a. Statement of Advice

62

As of 12 October 2021 Prepared for Antoine Morel Du-Boil What is this document about? This Statement of Advice documents your current financial circumstances; our recommendations for the future and contains information to help you to make a decision on whether to proceed with our advice. Where information relevant to our advice has been provided to you before, or separately with this Statement of Advice, we will make specific reference to it in the relevant section. Provided by Joshua Lee Financial Planner of Link Wealth Group Pty. Ltd. (ABN 98 157 712 055) Authorised Representative of AMP Financial Planning Pty Limited. Contact us Link Wealth Group Pty. Ltd. Level 1, 689 Burke Road, Camberwell VIC 3124 Ph: 03 9038 8267 Fax: 03 8678 1377 Email: [email protected] Statement of Advice

Transcript of a. Statement of Advice

Page br eak

As of 12 October 2021

Prepared for

Antoine Morel Du-Boil

What is this document about?

This Statement of Advice documents your current financial circumstances; our recommendations for the future and contains information to help you to make a decision on whether to proceed with our advice. Where information relevant to our advice has been provided to you before, or separately with this Statement of Advice, we will make specific reference to it in the relevant section.

Provided by

Joshua Lee Financial Planner of Link Wealth Group Pty. Ltd.

(ABN 98 157 712 055)

Authorised Representative of AMP Financial Planning Pty Limited.

Contact us

Link Wealth Group Pty. Ltd.

Level 1, 689 Burke Road, Camberwell VIC 3124

Ph: 03 9038 8267 Fax: 03 8678 1377

Email: [email protected]

Statement of Advice

12 October 2021

Mr Antoine Morel Du-Boil

450 Woori Yallock Rd

COCKATOO VIC 3781

Dear Antoine,

It’s our pleasure to work with you to achieve your goals. Enclosed is a copy of your statement of advice

(SOA) which details our analysis and my advice to you.

Please read the SOA thoroughly and if you have any queries or believe that relevant information may

have been overlooked or misinterpreted, please contact me before proceeding.

Our advice is current for 30 days from the date of this Statement of Advice. You may have already

instructed us to proceed with some or all of our recommendations. For any other recommendations, you

should confirm with us before acting on them. We can provide you further advice verbally or in writing.

I would be pleased to assist you in the implementation of this advice, including the completion and

lodgement of relevant application forms and associated documentation.

Thank you for the opportunity to be of service to you.

Yours sincerely,

Joshua Lee

Authorised Representative of AMP Financial Planning Pty Limited (AMPFP)

ABN 89 051 208 327

Australia Financial Services Licensee and Australia Credit Licensee

Licence No: 232706

Member of the AMP Group

Level 1, 689 Burke Road,

CAMBERWELL VIC 3124

See enclosures

Page 3 of 62

Table of contents

Table of contents ........................................................................................................................................ 3

About you .................................................................................................................................................... 4

Before you read our advice ....................................................................................................................... 6

Our advice ................................................................................................................................................... 7

Strategy Overview .................................................................................................................................... 9

Our recommendations ............................................................................................................................ 12

Our recommendations for FY 2022/23 ................................................................................................... 20

Future Recommendations ...................................................................................................................... 26

Summary of your position after our advice ............................................................................................. 28

Your investment strategy ........................................................................................................................ 30

Summary of your investment strategy .................................................................................................... 30

Your asset allocation .............................................................................................................................. 31

Summary of your products...................................................................................................................... 33

Your investments .................................................................................................................................... 33

Cost of your products .............................................................................................................................. 38

Your investment products ....................................................................................................................... 38

Details of your ongoing product costs .................................................................................................... 39

Staying on track to meet your goals ...................................................................................................... 40

Your adviser ........................................................................................................................................... 40

Our annual advice relationship ............................................................................................................... 40

Cost of our advice and services ............................................................................................................. 41

Details of our advice and service fees .................................................................................................... 42

What else you need to know ................................................................................................................... 43

Calculations and projections .................................................................................................................. 49

Fact sheets ................................................................................................................................................ 57

Selecting your investments..................................................................................................................... 57

Next steps ................................................................................................................................................. 60

Authority to proceed ................................................................................................................................ 61

Your acknowledgement .......................................................................................................................... 61

Page 4 of 62

About you The following is our understanding of your current situation. This information is used for the sole purpose

of providing you with appropriate advice.

A copy of the complete material used to collect your information can be provided on request.

Your personal details

Antoine Veronique

Date of birth 08/01/1956 23/02/1957

Age 65 64

Occupation Glazer On workers compensation – Retail

Clothes Shop Supervisor

Proposed retirement age 70 70

Marital status Married

Your cash flow

Antoine ($) Veronique ($) Total ($)

Income earned 75,000 28,400 103,400

Pension income 4,806 0 4,806

Total inflows 79,806 28,400 108,206

Tax payable (including Medicare) (15,262) 0 (15,262)

Net inflows 64,544 28,400 92,944

Expenses (38,672) (38,672) (77,344)

Total outflows (38,672) (38,672) (77,344)

Surplus (Deficit) 25,872 (10,272) 15,600

*You have told us that you save approximately $300 per week. We have used this information to work on

your cash flow position. It is important to note that this may not be an accurate representation of your

cash flow position but is only meant to be a reasonable basis for projecting financial information.

Your assets and liabilities

Owner Amount ($)

Personal or 'Lifestyle'

Motor Vehicle Antoine 12,000

Total 12,000

Savings and investments

Cash at bank Antoine and Veronique

25,000

Total 25,000

Superannuation

AMP Flexible Super - Super account (Signature Super post October 1st) Antoine 88,253

Total 88,253

Retirement income streams

AMP Flexible Super - Retirement account (Signature Super post October 1st) Antoine 52,938

Total 52,938

Total net worth 178,190

Page 5 of 62

Your retirement income stream

AMP Flexible Super - Retirement account (Signature Super post October 1st) Core Investments

Antoine

Pension summary

Age when pension purchased 59

Balance 52,938

Tax-free component –

Annual tax deduction* –

Reversionary No

First year payment summary

Pension payment before-tax 4,806

Minimum allowable pension payment 3,372

Maximum attainable pension payment 6,536

Tax rebate –

Pension payment frequency Fortnightly

Antoine's previous super contributions

Tax deductible contributions FY 2018/19 FY 2019/20 FY 2020/21

Salary sacrifice $9,780.00 $9,128.00 $7,712.00

Employer SGC contributions $3,310.93 $6,381.56 $4,471.63

Total $13,090.93 $15,509.56 $12,183.63

Non-tax deductible contributions Date deposited

Personal (non-tax deductible) contributions N/A N/A N/A

Page 6 of 62

Before you read our advice

Our understanding of your situation It’s important that we understand your circumstances and goals. We collected information about you so

we can provide the most appropriate advice for you to meet your goals.

Missing information As our advice is based on information you have provided, if any information you provided is incomplete or

incorrect, you risk making a commitment that may not be appropriate for you. It is important that you

inform us if this is the case, so we can review our recommendations.

Where to find more information This advice is based on, incorporates information from and should be read in conjunction with the

documents listed in a table on page 48. These documents have been provided to you, either previously or

with this advice. Further copies can be made available to you upon request.

Where this symbol has been used throughout this advice, we are referring to one of the documents identified in that table.

Things to consider It’s important that you understand the risks involved with our advice. We have detailed these risks under the Our advice and What else you need to know sections. Please consider them before proceeding with our advice.

Page 7 of 62

Our advice Your goals are the foundation of our advice. The most important thing is that we understand what’s

important to you and what financial success means for you.

Why have you sought advice? ⎯ “I would like to review my super now that I am 65 to ensure everything is set up in the way it should

be.”

What we will provide advice on The table below summarises the goals that have been agreed with you to be addressed in our advice.

Areas of advice Goals Priority

Superannuation / Retirement income / Cash flow / Super contributions

You would like to review the structure of your retirement savings to ensure you are structuring and growing your funds in the most tax-efficient manner for your future retirement at age 70. You would like to remain invested in line with your individual preferences, whilst exploring strategies to further grow your funds through fee and tax savings. You have no specific income needs in retirement and feel you will survive comfortably off the age pension. You, therefore, wish to ensure you are doing all you can to maximise the growth of your retirement savings

High

Estate Planning (Limited to beneficiary nominations)

You would like to ensure your family will receive all of your superannuation benefits in event of your passing with minimal tax withheld

High

What we will not provide advice on The table below outlines the areas of advice that you do not wish to receive advice on. By not receiving

advice on these matters, you may not have appropriate strategies in place to assist you in achieving any

goals you may have in these areas.

Retirement Planning

Reasons for not providing advice

You are not seeking any advice in relation to your retirement planning needs as you feel you will comfortably survive off the age pension as yourself and your wife live a very simple lifestyle on your farm you gifted to your child 6 years ago (Veronique’s son).

Risks of not addressing advice By not addressing this area of advice, you may be not addressing the long-term impacts of your strategy on your retirement.

When this will be addressed This will be addressed at your request/review or as required.

Insurances

Reasons for not providing advice You are not seeking any insurance-related advice as you currently hold no insurance inside super and do not wish to look to establish any as you are focused on growing your retirement savings.

Risks of not addressing advice

By not addressing this area of advice, you and your family may be financially vulnerable in the event you pass prematurely, become permanently disabled, suffer a medically traumatic illness, or unable to work because of disability or illness.

When this will be addressed This will be addressed at your request/review or as required.

Page 8 of 62

Budgeting

Reasons for not providing advice You are comfortable with your existing cash flow/expenditure as you live a very simple lifestyle and did not wish to seek any advice in relation to this.

Risks of not addressing advice By not addressing this area of advice, you may not be able to arrange your cash flow and budget in line with your needs.

When this will be addressed This will be addressed at your request/review or as required.

Centrelink

Reasons for not providing advice You are not seeking any Centrelink related advice as of right now and would do so upon retiring at age 70 if you feel you could not organize these yourselves.

Risks of not addressing advice By not addressing this area of advice, you may not be able to fully know what Centrelink benefits you are eligible to receive.

When this will be addressed This will be addressed at your request/review or as required.

Advice for spouse

Reasons for not providing advice You are unsure as to what benefits your wife held inside super and only wanted to address your own needs at this stage and then you would like me to discuss any areas I may be able to help with Veronique.

Risks of not addressing advice By not addressing both of your goals, you may not be able to provide the degree of comprehensiveness that you otherwise could.

When this will be addressed This will be addressed at your request/review or as required.

Page 9 of 62

Strategy Overview

Antoine Morel Du-Boil – Superannuation / Retirement

AMP Flexible Super – Super account

(Signature Super post October 1st)

$88,252.66

Investments

Super Easy Balanced

Rollover

CFS FirstChoice Wholesale Personal

Super

$1,500

Investments

100% CFS W/S Index Balanced

Personal Deductible Contribution

$30,000 drawdown from pension

Binding Non-lapsing Nominations

*Balance is net of initial plan fee

AMP Flexible Super – Retirement (Signature Super post October 1st)

account

$52,937.61

Investments

Super Easy Balanced

Pension Drawdown

$4,805

CFS FirstChoice Wholesale Personal

Pension

$135,482.77*

Investments

100% CFS W/S Index Balanced

Drawdown

$30,000 this FY

Pension Refresh

Conduct a pension refresh after re-

contribution leaving $1,500 in super

Binding Non-lapsing Nomination

Retain $1,500 in super and

rollover remaining balance

into pension account

Immediately

Page 10 of 62

Antoine Morel Du-Boil – Re-contribution Strategy

*Balance will depend on market fluctuations and

inclusive of the non-concessional contribution

FY 2022/23

CFS FirstChoice Wholesale Personal

Super

$1,500

Investments

100% CFS W/S Index Balanced

Personal Deductible Contribution

Minimum pension drawdown amount

Binding Non-lapsing Nominations

CFS FirstChoice Wholesale Personal

Pension

$147,307.77

Investments

100% CFS W/S Index Balanced

Re-contribute pension payment back

to super

Minimum pension drawdown

Pension Refresh

Conduct a pension refresh after re-

contribution leaving $1,500 in super

Binding Non-lapsing Nominations

Withdraw all funds from

both super and pension

and re-contribute back to

super through a NCC

Retain $1,500 in super and

rollover remaining balance

into pension account

CFS FirstChoice Wholesale Personal

Super

$1,500*

Investments

100% CFS W/S Index Balanced

Personal Deductible Contribution

$32,100 drawdown from pension

Non-concessional contribution

$10,325 (Tax savings from making a

personal deductible contribution last FY)

Binding Non-lapsing Nominations

CFS FirstChoice Wholesale Personal

Pension

$147,307.77*

Investments

100% CFS W/S Index Balanced

Drawdown

$32,100 FY2022/23

Binding Non-lapsing Nomination

Page 11 of 62

Antoine Morel Du-Boil – Future Recommendations

Remaining financial years until retirement at

age 70

Withdraw minimum required from allocated

pension each year and re-contribute into

super as personal deductible contribution

performing a pension refresh after each

financial year

Upon retirement at age 70

Hold all funds in allocated pension

Page 12 of 62

Our recommendations

Transfer more into your account-based pension Your retirement savings are currently held within a super accumulation account and an account-based

pension account. To transfer funds from your super into your pension account, you would first need to

transfer all the funds from your pension account into your super fund, before starting a new pension

account with the new balance.

To make sure you are in the most tax-effective position for retirement, we recommend you do the

following:

⎯ Transfer the full balance from your pension account to your super account.

⎯ Start a new pension account with the new balance.

1. Rollback the entire balance of your existing account-based pension to its accumulation phase, as per

the table below:

2. Once your rolled back pension benefits have been received, rollover the full balance of your existing

AMP Flexible Super – Super account to your recommended CFS FirstChoice Wholesale Personal Super,

as per the table below:

*Balance is the consolidated balance of your existing super and pension fund. This balance is net of the initial plan fee.

3. We recommend you retain $1,500 in your CFS FirstChoice Wholesale Personal Super.

We recommend you invest your CFS FirstChoice Wholesale Personal Super as follows:

CFS FirstChoice Wholesale Personal Super % $

CFS W/S Index Balanced 100.00% $1,500.00

Total 100.00% $1,500.00

We recommend you make a binding (non-lapsing) nomination on your super account in favour of your

preferred beneficiary or beneficiaries.

4. Once your rolled over super benefits have been received, roll over the majority of your recommended

CFS FirstChoice Wholesale Personal Super to your recommended CFS FirstChoice Wholesale Personal

Pension as per the table below:

Rollback from Amount Rollback to

AMP Flexible Super – Retirement Account (Signature Super post October 1st)

$52,937.61 AMP Flexible Super – Super

Account (Signature Super post October 1st)

Rollover from Amount Rollover to

AMP Flexible Super – Super Account (Signature Super post October 1st)

$136,982.77* CFS FirstChoice Wholesale

Personal Super

Rollover from Amount

CFS FirstChoice Wholesale Personal Super $1,500

Rollover from Amount Rollover to

CFS FirstChoice Wholesale Personal Super

$135,482.77* CFS FirstChoice Wholesale

Personal Pension

Page 13 of 62

We recommend you invest your CFS FirstChoice Wholesale Personal Pension as follows:

CFS FirstChoice Wholesale Personal Pension % $

CFS W/S Index Balanced 100.00% $135,482.77

Total 100.00% $135,482.77

5. Drawdown $30,000 for this financial year as pension payment from your recommended account-based

pension, as per the table below:

Furthermore, we recommend that:

⎯ We recommend your pension income be drawn from the CFS W/S Index Balanced investment.

Drawing your pension payment from the lowest risk underlying investment will minimise its

subjectivity to market volatility and will give the higher risk underlying investment options a

greater opportunity to grow without being drawn upon.

⎯ We recommend you make a binding (non-lapsing) nomination on your pension account in favour

of your preferred beneficiary or beneficiaries.

Benefits to you

▪ You will remain invested in line with your risk profile to ensure you still hold a sufficient level of growth

assets within your retirement savings. You will be maximising the funds you hold within the tax-free

environment of your allocated pension to further increase the growth of your funds.

▪ Drawing your pension payment from the cash account will ensure that your income payments are not

subject to market volatility and will give the market-linked investment options a greater opportunity to

grow without being drawn upon.

▪ As you are over 60 years of age, your pension payments will continue to be tax-free.

▪ As you will have a larger balance available in your pension account, this allows you to increase the

level of tax-effective income that you can draw.

Things to consider

▪ During the transfer process, your super will have time out of the market as the funds will need to be

sold down before the transfer can occur. During this time, you cannot take advantage of any positive

market fluctuations.

▪ A change in investments may alter the risk and/or return of your portfolio. When you invest, switch, or

withdraw all or part of your investment, a buy-sell or transaction fee may be charged by the fund

manager. Please refer to the Product Disclosure Statement for more information.

▪ Capital Gains Tax (CGT) may be incurred on the sale of your super investments if you follow our

recommendation. This may be reflected in the final balance available in your existing fund. We are

unable to estimate what the capital gain will be because your super fund does not provide information

that enables us to determine a potential gain or loss. We recommend you discuss CGT implications

with your tax adviser. We will not proceed with this transaction until you permit us to proceed.

▪ Unexpected earnings resulting in a taxable component can occur anytime there is a delay in moving

funds from super to pension phase.

Pension Payment Annual Amount Annual Amount

Minimum annual pension allowed (2.5% covid rate for this FY)

$3,387 The balance will depend on

market fluctuations

Maximum annual pension allowable (100%) $135,483 The balance will depend on

market fluctuations

Recommended pension drawdown $30,000 for this FY $32,100 for FY 2022/23

Page 14 of 62

▪ The amount able to be transferred into a retirement pension is capped at a total of $1.7 million.

Where total retirement pensions exceed this $1.7 million cap, the total value of these retirement

pensions will need to be reduced to comply with the cap. An ‘excess balance tax’ will otherwise apply.

▪ Where an individual accumulates superannuation amounts of more than $1.7 million, they can retain

this excess in a superannuation accumulation account. Alternatively, the excess can be removed

from the superannuation system and invested ‘outside’ of superannuation once a suitable condition of

release has been met.

▪ Once your pension has commenced, you will not be able to make additional contributions to your

balance. If additional contributions are required, your pension account will need to be rolled back to

super and restarted.

▪ By drawing a level of income higher than the minimum, you will be depleting your pension account

balance at a faster rate. This may impact your final retirement capital and hence the retirement

income you can achieve. However, it ensures you meet your current income need which is important

to you.

Page 15 of 62

Make a personal deductible contribution You would like to review the structure of your retirement savings to ensure you are structuring and

growing your funds in the most tax-efficient manner for your future retirement at age 70.

Between 2018/19 financial year to now, your total concessional contribution threshold over this period is

$75,000 – your concessional contribution cap is $25,000 per annum. You have made/received

contributions of $40,784.12 during this time, this means you have $34,215.88 of the unused cap.

We recommend that you contribute to super. The following table details our recommendation.

Make a personal deductible contribution

+We have anticipated your ongoing contributions based on your circumstances now. If any change were to occur, this advice may

not be appropriate for you. We recommend that we review your situation at least annually and prior to any further contributions

being made.

When you make a personal deductible contribution, you are contributing your after-tax dollars into your

super fund and claiming a tax deduction on the contributed amounts. Personal deductible super

contributions are a type of concessional contribution which is typically taxed at a maximum rate of 15%

when paid into your super fund.

We have agreed that the concessional contribution amount shown in the table above is the most you can

afford to contribute to your super without exceeding the concessional contribution cap.

We recommend the contributions be invested in line with your investment strategy.

Benefits to you

▪ You will be able to accumulate more wealth since earnings within super may be taxed at a lower rate

compared to investments outside of super. Any earnings derived from contributions into your super

are taxed at a maximum rate of 15%. This is typically a lower tax rate when compared to earnings

outside of super which is taxed at your marginal tax rate.

▪ You will benefit from an overall tax saving as your concessional contributions will be taxed at a rate of

15%, which is less than your marginal tax rate.

▪ Your contributions will not exceed the contribution cap; therefore, you will not be subject to any

excess cap penalties.

▪ You can use these funds to pay for your insurance premiums.

Things to consider

▪ The recommended contributions will have an impact on your cash flow.

▪ As your income is below $250,000 per annum, your concessional contributions will be taxed at a rate

of 15%.

Super fund Anticipated contribution+

CFS FirstChoice Wholesale Personal Super $30,000

Total $30,000

Page 16 of 62

The following scenario comparisons provide an illustration of the benefits and differences, with and

without making personal deductible contributions, and do not consider any other factors that may affect

your tax payable. This will bear the following savings on your tax amounts:

Taxable Income No Contribution With Contribution

Employment Income $75,000 $75,000

Allowable Deductions

- Personal Deductible

Contribution

- ($30,000)

Taxable income $75,000 $45,000

Tax Payable

Personal tax payable / (refundable) $15,262 $4,937

Contributions tax - $4,500

Total tax payable / (refundable) $15,262 $9,437

Personal Tax Savings - $10,325

Total Tax Savings - $5,825

Page 17 of 62

Make non-concessional contribution into super We recommend you to make a non-concessional contribution to super using the tax savings you get from

making a personal deductible contribution order to grow your retirement funds tax effectively. The

following table details our recommendation.

Make a lump-sum non-concessional contribution to super

*The non-concessional contribution made into super is equivalent to the tax-saving after making the personal deductible

contribution.

+We have anticipated your ongoing contributions based on your circumstances now. If any change were to occur, this advice may

not be appropriate for you. We recommend that we review your situation at least annually and prior to any further contributions

being made.

A non-concessional contribution involves you contributing your after-tax dollars into your super fund.

Since the tax has already been paid on your income, and you are not claiming a tax deduction on these

amounts, non-concessional contributions don’t get taxed when your super fund receives them.

We have agreed that the non-concessional amounts shown in the table above are the most you can

afford to contribute to your super.

We recommend the contributions be invested in line with your investment strategy.

Benefits to you

▪ You will be able to accumulate more wealth since earnings within super may be taxed at a lower rate

compared to investments outside of super. Any earnings derived from contributions into your super

are taxed at a maximum rate of 15%. This is typically a lower tax rate when compared to earnings

outside of super which is taxed at your marginal tax rate.

▪ Your contributions will not exceed the contribution cap; therefore, you will not be subject to any

excess cap penalties.

Things to consider

▪ A non-concessional contribution can only be made if your total superannuation balance is under $1.6

million as of 30 June of the previous financial year.

▪ Based on the information that you have provided to us, the recommended contribution amount is

within your relevant non-concessional contributions cap. There will be tax consequences for

contributions that exceed this cap. Please let us know if you have made any other non-concessional

contributions in this financial year or over the last two financial years that you have not told us about,

as this may affect our advice. Also, please first seek our advice before making contributions over our

recommendations. For information about contribution caps, please refer to the Product Disclosure

Statement.

▪ If you make excess non-concessional contributions, excess contributions tax may be payable.

However, you will be allowed to withdraw those excess contributions and 85% of an associated

earnings amount – calculated based on a formula. If this option is chosen, no excess contributions

tax will be payable, and the associated earnings will be taxed at your marginal tax rate, less a 15%

tax offset. If the excess contributions are left in the fund, they will be taxed at the top marginal tax rate

plus Medicare levy.

Super fund to contribute to Contribution*

FY 2022/23

CFS FirstChoice Wholesale Personal Super $10,325

Total $10,325

Page 18 of 62

Carry out a "pension refresh" of the recommended account-based pension Once the recommendations set above are implemented, we recommend you to carry out a pension

refresh of your account-based pension. To do this, you would first need to transfer all the funds from your

pension account into your super fund, before starting a pension account with the new balance (this is

known as a pension refresh strategy).

To make sure you are in the most tax-effective position for retirement, we recommend you do the

following:

1. Rollback the entire balance of your recommended CFS FirstChoice Wholesale Personal Pension to

your recommended CFS FirstChoice Wholesale Personal Super, as per the table below:

*Balance is net of $30,000 drawdown contributed into super as a personal deductible contribution.

2. We recommend you retain $1,500 in your CFS FirstChoice Wholesale Personal Super.

3. Once your rolled back pension benefits have been received, rollover majority of your super balance

to your recommended account-based pension, as per the table below:

*Balance is the remaining balance after retaining $1,500 in super. This balance is the consolidated balance of pension and super account.

We recommend you invest your pension and super funds in line with your investment strategy detailed in

the previous section. Your underlying pension and super funds will be invested in 100% CFS W/S Index

Balanced.

Benefits to you

▪ You will be refreshing your account annually to ensure you continue to hold as much funds possible

inside the allocated pension leading up to retirement.

▪ As you are over 60 years of age, your pension payments will continue to be tax-free.

Things to consider

▪ During the transfer process, your super will have time out of the market as the funds will need to be

sold down before the transfer can occur. During this time, you cannot take advantage of any positive

market fluctuations.

▪ A change in investments may alter the risk and/or return of your portfolio. When you invest, switch, or

withdraw all or part of your investment, a buy-sell or transaction fee may be charged by the fund

manager. Please refer to the Product Disclosure Statement for more information.

▪ Capital Gains Tax (CGT) may be incurred on the sale of your super investments if you follow our

recommendation. This may be reflected in the final balance available in your existing fund. We are

unable to estimate what the capital gain will be because your super fund does not provide information

that enables us to determine a potential gain or loss. We recommend you discuss CGT implications

with your tax adviser. We will not proceed with this transaction until you permit us to proceed.

Rollback from Amount Rollback to

CFS FirstChoice Wholesale Personal Pension

$105,482.77* CFS FirstChoice Wholesale

Personal Super

Rollover from Amount

CFS FirstChoice Wholesale Personal Super $1,500

Rollback from Amount Rollback to

CFS FirstChoice Wholesale Personal Super

$135,807.77* CFS FirstChoice Wholesale

Personal Pension

Page 19 of 62

▪ You are required to draw a minimum (currently 2.5%) pension payment from your account-based

pension every financial year.

▪ The minimum legislated amount of income that must be drawn:

⎯ Is calculated based on your age, and the value of your account-based pension when it

commences.

⎯ Is recalculated on 1 July each year based on the value of your account-based pension at that

time.

⎯ Will be pro-rata based on the number of days remaining in the financial year, where you have

started your pension on a day other than 1 July.

▪ Unexpected earnings resulting in a taxable component can occur anytime when there is a delay in

moving funds from the super to pension phase.

▪ The amount able to be transferred into a retirement pension is capped at a total of $1.6 million.

Where total retirement pensions exceed this $1.6 million cap, the total value of these retirement

pensions will need to be reduced to comply with the cap. An ‘excess balance tax’ will otherwise apply.

Transitional arrangements will apply for individuals as of 1 July 2017 if the excess capital in

retirement pensions is less than $100,000.

▪ Where an individual accumulates superannuation amounts of more than $1.6 million, they can retain

this excess in a superannuation accumulation account. Alternatively, the excess can be removed

from the superannuation system and invested ‘outside’ of superannuation once a suitable condition of

release has been met.

Page 20 of 62

Our recommendations for FY 2022/23

Make a personal deductible contribution You would like to review the structure of your retirement savings to ensure you are structuring and

growing your funds in the most tax-efficient manner for your future retirement at age 70.

We recommend that you contribute to super. The following table details our recommendation.

Make a personal deductible contribution

+We have anticipated your ongoing contributions based on your circumstances now. If any change were to occur, this advice may

not be appropriate for you. We recommend that we review your situation at least annually and prior to any further contributions

being made.

When you make a personal deductible contribution, you are contributing your after-tax dollars into your

super fund and claiming a tax deduction on the contributed amounts. Personal deductible super

contributions are a type of concessional contribution which is typically taxed at a maximum rate of 15%

when paid into your super fund.

We have agreed that the concessional contribution amount shown in the table above is the most you can

afford to contribute to your super.

We recommend the contributions be invested in line with your investment strategy.

Benefits to you

▪ You will be able to accumulate more wealth since earnings within super may be taxed at a lower rate

compared to investments outside of super. Any earnings derived from contributions into your super

are taxed at a maximum rate of 15%. This is typically a lower tax rate when compared to earnings

outside of super which is taxed at your marginal tax rate.

▪ You will benefit from an overall tax saving as your concessional contributions will be taxed at a rate of

15%, which is less than your marginal tax rate.

▪ Your contributions will not exceed the contribution cap; therefore, you will not be subject to any

excess cap penalties.

▪ You can use these funds to pay for your insurance premiums.

Things to consider

▪ The recommended contributions will have an impact on your cash flow.

▪ As your income is below $250,000 per annum, your concessional contributions will be taxed at a rate

of 15%.

Super fund Anticipated contribution+

CFS FirstChoice Wholesale Personal Super $32,100

Total $32,100

Page 21 of 62

The following scenario comparisons provide an illustration of the benefits and differences, with and

without making personal deductible contributions, and do not consider any other factors that may affect

your tax payable. This will bear the following savings on your tax amounts:

Taxable Income No Contribution With Contribution

Employment Income $77,100* $77,100*

Allowable Deductions

- Personal Deductible

Contribution

- ($32,100)

Taxable income $77,100* $45,000

Tax Payable

Personal tax payable / (refundable) $17,067 $6,111

Contributions tax - $4,815

Total tax payable / (refundable) $17,067 $10,926

Personal Tax Savings - $10,956

Total Tax Savings - $6,141

*We have assumed that your income is indexed at AWOTE. Awote rate is 2.80% per annum and is applied to all income annually.

Page 22 of 62

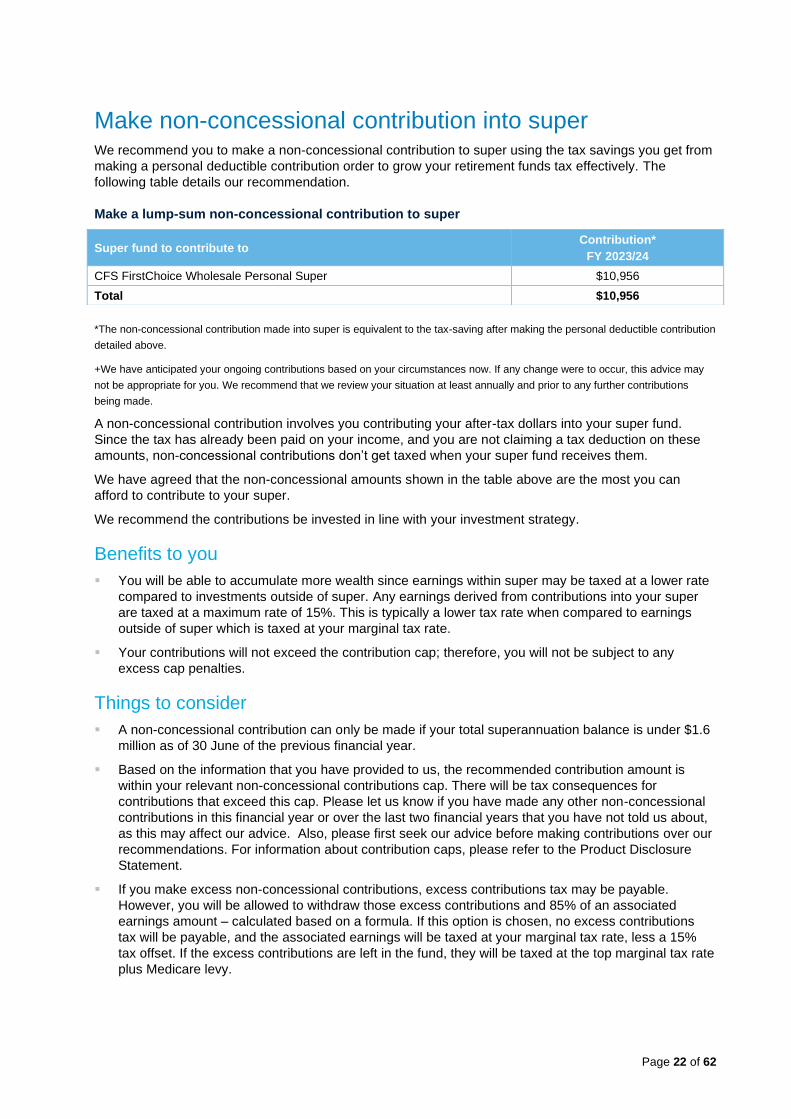

Make non-concessional contribution into super We recommend you to make a non-concessional contribution to super using the tax savings you get from

making a personal deductible contribution order to grow your retirement funds tax effectively. The

following table details our recommendation.

Make a lump-sum non-concessional contribution to super

*The non-concessional contribution made into super is equivalent to the tax-saving after making the personal deductible contribution

detailed above.

+We have anticipated your ongoing contributions based on your circumstances now. If any change were to occur, this advice may

not be appropriate for you. We recommend that we review your situation at least annually and prior to any further contributions

being made.

A non-concessional contribution involves you contributing your after-tax dollars into your super fund.

Since the tax has already been paid on your income, and you are not claiming a tax deduction on these

amounts, non-concessional contributions don’t get taxed when your super fund receives them.

We have agreed that the non-concessional amounts shown in the table above are the most you can

afford to contribute to your super.

We recommend the contributions be invested in line with your investment strategy.

Benefits to you

▪ You will be able to accumulate more wealth since earnings within super may be taxed at a lower rate

compared to investments outside of super. Any earnings derived from contributions into your super

are taxed at a maximum rate of 15%. This is typically a lower tax rate when compared to earnings

outside of super which is taxed at your marginal tax rate.

▪ Your contributions will not exceed the contribution cap; therefore, you will not be subject to any

excess cap penalties.

Things to consider

▪ A non-concessional contribution can only be made if your total superannuation balance is under $1.6

million as of 30 June of the previous financial year.

▪ Based on the information that you have provided to us, the recommended contribution amount is

within your relevant non-concessional contributions cap. There will be tax consequences for

contributions that exceed this cap. Please let us know if you have made any other non-concessional

contributions in this financial year or over the last two financial years that you have not told us about,

as this may affect our advice. Also, please first seek our advice before making contributions over our

recommendations. For information about contribution caps, please refer to the Product Disclosure

Statement.

▪ If you make excess non-concessional contributions, excess contributions tax may be payable.

However, you will be allowed to withdraw those excess contributions and 85% of an associated

earnings amount – calculated based on a formula. If this option is chosen, no excess contributions

tax will be payable, and the associated earnings will be taxed at your marginal tax rate, less a 15%

tax offset. If the excess contributions are left in the fund, they will be taxed at the top marginal tax rate

plus Medicare levy.

Super fund to contribute to Contribution*

FY 2023/24

CFS FirstChoice Wholesale Personal Super $10,956

Total $10,956

Page 23 of 62

Set up a super re-contribution strategy We have reviewed your situation and recommend you put in place a super re-contribution strategy using

your existing pension benefits. A super re-contribution strategy involves withdrawing a lump sum from

your pension balance and re-contributing this amount back into super as an after-tax contribution. This

will increase the tax-free portion of your pension balance.

To make sure you are in the most tax-effective position for retirement, we recommend you do the

following:

1. We recommend you roll back your pension to its accumulation phase, as detailed in the table below:

*Balance above does not consider investment growth. Balance is net of $32,100 drawdown contributed into super detailed in the section above.

2. We recommend you make a lump sum withdrawal from your super fund as follows:

*Balance above does not consider investment growth and is the consolidated balance of your pension and super balance (includes $1,500 balance in super, $32,100 concessional contribution, and $10,325 non-concessional contribution).

As you are over 60, the total lump sum super withdrawal will be tax-free.

3. Once the funds have been received in your bank account, we recommend you make an after-tax

contribution with the net withdrawal monies back to your CFS FirstChoice Wholesale Personal super

fund as follows:

Investment Amount

CFS FirstChoice Wholesale Personal Super $148,807.77

We recommend the contribution be invested in line with your investment strategy.

4. We recommend you to retain $1,500 in CFS FirstChoice Wholesale Personal Super detailed as

follows:

Investment Amount

CFS FirstChoice Wholesale Personal Super $1,500.00

5. We recommend you to rollover the remaining balance to the recommended CFS FirstChoice

Wholesale Personal Pension detailed as follows:

*Balance does not consider investment growth.

We recommend you invest your pension and super funds in line with your investment strategy detailed in

the previous section. Your underlying pension and super funds will be invested in 100% CFS W/S Index

Balanced.

Rollback from Amount Rollback to

CFS FirstChoice Wholesale Personal Pension

$104,882.77* CFS FirstChoice Wholesale

Personal Super

Super fund Member Lump-sum withdrawal

Super components Tax payable

(Tax-free) (Taxable)

CFS FirstChoice Wholesale Personal Super

Antoine $148,807.77 $0 $148,807.77 $0

Total $148,807.77* $0

Rollback from Amount Rollback to

CFS FirstChoice Wholesale Personal Super

$147,307.77* CFS FirstChoice Wholesale

Personal Pension

Page 24 of 62

Benefits to you

▪ The recommended strategy is designed to help you optimise the tax-free monies held within your

super funds.

▪ Converting more of your super benefits to a tax-free component will:

⎯ Increase the tax-free portion of your income stream payments, and reduce the amount included in

your assessable income when you commence a pension.

⎯ Give you estate planning benefits as your non-dependant beneficiaries will not have to pay tax on

the tax-free portion of the super benefits they receive if you were to die. The benefits of this

strategy to your beneficiaries are shown in the table below (based on today’s value of your super

benefit).

▪ Your contributions will not exceed the contribution cap; therefore, you will not be subject to any

excess cap penalties.

This table illustrates the expected impact of our advice on the taxable composition of your super.

Before our advice After our advice

Tax free component $0 $148,807.77

Taxable component $148,807.77 $0

Total balance $148,807.77 $148,807.77

Before our advice After our advice

Death benefit* $148,807.77 $148,807.77

Tax payable at 17% including Medicare Levy

$25,297.32 $0

Net proceeds $123,510.45 $148,807.77

*This amount will vary based on the account balance when you die. Balances do not include investment growth.

Things to consider

▪ Capital Gains Tax (CGT) may be incurred on the sale of your super investments if you follow our

recommendation. This may be reflected in the final balance available in your existing fund. We are

unable to estimate what the capital gain will be because your super fund does not provide information

that enables us to determine a potential gain or loss. We recommend you discuss CGT implications

with your tax adviser. We will not proceed with this transaction until you give us permission to

proceed.

▪ There may be costs in making a withdrawal from your super fund.

▪ The amount you contribute back into super will count towards your non-concessional contribution

cap.

Page 25 of 62

How we choose the right super and pension for you The right fund should provide you with the features you need to achieve your goals. To understand which

features would be important for you, we discussed your needs and considered your goals and personal

circumstances.

What do you want from your financial product

Owner How this meets your goals Available in

existing fund?

Superannuation/Pension features and benefits:

Index – low-cost investments that

simply track market returns with no

scope to outperform the market

Antoine You would like to invest in a simple low-

cost manner to minimise the fees on your retirement savings.

Yes

Type of investment:

Pooled – investments such as

managed funds Antoine

To allow you to invest in funds that can be tailored to your risk profile and low-

cost approach you are seeking.

Yes

Other

Facility to pay for advice fees from

your investments rather than your cash

flow

Antoine You would not like any advice to have any impact on your cash flow outside

super.

Yes

Superannuation only:

Access to non-lapsing binding nominations

Antoine You would like to ensure your benefits

are distributed in line with your wishes in the event of your passing.

Yes

A fund that accepts SG contributions, personal deductible contributions, and rollovers

Antoine

You would like to ensure your employer can continue to pay your SG whilst also allowing you to have the ability to make

your additional contributions

Yes

Access to a retirement income stream Antoine

You would like to maximise the level of funds you hold in the tax-free

environment of your allocated pension to maximise the growth of your savings.

Yes

Page 26 of 62

Future Recommendations

Carry out a "pension refresh" of your account-based pension on the remaining financial years until retirement We recommend you to withdraw the minimum required from the allocated-based pension from the cash

account each year and re-contribute it into super as a personal deductible contribution. We also

recommend you to perform a pension refresh after each financial year.

Benefits to you

▪ You will be refreshing your account annually to ensure you continue to hold as much funds possible

inside the allocated pension in the leading up to retirement.

▪ Drawing down your recommended pension payment (along with the other income you are currently

receiving), will allow you to meet your current income needs.

▪ As you are over 60 years of age, your pension payments will continue to be tax-free.

Things to consider

▪ You are required to draw a minimum (currently 2.5%) pension payment from your account-based

pension every financial year.

▪ The minimum legislated amount of income that must be drawn:

⎯ Is calculated based on your age, and the value of your account-based pension when it

commences.

⎯ Is recalculated on 1 July each year based on the value of your account-based pension at that

time.

⎯ Will be pro-rata based on the number of days remaining in the financial year, where you have

started your pension on a day other than 1 July.

▪ Unexpected earnings resulting in a taxable component can occur anytime when there is a delay in

moving funds from super to pension phase.

▪ The amount able to be transferred into a retirement pension is capped at a total of $1.6 million.

Where total retirement pensions exceed this $1.6 million cap, the total value of these retirement

pensions will need to be reduced to comply with the cap. An ‘excess balance tax’ will otherwise apply.

Transitional arrangements will apply for individuals as of 1 July 2017 if the excess capital in

retirement pensions is less than $100,000.

▪ Where an individual accumulates superannuation amounts of more than $1.6 million, they can retain

this excess in a superannuation accumulation account. Alternatively, the excess can be removed

from the superannuation system and invested ‘outside’ of superannuation once a suitable condition of

release has been met.

Page 27 of 62

Consolidate your retirement funds and set up a pension account We recommend you consolidate all of your funds into one account-based pension account upon reaching

age 70.

Benefits to you

▪ As you are over 60 years of age, your pension income will be tax-free.

▪ You will hold all of your funds within the tax-free environment of an allocated pension. You will

continue to invest in line with your growth appetite to ensure you are receiving sufficient growth over

the long term.

Things to consider

▪ Capital Gains Tax (CGT) may be incurred on the sale of your super investments if you follow our

recommendation. This may be reflected in the final balance available in your existing fund. We are

unable to estimate what the capital gain will be because your super fund does not provide information

that enables us to determine a potential gain or loss. We recommend you discuss CGT implications

with your tax adviser. We will not proceed with this transaction until you give us permission to

proceed.

▪ Unexpected earnings resulting in a taxable component can occur anytime there is a delay in moving

funds from the super to pension phase.

▪ Where you have accumulated superannuation amounts of more than $1.6 million, you can retain this

excess in a superannuation accumulation account. Alternatively, the excess can be removed from the

superannuation system and invested ‘outside’ of superannuation once a suitable condition of release

has been met.

▪ Once your pension has commenced, you will not be able to make additional contributions to your

balance. If additional contributions are required, your pension account will need to be rolled back to

super and restarted.

Page 28 of 62

Summary of your position after our advice

Antoine

Superannuation / Retirement income / Cashflow / Super contributions / Estate Planning (Limited to beneficiary nominations)

Goal

You would like to review the structure of your retirement savings to ensure you are structuring and growing your funds in the most tax-efficient manner for your future retirement at age 70. You would like to remain invested in line with your individual preferences, whilst exploring strategies to further grow your funds through fee and tax savings. You have no specific income needs in retirement and feel you will survive comfortably off the age pension. You, therefore, wish to ensure you are doing all you can to maximise the growth of your retirement savings

You would like to ensure your family will receive all of your superannuation benefits in event of your passing with minimal tax withheld

What we have recommended

We recommend you transfer more into your account-based pension through the following steps:

1. Rollback the entire balance of your existing account-based pension to its accumulation phase

2. Once your rolled back pension benefits have been received, rollover the full balance of your existing AMP Flexible Super – Super account to your recommended CFS FirstChoice Wholesale Personal Super

3. Retain $1,500 into your CFS FirstChoice Wholesale Personal Super and invest your funds in 100% CFS W/S Index Balanced

4. Once your rolled over super benefits have been received, roll over the majority of your recommended CFS FirstChoice Wholesale Personal Super to your recommended CFS FirstChoice Wholesale Personal Pension and invest your funds in 100% CFS W/S Index Balanced

5. Drawdown $30,000 for this financial year as pension payment

6. Drawdown $32,100 for FY 2022/23 as pension payment

We recommend you make a binding (non-lapsing) nomination on your super and pension account in favour of your preferred beneficiary or beneficiaries.

By utilising your un-used concessional contribution threshold, we recommend you make a $30,000 personal deductible contribution for this financial year to the recommended CFS FirstChoice Wholesale Personal Super.

We recommend you make a lump-sum non-concessional contribution amounting to $10,325.

For FY 2022/23, we recommend you to make a $32,100 personal deductible contribution to the recommended CFS FirstChoice Wholesale Personal Super.

For FY 2022/23, we recommend you to make a $10,956 non-concessional contribution to the recommended CFS FirstChoice Wholesale Personal Super.

Page 29 of 62

For FY 2022/23, we recommend you set up a super re-contribution strategy through the following steps:

1. We recommend you roll back your pension to its accumulation phase

2. We recommend you make a full lump sum withdrawal from your super fund

3. Once the funds have been received in your bank account, we recommend you make an after-tax contribution with the net withdrawal monies back to your CFS FirstChoice Wholesale Personal super fund

4. We recommend you to retain $1,500 in CFS FirstChoice Wholesale Personal Super invested in CFS W/S Index Balanced

5. We recommend you to rollover the remaining balance to the recommended CFS FirstChoice Wholesale Personal Pension invested in CFS W/S Index Balanced

For future recommendations:

- We recommend you to withdraw the minimum required from the allocated-based pension from the cash account each year and re-contribute it into super as a personal deductible contribution. We also recommend you to perform a pension refresh after each financial year.

- We recommend you consolidate all of your funds into one account-based pension account upon reaching age 70.

Benefits of our advice

You will remain invested in line with your risk profile to ensure you still hold a sufficient level of growth assets within your retirement savings. You will be maximising the funds you hold within the tax-free environment of your allocated pension to further increase the growth of your funds. You will begin to make personal deductible contributions each year to significantly reduce your taxable income and further aid in growing your retirement savings in a tax-efficient manner. You will be refreshing your account annually to ensure you continue to hold as much funds possible inside the allocated pension in the leading up to retirement.

You will now hold binding non-lapsing nominations on all of your funds. You will have also washed out all of the taxable components of your super prior to reaching age 67 to ensure that in the event of your children receiving your funds in event of your passing, no tax would be incurred on the receipt of your funds.

Your situation without our advice

You would continue to remain invested in line with your risk profile. However, you would not be optimising the structure of your retirement savings as you would hold a majority of your funds within the taxed environment of superannuation and not be using your annual pension drawdown in any manner to increase the growth of your retirement savings. You would not be making any personal contributions to reduce your taxable income and would therefore be paying higher rates of tax both inside and out of super.

You would continue to hold a non-binding nomination on your superannuation fund which does not guarantee your benefits will be distributed in line with your wishes in event of your passing. You will hold non-lapsing binding nominations on your allocated pension, whilst all of your funds would remain under the taxable component in the future and therefore if these funds were distributed to your non-dependent children in event of your passing they would incur 17% tax on the benefits.

Trade-offs

All investments carry risks. There is a possibility that their investments may not perform or even go down.

I have warned that there may be potential capital gains or losses, additional transactional cost, buy/sell cost, exit cost, etc. when simplifying and consolidating super funds.

In addition, you may lose potential return on investment while the funds are in transit between rollovers.

Page 30 of 62

Your investment strategy

We worked together to understand your expectations and how you feel about investment risk; your risk

profile. We then took your goals and timeframes into account to recommend an appropriate investment

strategy.

A well-developed investment strategy helps us to strategically regulate the allocation of your portfolio to

different asset classes, based on your personal circumstances, goals and the timeframes in which you

wish to achieve them.

Please refer to Selecting your investments on page 57 for more information on risk profiles, investment

strategies, different types of assets and the risks involved with investing.

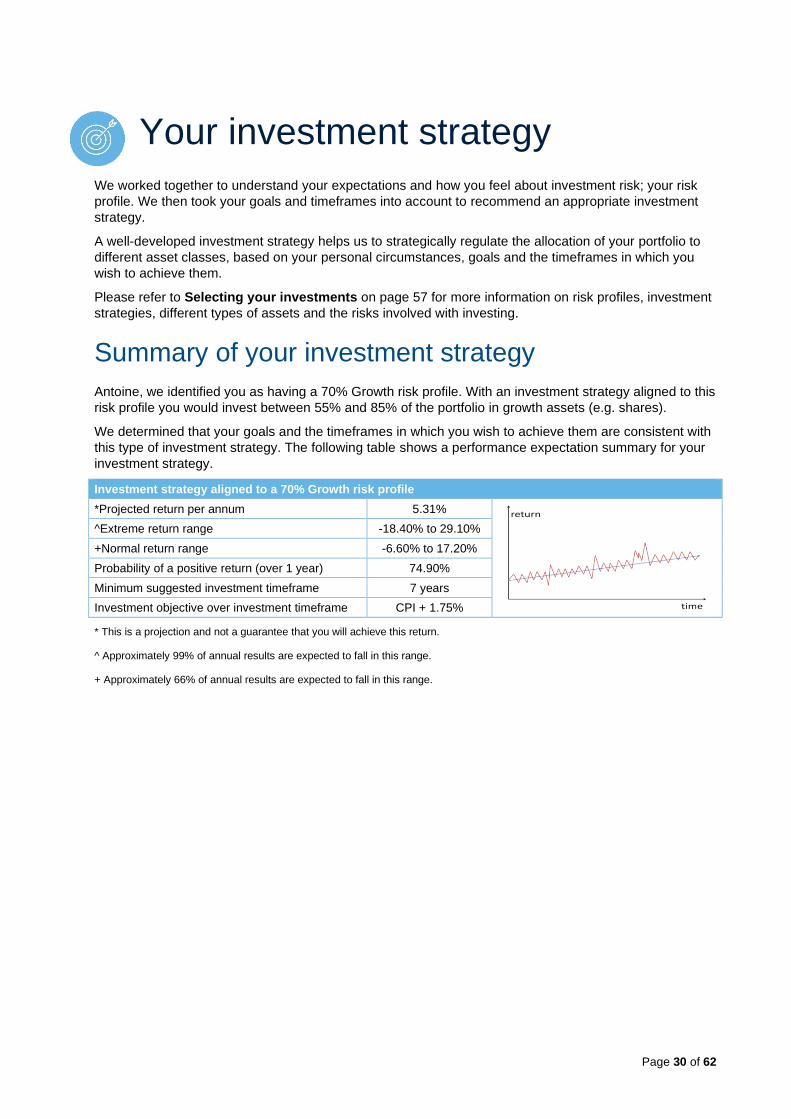

Summary of your investment strategy

Antoine, we identified you as having a 70% Growth risk profile. With an investment strategy aligned to this

risk profile you would invest between 55% and 85% of the portfolio in growth assets (e.g. shares).

We determined that your goals and the timeframes in which you wish to achieve them are consistent with

this type of investment strategy. The following table shows a performance expectation summary for your

investment strategy.

Investment strategy aligned to a 70% Growth risk profile

*Projected return per annum 5.31%

^Extreme return range -18.40% to 29.10%

+Normal return range -6.60% to 17.20%

Probability of a positive return (over 1 year) 74.90%

Minimum suggested investment timeframe 7 years

Investment objective over investment timeframe CPI + 1.75%

* This is a projection and not a guarantee that you will achieve this return.

^ Approximately 99% of annual results are expected to fall in this range.

+ Approximately 66% of annual results are expected to fall in this range.

Page 31 of 62

Your asset allocation

Our recommendations will result in your portfolio being allocated across the following investment assets:

Current

Asset class Actual $ Actual % Benchmark for

70% Growth risk profile

Variance

Australian Equities 34,069 24.13% 24.00% 0.13%

Australian Fixed Interest 11,380 8.06% 14.00% -5.94%

Cash 9,784 6.93% 5.00% 1.93%

Direct Property 0 0.00% 0.00% 0.00%

International Equities 52,763 37.37% 28.00% 9.37%

International Fixed Interest 10,900 7.72% 11.00% -3.28%

Other 9,982 7.07% 8.00% -0.93%

Property Securities/Infrastructure

12,312 8.72% 10.00% -1.28%

Total 141,190 100.00% 100.00%

*Other includes alternative assets which refer to any non-traditional assets that would not generally be found in a standard

investment portfolio. Due to the unconventional nature of some of these investments, they tend to be less liquid than traditional

investments. Examples of alternative assets include hedge funds, private equity and 'real' assets such as commodities and

agribusiness schemes.

The following table summarises your current asset allocation into ‘Defensive’ and ‘Growth’ assets.

Asset type Actual % Benchmark for 70% Growth risk profile

Variance

Defensive assets 22.71% 30.00% -7.29%

Growth assets 77.29% 70.00% 7.29%

Page 32 of 62

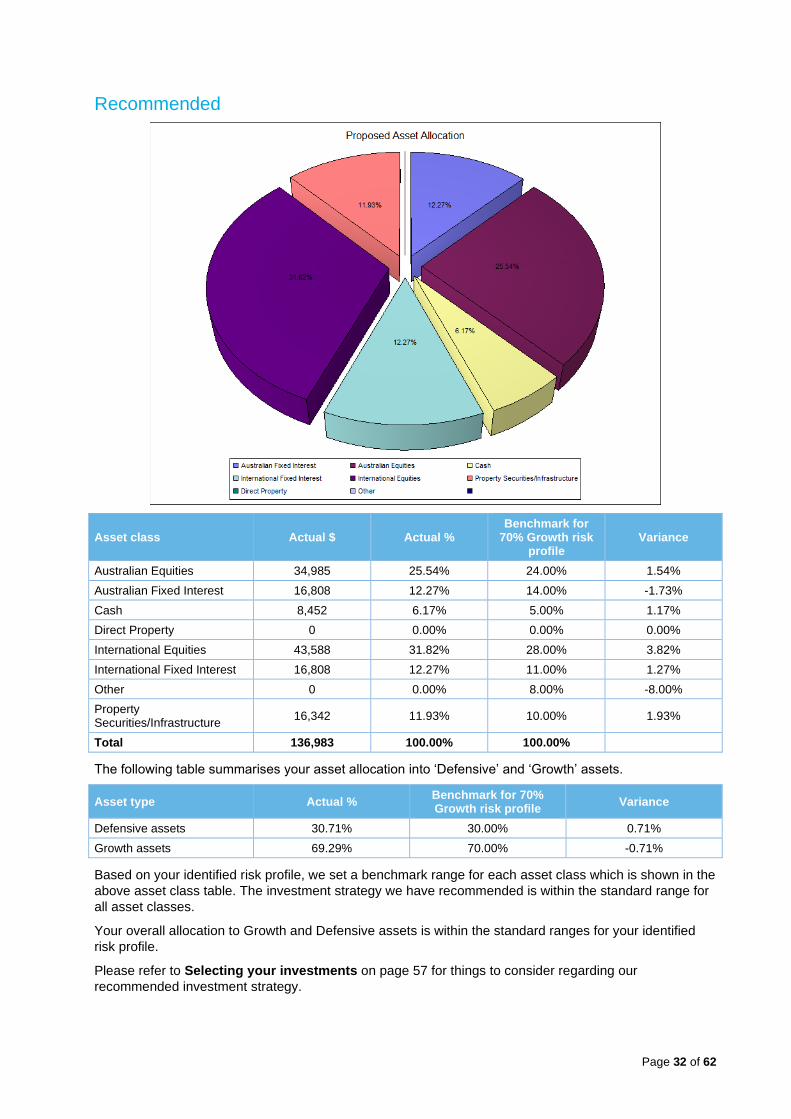

Recommended

Asset class Actual $ Actual % Benchmark for

70% Growth risk profile

Variance

Australian Equities 34,985 25.54% 24.00% 1.54%

Australian Fixed Interest 16,808 12.27% 14.00% -1.73%

Cash 8,452 6.17% 5.00% 1.17%

Direct Property 0 0.00% 0.00% 0.00%

International Equities 43,588 31.82% 28.00% 3.82%

International Fixed Interest 16,808 12.27% 11.00% 1.27%

Other 0 0.00% 8.00% -8.00%

Property Securities/Infrastructure

16,342 11.93% 10.00% 1.93%

Total 136,983 100.00% 100.00%

The following table summarises your asset allocation into ‘Defensive’ and ‘Growth’ assets.

Asset type Actual % Benchmark for 70% Growth risk profile

Variance

Defensive assets 30.71% 30.00% 0.71%

Growth assets 69.29% 70.00% -0.71%

Based on your identified risk profile, we set a benchmark range for each asset class which is shown in the

above asset class table. The investment strategy we have recommended is within the standard range for

all asset classes.

Your overall allocation to Growth and Defensive assets is within the standard ranges for your identified

risk profile.

Please refer to Selecting your investments on page 57 for things to consider regarding our

recommended investment strategy.

Page 33 of 62

Summary of your products

The products we recommend are an important part of your financial strategy.

Your investments

The following table shows the investment products we have recommended. The investment management

costs shown in the table may not be inclusive of other costs such as product administration fees. Please

refer to Cost of your products on page 38 for costs and fees of the recommended products.

Your super

Status Product amount Investment

management cost

Antoine's superannuation

CFS FirstChoice Wholesale Personal Super New

CFS W/S Index Balanced New 100.00% $1,500.00 0.15% $2.00

Subtotal 100.00% $1,500.00

Total $1,500.00

Your pension

Status Product amount Investment

management cost

Antoine's pension

CFS FirstChoice Wholesale Personal Pension New

CFS W/S Index Balanced New 100.00% $135,482.77 0.15% $203.00

Subtotal 100.00% $135,482.77

Total $135,482.77

CFS FirstChoice Wholesale Personal

CFS FirstChoice Wholesale Personal Super and Pension provides you with easy access to a wide range

of managed funds, shares and cash. Along with streamlined administration, you’ll benefit from extensive

online reporting, giving you more control of your investments.

Please refer to the Product Disclosure Statement for full details.

Page 34 of 62

Cost of replacing your investments We have made recommendations to replace your investments. As a result, you may incur exit and entry

costs and the ongoing fees you pay may change.

Initial product costs

The following tables show the net amount of your investments that will be available for transfer and for

investment, after deducting exit and entry costs.

Existing investments Initial amount Exit fees Brokerage Net amount available for

transfer

Antoine

AMP Flexible Super - Super account (Signature Super post October 1st)

$84,045.16* $0.00 $0.00 $84,045.16*

AMP Flexible Super – Retirement account (Signature Super post October 1st)

$52,937.61 $0.00 $0.00 $52,937.61

Recommended investments Initial amount Entry fees Brokerage Net amount available for investment

CFS FirstChoice Wholesale Personal Super $1,500.00 $0.00 $0.00 $1,500.00

CFS FirstChoice Wholesale Personal Pension

$135,482.77 $0.00 $0.00 $135,482.77

*Balance is net of initial plan fee.

Buy/sell costs

Buy/sell costs may apply, including for underlying managed funds held within managed portfolios which

you may own. Buy/Sell costs are the difference between the entry price and exit price of units and apply

when you buy or sell units. The spread is an estimate of the transaction costs of buying and selling assets

relating to your investment option. For example, on an investment in a managed fund of $1,000, if the

spread is 0.25%, the impact on your investment balance is a reduction of $2.50.

The buy/sell spreads apply for each recommended investment product option and are set out in the Product Disclosure Statement.

Capital gains tax (CGT)

Capital gains tax (CGT) may be incurred on the sale of investments currently held in your funds. CGT is payable on any gains made when selling the underlying investments in your current funds. This may be reflected in the final balance available from your existing fund. We recommend you discuss CGT implications with your tax adviser.

Page 35 of 62

Ongoing cost comparison

The tables below compare the estimated annual cost of the products you have now and the products we

recommend. They compare what we actually recommend against what your position would be if you were

to consolidate into one of your existing products.

We’ve assumed that the underlying investments in your existing products are invested in line with what

we have recommended in your new products. This is to diminish the variance in cost caused by differing

underlying investment options.

The following table shows the ongoing cost comparison for your super.

Before vs after comparison

Ongoing costs Existing Existing Recommended Recommended

Product name

AMP Flexible Super – Super account (Signature Super post October 1st)

AMP Flexible Super – Retirement

account (Signature Super post October

1st)

CFS FirstChoice Wholesale

Personal Super

CFS FirstChoice Wholesale

Personal Pension

Investment option Super Easy Balanced

Super Easy Balanced

CFS W/S Index Balanced

CFS W/S Index Balanced

Balance $88,253 $52,938 $1,500 $135,483*

Member + Admin fees $91 $91 $3 $253

Management fees $635 (0.72%) $381 (0.72%) $2 (0.15%) $203 (0.15%)

Less product rebates (% pa of investmenet

balance) $0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%)

Other fees $0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%)

Total cost $726 $472 $5 $456

$1,198 $461

Features 9 Investment

Options 4 Investment

Options 161 Investment

Options

162 Investment

Options

*Balance is net of initial plan fee.

Page 36 of 62

Like for like comparison (Super)

Ongoing costs Considered Considered Considered Considered Recommended

Product name

AMP Signature Super –

Essential Protection

AMP Flexible Super – Super

account (Signature Super post October 1st)

AMP MyNorth Super

MLC Wrap Super Series 2

- Full

CFS FirstChoice Wholesale Personal

Super

Investment option

AMP Balanced Index

Super Easy Balanced

MyNorth Index Balanced

Vanguard Growth Index

CFS W/S Index Balanced

Balance $1,500 $1,500 $1,500 $1,500 $1,500

Member + Admin fees

$82 $91 $91 $375 $3

Management fees $4 (0.26%) $11 (0.72%) $8 (0.56%) $4 (0.29%) $2 (0.15%)

Less product rebates (% pa of

investmenet balance)

$0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%)

Other fees $0 (0.00%) $0 (0.00%) $0 (0.00%) $1 (0.04%) $0 (0.00%)

Total cost $86 $102 $99 $380 $5

Features 41 Investment

Options 9 Investment

Options 431 Investment

Options 439 Investment

Options 161 Investment

Options

Page 37 of 62

Like for like comparison (Pension)

Ongoing costs Considered Considered Considered Considered Recommended

Product name

AMP Signature Super –

Allocated Pension

AMP Flexible Super –

Retirement account

(Signature Super post October 1st)

AMP MyNorth Pension

MLC Wrap Super Series 2

- Full

CFS FirstChoice Wholesale Personal Pension

Investment option

AMP Balanced Index

Super Easy Balanced

MyNorth Index Balanced

Vanguard Growth Index

CFS W/S Index Balanced

Balance $135,483* $135,483* $135,483* $135,483* $135,483*

Member + Admin fees

$471 $91 $91 $677 $253

Management fees $352 (0.26%) $975 (0.72%) $759 (0.56%) $393 (0.29%) $203 (0.15%)

Less product rebates (% pa of

investmenet balance)

$0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%) $0 (0.00%)

Other fees $0 (0.00%) $0 (0.00%) $0 (0.00%) $57 (0.04%) $0 (0.00%)

Total cost $823 $1,066 $850 $1,127 $456

Features 35 Investment

Options 4 Investment

Options 431 Investment

Options 439 Investment

Options 162 Investment

Options

*Balance is net of initial plan fee.

The above table(s) compares the ongoing product fees and costs for your existing and our recommended products based on the

relevant Product Disclosure Statement (PDS). If comparing a super wrap platform product with a non-platform super product, this

comparison is unlikely to be on a ‘like for like’ basis as the fee and cost amounts disclosed for managed funds offered on platform

products may not include certain transaction costs which are required to be included for non-platform super products. When

deciding whether to implement our advice, you should consider the ongoing product fees and costs as disclosed in the relevant PDS

and the features offered.

+ Investment management costs may include investment fees, performance fees, indirect costs (including any performance based

fees charged by the underlying investment managers), and other management costs. Investment management costs are calculated

based on the gross account balance after any initial fees. Where multiple investment options or investment products exist, this fee is

a weighted average of the applicable fees. Please refer to the relevant Product Disclosure Statements for further details.

^ The ongoing investment costs shown does not take into account any transaction fees.

Page 38 of 62

Cost of your products The table below summarises the costs and fees of the products we have recommended.

Your investment products

Initial cost to you

($)

Ongoing annual cost to you ($)

Total product costs 0.00 461.00

Details of your initial product costs

Type of fee Product amounts Costs to you

$ % $

Investment products Amount invested ($)

Ownership - Antoine

CFS FirstChoice Wholesale Personal Super

Initial contribution fee 1,500.00 0.00% 0.00

SG Contribution 7,500.00 0.00% 0.00

Personal Deductible Contribution 30,000.00 0.00% 0.00

CFS FirstChoice Wholesale Personal Pension

Initial contribution fee 135,482.77 0.00% 0.00

Investment products - Total 0.00

All products - Total initial product fees 0.00

Additional contributions to your investment

Any additional contributions not identified in the table above will be charged the contribution fee at the

same rate as shown above for the product.

Page 39 of 62

Details of your ongoing product costs

The costs can be charged as a fixed dollar amount or as a percentage of your relevant product balance.

They are calculated throughout the year and, if a fee is charged as a percentage, the amount of the fee

depends on the product balance within your investment, policy or loan at the time. The amounts below

are examples of ongoing fees charged over 12 months, assuming your balance was the same as your

initial investment, policy or loan. The actual amounts will be different. The figures should be used only as

a guide and are not the actual charges that will be made. Please note that the investment balances do not

take buy/sell spread into consideration.

Type of fee Product amounts Costs to you

$ % $

Investment Products Amount invested ($)

Ownership - Antoine

CFS FirstChoice Wholesale Personal Super

Administration fee- 1,500.00 N/A 3.00

Investment management costs* 1,500.00 0.15% 2.00

CFS FirstChoice Wholesale Personal Pension

Administration fee- 135,482.77 N/A 253.00

Investment management costs* 135,482.77 0.15% 203.00

Investment products - Total 461.00

* Investment management costs may include investment fees, performance fees, indirect costs (including any performance based

fees charged by the underlying investment managers), and other management costs. Investment management costs are calculated

based on the gross account balance after any initial fees. Where multiple investment options or investment products exist, this fee is

a weighted average of the applicable fees. Please refer to the relevant Product Disclosure Statements for further details.

Page 40 of 62

Staying on track to meet your goals

It’s important to review your situation regularly because it’s difficult to predict when things will change. It’s

equally hard to predict the effect that these changes will have on your goals and our advice.

There are also particular areas of your advice that should be reconsidered over time.

Your adviser

Joshua Lee

Level 1, 689 Burke Road, Camberwell, VIC 3124

03 9038 8267 | [email protected]

www.linkwealth.com.au

Financial Adviser of Link Wealth Group Pty Ltd

trading as Link Wealth Group Pty Ltd

ABN 98 157 712 055

Authorised Representatives of AMP Financial

Planning Pty Limited

ABN 89 051 208 327

Australian Financial Services Licensee and

Australian Credit Licensee

Licence No: 232706

Member of the AMP Group