Abengoa BIO World Congress June, 2013-1 bio world congress... · BIO World Congress Multiple...

23

ABENGOA Innovative technology solutions for sustainability BIO World Congress Multiple Feedstocks to Ethanol and Beyond June 19, 2013 Chris Standlee – Executive Vice President Abengoa Bioenergy US Holding, LLC

-

Upload

truongmien -

Category

Documents

-

view

216 -

download

0

Transcript of Abengoa BIO World Congress June, 2013-1 bio world congress... · BIO World Congress Multiple...

ABENGOA

Innovative technology solutions forsustainability

BIO World Congress

Multiple Feedstocks to Ethanol and Beyond

June 19, 2013

Chris Standlee – Executive Vice President

Abengoa Bioenergy US Holding, LLC

Engineering and construction

� 70 years of experience in energy infrastructures

� Proprietary know-how

� Leading international contractor in T&D

2

1

Concession-type infrastructures

� Solar, transmission lines, desalination, cogeneration and others

� Very low market risk

� Average contract term: 25 years

2

Industrial production

� Biofuels, industrial waste recycling

� High growth markets

� Market leaders

3

Abengoa’s business is structured around three activities

Energy Environment

We perform these three activities in two high growth sectors

Our business (I)

3

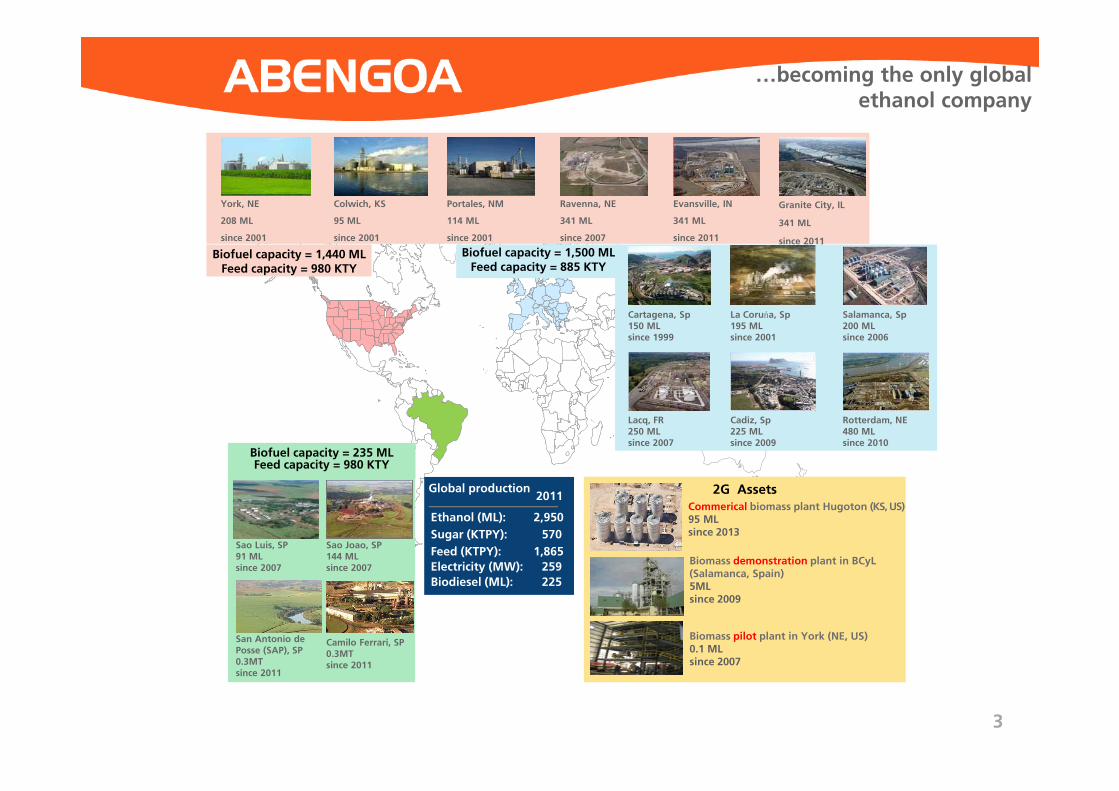

…becoming the only global ethanol company

Biofuel capacity = 1,440 ML Feed capacity = 980 KTY

York, NE

208 ML

since 2001

Colwich, KS

95 ML

since 2001

Portales, NM

114 ML

since 2001

Ravenna, NE

341 ML

since 2007

Evansville, IN

341 ML

since 2011

Granite City, IL

341 ML

since 2011

Biofuel capacity = 1,500 ML Feed capacity = 885 KTY

Cartagena, Sp150 ML since 1999

Lacq, FR 250 ML since 2007

La Coruńa, Sp195 ML since 2001

Cadiz, Sp225 ML since 2009

Salamanca, Sp200 ML since 2006

Rotterdam, NE 480 ML since 2010

Biofuel capacity = 235 ML Feed capacity = 980 KTY

Sao Luis, SP 91 ML since 2007

Sao Joao, SP 144 ML since 2007

San Antonio de Posse (SAP), SP 0.3MT since 2011

Camilo Ferrari, SP 0.3MT since 2011

Global production

Ethanol (ML):

Sugar (KTPY):

Feed (KTPY):

2,950

2011

570

1,865

Electricity (MW): 259

Biodiesel (ML): 225

2G AssetsCommerical biomass plant Hugoton (KS, US) 95 ML since 2013

Biomass demonstration plant in BCyL(Salamanca, Spain) 5ML since 2009

Biomass pilot plant in York (NE, US) 0.1 ML since 2007

4

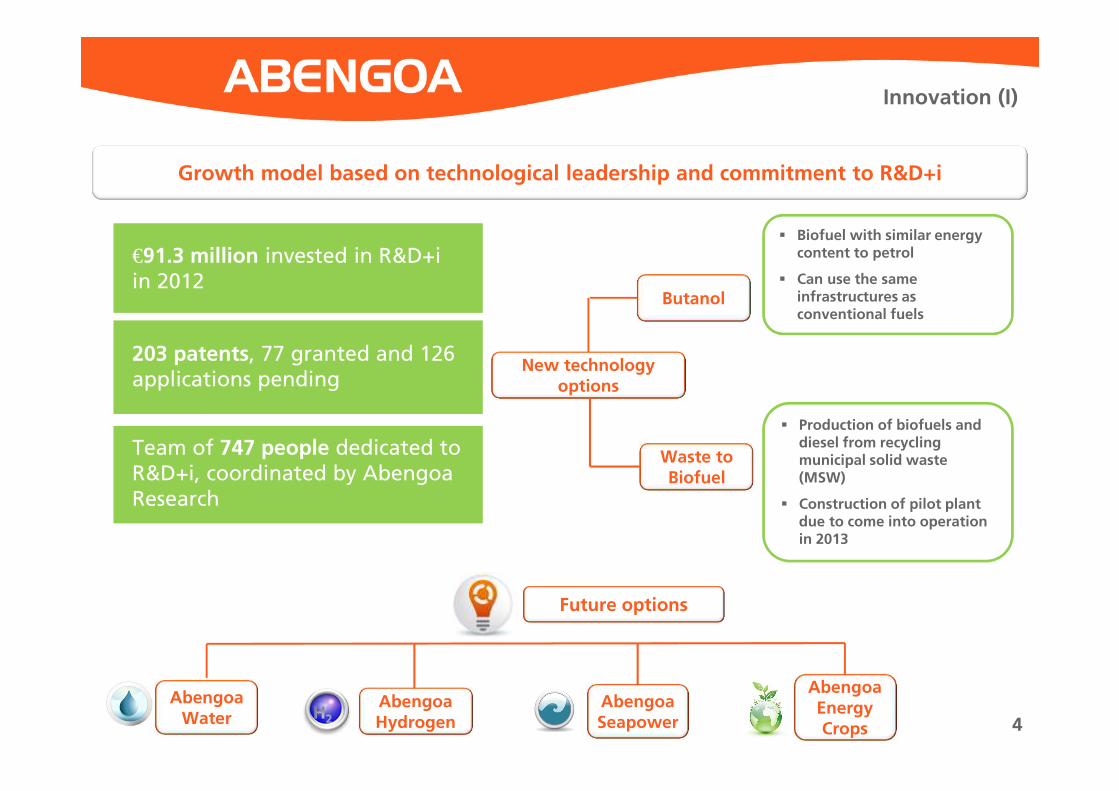

Innovation (I)

Growth model based on technological leadership and commitment to R&D+i

€91.3 million invested in R&D+i in 2012

203 patents, 77 granted and 126 applications pending

Team of 747 people dedicated to R&D+i, coordinated by Abengoa Research

Future options

Butanol

New technology options

Abengoa Water

Abengoa Hydrogen

Abengoa Energy Crops

Abengoa Seapower

Waste to Biofuel

� Biofuel with similar energy content to petrol

� Can use the same infrastructures as conventional fuels

� Production of biofuels and diesel from recycling municipal solid waste (MSW)

� Construction of pilot plant due to come into operation in 2013

Multi-bioproduct platform

Biofuels Power

BioPlasticsBiochemicalsW2B

2G biofuels Solid waste-to-biofuels

Technology applied to Agricultural

Biomass& Bagasse Conversion

We have used technology to develop a new platform…

Technology IP platform

3,000 ML/year existing sugar/biomass capacity in

operation

5

Core competencies

6

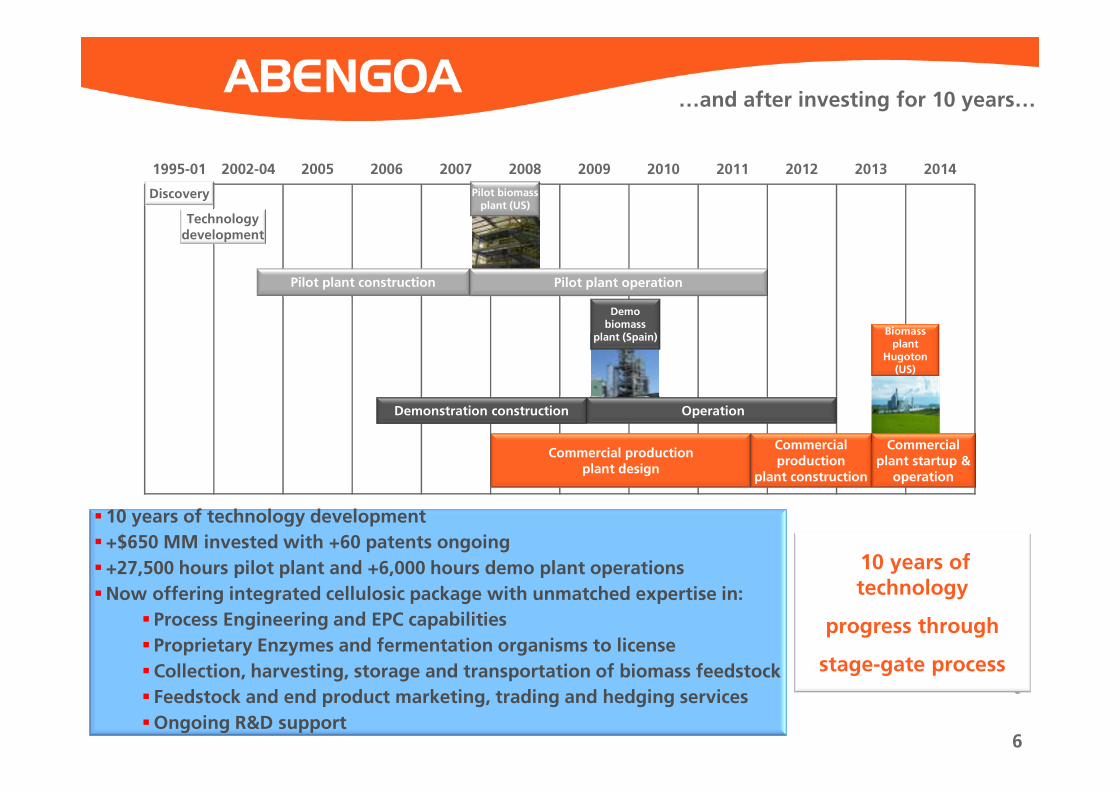

10 years of technology

progress through

stage-gate process

� 10 years of technology development

�+$650 MM invested with +60 patents ongoing

�+27,500 hours pilot plant and +6,000 hours demo plant operations

�Now offering integrated cellulosic package with unmatched expertise in:

� Process Engineering and EPC capabilities

� Proprietary Enzymes and fermentation organisms to license

�Collection, harvesting, storage and transportation of biomass feedstock

� Feedstock and end product marketing, trading and hedging services

�Ongoing R&D support

…and after investing for 10 years…

6

1995-01 2002-04 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Discovery

Pilot plant construction

Demonstration construction Operation

Commercial production

plant construction

Commercial plant startup &

operation

Pilot biomass plant (US)

Demo biomass

plant (Spain)Biomass plant

Hugoton (US)

Commercial production plant design

Technology development

Pilot plant operation

7

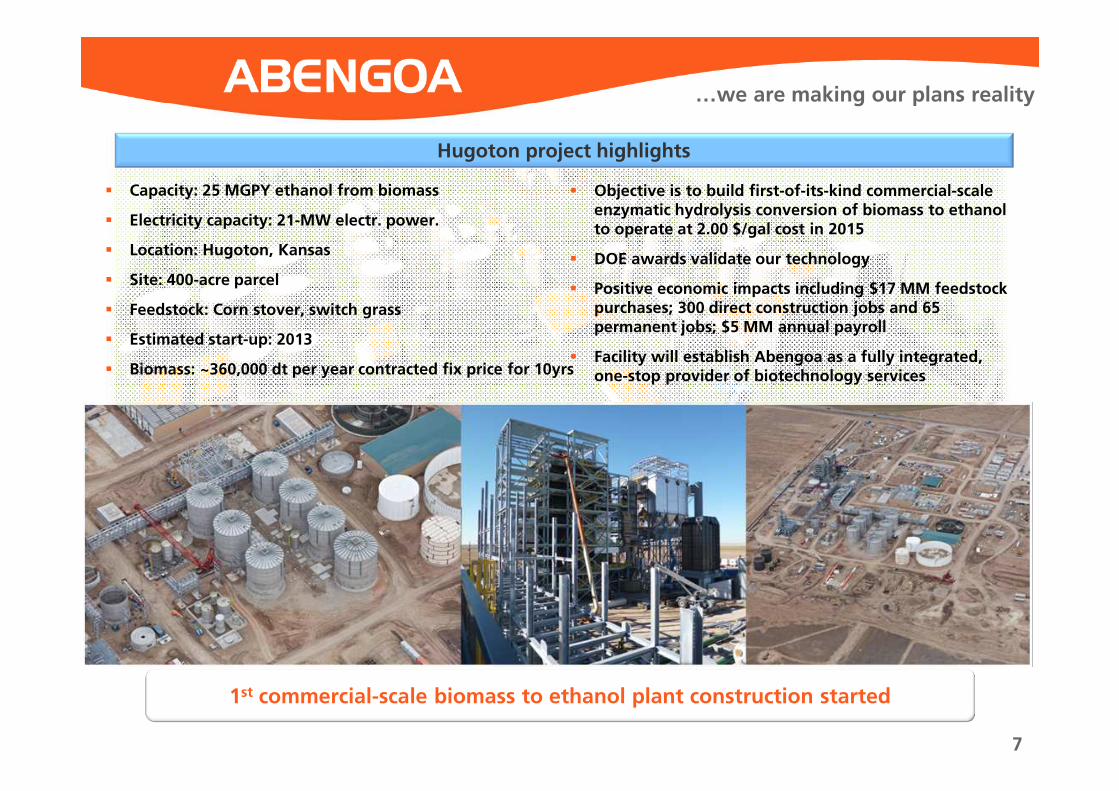

…we are making our plans reality

1st commercial-scale biomass to ethanol plant construction started

� Capacity: 25 MGPY ethanol from biomass

� Electricity capacity: 21-MW electr. power.

� Location: Hugoton, Kansas

� Site: 400-acre parcel

� Feedstock: Corn stover, switch grass

� Estimated start-up: 2013

� Biomass: ~360,000 dt per year contracted fix price for 10yrs

Hugoton project highlights

� Objective is to build first-of-its-kind commercial-scale enzymatic hydrolysis conversion of biomass to ethanol to operate at 2.00 $/gal cost in 2015

� DOE awards validate our technology

� Positive economic impacts including $17 MM feedstock purchases; 300 direct construction jobs and 65 permanent jobs; $5 MM annual payroll

� Facility will establish Abengoa as a fully integrated, one-stop provider of biotechnology services

8

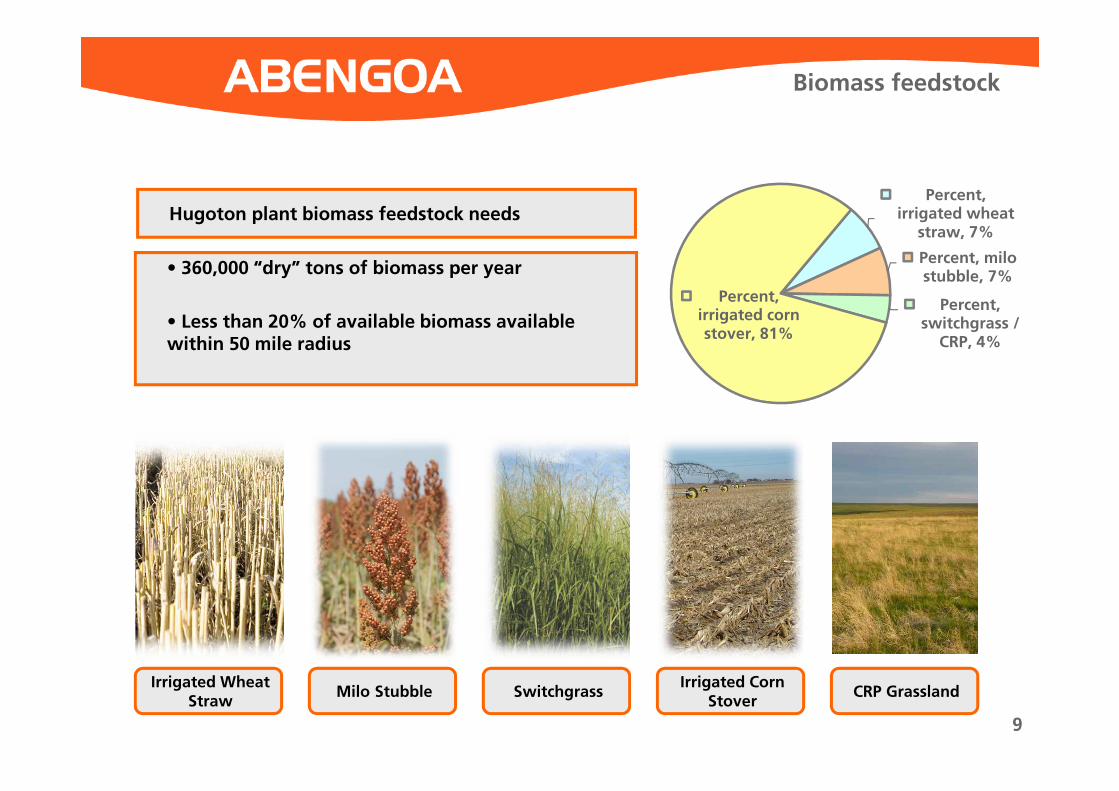

9

Irrigated Wheat Straw

Milo Stubble SwitchgrassIrrigated Corn

StoverCRP Grassland

• 360,000 “dry” tons of biomass per year

• Less than 20% of available biomass available within 50 mile radius

Hugoton plant biomass feedstock needs

Biomass feedstock

Percent, irrigated wheat

straw, 7%

Percent, milo stubble, 7%

Percent, switchgrass /

CRP, 4%

Percent, irrigated corn stover, 81%

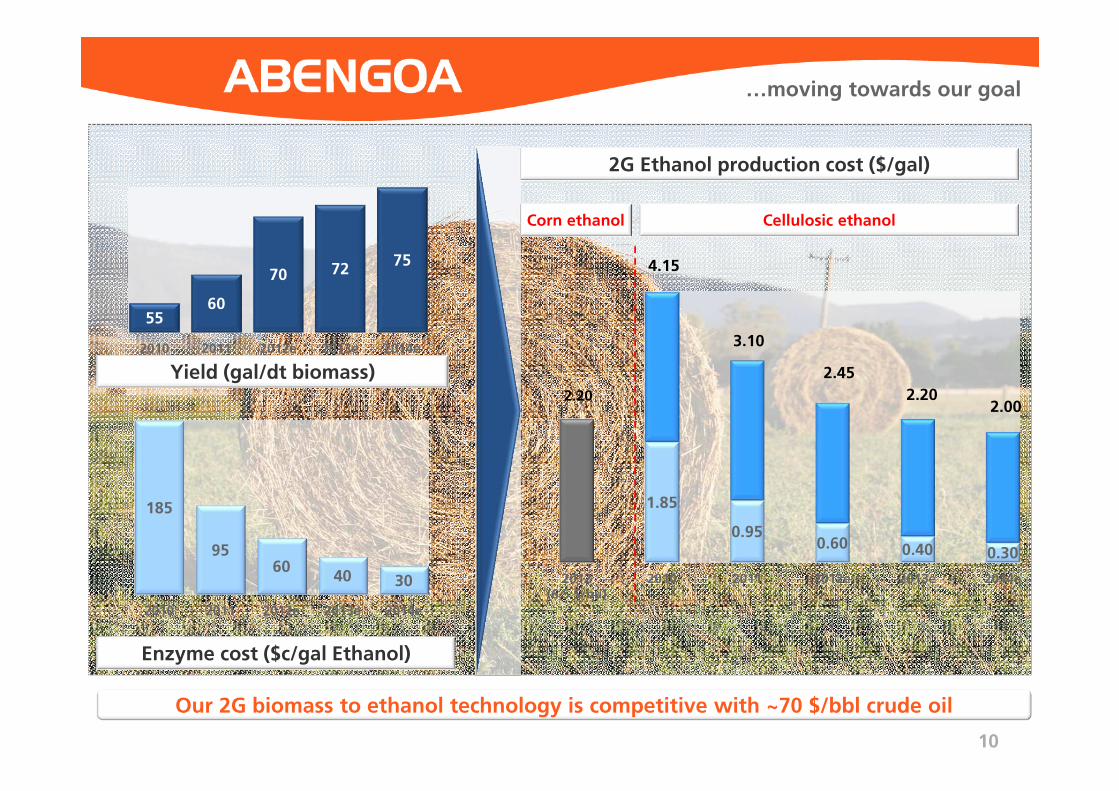

2G Ethanol production cost ($/gal)

…moving towards our goal

Yield (gal/dt biomass)

Enzyme cost ($c/gal Ethanol)

Corn ethanol Cellulosic ethanol

5560

70 7275

2010 2011 2012e 2013e 2014e

185

9560

40 30

2010 2011 2012e 2013e 2014e

1.85

0.950.60 0.40 0.30

2012(6.5 $/bu)

2010 2011 2012e 2013e 2014e

2.20

4.15

3.10

2.45

2.202.00

10

Our 2G biomass to ethanol technology is competitive with ~70 $/bbl crude oil

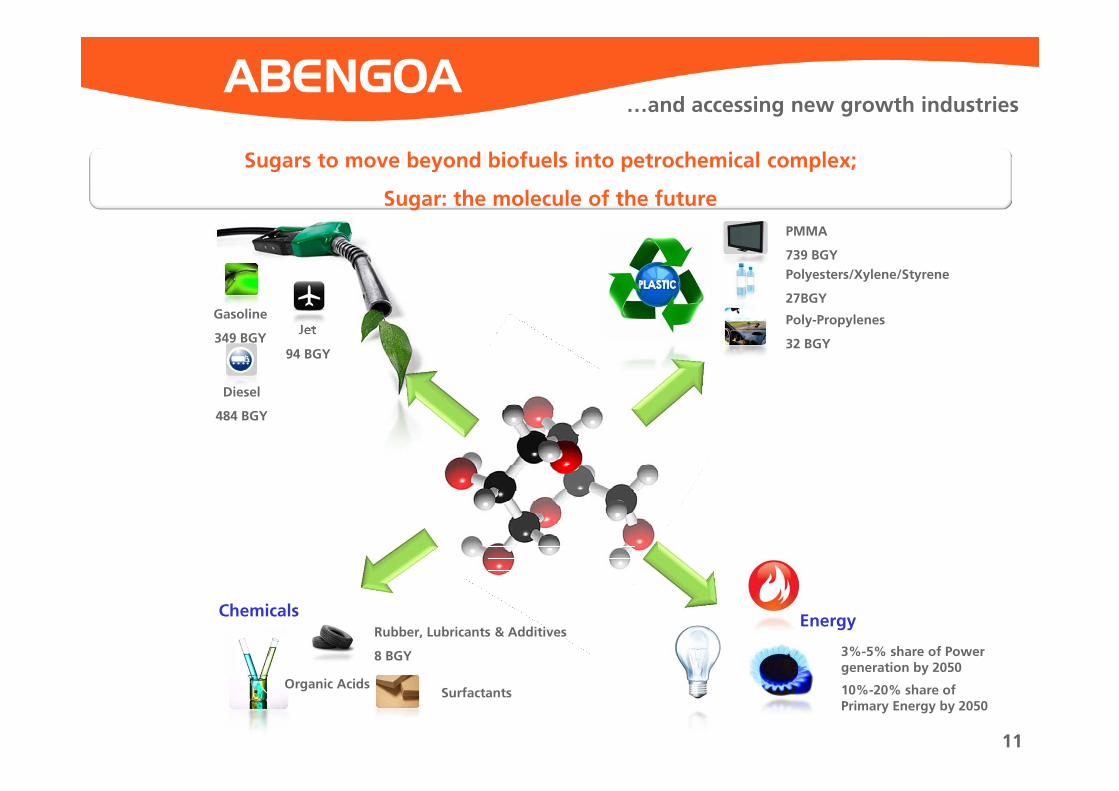

…and accessing new growth industries

Gasoline

349 BGY

Diesel

484 BGY

Jet

94 BGY

PMMA

739 BGY

Polyesters/Xylene/Styrene

27BGY

Poly-Propylenes

32 BGY

Rubber, Lubricants & Additives

8 BGY

Organic AcidsSurfactants

ChemicalsEnergy

3%-5% share of Power generation by 2050

10%-20% share of Primary Energy by 2050

Sugars to move beyond biofuels into petrochemical complex;

Sugar: the molecule of the future

11

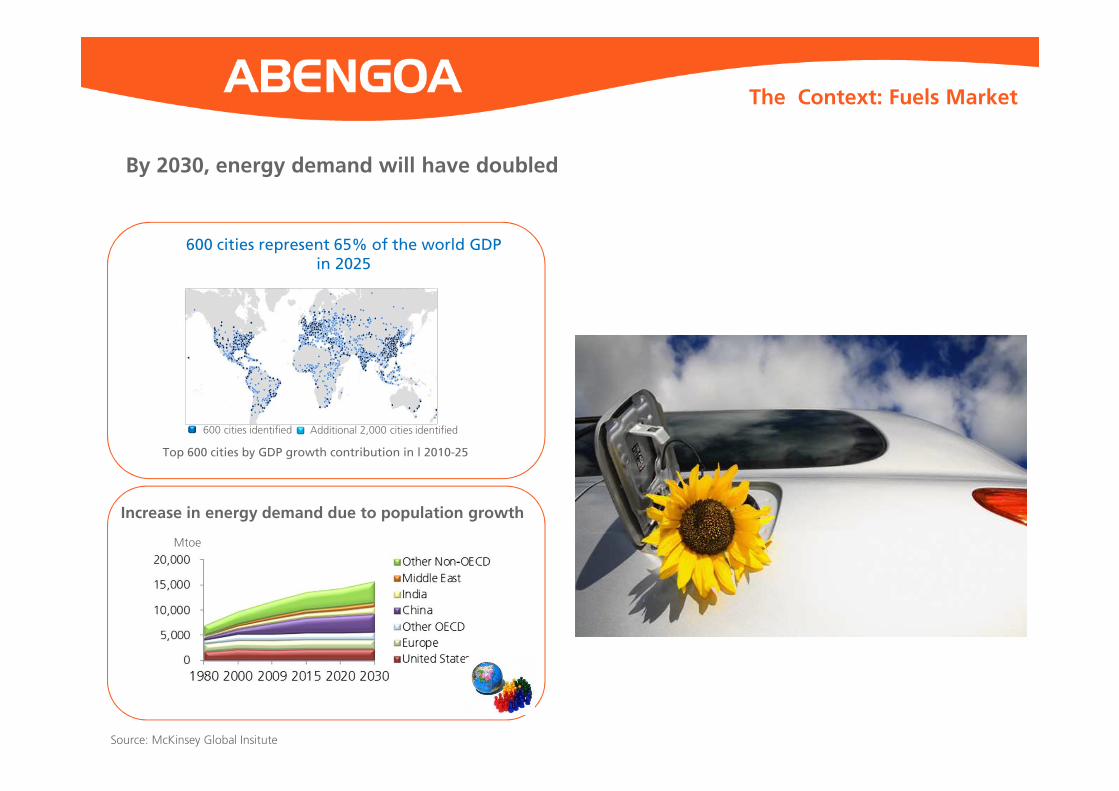

The Context: Fuels Market

Source: McKinsey Global Insitute

By 2030, energy demand will have doubled

Top 600 cities by GDP growth contribution in l 2010-25

600 cities represent 65% of the world GDP in 2025

600 cities identified Additional 2,000 cities identified

Increase in energy demand due to population growth

Mtoe

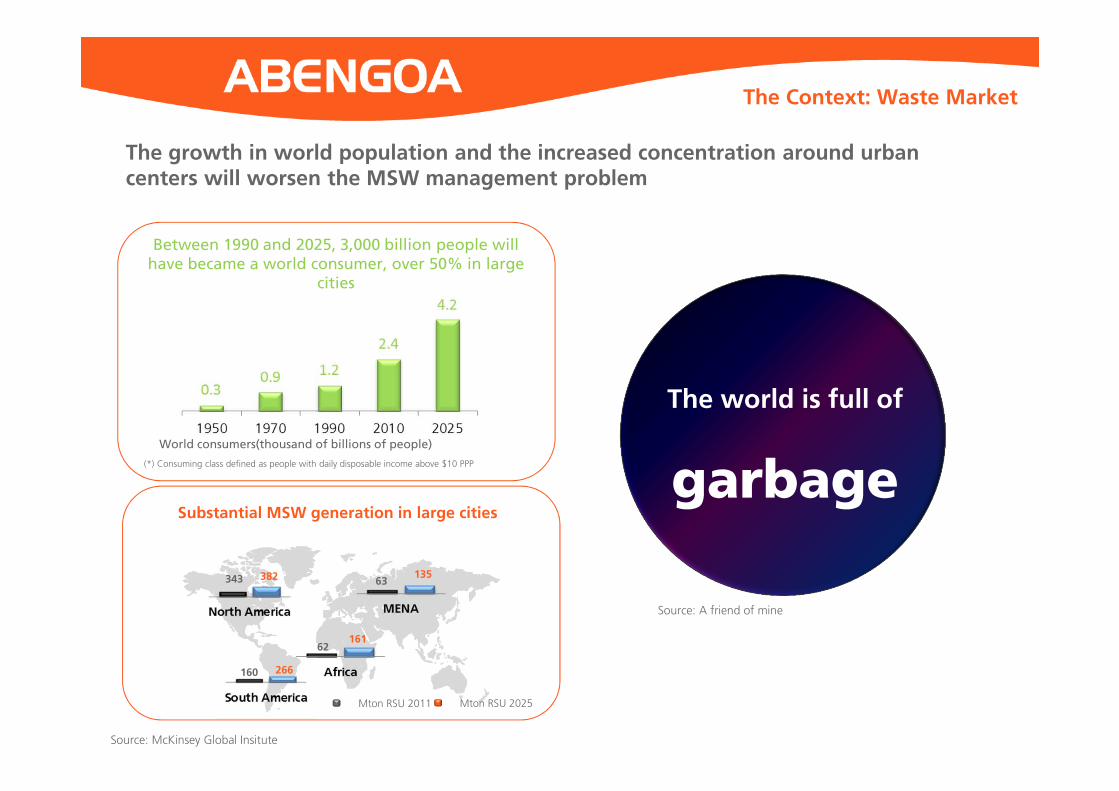

Between 1990 and 2025, 3,000 billion people will have became a world consumer, over 50% in large

cities

Source: McKinsey Global Insitute

World consumers(thousand of billions of people)

Substantial MSW generation in large cities

(*) Consuming class defined as people with daily disposable income above $10 PPP

16162

266160

382343 13563

Mton RSU 2011 Mton RSU 2025

The growth in world population and the increased concentration around urbancenters will worsen the MSW management problem

Source: A friend of mine

The Context: Waste Market

The world is full of

garbage

14

The Context: Waste Generation

The average person generates 2 kg of waste every day

75% of all that waste is recyclable. But 70% is landfilled.

The average person generates 2 kg of waste every day

75% of all that waste is recyclable. But 70% is landfilled.

15

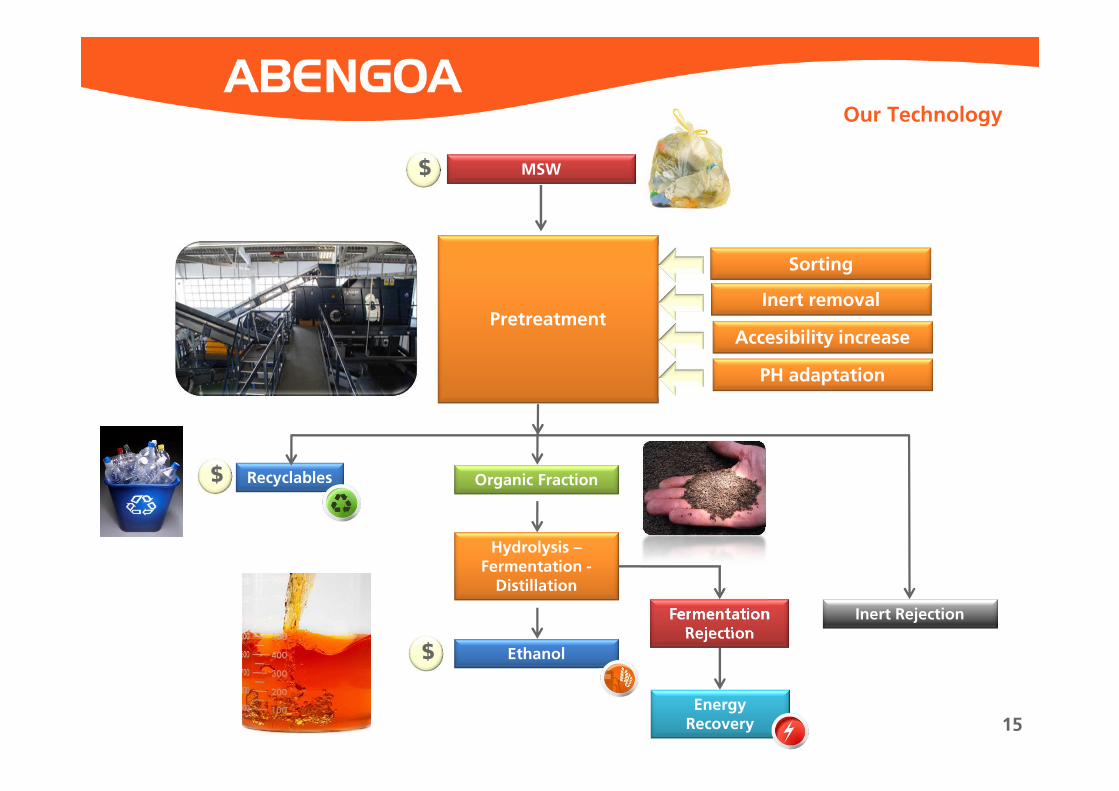

Pretreatment

MSW

Hydrolysis –Fermentation -Distillation

Organic Fraction

Ethanol

FermentationRejection

Inert Rejection

EnergyRecovery

Recyclables

Our Technology

Sorting

$$$

$$$

$$$

Inert removal

Accesibility increase

PH adaptation

16

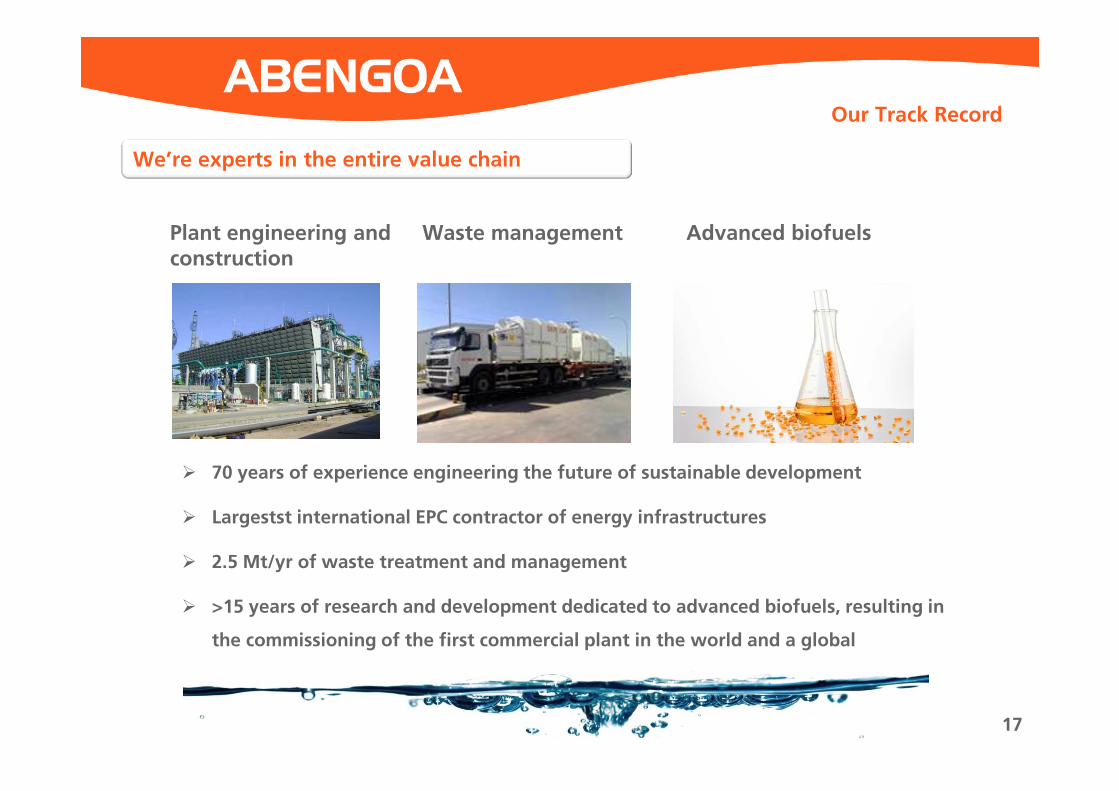

Our Track Record

Demonstration plant in Salamanca (Spain), which can process 25.000 t of MSW and produce up to a capacity of 1,5 ML of bioethanol.

17

Plant engineering and construction

Waste management

We’re experts in the entire value chain

Advanced biofuels

� 70 years of experience engineering the future of sustainable development

� Largestst international EPC contractor of energy infrastructures

� 2.5 Mt/yr of waste treatment and management

� >15 years of research and development dedicated to advanced biofuels, resulting in

the commissioning of the first commercial plant in the world and a global

production of 3100 ML/year in the three key markets (Europe, US & Brazil)

Our Track Record

18

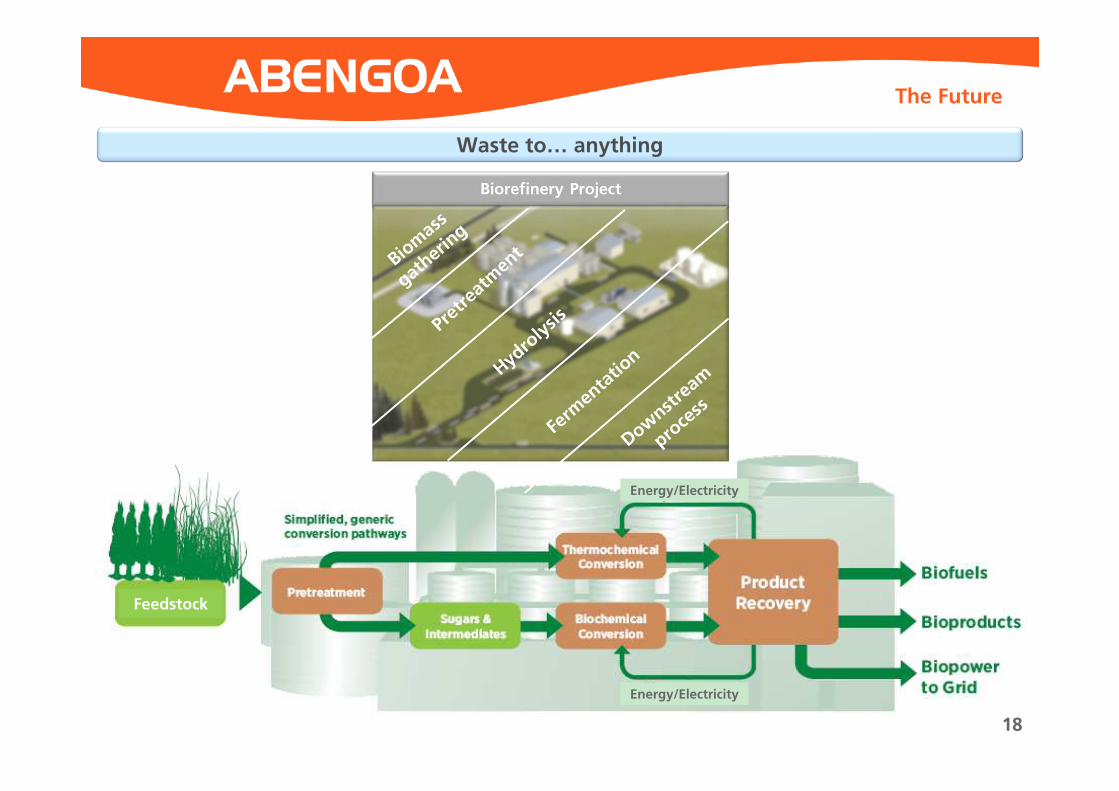

Waste to… anything

Energy/Electricity

Energy/Electricity

The Future

Feedstock

19

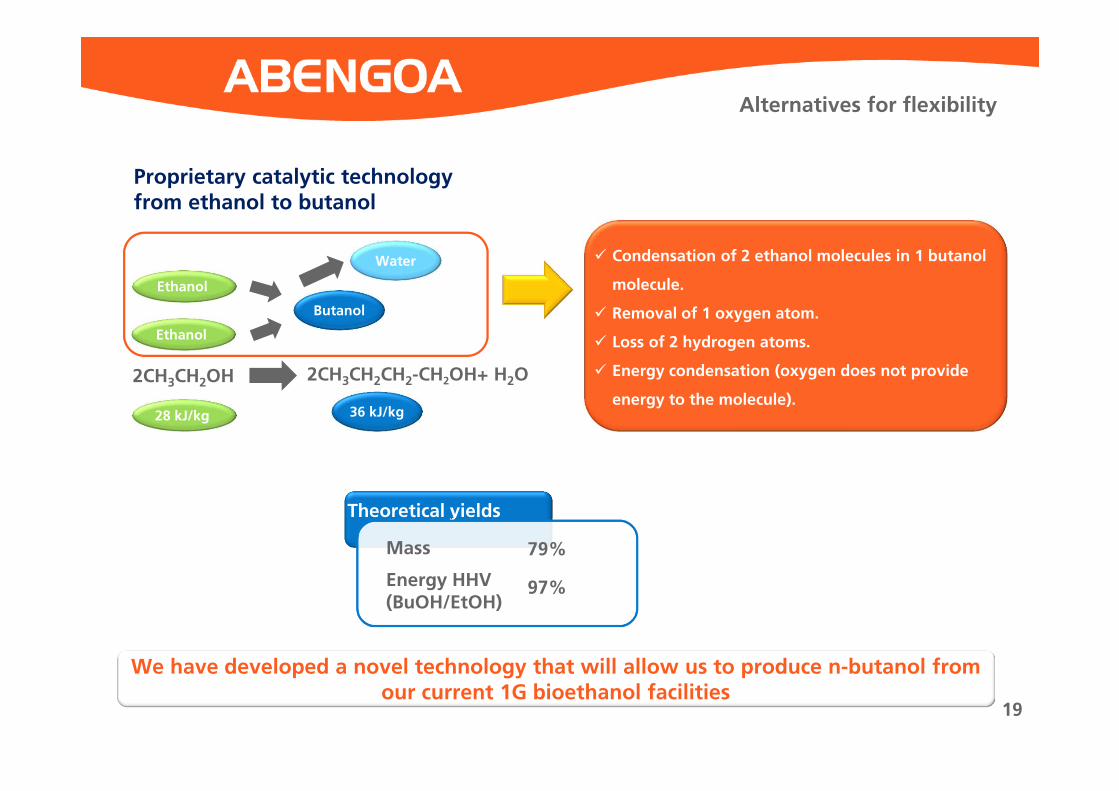

Ethanol

Ethanol

Butanol

Water � Condensation of 2 ethanol molecules in 1 butanol

molecule.

� Removal of 1 oxygen atom.

� Loss of 2 hydrogen atoms.

� Energy condensation (oxygen does not provide

energy to the molecule).

2CH3CH2OH 2CH3CH2CH2-CH2OH+ H2O

36 kJ/kg28 kJ/kg

Proprietary catalytic technology from ethanol to butanol

We have developed a novel technology that will allow us to produce n-butanol from our current 1G bioethanol facilities

Theoretical yields

Mass

Energy HHV (BuOH/EtOH)

79%

97%

Alternatives for flexibility

20

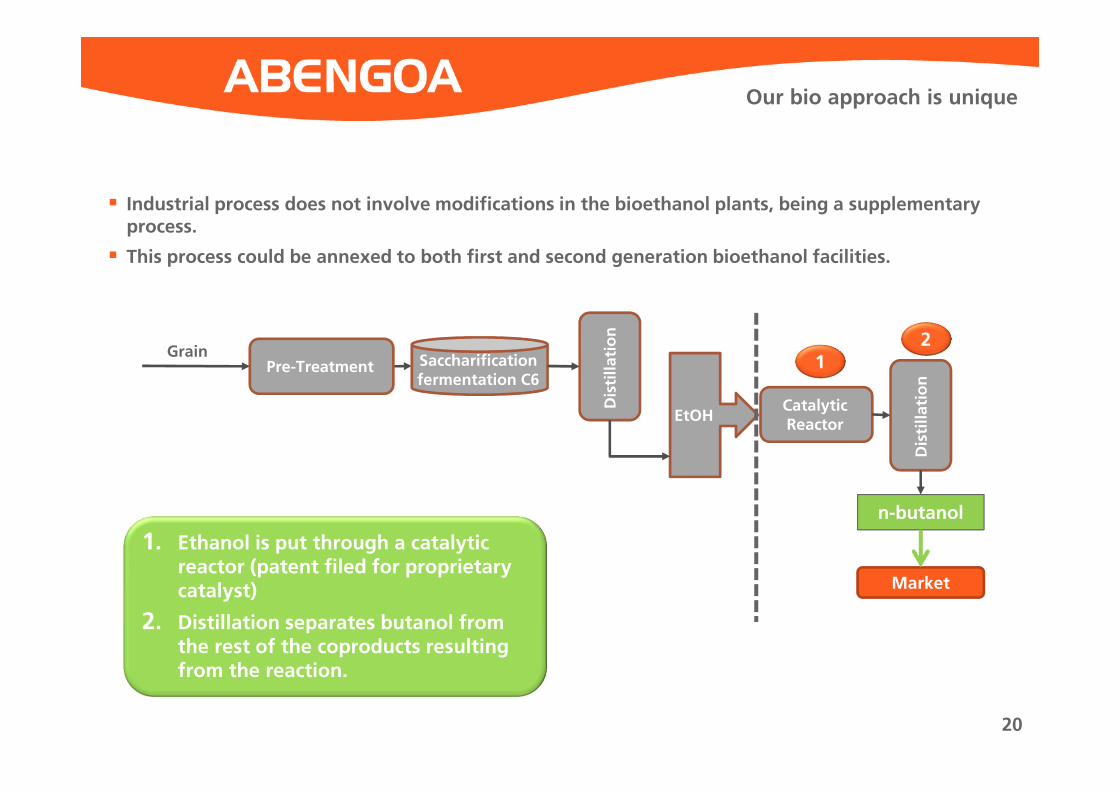

Distillation

Saccharificationfermentation C6

Pre-Treatment

EtOHCatalyticReactor

Distillation

Market

n-butanol

Grain

1. Ethanol is put through a catalytic reactor (patent filed for proprietary catalyst)

2. Distillation separates butanol from the rest of the coproducts resulting from the reaction.

21

� Industrial process does not involve modifications in the bioethanol plants, being a supplementary process.

� This process could be annexed to both first and second generation bioethanol facilities.

Our bio approach is unique

21

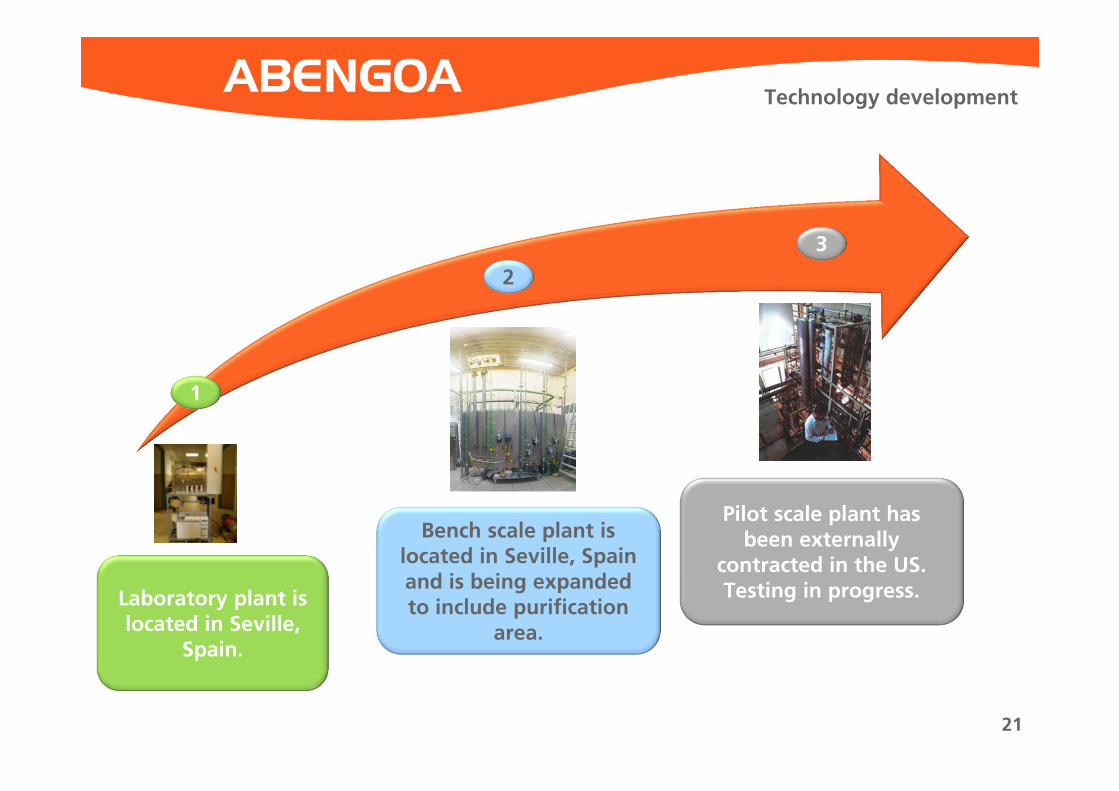

Laboratory plant is located in Seville,

Spain.

Bench scale plant is located in Seville, Spain and is being expanded to include purification

area.

Pilot scale plant has been externally

contracted in the US. Testing in progress.

Technology development

1

2

3

22

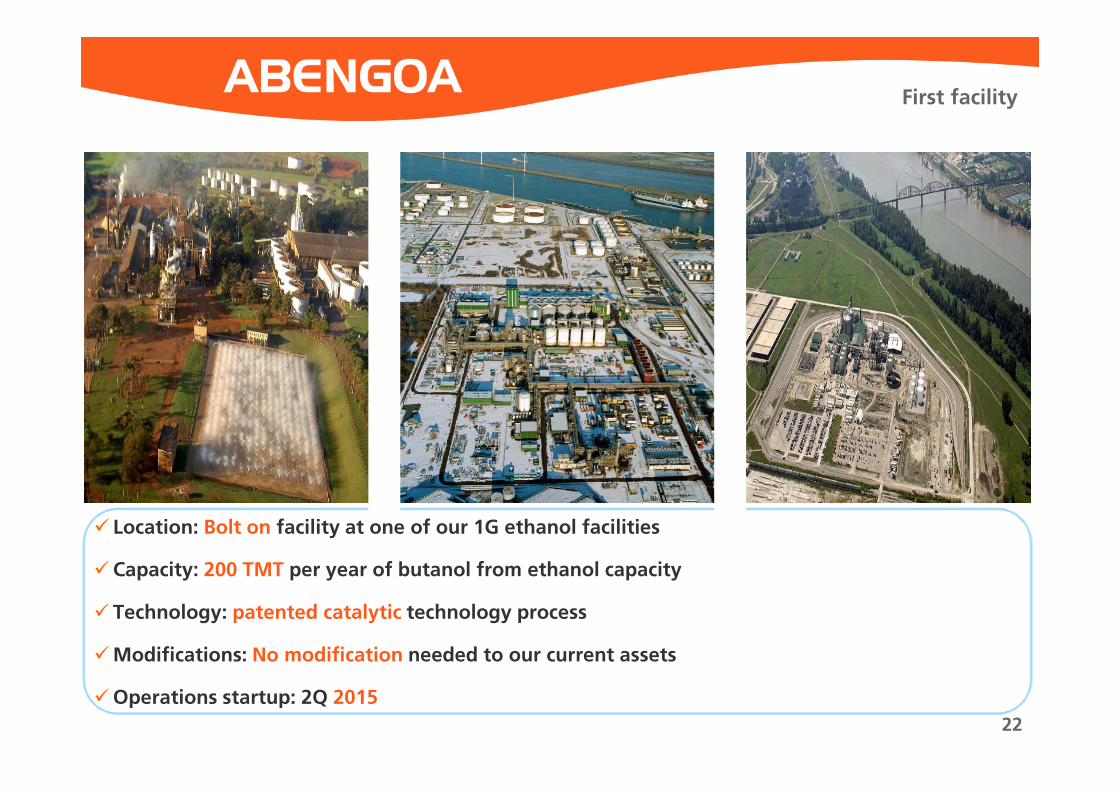

First facility

� Location: Bolt on facility at one of our 1G ethanol facilities

�Capacity: 200 TMT per year of butanol from ethanol capacity

� Technology: patented catalytic technology process

�Modifications: No modification needed to our current assets

�Operations startup: 2Q 2015

Questions