding research costs are fully expensed; see Appen- dix A. 161 Copyright © , Institute of Professional Accounting, 1999

Transcript of _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 1/32

Journal of Accounting ResearchVol. 36 Supplement 1998

Printed in U.S.A.

The Value Relevance

of Intangibles: The Case of

Software Capitalization

D A V I D A B O O D Y * A N D B A R U C H L E V f

1. Introduction

We examine the relevance to investors of information on the capitali-zation of software development costs, in accordance with the FinancialAccounting Standards Board's Statement No. 86 {SFAS No. 86).^ Softwarecapitalization, the only exception in the United States to the full ex-pensing rule of R&D {SFAS No. 2), pertains to the development com-ponent of R&D. It therefore provides a laboratory experiment for anaccounting treatment of intangibles that differs from the nearly univer-sal full expensing of intangible assets.^ Our examination of the ten-yearrecord of SFAS No. 86 is also motivated by the 1996 petition from the

Software Publishers Association {SPA) to abolish the standard. The FASBhas indicated (in an "Action Alert," dated August 28, 1996) that it willconsider the petition.

The major claim put forward by the SPA is that, given industrychanges since 1986, capitalization of software development costs doesnot benefit investors:

*LIniversity of California, Los Angetes; fNew York University. We acknowledge thehelpful comments of Brad Barber, Daniel Bens, Garry Biddle, Robert Herz, BertrandHorwitz, Robert Holthausen, James Leisenring, Ed Maydew, Krishna Palepu, MichaelWilliams, and Paul Zarowin.

' Th e essence of this statement is presented in Appendix A.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 2/32

162 ENHANCING THE FINANCIAL REPORTING MODEL: 199 8

The rationale underlying the capitalization of software development costs is to rec-ognize the existence of an asset of the corporation. However, an asset should berecognized . . . only if ultimate realization of the asset is reasonably assured. . . . Due

to factors such as the ever-increasing volatility in the software marketplace, the com-pression of product cycles, the heightened level of competition and the divergenceof technology platforms, realization of software assets has become increasingly un-certain even at the point of technological feasibility. . . . We do not believe that soft-ware development costs are a useful predictive factor of future product sales.'

To bolster tbeir claim, tbe Software Publisbers Association invokes inves-tors' attitudes toward "soft assets":

The members of the SPA CFO Committee . . . have indicated the substantial majorityof their investors, underwriters, and financial analysts believe financial reporting bysoftware companies is improved when all software development costs are charged to

expense as inctirred. These users of financial statements do not believe the record-ing of a "soft" asset for the software being developed is particularly relevant and doesnot aid the user of financial statements. The users of financial statements . . . have ahigh degree of skepticism when it comes to soft assets resulting from the capitaliza-tion of software development costs. (SPA Letter, March 14, 1996, p. 5.)

Tbus, tbe Software Publisbers Association concludes: "Financial report-ing and financial statements would be more reliable and consistent if allsoftware development costs were required to be cbarged to expense."

We examine tbe relevance to investors of public information on soft-ware capitalization by analyzing botb associations of financial data witb

capital market observables and earnings forecast accuracy. We also pro-vide evidence on potential motives underlying tbe software industry'spetition to abolisb SFAS No. 86 and tbe apparent endorsement of tbispetition by some financial analysts. Tbis petition raises intriguing inter-est-group questions, since software capitalization was strongly supportedin 1985 by tbe tben trade group of software companies— ADAPSO (tbeAssociation of Data Processing Service O rganizations).* Tbe sbift in atti-tudes toward capitalization is particularly puzzling given tbe flexibilityof SFAS No. 86, wbicb largely enables tbose wbo wisb to capitalize todo so and otbers to immediately expense software developments costs.Analysts' objection to capitalization is equally intriguing, since softwarecapitalization can be easily undone by subtracting tbe periodic capitali-zation figure from reported earnings and tbe capitalized software assetfrom total assets and equity. At best, capitalization is informative abouttbe success of software development programs and at worst tbe informa-tion can be ignored.

For a sample of 163 firms during tbe period 198 7-95 , we find tbat an-nually capitalized development costs are positively associated witb stock

'This is part (p. 4) of a letter, dated March 14, 1996, written by Ken Wasch, presidentof the Software Publishers Association (1730 M Street, Washing ton, D.C. 20036) to the

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 3/32

TH E VALUE RELEVANCE OF INTANGIBLES 1 63

returns and the cumulative software asset reported on the balance sheetis associated with stock prices. Furthermore, software capitalization data

are associated with subsequent reported earnings, indicating another di-mension of relevance to investors. We find no support for the view thatthe ju dg m en t involved in software capitalization decreases the qualityof reported earnings. Finally, we document a significant association be-tween development costs which were fully expensed by firms not follow-ing SFAS No. 86 and subsequent stock returns, consistent with a delayedinvestor reaction to product development of these companies.

In probing the reasons for the software producers' change in attitudetoward the capitalization of software development costs, we document asignificant mid-1990s shift in the impact of software capitalization on re-

ported earnings and return on equity of software companies. Whereasin the early period of SFAS No. 86 application (mid- to late-1980s) soft-ware capitalization increased reported earnings more than the decreasein earnin gs by the am ortization of the software asset (since that asset wasstill small), during the early 1990s the gap between the earnings impactsof capitalization and amortization narrowed, and in 1995 the capitaliza-tion and amortization positive and negative effects were roughly offset-ting. This impact on reported performance may have been among thereasons underlying the 5PA's petition to abolish SFAS No. 86. Analysts'objection to capitalization may be related to the random element intro-

duced by capitalization to reported earnings which, in turn, complicatesthe forecasting task. Indeed, we find that analysts' earnings forecast er-rors are positively associated with the intensity of software capitalization.

Our evaluation of the ten-year record of software capitalization in theUnited States is timely given the current interest in accounting for in-tangibles. For example, the FASB has recently established a Task Forceon Business Combinations to examine, among other things, the account-ing treatment of acquired intangibles, some of which (jR&'D-in-process)are immediately expensed by acquirers (Deng and Lev [1998] ).^ Also, the

Accounting Standards Executive Committee of the AICPA (AcSEC) re-leased in March 1998 a Statement of Position on accounting for softwarefor internal use (SFAS No. 86, the focus of this study, deals with softwareintended for sale), calling for the capitalization of certain developmentcosts in a similar manner to SFAS No. 86. Abroad, the International Ac-counting Standards Committee (IASC) is about to issue Standard No. 38on intangibles, which calls for the capitalization of internally developedintangibles with identifiable benefits (IASC [1998]). W hile SFAS No. 86deals only with the capitalization of postfeasibility dev elopm ent costs, anassessment of the record of SFAS No. 86 should benefit the reexamina-

tion of accounting for intangibles.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 4/32

1 64 DAVID ABOODY AND BARUCH LEV

2. Sam ple Selection and Summary Statistics

The initial sample for this study was the 463 firms on the 1995 Com-

pustat Industrial and Research Files c lass if ied as com put er p ro gra m m ingand prepackaged software (S/C codes 7370 -7372 ). We excluded 130 firmswith fewer than three years of existence as public companies during1987-95, to accommodate certain tests which require limited time-seriesdata (e.g., for computing two-year lagged changes in earnings). Eightyof the 130 firms deleted had an initial public offering in 1994 or 1995,wbile the remaining 50 were acquired or ceased to operate as publiccompanies after fewer than three years.^ We also excluded 64 firms thatwere not engaged in developing software products and 56 firms (primar-ily non-U.S. registrants) with no price or return data on the 1995 CRSPdatabase. Finally, we deleted 30 firms for which no or only one financialstatement could be located on Laser Disclosure or Lexis/Nexis (from whichwe obtained information missing from Compustat), as well as 20 firmswhich reported only purchased software, or for which information per-taining to internally developed software could not be separately iden-tified. The final sample consists of 163 software companies.

We used bo th the Current and Research Compustat Tapes to avoid sur-

vivorship bias. For example, a firm that was publicly traded during198 7-90 b ut failed in 1991 will be included in the sample. A m inor sur-

vivorship bias, however, may have been introduced by excluding firmswith less than three years of data, which eliminates from the samplerecent (1994 and 1995) IPOs.

Because Compustat generally aggregates the capitalized software assetwith other assets and includes the related amortization with cost of sales,we obtained the financial statements of the sample companies from La-ser Disclosure and Lexis/Nexis databases. We collected the following data:net capitalized software asset, the annual software development expense,the annual capitalized software amount, the annual amortization of thesoftware asset, and the occasional write-offs of capitalized software.'

Table 1 provides summary statistics for the sample companies.^ Thesales and total assets figures indicate that over the examined period

^ Following is our analysis of th e 50 deleted companies. T he financial data of 9 compa-nies were not available on Laser Disctosure. Eight companies did not engage in softwareproduction. Of the 33 remaining firms, 23 capitalized software development costs and 10fully expensed such costs, a ratio of capitalizers-to-expensers similar to that of our sample.The 33 deleted firms were public an average (median) of 18.1 (18.0) months. Twentycompanies were purchased (18 in pooling transactions and 2 in purchase transactions)and 13 companies went bankrupt. In section 5.1 we comment on the effects of including

the deleted companies on our regression results.'W e identified 58 software asset write-offs by our sample com panie s. Given this smallnumber, we did not examine the write-offs separately.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 5/32

THE VALUE RELEVANCE OF INTANGIBLES 165

I

bo

I

I,

1f

I

.2 '

I'S .

& 1

c

dan

s

c

da

1)

c

1)

dau

Ca

s

lan

u

s

Me

la

s

c<u

%

laV

Ye

in

CO

o

Ol

o

in

o

so

6CO

CO

CM

CO

O

O

o

6Ol

to

00

in

!0

o

9CM

00

in

1

CO

o

to

CM

o

CM

o

o

o

8

CO

to

CM

§o

o

o

CM

CO

CM

00

(31

CO

CO

oCOto

00

9in

CO

00

to

1

CO

o

in

CM

o

in

o

CO

oo

Ol00

CM

o

o

to

CO

00

c-lto

CO

00

O)

1

CO00

COCO

6

oCO

o

o

in

o

o

o

oCO

to

00

CM

00

oo

o

CO

o

1

CM

CO

00CM

1

to

CO

OlCO

9

CM

CO

o

in

CM

o

CO

o

o

o

• *

in

f;CO

oo1

CO

o

o

1

00

ino

OlCM

1

CO

in

to

Ol

9

oCO

o

to

C M

O

o

o

o

o

to

in

CO

o

o

CO

o

t31

O l

1

o

CO

in

CO

in

in

9

9

in

CM

o

t;

o

o

o

o

to

oin

00

00

CO

in

o1

00

o

Ol

1

CM

Ol

4

to

1

CM

O

o

OlCM

9

oc-l

o

Oi

o

Ol

o

oo

o

to

00

in

to

Ol

CO

00

oo

in

o

into

2

CO

to

Ol

Ol

2

in

CO

in

oCO

9

o

00

oo

00

(-1

o

oo

o

8to

0o1

o

toto

2

Ol

CO

5

COCM5

Ol

oin

1

9

a.

I2'3.S

a.o

.Sa lmInc ^

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 6/32

16 6 DAVID ABOODY AND BARUCH LEV

(1987-95) software companies, on average, quadrupled in size (dou-bling at tbe median). For both sales and total assets, tbe means are sub-stantially larger than the medians, indicating that the sample includes a

small number of very large companies. The increasing sample size (AOindicates that the software industry has not yet gone through a "shake-out period," typical of maturing industries, where the number of firmsgrows quickly during an initial stage, which is followed by a fast decline(shakeout) and stabilization of the number of competitors.^

The return on equity (ROE) figures in table 1 indicate that the me-dian sample ROE ranged between 10% and 20% during 1987-92, de-creasing to 8-15 % in 1993- 95 (the m ean i^QE fluctuates widely becauseof a few outliers).1" Th e redu ced ROE figures in recent years, reflecting

intensified competition and continued entry, are yet another indicationthat the software industry has not reached maturity. The steadily in-creasing market-to-book ratio, at both the mean and the median, indi-cates that investors' growth expectations of the software industry keeprising. The median debt-to-equity ratios are very small, yet at the mean,a software company has rough ly a 5:1 capitalization ratio , at book values.

Capitalization intensity (the annually capitalized portion of softwaredevelopment costs divided by total development costs, expensed as wellas capitalized) is among the key variables we examine. Both the meanand median values are stable at 25-30% through 1992 and decline

thereafter. This apparent sharp decline of capitalization intensity isdriven mainly by recent entrants to the industry, who tend to capitalizeless than older com panies. For exam ple, in 1987, sample firms tha t werepublicly traded for two years or less had a mean (median) capitalizationintensity of 30% (27%), whereas in 1995, similarly young firms had amean (median) capitalization intensity of 7.9% (0%).^^ In contrast, ma-ture sample firms that were public for at least eight years had a stablemean capitalization ratio of 23% throughout the 1987-95 period, whiletheir median capitalization intensity decreased from 18% to 15%.

Young companies may have low capitalization intensities because mostof their software development efforts have not yet reached the tech-nological feasibility stage required for capitalization (see Appendix A).Alternatively, analysts' frequent claims that software capitalization "con-taminates" financial reports and reduces earnings quality may have astronger effect on young firms trying to establish reporting credibility

8 On the industry shakeout phenomenon, see, for example, Gort and Klepper [1982]and Klepper and Graddy [1990].

1" The mean ROE series is influenced by ten very small firm-year observations (eightindependent firms) with a mean (median) book value of $1.24 million ($1.21 million).Removing those ten firm-years from the sample considerably reduces fluctuations in themean ROE.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 7/32

TH E VALUE RELEVANCE OF INTANGIBLES 16 7

than on mature companies. Analysts' skepticism concerning capitaliza-tion may have also induced some profitable mature firms to curtail cap-italization. Nevertheless, despite the recent decline in capitalization

intensity, many software companies still capitalize a substantial portionof development costs, as evidenced by the fact tbat the top quartile ofthe sample firms (ranked by capitalization) had a median capitalizationintensity of 48% in 1995.

3. Distinguishing "Cap italizers" from "Expen sers"

Since SFAS No. 86 affords considerable implementation flexibility tosoftware companies, it is important to distinguish at the outset betweensoftware capitalizers and immediate expensers.^2 Doing so sheds lighton whether capitalization is practiced by underperforming companiesto enhance their reported earnings and provides control variables.

Since SFAS No. 86 conditions capitalization on the technological as-pects of software development (e.g., the "product design" or a "workingmodel" must be completed prior to capitalization), economic factorsunderlying software development may influence the decision to capi-talize or expense. For example, immediate expensing may be suitablefor products with a short development period, while capitalization fitsproducts developed over several years. Since the specifics of firms' pro-

duction functions are difficult to identify from public information, weproxy for them by categorizing the sample firms by the type of productsdeveloped. We adopt the four software product types (or industry subdi-visions) used in the Deloitte and Touche [1996] annual survey: engi-neering, education and entertainment, business applications, and PCpackaged software.'^

'2 It is relatively easy for software companies to justify immediate expensing. For exam-ple, SFAS No. 86 requires that the expected net realizable value of the project exceed the

capitalized value of the software asset. Given the subjectivity in assessing expected net re-alizable values, it seems that managers who prefer immediate expensing can easily justifythis approach.

''Following are descriptions of the four product types taken from financial reports: En-gineering—"The firmdesigns, produces, and markets proprietary computer software prod-ucts for use in computer aided engineering." Education and Entertainment—"Develops,publishes, manufactures, and distributes high-quality educational software products forhome and school use." Business Applications —"Develops, licenses, and markets system soft-ware products, including monitoring and event management tools, back up and recoveryproducts, and data-base adm inistration tools to improve performance, reliability, and man-ageability of large scale mainframe systems software, open systems data bases, and variousother systems." PC Packaged Software—"Designs, develops, and markets systems and appli-

cation software which enab les users to work with professional creative too ls, assemble illus-trations, image, and text into fully form atted docum ents, ou tput d ocum ents directly to any

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 8/32

16 8 DAVID ABOODY AND BARUCH LEV

We then categorized as "expensers" firms that immediately expensedall of their software development costs; and as "capitalizers" those thatcapitalized a portion of those costs. Of the 163 sample firms, 34 ex-

pensed all of their development costs in every sample year, and 102firms capitalized a portion of their development costs every year. Fifteenfirms capitalized development costs in all but one year, and wereclassified as "capitalizers." Twelve companies that expensed in one pe-riod and capitalized in the other were classified as "expensers" in theperiod they exp ensed and "capitalizers" in the p eriod they capitalized. ^

Our classification of sample firms by product type and accountingpolicy (capitalization verstis full expensing) indicates that engineeringis the only product type where nearly all firms (96.7%) capitalize devel-

opment costs. However, this product type constitutes only 7.1% of thesample observations. In the other product types (education and enter-tainment, business applications, and PC packaged software) between65 % and 80% of the firms capitalize development costs, and pairwisesignificance tests for the differences between the number of "capitaliz-ers" and "expen sers" across the p rod uc t types failed to reveal statisticallysignificant differences (at the 0.05 level). We therefore con clud e th atproduct type does not systematically discriminate between "capitalizers"and "expensers."

To distinguish between "capitalizers" and "expensers," we considered

attributes derived from the debate which surrounded the 1985 softwarecapitalization Exposure Draft {FASB [1985]), where conjectures concern-ing why, when, and who will expense or capitalize development costswere advanced. Following are the discriminating candidates examined:

1. Firm Size, measured as the log of market value of equity threemonths after fiscal year-end. Large firms tend to spend a substantialpart of software development costs on basic research and on mainte-nance and upgrades of their products. These costs are expensed accord-ing to SFAS No. 86 (see Appendix A), and consequently, large firms areexpected to expense a larger share of development costs than smallerfirms.

2. Software Development Intensity, measured by the ratio of annual soft-ware development costs to sales. To the extent that economies of scalecharacterize the software industry, firms that spend more on softwaredevelop me nt will experien ce, on average, a higher success rate in devel-oping products, leading to a larger capitalization share. Accordingly, weexpect a positive association between development intensity and capital-ization rate.

3. Profitability, measured by net income converted to full expensing

(i.e., income plus software amortization, minus the annually capitalized

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 9/32

THE VALUE RELEVANCE OF INTANGIBLES 169

TABLE 2Eirm Attributes Associated with Capitalization Intensity

Regression Analysis for 778 Eirm-Years from 1987-95

95

= IK=87

Independent Variable

MV(Size)

X (Profitability)

Devint (Development Intensity)

Leverage

Beta (Systematic Risk)

Adjusted «2

Coefficient Estimate

-0.007

-0.040

0.269

0.001

0.006

(-Statistic

-4.397

-4.286

6.024

1.848

1.506

0.148

Variable definitions: CAPVAL is the annually capitalized development cost divided by year-end mar-ket value (zero for "expensers"). AfV(size) is the log of market value of equity three mon ths after fiscalyear-end. X (profitability) is net income plus theannual software amo rtization minus the ann ual capi-talized software (that is, earnings under full expensing) divided hy sales. Devint (development inten-sity) is the annual software development costs (capitalized software development plus softwaredevelopment expense) divided hy sales. Leverage is the long-term deht divided by equity (minus thesoftware asset), andbeta (systematic risk) is the CAPM^ of the stock, estimated over 100 days prior tofiscal year-end.

software) divided by sales. Given analysts' skepticism about software cap-italization, it is widely believed that profitable companies avoid capitali-zation in order not to taint tbe perceived quality of their earnings in

analysts' eyes.

4. Leverage, measured by long-term debt divided by book value of eq-

uity (minus the software asset). Leverage is a proxy for the restrictive-ness of loan covenants as motivators of capitalization; firms closer to

loan restrictions may favor capitalization which increases equity and

earnings.

3. Systematic Risk, or p. Basic research is in general riskier than prod-uct development. Basic research is also expensed according to SFAS No.

86, while product development is capitalized. Thus riskier firms, namely,those devoting a larger share of development efforts to basic research,can be expected to expense more than less risky companies.

Table 2 reports coefficient estimates from a regression of capitaliza-tion intensity (scaled by market value) on these five firm-specific at-

tributes.'^ The four variables found to be statistically significant at the

0.01 level are: size (log of market value), /r m profitability, software develop-ment intensity, and leverage (the latter is significant at the 0.05 level). The

signs of the significant coefficients are in the expected direction, indi-cating that smaller, less profitable, more leveraged firms, and those with

a higher ratio of development costs to sales (development intensity).

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 10/32

170 DAVID ABOODY AND BARUCH LEV

tend to capitalize more of their software development costs. Accord-ingly, in subsequent tests we control for those variables by including in

the regressions the predicted value of the discriminating regression.'^

4. Is Software Cap italization Value Relevan t'?

"Sophisticated investors will discount the earnings of software devel-opers by the amount of capitalized development expense. The financialand investment community will discount the assets of software develop-ers to limit the risk that balance sheets contain assets whose values are

overstated. Only unsophisticated investors will be fooled" (Systematics,Inc., letter to the FASB, November 13, 1984, on behalf of nine major

software producers). This letter claims that the relevance of softwarecapitalization ranges from the nonexistent (to sophisticated investors)to the negative (for the unsophisticated). We examine the value rele-vance of software capitalization using thr ee app roaches : associating stockreturns with contemporaneous financial data, associating prices with fi-

nancial data, and examining the predictive ability of capitalization datawith respect to subsequent earnings.

4.1 ANNUAL CAPITALIZATION DATA AND STOCK RETURNS

An association between unexpected capitalization-related items and

contemporaneous annual stock returns indicates the extent to whichthe information contained in software capitalization is consistent withthat used by investors (such an association test cannot, of course, indi-cate whether investors actually used capitalization data in assessing secu-rity va lues). We estimate the following cross-sectional regression:

95

Rn = X

+ ei, (1)

where R i is the firm's annual stock return, cumulated from ninemonths before fiscal t year-end through three months after it,ACAP^^ is

the annual change in the capitalized amount of software developmentcosts, AEXPji is the annual change of software development expenses of

"expensers," and AEXPCAP^^ is the annual change of the software devel-opment expense of "capitalizers." (For "capitalizers," the annual amountcapitalized {CAP^) plus the amou nt expensed {EXPCAP^) equals the an-

nual software development costs.) AAMRT^ is the annual change in the

amortization of the software asset for "capitalizers." X," is the adjusted

(presoftware development items) annual net income of firm i in year t

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 11/32

TH E VALUE RELEVANCE OF INTANGIBLES 17 1

(i.e., reported income plus the software development expense and theamortization of the software asset). AX ft is the annual change in ad-

justed net income. YR^t is a time indicator variable that equals one if anobservation is from fiscal year Y (as defined by Compustat), and zero oth-erwise. All right-hand variables (except YR^t and CAPPREjt) in expres-sion (1) are scaled by beginning-of-fiscal-year m arke t value. Th e a nnualchange form of the software variables in (1) proxies for the unexpectedvalues of these variables.

The variable CAPPRE^ in expression (1) is the predicted value for eachfirm-year obtained from the regression of software capitalization inten-sity on the five company attributes described in the preceding section(and defined in table 2). We include this predicted value in regression

(1) to control for company attributes systematically associated with thecapitalization decision.

We applied the increm ental information test suggested in Biddle, Seow,and Siegel [1995] to expression (1). We therefore test the incremental in-formativeness (with respect to stock returns) of tbe level and changes ofthe in de pe nd en t variables. Th e test indicated that for capitalized software(CAP), expen sed de velopm ent costs of "expensers" {EXP), and expensedcosts of "capitalizers" {EXPCAP), the ann ual changes of the variables areincrementally informative at better than the 0.10 level, whereas the levelsof those variables are not informative. With respect to the annual amor-

tization {AMRT), the test indicated that both level and changes are rel-evant. However, the level and the ch ang e of AMRT are highly corr elated ,so that we found it advisable to report regression results based on thechang e in AM RZ'''' With respect to earnings, the Biddle test indicated thatboth the level and changes were incrementally informative, consistentwith the findings of Easton and Harris [1991] and Ohlson and Shroff[1992]. Accordingly, expression (1) includes the level and ann ual cbang eof adjusted earnings.

If the cbange in annual capitalized development costs (ACAP) repre-

sents value-relevant information to investors, tben Pj in (1) should bepositive. Since EXP and EXPCAP (tbe total development costs of "ex-pensers" and the portion of annual development costs expensed by"capitalizers," respectively) likely include development expenditures in-curred before technological feasibility bas been achieved, we predictbo th P2 and P3 to be positive bu t smaller than Pj. Our reaso ning is thatwhile firms will generally undertake positive expected value projects,achieving technolog ical feasibility (indicated by capitalization) confirmsto investors that the project has a positive expected value. We predict P4to be negative as it captures tbe unexpected decline in value of the soft-

ware asset. Based on previous findings, P5 and Pg are pred icted to bepositive.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 12/32

17 2 DAVID ABOOD Y AND BARUCH LEV

4. 2 TH E SOFTWARE ASSET AND SHARE PRICES

Expression (1) examines the value relevance of the annual capitalized

development costs. To examine the value relevance (in the associationsense) of the cumulative software asset presented on the balance sheet,we used the following regression:

95

Pit = S pQYYRit + hEPSit + hBVPSft + hCAPSOFTn + e^ (2 )y = 8 7

where P^ is firm i's stock price three months after fiscal year-end,is reported annual earnings per share, BVPSfi is the book value of equityper share minus the capitalized software asset per share at year-end, andCAPSOFTit is the net balance of the software asset per share (YR^ areyear dummies defined above). If investors value the cumulative amountof capitalized software, we expect |33 > 0.

Although equation (2) is frequently used in empirical research (e.g.,Collins, Maydew, and Weiss [1997]), it suffers from several shortcom-ings. AVhile the variables are all per share, and firm size (BVPS) is amo ngthe independent variables, it is not clear whether scale (size) is fullycontrolled for.'^ Moreover, omitted variables are likely to affect theprice regression (2) more than the returns regression (1), since in the

latter the omitted variables which are constant over time are eliminatedby the differencing operation.

4 .3 CAPITALIZED SOFTWARE AND SUBSEQUEN T EARNINGS

Our third set of value relevance tests examines the association be-tween capitalization-related variables and future earnings. Because theprediction of future earnings is of considerable im portan ce to investors,we interpret a positive association between capitalized software and sub-sequent earnings as evidence of value relevance. A positive associationis a priori expected, since software capitalization indicates the develop-

ment program has achieved technological feasibility and the capitalizedprojects have, in management's opinion, positive net present value.(However, if managers systematically abuse their discretion in determin-ing technological feasibility and expected profitability of the developedprojects, there should be no relation between capitalization of develop-ment costs and subsequent performance.) We also test whether the de-velop ment costs of firms which, as a m atter of policy, fully expense them(e.g., Microsoft, Novell) are nevertheless associated w ith future com panyperformance.

'^However, expression (2) is the one recommended by Barth and Kallapur [1996,

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 13/32

TH E VALUE RELEVANCE OF INTANGIBLES 1 7 3

The following cross-sectional model is used in the intertemporal test:

95

A X f, = I Po Y^Rit + Pi A X ?,_i +y = 8 7

ni + e,-, (3)

where A X ," is year t annual change in reported incom e, either operatingor net income, 6e/ore software development expenses (the software devel-opment and amortization expenses were added back to income when ap-propriate) . For firms that did not deduct software development expensefrom operating income, we of course did not make the adjustment. We

estimate expression (3) with one-year-ahead (AX,") and two-year-ahead(AX"(+i) earnings changes. (There are thus, in total, four regressionsinvolving one- and second-year-ahead operating and net income.) In (3)^^i,t-l ^^ ^^^ lagged (year t- I) annual change in reported income (ei-ther operating or net income), where software development and amor-tization expenses were added back; ACAP;^_i is the annual change incapitalized software development costs in year t - I relative to t - 2;AEXPii_i is the annual change in software development expense of fullexpensing firms in year t-l, and zero for "capitalizers"; AEXPCAP^.i isthe annual change in the development expense of capitalizing firms in

year t - 1, and zero for "expensers"; CAPPRE^.^ is the predicted valueobtained from the regression of software capitalization on the five com-pany attributes described in section 3. We include CAPPRE^.i to controlfor company attributes associated with the capitalization decision. Allright-ha nd variables in equation (3) (except CAPPRE^_i and the year in-dicators YR^f) are deflated by beginning-of-fiscal-year t - 1 market value.

We expect Pg > 0 since projects reaching technological feasibilityshould increase near-term earnings. We predict P4 to be smaller than Pgbecause investment in projects that have not reached technological fea-sibility should take, on average, more than a year or two to be reflected

in earnings. Moreover, the development cost expensed by capitalizingfirms {AEXPCAPit) may also reflect the cost of failed projects which, nat-urally, will not contribute to future earnings. We have no prediction forP3, since fully expensing firms provide no information to distinguish be-tween projects before and after technological feasibility, or for the othercontrol variables {YR^, AXfj.^, and

5. Empirical Eindings

5.1 CONTEM PORAN EOUS ANALYSESTable 3 presents estimates of regression (1) for the pooled sample and

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 14/32

174 D A V ID A B O O D Y A N D B A R U C H L E V

S

• o

£ I< Iua

&

•^ m en

d 4

ti l> 00a; o oS ^ "!

00 t^

00 eo

.2

I- c

2 ''J

in toQQ {^ l O 00

CO lO

I > CT >

CT l 0 0 CO

C l f^ CO *^ "*

o o ^

o i^A ^

u o o.9 <- u_ XI .o

§ E 6«J 3 3 — (M

S Z Z N N

2 5=0 1-2 4

c E

a; •« X)

K - 3 .

o•o

11Ji E

E ,~ bo c

5 I E

rt

c s

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 15/32

TH E VALUE RELEVANCE OF INTANGIBLES 17 5

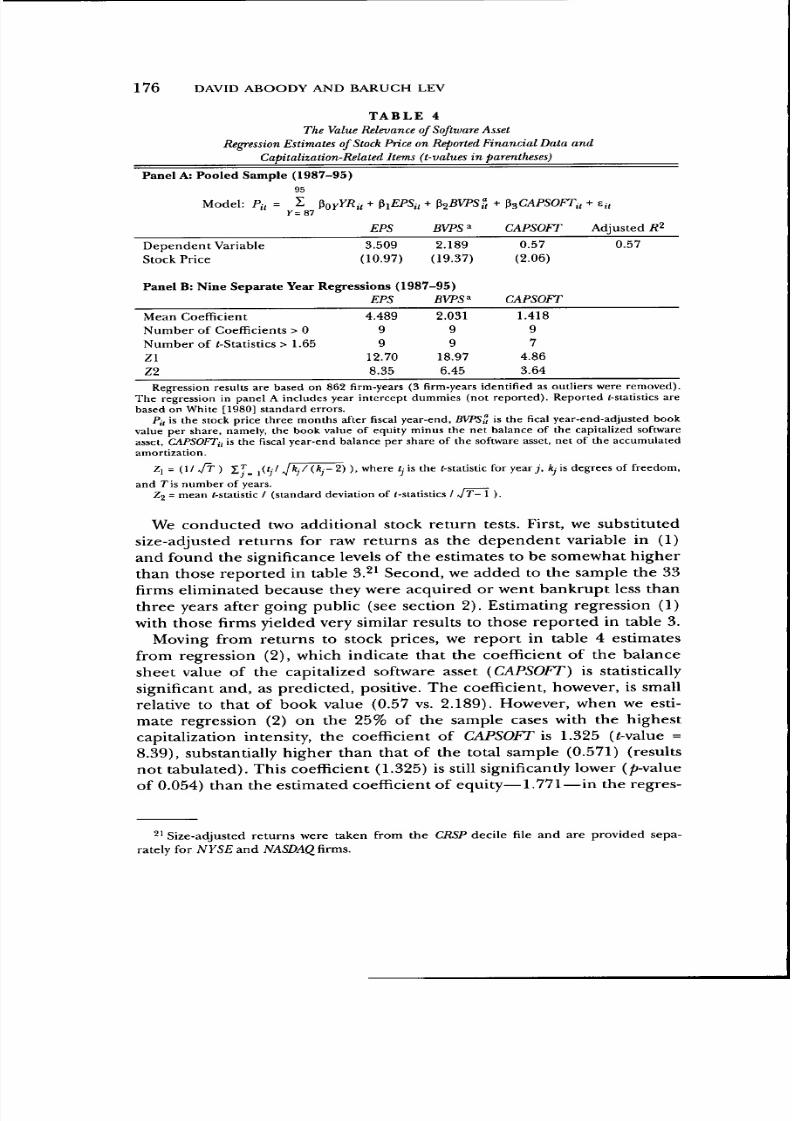

highly statistically significant. In addition, as reported in panel B, theun expected software capitalization coefficient (ACAP) is positive in all

of the nine annual regressions, with ^statistics>

1.65 in six of nine years.The across-years significance level of ACAPis 0.01, as indicated by bothZ-statistics.^^ The yearly regressions also indicate that the estimatedcoefficient of unexpected amortization (AAMRT) is negative in all years,as expected, with ^statistics > | l .65| in four of nine years (the across-years significance level is 0.01 for Zl and for Z2).^^

In contrast to the large and highly significant coefficient of the soft-ware capitalization variable (ACAP), the estimated coefficient of fullyexpensed development costs (AEXP) is only 0.667 (^-statistic = 1.394). Inthe individual year regressions (bottom panel of table 3), the coefficient

of AEXP was positive in seven of the nine regressions and statisticallysignificant (t > 1.65) in three regressions. The low significance level ofthe unexpected development costs incurred by "expensers" may be par-tially due to the small number of observations (152) in this subsample,or it may reflect investors' reaction to the absence of information in thefinancial reports of full expensers on the progress of their developmentefforts.

The coefficient of the portion of development costs expensed by "cap-italizers" (AEXPCAP) is statistically insignificant in the pooled regres-sion (t = -0.118) as well as in each individual year, perhaps becauseinvestors cannot distinguish between the portion of development costsrepresenting research efforts preceding technological feasibility and theportion representing failed development efforts.

Our yearly regressions allow us to examine directly one of the claimsin the Software Publishers Association petition to the FASB—that overtime capitalized software development costs lost their relevance to inves-tors. Inspection of the yearly coefficients of the annually capitalized de-velopment cost (ACAP), not reported in table 3, indicates the contrary:the coefficients of A CAP were insignificant in the early sample years,

1987-89, and statistically significant (at the 10% level) in each of theyears, 1990 to 1995. This suggests that over time the credibility of theamounts of capitalized software development costs increased in capitalmarkets rather than decreased.

Zl-statistic, which assumes residual independence, is (\l JT ) x ' =

Jkj/(,kj-2) j where tj is the (-statistic for year), kj is degrees of freedom, and Tis number

of years. The Z2-statistic, which accounts for cross-sectional and temporal residual depen-

dence, is mean (-statistic / (standard deviation of (-statistics / jT - 1 ) (see White [1984]).2" All the reported (-statistics are based on White's [1980] standard errors. Diagnostic

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 16/32

176 DAVID ABOODY AND BARUCH LEV

TABLE 4

Th e Value Relevance of Software Asset

Regression Estimates of Stock Price onReported Einandal Data and

Capitalization-Related Items (t-values in parentheses)

Panel A: Pooled Sample (1987-95)

95

Model: P., = £ PoyJ'fiK=87

Dependent Variable

Stock Price

ii + PiEPSj

EP S

3.509

(10.97)

1+ PgBVPSf,

BVPS'

2.189

(19.37)

Panel B: Nine Separate Year Regressions (1987-95)

Mean Coefficient

Number of Coefficients > 0

Number of (-Statistics > 1.65

Z l

Z2

EPS

4.489

9

9

12.70

8.35

BVPS''

2.031

9

9

18.97

6.45

+ P3 CAPSOi

CAPSOFT

0.57

(2.06)

CAPSOFT

1.418

9

7

4.86

3.64

Adjusted R^

0.57

Regression results are based on 862 firm-years (3 firm-years identified as outliers were removed).The regression in panel A includes year intercept dummies (not reported). Reported (-statistics are

based on White [1980] standard e rrors.Pi, is the stock price three months after fiscal year-end, BVPSti is the fical year-end-adjusted book

value per share, namely, the book value of equity minus the net balance of the capitalized softwareasset, CAPSOFTi, is the fiscal year-end balance per share of the software asset, net of the accumulatedamortization.

Z] = ( 1 / / T ) X^_ i ( ' ; ' / V ^ T * J ^ ^ ) ). where ( is the (-statistic for year) , ftyis degrees of freedom,and r is number of years.

Zj = mean (-statistic / (standard deviation of (-statistics / JT- 1 ).

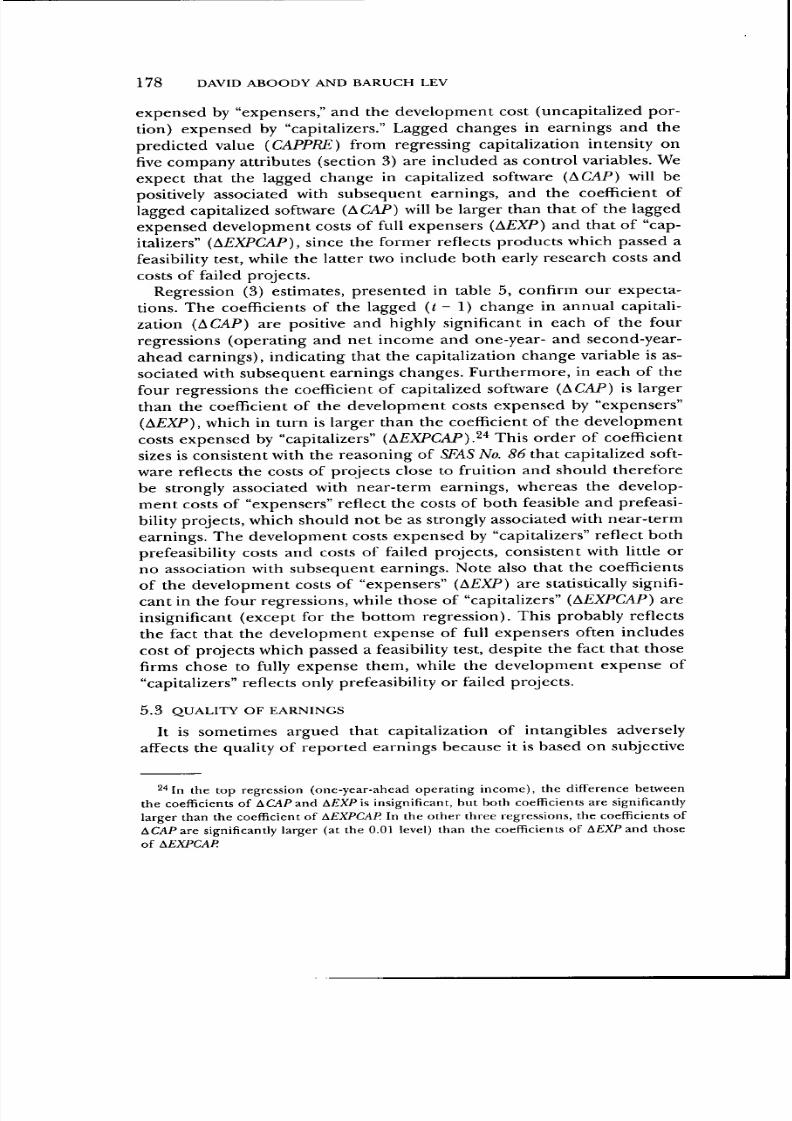

We conducted two additional stock return tests. First, we substitutedsize-adjusted returns for raw returns as the dependent variable in (1)

and found the significance levels of the estimates to be somewhat higherthan those reported in table 3.^^ Second, we added to the sample the 33

firms eliminated because they were acquired or went bankrupt less thanthree years after going public (see section 2). Estimating regression (1)

with those firms yielded very similar results to those reported in table 3.Moving from returns to stock prices, we report in table 4 estimates

from regression (2), which indicate that the coefficient of the balancesheet value of the capitalized software asset {CAPSOFT) is statisticallysignificant and, as predicted, positive. The coefficient, however, is smallrelative to that of book value (0.57 vs. 2.189). However, when we esti-mate regression (2) on the 25% of the sample cases with the highestcapitalization intensity, the coefficient of CAPSOFT is 1.325 (<-value =

8.39), substantially higher than that of the total sample (0.571) (resultsnot tabulated). This coefficient (1.325) is still significantly lower (jb-value

of 0.054) than the estimated coefficient of equity—1.771—in the regres-

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 17/32

TH E VALUE RELEVANCE OF INTANGIBLES 1 77

sion of the top 25% capitalizers, indicating that investors discount, onaverage, the capitalized software asset relative to tangible assets.

Panel B of table 4 presents estimates of equa tion (2) from individualyear regressions, 1987 to 1995. The across-years significance level of tbesoftware asset {CAPSOFT) is 0.01, as indicated by botb Z-statistics. Fur-thermore, in all nine years tbe coefficient of CAPSOFT is positive and inseven years tbis coefficient is significant at tbe 0.10 level. Tbe CAPSOFTcoefficient is insignificant in 1987 and 1988, perbaps because in tboseearly years of application of SFAS No. 86 investors were still skepticalabout tbe credibility of software capitalization.

To summarize, tbe analyses reported above indicate tbat botb tbe an-nual software capitalization amount and tbe cumulative software asset

are positively and significantly associated witb stock returns and prices,respectively.22 Wbile tbe software asset reported on tbe balance sbeetappears to be discounted by investors relative to tangible assets, we findno support for tbe Software Publisbers Association's claim tbat softwarecapitalization data are irrelevant to investors' decisions. In assessing ourfindings, it sbould be noted tbat wbile over 70% of sample firms capital-ize a portion of tbeir software development costs, tbe capitalized por-tion is, on average, ratber small, a fact wbicb works against findingsignificant associations between capitalization-related items and capitalmarket observables.

5.2 INTERTEM PORAL ANALYSIS

We augment tbe contemporaneous capital markets analysis presentedabove witb an intertemporal test of tbe association between capitaliza-tion data and subsequ ent earnings— regression (3).23 Earnings cbanges(alternatively, operating and net income) in years t and t + I are re -gressed on lagged cbanges in capitalized software, tbe development costs

2 Eccher [1995] reached a difFerent conclusion: software capitalization is not value rel-evant, while amortization of the software asset is relevant. The different conclusion ap-pears to be due mainly to sample size and period (although the methodology of the twostudies is also substantially different). While Eccher's sample period is 1988-92 (303 firm-years), ours is 1987-95 (862 firm-years). Furthermore, Eccher reports that 9% of her sam-ple firms fully expensed developm ent costs, while 20% of our sample are full expensers.

We estimated Eccher's basic regression on our data: market-to-book ratio regressed onrevenue growth, R&fD expensed, R&D capitalized, expected cash flows, and percentagewrite-offs. While Eccher finds the coefficients of RisfD expensed and R&D capitalized veryclose (leading to her conclusion that R&O capitalization is not value relevant), we find thetwo coefficients in our sample significantly different. The estimated coefficient of theR&D expense is 0.450 (p-va\ue = 0.073), while the coefficient of the capitalized R&D is

3.940 (/(-value = 0.001). The difference between these coefficients is significant at the 0.01level. In this footnote, we use the term R&D to conform with Eccher's study, while in ourpaper we use the term "software development cost."

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 18/32

1 78 DAVID ABOO DY AND BARUCH LEV

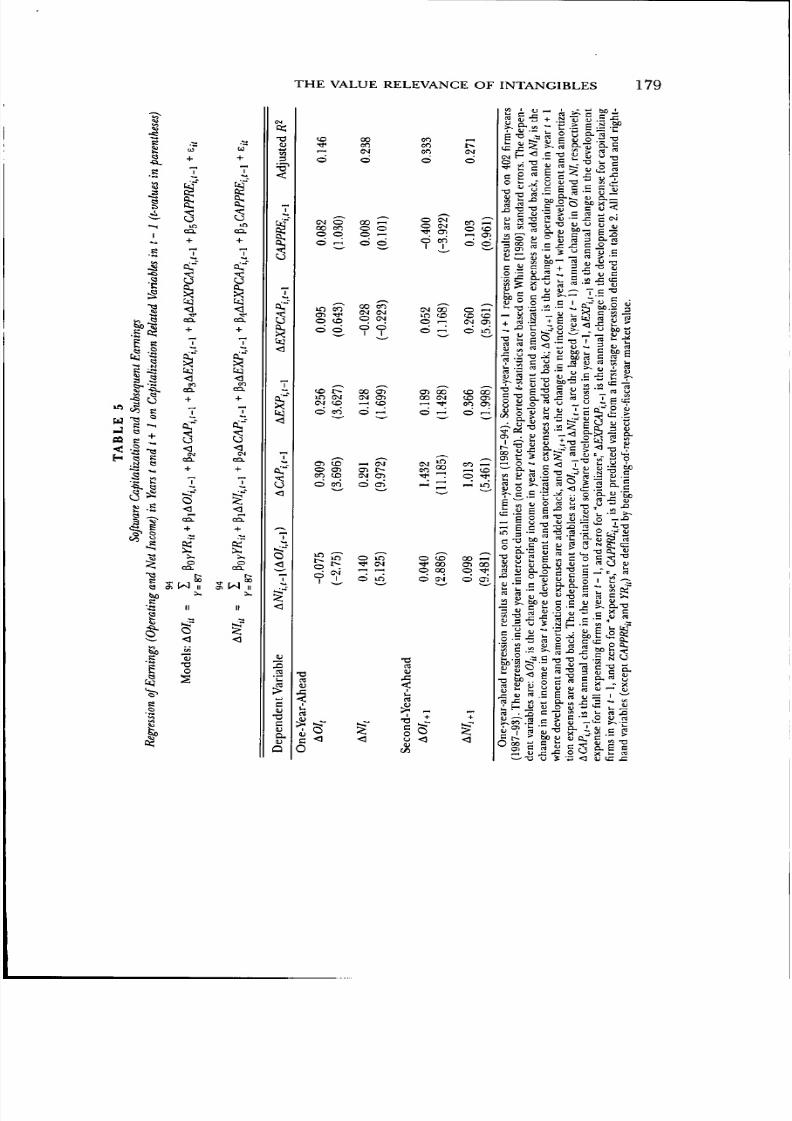

expensed by "expensers," and the development cost (uncapitalized por-tion) expensed by "capitalizers." Lagged changes in earnings and thepredicted value (CAPPRE) from regressing capitalization intensity on

five company attribute s (section 3) are inclu ded as con trol variables. Weexpect that the lagged change in capitalized software (ACAP) will bepositively associated with subsequent earnings, and the coefficient oflagged capitalized software (ACAP) will be larger than that of the laggedexpensed development costs of full expensers (AEXP) and that of "cap-italizers" (AEXPCAP), since the former reflects products which passed afeasibility test, while the latter two include both early research costs andcosts of failed projects.

Regression (3) estimates, presented in table 5, confirm our expecta-

tions. The coefficients of the lagged (t-l) change in annual capitali-zation (ACAP) are positive and highly significant in each of the fourregressions (operating and net income and one-year- and second-year-ahead earnings), indicating that the capitalization change variable is as-sociated with subsequent earnings changes. Furthermore, in each of thefour regressions the coefficient of capitalized software (ACAP) is largerthan the coefficient of the development costs expensed by "expensers"(AEXP), which in turn is larger than the coefficient of the developmentcosts exp ensed by "capitalizers" (AEXPCAP).^* This ord er of coefficientsizes is consistent with the reasoning of SFAS No. 86 that capitalized soft-

ware reflects the costs of projects close to fruition and should thereforebe strongly associated with near-term earnings, whereas the develop-ment costs of "expensers" reflect the costs of both feasible and prefeasi-bility projects, which should no t be as strongly associated with nea r-termearnings. The development costs expensed by "capitalizers" reflect bothprefeasibility costs and costs of failed projects, consistent with little orno association with subseq uen t earn ings. Note also that the coefficientsof the development costs of "expensers" (AEXP) are statistically signifi-cant in th e four regressions, while those of "capitalizers" (AEXPCAP) areinsignificant (except for the bottom regression). This probably reflects

the fact that the development expense of full expensers often includescost of projects which passed a feasibility test, despite the fact that thosefirms chose to fully expense them, while the development expense of"capitalizers" reflects only prefeasibility or failed projects.

5.3 QUALITY OF EARNINGS

It is sometimes argued that capitalization of intangibles adverselyaffects the quality of reported earnings because it is based on subjective

2''In the top regression (one-year-ahead operating income), the difference betweenthe coefficients of ACAP and AEXP is insignificant, hut both coefficients are significantly

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 19/32

THE VALUE RELEVANCE OF INTANGIBLES 179

s .

1

^

- 1 t3

M e l< • - •«

^ S I

Is

<+

s w

I:II

<u

•ao

S

00

CM

d

CM O OC "

W CO O O

9 9 q -Hd - ; ^ o

00 CO

CM CMO CM

eoeoeo CM

d

C] •^

CO -HO to

a;

i n CM CM OlCM to r-i to

d CO d r^

CM 00 O ^in to to toq H CM CT lo •—I o in

to 00to a>eo c^

d .-

gCO

d

t o

SfiCM

d

CM

d>

eo «—' to

f-<' i n

o to• * 0 0q 0 0

d CM

oo -HCl 00

o ^

c <

o

as<j s si

-" - ^-r

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 20/32

18 0 DAVID ABOODY AND BARUCH LEV

assumptions and is open to manipulation.^^ If indeed investors perceiveearnings under full expensing of software development costs to be ofhigher quality than earnings under capitalization, that is, if investors

adjust the latter for the software capitalization, then the association be-tween adjusted earnings (where the capitalization is reversed) and stockreturns should be stronger than that between reported earnings (re-flecting capitalization) and stock returns.

We examined this question by regressing annual raw returns on thelevel and change of reported earnings, and alternatively on the level andchange of adjusted earnings (the adjustment involves subtracting the cap-italization of development costs from earnings and adding back to earn-ings the amortization of the software asset). Both the level and change of

earnings are deflated by the beginning-of-period market value of thefirm.We find that the estimated coefficients of the level and changes of

reported earnings (0.441 and 0.528) are higher than the coefficients ofadjusted earnings (0.265 and 0.373), and the R^ of the former regres-sion (0.062) is reliably larger (at the 0.08 level) than that of the latterregression (0.036). We thus find no evidence that software capitalizationreduces earnings quality.

6. Delayed Reaction to Expensing?

Evidence derived from the stock return analysis (table 3) indicatesthat investors distinguish between capitalized and expensed software de-velopment costs; while unexpected values of the former are positively as-sociated with stock returns, unexpected values of the latter are not. Theinsignificant coefficient {AEXP in table 3) of the development costs offirms which, as a matte r of policy, fully expense those costs is intrigu ing,since those firms obviously develop projects which pass feasibility tests.After all, many of the full expensers are successful software developers,and their profitability is, on average, higher than that of firms which

capitalize developm ent costs (see table 2). A possible explan ation forthe insignificant coefficient of the development costs of full expensers isthat, absent disclosures about the progress of projects under develop-ment, investors cannot distinguish among costs of projects that passedthe feasibility stage, prefeasibility costs, and costs of failed projects.^^Given this uncertainty, investors may discount the development costs offull expensers.

5 For exam ple: "And, the last point, which I think is a critical po int from my view is tha t

[software capitalization] overall would reduce the quality of earnings. It would make it

more difficult for me to assess which companies are doing well or not" (James Mendelson,

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 21/32

TH E VALUE RELEVANCE OF INTANGIBLES 18 1

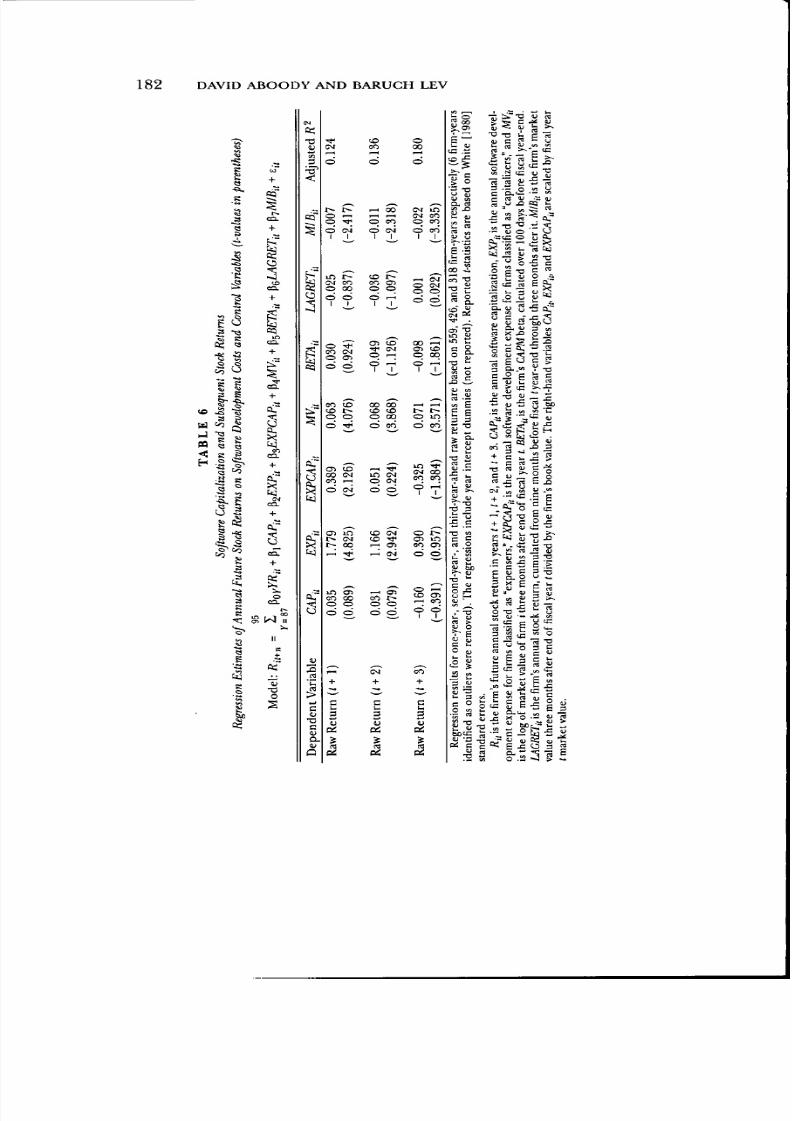

We examine this conjecture by testing for an association between cur-rent development costs and future stock returns. Specifically, if the de-velopment costs of full expensers are discounted because of investoruncertainty about the progress of the underlying projects, the resolu-tion of this uncertainty as projects reach fruition should induce positivereturns. In contrast, the development costs of "capitalizers," which pro-vide information on the success of their production efforts by the act ofcapitalization, should not be associated with subsequent returns. Thistest is formalized in (4).

95

Ri,t^n = ^Y= 87

+ t^ (4)

where Rit+n ('"•- 1>2,3) is the firm's annual stock return in the first, sec-ond, and third year after fiscal t (the return cumulation starts in thefourth month after end of fiscal t). CAP^ is the annual software capitali-zation, EXP^t is the annual software development expense of "expensers,"and EXPCAPit is the annual software development expense of "capitaliz-ers." MVjt is the log of market value of firm i three months after end offiscal year t, BETA^t is the firm's CAPMbeta calculated over 100 days be-fore fiscal year-end , LACRETn'is the firm's annua l stock return cum ulatedfrom nine months before fiscal t year-end through three months after it,and MIBji is the firm's market value three months after end of fiscalyear t divided by its book value. The right-hand variables CAP,,, EXP^,and EXPCAPit are scaled by fiscal year t market value. Size (MV;,), risk(BETAit), and market-to-book (MIB^) are risk and performance controlvariables (e.g., Fama and French [1992]). The recent return (LAGRETn)accounts for price momentum (Brennan, Chordia, and Subrahmanyam[1998]). Controlling for those risk and performance dimensions allowsus to focus on the incremental association between software development

costs and subsequent returns.Estimates of (4) are reported in table 6 for each of the three years fol-

lowing year t. Consistent with our conjecture, the development costs offull expensers (EXP), which were not associated with contemporaneousreturns (table 3), are positively and significantly associated with futurereturns. The size of the coefficient decreases over time as informationabout products under development is revealed to the market.^^ The in-formation revelation is relatively quick (2-3 years), commensurate withthe typically short production period of software products. The associa-tion between full expensers' development costs and subsequent returns

2'We also estimated regression (4) for individual years 1985-94 (not reported in table

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 22/32

182 DAVID ABOODY AND BARUCH LEV

is u

d CM d CM

in i>CM COq 00

d d

I I

o • *CO CMq Old d

CO !Oto i>o o

O 5 t o00 CM

eo ^

CTl int ^ CMt^ 00

? 7

q r-;d -HI I

o00

CM i nCM COO CO

rH CMO CMq qd d

0 0 - HCTl US

o oo

00 00 — I - Hto to r^ t -q 00 q inO CO O CO

in CMq CM

d d

to CMto •«>^ CTl

r^ CM

i neoo

CT l0 0

oCO

o

CT l

oo o o o

CM

+

c2u

I

i n • *CM 00CO CO

o t^CTl inC O CT l

d d

ai T3

Z g 2-S ,5£ a. u 3 en

CO

+

c

1

o

CQ

-ve

u0

fo2

c0

r

v0

IH

we(A

oi?

botc

cu

Tl

0u

u

"H

ta

kr

, sou

cc

u, 3

1jz :

" t.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 23/32

TH E VALUE RELEVANCE OF INTANGIBLES 1 8 3

is both Statistically significant and economically meaningful; on average,first-year- and second-year-ahead ann ual return s of 3.17% and 2.12%,

respectively, are associated with the fully expensed development costs.Also, as conjectured, the development costs of "capitalizers" (CAPand

EXPCAP) are not generally associated with subsequent returns. The ex-ception is EXPCAP in the first-year-ahead regression, but note its smallcoefficient, 0.389, relative to that of full expensers, 1.779. This suggeststhat capitalization information affects the contemporaneous pricing ofsecurities. Finally, it is unlikely that the different patterns of subsequentreturns of capitalizing and expensing companies are due to differentrisk characteristics, since various risk dimensions are accounted for inexpression (4) and all firms belong to the same industry.

If, as suggested by the evidence in table 6, the full expensing of devel-op m en t costs is associated with a delayed investor reaction (un de rrea c-tion), why don't all software companies capitalize development costs?Two answers are plausible. First, the delayed reaction might not be largeenough to offset other managerial considerations, such as concern withanalysts' claims that capitalization degrades the quality of earnings andthe integrity of the balance sheet. Second, managers may not be awareof the uncertainty discount we document. After all, to the best of ourknowledge, ours is the first comprehensive evidence consistent with de-layed investor reaction to full expensing of software development costs.

7. W hy the Petition to Abolish SFA S No. 86?

Our analysis indicates that data on capitalized software developmentcosts summarize information relevant to investors. What, then, promptedthe 1996 Software Publishers Association {SPA) petition to abolish SFASNo. 86'? This question is particularly intriguing, given the considerableimplementation flexibility afforded by this standard.

An analysis of the reporting consequences of intangibles' capitaliza-

tion vs. expensing (e.g.. Beaver and Ryan [1997]) suggests that early inthe life of a firm or an industry, when the growth of intangible invest-ment generally exceeds the firm's return on equity, capitalization en-hances reported income proportionately more than equity, implying ahigher reported return on equity {ROE) or return on assets {ROA) un-der capitalization than under full expensing. As the firm matures, itsprofitability generally increases, while the rate of intangible investmentdeclines; the enhancing effect of capitalization on income diminishes,while the cumulative effect of capitalization on equity or total assets in-creases, resulting in a higher ROE and ROA under expensing than under

capitalization. The inflection point lies close to the point where thegrowth rate of intangible investment equals the firm's ROE under ex-

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 24/32

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 25/32

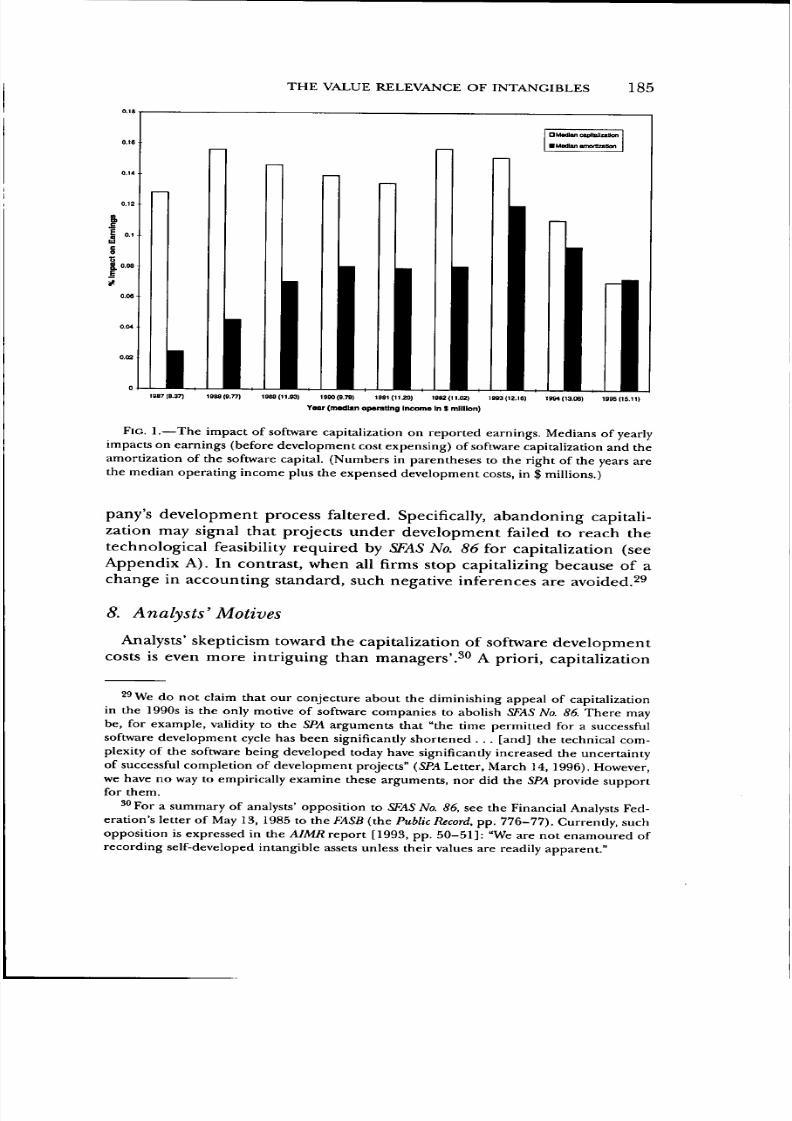

TH E VALUE RELEVANCE OF INTANGIBLES 18 5

1987(8.37) 1S88B.77 ) IS S9(lt .g3) 1990(0.70) 1901(11.201 1902(11.02) 1903(12.16) 1904(13.06) 1905(15.11)

Yaar (mwllan op erating I ncom e In $ mil l ion)

FIG. 1.—The impact of software capitalization on reported earnings. Medians of yearlyimpacts on earnings (before developm ent cost expensing) of software capitalization and theamortization of the software capital. (Numbers in parentheses to the right of the years are

the median operating income plus the expensed development costs, in $ millions.)

pany's development process faltered. Specifically, abandoning capitali-zation may signal that projects under development failed to reach thetechnological feasibility required by SFAS No. 86 for capitalization (seeAppendix A). In contrast, when all firms stop capitalizing because of achange in accounting standard, such negative inferences are avoided.^^

8. Analysts' Motives

Analysts' skepticism toward the capitalization of software developmentcosts is even more intriguing than managers'.^" A priori, capitalization

^ We do not claim that our conjecture about the diminishing appeal of capitalizationin the 1990s is the only motive of software companies to abolish SFAS No. 86. There maybe, for example, validity to the SPA arguments that "the time permitted for a successfulsoftware development cycle has been significantly shortened . . . [and] the technical com-plexity of the software being developed today have significantly increased the uncertaintyof successful completion of development projects" {SPA Letter, M arch 14, 1996). However,we have no way to empirically examine these arguments, nor did the SPA provide supportfor them.

^ For a summary of analysts' opposition to SFAS No. 86, see the Financial Analysts Fed-

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 26/32

1 86 DAVID ABOO DY AND BARUCH LEV

allows managers to inform investors about the progress and success ofthe software development program. In the worst case, if concerns aboutmanipulation are overwhelming, software capitalization can be easily

undone by subtracting the periodic capitalized amount from earnings.Of course, if well-connected analysts obtain private operating informa-tion on products under development, their success rate, and expectedmarket share, then analysts' objection to the public disclosure of suchinformation (partially provided via the capitalization and amortizationof software development costs) is understandable.

This self-serving motive is very difficult to substan tiate empirically. Wetherefore focus on another, perhaps equally compelling, explanationfor analysts' opposition to capitalization, which is related to the effect ofsoftware capitalization on the accuracy of analysts' earnings forecasts.Software development costs typically account for 20-30% of revenues;capitalization of an unknown portion of such a large cost componentincreases the difficulty of predicting the development expense (total de-velopment cost minus capitalization) and consequently predicting earn-ings, since the amount capitalized each period is determined by thelargely unpredictable success rate and profit potential of the products un-der development. Analysts concerned with the size of their earnings fore-cast errors can therefore be expected to view capitalization negatively.^^

To examine this conjecture, we computed analysts' relative earnings

forecast errors for the sample firms (reported annual earnings per shareminus Zacks analysts' forecasts, divided by stock price at year-end). Weexpect a positive association between the absolute size of analysts' fore-cast errors and the extent of software capitalization.^^ We measure theexten t of software capitalization by the an nua l am ou nt capitalized, scaled

' ' The sample data on th e relative volalility of software deve lopm ent expenses with andwithout capitalization are consistent with this conjecture. Specifically, we computed forcapitalizing firms with at least six years of data in the sample the firm-specific variance of

total annual d evelopm ent costs and the pa rt of the cost that was expen sed. By our con-jecture, the former (which is analogous to the software expense of ftill expensing firms)should be smaller than the latter. This indeed is the case; the sample mean (median) ofthe variances is 0.0957 (0.0630) for total developments costs and 0.1319 (0.0804) for theexpensed part of development costs (i.e., total cost mintis capitalization). The differencein the means (medians) is significant at the 0.07 (0.01) level. Capitalization is thus asso-ciated with an increased variance of the portion of software development cost which isexpensed.

•^ As a first cut, we computed the sample m ean and m edian of analyst forecast erro rs forsoftware capitalizing and full expensing firms. The mean (median) errors for "capitalizers"are 0.010 (0.0017) and for "expensers" 0.0079 (0.0006). Thus, consistent with our conjec-ture, the forecast errors for "capitalizers" are larger than those of full expensers (the differ-ence in the means is not significant at conventional levels, while that of the medians issignificant at the 0.01 level). The above unconditional differences in the quality of fore-

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 27/32

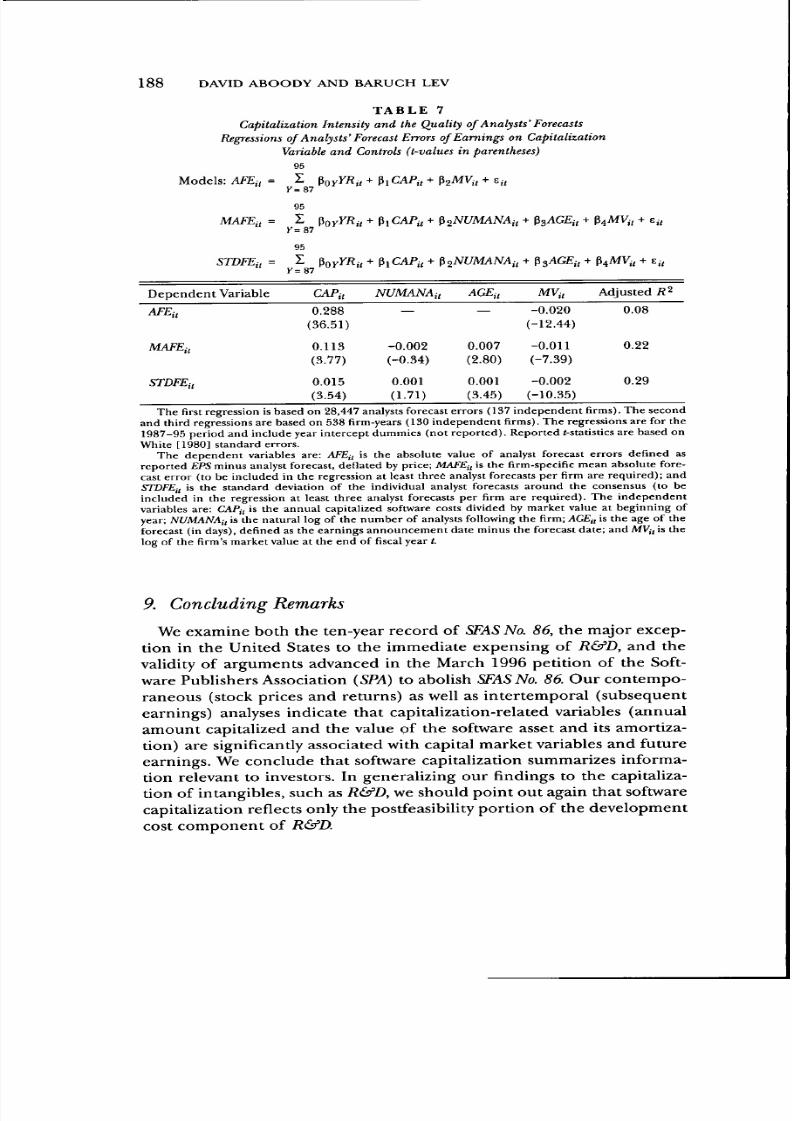

TH E VALUE RELEVANCE OF INTANGIBLES 18 7

by beginning-of-year m arke t value (CAP in expression (5)).^^ We alsocontrol for factors related to forecast accuracy: the age (horizon) of theforecast, the number of analysts io\\^o\N'\n^ the firm, and yirm size?^ Expres-

sion (5) presents our regression model:

95

FEn = IY= 87

+ Zit (5 )

where FEn is, alternatively, absolute value of individual analysts' relativeforecast errors, firm-specific average forecast error, or the firm's stan-dard deviation of the forecast error. The forecast error is measured asthe absolute value of reported annual EPS minus the forecast, scaledby end-of-year stock price. YR^ are year dummies, CAP^ is the annualamount of software development cost which was capitalized by the firm,scaled by beginning-of-year market value, NUMANAn is the number ofanalysts following the firm, AGEn is the interval (in days) between theforecast date and the earnings announcement date, and MV^ is the logof the firm's market value of equity at year-end.

Table 7 presents estimates from the th ree regression versions of (5).In a regression of absolute value of individual forecast errors on capi-talization intensity and market value, CAP is positively associated with

the absolute size of forecast errors, and size (MV) is negatively relatedto the forecast error. The second regression in table 7 reports firm-specific absolute mean forecast errors regressed on capitalization inten-sity and all three control variables. Capitalized development costs (CAP)are positively associated with analysts' mean forecast error. Forecast ageand firm size are significantly associated with the mean forecast error inthe expected direction. Finally, in the third regression, capitalization in-tensity is also significantly and positively associated with the firm-specificstandard deviation of analysts' forecasts.

Our findings are thus consistent with the conjecture that analysts' ob-

jection to software capitalization may be related to the adverse effect ofcapitalization on the quality of their earnings forecasts. This conclusionseems to run counter to our previous conclusion (section 5.2) that cap-italization improves the prediction of earnings. In fact, these findingsare not inconsistent because the findings in section 5.2 (and table 5) arefor earnings before the software expense. The analyst forecast results re-late to reported earnings after the expensing of software developmentcosts and indicate that capitalization introduces noise to these earnings.

' ' Other capitalization intensity measures— annual capitalization to total developm entcosts and the ratio of the capitalized asset to equity—yield results similar to those reportedin table 7.

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 28/32

188 DAVID ABOODY AND BARUCH LEV

T A B L E 7Capitalization Intensity and the Quality of Analysts' Forecasts

Regressions of Analysts'Forecast Errors of Earnings on Capitalization

Variable and Controls (t-values in parentheses)95

M od els: Affi,, = I Por^ '^i/ + Pi CAP^ + PaMVi, + 6,,Y = 87

STDFEi, =

95

K=87

95

,, + P4MV,, + e,,

;,+ Pi CAP;, + ,/ + Ev,

Dep enden t Variable NUMANAi, Adjusted ,

0.288(36.51)

0.113(3.77)

0.015(3.54)

-0.002

(-0.34)

0.001(1.71)

0.007(2.80)

0.001(3.45)

-0.020(-12.44)

-0.011

(-7.39)

-0.002(-10.35)

0.08

0.22

0.29

The first regression is based on 28,447 analysts forecast errors (137 independent firms). The secondand third regressions are based on 538 firm-years (130 inde pen den t firms). The regressions are for the1987-95 p eriod an d include year Intercept dummies (not rep orted ). Reported (-statistics are based onWhite [1980] standard errors.

The dependent variables are: AFEn is the absolute value of analyst forecast errors defined as

reported EPS minus analyst forecast, deflated by price; MAFEj, is the firm-specific mean ab solute fore-cast error (to be included in the regression at least thre t analyst forecasts per firm are req uired ); andSTDFEi, 's * ^ standa rd deviation of the individual analyst forecasts aroun d the consen sus (to beincluded in the regression at least three analyst forecasts per firm are required). Tbe independentvariables are; CAPi, '* 'he annual capitalized software costs divided by market value at beginning ofyear; NUMANAi, is the natural log of the number of analysts following the firm; AGEi, is the age of theforecast (in days), defined as the earnings ann oun cem ent date minus the forecast date; and AfVj, is thelog of the firm 's market value at the en d of fiscal year (.

9. Concluding Remarks

We examine hoth the ten-year record of SFAS No. 86, the major excep-tion in the United States to the immediate expensing of R&D, and thevalidity of arguments advanced in the March 1996 petition of the Soft-ware Puhlishers Association (SPA) to aholish SFAS No. 86. Our contempo-raneo us (stock prices and returns) as well as intertem pora l (suhsequentearnings) analyses indicate that capitalization-related variables (annualamount capitalized and the value of the software asset and its amortiza-tion) are significantly associated with capital market variables and futureearnings. We conclude that software capitalization summarizes informa-tion relevant to investors. In generalizing our findings to the capitaliza-tion of intangibles, such as R&D, we should point out again that softwarecapitalization reflects only the postfeasibility portion of the development

8/8/2019 _Aboody D, Lev B - The Value Relevance of Intangibles, The Case of Software Capitalization

http://slidepdf.com/reader/full/aboody-d-lev-b-the-value-relevance-of-intangibles-the-case-of-software 29/32

THE VALUE RELEVANCE OF INTANGIBLES 189

Regarding the motives underlying the SPA petition, we provide evi-

dence that during the 1990s the appeal of software capitalization in terms

of enhancing reported earnings continually diminished. As for financial

analysts' skepticism about capitalization, we provide evidence that soft-

ware capitalization is associated with larger errors in analysts' forecasts

of earnings, due to the random element introduced to earnings by cap-

italization. This adverse effect of capitalization on the quality of forecasts

may help explain the objections of some analysts to software capitaliza-

tion in particular, and to the capitalization of intangible investments

(e.g., R&D) in general.

APPENDIX A

Summary of SFAS No. 86: Accounting for the Costs

of Computer Software to be Sold, Leased,

or Otherwise Marketed ^^

This statement covers only software developed for sale, and not (1) softwaredeveloped or purchased for internal use, or (2) software developed for otherentities, based on a contractual agreement.

The first stage of a software develo pm ent program starts with the initiation of

the software project and ends when technological feasibility is achieved. All costs

incurred during this stage are expensed as research and development costs, ac-cording to SFAS No. 2 [1974].

The conditions specified by SFAS No. 86 for the establishment of technologi-cal feasibility are essentially:

1. The detail program design has been completed, and all the technical re-

quirements are met to produce the software.

2. The enterprise has confirmed completion of the program design and thatthere are no technological uncertainties concerning development issues.

All development costs incurred during the second stage—from the establish-ment of technological feasibility to the date when the software is ready to be re-