A social science that studies the allocation of scarce to agricultural economics.pdf · A social...

60

Transcript of A social science that studies the allocation of scarce to agricultural economics.pdf · A social...

A social science that studies the allocation of scarce

resources used to produce the goods and services that

satisfy unlimited consumer wants and needs .

Factors of production, or "inputs"

• Land

• Capital

• Labor

• Entrepreneurship

(Management)

• All raw materials available in nature, i.e. coal, wood,

crude oil, iron, fish, etc.

• The raw materials found in nature are called natural

resources.

• Natural resources become factors of production when we

use them to produce goods.

• Some resources, like wheat and cattle, are renewable.

they can be reproduced.

• Other resources are limited, or nonrenewable, like coal,

iron, and crude oil.

• The amount of natural resources available to a society

has a direct effect on its economy.

• Man-made resources used for further production

(used to produce other goods and services).

• Examples: machines, buildings, tools

• Features:

– Man made

– It raises the productivity of other factors

All the human physical and mental skills that can be used

in the production of goods and services.

• Measured in terms of time (man hour)

• Labour supply = no. of workers x no. of working hours

per worker

• Factors affecting labour supply:

– Size of population

– Size of working population

– No. of working hours

Labour Supply:

– population growth (by natural growth or immigration)

– monetary rewards

– import of labour from other countries

– retirement age (e.g. from 65 to 70)

– school leaving age (e.g. from 17 to 16)

• Measured in terms of output per unit of labour

Average labour productivity = average output per man hour

April 2016 Firm A Firm B

Number of working hours per worker 240 180

Units of output 7200 6400

Average labour productivity 30 35.6

Firm B has a higher labour productivity than firm A

• Better education and training

• Other factors of production (quantity & quality)

• Better management or organization

• Better working conditions

• Greater fringe benefits (housing allowances, medical care,bonus, meal.)

• Geographical mobility: the case at which labor can move

from one working place to another.

• Occupational mobility: the case at which labor can change

from one type of job to another.

Also known as Management.

The ability to organize production, innovate, and take

risks. Ability to collect information, and analyze that

information to solve problems or create opportunities.

• Takes the initiative in combining land, labor, and capital

in order to produce a good or service.

• Undertakes basic decision-making for the business.

• Takes risk of losing money or going bankrupt.

• Forms a business and introduces new products and

techniques of production.

• Land receives Rent

• Capital receives Interest

• Labor receives Wages

• Management receives Profit

• Factors of production are used to produce things that

people want.

• These "things" are known as commodities. Commodities

consist of goods and services.

Economic Goods: Tangible items in which the quantity demanded by

society exceeds the quantity available at a price equal to zero.

Qd > Qs @ P = 0

Free Goods: Tangible items in which the quantity available

exceeds the quantity demanded at a price equal to zero.

Qd < Qs @ P = 0

Consumer Goods: Are economic goods used directly by

consumers to generate satisfaction. (Durable Goods, Non-

durable Goods).

Capital Goods: Man-made goods used to produce consumer

goods.

Services are intangibles such as mowing, education, tractor

repair, landscape planning, hair cuts, etc.

• Scarcity forces every economic system, every

business, every individual to make choices.

• A decision to produce one commodity frequently

implies a decision to produce less of another

commodity (production possibilities curve).

Scarcity simply means that there is not enough factors of

production in the world to create all of the goods and

serv ices that peop le des i re a t a Price = 0 .

Three core issues must be resolved

• What to produce?

• How to produce?

• For whom to produce?

How will these scarce resources be used ?

(1) Will we use crude oil to make gasoline, plastics, fertilizers

etc.

(2) Use fertilizer to raise corn, soybeans, tobacco, cotton etc.

(3) Use corn to feed people, feed hogs to produce pork, feed

beef cattle to produce beef, feed dairy cattle to produce

milk.

• Often, the decision to produce a particular

commodity may lead to the decision to completely

stop production of another.

• In other words, some tradeoffs must be made since

we do not have the resources to produce the variety

and quantity of commodities we would like to

produce.

Limited Resources & Unlimited Wants

Scarcity

Choices

Opportunity Cost

Whenever resources are used for any activity, the user is

trading off the opportunity to use those resources for

other things.

The value of the trade-off is represented by the

opportunity cost.

Opportunity Cost = Value of best foregone alternative

• Opportunity cost of any choice - What we forego when we make that choice

Opportunity cost graphically:

The production possibilities curve (PPC)

represents all possible combinations of total

output that could be produced assuming

• There is a fixed amount of productive resources for the

time period

• The efficient use of those resources

• Resources are fully employed

• Production is for a specific time period

• Technology does not change over the time period

Each point on the production

possibilities curve depicts an

alternative mix of output

The PPC is bow outward

because of the law of

increasing relative cost

Point R lies outside the PPC

and is impossible to achieve

during the time period

assumed.

If the nation is at point

S, it means that its resources

are not being fully utilized.

We have unemployment.

Point S is called an

inefficient point, which

is defined as any point

below the PPC.

Production possibilities curve illustrates

two essential principles:

1-Scarce resources

2-Opportunity costs

Attainable

Unattainable

• Show the different combinations of goods and

services that can be produced with a given amount of

resources.

• No „ideal‟ point on the curve.

• Any point inside the curve – suggests resources are

not being utilised efficiently.

• Any point outside the curve – not attainable with the

current level of resources.

• Useful to demonstrate economic growth and

opportunity cost.

• The reason that we face the law of increasingrelative cost (which causes the PPC to bowoutward) is that certain resources are better suitedfor production of some goods than they are forother goods.

• Specialization

– Method of production in which each firm concentrates on a

limited number of activities

• Exchange

– Practice of trading with others to obtain what we want

• Allows for

– Greater production

– Higher living standards than otherwise possible

• Agricultural Economics is a branch of economics in which

the principles and methods of economics are applied to

the agriculture industry.

• The problem of the scarcity has the vital importance in

agriculture economics too because Land is limited and it

is impossible to increase land with the help of human

efforts. Keeping this fact in mind, the land should be

utilized in such a way that we obtain the maximum

production from it that result in the satisfaction of human

being.

The agriculture sector has the following main areas:

1. Crops Production

2. Fruits Production

3. Forestry

4. Live stocks

5. Poultry farming

6. Bees Keeping

7. Fisheries

Why

Agriculture Economics

as a

Separate Discipline

Agriculture sector is different than industrial sector in various

ways. In the coming slides we will compare the agriculture and

Industrial sector which lead us to the conclusion that

agriculture economics should be studied as a separate

discipline.

• In industrial production, from a small piece of land, with the

help of huge investment, plant is constructed that can

produce bulks of production on every production floor. But

in agriculture beside the Labor and Capital, a large area of

land is required to increase the agriculture production.

Proportion of Land use

• Various agricultural products have common supply such as

with wheat the supply of straw, with meat the supply of skin

increases. But in industry it is not common.

Common Production

• The supply of industrial products can change with the

change in prices in the market, but the supply of agricultural

products can not be increase. It has an inelastic supply.

Inelastic Supply

• The goods produced by agriculture and industrial

sectors are different. The agricultural products are

mostly perishable while industrial products are mostly

durable. Hence, the need for a separate study on the

part of agriculture economics rise.

• The weather change has a serious effect on the

agricultural production and that is the reason due

to which agricultural production is either surplus or

shortage while industrial production is free from the

weather changes.

• In agriculture, the labor are unorganized. They get wages

below the subsistence level. Hence the financial position of

labor is very weak.

• On the contrary, the industrial labor is well-organized. They

get better wages. They formulate their unions.

• Because of non-existence of trade unions in agri sector, the

relationship between the land-owner and the tillers remains

stable, though the agri workers get lower wages.

• Generally, the government of LDCs are crazy to

industrialize themselves as soon as possible. For this

purpose, they give certain facilities to the industrialists.

Moreover, the industrial sector is provided benefits in the

form of cheaper loans, tax holidays, better means of

transportation and communication. In such situation, the

problems and issues of agri sector will be different from

industrial sectors. Therefore, to deal with them, agriculture

economics will be needed.

Author: Kamil Maitah

Suprvisor: Ing. Jiří Mach, Ph.D.

Content

Introduction.

The objectives.

The Methodology.

World crude oil reserves, production and price develpment.

Saudi Arabia crude oil production.

The impact of crude oil price fluctuations on Saudi Arabian

economy.

Conclusions.

Introduction

Contemporary society has been built on crude

oil.

Crude oil is essentially vital to the world

economy.

It is not just the non-renewable resource, but as

well the "strategic resource”.

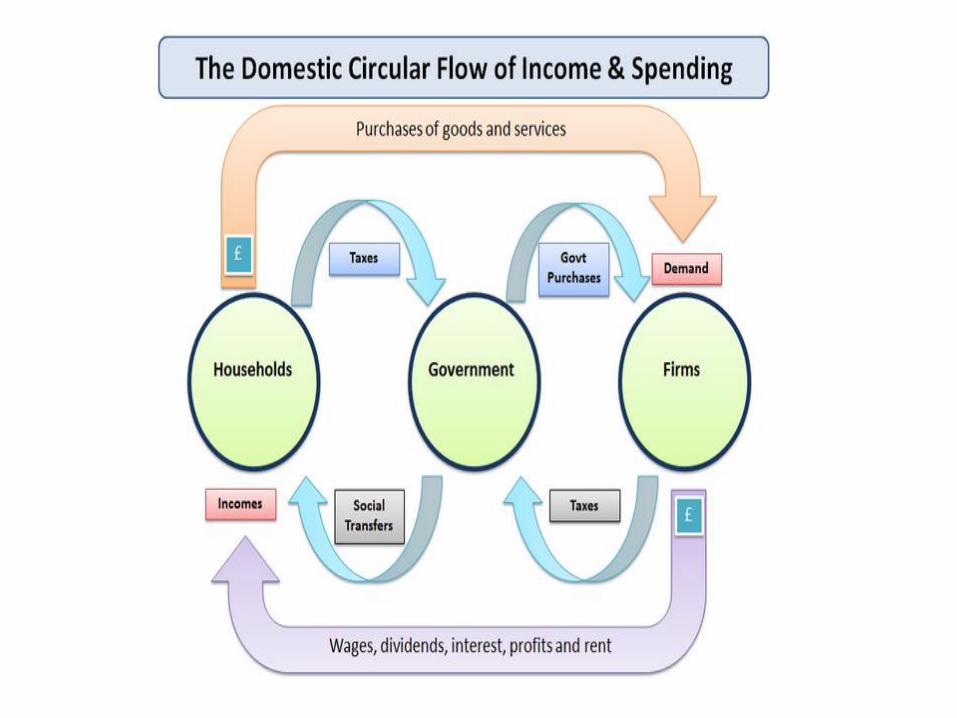

A- Households supply

resources in the resource

market and demand goods and

services in the product market

B- Firms supply goods and

services in product market and

demand resources in the

resource market

C- Money flows in resource

market determine wages,

interest, rents, and profits

which flow as income to

households

D- Product markets determine

the prices for goods and

services which flow as revenue

to firms

• The resource market coordinates the actions of businesses demanding resources and households supplying them in exchange for income.

• The loanable funds marketbrings net household saving and the net inflow of foreign capital into balance with the borrowing of businesses and governments.

• The foreign exchange marketbrings the purchases (imports)from foreigners into balance with the sales (exports plus net inflow of capital) to them.

• The goods & services marketcoordinates the demand for and supply of domestic production (GDP).

There are four kinds of policy that the government has used

to influence the macroeconomy:

1. Fiscal policy

2. Monetary policy

3. Growth or supply-side policies

4. Trade policy

Real-Nominal PRINCIPLE

What matters to people is the real value of

money or income - its purchasing power - not

the “face” value of money or income.

• The term "real" means adjusted for inflation.

• Nominal GDP is a measure of national output based on the

current prices of goods and services. It is also called “money GDP”.

• Real GDP is a measure of the quantity of final goods and services

produced, obtained by eliminating the influence of price changes

from nominal GDP.

• Inflation is an increase in the overall price level of goods

and services in an economy over a period of time.

• When the general price level rises, each unit of currency

buys fewer goods and services (purchasing power is falling).

• Due to inflation the value of 1 USD today is more than 1

USD in the future.

• Inflation is adjusted for by using real values instead of

current values.

Interest rate is a rate which is charged or paid for

the use of money.

• Provides incentives ... to consumers, producers, labor and owners of productive resources

• Allocate resources ... alternative ways to provide goods and services

Rate at which one currency may be converted into

another. The exchange rate is used when simply

converting one currency to another (such as for the

purposes of travel to another country), or for engaging in

speculation or trading in the foreign exchange market.