A Valuation of Novartis including a Real Option Analysis...

86

Master Thesis Marcel Reinders MSc in Finance & International Business A Valuation of Novartis including a Real Option Analysis Based on a Drug R&D Project 01.09.2010 Sign up: April 1 st 2010 Deadline: September 1 st 2010 Academic Advisor: Peter Løchte Jørgensen (PhD) Århus School of Business September 2010

Transcript of A Valuation of Novartis including a Real Option Analysis...

Master Thesis Marcel Reinders MSc in Finance & International Business

A Valuation of Novartis including a Real Option

Analysis Based on a Drug R&D Project

01.09.2010

Sign up: April 1st

2010

Deadline: September 1st

2010

Academic Advisor: Peter Løchte Jørgensen (PhD)

Århus School of Business

September 2010

2 of 130

Table of Contents

Inhalt Table of Contents.......................................................................................................................... 2

List of Figures ................................................................................................................................ 5

List of Tables ................................................................................................................................. 6

Preface .......................................................................................................................................... 7

1 Introduction ............................................................................................................................... 8

1.1 Problem Statement ............................................................................................................. 8

1.2 Methodology and Required Data ........................................................................................ 8

1.3 Introduction of Novartis ...................................................................................................... 9

1.4 Limitation ............................................................................................................................ 9

1.5 Structure ............................................................................................................................ 10

2 Historical Performance ............................................................................................................ 10

2.1 Relevant Accounting Issues ............................................................................................... 10

2.2 Invested Capital ................................................................................................................. 13

2.3 NOPLAT .............................................................................................................................. 13

2.4 Revenue Growth ............................................................................................................... 14

2.5 Return on Invested Capital ................................................................................................ 15

2.6 Free Cash Flow .................................................................................................................. 17

2.7 Credit Health ..................................................................................................................... 17

2.8 Stock Market Performance ............................................................................................... 18

3 Strategic Business Analysis ...................................................................................................... 20

3.1External Analysis ................................................................................................................ 20

3.1.1 PESTEL Analysis .......................................................................................................... 20

3.1.1.1 Political Factors ................................................................................................... 20

3.1.1.2 Economic Factors ................................................................................................ 22

3.1.1.3 Socio-Cultural Factors ......................................................................................... 23

3.1.1.4 Technological Factors .......................................................................................... 24

3.1.1.5 Environmental Factors ........................................................................................ 25

3.1.1.6 Legal Factors ........................................................................................................ 25

3.1.2 Market Definition and Size, Growth and Market Share ............................................. 26

3.1.2.1 Market Definition and Market Size ..................................................................... 26

3.1.2.2 Market Growth .................................................................................................... 27

3.1.2.3 Market Share ....................................................................................................... 28

3.1.3 Porter’s Five Forces Model ......................................................................................... 28

3.1.3.1 Bargaining Power of Suppliers ............................................................................ 29

3 of 130

3.1.3.2 Threat of New Entrants ....................................................................................... 29

3.1.3.3 Bargaining Power of Buyers ................................................................................ 29

3.1.3.4 Threat of Substitute Products ............................................................................. 29

3.1.3.5 Industry Competition .......................................................................................... 30

3.1.4 Key Industry Success Factors ...................................................................................... 30

3.1.4.1 Research and Development ................................................................................ 31

3.1.4.2 Competent Employees ........................................................................................ 31

3.1.4.3 Organizational Efficiency and Product Quality .................................................... 31

3.1.4.4 Financial Strength ................................................................................................ 31

3.1.4.5 Marketing and Sales ............................................................................................ 31

3.1.5 Competitor Analysis ................................................................................................... 31

3.1.5.1 Objectives ............................................................................................................ 32

3.1.5.2 Resources ............................................................................................................ 33

3.1.5.3 Past Performance ................................................................................................ 34

3.1.5.4 Product Portfolio ................................................................................................. 35

3.2 Internal Analysis ................................................................................................................ 37

3.2.1 Corporate Strategy ..................................................................................................... 37

3.2.2 Corporate Culture ...................................................................................................... 38

3.2.3 Value Chain Analysis ................................................................................................... 40

3.2.3.1 Primary Activities ................................................................................................ 40

3.2.3.2 Supporting Activities ........................................................................................... 41

3.2.4 Product Portfolio and Customers ............................................................................... 42

3.3 SWOT Analysis ................................................................................................................... 47

3.3.1 Strengths .................................................................................................................... 47

3.3.2 Weaknesses ................................................................................................................ 48

3.3.3 Opportunities ............................................................................................................. 48

3.3.4 Threats ........................................................................................................................ 49

4 Cost of Capital .......................................................................................................................... 49

4.1 The Cost of Equity ............................................................................................................. 50

4.1.1 The Risk Free Rate ...................................................................................................... 50

4.1.2 The Beta of Novartis ................................................................................................... 51

4.1.3 The Market Risk Premium .......................................................................................... 53

4.2 The after Tax Cost of Debt................................................................................................. 54

4.3 The Capital Structure of Novartis ...................................................................................... 55

4.4 WACC Sensitivity Analysis ................................................................................................. 57

5 Forecasting Performance ........................................................................................................ 58

5.1 Base Case Scenario ............................................................................................................ 59

5.2 Worst Case Scenario.......................................................................................................... 61

4 of 130

5.3 Best Case Scenario ............................................................................................................ 62

6 Valuation of Flexibility-A Real Option Approach.................................................................... 63

6.1 The Value of Flexibility ...................................................................................................... 63

6.2 Development Process ........................................................................................................ 64

6.3 Market and Technical Risk ................................................................................................ 66

5.4 Static NPV .......................................................................................................................... 66

6.5 The Real Options Valuation Approach .............................................................................. 68

6.5.1 Framing the Problem .................................................................................................. 68

6.5.2 Binominal Tree of Underlying Values ......................................................................... 70

6.5.3 The Value of the Option ............................................................................................. 71

7 Calculating and Interpreting Results ....................................................................................... 73

7.1 Value of Operations .......................................................................................................... 74

7.1.1 Discounted Cash Flow ................................................................................................ 74

7.1.2 Continuing Value ........................................................................................................ 74

7.1.3 Value of Operations ................................................................................................... 74

7.2 Equity Value ...................................................................................................................... 75

7.2.1 Value of Non-Operating assets .................................................................................. 75

7.2.2 Value of Non-Equity Claims ........................................................................................ 75

7.2.2.1 Debt ..................................................................................................................... 75

7.2.2.2 Debt Equivalents ................................................................................................. 75

7.2.2.3 Hybrid Claims ...................................................................................................... 76

7.2.2.4 Minority Interest ................................................................................................. 76

7.2.3 Value per Share .......................................................................................................... 76

7.3 Verifying Valuation Results ............................................................................................... 77

7.3.1 Sensitivity Analysis ..................................................................................................... 77

7.3.2 Multiples Analysis ....................................................................................................... 78

7.3.3 Plausibility Analysis .................................................................................................... 80

8 Conclusion ................................................................................................................................ 82

List of Literature ......................................................................................................................... 84

List of Appendices ....................................................................................................................... 87

5 of 130

List of Figures

Figure 1: Invested Capital………………………………………………………… 13

Figure 2: NOPLAT……………………………………………………………….. 13

Figure 3: Total Operating Income………………………………………………... 14

Figure 4 Novartis CAGR…………………………………………………………. 14

Figure 5: Sales by Division………………………………………………………. 15

Figure 6: Return on Invested Capital……………………………………………... 16

Figure 7: Free Cash Flow………………………............................................... 17

Figure 8: Total Shareholder Return………………………………………………. 19

Figure 9: Group Net Sales by Region…………………………………………….. 22

Figure 10: Global Market Sales by Region……………………………………... 26

Figure 11: Total Market Sales……………………………………………………. 27

Figure 12: Market Share………………………………………………………….. 28

Figure 13: Porter’s Five Forces Model…………………………………………… 28

Figure 14: R&D of Net Sales…………………………………………….. ……... 33

Figure 15: Total Assets…………………………………………………............... 34

Figure 16: Pfizer Source of Revenue…………………………………………….. 35

Figure 17: GSK Source of Revenue……………………………………………… 35

Figure 18: Novartis Portfolio Matrix…………………………………………….. 43

Figure 19: Novartis Product Life Cycle………………………………………….. 46

Figure 20: Novartis Scatter Plot………………………………………………….. 51

Figure 21: Novartis Regression Output…………………………………………... 51

Figure 22: Novartis Rolling Beta………………………………………………… 53

6 of 130

List of Tables

Table 1: Sales by Region………………………………………………................. 27

Table 2: R&D Expenditure……………………………………………………….. 33

Table 3: Novartis Pipeline………………………………………………………... 41

Table 4: Novartis Bond Yield……………………………………………………. 55

Table 5: Novartis Capital Structure………………………………………………. 56

Table 6: WACC Sensitivity………………………………………………………. 57

Table 7: Key Figures Base Case Scenario………………………………………... 60

Table 8: Key Figures Worst Case Scenario………………………………………. 61

Table 9: Key Figures Best Case Scenario………………………………………… 62

Table 10: BAF 312 Budget……………………………………………………….. 67

Table 11: BAF 312 Development Cost…………………………………………... 67

Table 12: Value of Operations: DCF Approach………………………………….. 74

Table 13: Value of Equity………………………………………………………… 76

Table 14: Sensitivity Analysis Results…………………………………………… 77

Table 15: Multiples Analysis……………………………………………………... 79

7 of 130

Preface

This thesis has been written as part of the curriculum of the 2-year Master of Science

program in Finance and International Business at the Århus School of Business. The

goal of this paper has been to come up with an estimate of the fair value of the Swiss

pharmaceuticals producer Novartis including a real options approach to value the true

NPV of a new drug development project.

Because the valuation is done from an external perspective no internal information was

available other than what is disclosed by Novartis in annual reports. Additional

information needed for this paper was retrieved from a variety of sources such as

published articles, books, scientific research papers and web pages.

I would like to express my personal gratitude to my supervisor Peter Løchte Jørgensen

for his guidance and assistance during the time the thesis was written. He was always

available and his contribution is highly appreciated.

8 of 130

1 Introduction

Chapter one serves as an introduction to the master thesis providing an outline of the

problem statement, describing the methodology employed as well as the data required.

Furthermore it briefly introduces the company of focus, Novartis, points out the

limitations of thesis and lastly provides a outline of the structure of the thesis.

1.1 Problem Statement

The goal of the paper is the valuation of the pharmaceutical company Novartis and to

estimate its fair market value. To achieve this goal, the historical performance within

the context of its industry and market conditions is analyzed to provide insights into the

company’s future performance and thus its intrinsic value.

Furthermore, a real-option analysis will be conducted based on a research and

development project for a new drug. This process will reveal the value of flexibility that

comes along with research and development for a new drug which cannot be determined

with a common and static NPV analysis. The goal is to show that often a project is

dismissed as value destroying because flexibility is not considered in the calculation

thus foregoing possible value for the company.

1.2 Methodology and Required Data

In order to get a picture of Novartis’ historical performance, a financial analysis will be

performed based on the company’s balance sheet and income statement from the

previous years. A strategic business analysis will also be conducted, including a

PESTEL and competitor analysis, Porter’s 5 forces and finally a SWOT analysis based

on the information generated from the strategic business analysis.

To estimate the enterprise value of the company, the discounted cash flow method will

be used and for calculating the cost of equity the CAPM model is used, whereby the

equity risk premium will be estimated based on historical data from the S&P 500

market index. If need be, the Black and Scholes formula for pricing an option will be

employed to calculate the value of option packages for executive management payment

schemes. In order to value flexibility with real option analysis, a binomial lattice with

risk-neutral-probabilities will be applied.

Data input required for writing the paper are the annual reports from Novartis to

determine past and future performance. Also required is data on the company’s

environment that reveals information about the industry, its participants as well as

9 of 130

possible threats and opportunities for the company. To determine the company’s cost of

equity data from the financial markets is required, such as stock returns, index returns as

well as government bond rates. As far as the data requirements for the real option

analysis is concerned, various assumptions have to be made with regard to the present

value of the drug’s estimated future cash flow, required investments, volatility and steps

of the research and development process. These assumptions are necessary due to

undisclosed information by the company.

1.3 Introduction of Novartis

Novartis is a biotechnology and pharmaceutical company which is headquartered in

Basel, Switzerland (Novartis, 2010).1 The name Novartis has Latin origin (novae artes),

meaning new arts. Novartis was founded in 1996 after the merger of the two Basel

located pharmaceutical and chemical companies Ciba-Geiger AG and Sandoz. In 1996

the merger of these two companies was the biggest merger in the world up to that date.

Today Novartis is the third largest pharmaceutical company in the world with about

100.000 employees worldwide and annual revenues of more than 46 billion USD in

2009. It is also one of the fastest growing companies in the industry which also puts big

effort into research and development of new drugs. In 2008 Novartis was ranked on

second place in Fortunes magazine’s “World’s most admired companies” survey in the

pharmaceutical industry. Novartis has four main business areas which are:

- Pharmaceuticals: innovative drugs which are protected by patents

- Vaccines and diagnostics: vaccines and diagnostics to protect humans against

life-threatening diseases

- Sandoz: generic pharmaceuticals that substitute branded drugs after patent

expiration

- Consumers health: over-the-counter drugs, animal health and CIBA Vision

1.4 Limitation

It is important to note that the valuation was performed from an outside perspective

from which no internal information was available for the valuation process.

Furthermore, the competitor analysis is only based on the two most important

competitors of Novartis due to time and page limit. The pharmaceutical industry is

1 http://www.novartis.com/about-novartis/index.shtml

10 of 130

highly fragmented with hundreds of competitors around the world analyzing all of them

is impossible. Regarding the real option analysis it should be noted that the budget and

key parameters are based on assumption due to lack of inside information. To get an

estimate of volatility the plan for doing a Monte Carlo analysis was abandoned. The

reasoning is that this would not generate additional value since no information was

available in what range revenues of the potential new drug can change.

Nevertheless, the assumptions made during the valuation process where made to the

best of knowledge and are deemed reasonable and largely approximate reality in a

satisfying manner.

1.5 Structure

The thesis structure consists of an introduction in chapter 1 after which the historical

performance of Novartis is discussed in chapter 2. In chapter 3 the strategic business

analysis of Novartis is done after which the weighted average cost of capital of Novartis

is estimated in chapter 4. In chapter 5 the future performance of Novartis is forecasted

and in chapter 6 a real options analysis for a potential new drug of Novartis is

performed. In chapter 7 the final results are calculated and interpreted. In the chapter 8

the thesis is concluded.

2 Historical Performance

In chapter two the historical performance of Novartis is analyzed based on annual

reports of the previous ten years. In order to accurately assess a company’s potential to

generate cash flows in the future and forecast its performance, it is necessary to analyze

the company’s past development and the drivers behind this development. The main

source for an external analysis is thus the financial statements provided by Novartis.

First relevant accounting issues will be addressed which is followed by an analysis of

invested capital, net operating profit less adjusted taxes (NOPLAT), revenue growth,

return on invested capital (ROIC), free cash flow, credit health and stock market

performance.

2.1 Relevant Accounting Issues

In the analysis of Novartis several accounting issues require special attention. These are:

11 of 130

• Accounting standards: Novartis follows the International Financial Reporting

Standards (IFRS) since 2001 which are published by the International

Accounting Standards Board (IASB). Before 2001 Novartis had been following

International Accounting Standards (IAS) published by the International

Accounting Standards Committee (IASC) which was succeeded by the IASB

which largely adopted the IAS standards as a basis for further development.

• Acquisitions and goodwill: Novartis has acquired a number of companies over

the years in order to acquire new technologies, product rights and diversify its

product portfolio. Acquisitions are consolidated into the financial statements

while the excess purchase price over the fair value of net assets acquired is

recorded as goodwill in the balance sheet (Novartis, 2009, p. 187). Since 2005

Goodwill is not subject to amortization but considered to have indefinite life

which is tested annually for impairment.

• Operating leases: Novartis is in engaged in a number of operating lease contracts

to finance tangible assets which do not appear on the balance sheet but are part

of operating activities. The value of these leases was calculated by using the

following formula:

����� ����� ����� ������

�� � 1����� ����

The rental expenses were taken from the annual reports as disclosed by Novartis

and the average asset life was estimated to be 10 years. The calculation of the

company’s cost of debt is explained in chapter 4.

• Operating cash: Novartis holds enormous amounts of cash and cash equivalents.

The amount of operating cash was estimated at 2% of total annual revenues

which seems to be reasonable according to Koller, Goedhart and Wessels (2005,

p.171). The remaining cash is considered to be excess cash.

• Marginal tax rate: With the information provided by Novartis on tax rates a

precise calculation of the marginal tax rate was not possible. Marginal tax rate is

defined as the tax rate on an additional dollar of income and therefore the

average tax rate reported by Novartis was used to approximate the marginal tax

rate. Reason for this is the fact that Novartis operates in many different countries

worldwide with different tax rates making an average of these tax rates a

12 of 130

reasonable proxy for a tax rate on the next dollar of income. The marginal tax

rate used for calculations is 15.22%.

• Research and development costs: According to IFRS Novartis expenses all

research and development (R&D) costs through the income statement for which

uncertainties exist whether or not future sales can be generated. R&D costs will

only be capitalized as intangible assets by Novartis when approval has been

granted by authorities in a major market (Novartis, 2010, p.191). However, for

technology companies as well as pharmaceutical companies such as Novartis,

research and development is very important and failure to recognize these costs

as intangible assets can lead to an understatement of invested capital. This would

result in an overstatement of return on invested capital (Koller, Goedhart and

Wessels, 2005, p.200). Therefore, to get a more accurate estimate of invested

capital, research and development costs will be capitalized.

• Pension plan: Novartis offers both defined contribution as well as defined

benefit pension schemes. As far as defined benefit plans are concerned, which

are important for valuation purposed, the fair value of plan assets in 2008 and

2008 was less than defined benefit obligations required thus resulting in net

liabilities of $ 428 million (Novartis, 2010, p.232). These liabilities have to be

subtracted from enterprise value when calculating equity value.

• Share split: In 2001 a 40:1 share split was approved by shareholders at the

annual general meeting, becoming effective on May 7th, 2001. Thus,

shareholders exchange one share with a nominal value of 20 Swiss Francs

(CHF) for 40 shares with a nominal value of 0,50 CHF per share. All share

related data has been adjusted to the changes of the share split (Novartis, 2002,

p.72).

• Change of reporting currency: In 2003 the reporting currency of consolidated

financial statements of Novartis was changed from CHF to U.S. Dollars from

January 1st, 2003. Reasons for the change of reporting currency are the increased

importance of sales in the United States as well easier comparison of financial

statements between peer companies of the pharmaceutical industry (Novartis,

2004, p.111).

• Dividends: Since the foundation of Novartis, the company has paid out annual

dividends to shareholders on a continuous basis. In 2009 board of directors

13 of 130

Source: own design

Source: own design

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

14.117

29.724

54.853

68.983

Figure 1: Invested Capital ($ Mio.)

0,00

2.000,00

4.000,00

6.000,00

8.000,00

10.000,00

12.000,00

14.000,00

2001 2002 2003 2004 2005 2006 2007 2008 2009

5.805,98

8.653,71

11.316,17 12.068,75

Figure 2: NOPLAT (in Mio.)

proposed a 5% increase in dividend payment at the Annual General Meeting.

This would be the 13th consecutive dividend increase since 1996.

2.2 Invested Capital

Invested capital represents operating assets less operating liabilities (Koller, Goedhart

and Wessels, 2005, p.165). In the case of Novartis research and developments costs

were capitalized since they represent significant intangible assets for a pharmaceutical

company such as Novartis. Operating

invested capital including goodwill and

intangible assets increased continuously

from 2001 until 2009 by 454%. As

depicted in figure 1 invested capital

increased significantly due to increased

research and development activities and

acquisitions in the period 2004 to 2009.

Notable acquisitions in this period were Hexal, Eon Labs and Chiron. In 2009 invested

capital totaled about 68.9 billion USD of which 20,4% can be attributed to net property,

plant and equipment and 73,8% to goodwill and intangible assets. For more detailed

information refer to appendix 1.

2.3 NOPLAT

NOPLAT represents total income generated from company operations that are available

to investors of Novartis. As can be seen from the figure 2 Novartis was able to increase

NOPLAT continuously over the years from 2001 until 2009. NOPLAT increased from

2001 to 2009 by 208%. Reason for the

positive development of NOPLAT over the

years is the steady growth in net income due

to increasing revenues. The increasing

development of NOPLAT was interrupted in

2005 and then increased again sharply in 2006.

Reason for this development was a change in

deferred tax assets and deferred tax liabilities. In 2008 and 2009 NOPLAT even kept

growing despite negative influence of currency effects. For more detailed information

on NOPLAT, please refer to appendix 1.

14 of 130

Source: own design

0

10.000

20.000

30.000

40.000

50.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

22.199 24.864

36.749

45.103

Figure 3:Total Operating Revenue (in Mio.)

11,1%

12,0%

9,4%

8,6%

6,8%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

2005 2006 2007 2008 2009

Figure 4: CAGR - Novartis

Source: own design

2.4 Revenue Growth

The group sales of Novartis have been

constantly increasing since 2001 as visible

in figure 3. Reason for the constant

increase in sales is the increasing need of

aging people for reliable and effective

medicines as well as strong product

growth and the launch of additional new

medicines. Also important is the fact that Novartis has put considerable effort in the past

to expand its business worldwide and has established a diversified portfolio of health

care products. In 2009, group sales increased by 11% in local currencies and by 7% in

USD to roughly 44.3 billion USD, making Novartis one of the strongest growing

companies in the industry (Novartis, 2010, p.7).

When looking at the five year compound annual growth rate (CAGR) for the last five

years the picture is a different one. From

2005 until 2009 the CAGR shrunk from

11,1% to 6,8% as depicted in figure 4.

Possible explanations for this

development are increasing

governmental pressure to lower prices,

currency fluctuations, as well as

increased competition from other generic

drugs and illegal copies and other

pharmaceutical companies. Global economic downturn in the last 3 years has also

effected the revenue growth of Novartis to some extent. Revenue growth has been

mostly generated internally, however partially growth has been generated by acquisition

of companies such as Hexal, Eon Labs and Chiron.

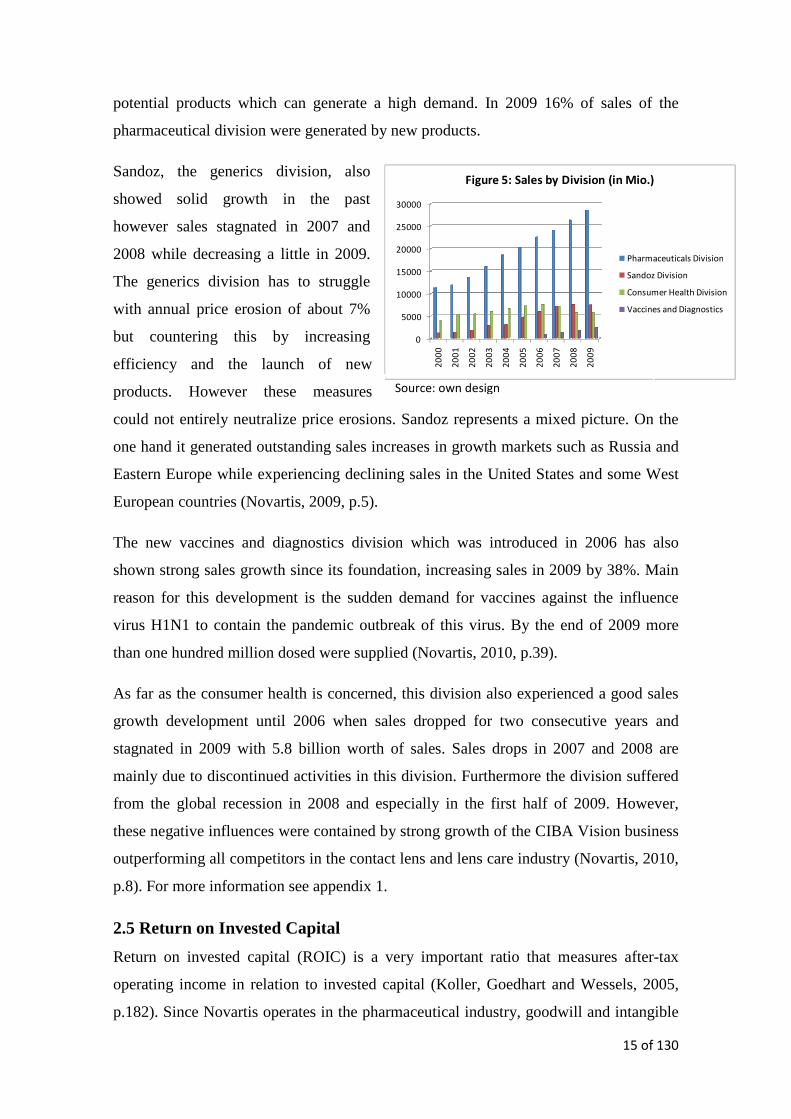

When taking a closer look at sales on the divisional level as depicted in figure 5 is

becomes evident that the pharmaceuticals division (drugs that are protected by patents)

generated the lion share of sales in the past. The products sold by this division are high-

tech products which are very expensive and usually have high margins. Another reason

for the positive sales development of this division is that it regularly launches new high

15 of 130

0

5000

10000

15000

20000

25000

30000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Figure 5: Sales by Division (in Mio.)

Pharmaceuticals Division

Sandoz Division

Consumer Health Division

Vaccines and Diagnostics

Source: own design

potential products which can generate a high demand. In 2009 16% of sales of the

pharmaceutical division were generated by new products.

Sandoz, the generics division, also

showed solid growth in the past

however sales stagnated in 2007 and

2008 while decreasing a little in 2009.

The generics division has to struggle

with annual price erosion of about 7%

but countering this by increasing

efficiency and the launch of new

products. However these measures

could not entirely neutralize price erosions. Sandoz represents a mixed picture. On the

one hand it generated outstanding sales increases in growth markets such as Russia and

Eastern Europe while experiencing declining sales in the United States and some West

European countries (Novartis, 2009, p.5).

The new vaccines and diagnostics division which was introduced in 2006 has also

shown strong sales growth since its foundation, increasing sales in 2009 by 38%. Main

reason for this development is the sudden demand for vaccines against the influence

virus H1N1 to contain the pandemic outbreak of this virus. By the end of 2009 more

than one hundred million dosed were supplied (Novartis, 2010, p.39).

As far as the consumer health is concerned, this division also experienced a good sales

growth development until 2006 when sales dropped for two consecutive years and

stagnated in 2009 with 5.8 billion worth of sales. Sales drops in 2007 and 2008 are

mainly due to discontinued activities in this division. Furthermore the division suffered

from the global recession in 2008 and especially in the first half of 2009. However,

these negative influences were contained by strong growth of the CIBA Vision business

outperforming all competitors in the contact lens and lens care industry (Novartis, 2010,

p.8). For more information see appendix 1.

2.5 Return on Invested Capital

Return on invested capital (ROIC) is a very important ratio that measures after-tax

operating income in relation to invested capital (Koller, Goedhart and Wessels, 2005,

p.182). Since Novartis operates in the pharmaceutical industry, goodwill and intangible

16 of 130

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

80,0%

90,0%

100,0%

Figure 6: Return on Invested Capital

ROIC (w/o intangible

assets)

ROIC (w/ intangible

assets)

Source: own design

assets are very important and R&D expenditure should be capitalized. Therefore ROIC

is calculated including intangible assets (Koller, Goedhart and Wessels, 2005, p. 200).

As can be seen from figure 6 the

difference between ROIC with and

without intangible assets its very

significant showing that a significant

part of Novartis’ invested capital results

from intangible assets. ROIC has been

decreasing over the years due to rapid

investment in research and development

and goodwill even though sales could be increased in every year since 2001.

To find out how the operational drivers affect the return on invested capital for the last

five years a ROIC tree has to be set up (see appendix 2). The ROIC tree reveals that

Novartis’ ROIC is primarily driven by its high operating margin which in turn is driven

by its high gross margin. Here Novartis can clearly profit from its pharmaceutical

division which markets new drugs which are protected by patents that enable the

company to generate high margins. This is a likely source of competitive advantage for

Novartis, which is able to get approval from authorities on a regular basis to market new

drugs which are protected by patents.

With regard to average capital turns, it is obvious that efficient use of capital is not a

source that drives return on invested capital. Due to high research and development

expenditures, which increased over the years and that are considered part of invested

capital, average capital turns actually have a negative effect on ROIC. However,

without a significant research and development effort Novartis would not be able to

develop new highly effective drugs that could generate high margins. Another important

factor in determining ROIC is the cash tax rate. Novartis benefits from low cash tax

rates that positively influence ROIC. The cash tax rate varied significantly over the last

five years mainly due to big annual differences in deferred tax liabilities. In 2004 the

cash tax rate was even negative due to a massive increase in deferred tax liabilities.

Finally, at the end of the ROIC tree, the final ROIC is presented for each given year.

ROIC decreased from 2005 until 2008 mainly due to increases in intangible fixed assets

that resulted in low average capital turns in spite of a constantly high operating margin.

17 of 130

Source: own design

-4000,0

-2000,0

0,0

2000,0

4000,0

6000,0

8000,0

2001 2002 2003 2004 2005 2006 2007 2008 2009

4743,2

1283,9

3549,93442,7

-2610,8

-3583,3

5100,4

6120,2

7427,8

Figure 7: Free Cash Flow (in mio.)

2.6 Free Cash Flow

Free Cash Flow is the after-tax cash flow

available to debt and equity holders. It is

defined as NOPLAT plus noncash operating

expenses net of investments in invested

capital (Koller, Goedhart and Wessels, p.164).

As can be seen from figure 7 free cash flow

generated by Novartis underwent a kind of

mixed development in the past nine years. After 2001, free cash flow dropped

significantly mainly due to increased investments in working capital and capital

expenditures. Furthermore in 2002 investments in operating leases were introduced

which further reduced free cash flow.

In 2003 and 2004 free cash flow increased to almost 5.6 billion USD mainly because of

increased NOPLAT and less working capital even though investments in intangible

assets and goodwill increased. In 2005 and 2006 Novartis generated negative free cash

flow of $2.6 and $3.6 billion. Main cause for this negative development was intangible

assets and acquisitions related costs.

In the following years of 2007 until 2009 Novartis was able to generate positive cash

flows again which increased from $5.4 billion in 2007 to $7.4 billion in 2009. The

increased positive cash flows were mainly caused by higher sales and NOPLAT as well

as lower gross investment and lower investment in intangibles. For more detailed

information refer to appendix 1.

2.7 Credit Health

In the past Novartis has maintained a conservative financing strategy using little

external financing and maintaining a solid creditworthiness and a strong ability to meet

its debt obligations. Proof for this is the credit rating by various rating agencies, such as

Standard & Poor’s or Fitch. Until 2008 Novartis was rated with AAA certifying

Novartis excellent creditworthiness making Novartis one of only a few non-financial

companies worldwide to achieve the highest rating (Novartis, 2008, p.171). Reason for

this is the company’s capability to generate strong earnings together with employing

low levels of external financing.

18 of 130

In 2008 and 2009 however, rating agencies downgraded Novartis lower their ratings by

three steps from AAA to AA-. The rating agencies justified their action with Novartis’s

purchase of 77% of Alcon share for 39 billion USD which according to Novartis would

be mostly financed by issuing debt. This decision also affected the interest coverage

ratio. From 2007 to 2009 the interest coverage decreased from 45 to 24.5 due to a

significant increase in interest expenses from 237 million USD in 2007 to 551 million

USD in 2009.

According to Moody’s Analyst Novartis will require additional external financing to

ensure adequate liquidity and moreover the Novartis blockbuster Diovan, which is the

company’s highest sales generating drug, will lose patent protection in Europe as of

May 2011 (Stocks, 2010)2.

2.8 Stock Market Performance

The first ten years of the new century have been an experience of mixed feeling and

mediocre performance for the Novartis share with a lot of ups and downs (see appendix

3). After the burst of the internet bubble at the beginning of the decade equity markets

were pressured on a global scale and the share of Novartis dropped in value by 16%

from 71.63CHF to 60.00 CHF. Other pharmaceutical companies were also affected

since the MSCI World Pharmaceutical Index decreased by 15%. In 2002 the situation

did not improve with equity markets still under pressure. Again, the stocks of Novartis

decreased by 16% from 60 CHF to 50.45 CHF. In 2003 however, situation improved

with equity markets recovering from a difficult period between 2000 and 2002. The

MSCI World Pharmaceutical Index increased by 14%. Novartis share also recovered

over the year, increasing broadly together with industry peers by 11% from 50.45 CHF

to 56.15 CHF. After a bit of a deadlock in 2004 where markets faced a challenging

environment and the Novartis share increased by 2%, global equity markets further

recovered in 2005 which saw the Novartis share increasing by 21% from 57.30 CHF to

69.05 CHF due to continued strong earnings, a good product portfolio and appropriate

strategic direction (Novartis, 2006, p.6). With this performance, the company

outperformed the majority of its global pharmaceutical peers (Novartis, 2006, p.134).

2http://www.stocks.ch/nachricht/KREDITRATING_Novartis_Moody_s_bestaetigt_Aa2__senkt_Ausblick_

auf_negative__37251

19 of 130

Source: own design

-15%

-14%

13%

4%

23%

4%

-9%

-12%

11%

-0,2 -0,15 -0,1 -0,05 0 0,05 0,1 0,15 0,2 0,25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Figure 8: Total Shareholder Return

In 2006 equity markets kept recovering despite a sharp mid-year recession. The

Novartis share has increased only by 2% to 70.25 CHF, despite outstanding

performance in 2006 with a 15% rise in group net sales and a 17% increase in net

income. In 2007, Novartis shares have declined by a whopping 12% to 62.10 CHF.

Most pharmaceutical companies experience negative share price performance due to

volatility of equity markets as well as lack of interest by investors in the pharmaceutical

industry. Despite record results of the company, the performance was not reflected in

the share price. The pharmaceutical industry seems to suffer from devaluation resulting

sharp declines of price/earnings ratios. Reasons for this are the increasing suspicion of

financial markets towards the industry as well as the fact that governments are trying to

cut health care costs by forcing the pharmaceutical industry to lower drug prices

(Novartis, 2008, p.10).

In 2008 the financial crisis that originated in the United States hit the global markets

which also caused the Novartis share to drop by 15% from 62.10 CHF to 52.70 CHF.

However, the stock perceived by investors as a defensive investment, offered protection

from global market turmoil which led to unseen losses in decades. Thus Novartis was

the top performing stock in the pharmaceutical industry in 2008 and even outperformed

the Morgan Stanley World Pharmaceutical Index which fell by 20% (Novartis, 2009,

p.11 and p.174).

2009 saw an improved performance of

the Novartis share which increased by

7% to 56.50 CHF reflecting the

consistent good performance of the

company and its ability to cope with

adverse economic situations as caused by

the financial crisis in 2008 and 2009.

Furthermore, since the company’s

founding 1996, Novartis has consistently delivered a good performance providing

investors with a 9% annual total shareholder return compared to 7.5% of large industry

peers (Novartis, 20010, p.179). As can be seen from figure 8 total shareholder return

underwent a mixed development from 2000 until 2009 however negative returns could

have even been higher if it were not for the constant high dividends paid by Novartis to

its shareholders.

20 of 130

3 Strategic Business Analysis

In this chapter the strategic business environment of Novartis is analyzed. First an

analysis of the external business environment of Novartis is conducted which is

followed by an internal analysis of Novartis. The strategic business analysis is then

concluded with a SWOT analysis.

3.1External Analysis

In order to analyze the external business environment of Novartis a PESTEL analysis is

done and the global pharmaceutical market’s size and growth is determined. Then

Porter’s five forces are analyzed followed by a key industry success factors analysis.

Finally, the competitors of Novartis are analyzed.

3.1.1 PESTEL Analysis

The PESTEL framework is a method to analyze the macro environment of a company.

It assists in understanding the external factors that influence the development of a

company. There a six such type of factors: political, economical, socio-cultural,

technological, environmental and legal. These factors are not mutually exclusive and

can affect a company from more than just one angle (Lynch, 2006, p.84-85).

3.1.1.1 Political Factors Political issues a very relevant in the pharmaceutical and healthcare industry and can

influence the profitability of a pharmaceutical company considerably. This is especially

true for countries that have a government sponsored healthcare system.

In the last 50 years medical development has made huge progress leading to an aging

population. People being 65 and older account for an increasing part of the world’s

population. Reasons for this are higher life expectancy and declining birth rates. In the

last 50 years the global population has doubled reaching roughly seven billion people

(Novartis, 2010, p.145). Furthermore, especially in the industrialized world and

emerging markets bad eating habits combined with a lifestyle lacking physical activity

are increasingly causing chronic diseases. A major problem is obesity which is the

prime cause for diabetes and cardiovascular conditions.

This in turn poses a growing burden for many national healthcare systems. Costs related

to healthcare and medicines continue to increase as a percentage of Gross Domestic

Product (GDP) in many countries, leading governments to seek ways to lower these

21 of 130

costs (Novartis, 2010, p.144). Possible ways to cut these costs are increased usage of

generic medicines, restricted access to new medicines, price regulations, changes in

patent-protection periods and forcing patients to pay a bigger portion of healthcare costs

(Rheinische Post, 2010)3. In the United States, the biggest market for pharmaceuticals,

70 per cent of total prescription volume is accountable to generic medicines severely

limiting sales growth of new medicines (Novartis, 2010, p.145). Whatever decisions

will be made in the future, the pressure of insurances and regulators on pharmaceutical

companies is likely to rise.

Especially prices and patent periods for new innovative medicines generate rising

controversy and political discussion worldwide due to growing healthcare expenditure

while global economic growth is slow and the overall economic situation being fragile.

But also important to note is the fact, that costs per drug approved have risen

dramatically in recent years. According to the Tufts Center for the Study of Drug

Development, worldwide pharmaceutical companies have spent nearly $50 billion in

2010 on R&D activities. R&D spending for a new molecular entity approved has

increased by more than 200 per cent to $3,7 billion for the period of 2006-2008

compared to only $1,2 billion for the period between 1998 and 2000 (Novartis, 2010,

p.145). This is a result of increased and more rigorous safety requirements by health

authorities especially in the United States. In recent years regulators demanded more

clinical trial data with higher number of participants making regulatory approvals more

costly and more challenging as well as increasing the risk of recalls.

Despite the heated debate about healthcare costs, people and regulators (who still

demand effective and a high quality medicines) easily forget that developing new drugs

is a lengthy, risky and costly process that is far from certain which often does not result

in a desired outcome, namely a new approved drug (Schwartz and Moon, 2000, pp.87-

88). Regulatory Approval for new drugs might take up to ten years and can involve

costs of over one billion USD but productive R&D activities remain vital to the success

of Novartis (Novartis, 2007, p.132). Therefore long patent protection periods are

necessary to enable innovative pharmaceutical companies, such as Novartis, that do not

just produce generics, to get compensation for their investments in research and

development. Furthermore, if healthcare authorities will start to regulate prices for new

3http://www.rp-online.de/politik/deutschland/Roesler-fordert-Beitrag-der- Pharmaindustrie_aid_821926.html

22 of 130

Source: own design

32%

42%

18%

8%

Figure 9: Group Net Sales by Region

United States

Europe

Asia/Africa/Australasia

Canada Latin America

medicines, as suggested by politicians in Europe and the United States, in order to lower

prices and thus costs to the healthcare systems, Novartis and it peers will face further

problems to recover their initial product development costs.

As can be seen from the information provided above political factors can have a huge

impact on the operations of Novartis and its profitability. Should the development keep

heading in this direction that prices will have to be further lowered and that even current

patent-periods be shortened than developing new effective drugs will become extremely

difficult. As a result the number of new drugs that will become available to patients in

need might be severely reduced.

3.1.1.2 Economic Factors Economic factors also play an important role, that effect a pharmaceutical company

such as Novartis. Maintaining a healthcare system that provides effective treatment and

medicines costs a lot of money. Therefore it is not surprising that Novartis generates

about three quarters of its group net sales in countries of the developed world, such as

the US, EU and Japan, that generate considerable economic strength. This is depicted in

figure 9.

These countries also generate the highest GDP (see appendix 4). This economic wealth

is also reflected in Novartis’ sales by

region record. However, one should not

neglect the strong and stable economic

growth of emerging markets despite effects

of the global financial crisis. IMS Health

forecasts between 12 and 15% growth in

2010 and the coming years in these areas,

presenting Novartis with extremely

lucrative sales opportunities (Novartis, 2010, p.143).

As far as economic volatility is concerned, pharmaceutical companies are also affected

by economic downturn and recession but not as severely as other industries such as

consumer goods or luxury goods industries. Reason for this is the fact that patients

cannot give up medication they rely on when the overall economy is in recession.

Demand for drugs is more independent from the economic situation than other goods

since they cover a basic need.

23 of 130

Thus the pharmaceutical industry is considered a non-cyclic industry. Investors perceive

Novartis as a defensive investment with strong performance despite turmoil on stock

markets proven by the fact that Novartis outperformed other indices such as the Swiss

Market Index and MSCI Pharma Index during the crisis in 2008 (Novartis, 2009, p.174)

(see also appendix 5).This is also supported by the pharmaceutical industry’s average

beta of 0,7 4 showing that the industry is not very sensitive to economic volatility. If the

market changes by one per cent the pharmaceutical industry would only change by

0,7%.

Another important factor that affects Novartis in some way is the situation on global

capital markets. Even though financial markets have recovered to a somewhat stable

situation after the global financial crisis the ex-ante situation where corporations had

almost unlimited access to money will unlikely be restored. This however, does not

pose too much of a problem for Novartis since it follows a more conservative capital

structure.

Novartis is a worldwide operating company and thus faces exchange rate exposure

which might have significant effect on the company’s operating results as well as

reported value of assets. Transaction exposure is not too much of challenge because

most operating costs are incurred where necessary local currencies are generated

through sales (see appendix 6). Nevertheless Novartis still has to engage in hedging

activities to manage currency exposure.

3.1.1.3 Socio-Cultural Factors Socio-cultural factors are fundamental growth drivers for Novartis and they remain

strong for the foreseeable future increasing demand for healthcare products. Main

drivers are demographic and socio-economic developments such as increasing

population, higher life expectancy as well as changing lifestyle due to increased

prosperity. Novartis expects to keep expanding in the next years both in traditional

markets such as the United States, Europe, Japan and emerging markets. Emerging

markets are considered by IMS Health as Brazil, China, India, Mexico, Russia, South

Korea and Turkey (Novartis, 2010, p.143-145).

4 Demadoran beta by industries

http://pages.stern.nyu.edu/~adamodar/

24 of 130

The world population is expected to surpass nine billion in 2050 with increase portion

of the population being 65 years or older. A study by the US State Department in 2007

forecasted that in 2030 one billion people worldwide will be 65 years or older. Studies

show that disease occurrence and drug consumption rise with age (Novartis, 2010,

p.143). Furthermore economic growth, increased automation and changing lifestyle and

eating habits will continue to cause chronic diseases such as cardiovascular diseases,

diabetes, cancer and serious other diseases. A World Health Organization (WHO) study

in 2006 reported that obesity and overweight are not only a problem of wealthy

countries but are also increasing dramatically in low and middle income countries.

Obesity is a prime cause for diabetes and cardiovascular diseases. The WHO predicts

that diabetes will increase to 330 million people worldwide compared to only 30 million

in 1985 (Novartis, 2010, p.144).

Novartis is able to provide many different products in order to help patients with their

diseases and will continue to invest heavily in research and development. The predicted

developments mentioned above represent high future income potential for Novartis and

will remain a distinguishing characteristic of the healthcare industry in the future.

3.1.1.4 Technological Factors Technological progress is very important for pharmaceutical companies, especially for

those like Novartis that follow a strategy of differentiation and innovation.

Technological progress has been astonishing in the last 20 to 30 years and will keep

advancing in the future. This is a clear result of a tenfold increase in R&D investment

by the global pharmaceutical industry in the last 20 years according to the PhRMA, a

US industry trade association (Novartis, 2010, p.144).

Technological progress and advanced understanding of many diseases are a basis for the

ongoing development of better ways of treatment. Recent advances in the analysis of

human genome data will further improve information on the role of genes and proteins

within the human body. Based on this information it is expected that the number of drug

developments will continue rise even further (Novartis, 2009, p. 140). Of course, no

miracles can be expected over night but steady research will pay off in the future with

new breakthroughs in knowledge and treatment.

25 of 130

3.1.1.5 Environmental Factors Environmental factors are important external aspects that cannot be ignored by

companies, especially pharmaceutical companies. Increased environmental awareness

among patients, consumers and people in general, combined with global warming and

other environmental hazards have forced companies to make adjustments. Increasingly

consumers do not only request high quality and safe medicines from producers but also

environmental friendly production procedures and plans to reduce energy and resource

consumption. This has led pharmaceutical companies and companies from other

industries to create environmental friendly images as well as plans for sustainable

development. Failure to follow this trend could have serious consequences on the

company’s image leading people to belief that the company is polluting the

environment and ruthlessly exploiting the resources of the planet

As a result Novartis has early on included environmental issues in his code of ethical

business conduct in which it commits itself to the conservation of energy and other

resources. Furthermore, Novartis recognizes the rights of animals. Animal testing is an

indispensable part of experimental studies for new drugs without which the

development of new drugs would be nearly impossible. Despite the fact that Novartis

abides to the highest standards for its animals and reduces animal testing whenever

possible the company and its employees are frequently harassed by militant animal

rights activists in an almost terroristic manner (Novartis, 2010, p.66).

With regards to carbon dioxide emissions, Novartis was one of the early signatories of

the Kyoto protocol in 2005. Since then Novartis has constantly put effort into reducing

greenhouse emission, increasing energy efficiency and increasing usage of renewable

energy resources. Novartis is constantly increasing the Group’s solar power capacity on

a worldwide scale for example (Novartis, 2010, pp.83-84). Novartis’ environmental

efforts are frequently honored by appearing at the top of Fortune magazine’s list of most

admired companies among others.

3.1.1.6 Legal Factors Companies active in the pharmaceutical industry face already strict and rigid legal

regulation around the world, especially in the United States and Europe. There, the local

health authorities responsible for drugs approvals and related matters are the Food and

Drug Administration (FDA) and the European Medicines Agency (EMEA) respectively.

These agencies have immense political and legal power and are pressuring Novartis and

26 of 130

Source: own design

323,8

263,9

106,6

9547,9

Figure 10: Global Market Sales by Region

North America

Europe

Asia/Africa/Australia

Japan

Latin America

other industry peers to lower prices and provide enormous loads of information on

safety, efficiency and risk/benefit profile for evaluation and approval purposes. This

development is likely to continue and even increase with requirements and legislation

getting stricter and more involved. Proof for this is the Food and Drug Administration

Amendments Acts 2007 signed by former President George W. Bush5 .

As a result, the drug approval rate in general is expected to decline. For Novartis and

other industry peers this means that research and approval activities will get

increasingly expensive and will further elevate the risk of recalls, setback and possible

loss of market share (Novartis, 2010, p.145).

Along with increases in regulation, a trend of increasing litigation against the

pharmaceutical industry can be recognized. As a result Novartis is increasingly involved

in legal proceedings due to various causes that could lead to substantial liabilities which

might not be covered by insurance in total. Since legal proceedings are very

unpredictable, negative effects on results of operations are probable (Novartis, 2010,

p.146).

3.1.2 Market Definition and Size, Growth and Market Share

In this section the market in which Novartis operates is defined. Furthermore market

size, growth and share will be analyzed.

3.1.2.1 Market Definition and Market Size The pharmaceutical industry is a multi-billion

dollar industry made up of about 200 major

companies. The market is not controlled by a

single company that has overwhelming market

share. However, the most profitable companies

control market share of mid single digit market

share (Castner, Hayes, Shankle, 2007)6. The

global pharmaceutical market in which

Novartis operates is defined as patent-protected pharmaceuticals, generic

pharmaceuticals, vaccines and diagnostic tools and over-the-counter medicines. In 2009

the global pharmaceutical market’ size amounted to about $837 billion in sales 5 US Food and Drug Administration:

http://www.fda.gov/ForConsumers/ConsumerUpdates/ucm061229.htm 6 http://www.duke.edu/web/soc142/team2/firms.html

27 of 130

Source: own design

Table 1: Sales by Region

Region Sales 2009 Growth 2009 Forecast 2010 CAGR 2009-2014

North America 323,8 5,5% 3-5% 3-6%

Europe 263,9 4,8% 3-5% 3-6%

Asia/Africa/Australia 106,6 15,9% 13-15% 12-15%

Japan 95 7,6% 0-2% 2-5%

Latin America 47,9 10,6% 10-12% 12-15%

Total 837,2 7,0% 4-6% 5-8%

Source: Data from IMS Health

0

100

200

300

400

500

600

700

800

900

515562

605650

694742

782837

Figure 11: Total market sales (USD billion)

revenues. Of this, about 70% are accountable to North America, which is the largest

market for pharmaceuticals and Europe as seen in figure 10.

3.1.2.2 Market Growth In the year 2009 total global

pharmaceutical sales amounted to $837

billion as mentioned before. In 2002 total

market sales in this industry amounted to

$515billion yielding an increase of about

63% over eight years. The compound

annual growth rate (CAGR) from 2004 to

2009 was 6,7%. As can be seen from figure 11 total global sales in the pharmaceutical

industry were able to grow annually from 2002 to 2009. As depicted in table 1 North

America and Europe are still the largest markets, however the growth rates of these

markets have slowed down to about 5% in recent years. Meanwhile, markets such as

Asia and Latin America are increasing with double digit growth and are considered the

markets of the future. They

consists of emerging

markets such as China,

India, Russia, Brazil will

become of strategic

importance in the near future due to growing economic wealth. As for the future, North

American and European markets are expected to grow at moderate rate of 3-5% while

Asia and Latin America are expected to keep growing fast with growth rates in excess

of 10%. At times of decreasing pharmaceutical sales growth in many developed

countries, the long-term economic expansion in many emerging markets has led to

higher growth rates contributing to the industry’s global performance (Novartis, 2010,

p.143). The CAGR for total industry sales for the period 2009-2014 is forecasted to be

between five and eight per cent. All market related data mentioned above is based on

IMS Health data7.

7IMS Health Incorporated (2010)

http://www.imshealth.com/portal/site/imshealth/menuitem.a46c6d4df3db4b3d88f611019418c22a/?v

gnextoid=e599410b6c718210VgnVCM100000ed152ca2RCRD&cpsextcurrchannel=1

28 of 130

Source: own design

Figure 13: Porter’s Five Forces

7,3% 7,0% 6,5% 6,2% 6,0%

5,9% 6,5% 6,0% 4,5% 5,5%4,3% 4,9% 5,6% 5,4% 5,7%5,0% 5,3% 5,3% 5,4% 5,4%5,1% 5,4% 5,5% 4,9% 5,0%

72,4% 71,0% 71,1% 73,5% 72,5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009

Figure 12: Market Share

Others

Sanofi-Aventis

Novartis

Roche

GlaxoSmithKline

Pfizer

3.1.2.3 Market Share With regard to market share it can be

concluded that no single company controls

an overwhelming portion of the market.

Together the five biggest companies in the

industry Pfizer, Roche, Novartis,

GlaxoSmithKline and Sanofi-Aventis make

up about 28% of the total global

pharmaceutical market. The difference in

market share between these companies is very small and lies within 1%. Pfizer has the

largest market share with 6% as figure 12 is showing. The remaining a 72% of market

share are attributable to various other pharmaceutical companies around the world. The

figure also shows that the situation has not changed significantly over the last five years.

However, some small developments are noteworthy. Novartis, for example, was able to

increase its market share while Pfizer apparently lost more than 1% of market share

over the last 5 years.

3.1.3 Porter’s Five Forces Model

In the figure 13 Porter’s Five Forces Model is depicted. The model assissts in

understanding the competitive

environment of a company which

can have various implications. The

goal of the Five Forces Analysis is

to investigate how a company can

develop opportunities in its

environment while protecting

itself against market competition

as well as other threats. Thus this

analysis is concerned with the

forces that determine industry

competition (Lynch, 2006, pp.93-

94). The model employs five parameters that influence competition in a given industry.

These parameters are: bargaining power of suppliers, threats of potential new entrants,

bargaining power of buyers, threats of substitute products as well as rivalry among

29 of 130

existing firms. In the following these five key parameters are explained with regard to

the pharmaceutical industry.

3.1.3.1 Bargaining Power of Suppliers Novartis is a very large corporation with operations worldwide which also enables the

company to source necessary suppliers from different areas. Furthermore, the necessary

ingredients for drugs are largely of commodity nature where the real competence lies in

the exact chemical composition. Due to these reasons Novartis is estimated to have a

very good negotiating power. However, it should be noted that whenever a strategic

cooperation is entered with a supplier, dependence on this supplier increases and thus

the bargaining power of the supplier.

3.1.3.2 Threat of New Entrants The threat of potential new entrants in the pharmaceutical industry is estimated to be

small. Reasons for this assessment are the high initial costs, especially for research and

development and the years of experience and trust that existing industry participants

have. In the pharmaceutical industry it is important for companies to be perceived as

reliable and trustworthy by patients. Building such an image requires a long time and a

lot of financial effort.

3.1.3.3 Bargaining Power of Buyers Buyers in the pharmaceutical industry are considered to be governmental and public

healthcare institutions of various types and patients as end consumers. Bargaining

power of patients is assessed to be low to medium because if a patient relies on a certain

medicine that is even protected by a patent, bargaining power is relatively low. The only

power the patient has is to make is opinion public in case he is dissatisfied with the

product or the company and thus try to get some leverage over the image of the

company. Governmental and public healthcare institutions have more negotiating power

because of the size of their organization. Especially governmental healthcare institutions

put more pressure on pharmaceutical companies to lower prices and increase product

safety and availability.

3.1.3.4 Threat of Substitute Products The threat posed to Novartis and other industry peers based on substitution by other

products is considered to be low. First of all if substitution means product copies, patent

laws protect new pharmaceutical products for extensive periods of time. Furthermore,

enforcement of patent laws throughout the world has become more effective due to

30 of 130

agreed treaties between many countries to protect intellectual property. Secondly, if

substitution means to substitute one medicine for another from a rival company,

problems can occur with patient’s tolerance. Some patients cannot tolerate other equal

medicines due to various problems such as side effects, making a switch of products

difficult or impossible.

3.1.3.5 Industry Competition The pharmaceutical industry has various fields of special expertise, such as

pharmaceuticals, generics, vaccines or over-the-counter medicines that make it

impossible to make an overall assessment of competition. In the vaccines and patent-

protected pharmaceuticals part of the industry competition is low to medium because

products are very diversified. On the other hand competition in the generic

pharmaceutical industry is very high and intense (Novartis, 2010, p.145). In this

segment of the industry competition is mostly based on prices because these products

are considered commodities. Furthermore, efforts to shift more healthcare costs to

patients further intensify competition based on price. In the over-the-counter medicines

niche, competition is also high but focuses more on consumer brand acceptance and

loyalty than on price.

In conclusion, it can be summarized that industry forces from suppliers, new entrants,

buyers and substitution are low to medium. However, internal industry competition is

high in many parts of the industry and is expected to increase further in the future.

3.1.4 Key Industry Success Factors

Key factors for success in an industry are resources, skills that are essential to achieve

success where success if often measured in profitability. Key factors of success are

common to all companies in an industry and do not differ from one company to another

(Lynch, 2006, p.92). Determining key success factors for the pharmaceutical industry

helps to assess whether or not Novartis has competitive advantage in these areas and

whether it is able to generate and sustain future profitability. For the pharmaceutical

industry key success factors are determined to be Research and Development,

competent employees, organizational efficiency and product quality, financial strength

as well as marketing and sales.

31 of 130

3.1.4.1 Research and Development Successful research and development activities are necessary to bring new approved

medicines to the market and to keep the pipeline filled with potential new medicines.

Only if a company is successful in its research and development of new drugs it will be

able to receive new patents which enable the company to receive high rates of return.

These in turn are necessary to finance research and development activities continuously.

3.1.4.2 Competent Employees For a pharmaceutical company it is especially important to attract and hire highly

qualified employees because the pharmaceutical business has high technological and

scientific requirements. Furthermore, talented people are necessary to market and sell

new medicines and convince patients and physicians of the benefits of the new drugs.

3.1.4.3 Organizational Efficiency and Product Quality Organizational efficiency is becoming increasingly important because external pressure

from governments and other health institutions to reduce healthcare costs and prices for

medicines has been increasing significantly in recent years. To cope with these

requirements pharmaceutical companies have to streamline their processes and reduce

costs. This however cannot be achieved at the expense of product quality or safety.

Inadequate quality and safety could have disastrous effects on the image of the company

and thus customer loyalty.

3.1.4.4 Financial Strength Financial strength is also considered to be a key success factor. Financial strength is

required to finance the increasing costs for research and development. Furthermore,

strategic acquisitions to acquire needed technologies or to set up new strategic business

units require large amounts of capital and financial strength. The same is true for market

expansion into emerging markets that will be of strategic importance in the near future.

3.1.4.5 Marketing and Sales Marketing and sales is also an important area necessary for success. Patients and

physicians have to be convinced of the benefits of new medicines and distribution

networks have to be set up in order to market products in emerging markets.

3.1.5 Competitor Analysis

In this section two competitors that are similar to Novartis are analyzed. In an ever

complex economic situation analyzing and understanding immediate competitors is very

important. In the global pharmaceutical industry there are many competitors but it is not

32 of 130

possible to analyze all of them. Therefore a choice has to be made and usually the one