A Study of the Relationship Between Spot Product … Study of the Relationship Between Spot Product...

106

OXFORD Ns-nrn ENERGY STUDIES = FOR- A Study of the Relationship Between Spot Product Prices and Spot Crude Prices Robert Bacon Oxford Institute for Energy Studies WPM 5 1984

-

Upload

vuongthuan -

Category

Documents

-

view

222 -

download

1

Transcript of A Study of the Relationship Between Spot Product … Study of the Relationship Between Spot Product...

OXFORD Ns-nrn E N E R G Y STUDIES

= FOR-

A Study of the Relationship Between Spot Product

Prices and Spot Crude Prices

Robert Bacon

Oxford Institute for Energy Studies

WPM 5

1984

The c o n t e n t s o f t h i s paper a r e f o r t h e purposes of s t u d y and d i s c u s s i o n and d o not represent the v iews of the Oxford I n s t i t u t e for Energy Studies or any of its members.

Copyright 0 1984 Oxford I n s t i t u t e for Energy S t u d i e s

ISBN 0 948061 05 7

TABLES

Table I R e l a t i o n s h i p s Between Spot P r i c e Measures f o r Arab Light

I1 R e l a t i o n s h i p s Between Spot P r i c e Measures f o r Nigerian Light

111 Months wi th Extreme Disagreements Between S e r i e s

I V R e l a t i o n s h i p s Between Netbacks f o r Arab Light

V R e l a t i o n s h i p s Between Netbacks f o r N i g e r i a n L i g h t

V I C o r r e l a t i o n s f o r Saudi Netbacks (1981.01-1983.06)

V I 1 C o r r e l a t i o n s f o r Nigerian Netbacks (1981.01-1983.06)

V I 1 1 The Normal Margin Model (1976 .01-1983.06)

IX Estimated Normal Margins f o r Various Sub-Per iods

X Estimated Normal Margins a t D i f f e r e n t Refinery Centres

XI Regression of Arab Light Margin on Nigerian Light Margin

XI1 R e l a t i o n s Between Netbacks and Spot Crude P r i c e s for Arab Light

XI11 R e l a t i o n s Between Netbacks and Spot P r i c e s f o r Nigeria

XIV The Impact of Spot and O f f i c i a l P r i c e s o n Metbacks for Arab Light

XV The Impact of Spot and O f f i c i a l P r i c e s on t h e Netback f o r Nigerian Light

27

27

28

34

35

36

36

41

45

48

49

78

80

82

83

TABLE OF CORTEldS

B . l

B.2

B.2.1

B.2.2

8.3

B.3.1

B . 3 . 2

B.4

B.5

B . 5 . 1

B.5.2

B.5.3

B . 5 . 4

INTRODUCTION

PART A: PRINCIPAL FINDINGS OF THE STUDY

PART B: DETAILED ANALYSIS

The R e l a t i o n Between Spot Crude P r i c e s and Spo t Product Values

The Data

Spot Crude P r i c e s

Netback Data

A Simple Model R e l a t i n g Spot Product Values and Spot Crude Prices

The Model

The Goodness of F i t of t h e Normal Margin Model

Economic F a c t o r s Determining t h e Netback t o Crude Margin

Further S t a t i s t i c a l Tests on t h e R e l a t i o n s h i p s Between Product and Crude P r i c e s

An Unconstrained Re la t ionsh ip

O f f i c i a l P r i c e s as Explanatory Var i ab le s

Dynamic Equation6

V a r i a t i o n s B e tween Ref i n e r ies

DATA APPENDIX: KEY TO ABBREVIATIONS

1 7

23

30

3 7

40

51

76

81

85

90

94

NOTES 96

XVI Lags Between Spot Prices and Netbacks of Arab Light

XVII Lags Between Spot Prices and Netbacks for Nigerian Light

XVIII Relat ion Between Netback and Spot Price for Various R e f iner ies fo r Arab Light f o r the Third Episode

X I X Relat ion Between Netback and Spot and O f f i c i a l Prices f o r Arab Light for Various Ref iner ies for the Fourth Episode.

86

87

92

92

I ATBODU CT I OH

T h i s p a p e r i s an i n v e s t i g a t i o n i n t o t h e r e l a t i o n

between crude o i l p r i c e s and t h e p r i c e s of the products made from

r e f i n i n g crude o i l . Commentators on t h e o i l market o f t e n focus

o n a measure of t h e d i f f e r e n c e be tween t h e " v a l u e " of t h e o i l

once c o n v e r t e d i n t o p r o d u c t s and t h e c o s t of t h e c r u d e o i l

i t s e l f . There has been very l i t t l e pub l i shed work on the n a t u r e

and b e h a v i o u r of t h i s m a r g i n and t h e f i r s t p a r t of t h e s t u d y i s

a d d r e s s e d t o t h e p r o b l e m of m e a s u r i n g and summar i s ing its

behaviour.

Once some p a t t e r n s f o r t h e margin between t h e two s i d e s

of t h e o i l market - crude and products - have been e s t a b l i s h e d ,

t h e p a p e r i s t h e n a b l e t o t u r n to t h e q u e s t i o n of model l i n g t h e

r e l a t i o n s h i p be tween t h e t w o se r i e s , and t h i s r e q u i r e s some

a n a l y s i s of t h e markets concerned.

The p a p e r c o n c e n t r a t e s on two c r u d e o i l s (and t h e i r

a s s o c i a t e d p r o d u c t values), A r a b i a n L i g h t (33.9 'API) and

N i g e r i a n L i g h t (37.7 OAPI). The r e a s o n f o r c h o o s i n g t h e s e two

p a r t i c u l a r crudes i s t h a t d a t a i s a v a i l a b l e for long per iods and

t h a t t h e i r p r i c e behaviour is n o t t o o s imilar (as would be Arab

and I r a n i a n Light f o r example).

A p a r t i c u l a r p r o b l e m w i t h s t u d y i n g t h e s e c o n c e p t s i s

t h a t t h e r e is n o " o f f i c i a l " s o u r c e of d a t a f o r t h e c r i t i c a l

c o n c e p t s . I n s t e a d t h e r e a r e s e p a r a t e e s t i m a t e s p roduced by

1

v a r i o u s p r i v a t e agencies and t h i s l e a d s t o t h e unusual s i t u a t i o n

of having mu1 t i p l e o b s e r v a t i o n s ( e s t ima tes ) f o r t h e same concept.

An important p a r t of t h e paper is t h e r e f o r e devoted t o comparison

of t hese v a r i o u s d a t a sources.

The p a p e r i s d i v i d e d into two s e c t i o n s . Part A

d e s c r i b e s t h e main r e s u l t s , both a n a l y t i c a l and s t a t i s t i c a l , of

t h e study. This s e c t i o n i s se l f - con ta ined but does n o t i nc lude

any d i s c u s s i o n of how t h e r e s u l t s were der ived. For r e a d e r s who

are i n t e r e s t e d i n t h e d e r i v a t i o n of t h e r e s u l t s and t h e d e t a i l s

of t h e i n v e s t i g a t i o n Part B cove r s t h e same m a t e r i a l but a t much

g r e a t e r l e n g t h . The a r r a n g e m e n t of p a r t B i s a s follows.

S e c t i o n B.l p r e s e n t s t h e b a s i c c o n c e p t s t o be u s e d i n t h e

a n a l y s i s and t h e f u n d a m e n t a l h y p o t h e s i s of t h e "normal margin"

(between s p o t crude p r i c e s and s p o t product p r i ces ) . Sec t ion B.2

is concerned wi th t h e d a t a used, w i th t h e va r ious sou rce of d a t a

and w i t h a c o m p a r i s o n be tween d i f f e r e n t s o u r c e s f o r t h e same

concep t . S e c t i o n B.3 p r e s e n t s t h e s t a t i s t i c a l a n a l y s i s of t h e

b a s i c h y p o t h e s i s which i s t h a t t h e 'netback' ( t h e v a l u e of t h e

p r o d u c t s o b t a i n e d from a b a r r e l of c r u d e l e s s t r a n s p o r t and

product ion c o s t s ) moves i n a d o l l a r f o r d o l l a r r e l a t i o n s h i p with

t h e s p o t c r u d e p r i c e a t t h e p o i n t o f s a l e . T h i s s i m p l e

h y p o t h e s i s is n o t s u p p o r t e d by t h e d a t a . S e c t i o n B.4 t h e n

o u t l i n e s some new h y p o t h e s e s , a s a r e a c t i o n t o t h e r e s u l t s of

s e c t i o n B.3, which a n a l y s e t h e e x t e n t t o which concen t r a t ion on a

s imple market i n e q u i l i b r i u m (as assumed i n B.3) does c o r r e c t l y

inco rpora t e prob 1 e m s r a i s e d by c e r t a i n impor t a n t i n s t i t u t i o n a 1

f e a t u r e s eg geograph ica l s e p a r a t i o n of markets, t h e e x i s t e n c e of

2

a two t i e r c r u d e p r i c e s y s t e m , and t h e e x i s t e n c e of r e f i n e r i e s

wi th d i f f e r e n t cos t s t r u c t u r e s . Some of t hese new hypotheses a r e

t h e m s e l v e s t e s t e d and t h e r e s u l t s p r e s e n t e d i n B.5. The

conclus ion t o s e c t i o n B is i n e f f e c t p a r t A of t h e paper so t h a t

no s e p a r a t e conclusion i s r e q u i r e d . The unifying d e v i c e f o r

hand1 i n g a v e r y complex marke t is t h a t of a s k i n g how t h e two

s i d e s (crude and products) would be r e l a t e d i f the market were i n

e q u i l i b r i u m and u s i n g t h e s i m p 1 i c a t i o n s t h a t t h i s p e r m i t s t o

carry out a s e r i e s of tests on t h e o p e r a t i o n of t h e market.

3

PART A : PRIBCIPAL FIRDIIVGS OF THE STUDY

The b a s i c h y p o t h e s i s t h a t r u n s t h r o u g h a l l s t u d i e s

r e l a t i n g product p r i c e s t o crude p r i c e s i s t h a t t h e v a l u e of t h e

p r o d u c t s , n e t t e d back t o t h e p o i n t of s a l e of t h e c r u d e , should

be s y s t e m a t i c a l l y r e l a t e d t o t h e p r i c e of t h e c rude . The

d i f f e r e n c e between t h e two c o n c e p t s , which w e s h a l l c a l l t h e

" n e t b a c k margin", or s i m p l y t h e "margin", h a s been used a s a

measu re o f p r o f i t o r loss f o r r e f i n e r i e s o r as a tool t o d e c i d e

w h e t h e r t h e marke t i s s u b s t a n t i a l l y out of equi l ibr ium. There

has been an i m p l i c i t assumption t h a t t h e r e i s a ''normal" margin

between t h e two s e r i e s and t h a t t h e a c t u a l v a l u e of t h e margin i s

n o t expected t o move away from t h i s v a l u e by s u b s t a n t i a l amounts

or f o r l o n g p e r i o d s . We show t h a t , i n d e e d , i f t h e r e i s

e q u i l i b r i u m in t h e markets w i t h a p e r f e c t l y compe t i t i ve s t r u c t u r e

t h e n t h e n e t b a c k c o r r e c t l y c a l c u l a t e d f o r a m a r g i n a l r e f i n e r y

would b e e x p e c t e d t o b e s l i g h t l y a b o v e t h e c r u d e p r i c e b u t t o

move with it.

To t e s t t h i s hypothes is of t h e "normal" margin d a t a on

both ne tbacks and spot c rude is required. There i s no " o f f i c i a l "

d a t a on e i t h e r concept but t h e r e a r e s e v e r a l u n o f f i c i a l series of

d a t a . Comparing t h e d a t a o n i d e n t i c a l c o n c e p t s on a m o n t h l y

b a s i s over t h e p e r i o d 1 9 7 6 t o 1983 r e v e a l s two g e n e r a l and

important f ind ings . Sources d o d i f f e r s y s t e m a t i c a l l y o v e r t h e

w h o l e p e r i o d and t h e r e a r e s u b - p e r i o d s of g r e a t d i s a g r e e m e n t .

4

For crude d a t a fou r sources were used:

( i > OPEC B u l l e t i n

( i i ) Petroleum I n t e l l i g e n c e Weekly

( i i i ) Middle East Petroleum and Economic Pub l i ca t ions

( i v ) An indus t ry es t imate .

The main s p e c i f i c f i n d i n g s were t h a t t h e OPEC B u l l e t i n f i g u r e is

s i g n i f i c a n t l y g r e a t e r on average than t h e o t h e r sou rces over t h e

p e r i o d (by be tween one and two p e r c e n t ) . On a v e r a g e t h e o t h e r

t h r e e sources a r e c l o s e but vary between each o ther by an amount

e q u a l t o abou t 65 c e n t s . I n t h e f i r s t e i g h t months of 1 9 7 9 t h e

d i f f e r e n c e between sources i s o f t e n very g r e a t - f o r Arab Light

the maximum d i f f e r e n c e reaches $6 w h i l e for Nigerian t h e maximum

d i f f e r e n c e i s $3. This "measurement e r r o r " i n t h e spo t p r i c e i s

s o l a r g e t h a t no s t a t i s t i c a l work shou ld i n c l u d e t h i s period.

For netback d a t a t h r e e sou rces were u t i l i s e d :

(i) Petroleum I n t e l l i g e n c e Weekly

( i i ) OPAL

(iii) An i ndus t ry e s t ima te .

Netback d a t a d i s t i n g u i s h e s not on ly t h e crude used but a l s o t h e

l o c a t i o n of t h e r e f i n e r y and t h e t y p e of r e f i n e r y assumed.

Comparisons between t h e sources f o r i d e n t i c a l concepts r e v e a l e d a

c l o s e agreement between a l l t h r e e b u t w i th OPAL below b o t h o t h e r

sources f o r both crudes. Again t h e d i f f e r e n c e s between sources

a r e a t t h e i r g r e a t e s t i n 1979. Rather s u r p r i s i n g l y t h e agreement

between sources i s c l o s e r f o r netbacks than f o r crudes. However,

c l o s e n e s s of s e r i e s i s n e i t h e r a n e c e s s a r y n o r a s u f f i c i e n t

5

c o n d i t i o n f o r t h e s e r i e s to be a c c u r a t e , e v e n though i t d o e s

i n c r e a s e c o n f i d e n c e in t h o s e s e r i e s w h i c h a r e a r r i v e d a t

independent ly . Hence a l l t h e subsequent s t a t i s t i c a l work, which

i s b a s e d on u s i n g a s e r i e s which i s n o t an " o u t l i e r " , must b e a r

t h e q u a l i f i c a t i o n t h a t measurement e r r o r is p o s s i b l e . However it

is an i m p o r t a n t f i n d i n g t h a t n o n - i n d u s t r y p u b l i s h e d d a t a on

n e t b a c k s a r e v e r y c l o s e to t h o s e a c t u a l l y u s e d by an an a c t u a l

a g e n t . The d e t a i l e d knowledge of t h e m a r k e t d o e s n o t p roduce

n o t i c e a b l y d i f f e r e n t f i gu res .

Given the amount of measurement e r r o r t h a t t hese ser ies

r e v e a l i t i s q u i t e l i k e l y t h a t t h e o r e t i c a l models, based on i d e a l

d a t a , w i l l n o t be a b l e t o be f i t t e d e x a c t l y t o t h e d a t a . T h e r e

w i l l b e a n e r r o r t e r m of a n i r r e d u c i b l e minimum however t he

a n a l y s i s is conducted.

The d e t a i l e d e x a m i n a t i o n of d a t a on p r o d u c t n e t b a c k s

and spo t crude p r i c e s ove r t h e lengthy per iod 1976 t o 1983 makes

it c l e a r t h a t t h e r e is a very c l o s e t i e between t h e two s i d e s of

t h e o i l m a r k e t , i e be tween p r o d u c t s and c r u d e . However, t h e

exac t n a t u r e of t h e r e l a t i o n s h i p raises some i n t e r e s t i n g a s p e c t s

t h a t a r e u n l i k e l y t o h a v e b e e n a p p a r e n t s o l e l y f rom a p r i o r i

t h e o r i s i n g or from empi r i ca l a n a l y s i s of s h o r t runs of da ta .

The two major f i n d i n g s a r e t h a t :

(i) The r e l a t i o n s h i p between spot product netbacks and s p o t crude pr ices a p p e a r s t o b e e p i s o d i c (however t h e r e l a t i o n s h i p i s f o r m u l a t e d ) . The s h i f t i n g i n the r e l a t i o n s h i p d o e s n o t a p p e a r t o b e c o n t i n u o u s , i n d i c a t i n g the o m i s s i o n of some c o n t i n u a l l y v a r i a b l e factor, but is rather discontinuous, indicating the e f f e c t of a factor vhich changes at d iscrete in terva l s .

( i i ) The r e l a t i o n s h i p between the two series c o u l d only be c o n s i s t e n t v i t h a prof i t maximising o p e r a t i o n of t h e

6

market i f the period of adjustment to change i s slow and/or there are large fixed cost elerents involved in adjustment to large shifts in the market situation. The persistence of the netback a t a l e v e l below the spot p r i c e ( r a t h e r than above i t ) i s an important characteristic of the market which requires explanation. In particular the persistence of th i s phenomenon even when the data are analysed separately for each episode i d e n t i f i e d i n (i) c l e a r l y r e q u i r e s f u r t h e r inve s t i g a t ion.

The v i e w i m p l i c i t in t h e " t r a d e j o u r n a l s " a p p e a r s t o b e

t h a t t h e d i f f e r e n c e between t h e netback and t h e s p o t crude p r i c e s

- t h e netback margin - f l u c t u a t e s around a normal v a l u e (which is

by i m p l i c a t i o n c o n s t a n t ) . D e v i a t i o n s f rom t h e m a r g i n c a n be

t a k e n a s i n d i c a t i n g changes i n t h e s t a t e of t h e m a r k e t and a l s o

t h e f i n a n c i a l ( p r o f i t o r l o s s ) p o s i t i o n o f f i r m s . The "normal

margin" hypothesis has t o be d i sca rded for two s e p a r a t e reasons.

F i r s t l y , o v e r l o n g p e r i o d s , t h e a v e r a g e o r t y p i c a l m a r g i n

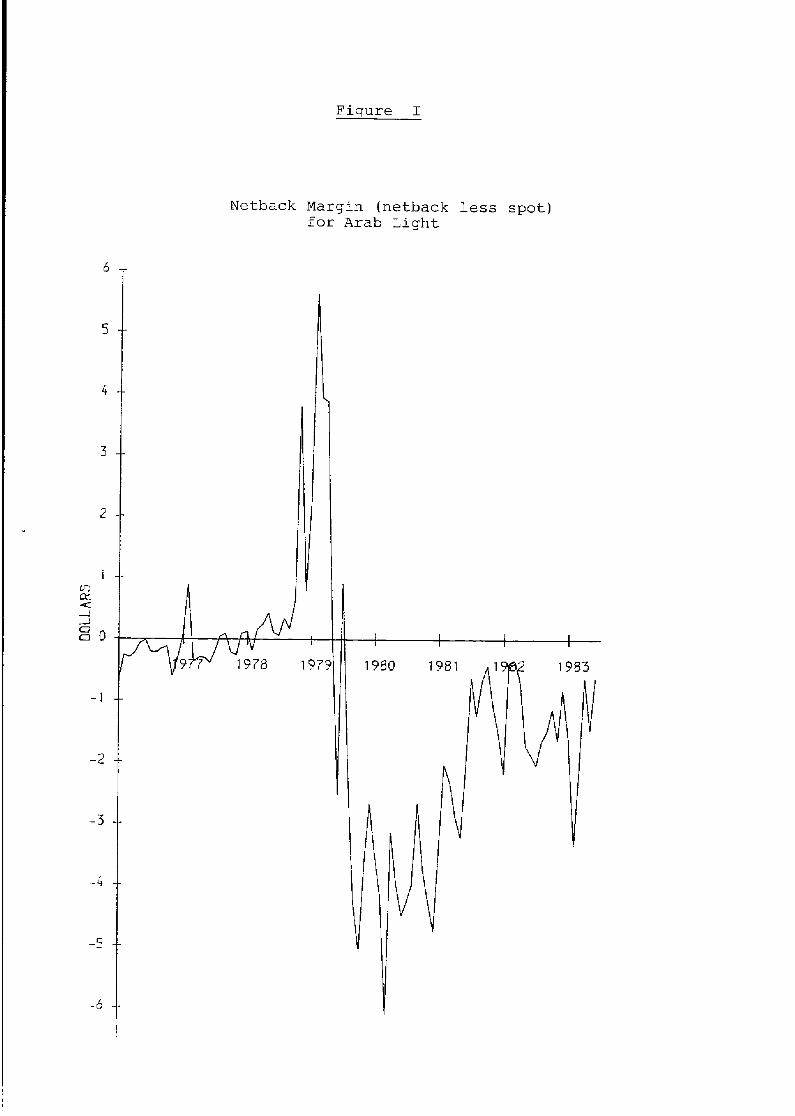

changes. F igu res I and I1 make i t c l e a r how sharp t h e s e changes

a r e . The second r e a s o n f o r a b a n d o n i n g t h e "normal marg in"

c o n c e p t , e v e n for i d e n t i f i e d e p i s o d e s , i s t h a t the d o l l a r € o r

d o l l a r response i t imposes can be b e t t e r e d by a r e l a t i o n s h i p w i t h

a m a r g i n t h a t v a r i e s c o n t i n u o u s l y w i t h t h e g e n e r a l o i l p r i c e

l e v e l . The e x i s t e n c e o f a p e r c e n t a g e r a t h e r t h a n a n a b s o l u t e

mark-up (or mark-down) r e c e i v e s s t r o n g s u p p o r t f rom t h e d a t a .

However, i t i s i m p o r t a n t t o n o t i c e t h a t t h i s p e r c e n t a g e m a r g i n

changes be tween e p i s o d e s and t h a t no f i n a l e x p l a n a t i o n for why

t h i s should be i s a r r i v e d a t .

The e p i s o d e s t h a t a r e i d e n t i f i e d f o r b o t h Arab L i g h t

and N i g e r i a n L i g h t a r e : ( a ) f rom J a n u a r y 1 9 7 6 t o l a t e i n 1978;

( b ) from l a t e 1978 t o l a t e summer 1 9 7 9 ; ( c > from l a t e summer

7

1979 t o sp r ing 1981; (d) from sp r ing 1981 t o t h e end of 1983.

In t h e first episode ( Jan 1976- l a t e 1978) spo t p r i c e s

and t h e netback a r e a lmost i n a d o l l a r f o r d o l l a r r e l a t i o n s h i p

( w i t h a s t a n d a r d e r r o r of e s t i m a t e of 30 c e n t s f o r Arab and 50

c e n t s f o r N i g e r i a n ) . T h i s seems t o f i t t h e e x p e c t e d p a t t e r n ,

p a r t i c u l a r l y f o r t h e indus t ry d a t a - t h e two s i d e s of t h e market

are very c l o s e l y r e l a t e d and t h e netback is s l i g h t l y h igher than

t h e s p o t p r i c e . T h i s wou ld be q u i t e c o n s i s t e n t w i t h a n M C = M R

cond i t ion f o r p r o f i t maximisation, wi th a f a 1 l i n g demand cu rve

h a v i n g a l o w e r MR t h a n t h e c o s t of p r o d u c t s and a r i s i n g c o s t

c u r v e wi th a higher MC than t h e cos t of r e f i n i n g average b a r r e l .

Both e f f e c t s would be expected t o be very s l i g h t ; hence t h e s m a l l

p o s i t i v e margin of t h e netback over spot i s not su rp r i s ing . The

very t i g h t f i t f o r t h i s per iod sugges t s t h a t i t is u n l i k e l y t h a t

o t h e r v a r i a b l e s w o u l d h a v e a s i g n i f i c a n t r o l e t o p l a y

( p a r t i c u l a r l y t h e o f f i c i a l p r i c e which was almost i d e n t i c a l t o

t h e s p o t p r i c e ) . T h i s p e r i o d , f o r R o t t e r d a m p r o d u c t p r i c e s , i s

c o n s i s t e n t w i th t h e "normal margin" hypothes is where t h e margin

is v e r y s l i g h t l y p o s i t i v e o r n e g a t i v e d e p e n d i n g on t h e d a t a

source. One s t r ange f i n d i n g (common t o a l l per iods) i s t h a t the

margin f o r Arab Light is c o r r e l a t e d wi th t h e margin f o r Nigerian

Light. I n equ i l ib r ium t h e r e would be no such c o r r e l a t i o n and so

t h i s suggests t h a t t h e r e are demand s i d e shocks (hence common t o

a l l c r u d e s ) which a r e f e l t on a l l p r o d u c t p r i c e s b u t which a r e

t r a n s l a t e d back to d i f f e r e n t d e g r e e s t o t h e v a r i o u s c r u d e s .

S ince t h e "normal margin" model is t h e b e s t f i t t i n g found f o r t h e

f i r s t e p i s o d e , t h e f i n d i n g c a n n o t be s i m p l y a t t r i b u t e d t o

8

s p e c i f i c a t i o n e r r o r .

The second episode, f rom l a t e 1 9 7 8 t o mid 1979, saw a

l a r g e number of unexpected e v e n t s and e x t e r n a l p r ice movements

a p p e a r in a v e r y s h o r t p e r i o d . I t can s c a r c e l y be t r e a t e d a s a

s i n g l e homogeneous p e r i o d ( e v e n t h e d a t a i s more t h a n u s u a l l y

suspect) and a l l a t tempts t o do so produced r e l a t i o n s h i p s of t o o

poor a s t a t i s t i c a l f i t f o r u s e f u l a n a l y s i s . The one s t r i k i n g

f e a t u r e of t h i s p e r i o d ( o f t e n t h o u g h t of as b e i n g domina ted by

t h e s u p p l y d i s r u p t i o n of t h e I r a n i a n r e v o l u t i o n ) i s t h a t

on averaRe netbacks were some 5 % higher than s p o t f o r Arab Light

and 12% higher f o r Nigerian Light. This f i n d i n g is a l l t h e more

remarkable because i n a l l o t h e r episodes netbacks have been on

average below s p o t pr ices . Rowever, the v a r i a t i o n s w i t h i n t h e

p e r i o d a r e so g r e a t t h a t o n l y a m o n t h by month a n a l y s i s of t h e

f i g u r e s b a s e d on i n s t i t u t i o n a l and f a c t u a l m a t e r i a l c o u l d

e s t a b l i s h any f i rm conclusion.

The t h i r d episode, s t r e t c h i n g f rom l a t e i n 1979 t o

e a r l y in 1981, corresponds to a period i n which t h e s p o t p r i c e of

t h e crude i n q u e s t i o n was above t h e o f f i c i a l p r i ce . This can be

i n t e r p r e t e d as a per iod of excess demand ( a t the g i v e n o f f i c i a l

p r i c e s ) where l i m i t e d s u p p l i e s meant t h a t b u y e r s of m a r g i n a l

c a r g o s w e r e w i l l i n g t o pay more t h a n t h e o f f i c i a l p r i c e . Fo r

t h i s p e r i o d t h e "normal margin" was v e r y s t r o n g l y n e g a t i v e -

(around $3 f o r Arab Light and $2 f o r Nigerian). There has been a

temptat ion t o suggest t h a t t h i s i n d i c a t e s producers ope ra t ing a t

a loss, b u t t h i s i g n o r e s t h e d i f f e r e n c e be tween m a r g i n a l and

a v e r a g e c o n c e p t s . S i n c e most c r u d e was bough t a t o f f i c i a l

9

p r i c e s , below t h e spo t p r i c e , t h e t o t a l c o s t s of r e f i n i n g cou ld

w e l l have been below t h e t o t a l revenue even though t h e marginal

c o s t f o r t h e r e f i n e r y chosen was above marginal revenue according

t o t h e d a t a .

For t h i s p e r i o d t h e p e r c e n t a g e m a r g i n model e x p l a i n s

t h e d a t a b e t t e r t han t h e a b s o l u t e margin model, and g i v e s a Saudi

netback a t 90% of s p o t p r i c e and a Nigerian netback of 95% of t h e

spo t p r i ce . The accuracy of t h e equa t ions i s s u b s t a n t i a l l y l e s s

than those f o r t h e f i r s t per iod f o r Arab L igh t , suggest ing t h a t

some o t h e r v a r i a b l e may be invo lved . The low v a l u e of t h e Durbin

Watson s t a t i s t i c confirms t h i s f inding. There a r e two cand ida te s

f o r i n c l u s i o n i n t h e equations. F i r s t l y , t h e o f f i c i a l p r i c e must

be t e s t e d s i n c e , i n a p e r i o d when t h e s p o t i s h i g h e r t h a n t h e

o f f i c i a l p r i c e i t m i g h t b e e x p e c t e d t h a t t h e l o w e r p r i c e wou ld

d e t e r m i n e p r o d u c t p r i c e s , a t l e a s t i n p a r t . When b o t h s p o t and

o f f i c i a l p r i c e s were included a s exp lana to ry v a r i a b l e s f o r t h e

n e t b a c k t h e n t h e s p o t v a r i a b l e c o n t i n u e d t o be s t r o n g l y

s i g n i f i c a n t , but t h e o f f i c i a l p r i c e was comple t e ly i n s i g n i f i c a n t

and added n o t h i n g t o t h e d e g r e e of e x p l a n a t i o n . T h i s i s s t r o n g

c o n f i r m a t i o n of t h e h y p o t h e s i s t h a t p r i c i n g was c a r r i e d o u t o n

m a r g i n a l i s t l i n e s and n o t on an average c o s t basis . T e s t s were

a l s o c a r r i e d o u t f o r t h e p r e s e n c e of l a g s by a n a l y s i n g spot

p r i c e s l e a d i n g n e t b a c k s and n e t b a c k s l e a d i n g s p o t p r i c e s . No

e v i d e n c e f o r l a g g e d r e l a t i o n s h i p s ( w i t h o r w i t h o u t o f f i c i a l

p r i c e s ) cou ld be found f o r t h i s episode.

Hence f o r t h e per iod of excess demand t h e d a t a s u p p o r t s

a h y p o t h e s i s of m a r g i n a l i s t p r i c i n g w i t h r a p i d a d j u s t m e n t t o

10

s h o c k s a r i s i n g f rom e i t h e r side of t h e marke t . The one f e a t u r e

wh ich c a n n o t b e s o s i m p l y e x p l a i n e d is t h e d e g r e e t o wh ich t h e

netback i s p e r s i s t e n t l y below t h e spo t pr ice . If it was p u l l e d

down by t h e o f f i c i a l p r i c e we migh t h a v e e x p e c t e d t o f i n d t h e

o f f i c i a l p r i c e s i g n i f i c a n t . The d a t a from a l l sources confirms

t h i s n e g a t i v e margin and f o r a genuinely marginal r e f i n e r y t h e

n e t b a c k would h a v e been l o w e r s t i l l . I n o r d e r t o a r g u e t h a t

marginal revenue was s y s t e m a t i c a l l y underestimated by t h e netback

c o n c e p t i t would be n e c e s s a r y t o show t h a t t h e s p o t p r o d u c t

p r i c e s were n o t t h e a p p r o p r i a t e marginal concepts and were lower

than t h e t r u e marginal revenues from products , o r t h a t t h e c o s t s

n e t t e d o u t ( t r a n s p o r t , r e f i n e r y e t c . ) were t o o l a r g e . S i n c e

t h e s e cos t elements were probably less than a d o l l a r i n t o t a l t h e

margin of e r r o r on t h e c o s t s i d e cou ld not p o s s i b l y e x p l a i n t h e

n e g a t i v e netback margin.

The o b s e r v a t i o n t h a t n e t b a c k s were b e l o w s p o t c r u d e

p r i c e s t h e n p r e s e n t s a p r o b l e m of i n t e r p r e t a t i o n . I t i s w e l l

known t h a t some r e f i n e r s r a n a t a loss and o u r d a t a m e r e l y

a p p e a r s t o c o n f i r m it . Even t h e p e r s i s t e n c e of t h e l o s s o v e r a

year and a h a l f is eas i ly exp la ined i f t h e r e a r e l a r g e e x i t and

r e - e n t r y c o s t s ( m o t h b a l l i n g c o s t s ) . C l e a r l y i t c a n o f t e n be

b e t t e r t o run a t a s m a l l l o s s t han t o incur t h e s e l a r g e shutdown

c o s t s . However t h e p e r s i s t e n c e of mara ina l l o s s e s cannot be so

e a s i l y explained. Sec t ion B4 of t h e paper a n a l y s e s a series of

a s p e c t s of t h e m a r k e t i n o r d e r t o s e e w h e t h e r i n s t i t u t i o n a l

f a c t o r s c o u l d e x p l a i n t h i s f i n d i n g . I t i s a r g u e d t h a t u n l e s s

t h e r e i s g e n e r a l n o n - p r o f i t making b e h a v i o u r w e do n o t h a v e a n

11

adequate exp lana t ion f o r t h i s phenomenon. Thus w e must conclude

t h a t t h e t h i r d e p i s o d e p r e s e n t s a p u z z l e - p r i c e s were s e t o n a

m a r g i n a l i s t b a s i s but t h e r e was a p e r s i s t e n t margina l l o s s on t h e

d a t a a s c a l c u l a t e d .

The final episode, which r u n s f r o m e a r l y 1 9 8 1 t o end

1983, a l s o p re sen t s a complex p i c tu re . The percentage margin and

a b s o l u t e margin hypotheses work e q u a l l y w e l l and both show t h e

netback below t h e spo t p r i c e f o r Arab Light , w i t h Nigerian Light

showing a lmost a d o l l a r f o r d o l l a r r e l a t i o n s h i p . The goodness of

f i t is b e t t e r t h a n i n t h e p r e v i o u s e p i s o d e and as good a s t h e

f i r s t episode f o r Nigerian (but no t f o r Arab Light) . The period

of t h e f i n a l e p i s o d e w a s one i n which t h e s p o t p r i c e was l ower

than t h e o f f i c i a l pr ice . S ince t h i s phenomenon is d i f f i c u l t t o

e x p l a i n i n a t w o - t i e r marke t s y s t e m u n l e s s b u y e r s t a k e a

p o r t f o l i o t y p e choice even a t t h e margin ( i e buy some o f f i c i a l

even though i t is more expens ive than spot ) , t e s t s were c a r r i e d

o u t t o s e e w h e t h e r t h e o f f i c i a l p r i c e a s we1 1 as the s p o t p r i c e

a f f e c t e d t h e netback. There was confirmation of t h i s hypothesis

for Arab Light but not f o r Niger ian Light. Such a f ind ing could

be e x p l a i n e d i f b u y e r s f e l t i t l e s s i m p o r t a n t t o pay t h e

i n s u r a n c e of p u r c h a s i n g N i g e r i a n a t o f f i c i a l p r i c e s t h a n

purchasing Saudi a t o f f i c i a l p r i ces .

A second, unusua l , f e a t u r e of t h e l a s t episode i s t h a t

f o r t h e f i r s t time ev idence of lagged r e a c t i o n s was found. The

spo t p r i c e was r e l a t e d t o both t h e cu r ren t and one month lagged

netback f o r bo th Arab and Niger ian crudes. It i s n o t obvious why

t h e r e s h o u l d be a l a g t o demand s i d e i n f l u e n c e s only when t h e

12

s p o t is below t h e o f f i c i a l pr ice . The e f f e c t was small ( w i t h an

ave rage l a g of one week) and o n l y w i t h d a t a based on s h o r t e r time

pe r iods could a proper dynamic a n a l y s i s be undertaken.

Even f o r t h e f i n a l episode when netbacks a r e r e l a t e d t o

s p o t and o f f i c i a l p r i c e s (and o f f i c i a l p r i c e s a r e h i g h e r t h a n

s p o t ) t h e sum of t h e c o e f f i c i e n t s i s less than un i ty , i n d i c a t i n g

a l o s s a t t h e margin. Since the netback i s c a l c u l a t e d t o be l e s s

t h a n t h e s p o t p r i c e t h e n e v e n on a n a v e r a g e c o s t i n g b a s i s a

r e f i n e r y would show a loss according t o these f igu res . Hence t h e

f i n a l p e r i o d p r o v i d e s d a t a which s u g g e s t s t h a t t h e p e r i o d of

a d j u s t m e n t t o a new marke t s t r u c t u r e i s v e r y l e n g t h y ( o v e r 4

y e a r s ) o r t h a t o n a c o n v e n t i o n a l c o s t i n g b a s i s most r e f i n e r i e s

a r e prepared not t o prof it maximise because continued product ion

s e r v e s o t h e r ends. These f i n d i n g s mus t be l o o k e d a t i n t h e

con tex t of t h e wider range of d a t a on r e f in ing . The s t a t i s t i c a l

a n a l y s i s has concent ra ted l a r g e l y on b a s i c r e f i n i n g a t Rotterdam.

T h i s c h o i c e took i n t o a c c o u n t s e v e r a l f a c t o r s . F i r s t l y , i t

a l l o w e d t h e l o n g e s t r u n o f d a t a . S e c o n d l y , i f m a r k e t s a r e i n

e q u i l i b r ium then t h e netback should be t h e same everywhere except

f o r random f l u c t u a t i o n s . Th i rd ly , on a m a r g i n a l i s t argument i t

wou ld be t h e h i g h e s t c o s t p l a n t s u r v i v i n g i n a n i n d u s t r y t h a t

w o u l d j u s t b r e a k e v e n and which s h o u l d t h e r e f o r e be u s e d f o r

t e s t s concerning market behaviour. Data on complex r e f i n i n g show

t h e n e t b a c k h i g h e r t h a n t h e s p o t p r i c e f o r most o f t h e f i n a l

pe r iod under study. This of course i s n o t a proof t h a t e v e n such

a r e f i n e r y o p e r a t e d a t a p ro f i t ( b e c a u s e o f f i c i a l p r i c e s were

somet imes h i g h e r s t i l l ) b u t d o e s warn a g a i n s t t h e u s e of

13

gene ra l i s a t i o n s on prof i t s or l o s s e s .

A n a l y s i s of t h e m o d e l s when a p p l i e d t o n e t b a c k s as

d i f f e r e n t i a t e d by l o c a t i o n ( and by t e c h n o l o g y ) shows t h a t as

be tween c e n t r e s t h e r e s u l t s a r e v e r y s i m i l a r . Ne tbacks a r e

r e l a t e d to s p o t p r i c e s when t h e r e is " e x c e s s demand'' d u r i n g t h e

t h i r d episode, and a r e r e l a t e d t o both spo t and o f f i c i a l p r i c e s

d u r i n g t h e f o u r t h e p i s o d e when t h e r e i s " e x c e s s supply." The

weakest l i n k between netbacks and crude p r i c e s appears t o be f o r

t h e US case. In g e n e r a l , t h e r e l a t i o n between Rotterdam netbacks

and c r u d e p r i c e s f o r Arab L i g h t i s as c l o s e a s f o r any o t h e r

c e n t r e .

The a n a l y s i s of t h e r e l a t i o n s be tween t h e p r o d u c t

p r i c e s , as summarised by t h e netback, and crude p r i c e s shows t h a t

t h e two s i d e s of t h e market a r e very c l o s e l y I inked on a month by

month bas i s . The n a t u r e of t h e l i n k has changed, n o t always i n a

p r e d i c t a b l e f a s h i o n (eg between t h e f i r s t and t h i r d episodes) ,

b u t t h e r e l a t i o n s h i p s seem f a i r l y s t a b l e o v e r t h e medium r u n .

There is, however, a r e s i d u a l d i f f e r e n c e between t h e s e r i e s which

a p p e a r s t o b e u n p r e d i c t a b l e . The a v e r a g e m a g n i t u d e of t h i s

u n e x p l a i n e d component i s a t l e a s t a b o u t 50 c e n t s . T h i s means

t h a t ( u s i n g t h e u s u a l 9 5 % c o n f i d e n c e i n t e r v a l ) g i v e n t h e s p o t

p r i c e t h e n e t b a c k c a n be p r e d i c t e d w i t h i n p l u s o r minus $1 ( and

v i c e v e r s a ) . It d o e s n o t a p p e a r l i k e l y , g i v e n t h e p r e s e n c e of

measurement e r r o r s i n t h e d a t a , t h a t any s u b s t a n t i a l improvement

can e a s i l y be made i n t h e e x p l a n a t i o n of t h e r e l a t i o n s h i p between

t h e two s i d e s of t h e marke t . I t i s p o s s i b l e t h a t v e r y complex

dynamic m o d e l s m a y improve t h e f i t of t h e model and i n d e e d t h e

14

s h i f t i n g m a r g i n h a s i t s e l f to be e x p l a i n e d . However t h e

t e c h n i q u e s r e q u i r e d would p r o b a b l y be of a n o r d e r o f magn i tude

more d i f f i c u l t t o u s e and t h e p o t e n t i a l g a i n f rom any a p r i o r i

model r a t h e r u n c e r t a i n and p o s s i b l y s m a l l . The marg in of

accuracy of e x p l a n a t i o n is c r u c i a l when we t u r n t o t h e o t h e r use

of netbacks - t h a t of judging whether o f f i c i a l d i f f e r e n t i a l s a r e

o u t of l i n e . The t e c h n i q u e , a s e x p l a i n e d by PIW, is t o compare

t h e n e t b a c k / o f f i c i a l d i f f e r e n t i a l f o r v a r i o u s c r u d e s . Those

which a r e h i g h ( o r low) r e l a t i v e t o t h e d i f f e r e n t i a l f o r t h e

"marker" (Arab L i g h t ) i n d i c a t e w h e t h e r an o f f i c i a l p r i c e i s

r e l a t i v e l y t o o low ( o r h igh) . S y m b o l i c a l l y w e c a l c u l a t e f o r

example :

(MN - NO) - ( S A - SO> (1)

where :

NN = Nigerian netback NO = O f f i c i a l p r i c e of Nigerian Light SN = Saudi netback SO = O f f i c i a l p r i c e of Arab Light .

If this i s z e r o the o f f i c i a l p r i c e s a r e s a i d t o be i n

l i n e wi th market r e a l i t i e s - i f i t i s p o s i t i v e t h e o f f i c i a l p r i c e

of N i g e r i a n i s r e l a t i v e l y t o o low, w h i l e i f i t i s n e g a t i v e t h e

o f f i c i a l p r i c e of N i g e r i a n is r e l a t i v e l y t o o h igh . T h i s

c a l c u l a t i o n assumes t h a t t h e n e t b a c k s d o a c t u a l l y measu re t h e

v a l u e of t h e c r u d e a t t h a t t i m e and t h a t t h e m a r g i n i s a b s o l u t e

and not r e l a t i v e . The measurement e r r o r s i n t h e netback toge ther

w i t h t h e e v i d e n c e t h a t n e t b a c k s d o n o t measu re t h e e q u i l i b r i u m

v a l u e of t h e c r u d e a t t h e m a r g i n i m p l i e s t h a t t h e r e w i l l b e a

15

random term or even a systematic term missing from (1). Hence a

systematic study of d i f f e r e n t i a l s would be needed t o investigate

t h e i r behaviour and i n p a r t i c u l a r t h e r e l a t i v e s i z e of spot

d i f f erent ia 1 s t o ne tback d i f f e r e n t i a l 6.

16

PART B : DETAILED ABULYSIS

B. 1 THE BELBTIOB BETWEEH SPOT CRUDE PRICES ARD SPOT PRODUCT VALUES

The b a s i c hypothes is i s t h a t crude p r i c e s and t h e v a l u e

of t h e p r o d u c t s o b t a i n e d f rom t h e c r u d e a r e s y s t e m a t i c a l l y

r e l a t e d . S p e c i f i c a l l y we c a n c o n s i d e r t h e % y i e l d of p r o d u c t s

(naphtha, g a s o l i n e , f u e l o i l e t c ) from crude o i l f o r a " typ ica l "

r e f i n e r y . The sum of t h e s h a r e s times t h e p e r u n i t p r i c e f o r

each product i s known as t h e "gross product va lue" (worth) and i s

t h e revenue f o r t h a t r e f i n e r y r e s u l t i n g from the r e f i n i n g of one

e x t r a b a r r e l o f o i l . I n o r d e r t o compare t h i s w i t h t h e c o s t of

i n p u t s w e must look a t t h e c o s t o f t h e c r u d e o i l c i f , and t h e

o the r r e f i n i n g costs. I f we concen t r a t e on a shor t - run marginal

a n a l y s i s t h e n t h e r e i s no e x t r a c a p i t a l c o s t i n v o l v e d i n

r e f i n i n g another b a r r e l of o i l (below f u l l capac i ty ) but t h e r e

a r e r u n n i n g c o s t s of o p e r a t i n g t h e r e f i n e r y . I t wou ld t h u s be

p o s s i b l e t o b u i l d up t h e e x t r a s h o r t - r u n c o s t s by t a k i n g t h e

crude o i l p r i c e ( a p p r o p r i a t e l y def ined) fob, adding on t r a n s p o r t

and insurance c o s t s t o o b t a i n t h e c i f o i l p r ice and then adding

on t h e r e f i n i n g c o s t . The r e s u l t i n g c o s t could b e compared t o

t h e r e v e n u e f i g u r e . However , i n d u s t r y p r a c t i c e h a s been t o

"Netback" t h e revenue by s u b t r a c t i n g r e f i n i n g c o s t s and t r a n s p o r t

c o s t s t o o b t a i n t h e "value" of the o i l i n t h e p r o d u c e r c o u n t r y .

T h i s c o n c e p t i s known by s e v e r a l names: o f t e n c a l l e d t h e " fob

1 7

n e t b a c k " o r t h e " i m p l i e d f o b c r u d e o i l n e t b a c k v a l u e ' ' (OPAL) or

t he ''spo t product e q u i v a 1 e n t v a 1 uel' ( i ndus t ry t e r m ino 1 ogy).

The d i f f e r e n c e between what w e s h a l l from now on c a l l

t h e "netback" and t h e c r u d e p r i c e , w e s h a l l c a l l t h e "ne tback

margin". The r e s u l t i n g f i g u r e is f r e q u e n t l y used in t w o ways :

( i ) "General ly , t h e spo t v a l u e of t h e r e f i n e d b a r r e l a t t h e

producer ' s l o a d i n g p o r t i s compared w i t h .... c r u d e p r i c e s t o

determine p r o f i t o r l o s s " (PIW(supp) 7 March 83 p4).

( i i ) Dif fe rences between spo t product v a l u e s of the major

c rude o i l s are r e l a t e d t o d i f f e r e n c e s i n o f f i c i a l crude ( f o r t h e

same p a i r s of c r u d e s ) t o show w h e t h e r " t h e v a r i a t i o n s o r

" d i f f e r e n t i a l s " among the o f f i c i a l crude p r i c e s a r e a l i g n e d w i t h

s p o t product market r e a l it ies" (PIW, ib id) .

I n a l l s u c h a p p l i c a t i o n s t h e d i f f e r e n c e be tween t h e

r e l a t e d s e r i e s have been c a l c u l a t e d which i m p l i e s t h e e x i s t e n c e

of a 'normal' a b s o l u t e margin between the series. I n f a c t , t h e r e

are f o u r d i s t i n c t t ypes of netback margin t h a t can be c a l c u l a t e d

and t h i s i s o n e s o u r c e of v a r i a t i o n t h a t mus t be a l l o w e d f o r .

The p l u r a l i t y arises because crude o i l is s o l d e i t h e r on t h e s p o t

m a r k e t ( a t s p o t p r i c e s ) o r a t o f f i c i a l p r i c e s , and p r o d u c t s a r e

s o l d e i t h e r on t h e s p o t p r o d u c t m a r k e t ( a t t h e f a c t o r y g a t e ) o r

a t c o n t r a c t p r i ces . Furthermore, it i s p o s s i b l e (OPAL) t o extend

t h e l e n g t h of t h e c h a i n of n e t t i n g back by s t a r t i n g w i t h t h e

i n l a n d ' ' m a r k e t p r i c e s of p r o d u c t s and s u b t r a c t i n g d u t i e s and I'

marketing c o s t s ( t o give composite proceeds ex-ref inery).

18

I n f a c t s t a n d a r d a n a l y s i s of t h e c r u d e o i l m a r k e t

( r a t h e r than t h e product market) concen t r a t e s on using t h e s p o t

product concept and combining t h i s e i t h e r w i t h spo t crude p r i c e s

o r w i t h o f f i c i a l crude p r i ces .

B e f o r e w e t u r n t o t h e q u e s t i o n of which of t h e s e two

, m a r g i n s t o examine we must f i r s t look in more d e t a i l a t t h e

c a l c u l a t i o n of t h e netback i t s e l f . The netback is r e f e r r e d t o by

t h r e e c r i t i c a l parameters:

(i) t h e t y p e of crude being used;

(ii)

( i i i )

t h e type of r e f i n i n g process being used;

t h e l o c a t i o n of t h e r e f i n e r y .

The f i r s t two c a t e g o r i e s must be t aken into account because t h e r e

i s no u n i v e r s a l l y t y p i c a l r e f i n e r y - t h e y i e l d s v a r y b e t w e e n

c r u d e s , t h e y a l s o depend on t h e t y p e and l o c a t i o n of t h e

r e f i n e r y . The c r u d e s w e c o n s i d e r a r e j u s t Arab L i g h t and

N i g e r i a n L i g h t , b u t t h e s e h a v e d i s t i n c t l y d i f f e r e n t y i e l d

percentages a s the PIW annual supplement r e v e a l s . Furthermore,

e v e n f o r a g i v e n t y p e of r e f i n i n g t h e t y p i c a l o r a v e r a g e y i e l d

f o r a p a r t i c u l a r c r u d e w i l l v a r y b e t w e e n l o c a t i o n s , b e c a u s e

r e f iaeries a r e s p e c i f i c a l l y designed w i t h l o c a l demand c o n d i t i o n s

i n mind. Hence PIW u s e s y i e l d p e r c e n t a g e s w h i c h a r e c r u d e and

l o c a t i o n s p e c i f i c f o r t h e same t y p e o f r e f i n i n g . T h e r e a r e s i x

19

l o c a t i o n s f o r r e f i n e r i e s used by PIW:

( i ) Rotterdam

( i i ) US Gulf Coast

( i i i ) Caribbean

( i v ) P e r s i a n Gulf

( v ) Singapore

( v i ) I t a l y .

Other sources concen t r a t e on Rotterdam and/or t h e US Gulf .

The techniques of r e f i n i n g assumed by t h e v a r i o u s d a t a

sources a r e d i f f e r e n t , eg PIW assumed t h a t non-US r e f i n e r i e s a r e

of a s imple toppinglreforming type w h i l e its f i g u r e f o r t h e US is

for a c o n v e r s i o n t y p e r e f i n e r y . OPAL u s e s f o r R o t t e r d a m b o t h

b a s i c hydro-skimming (p r imary d i s t i l l a t i o n and r e f i n i n g ) and

c o n v e r s i o n ( c a t a l y t i c c r a c k i n g and a l k y l a t i o n ) t y p e r e f i n e r i e s .

These two t y p e s of r e f i n e r y w e s h a l l r e f e r t o a s b a s i c and

complex ( a l though the l a t t e r is something of a h o l d a l l term).

G i v e n t h a t we d e c i d e wh ich r e f i n e r y we w i s h t o u s e w e

must t h e n v a l u e i t s p r o d u c t s by l o c a l s p o t p r o d u c t v a l u e s and

s u b t r a c t m a r g i n a l r u n n i n g c o s t s , i n s u r a n c e c o s t s and f r e i g h t

c o s t s . This l a s t i s c a l c u l a t e d on a m a r g i n a l b a s i s u s i n g

Wor ldsca le f r e i g h t r a t e s from t h e producer country t o t h e country

i n which t h e r e f i n i n g i s being eva lua ted .

From d e f i n i t i o n s w e n e x t t u r n t o t h e b a s i c h y p o t h e s i s

which is t h a t , f o r a g iven crude, t h e netback and crude p r i c e a r e

r e l a t e d . G i v e n t h a t w e h a v e d e c i d e d t o u s e s p o t p r o d u c t

v a l u a t i o n s w e must d e c i d e which c r u d e p r i c e t o use . The

c a l c u l a t i o n s a re e x p l i c i t l y on a margina l b a s i s , as t h e exc lus ion

20

of c a p i t a l c o s t e lements makes c l e a r . Hence t h e c o r r e c t p r i c e i s

t h a t which i s m a r g i n a l t o t h e buyer . Here i t m i g h t be t h o u g h t

t h a t t h e lower of t h e o f f i c i a l and s p o t p r i c e s would be marg ina l ,

but t h i s ignores how a t w o - t i e r p r i c e s y s t e m o p e r a t e s . We must

a s k why t h e two p r i c e s a r e n o t e q u a l i s e d by p u r c h a s e s s h i f t i n g

demand t o t h e l o w e r (and d r i v i n g i t u p u n t i l t h e two meet). I f

t h e s p o t p r i c e i s a b o v e t h e o f f i c i a l , i t i s h e l d t h e r e by t h e

r a t i o n i n g of s u p p l i e s on t h e o f f i c i a l m a r k e t - i n s u c h a

s i t u a t i o n t h e s p o t p r i c e is g e n u i n e l y m a r g i n a l . The more

d i f f i c u l t c a s e i s t h a t where t h e s p o t is ( p e r s i s t e n t l y ) b e l o w

o f f i c i a l . Given t h a t n o t a l l crude is being bought on s p o t t h i s

w i l l only happen i f t h e r e is some reason f o r p r e f e r r i n g o f f i c i a l

o i l d e s p i t e t h e f a c t t h a t it is more expensive. We w i l l r e t u r n

t o this po in t later and assume f o r t h e p r e s e n t t h a t spot crude is

t h e m a r g i n a l s o u r c e of s u p p l y where s p o t p r i c e s a r e a b o v e o r

below o f f i c i a l p r i c e s .

Thus t h e b a s i c h y p o t h e s i s i s t h a t t h e n e t b a c k (NI i s

r e l a t e d t o t h e s p o t crude ('3) pr i ce :

N = f (SI (2 )

T r a d i t i o n a l l y a n a l y s i s has centred on t h e margin between those

two magnitudes so t h a t w e cou ld s p e c i a l i s e t h e f u n c t i o n t o

N = a + S (3 )

Since t h e r e l a t i o n s h i p i s n o t thought t o h o l d i d e n t i c a l l y a t a l l

t i m e s we can make i t s t o c h a s t i c by adding a t e r m U, which s t a n d s

for t h e sum of a l l o t h e r i n f l u e n c e s on t h e r e l a t i o n :

Nt = a + S, + ut (4)

where t h e s u b s c r i p t d e n o t e s t h e t i m e p e r i o d . The t e r m U s h o u l d

21

e x h i b i t no s y s t e m a t i c b e h a v i o u r - i f i t d o e s t h e n t h e

r e l a t i o n s h i p between t h e netback and t h e spot c rude p r i c e would

n o t be just on a v e r a g e a c o n s t a n t . Hence it would n o t b e

p o s s i b l e t o dec ide whether a p a r t i c u l a r v a l u e of t h e margin was

high or low - t h i s would have t o be decided r e l a t i v e t o t h e o the r

f a c t o r s determining t h e margin. Another way t o look a t t h e same

p o i n t i s t h a t i n d e c i d i n g w h e t h e r a p a r t i c u l a r v a l u e of t h e

marg in was u n u s u a l l y h i g h o r low t h e v a r i a n c e of t h e random

f l u c t u a t i o n (U> i s a c r i t i c a l component. I f we were a b l e t o

e x p l a i n p a r t of U b y i n c l u d i n g e x t r a f a c t o r s t h e n t h e r a n g e o f

randomness for t h e margin would decrease and we should be a b l e t o

spo t more e a s i l y when an i n d i v i d u a l v a l u e was abnormal.

E q u a t i o n ( 4 ) p r o v i d e s a p u r e l y mechanis t ic hypothes is

t o tes t . Although w e have i m p l i c i t l y suggested t h a t t h e concepts

used a r e margina l revenues and c o s t s w e have not y e t s p e l l e d ou t

t h e economic a s s u m p t i o n s which would j u s t i f y s u c h c l a i m s , and

w i t h o u t which a h y p o t h e s i s of how t hey a r e l i n k e d c a n n o t be

constructed. This deeper ques t ion is taken up i n s e c t i o n B.3.

22

B.2 THE DATA

B . 2 . 1 SPOT CRUDE PRICES

The d i s t i n g u i s h i n g f e a t u r e of spot p r i c e d a t a for crude

o i l is t h a t t h e r e i s no o f f i c i a l s e r i e s . I n s t e a d i n t e r e s t e d

p a r t i e s , s u c h as p r o d u c e r s , r e f i n e r s and c o n s u l t a n c i e s t e n d t o

produce t h e i r own f i g u r e s , This has r e s u l t e d i n a m u l t i p l i c i t y

of e s t ima tes f o r t h e same concept, caused i n p a r t by t h e l a c k of

an agreed methodology and i n p a r t by c e r t a i n f e a t u r e s of t h e o i l

market.

Crude o i l i s no t t raded on a p a r t i c u l a r market “ f l o o r ”

- t h e r e is no l o c a t i o n a t which a l l t h e d e a l s a r e made and a t

which t h e d a t a might be c e n t r a l l y r e g i s t e r e d . In s t ead d e a l s are

i n d i v i d u a l l y r e g i s t e r e d between agen t s who a r e spread worldwide.

Hence d a t a must b e c o l l e c t e d by some form of s u r v e y approach .

T h i s l e a d s t o a f i r s t s o u r c e of v a r i a t i o n - an a g e n t a t a

p a r t i c u l a r t i m e may b e a b l e t o p r o v i d e a p r i c e “done” (ie

a c t u a l l y t r ansac ted ) or m e r e l y a pr ice I’offered”. Pub1 i c a t i o n s

which sometimes r e p o r t both f o r t h e same time per iod sugges t t h a t

a t p re sen t ( i n a r a t h e r t r a n q u i l environment) t h e s e two concepts

a r e v e r y c l o s e . Hence t h e r e i s a s o u r c e of a m b i g u i t y i n t h i s

a s p e c t of t h e d a t a . T h i s sho r t - coming is l i k e l y t o be more

s e r i o u s i n t h e f i r s t p a r t of our per iod , when t h e spo t market was

v e r y “ t h i n “ and few t r a n s a c t i o n s a c t u a l l y t o o k p l a c e e v e n € o r

major crudes.

23

A second p r o b l e m f o r s p o t p r i c e d a t a i s t h e d a t i n g of

t h e c o n t r a c t . I f w e a r e c o n s i d e r i n g , s a y , December p r i c e s w e

c o u l d e i t h e r f o c u s on p r i c e s " in t h e month" o r p r i c e s " f o r t h e

month". The fo rmer r e f e r s t o c o n t r a c t s made i n December wh ich

w i l l a c t u a l l y be implemented some l i t t l e t i m e ( u p t o 2 o r 3

months) ahead , w h i l e t h e l a t t e r r e f e r s t o p r i c e s s e t on o r

be fo re December t h a t w i l l be payable on o i l r e c e i v e d i n December.

C l e a r l y t h e l a t t e r w i l l be much more l a b o r i o u s t o b u i l d up on a

t i m e s e r i e s b a s i s . These two c o n c e p t s a l s o s u g g e s t t h a t

d i f f e r e n t a g e n c i e s may h a n d l e t h e d a t i n g p r o b l e m in d i f f e r e n t

ways. I n f a c t , s i n c e t h e r e i s no c l e a r s t a t e m e n t of t h e

p r i n c i p l e s on which any series i s c a l c u l a t e d , i t i s not p o s s i b l e

t o come t o any d e c i s i o n as t o which s e r i e s i s t h e b e s t for

e m p i r i c a l work. We need t o l o o k a t a l l t h e s o u r c e s and compare

t h e i r performance.

For t h e purposes of this study w e ob ta ined monthly d a t a

from four d i f f e r e n t sources.

(1) OPEC B u l l e t i n

We c a l l t h e s p o t p r i c e s f rom t h i s s o u r c e SSO and NSO.

This s o u r c e , which is a v a i l a b l e on a w e e k l y b a s i s , b e g i n s i n

J a n u a r y 1 9 7 9 and r u n s c o n t i n u o u s l y u n t i l t h e end of our p e r i o d

(December 1983). It is a n a v e r a g e of 4 w e e k l y f i g u r e s and i s a

mid-month f igu re .

( 2 ) Middle Eas t Petroleum and Economic P u b l i c a t i o n s (MEPEP)

T h i s d a t a s o u r c e p r o v i d e s w e e k l y d a t a f r o m t h e

b e g i n n i n g of our p e r i o d (which s t a r t s at J a n u a r y 1976) . The

week ly a v e r a g e s a g a i n p r o d u c e a mid-month f i g u r e . W e d e n o t e

24

t h e s e by SSM and NSM.

( 3 ) Indus t ry Sources

Many l a r g e r e f i n i n g and producing companies c o n s t r u c t

t h e i r own " b e s t e s t i m a t e s " of t h e p r i c e by combining a l l t h e

knowledge a v a i l a b l e t o them. We h a v e one such s o u r c e ( S S I and

N S I ) f rom t h e b e g i n n i n g of o u r p e r i o d ( J a n u a r y 76) t o t h e end o n

a monthly bas i s .

( 4 ) Petroleum I n t e l l i g e n c e Weekly (PIW)

This aga in is a mid-month average.

This p u b l i s h e s d a t a on spot p r i c e s from January 1978 t o

t h e p re sen t f o r t h e two crudes i n ques t ion (denoted S S P and NSP).

We can summarise t h e r e l a t i o n s h i p s between t h e v a r i o u s

s p o t p r i c e s i n terms of r e g r e s s i o n models. The model r e g r e s s e s

one se r ies on a n o t h e r ( o v e r t h e maximum d a t a p e r i o d common t o

b o t h ) w i t h o u t i n t r o d u c i n g a c o n s t a n t . I f t h e s e r i e s were

i d e n t i c a l t h e r e g r e s s i o n c o e f f i c i e n t would b e u n i t y , t h e

c o r r e l a t i o n u n i t y and t h e s t a n d a r d e r r o r o f e s t i m a t e ( a v e r a g e

r e s i d u a l ) zero. The r e s u l t s a r e shown i n Tab le s I and I1 ( ~ 2 7 ) .

The t a b l e s show two important f e a t u r e s .

(i> For b o t h c r u d e s t h e OPEC B u l l e t i n f i g u r e is

s i g n i f i c a n t l y g r e a t e r t h a n a l l t h e o t h e r f i g u r e s (by a f a c t o r

r a n g i n g f r o m 1 t o 2 p e r c e n t ) . T h i s i m p l i e s t h a t a t a p r i c e of

$30 p e r b a r r e l t h e OPEC b u l l e t i n p r i c e would be about 30-60 cen t s

a b a r r e l higher t han o t h e r series.

(ii) The o the r t h r e e s e r i e s a r e a l l very c l o s e t o each

o t h e r and i n g e n e r a l do not d i f f e r s i g n i f i c a n t l y . However, t h e

s tandard e r r o r of estimate f o r a l l s i x cases , exc lud ing t h e OPEC

B u l l e t i n , i s between 50 c e n t s and 80 cents. Hence a l though t h e

25

c o r r e l a t i o n i s very h igh t h e average e r r o r i s t h e same o rde r of

m a g n i t u d e a s t h e d i f f e r e n c e be tween t h e s e s e r i e s and the OPEC

B u l l e t i n s e r i e s when t h e p r i c e i s around $30. I n v e s t i g a t i o n of

t h e r e s i d u a l s r e v e a l s a few months when t h e r e s i d u a l s a r e many

t i m e s the s tandard e r r o r of es t imate . S ince t h e r e s i d u a l s f o l l o w

a "t" d i s t r i b u t i o n i t would be expected t h a t approximately one i n

a hundred would be more than t h r e e times as l a r g e as t h e s tandard

e r r o r of es t imate . Table I11 ( ~ 2 8 ) l i s t s t h e months and t h e s i z e

o f t h e m u l t i p l e when t h i s c r i t e r i o n is exceeded . It i s n o t

s u r p r i s i n g t h a t t h e only per iod of s u b s t a n t i a l d i s a g r e e m e n t i s

t h e f i r s t e i g h t months of 1979, when t h e s p o t p r i c e w a s moving

with g r e a t r a p i d i t y and t h e r e was a g r e a t d e a l of u n c e r t a i n t y i n

t h e marke t . F o r t h e c a s e of Arab L i g h t t h e s p o t p r i c e f o r May

1979 r a n g e s f rom $28.35 f o r SSI, t o $28.95 f o r SSO, t o $30.67 f o r

SSM and up t o $34.25 for SSP. The extreme d ive rgence i s f o r SSP

w h i c h is usually v e r y c l o s e t o SSI and SSM. With 8 r a n g e of $6

in $30 t h e r e i s c l e a r l y a very s u b s t a n t i a l measurement e r r o r f o r

t h i s month, and i t s h o u l d n o t b e i n c l u d e d i n any s p e c i f i c t e s t s

o f h y p o t h e s e s s i n c e such a n ex t r eme " o u t l i e r " c o u l d a f f e c t t h e

t o t a l p i c t u r e t o a g r e a t e x t e n t . By compar i son t h e r a n g e o f

p r i c e s for Nigerian Light i n t h e same month i s SSO a t $31.13, SSI

a t $33.35, S S P a t $34.25 and SSM a t $ 3 4 . 5 . T h i s r a n g e o f $3 is

l a r g e , but only h a l f t h a t of Arab Light. The per iod of extreme

disagreement f o r Arab Light i s s h o r t e r being j u s t May, June and

J u l y of 1979, w h i l e for N i g e r i a n L i g h t t h e p e r i o d e x t e n d s from

J a n u a r y t o August 1979 w i t h t h e a d d i t i o n of J u n e 1981. As a

check an agreement between t h e s e r i e s which are a v a i l a b l e for t h e

26

TABLE I: RELATIOIM€IPS BETWEEB SPOT PRICE MEASURES FOB ARAB LIGHT

Regress ion Dependent Independent Per iod C o e f f i c i e n t Sqd. SEE DWS Equat ion va r i a b l e var iab 1 e (SE) c o r r e l - No. a t ion

(R1) S S I S SM 76.01- 0.997 0.997 0.51 1.59

(R2) s SP SSI 78.01- 1.000 0.991 0.81 2.21

(R3) s SP S SM 78.01- 0.997 0.992 0.71 2.72

(R4) s SP sso 79.01- 0.985 0.954 1.01 2.01

(R5) sso SSI 79.01- 1.015 0.989 0.51 1.19

(R6) sso S SM 79.01- 1.011 0.984 0.61 1.61

( R I 3 ) SSI S SM 76.01- 1.00 0.999 0.22 0.79

........................................................................

83.12 (0.002)

83.12 (0.003)

83.12 (0.003)

83.12 (0.004)

83.12 (0.002)

83.12 (0.002)

78.12 (0.001) 81.01- 83.12

TABLE 11: BELBTIOASHIPS BETWEEB SPOT PRICE LIRASWES FOR HIGEEFA% LIGHT

(R7) NSI NSM 76.01- 83.12

(R8) NSP NSM 78.01- 83.12

(R9) NSP NSI 78.01- 83.12

(R10) NSP NSO 79.01- 83.12

(R11) NSO MSI 79.01- 83.12

(R12) NSO NSM 79.01- 83.12

(R14) NSI NSM 76.01- 78.12 81.01- 83.12

1.004 0.996 0.63 1.90

0.998 0.993 0.70 1.97

0.994 0.995 0 . 5 9 1.56

0.981 0.972 0.81 1.16

1.012 0.973 0.79 1.81

1.017 0.960 0.96 1.76

1.0037 0,999 0.30 1.37

(0.002)

(0.003)

(0.002)

(0.003)

(0 .003>

(0.004)

(0.0013)

27

TABLE 111: MOHTHS WITH EXTBEHE DISBC;BKEMENTS* BETWEEH SERIES

( a ) Arab Light

SSI s SP s SP SSP sso sso +SSM SSI S SM sso S S I SSM

79.05 4.3 79.05 7 . 3 79 .05 5.2 7 9 . 0 5 5 .7 7 9 . 0 5 3 . 4

79.07 5.0 79.06 3 . 4 79 .07 3.7

( b ) Nigerian Light

NSI NSP NSP NSP NSO NSO NSM NSI NSM NS 0 NSI NSM

79.01 81.06 79.06 79.02 79.05 7 9 . 0 5 3 . 8 3 . 5 3 . 2 3 . 2 3 . 3 4.1

7 9 . 0 8 3.7

* An extreme d ive rgence i s a r e s i d u a l g r e a t e r t han t h r e e times

t h e s tandard e r r o r of estimate. It is measured i n m u l t i p l e s of the SEE.

l o n g e s t per iod, we re-ran the r e g r e s s i o n s omi t t i ng t h e two y e a r s

1979 and 1980. The r e s u l t s a r e shown i n T a b l e s 1 and I1 and as

e q u a t i o n s (R13) and (R14). Over t h e n o n - t u r b u l e n t p e r i o d t h e

s e r i e s are extremely c l o s e with s t a n d a r d e r r o r s of estimate t h a t

a r e a b o u t h a l f t h o s e of when 1979 and 1 9 8 0 d a t a a r e i n c l u d e d .

The measurement e r r o r problem f o r t h i s abbrev ia t ed pe r iod i s n o t

non-existent but is very small and shou ld not b i a s t h e r e s u l t s t o

1 any g r e a t ex ten t .

I n c o n c l u s i o n we c a n f e e l f a i r l y s a f e t h a t t h e PIW,

28

MEPEP and industry based s e r i e s w i l l g i v e s i m i l a r r e s u l t s ,

part icular ly i f some months during 1979 are de leted from whatever

s t a t i s t i c a l t e s t s are t o be run. The OPEC B u l l e t i n s e r i e s i s

s ign i f i cant ly greater than the other ser i e s and its use could be

expected t o lead t o d i f ferent r e s u l t s from the others.

29

B.2.2 HETBBCK DATA

The cons t ruc t ion of netback series r e q u i r e s information

on f o u r elements:

( i ) t h e spot product p r i c e s i n a p a r t i c u l a r market;

(ii) t h e r e f i n e r y y i e l d s i n t h a t market ;

( i i i ) t h e running c o s t s per b a r r e l f o r t h e r e f i n e r y ;

( i v ) t h e t r a n s p o r t and insurance c o s t s between t h e r e f i n e r y and the expor t po in t of t h e crude under cons idera t ion .

Given these requirements and t h e absence of any o f f i c i a l

agency i t i s n o t s u r p r i s i n g t h a t t h e r e a r e a m u l t i p l i c i t y of

e s t i m a t e s of t h e n e t b a c k e v e n f o r a g i v e n c r u d e a t a g i v e n

r e f i n e r y l o c a t i o n . G i v e n t h e c o m p l e x i t y o f t h e c a l c u l a t i o n s

r equ i r ed it is not s u r p r i s i n g t h a t t he re should be susp ic ion of

f i g u r e s produced by agencies no t i nvo lved i n r e f i n i n g . However,

pub l i shed f i g u r e s are an important source of common information

which must be inves t iga t ed .

We have used t h r e e sources of d a t a bu t f o r each source

t h e r e i s more than one ne tback s o t h a t t h e t o t a l number of series

a v a i l a b l e i s r a t h e r l a rge . Each source i d e n t i f i e s e i t h e r more

t h a n one l o c a t i o n of t h e r e f i n e r y or more t h a n one t y p e of

r e f i n e r y (or both).

30

( i > Petroleum I n t e l l i g e n c e Weekly (PIW)

This major source p u b l i s h e s d a t a on Saudi netbacks from

R o t t e r d a m on a m o n t h l y b a s i s f rom t h e b e g i n n i n g of o u r p e r i o d

(SNPIWR). Four o t h e r c e n t r e s , t h e C a r i b b e a n (SNPIWC), t h e

P e r s i a n Gulf (SNPIWP), Singapore ( S N P r W S ) and I t a l y (SNPIWI) were

added i n September 1976 and a s i x t h c e n t r e , t h e U S Gulf (SNPIWU)

i n J a n u a r y 1977. The a v e r a g e of t h e s e s e r i e s (SNPIW6) h a s a l s o

been cont inuously publ ished from t h e beginning of 1977. S i m i l a r

s e r i e s h a v e b e e n p u b l i s h e d f o r N i g e r i a n s i n c e 1979 f o r f i v e

c e n t r e s ( N N P I 8 5 ) i n c l u d i n g R o t t e r d a m (NMPIWR), w i t h 4 c e n t r e s

back to January 1979 and j u s t Rotterdam back t o January 1976.

A l l t h e PIW d a t a , w i t h t h e e x c e p t i o n o f US n e t b a c k s ,

assume t h e r e f i n i n g t o be of t h e b a s i c t o p p i n g / r e f o r m i n g t y p e .

The y i e l d p a t t e r n s a r e v a r i e d be tween summer and w i n t e r months

b u t a p a r t f rom t h i s were unchanged u n t i l J u l y 1983. From t h a t

month on the y i e l d s were a l t e r e d and t h i s i n c r e a s e d t h e Gross

Product Value by approximately Z X , g i v i n g a sharp d i s c o n t i n u i t y

a t t h a t d a t e . F o r t h e U S a r e f i n e r y w i t h c o n v e r s i o n

p o s s i b i l i t i e s ( u p g r a d i n g h e a v i e r p r o d u c t s i n t o l i g h t e r ) i s

assumed throughout t h e period.

PTW assumed i n 1982 t h a t t h e r e f i n i n g c o s t w a s about 20

c e n t s a b a r r e l ( t h i s f i g u r e is a l t e r e d y e a r l y ) and t r a n s p o r t

c o s t s ( c a l c u l a t e d on a m o n t h l y b a s i s ) were 8 5 c e n t s a b a r r e l .

E r r o r s i n t h e s e e l e m e n t s a r e n o t l i k e l y t o a f f e c t t h e n e t b a c k

very g r e a t l y .

I t i s c l e a r t h a t t h e PIW d a t a o f f e r s a v e r y wide

geograph ica l coverage and t h a t f o r b a s i c r e f i n i n g t h e long r u n s

31

of d a t a on a cons t an t b a s i s a r e very v a l u a b l e .

( i i > OPAL

A second source of pub l i shed d a t a is provided by OPAL.

They g i v e d a t a s t a r t i n g i n J a n u a r y 1980 f o r n e t b a c k s f rom

R o t t e r d a m for b o t h b a s i c hydroskimming and a c o n v e r s i o n t y p e

r e f i n e r y (SNOPAB, SNOPAC, NNOPAB and NNOPAC). I n 1983 t h e y

assumed r e f i n i n g c o s t s of 30 cen t s and 45 c e n t s f o r t h e two types

of r e f i n e r ies .

( i i i ) Indus t ry Data

As wi th spo t crude p r i c e s it i s important f o r companies

i n t h e o i l i ndus t ry t o c a l c u l a t e t h e v a l u e of netbacks based on

t h e i r own e x p e r i e n c e r a t h e r t h a n on t h a t o f some h y p o t h e t i c a l

t y p i c a l r e f i n e r y . We h a v e s u c h d a t a , c a l c u l a t e d f o r a s i m p l e

( b a s i c ) r e f i n e r y from J a n u a r y 1 9 7 6 for R o t t e r d a m ( S N R B I , N N R B I )

and f o r complex r e f i n i n g from January 1981 f o r both Rotterdam and

t h e US Gulf (SNRCI, SNUCI, NNRCI and NNUCI) .

There a r e v a r i o u s t y p e s of comparisions t h a t might be

made between t h e netback ser ies (between l o c a t i o n s , between types

of r e f i n e r y and be tween d a t a s o u r c e ) . For r e a s o n s t h a t w i l l

become apparent , it i s s e n s i b l e t o concen t r a t e on t hose f i g u r e s

wh ich a r e f o r t h e same l o c a t i o n and t h e same t y p e of r e f i n i n g

process. W e begin w i t h b a s i c r e f i n i n g a t Rotterdam €or which a l l

t h r e e s o u r c e s g i v e d a t a . ( p p s 34 and 35) g i v e

t h e r e s u l t s for r e g r e s s i o n s between t h e ser ies (without i n t e r c e p t

terms) r u n o v e r t h e l o n g e s t pe r iods a v a i l a b l e .

T a b l e s I V and V

We can s e e from t h e t a b l e s

t h e l o n g e s t per iod (PIW and indus t ry

t h a t t h e d a t a a v a i l a b l e f o r

bas i c r e f i n e r y a t Rotterdam)

32

a r e i n c l o s e agreement ( E q u a t i o n s (Et151 and (R20)). The OPAL

d a t a , f o r b a s i c r e f i n i n g , h a s a v e r y c l o s e f i t t o PIW, a s

measured by t h e s tandard e r r o r of es t imate , for both Arabian and

N i g e r i a n . For A r a b i a n i t i s s i g n i f i c a n t l y l e s s t h a n t h e o t h e r

two s o u r c e s (by 1.5 t o 2 p e r c e n t ) . For N i g e r i a n t h e OPAL f i g u r e

i s j u s t s i g n i f i c a n t l y l e s s t h a n t h e PIW f i g u r e bu t i t is

s u b s t a n t i a l l y l e s s t h a n t h e i n d u s t r y d a t a . Hence f o r b a s i c

r e f i n i n g at Rotterdam t h e r e i s a very l a r g e measure of agreement

between t h e series, w i th s tandard e r r o r s much less than those f o r

equat ions l i n k i n g t h e va r ious spo t p r i c e measures.

For complex r e f i n i n g i n Rotterdam t h e OPAL s e r i e s f o r

Arabian and Nigerian a r e s i g n i f i c a n t l y l o w e r t h a n t h e i n d u s t r y

d a t a (3 -4%) , w h i l e f o r US d a t a using complex r e f i n i n g t h e PIW and

indus t ry d a t a a r e a lmost i d e n t i c a l on average.

An e x a m i n a t i o n of t h e r e s i d u a l r e v e a l s o n l y two

obse rva t ions f o r which t h e r e s i d u a l is g r e a t e r than t h r e e times

t h e s tandard e r r o r of es t imate . One case is May 1 9 7 9 f o r S N P I W R

and SMRBI, and t h e o t h e r is January 1981 f o r SNPIWU and SNUCI ( i n

both cases t h e margin was o n l y j u s t ove r t h r e e s tandard e r ro r s ) .

The c a s e of May 1 9 7 9 is n o t s u r p r i s i n g - t h e t u r b u l e n c e i n t h e

c r u d e spot marke t a f f e c t e d t h e s p o t p r o d u c t m a r k e t , and s l i g h t

v a r i a t i o n s i n d a t a c o l l e c t i o n p r o c e d u r e s a t s u c h a t i m e c o u l d

e a s i l y change t h e sampled v a l u e by $1.5.

I n summary t h e netback series a r e i n c l o s e r agreement

than the p r i c e d a t a - t h e r e a r e g e n e r a l l y h ighe r c o r r e l a t i o n s and

fewer p o i n t s of extreme disagreement. The i n d u s t r y and PIW d a t a

correspond extremely c l o s e l y and a r e a t v i r t u a l l y t h e same l e v e l ,

33

TABLES IV: BELBTIOBSBIPS BETWEEN BETBACKS FOE ARAB LIGHT

( a ) Basic Refining a t Rotterdam

(RI51 SNIWR SNRBI 76.01- 1.001 0.997 0.47 1.04

(R16) SNPIWR SNOPAB 80.01- 1.016 0.985 0.30 1.39

(RI 7 ) SNRBI SNOPAB 80.01- 1.020 0.977 0.37 0.45

83.06 ( 0 . 0 0 2 )

83.06 (0.001)

83.12 (0.002)

(b) Complex Refining a t Rotterdam

SNOPAC SNRCI 81.01- 0 .954 0.985 0.32 0 . 3 5 (RI81 83.12 (0.002)

( c ) Complex Refining i n US

(R19) SNPIWU SNUCI 81.01- 0 . 9 9 5 0 .955 0 .53 1.50 83.06 (0.003)

34

TABLE V: RELBTIOHSEIPS BKTWIZElU HETBACKS FOR BIGERIBlP LIGHT

(a) Basic RefininE a t Rotterdam

(R20) NNPIWR NNRBI 76.01- 0.981 0 .998 0.43 1.12

(R21) NNPIWR NMOPAB 80.01- 1.003 0.985 0.34 0 .94

(R22) NNRB I NNOPAB 80.01- 1.020 0.986 0 . 3 6 0.74

83.06 (0.002)

83.06 (0.002)

83.12 (0.002)

(b) Complex Refining a t Rotterdam

(R23 1 NNRCI NNOPAC 81.01- 1.030 0.984 0.42 0.52 83.12 (0.002)

w h i l e t h e OPAL d a t a move l e s s c l o s e l y wi th t h e o t h e r two sources

and a r e below them on average. This is an important r e s u l t g i v e n

t h e n a t u r a l tendency t o t r u s t i ndus t ry d a t a more i n t h i s case.

F i n a l l y , t o r o u n d o f f t h e p i c t u r e , we g i v e t h e

( u n s q u a r e d ) c o r r e l a t i o n m a t r i x be tween a l l n e t b a c k s f o r t h e

common p e r i o d f o r which w e h a v e d a t a on a l l of them ( T a b l e s V I

and VII) . It i s c l e a r f rom t h o s e t a b l e s t h a t t h e h i g h e s t

c o r r e l a t i o n s occur be tween s e r i e s w i t h d i f f e r e n t s o u r c e s but

which have i d e n t i c a l d e f i n i t i o n s . Corr e 1 a t i o n s b e tween s e r i e s

f o r s imple and complex r e f i n i n g or between Rotterdam and t h e US

a r e apprec i ab ly lower even when t h e d a t a sou rce i s t h e same.

For both p r i c e and netback d a t a t h e r e a r e a l t e r n a t i v e

s o u r c e s o f d a t a which ma tch v e r y c l o s e l y and w h i c h e x t e n d o v e r

long per iods. It i s tempting t o assume t h a t t h e c l o s e n e s s of t h e

s e r i e s p roves t h a t they a r e c o r r e c t and o t h e r s e r i e s a r e wrong;

however , a l t h o u g h t h i s c l e a r l y s t r e n g t h e n s t h e i r c l a i m t o b e

35

correct it does not const i tute a proof, and we w i l l need to bear

t h i s i n mind when using t h e s e r i e s in t h e l a t t e r part of t h i s

paper .

TABLE VI: COBBELATIOBS PCR SAUDI EETBAmS (1981.01-1983.06)

SNPIWR SNRBI SNOPAB SNOPAC SNRCI SNPIWU SNUCI

SNPIWR 1.000

SNRBI 0.988 1.000

SNOPAB 0.992 0.993 1.000

SNOPAC 0.966 0.964 0.981 1.000

SNRCI 0.966 0.956 0.978 0.976 1.000

SNPIW 0.910 0.884 0.915 0.933 0.907 1.000

SNUCI 0.919 0.894 0.927 0.933 0.920 0.977 1.000

TABLE V I I : COBBELBTIORS FOB HIG'HtIAH HETBAmS (1981.01-1983.06)

NNPIWR NNRB I NNOPAB NNOPAC NNRCI

NNPIWR 1.000

NNRB I 0.989 1 .ooo

NNOPAB 0.993 0.993 1 .ooo

NNOPAC 0.983 0.976 0.990

NNRCI 0.976 0.973 0.980

1 .ooo

0.990 1 .ooo

36

B . 3 A SIHPLE MODEL BELBTIHG SPOT PRODUCT VBLWS Al9D SPOT CRUDE PRICES

B.3 .1 THE HODEL

I n t h e i n t r o d u c t o r y s e c t i o n o f t h i s pape r w e a r g u e d

t h a t t h e netback and spo t p r i c e for a g i v e n crude a r e t r e a t e d i n

t h e l i t e r a t u r e a s i f t h e y were r e l a t e d by a s i m p l e e q u a t i o n of

t h e type :

where ut i s a random term a t time t. I f t h i s term is random then

i t s v a l u e should on average be zero and success ive v a l u e s of t h e

random term should n o t be s y s t e m a t i c a l l y r e l a t e d . Such a model

has two imp 1 i c a t ions:

( i > If t h e s t a t i s t i c a l d i s t r i b u t i o n of t h e random t e r m were

known t h e n any p a r t i c u l a r v a l u e of t h e m a r g i n ( N t - S t ) could b e

c o m p a r e d w i t h t h e " n o r m a l m a r g i n " a n d a m e a s u r e m e n t of

abnormali ty der ived . Extreme d e v i a t i o n s would symbolise changes

i n t h e market.

( i i ) Once t h e no rma l d i f f e r e n t i a l s f o r s e v e r a l c r u d e s were

e s t a b l i s h e d (al , a2....) then we could compare a c t u a l margins t o

see whether one was unusua l ly l a r g e r e l a t i v e t o another. This

t y p e of c a l c u l a t i o n h a s been s u g g e s t e d a s a g u i d e t o r e l a t i v e

p r o f i t a b i l i t y and hence t o demand pressure . It is important t o

r e c o g n i s e t h a t i f ut i s i ndeed random t h e n t h i s month's v a l u e s

c a n p r e d i c t only t h a t f o r n e x t month t h e marg in w i l l b e a t i t s

37

"normal" v a l u e . O v e r s h o o t i n g i n one p e r i o d d o e s n o t make it

more, o r l e s s l i k e l y t h a t t h e r e w i l l be overshoot ing i n t h e next

p e r i o d . I f s u c h p a t t e r n s e x i s t e d w i t h h i s t o r i c d a t a t h e n

e q u a t i o n s s u c h as ( 4 ) would t e n d t o show s e r i a l c o r r e l a t i o n

between success ive v a l u e s of ut.

A d i f f e r e n t p o i n t t o emerge f rom t h i s s t a t i s t i c a l

a p p r o a c h is t h a t t h e c o e f f i c i e n t of t h e s p o t p r i c e s h o u l d b e

u n i t y and t h a t t h e r e s i d u a l s h o u l d n o t b e c o r r e l a t e d w i t h the

s p o t p r i c e ( i e t h a t a l l s y s t e m a t i c i n f o r m a t i o n on t h e c u r r e n t

l e v e l of t h e netback is contained i n t h e spo t pr ice) . I f e i t h e r

of t h e s e r e s t r i c t i o n s d i d n o t h o l d t h e n t h e b a s i c way of u s i n g

t h e e q u a t i o n would h a v e t o change. Suppose , f i r s t l y , t h a t t h e

c o e f f i c i e n t on t h e spot p r i c e i s not u n i t y ( i e t h a t t h e two

s e r i e s a r e n o t i n a d o l l a r f o r d o l l a r r e l a t i o n s h i p ) :

Nt = a + ( 1 + b ) St + U (5)

I n t h i s case t h e margin is a f u n c t i o n of t h e s p o t p r i c e :

(Nt - St) = a + b S, + ut ( 6 )

Depending on t h e s i g n of b t h e marg in wou ld t e n d t o na r row o r

widen a t h i g h p r i c e s . T h i s would mean f i r s t l y t h a t a t t e m p t s

m e r e l y t o focus on t h e s i z e of t h e c u r r e n t margin as an i nd ica to r

of whether t h e market was d i s tu rbed would be mis l ead ing - a h igh

v a l u e of t h e marg in c o u l d m e r e l y b e a r e s u l t of t h e h i g h s p o t

p r i c e and n o t because of any d i s e q u i l i b r i u m between t h e two s i d e s

of t h e market. Futhermore, a s w e s h a l l see l a t e r , a r e l a t i o n s h i p

such as ( 6 ) would r a i s e problems of economic i n t e r p r e t a t i o n a s t o

how such a s i t u a t i o n could come about.

38

The second case (of an o m i t t e d v a r i a b l e ) c o u l d be

w r i t t e n :

Nt = a + ( 1 + b) St + cZt + ut ( 7 )

I f t h e e q u a t i o n i s e s t i m a t e d o r u s e d ( i n t h e fo rm o f t h e c u r e n t

margin) without a l l o w i n g for t h e i n f l u e n c e of v a r i a b l e 2 (what

ever t h a t might be) t hen aga in t h e a c t u a l margin cou ld seem t o be

most u n u s u a l e v e n though it would be c o m p l e t e l y e x p l i c a b l e i n

terms of t h e l e v e l of v a r i a b l e Z.

To summar ise , t h e u s e of t h e a c t u a l m a r g i n (N-S) t o

i n d i c a t e any form of market tendency i m p l i e s t h a t such a margin

has a normal value. This hypothes is p l a c e s s t rong r e s t r i c t i o n s

of a t e s t a b l e n a t u r e on t h e r e l a t i o n between the two s e r i e s . If

t h e r e s t r i c t i o n s can be shown not t o have he ld , t o a s i g n i f i c a n t