A-V a'I(m- ~~-F Report No. 6892-ME · This document has a resticted disibution and may be used by...

129

Documentof The World Bank FOR OFFICIAL USE ONLY A-V a'I(m- ~~-F Report No. 6892-ME STAFF APPRAISAL REPORT MEXICO STEEL SECTOR RESTRUCTURING PROJECT February 8, 1988 Country DepartmentII Industry,Trade, Finance Sector OperationsDivision Latin America and the CaribbeanRegional Office This documenthas a resticted disibution and may be used by reciplents only in the performance of their officialduties. Its contents may not otherwise be disclosed without World Bank aothorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of A-V a'I(m- ~~-F Report No. 6892-ME · This document has a resticted disibution and may be used by...

Document of

The World Bank

FOR OFFICIAL USE ONLY

A-V a'I(m- ~~-F

Report No. 6892-ME

STAFF APPRAISAL REPORT

MEXICO

STEEL SECTOR RESTRUCTURING PROJECT

February 8, 1988

Country Department IIIndustry, Trade, Finance Sector Operations DivisionLatin America and the Caribbean Regional Office

This document has a resticted disibution and may be used by reciplents only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank aothorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS - Peso (Mex$)

An exchange rate representing the mid-June 1987 freemarket rate has been used in the project analysJs:

US$1 - Mex$1,235

The most recent exchange rate as at January 26, 1988, was:

US$1 - Mex$2,206 in the free market

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS AND ACRONYMS

AHMSA - Altos Hornos de Mexico S.A.BOF - Basic Oxygen FurnaceCANACERO - Camara Nacional de la Industria del Hierrc, y del AceroCMC 1/ - Carbon y Minerales Coahuila S.A.DRC - Domestic Resource CostEAF - Electric Arc FurnaceFISA - Fundidora Monterrey S.A.HYLSA - IiYLSA S.A.mtpy - million tonnes per yearNAFIN - National Financiera S.N.C.NKK - Nippon Kokan of JapanOHF - Open Hearth FurnaceRMD - Raw Materials Division of SIDERMEXSECOFI - Secretaria de Comercio y de Fomento IndustrialSEMIP - Secretaria de Energia, Minas y Industria ParaestatalSICARTSA - Siderurgica Lazaro Cardenas Las Truchas S.A.SPP - Secretaria de Programacion y PresupuestoTAMSA - lubos de Acero de Mexico S.A.tpy - tonnes per yearUEC - United Engineers and Consultants (Div. of US Steel)

1/ CMC is the legal entity being set up as a holding company tooversee the mining operations of the Raw Materials Division ofSIDERMEX.

ION OFFkAL US ONLY

MEXICO - STEEL SECTOR RESTRUCTURING PROJECT

TABLE OF CONTENTS

Page No.

LOAN AND PROJECT SUMMARY i - iv

I. INTRODUCTION ................... .O 0 1

II. BACKGROUND e 2

A. The Economy - Recent Structural Changes 2.................. B. The Steel Sector *............... , 3C. Structure and Main Institutions 4 6D. The Policy Framework ... .................................. 6

III. STRATEGIC ISSUES AND BASIS FOR SECTOR REFORM ................ 8

A. Strengths and Weaknesses ........................ . , 8B. The Strategic ;ssues ..................................... 9C. Agenda for Policy Reform ................................. 10

IV. THE RESTRUCTURING PROGRAM ................................... 11

A. Objectives *..........o......o......* 000e00oooo00ooo 000o 11B. Global Policy Actions ..............0........ , 0e..000 e. 12Co SIDERMEX .eo........o...00000oo 0o 00o0oo 0oooo0oo0o00o00oooo 14D. Private Sector .............. 17

V. THE PROJECT o...................................O,.. ....... 18

A* Objectives ....oo.ooo..o..o.oo......oo. e oe*o 18B. Project Description *o.ooe...oo.o........ e...............o 19C. Project Management, Organization and Implementation ...... 21D. Role of NAPIN *.....0.......... ...............e......o 23g. Training and Manpower Development soeoo0ooo00)00o000000000@ 23Fo Environmental Issues ..................................... 24

VI. CAPITAL COST, PINANCING PLAN, PROCUREMENT AND DISBURSEMENT oo. 25

A. Capital Cost ooooo........................................ 25B. Financing Plan oo.....................................o ... 26C. Onlending Arrangements .0..........................o..o.... 28D. Procurement o..ooo...o.oo.o.o..ooooo.o.oo.oo...o....o* 29E. Allocation of the Loan and Disbursements ................. 30F. Auditing .*000000000000,00 000000000000000000w [email protected] 32

This report was prepared on the basis of appraisal missions in March andMay 1987 by Messrs. R. Venkateswaran, E. Mangan, I. Rivera and G. Konomos(Consultant) with assistance from Mr. X. Simon, and in the raw materialssegments by Messrs. F. Remy, S. von Klaudy and L. Moran (Consultant) allformerly of the Industry Department. Mr. J. Malatinsxky of the LatinAmerica and Caribbean Region also assisted in the preparation.

Thidocumenthmansetitedditbudtnand maybeoud by re -in oly in d peformneoof thek officW dutis Its contents maY no othwise be dicosed wihout Wod bnkauthoizbon.

TABLE OF CONTENTS (contd.) Page J4o.

VII. FINANCIAL EVALUkTION .......................... 33

A. Assumptlons Used and Forecast of Production Costs .*.. . 33B. Financial Projections ..................... 36C. Financial Covenants ..... e.............. *.*.... 40D. Financial Rate of Return ................................ 40

VIII. ECONOMIC EVALUATION AND RISKS ............................... 42

A. Assumptlons .................................... 42S. Economic and Rate of Return Analysis .................... 42C. Domestic Resource Costs and CompetitLve Positlon ......... 44D. Benefits and Risks * ..................................... 45

IX. AGREEMENTS REACHED AND RECOMMENDATION ....................... 46

ANNEXES

2-1 The Steel Sector in Mexico ................................ 492-2 Raw Haterial Supply Position .............................. 552-3 The Policy Framework and Proposed Policy Changes .......... 63

3-1 Operations Technology and Strategic Position 713-2 Competitive Position of Raw Materials 773-3 The Steel Market in Mexico ..... *.*.*................ 81

4-1 Matrix of Issues, Measures and Actions 874-2 Steel Sector Policy Letter 89

5-1 Imports Eligible for Financing ..... 935-2 The AHKSA Component ..................................... 94

Appendix 1 - Environmental Control 995-3 The CMC Componentt 1025-4 SIDERMEX - Strategic Planning Studies 1055-5 The HYLSA Component 107

6-1 Summary Project Cost - AHMSA Project Component - Part Bo1 . 1106-2 Summary Project Cost - CMC Project Component - Part B.2 1116-3 Summary Project Cost - HYLSA Project Component - Part C 1126-4 Sumary Total Project Cost - Parts B and C ................ 1136-5 Estimated Disbursement Schedule of Bank Loan .............. 114

MAPS

IBRD 20418 - Steel Mills and Major MarketsIBRD 20419 - Iron Ore Mines, Coal Mlnes and Natural Gas Pields

TABLE OF CONTENTS (contd.)

SELECTED DOCUMENTS AND DATA AVAILABLE IN THE PROJECT FILE

A. Reports and Studies on Steel Subsector

Al IBRD: Mexico Steel Sector Strategy Study, October 1936 (ReportNo. 6429-ME)

A2 Miscellaneous Market and Sector Data (see also Al above)

B. Reports and Documents on Companies and Individual Project Components

34.1 SIDERMEX: Convenio and Supporting Studies and Annexes on SIDERMEXRestructuring Progzam

B5.1 AHMSA: Industrial Reconversion Project, Phase I - Technical andFinancial Feasibility Study

B5.2 AHNSA: Report of UEC Consultants (incorporated i BSi.1 above)

B5.3 Raw Materials Division: Report of UEC Consultants (METCHEMDivision). Fe&sibility Study and Technical Proposal

B5.4 HYLSA: Report of Nippon Kokan Consultants (February 1987)

B35.5 HYLSA: Technical and Financial Feasibility Studies

B6.1 AHMSA: Detailed Cost Estimates

36.2 Raw Materials Division: Detailed Cost Estimates

B6.3 HYLSA: Detailed Cost Estimates

B7.1 Working Papers on Financial Analyses of AHMSA, HYLSA and RavMaterials Division Components including Feasibility Studies preparedby the Companies

B8.1 Working Paper on Economic Analysis of Products and Project ComponentsPrepared by Bank staff

MEXICO - STEEL SECTOR RESTRUCTURING PROJECT

Loan and Project Summary

Borrower: Nacional Financiera, S.N.C.

Guarantor: United Mexican States

Beneficiaries: Government, SIDERMEX, AHMSA, CMC and HYLSA.

Amount: US$400 million equivalent

Term:s 15 years, including 3 years grace, at the standardvariable interest rate.

Loan andProdeetDescription: The proposed Bank loan would help finance the foreign

exchange cost of a major restructuring and policy reformprogram for the Mexican steel industry. The public sectorportion of the program aimed at rationalizing SIDERMEX hasalready resulted in the shutdown of one major steel plant,ENSA, and includes an additional reduction in steelmakingcapacity and shift in product mix at its largest remainingplant, AHMSA. Investments are aimed at rehabilitation,cost reduction and quality improvement of the flat productlines at AHMSA and supporting raw material supply. Asimilar program is included for the privately owned HYLSAMonterrey flat product facilities in order to maintain itsdomestic competitive market position. Investments areonly included in facilities for which the long-termdomestic market needs have been identified.

Part A-(US$100 million) is tied to implementation of pricedecontrol, trade reform, including elimination of OfficialReference Prices for steel products and reduction andequalization of steel tariffs, and presentation of aGlobal Steel Sector Policy Statement to expose theindustry to international competition. It would fiaan&eeligible raw material and steel product imports during theadjustment period.

Part B (Us$225 million) provides financing for theSIDERMEX restructuring program comprising the physicalrehabilitation of the AMHSA steel works (UJ$170 million)and rehabilitation and restructuring of SIDERMEX Miningoperations (US$50 million). It also provides assistancein corporate-wide organizational and financialrestructuring and for development of SIDERMEX's long-termstrategy (US$5 million).

Part C (US$75 million) supports the restructuring effortof HYLSA in the modernization of its flat productsfacility, in parallel with the financial restructuringpackage under negotiation with creditor banks.

- ii -

Onlending Termsand Conditions: Part A, the Inpat Materials and Steel Product Imports

Component of the Project, to Government, at 0.25% abovethe Bank's standard variable interest rate and with thesame terms as the Bank loan. Parts B and C, in support ofthe SIDERMEX Restructuring Program and HYLSARestructuring, respectively, to SIDERMEX, AHMSA, SIDERMEXMines (Carbon y Minerales de Coahuila, SA, CMC) and HYLSA,at a rate equal to 110% of the Bank's standard variableinterest rate and with the same terms as the Bank loan.

Benefits andRisks: The decontrol of domestic steel prices, coupled with the

trade liberalization measures already implemented and theoverall restructuring of the steel subsector, will lead toefficient import competition, forcing domestic steel pro-ducers to improve quality and product mix in order toserve better downstream steel consuming industries. Bud-getary transfers to the public steel sector, and indirectsubsidies to the industry as a whole, would be eliminatedand the necessary internal funding would be provided forthe proposed restructuring and rehabilitation of thephysical plant of the entire subsector. The physicalrehabilitation of the AHMSA, and HYLSA plants will sub-stantially improve the international competitiveness offlat products both in terms of better quality and loweroverall cost. Rationalization of existing capacity willalso allow the two plants to improve utilization. Down-stream users of flat products will be able to obtain awider range of quality flat products at lower cost. Therehabilitation of the SIDERMEX mines will allow lower costexploitation of available resources and maintain Mexico'scomparative advantages in steel production. Technicalassistance (financed from other sources) will enable thesteel producers to map out viable long-term strategies andthe means to implement them.

The main potential risk is that the Government will delayactions on complete price decontrcl which could aggravatethe financial position of steel producers and induce areturn to higher protection. The steel price increasesaccorded in December 1987 and January 1988, and the agree-ment on monthly adjustments of steel prices in real termsbased on changes in the Consumer Price Index until elimi-nation of price controls by not later than December 31,1988 minimize this risk. Additional risks include areversal of agreed policy actions and a sharp real appre-ciation of the exchange rate which could affect projectviability. The agreements concerning the definition offuture investment strategy, the Government's commitment tothe liberalization program, the substantial physicalrestructuring and rehabilitation of the public sector com-panies, and agreement on Action Plan for monitoring opera-tions and performance of the target companies all combineto mitigate the potential adverse impact of the aboverisks.

- iii -

EstimatedDisbursements: Part A of the Loan would be disbursed in two equal

tranches linked to trade liberalization., price decontroland elaboration of a Global Steel Sector PolicyStatement. Retroactive financing up to a maximum ofUS$20 million for eligible import expenditure afterNovember 1, 1987, would be allowed. The first tranchewould be available for disbursement at loan effectiveness.The second tranche would be released upon completeelimination of any remaining price controls on domesticsteel products, continued maintenance of the tradeliberalization measures, and presentation of the GlobalSteel Sector Policy Statement along substantially agreedlines. The second tranche release is expected in January1989.

Parts B and C of the Loan would be disbursed againsteligible goods and services procured under World Bankguidelines, including retroactive financing up to amaximum of US30 million equivalent for expendituresincurred after February 1, 1987.

EstimatedProject Cost: The estimated project cost and financing requirements (not

including normal capital replacements) for the period1987-1991, are summarized in the following table:

Local Foreign Total(USJi0llion equivalent)

Part A - 100 100Parts B and CEquipment and Spares 88 328 416Civil Works/Erection 91 10 101Engineering Project Management 17 17 34TA/Training 8 18 26

Base Cost 204 373 577

khysical Contingencies 25 36 61Price Escalttion 38 30 68

Installed Cost 267 439 706

Taxes and Duties 104 - 104Total Installed Cost 371 439 iiRS

Incremental Working Capital 80 20 100Total Project Cost 451 195 !i

Interest during Construction 4 36 40

Total Financing Required 455 495 950

GRAND TOTAL 455 595 1,050

- iv -

FinancingPlant The proposed financing plan for the Project is summarized

in the following table:

Local Foreign Total(in US$ M equivalent)

IBRD - 400.0 400.0Local Baars 64.0 - 64.0AMSA 185.0 92.0 277.0CMC 78.0 56.0 134.0SIDERMEX 3.0 - 3.0RYLSA 125.0 47.0 172.0

455.0 595.0 1,tO0.0

EstimatedSchedule ofDisbursements: IBRD FY: 1988 1989 1990 1991 1992 1993

Annual 58.1 108.8 110.4 86.8 26.4 9.5Cumulative 58.1 166.9 277.3 364.1 390.5 400.0

Economic Rateof Return: In excess of 18?

Staff AppraisalReport: No. 6892-ME dated February 8, 1988

&-mv8 IBRD - 20418 - Steel Wines and Major MarketsIBRD - 20419 - Iron Cra Mines, Coal Mines and Natural GasFields

MEXICO - STEEL SECTOR RESTRUCTURING PROJECT

I. INTRODbCTION

1.01 The Government of Mexico (GOM) has requested a Bank loan to helpfinance the restructuring of the Mexican steel industry, and support policyreforms that will substantially alter the manner in which steel producersconduct and develop their business in the coming years. The proposed leanof US$400 million equivalent comprises three major elements: Part A(US$100 million) is tied to implementation of wide-ranging policy measureswith specific emphasis on exposing the industry to internatio2kalcompetition, and would finance steel-related imports during the adjustmentperiod. Part B (US$225 million) provides financing for the restructuringneeds of the public sector steel company, SIDERMEX, including the physicalrestructuring of its integrated steel plant and the country's major flatproduct facility, AHMSA, and its coal and iron ore mining operations, aswell as corporate-wide organizational and financial restructuring andlong-term strategy formulation. Part C (US$75 million) supports therestructuring efforts of the major private sector steel producer, HYLSA, inthe modernization of its flat products facility at Monterrey, in parallelwith a financial restructuring package that has been negotiated withcreditor banks.

1.02 Project financing requirements, including contingencies, priceescalation, interest during construction and incremental working capitalare estimated at US$946 million equivalent net of US$104 million equivalentof taxes and duties, with about US$595 million equivalent in direct andindirect foreign exchange costs. The proposed Bank loan of US$400 millionwould thus cover about 67% of the estimated direct and indirect foreignexchange costs, or about 421 of the total financing requirements net oftaxes. The balar.ce of the financing needs are to be met from internal cashgeneration and from short-turm borrowing for working capital. Supplierscredits and/or cofinancing represent other possible funding sources.

1.03 Bank involvement in the project arose from initial discussionswith Mexican authorities in 1985, as part of the review of the country'ssectoral investment plans. A Bank mission in May 1986 carried out a SteelSector Strategy Review (Report No. 6429-ME). Bank missions in Septemberand November 1986, reviewed this report and its recommended changes insteel sector pricing policy and the product mix and investment strategy ofSIDERMEX, with Government authorities, SIDERMEX management, and privatesector representatives. Following these reviews, project identificationwas completed and SIDERMEX and HYLSA began to assemble the technicaldetails with the help of outside consultants. A Bank mining review missionfirst visited Mexico in January 1987. The project was preappraised inFebruary 1987. Appraisal was initiated in March and completed in May 1987when the final technical reviews by consultants became available.

1.04 Previous Bank involvement in the steel sector began in 1972 whenMexico embarked on a rehabilitation and expansion program designed toincrease raw steel capacity to about 9.2 million tons per year by 1980 and11.0 million tons by 1985 in order to satisfy growing domesti.- demand andto improve productivity of their existing facilities. As part of thisprogram, in 1973 the Bank extended a loan (President's Report No. P-1307-ME

- 2 -

of August 21, 1973 and Appraisal Report No, 220-ME dated August 10, 1973)of US$70.0 million to SICARTSA to finance a new integrated steel plant atLazaro Cardenas on the Pacific Coast. The plant has a capacity of1.1 muilion tons per year of non-flat products (rebars, merchant bars, wirerods). The project also included the development and exploitation of acaptive iron ore mine and a port to handle imported raw materials (mainlycoking coal) and export of excess finished products. The project wasimplemented and commissioned in collaboration with British SteelCorporation under a general know-how and technical assistance agreement.The project was completed successfully, a few months behind schedule andwith some cost overruns due to the particularities of the project(greenfield plant in an underdeveloped region, new staff, period of highinflation throughout the world, etc.). The plant is now operating close torated capacity producing high-quality non-flat products at internationallycompetitive costs.

,05 In 1976, the Bank approved a loan of US$95.0 million for thesecond stage of the SICARTSA program (Appraisal Report No. 1060-ME ofJune 15, 1976) designed to produce 1.7 million tpy of flat steel products(hot and cold rolled coils and sheets). The Government of Mexico, whichchanged shortly after the approval of the loan, decided to reconsider theproject and consequently cancelled the Bank loan. A new project, based ondirect reduced iron ore, producing different flat products (heavy plate),was presented to the Bank in 1979/80. The Bank decided not to participatebecause the market demand analysis for the new product was consideredinsufficient. The project, SICARTSA II, is still under construction withfinancial and technical assistance from Japan and che United Kingdom.

II. BACKGROUND

A. The Economy - Recent Structural Changes

2.01 Following three decades of high and stable economic growth fromthe 1940s through the 1960s, the Mexican economy started to slow down inthe early 1970s. The Government attempted to foster growth throughexpansion of the public sector. The oil boom of the mid-1970s inducedfurther inflationary expansion that led to a basic disequilibrium, whichaccelerated external borrowing. This brought about a generalized financialcrisis in 1982. Since its onset in August 1982, there has been a growingrecognition that a return to sustainable growth would require not onlystabilization policies, but also far reaching structural reforms on thesupply side of the economic structure. This perception gained ground afterthe 1982 stabilization program faltered in late 1985 (partly due toinsufficient focus on structural change) and became a central issuefollowing the collapse of international oil prices in early 1986. TheGovernment responded to the 1985/86 crisis by intensifying stabilizationmeasures and introducing significant structural changes focusing on tradeliberalization, encouraging private sector activity and reducing the roleof the public sector while increasing its efficiency. Implementation oftrade liberalization measures was accelerated in 1987.

2.02 The most fundamental policy reform in this economic program isthe shift from inward-oriented protected growth towards an

-3-

outward-oriented, open market development strategy, based on graduallydeclining protection and eliminating price controls to improve theefficiency and export competitiveness of the economy. Such a shift isparticularly significant to the steel sector in terms of the implicatinasof trade liberalization, the elimination of domestic price controls onsteel products and the role of external competition in bringing efficiencyand market response to the sector. The steel sector is part of theinfrastructure for downstream engineering industries with considerableexport potential, and as such its competitiveness in price, quality andservice will play a strategic role in the success of the newoutward-oriented development model.

2.03 A second fundamental structural change is the decision to clarifythe role of the public sector in the production side of the economy byimproving the performance and reducing the influence cf state-ownedenterprises and actively stimulating the private sector. Along tb'selines, the Government has intensified its efforts in divestiture, selling,merging, closing and/or transferring of several public sector firms, and inindustrial restructuring. In particular, in the steel sector there hasbeen substantial progress along these lines in 1986. SIDERMEX has shutdown one of its largest integrated plants. The company itself has beenreorganized with large numbers of its subsidiary companies 5ol4, liquidatedor transferred and further measures, of which this project i, an importantstep, are being planned. The end result of this process will be a smallerbut more efficient public sector, coupled with a growing private sectorplaced in a framework of healthy intervational competition.

B. The Steel Sector

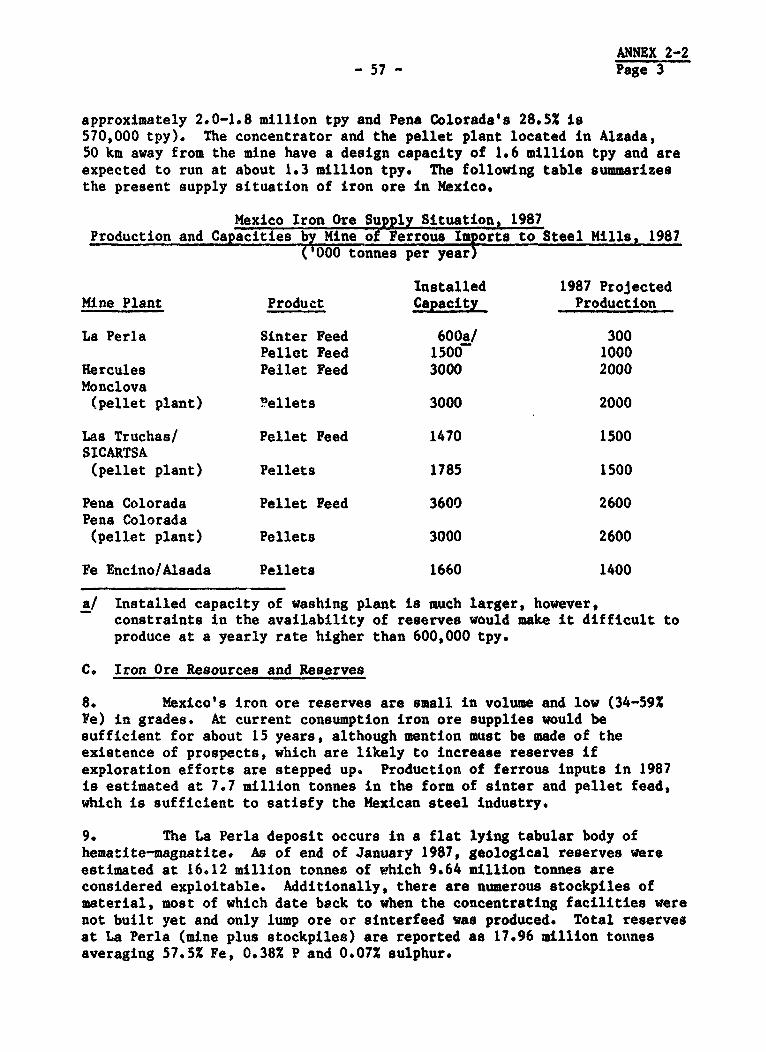

2.04 The Mexican steel industry is of substantial size with atheoretical installed capacity in 1987 of just over 9.0 mtpy of crudesteel. After relatively modest growt!s in the 1940s and 1950s, highlyprotectionist policies, heavy government investment and large budgetarytransfers and input subsidies allowed the industry to grow rapidly in the1960s and 19709, at 10.2X and 7.5% p.a., respectively, with productionbasically in balance with consumption. During the oil boom of 1976-81,demand for steel products grew substantially faster (14.9Z p.a.) thanproduction (9% p.a.) and imports increased from 0.3 to 2.5 mtpy in thatperiod. The economic crisis of 1982 severely hit the steel industry;domestic steel demand contracted by about 45X, imports by 86Z, and domesticproduction by 13X. The debt burden of the companies grew out of allproportion, and cash flow problems led to inadequate maintenance and abacklog in technological development. After 1983, there was some recovery,but neither consumption nor production reached the 1981 level (Annex 2-1).

2.05 At the end of 1986, the steel industry employment was nearly65,000 and the annual production was 7.2 million tonnes of ' ude steel and5.6 million tonnes of finished products. The production and consumption ofsteel products in the country was basically in balance. The overallproduction and consumption balance has changed from net imports ofUS$1,750 million in 1981 to an import/export balance at aboutUS$260 million of finished products in 1986 (Annex 2-1).

- 4-

C. Structure and Main Institutions

2.06 In its present structure, the industry comprises five integratedprodacers and 23. non-integrated mini-mills, and a number of Independentrerollers scattered throughout the country. There are effectively twomajor operating entities in the sector, SIDERMEX and HYLSA, which accountfor over 80% of the production, value added and employment. More detailsare in Annex 2-1. Map IBRD 20418 shows the main steel plant locations. Atpresent the Mexican steel industry receives practically all its rawmaterial supplies (iron ore, coking coal and flux) from internal sourceswith the exception of (i) steel scrap, a large part of which is imported,and (ii) occasional small quantities of coking coal or pellets forSICARTSAe Mexico's reserves of iron ore are low grade and relatively smallwhile proven coking coal reserves in the north are larger and richer (seeAnnex 2-2). Map IBRD 20419 shows the location of the main iron and coalmines in the country.

2.07 Several government agencies are involved in policy formulation,control and promotion of the steel industry in Mexico. The most importantis the Secretariat of Energy, Mines and Parastatal Industry (Secretaria deEnergia, Minas e Industria Paraestatal - SEMIP) which directly supervisesSIDERMEX in terms of both current operations and investment policies andprograms. SEMIP's influence extends beyond its public sector role.Although formal authority over industrial policies in general and steelsector policy in particular rests with the Secretariat of Commerce andIndustrial Development (Secretaria de Comercio y Fomento Industrial -SECOFI), the predominant position of SIDERMEX insures that, in practice,SIDERMEX and SEMIP exercise substantial influence on government policyformulation for the steel sector, including such matters as price controls,quotas and trade restrictions, tariff levels, subsidies and investmentplans and programs. Besides SEMIP and SECOFI, a third major player in theGovernment's policy-making role is the Secretariat of Planning andBudgeting (Secretaria de Programacion y Presupuesto - SPP); it coordinatesthe preparation of medium-term plans, approves the capital and annualoperating budgets of the parastatal steel companies, and monitors theirimplementation.

2.08 SIDERMEX was established in 1979, to manage the activity of thethree public steel companies: AHMSA, FMSA, SICARTSA and their 87subsidiaries in mining, downstream manufacturing, marketing anddistribution, and real estate. Although, SIDERMEX was initially successfulin coordinating the strategic activities of the public steel sector, it didso at the expense of excessive centralization of commercial, financial andoperational activities in the hands of a corporate management, leading toinefficient plant operation. The centralization of a large part of thedecision making authority also resulted in an isolation of the SIDERMEXplants from the needs of the ,arkets, The organizational and legalstructure were complicated. The large number o' subsidiaries with verywide ranging missions diluted the management effort.

2.09 The operating performance of the SIDERMEX steel companies variedsubstantial'y, reflecting the technology in place, the state of repair ofthe facilities and the stability and the competence of the plant management

- 5 -

concerned. The unfavorable economic environment in which these companiesoperated (low controlled output prices, depressed market, etc.) led to highoperational losses compounded by very high debt service obligations. By1986, SIDERMEX debt exceeded US$1.75 billion equivalent, of which roughlyUS$0.9 billion equivalent was foreign debt. A substantial portion of thisdebt represented the financing of non-performing assets, including over 50%in the SICARTSA II facility still under construction and awaiting furtherdecision on its target completion. The earning power of the remainingassets was considerably lower than their book values and considerablydiminished by the state of disrepair, the technical and organizationalinefficiencies, and the lack of coherent government policies towards thesector. By the end of 1985 it had become obvious that no seriousimprovement could be made in the performance of the public sector companieswithout deep changes in the organizational and financial structure ofSIDERMEX and in the economic environment surrounding the steel sector.Consequently, early in 1986, the GOM appointed a new management team andgave it the mandate to implement the major steps of a restructuring programaimed at restoring SIDERMEX efficiency and competitiveness and torestructure its organization, financial position, management andoperations. The restructuring program is discussed in Chapter IV.

2.10 HYLSA vas founded in 1942 as a tin reroller. In the 1950s HYLSAdeveloped the first industrial process for production of direct reduced(DR) sponge iron with operation starting in 1957. The company grewsteadily, through the 1950s and 1960s establishing a non-flat productfacility in 1969 and integrating it backwards through an improved DRprocess. Over the years, HYLSA remained the major cash earner for the AlfaIndustrial Conglomerate (Grupo Industrial Alfa - Alfa). In the 1970s, Alfaundertook a substantial diversification program financed in part throughthe HYLSA cash engine. The economic crises of the early 1980. left HYLSAand the parent Alfa saddled with an extraordinary debt burden. Thefinancial restructuring of the Alfa debt was completed in 1986 and a numberof activities are being spun off. HYLSA's debt burden reachedUS$1.15 billion equivalent at the end of 1986, about 25% of whichrepresented mounting payments arrears. The bulk of the debt is owed toforeign (mainly US) commercial banks. A financial restructuring packagehas been negotiated that allows for conversion of up to US$375 million ofHYLSA's debt into equity and provides for flexibility in repayment of theremaining debt through separation into mandatory and optional tranches,each bearing different rates of interest. The agreement also provides forHYLSA's implementing its capital expenditure program aimed at rest.Jring itscompetitiveness. Provision is also made for infusion of new debt insupport of the capital program. The restructuring package and relatedterms have been drawn up but remain to be cleared by all the institutionsinvolved. A final signed package is expected to be completed in mid-1988.The restructuring package provides an acceptable and reasonable basis forHYLSA to resolve its financial crisis and allow it to remain as a majorproducer in the Mexican steel sector.

2.11 The other entities in the sector, TAMSA and the semi-integratedproducers and rerollers, have been founded mainly in the past 20 years,with TAMSA being the oldest at over 35 years. Its activities, however,fall outside the direct ambit of the traditional steel product markets, its

- 6 -

main product - seamless pipes - being for use mainly in oil exploration.TAMSA's financial position has deteriorated in the past three years. Thecompany is burdened with over US$600 million equivalent in term debt, over60X of which is owed to foreign commercial banks. A substantial part ofthis debt was incurred in financing a major plant expansion in the early1980s based on optimistic views of the oil industry and consequent demandprojections for oil field products. Although TAMSA is seeking arestructuring agreement with its creditor banks its very specializedproduction profile serving a specific market (mainly PEMEX) would onlyconstitute a small part of the whole steel sector restructuring. Severalsmaller producers including those involved in stainless and specialtysteels are also facing financial structure problems. As a condition of theproposed project, NAPIN will make available funds from other sources,including existing Bank credit lines to all of these producers includingTAMSA for assistance in preparation of physical, organizational orfinancial restructuring studies.

2.12 All steel companies are grouped under a steel producers'association, the Camara Nacional de la Industria del Hierro y del Acero(CANACERO), which has mainly functioned as a spokesman for the industry, asa forum for exchange of basic market and technical information, and as alobby for favorable steel policies. CANACERO's influence on policy hasbeen minimal, however, reflecting the past divergence of opinions onfundamental policy issues such as price controls, tariff and quotaprotection, etc. between the private sector producers and the SIDERMEXgroup. Moreover, the protective environment of the 19609 and 19709 and thesubstantial market control and price levels of that era provided littleincentive to the steel industrv to develop an effective association. Therecent structural changes in the Mexican economy and the consequent adverseimpact on the steel sector have brought about a change in attitudes as welland CANACERO is now beginning to take a more active role in lobbying onbehalf of the industry's interests in a more unified manner.

D. The Policy Framework

2.13 The steel industry is an important part of Mexico's manufacturingsector and has significant impact on the availability, cost and quality ofmaterial inputs for downstream manufacturing, particularly, the engineeringand capital goods industries. Over the past two decades, the Governmenthas created and applied a policy framework intended to be favorable to thisindustry. This framework was successful in creating a steel industry ableto meet the steel demand of the country in quantitative terms, but one thatis now unable to satisfy the expectations of supplying low-cost andhigh-quality steel products to the market place. The highly protectionisttrade policies before 1985 (Annex 2-3) included:

(a) quantitative restrictions, that covered 100% of imports in 1982and 1983;

(b) high tariffs (up to 401 for steel products);

(c) unrealistically high official reference prices, that served asthe basis for calculating the amount of custom duties, resultingin a substantial increase of duties to be paid;

- 7 -

(d) domestic content requirements for capital goods and automotiveindustries; and

(e) public sector procurement practices which gave preference todomestic products over imports.

This trade regime had created an inward oriented industry that faced verylimited import competition making it difficult for the downstream users(especially for the export-oriented manufacturers of engineering products)to obtain high-quality, competitively priced steel products in neededspecifications, lot sizes and delivery schedules.

2.14 The key policy issue addressed in the restructuring project andthe proposed loan is the decontrol of steel prices which have been set inthe last two years below both the total cost of the efficient Mexicanproducers and below the actual landed cost of imports (not includingtariffs). As discussed in Annex 2-3, the price control deprives theproducers of the financial benefit of protection and does not provide anyincentive for improvement of product quality and service to customers. Inaddition, the low level of profitability and return on investmentdiscourages entry of new private investment capital into the sector. Inother words, the price control offsets the resource generating benefit ofthe protection while all the negative impact of the protection remains infull effect both for the steel industry and for the downstream users.

2.15 An important element of the Government's policy towards the steelindustry is its direct participation in the production activities.The public steel sector was created as a result oi the takeover of the thentwo largest private sector steel producers, AHMSA and PMSA, in order tosave them from bankruptcy and to avoid the layoff of thousands of workers.In the 1970s, the Government establinhed a new integrated steel works,SICART8A, partly to meet the fast growing domestic demand, partly topromote the development of the remote region of Lazaro Cardenas.Government policy regarding its direct investment in steel has changedsubstantially in the last two years. Action has been taken to streamlinethe public sector steel companies, to stop uneconomic activities and spinoff non-essential plants. After years of futile efforts to convert FMSAinto a healthy, profit-making company, the Government closed it in April1986. Further public investment plans have been reduced drastically and alarge number of SIDERMEX subsidiaries have been or will be transferred,sold or liquidated (Chapter IV).

2.16 Despite the increasing clarity on the public sector's investmentstrategy, Mexico lacks a global steel policy and long-term strategy,clearly defining the respective roles of the public and private sectors,and assuring the conformity between the development plans and the expectedneeds of the market. The present situation discourages major investmentsin the private sector and makes it very difficult to develop optimalinvestment programs in both the public and private sectors. The SteelSector Restructuring Project and proposed Bank loan will, among others,address this situation through the elabcration by GOM of a Global SteelSector Policy Statement based on the Policy Letter (Annex 4-2) that waspresented by GOM at negotiations.

-8-

III. THE STRATEGIC ISSUES AND BASES FOR SECTOR REFORM

A. Strengths and Weaknesses

3.01 A detailed analysis of the Mexican steel industry's currentoperating performance, cost and quality competitiveness, and its strengthsand weaknesses was carried out under the sector strategy study completed in1986. The main findings and conclusions of that analysis are presented inAnnex 3-1. The technical comparisons of the major steel plant operationsin the country lead to the following main conclusions:

(a) non-flat products are by and large produced in modern facilitiesin both the private and public sector and are quality and costcompetitive with international norms; the sole exception isAHNSA's outdated facility; the strategic implications arediscussed in para 3.07 and 3.08 below;

(b) the industry's main weakness lies in the quality and cost of itsflat product lines at both AHMSA and HYLSA; modernization ofthese facilities would enable both producers to substantiallyimprove their competitiveness and strategic position.

3.02 The mining operations are analyzed in Annex 2-2 and Annex 3-2.The main conclusion from this analysis are:

(a) coking coal and iron ore production in Mexico appear competitivefrom economic and financial points of view, and can be expectedto maintain this position if no major shifts in relative costs(labor, energy, transport) occur;

(b) coking coal production shows substantial potential for furthercost and quality improvements as older mines are closed and newmines are opened with concomitant changes in mining techniquesand higher productivity;

(c) iron ore is generally of lower grade but even with higherprocessing costs is competitive as inputs to the steel industryon both an economic and financial basis; and

(d) there is small room for improvement in two of the iron minesbecause they are nearing depletion; the remaining three ironmines and the coal mines could show improved cost performancethrough increased capacity utilization rates.*

3.03 The marketing and distribution practices and infrastructure havebeen deficient, particularly those of SIDERMEX. Past protectionistpolicies held back the development of an efficient and competitivedistribution network. This deficiency has particularly affected thesmaller companies in the engineering industries and capital goods, whichhave suffered from inadequate and unpredictable supply of steel products.

-9-

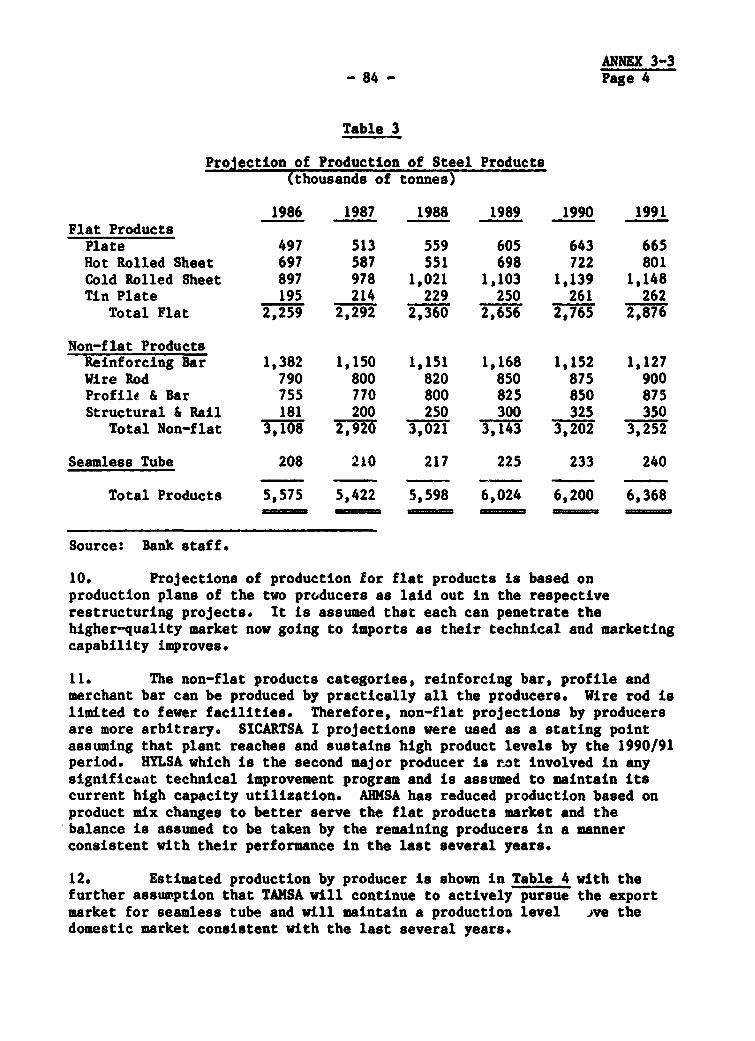

B. The Strategic Issues

3.04 An analysis of the present and potential steel market demand andsupply in Mexico is presented as Annex 3-3. Domestic producers arepresently unable to supply high-quality steels to the domestic market,particularly for the rapidly growing capital goods and manufactured metalproducts subsectors. Mexican producers in these subsectors have potentialcomparative advantages in three significant areas, viz., labor cost,proximity to substantial riarkets, and indigenous resources. Recentgovernment policy changes have added an additional factor that has spurredrapid growth and an export-oriented internationally competitive approach.As a result, this segment of t.he steel market is the most demanding interms of the quality dimension and cost competitiveness. The ability ofthe steel industry, and particularly the flat product producers, to adaptto the changing needs of this segment of the steel market is a key factorin Its future growth.

3.05 The bases for projecting steel demand are an assumption of amodest rate of growth of 3-4% p.a. of GDP in the next five years and afurther opening of the Mexican economy which is expected to lead to afaster-than-average growth of the manufacturing industry. This is expectedto result in an average growth in demand through 1991 of about 4.4% p.a.from the 1986 level for flat products, 3.2% p.a. for non-flats and 3.5%p.a. for seamless tubes, or 3.8% p.a. for all products.

3.06 Although overall demand growth is projected to be slow, there aremajor opportunities for the Mexican steel industry in diversification ofthe product mix and improvement of product quality to capture a greatershare of the specialized market segments that show higher than averagegrowth potential. The strategic analysis described in Annex 3-1 indicatesthat from a wide range of flat and non-flat products, Mexican producershave considerable potential for improvement of their competitiveness tocover not only their short-run marginal cost, but their long-run economiccosts as well (see paras 8.08-8.10). The restructuring Fcogram in theshort run and the proposed project are designed to tap thts potential whichwould benefit both the steel industry and its downstream tiers particularlyin the capital goods and manufactured metal products subsectors.

3.07 The main conclusions from an assessment of the industry'sstrategic position in relation to the potential market demand and takinginto account the industry's cost and quality factors are that the steelindustry is well placed in the non-flat product area. The opportunity thatneeds to be tapped is the demand for high-quality bar products that couldbe produced in SICARTSA's modern facilities and the shift of thesefacilities from export to domestic production. However, the AHMSA non-flatproduct lines are clearly in a weak strategic position with respect to costand quality. Abandonment of these lines could provide the private sectorproducers with the opportunity to expand production, provided the pricingincentives are in place. Structural profiles are an exception to thisgeneral thrust. Further analysis shows that AHMSA should continue toproduce structural steel profiles (wide flanges, beams, etc.) as well asmodify its structurals mill to produce rails for the domestic market (seealso para 8.09).

- 10 -

3.08 The strategic thrust that can be derived from the analysis isthat, in the short and medium term, Mexico should (i) concentrate onimproving the quality and cost factors in the flat product lines; and(ii) focus its most modern non-flat facilities on the internal markets toservice a demand for higher-quality products. With regard to raw materialresources, a crucial issue is whether available iron ore reserves and thecapacity of existing mines and new projects will be able to satisfy futuredemand of the steel industry. As a general conclusion, local supplysources, based on current reserve estimates would be sufficient to meetiron ore demand fully in the short and medium term, and coking coal demandin the longer term, well into the next century. Periodic reassessments ofthese global forecasts will obviously have to be made in the light of newexploration results.

C. Agenda for Policy Reform

3.09 The strategic development issues facing the Mexican steelindustry also have a major impact on future trade liberalization. Thepolicy reform proposals which underlie the comprehensive program ofrestructuring are aimed at creating the framework under which the steelindustry can achieve greater competitiveness in the coming years andthereby open the way for liberalization measures affecting downstreamindustries. Annex 2-3 presents an analysis of the main policy reformproposals.

3.10 Given that the program of trade liberalization and tariffreduction has already been agreed, the most critical element in theshort-term agenda for policy reform is the elimination of domestic pricecontrols. As discussed in greater detail in Annex 2-3, this will permitthe rise of domestic steel prices to their opportunity cost levels andeventually, as quality improves with the project, to the level of CIF plustariff. This measure would also allow the steel producers to obtain thefinancial benefits of the announced tariff policy and, thereby, generatethe funds necessary for adequate maintenance of facilities, upgrading oftechnology and servicing of the debt. It would also allow the Governmentto eliminate budgetary transfers averaging about US$75-100 million a yearto cover both operational losses and to support capital expenditures in thepublic sector and indirect subsidies to the industry as a whole. It wouldattract needed new investment capital to the steel sector, and will lead toefficient import competition forcing domestic producers to improve qualityand product mix and to serve better their customers. This willsubstantially improve the supply of steel products in the domestic marketas producers become more specialized and more competitive. These measureswould further facilitate movement towards liberalizing domestic contentrequirements in downstream manufacturing industries, such as auto parts,for which a broader approach is foreseen. The proposed policy reforms inthe steel sector are vital in ensuring greater competitiveness in both costand quality terms.

3.11 The steel sector report prepared by the Bank recommended that aglobal steel sector policy be elaborated by Government with activeparticipation of the private sector. This policy should include a clearstatement of Government's intent in order to encourage private sectorinvestments and permit it to seek its market niches and exploit its

- 11 -

comparative advantages in an effective manner. The first practical step inthis direction has been the completion of a comprehensive, in-depth marketstudy which serves as a basis for the medium and long-term strategy. Themain objective of the study was to review the structural changes occurringin the demand for steel products, identify the market niches that presentthe greatest opportunities for domestic steel producers, and assess thebasis for longer-term market growth, so that appropriate supply strategiescan be defined and implemented. Consultants were appointed under the aegisof CANACERO and the study was completed in October 1987. This studyprovides the input for the strategic planning study that has beenundertaken by SIDERMEX and for other less formal studies by the privatesector producers. The Government has agreed to elaborate the Global SteelSector Policy Statement by July 31, 1988, i.e., after the presentation ofthe SIDERMEX Long-range Strategic Plan (para 4.10). The Government'sPolicy Letter, providing the outline for the Steel Sector Reform Program,is discussed in para 4.02.

3.12 While no specific annual targets are included in the policyreform program concerning budgetary transfers and subsidies, theGovernment's clear intentions, as articulated in the SIDERMEX convenio andconfirmed in the Policy Letter (para 4.02), are to reduce and eliminatedirect and indirect subsidies and transfers to the public sectorcompanies. With the expected implementation of the recommended policychanges, the steel industry will be able to operate, modernize and evenmodestly expand on the basis of its sales revenues. The total eliminationof direct subsidies and government transfers to the steel industry is alsoexpected to occur in a relatively short time.

IV. THE RESTRUCTURING PROGRAM

A. Objectives

4.01 The Steel Sector Restructuring Program involving public andprivate sector producers is an important element in Mexico's generaladjustment process. Reflecting the strategic thrust described inpara 3.08, major objectives of the program are to maintain, enhance andrestore the sector's competitiveness and restructure its technical,financial and organizational characteristics:

(a) On the policy side by:

(i) eliminating domestic price controls, reducing and makinguniform tariffs on steel products and eliminating officialreference prices in line with the agreed calendar of tradepolicy reforms, so as to assure competitiveness in themarketplace; and

(ii) reducing and eventually eliminating government subsidies toproducers.

(b) On the technical side by:

(i) closing down uneconomic operations, reducing or eliminatingproduction inefficiencies, and optimizinag existing and

- 12 -

planned new facilities in terms of the product mix andmarkets served;

(ii) carrying out economically justified immediate and urgentinvestments in catch-up maintenance, debottlenecking ofexisting productive facilities, quality control andproductivity improvements; and

(iii) undertaking the market and technical studies needed to planfor the longer-term investment needs of the sector.

(c) On the organizational side by: improving the management andorganization of SIDERMEX by decentralizing the decision-makingprocess and devolving operating responsibilities to the steel,mining and other operating units, placing particular emphasis ontheir market responsiveness.

(d) On the financial side by: improving the financial condition ofSIDERMEX, the major private sector producers, HYLSA and TAMSA,and other semi-interrelated producers by undertaking neededfinancial restructuring and financial engineering of theirbalance sheets.

B. Global Policy Actions

4.02 Following discussions on the underlying trade and price controlpolicy framework, a number of actions have been taken as part of theGovernment's trade liberalization program, supported by the Bank's First(TPL I, Loan No. 2745-ME) and Second (TPL II, Loan No. 2882-ME) TradePolicy Loans. Import tariffs for finished non-flat steel products werereduced in 1986 from 40% to 37%, and on most flat products were reducedfrom 25% to 20%. Recently, tariffs on all steel products were reduced to0% to 15%. All quantitative restrictions for import of steel products wereeliminated. The Government's policy actions are included in the PolicyMatrix (Annex 4-1) and in the Policy Letter providing an outline ofGovernment intentions with respect to the steel sector (Annex 4-2). Theseaction measures and policy intentions constitute the Steel Sector ReformProgram, summarized as follows:

(a) The Government plans to open the steel market in Mexico tointernational competition so that the manufacturing sector willbenefit from high-quality, low-cost input materials. Changesinclude the elimination of quantitative restrictions and officialreference prices for imported steel products. In December 1987tariffs were reduced to 0% to 15%.

(b) Steel price controls will be totally eliminated not later thanDecember 31, 1988. Prior to this event, the Government willcontinue to adjust the domestic prices of all steel productsmonthly based on the anticipated changes in the Consumer PriceIndex in order to dampen any possible sharp increases andfluctuations that might occur after complete price decontrol.The price increases accorded in December 1987 and January 1988have already brought all domestic product prices to or aboveequivalent international landed price levels and continuedadjustments will maintain the domestic price levels in realterms.

- 13 -

(c) Through these policy changes the Government seeks to provide astable long-run framework of trade and domestic industrialpolicies that in the new open market environment will provide thenecessary incentives for efficient production of quality productsand the conditions necessary for proper long-term planning. Itis the Government's intention to maintain these policies in orderto ensure the development of an internationally competitive steelindustry able to operate without further protection.

(d) The Government has taken significant restructuring steps with itsparastatal steel company, SIDERMEX, including (i) thhe closing ofthe inefficient steel plant, Fundidora de Monterrey ;.A.;(ii) the financial and organizational restructuring cf SIDERMEX;and (iii) the closure, spin-off, reduction and consolidation ofits subsidiary companies. The Government plans to continue thetransformation of SIDERMEX into an effective holding company thatperforms strategic management and general supervisory functionsover the entire parastatal steel sector.

(e) By March 31, 1988, SIDERMEX will publish a Long-term StrategicPlan which will include details of the remaining restructuringwork and the investment program supported by the proposed Bankloan. This plan will elaborate further on the issues regardingmanagement and organization as well as details pertaining tofacilities to be operated and products to be produced in the nextfive years. Government investment will be limited to furtherbalancing and technical upgrading of existing facilities and tocompletion of existing projects that are shown to be economicallyand financially viable.

(f) In the long term the Government plans to eliminate all budgetarytransfers to SIDERMEX. After the publication of the SIDERMEXStrategic Plan, Government will further elaborate and publish aGlobal Steel Sector Policy Statement, not later than July 31,1988, substantially along the lines indicated in the PolicyLetter. tn particular, the Global Policy will be consistent withboth the guiding principles of the SIDERMEX Strategic Plan andwith the Plan itself. These actions will clearly define thescope and extent of the public sector's investment and operatingstrategies and investment plans, and will, thereby, allow theprivate sector to plan its own operations and investments. TheGovernment's goal is to continue the transformation of the sectorinto a group of solvent and viable companies with well-maintainedfacilities, producing internationally competitive products tobetter serve the country's downstream users including the growingexport-oriented manufacturing industries.

As they are vital to the short- and long-term success of therestructuring effort, and to the viability of the physicalinvestments to be implemented under this project, the continuedmaintenance of the price decontrol and trade liberalizationmeasures is a covenant of the entire proposed loan.

- 14 -

C. SIDERMEX

Overall Restructuring Thrust

4.03 Significant progress has been made by the Government with regardto the restructuring of SIDERMEX operations and following actions have beentaken:

(a) The country's least viable and most loss-ridden steel plant, FMSAat Monterrey was closed in May 1986;

(b) The Government and SIDERMEX worked out a comprehensiverestructuring program of the public steel sector and inSeptember 1986, signed an agreement (Convenio), which providedfor major financial restructuring of SIDERMEX companies (AHMSAand SICARTSA), defined the overall program of physical plantrestructuring and organizational changes to be carried out withGovernment assistance, and specified SIDERMEX obligations interms of performance improvements, productivity targets andprofitability goals.

(c) The corporate structure of SIDERMEX was rationalized, withdevolution of responsibility for all operating, marketing andfinancial activities from corporate level to the plant operatinglevels. The number of corporate employees was reduced from 1,070to approximately 800 with further reductions contemplated.

(d) A large part of SEMIP's decision making authority was delegatedto SIDERMEX corporate management; and

(e) The process of rationalization of the size and profile ofSIDERMEX has been initiated. Ten of the former SIDERMEXsubsidiaries have been transferred under direct control ofSEMIP. A process of sale of 22, liquidation of 20, andconsolidation of the remaining companies into 24 units has seenstarted, and substantially completed (see para 4.06).

4.04 The SIDERMEX Restructuring Program incorporated in the Convenioaddresses the most urgent aspects of operational changes needed to restoreSIDERMEX's competitive position, including the rehabilitation of existingfacilities and undertaking the organizational and financial changes toaccomplish the basic objectives. The Convenio provided that SIDERMEX wouldlaunch these actions as a medium-term program, while studying a longer-termstrategic plan to be decided upon and implemented as soon as the requisitefinancing plan and detailed investigations were ready. The proposedproject addresses the implementation of the medium-term restructuring.

Organizational Changes

4.05 At the beginning of 1986, SIDERMEX consisted of 3 integratedsteel plants and 87 subsidiaries. Most of the subsidiaries were engaged inactivities not closely related to the steelmaking and marketing process.The decision of the Government was to keep in the SIDERMEX group the largeintegrated steel producers, the coal and ore mines, some of the marketing

- 15 -

network, ferro alloy producers, and the production of refractorymaterials. The rest will be divested from the SIDERMEX portfolio. At theend of the reorganization process, SIDERMEX will have 2 integrated steelplants, a raw materials operating group and 24 related subsidiaries mainlyin mining of iron ore and coal, and production of refractories.

4.06 A major change that is an integral part of the current phase ofSIDERMEX restructuring is the shut down of its most problematic plant, FMSAat Monterrey. This was a painful decision, since it liquidated nearly9,000 direct jobs and many thousa;ds of indirect jobs. Associated mineshave since then also been shut down affecting some 2,000 workers in smallcommunit.es. SIDS-RMEX and the Government have examined the socialimplications of these changes and after discussions with the trade unions,have agreed on compensation measures. After the signing of the Convenio in1986, the restructuring process continued with ten of the former SIDERMEXsubsidiaries transferred under direct control of SEMIP and 42 companiesbeing sold to the private sector or liquidated. The remaining 35subsidiaries are being consolidated into 24 units. Furthermore, the miningsubsidiaries are being grouped into a single holding company, CMC, with itsfinancial structure being rationalized through a recapitalization programaimed at eliminating inter-company debts, and allowing for transparency inthe transfer pricing sales between the mining group and the steel plants(see para 7.07).

4.07 The Convenio will transform SIDERMEX into a holding company thatperforms strategic management and general supervisory functions over theparastatal steel sector. The responsibility and autonomy of the plantmanagement will be substantially increased. The marketing and productionplanning activity has already been transferred from the SIDERMEX corporatemanagement to the plants. The new organization, which is already in placeadministratively, will -Je legally formalized in 1988 not later than 90 daysafter loan signature (para 5.14). It will group all operations under fiveindependent operational entities: AEMSA, SICARTSA, the raw materialsdivision under the corporate name Carbon y Minerales Coahuila S.A. (CMC),Refractories and related operations, and international marketing and othernon-technical units. This reorganization will considerably improve themanagement of both the steel producing and non-steel related companies.

Financial Restructuring

4.08 In the framework of the Convenio, the Government assumed andconverted to equity about US$883 million equivalent or 50% of theUS$1.75 billion equivalent total debt of the SIDERMEX companies. AnotherUS$250 million of FMSA debt will be dealt with in the bankruptcy process ofthat enterprise. The conversion of debt includes essentially all capitalrepayment falling due in 1986, 1987 and M9A8 and the interest payable fromFebruary to September 1986. This operation makes the debt more realisticand manageable, but does not offer a final solution of the problem,especially if account is taken of the growth of debt expected in relationwith the possible continuation of the SICARTSA II investment.Decontrolling prices would permit the companies to generate a large portionof the funds needed to service the debt, but probably further financialrestructuring measures will be needed in the future, including a possiblewrite-down of some remaining SIDEIMEX assets which consultants will reviewunder the project (para 4.12).

- 16 -

Technical Restructuring

4.09 Key weaknesses in the mines and steel plants are due toinsufficient funds in recent years allocated for maintenance and facilityupgrading that have resulted in higher operating costs and lower productquality. In addition, technical improvements, particularly in automationand systems development, have not been carried out even in the more modernfacilities. The sector strategy review and the competitiveness analysescarried out earlier have identified that the product mix of the plants donot fully correspond to (i) the requirements of the market, (ii) thetechnical conditions of the plants, and (iii) the possibilities ofspecialization between the large public and private producers. There isgeneral technical agreement between SIDERMEX and the Bank that certainspecialization should be developed among the public and private sectorplants, e.g., flat products at AHMSA and HYLSA and non-flat products atSICARTSA I and in the private sector. Taking into account this strategicthrust and existing technical weaknesses, SIDERMEX has developed theshort-term investment program with the assistance of US Steel EngineeringConsultants (para 5.11) that is the basis for the project componentsdescribed in Chapter V.

Long7term Action

4.10 By the end of the proposed project, SIDERMEX is expected to be agroup of solvent and viable companies with well maintained facilities,producing internationally competitive quality products at lower cost thannow and with an adequate product mix to better serve the downstreamsteel-consuming industries. However, this immediate phase of therestructuring process does not include all the potentially neededmodernization, balancing or the completion of the investments in progress.SIDERMEX is therefore carrying out a long-term strategy study to define thebasis for its development through the 1990s. The Strategic Plan will beconsistent with the guiding principles spelt out in the Policy Letter(para 4.02(e) and (f)). Terms of reference for this work were reviewed andagreed by the Bank. British Steel Corporation Overseas Services (BSCOS)was selected and has carried out the task. SIDERMEX will present itslong-term strategy proposal for Bank review by March 31, 1988. The marketstudy (para 3.11) has also provided a major planning input to th2e strategystudy. The strategy developed for SIDERMEX will provide the basis for theGovernment's Global Steel Policy statement which will define the role ofthe public sector and along with the results of the market study theopportunities available for the private sector.

4.11 The integration of the proposed SICARTSA II investment programinto the SIDERMEX complex is a critical element in the long-term strategy.The completion of this investment parallel with further facilitiesrestructuring in the AHMSA plant may lead to excess capacities,particularly in plate production. Therefore, disetssion with SIDERMEX andthe Government has led to an understanding that alternatives to completionof SICARTSA II would be evaluated on their technical, economic andfinancial merits once the medium-term product and market studies arecompleted. Such an evaluation would be completed as part of thepresentation of the SIDERMEX Long-term Strategic Plan and will include:

- 17 -

(a) review and discussion with the Bank of the conclusions andrecommendations of its long-term strategy study in particular, those withrespect to major investments in facilities not included in the now agreedRestructuring Program and use of facilities not now in operation;(b) implementation of the agreed elements of the long-term strategy inaccordance with investment criteria, financing plans and implementationschedules that are acceptable to the Bank; and (c) annual review of theplani and progress achieved.

4.12 In reviewing the SIDERMEX financial restructuring alreadyeffected by the Government, and in particular, the financial pi. pects forits steel companies, it has became apparent that there is a need forfurther balance sheet restructuring, including revaluation of the fixedasset base in relation to the earnings potential and a correspondingwritedown of the equity base, so that future SIDERMEX financial performanceis measured against achievable financial return criteria and reflects theoverall cost of equity and loan capital. It has been agreed that withinsix months after the signing of the loan documents SIDERMEX will carry out,based on agreed Terms of Reference: (i) a complete analysis andrevaluation of its fixed assets, including fixed assets of all of itssubsidiaries, and (ii) an adjustment and updating of the relevant balancesheets based on these results.

D. Private Sector

4.13 The most important elements of the restructuring needs of theprivate sactor pertain to the current financial situation at HYLSA andTAMSA, the two integrated producers. Other private sector producers, ingeneral, appear to be in relatively satisfactory financial condition,although profit margins have eroded in recent years and iivestment risksincreased. The policy reform package described in para 4.02, by and large,would be sufficient of itself to strengthen the financial position of thesmaller, non-integrated steel producers and to provide the right signals tothem to reinvest in the potentially profitable market niches, and toattract new entrants to the industry. The case of HYLSA and TAMSA is,however, more problematic. Financial restructuring is a necessarycondition for their survival as viable and dynamic entities.

4.14 As described in para 2.10, HYLSA owes about US$1.2 billion and inthe present economic environment is not capable of generating sufficientfunds on the existing facilities to fully service this debt. The companyhas recently completed negotiations on the restructuring of its debt withthe advisory committee of the creditor banks. Since HYLSA, like theSIDERMEX companies, did not have sufficient funds in recent years for /maintenance and upgrading of its facilities, it badly needs to carry out amajor rehabilitation and modernization program. The program has beendefined by HYLSA with consultant assistance (see para 5.12) and forms thebasis for the proposed project component. The implementation of thisprogram is essential for HYLSA to maintain its competitive edge and retainits market share in a period when its main coLpetitor, SIDERMEX, iscarrying out a significant improvement program. As discussed in para 2.10,the restructuring agreement with the banks would allow it to retainsufficient financial capacity for the implementation of the minimuminvest:ment program. The financial assessment of the HYLSA rehabilitation

- 18 -

component of the project reflects the preliminary agreements reachedbetween HYLSA and the creditor banks (para 7.08). Signature of the finalagreements with terms acceptable to the Bank is an agreed disbursementcondition for the HYLSA component of the proposed loan (para 6.06).

4.15 Based on the analysis, it appears that, taking into account theterms of the financing restructuring plan, the major capital investmentneeds, and HYLSA's working capital requirements for ongoing operations,HYLSA would not appear capable of carrying out a successful rehabilitationand modernization program without financial assistance under the proposedproject. Moreover, the financial restructuring package would permit HYLSAto obtain additional substantial write-down of the debt burden if part ofthe annual free-cash flow in the early years were to be used to retiredebt. To the extent that HYLSA is able to finance at least a part of itsinvestment needs from new external sources, the restructuring of HYLSA'sbalance sheet could be accelerated, resulting in a sounder capitalstructure. This would also allow HYLSA to remain a stronger competitor tothe public sector in the domestic market.

4.16 Coupled with the financial restructuring needs (para 2.11), sometechnical restructuring involving new technology and upgrading of existingfacilities of smaller producers in the private sector, particularly thespecialty-steels producers, have been identified by the Government.Although these requirements are not specifically funded under the presentproject, NAFIN has agreed that technical assistance for these purposes willbe provided from other funding sources, including existing Bank creditlines, already available to it. Funding for subsequent investment andworking capital needs would also be channeled through existing creditlines, including existing Bank loans, with additional funds possiblyincluded in a proposed Industrial Restru^turing loan.

V. THE PROJECT

A. Objectives

5.01 The project is based on the strategic analysis discussed inChapter III and supports the policy reform measures discussed inChapter IV. Its first objective is to assist the Mexican Government inimplementing a comprehensive and far-reaching reform of the steel sectorand in carrying out the needed restructuring actions. Its second objectiveis to assist the major players to rehabilitate potentially efficient plantand equipment with demonstrable viability, enhance product quality andreduce product costs, eliminate bottlenecks to achieve better utilizationof existing capacity, improve technical, financial and managerial controlsand information systems, train operations and maintenance staff and developthe human resources to achieve the overall objectives of greatercompetitiveness and responsiveness to market needs. Its final objective isto assist the Government and the industry in elaborating their long-termstrategies and policies to achieve a healthier development of the steelsector in line with the country's development objectives. The projectspecifically avoids investments in product lines and facilities whoseviability is dependent on the outcome of the ongoing market study and theSIDERMEX long-term strategy study.

- 19 -

B. Project Description

5.02 The proposed project consists of three parts: Part A is an InputMaterials and Steel Products Import component tied to implementation ofagreed policy reforms; Part B addresses the restructuring needs of SIDERMEXand its operating entities; and Part C supports the rehabilitation andmodernization of the HYLSA flat product facilities as part of itsrestructuring program.

Part A: Input Materials and Steel Products Import Component

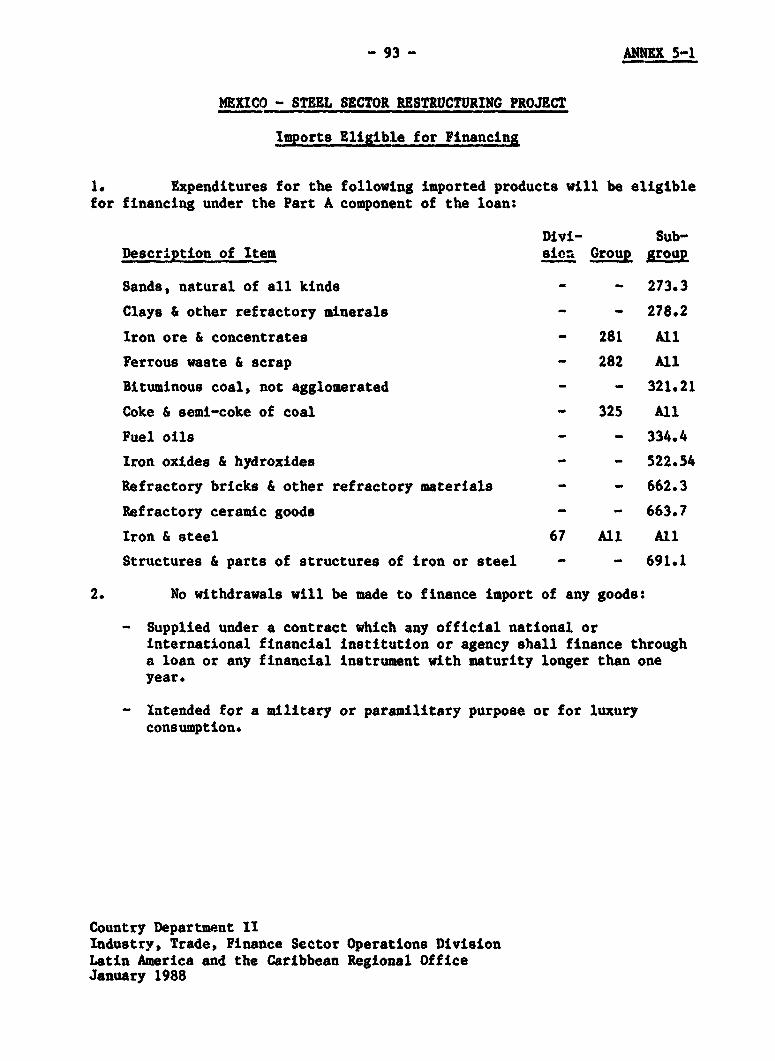

5.03 This component is intended to support the Steel Sector ReformProgram of the Government described in paras 2.13-2.16 and 4.02. Thisprogram is in the process of execution having been launched by theGovernment in early 1986 with important components already implemented.Finalization and implementation of major components, including theelimination of domestic price controls, are under way. The policy reformwill substantially alter the manner in which the steel industry conductsits business and develops in the coming years. It is expected that thefurther deepening of the reform process will result in increased steelimports during the adjustment period when the industry will be carrying outits restructuring and rehabilitation. Accordingly, this component willsupport both the consolidation of the already adopted measures and theintroduction of new ones, and would finance a part of the increased importsduring the adjustment period.

5.04 The Government has already carried out twio of the triggeringevents, i.e., elimination of ORPs for all steel products, one of the eventsfor release of Tranche I, and reduction and equalization of tariffs onsteel products to no more than 25%, one of the events for release ofTranche II. In addition, the price adjustment in mid January 1988 and thepresentation of the Policy Letter at negotiations complete all actionsrequired for release of the first tranche at loan effectiventss. Thesecond tranche release will be triggered by final decontrol of all steelproduct prices, and the final elaboration of a Global Steel PolicyStatement by the Government. The two tranches will be in equal amounts(see para 6.12) and will be used to finance eligible imports as set out inAnnex 5-1.

Part B: SIDERMEX Restructuring Program

5.05 The SIDERMEX program includes: investments in the major flatproduct facility, AHMSA, aimed at improving the quality and competitivenessof its hot and cold rolling lines and improving the utilization of itsheavy section mill through the addition of equipment for the production ofrail; investments in the raw materials division, CMC, to ensure adequatecoal and iron ore supplies for the steel plants; and assistance to SIDERMEXin strategic planning and other studies.

5.06 The AHMSA component is detailed in Annex 5-2 and concentrates onshifting the product mix to flat products, heavy structurals and rails withan overall reduction in steelmaking capacity and improvements in qualityand lowering of costs of production, primarily in hot and cold rolled sheetand tin plate. The major technical thrust is to (i) rationalize thesteelmaking and continuous casting facilities; (ii) rehabilitate and

- 20 -

improve the quality and productivity of the hot strip mill; (iii) balancethe cold rolling mills and improve the quality of cold rolled products;(iv) provide catch-up maintenance throughout plant operations and in theplant-wide utilities and services; (v) expand the product line by using theunderutilized heavy structural mill for the production of rail; and(vi) provide for enhancement of systems and training. The investmentsinclude, equipment for improvement of the steel-making facilities, the hotand cold rolling mills, rail section mill and plant-wide maintenancesincluding utilities and services, as well as services of consultants forenhancement of management information systems, engineering and projectmanage.ent and development of training programs and expenditures foroverseas training of operating personnel. About 900 man-months ofconsultant services are included.

5.07 The CMC component is detailed in Annex 5-3 and is concentrated onraising productivity in the coal mining operations and strengthening theHercules iron ore operation, bringing it to its intended level ofoperation, through a mixture of maintenance and equipment renewal,debottlenecking investments, systems and controls and technical assistancefor project management, operational improvements and upgrading of technicalskills. The proposed investments include replacement of mining, transportand conveyor equipment, purchase of new coal crushers, installation of aniron ore concentrator facility and consultant services (250 man-months) forimplementation of accounting and management information systems, ana forproject management and training.

5.08 Strategic planning studies for SIDERMEX are detailed inAnnex 5-4. The main objectives of these studies are to assist SIDERMEXmanagement in: (i) carrying out a long-term strategic study including thenecessary supporting technical studies; (ii) undertaking the corporate-wideasset revaluation exercise and translating the results into a suitablefinancial structure; (iii) implementing the organizational and financingrestructuring measures that emerge after the completio: of the long-termstrategic studies; (iv) assisting in the detailed planning of the long-termstrategic investments; and (v) providing assistance fo: implementation ofcorporate level management information systems. To these ends, thiscomponent would include consultant services of about 445 man-months.

Part C: HYLSA Restructuring Program