a. Social Responsibility b. Environment PASSION FOR...

123

Table of Contents 1. AmBev 2. Highlights 3. Message to shareholders 02 4. Map of Operations 04 5. Beer Brazil 07 6. Soft Drinks Brazil 11 7. Hispanic Latin America (HILA) 15 8. North America 19 9. Passion for Execution 23 10. Brands 26 11. Distribution 29 12. Cost Consciousness 33 13. Financial Discipline 36 14. Culture 38 15. AmBev People 42 16. Sustainability 47 a. Social Responsibility 48 b. Environment 52 c. Corporate Governance 56 17. Shares as an Investment 59 18. Our Team 60 19. Financial Section 62 2005 Annual Report 2005 Annual Report PASSION FOR EXECUTION

Transcript of a. Social Responsibility b. Environment PASSION FOR...

Table of Contents

1. AmBev2. Highlights3. Message to shareholders 024. Map of Operations 045. Beer Brazil 076. Soft Drinks Brazil 117. Hispanic Latin America (HILA) 158. North America 199. Passion for Execution 23

10. Brands 2611. Distribution 2912. Cost Consciousness 3313. Financial Discipline 3614. Culture 3815. AmBev People 4216. Sustainability 47

a. Social Responsibility 48b. Environment 52c. Corporate Governance 56

17. Shares as an Investment 5918. Our Team 6019. Financial Section 62

2005 Annual Report

2005A

nnual Report

PASSION FOR EXECUTION

AmBev

Present in 14 countriesof the Americas AmBev is the largest consumer goods company in Braziland Latin America’s largest brewer, with operations in 14 countries in the three Americas. Based upon a globalalliance with InBev, as of 2004 we became part of the world’s largest platform for the production andmarketing of beer. This association also made it possiblefor us to enter North America through the incorporationof the Canadian brewer Labatt and the internationalexpansion of the Brahma brand to 15 countries in Europeand North America, for a total presence in 23 countries.

Created in 1999 through the merger of the Brahma andAntarctica brewing companies, AmBev has the largestbeverage portfolio in Brazil, including the Brahma,Antarctica, Skol and Bohemia brands, as well as softdrinks, the Gatorade isotonic beverage, Lipton teas andFratelli Vita bottled water. Among our stable of softdrinks, of particular note are Guaraná Antarctica,produced from a typical Amazonian fruit, and Pepsi-Cola.

In 2005, approximately 30% of our EBTIDA derived fromour Hispanic Latin American operations and Canada.Besides Brazil, we also are the market leader inArgentina, Bolivia, Paraguay and Uruguay.

This leadership is the result of our Passion for Execution,for always doing more regarding everything that involvesour business – and always doing it better, by imposingchallenging targets upon ourselves and being able tocount on a team made up of the most talentedprofessionals in the market.

Highlights 2004 2005 Variation

R$ million R$ million %

Income statmentNet Revenues 12,007 15,959 32.9%Gross Earnings 7,226 10,216 41.4%General and Administrative Expenses 3,611 5,174 43.3%EBIT 3,615 5,043 39.5%Net Earnings 1,162 1,546 33.1%

Balance SheetTotal Assets 33,017 33,493 1.4%Cash and cash equivalents 1,505 1,096 -27.2%Total Debt 7,811 7,204 -7.8%Net Equity 16,976 19,867 17.0%

Cash Flow and Profitability EBITDA (R$ million) 4,537 6,305 39.0%EBITDA Margin 37.8% 39.5% 1.7 ppCapital Expenditures (R$ million) 1,274 1,370 7.5%Return on Equity (%) 10.8% 7.8% - 3 pp

Share information (R$/ thousand shares)Book Value (*) 258.97 304.03 17.4%Earnings per Share (*) 17.72 23.65 33.5%Dividends (ON) 20.86 23.07 10.6%Dividends (PN) 22.95 25.38 10.6%Payout of Dividends 114.0% 109.0% -5 pp

CapitalizationMarket Capitalization (R$ million) 40,424 53,646 32.7%Net Debt (R$ million) 6,305 6,107 -3.1%Minority Stakes (R$ million) 219 123 - 43.9%Shares in Circulation (thou.) (*) 65,553 65,346 -0.3%Equivalent ADRs (thou.) (*) 655.5 653.5 -0.3%

* Values adjusted for the share bonus issued on May 31. 2005

0

0.5

1.0

1.5

20

02

20

03

20

04

20

05

1,4

12

1,1

62

1,5

46

1,5

10

20

01

78

5

Net Income R$ million

0

5

10

15

20

01

20

03

20

04

20

05

8,6

84

12

,0

07 15

,9

59

6,5

26

20

02

7,3

25

Net RevenuesR$ million

20

01

37.8%37.0%

30.5%35.4%

20

02

20

03

20

04

20

05

6,3

05

4,5

37

3,0

72

1,9

90

2,7

10

EBITDA and EBITDA Margin

EBITDA (R$ million) EBITDA Margin (%)

39.5%

Beer BrazilHispanic Latin America (HILA)Soft Drinks Brazil North America

25%

52%

13%

10%

Breakdown of net revenues

The company posted exceptional results in 2005, with a rise of 33% in net revenues and 39% in cash generation,

delivering an EBITDA of R$ 6.3 billion and a 39.5% margin. The continued growth of the Brazilian economy

and a positive situation in all Latin American countries in which we are active contributed to the development

of our operations.

We are convinced that a result of this magnitude only has been possible thanks to the action of our People, a team

that is formed through an efficient policy of recruitment, our results-oriented culture and recognized ability of

retaining the best talents. Looking toward the future, we are maintaining our commitment to continue delivering

results and to be a benchmark company in the beverages industry.

We are dedicated to accomplishments. This enthusiasm encompasses all stages of our business, beginning with the

selection of the barley and other raw materials for our products; continuing with the development of new beverages,

in the bottling, marketing, distribution and point-of-sale relationship processes; and winding up in the initiatives

that we use to assure consumer preference for our brands. We continued to focus on execution of operations.

Our manufacturing facilities have reached high operating and environmental efficiency levels . Our brands’ images

are strengthened by the creativity of our marketing, making use of effective and innovative campaigns.

Our increasingly motivated sales force seeks to exploit the opportunities in the markets in which we are present.

And our logistics operations continue to be efficient, guaranteeing that our customers are satisfied with the services

they receive from AmBev.

Our focus on cost reductions is more and more present on a daily basis, independent of the results that have been

achieved. This year, efficient efforts of our purchasing department coupled with synergies with InBev made

it possible for AmBev to maintain high profit margins despite a sharp rise in the cost of some inputs, such as

aluminum and sugar.

Message to shareholders

With net revenues growth of 33% and an EBTIDA of R$ 6.3 billion, AmBev continues committed to pursuing evenbetter results

02. AmBev | Annual Report | 2005

The year was an excellent one for operations in Brazil, with a solid rise in beer volumes being particularly noteworthy.

In the soft drinks segment, we increased volumes and profitability; but we believe that opportunities exist for further

strengthening this operation.

We encountered a very tough competitive environment in North America. Nevertheless, it was possible to boost our

profitability through a strong mix of cost controls and a focus on efficiencies.

In Hispanic Latin America, Quilmes Industrial S.A. (Quinsa) brought in exceptional results for our operations in the

Southern Cone countries, which comprises the markets of Argentina, Uruguay, Paraguay, Bolivia and Chile.

We also posted a good performance in Venezuela. In the other Latin American countries, the difficulties we faced

during 2005 have served as a learning experience and a factor of motivation that will help us deliver strong

performances in the near future.

We restructured the debt of our Canadian operation in 2005 in conditions that were more favorable to us, which led

the Fitch classification agency to elevate AmBev’s rating to BBB-, investment grade, at the beginning of 2006.

As with Standard & Poors in 2004, we were the first Brazilian company to obtain this classification from Fitch.

We are a company with a Passion for Execution. Our strong culture has created a company in which each employee

acts like an owner, leading us to achieve results that at first appear to be impossible. We are proud of our People and

we credit our entire staff for the fantastic year that was 2005.

Luiz Fernando EdmondChief Executive Officer for Latin America

Carlos Alves de BritoChief Executive Officer for North America in 2005 and

currently co-chairman of the Board of Directors

Victório Carlos De MarchiCo-chairman of the Board of Directors

Luiz Fernando Edmond

Carlos Alves de Brito

Victório Carlos De Marchi

2005 | Annual Report | AmBev .03

04. AmBev | Annual Report | 2005

Map of Operations

Canada

Brazil

DominicanRepublic

Guatemala

NicaraguaEl Salvador

Venezuela

Ecuador

Peru

Bolivia

Paraguay

ArgentinaUruguay

Chile

Argentina

Beer market (m HL) 15.2Per capita consumption (liters) 40.3Installed capacity (m HL) 16.1

Bolivia

Beer market (m HL) 2.3Per capita consumption (liters) 25.4Installed capacity (m HL) 2.8

Brazil

Beer market (m HL) 93.2Per capita consumption (liters) 51.4Installed capacity (m HL) 98.3

Canada

Beer market (m HL) 22.2Per capita consumption (liters) 69.0Installed capacity (m HL) 15.0

Chile

Beer market (m HL) 4.7Per capita consumption (liters) 29.1Installed capacity (m HL) 0.8

Ecuador

Beer market (m HL) 2.6Per capita consumption (liters) 19.8Installed capacity (m HL) 1.0

El Salvador

Beer market (m HL) 0.8Per capita consumption (liters) 12.6Installed capacity (m HL) –

Guatemala

Beer market (m HL) 1.2Per capita consumption (liters) 9.5Installed capacity (m HL) 1.4

Nicaragua

Beer market (m HL) 0.6Per capita consumption (liters) 10.5Installed capacity (m HL) –

Paraguay

Beer market (m HL) 1.9Per capita consumption (liters) 31.4Installed capacity (m HL) 2.2

Peru

Beer market (m HL) 7.1Per capita consumption (liters) 25.6Installed capacity (m HL) 1.0

Dominican Republic

Beer market (m HL) 3.1Per capita consumption (liters) 34.3Installed capacity (m HL) 1.0

Uruguay

Beer market (m HL) 0.6Per capita consumption (liters) 17.5Installed capacity (m HL) 1.1

Venezuela

Beer market (m HL) 22.0Per capita consumption (liters) 83.3Installed capacity (m HL) 3.2

North AmericaNet Revenues: R$ 3,976 millionEBITDA: R$ 1,433 millionEBITDA Margin: 36.0%Beer market in Canada: 22.2 million HLTotal beer sales: 10.9 million HLExports to the USA: 1.8 million HL

BrazilNet Revenues: R$ 9,902 millionEBITDA: R$ 4,319 millionEBITDA Margin: 43.6%Beer market: 93.2 million HLTotal beer sales: 62.5 million HLTotal soft drink sales: 20.3 million HL

Hispanic Latin America (HILA) Net Revenues: R$ 2,080 millionEBITDA: R$ 553 millionEBITDA Margin: 26.6%Beer market: 62.0 million HLTotal beer sales: 19.8 million HLTotal soft drink sales: 11.9 million HL

Note: Installed capacity refers only to beer (excluding soft drinks).Source: AmBev (capacities) and Euromonitor (market estimates and per capita consumption).

2005 | Annual Report | AmBev .05

Beer Brazil

Exceptional performance,driven by brands

and execution

The world’s fifth largest beer market, Brazil also is our

main operation, responsible for 59% of consolidated

EBITDA in 2005. EBITDA growth was 28.7%, totaling

R$ 3.7 billion. We ended the year with a 69.4% market

share, with an average annual share of 68.3%.

It was an exceptional year, with an 8.2% increase in

sales volume – the highest rate in the past ten years

– that exceeded the 7% expected and the 6.5% growth

in the overall market, according to ACNielsen’s

estimate. The volumes were driven by the

performance of our main brands and the efficiency in

execution at points of sale. We knew how to capture

the benefits deriving from the recovery of the

Brazilian economy and the greater confidence of

consumers that came with it.

The management of the brands and revenues assured

for us strong performance in the premium segment:

Bohemia grew 28% and Original rose 44%. Our direct

distribution strategy and growth for the premium

segment continued to increase revenues above the

rate of inflation – 8.7% compared to 5.7% (IPCA).

69.4%

2005 | Annual Report | AmBev .07

marketshare

8.2%growth involume

One highlight was the launch of Brahma in another 15

countries outside of Latin America, with special

success in the Ukraine and Russia. Inversely, in Brazil

we launched Stella Artois draft and bottled beer

exclusively for distinctive points of sale.

We seek creative options for new consumption

occasions as part our strategy to increase per capita

consumption and we have become the first beverage

company to introduce a draft beer franchise: the

Quiosque Chopp Brahma (Brahma Draft Beer Kiosk),

developed in 2003 for shopping center corridors,

airports, bus stations and shop galleries was the

fastest-growing franchise in 2005 out of a universe of

some 110 different master franchises analyzed by the

2005 Guide published by the Brazilian Franchising

Association (ABF). At year’s end, there were

60 Quiosque Brahma Chopp franchises in operation,

with a sales volume per unit that was double the draft

beer market average.

Another successful experience was Chopp Brahma

Express, a home delivery service for draft beer and

equipment. In addition, in July 2005 we created a

Chopp Brahma Express showroom that offers

consumers total brand experience. At the end of

the year, it became the single largest draft beer

point-of-sale in the city of São Paulo.08. AmBev | Annual Report | 2005

Beer Brazil

We are very proud of our beer business and reaffirm our

commitment to be proactive and to take the measures

that are necessary to ensure its continuous growth, both

in terms of market share as well as the profitability of

our operations. We are challenged each and every day to

further expand the beer market in Brazil.

We continued our equally successful brand exposure

initiatives, such as Skol Beats – the largest electronic

musical event in Latin America – and the Brahma Box –

the most traditional viewing location for the Rio de

Janeiro Carnival parade, bringing together Brazilian and

international celebrities. We also put on another edition

of the Boteco Bohemia, with consumers electing the

best places to drink beer, and we created the Confraria

Bohemia, designed to allow the brand to be more

closely involved with the field of gastronomy.

We instituted the Society of Beer, a relationship location

with consumers offering information about the beer

production process and consumption tips. The idea is to

teach beer lovers to become true master brewers while

merging the beverage with the art of cooking.

2005 | Annual Report | AmBev .09

1

5

6

9 11

15

26 2

8

31

38

60

Growth of the Quiosque Brahma Chopp network(number of units)

2Q

- 2

00

3

3Q

- 2

00

3

4Q

- 2

00

3

1Q

- 2

00

4

2Q

- 2

00

4

3Q

- 2

00

4

4Q

- 2

00

4

1Q

- 2

00

5

2Q

- 2

00

5

3Q

- 2

00

5

4Q

- 2

00

5

Soft Drinks Brazil

Healthy growth and thepotential for major gains

We are the second largest producer of soft drinks in

Brazil, with a 17% market share. We have a complete

portfolio of non-alcoholic beverages, led by Guaraná

Antarctica – the best selling soft drink in its segment in

Brazil – and by Pepsi-Cola – the second-ranked cola in

the market. We also produce and market the Gatorade

isotonic drink as well as Lipton Ice Tea, leaders in their

categories, and the Fratelli Vita bottled water.

We operate in the soft drinks market through a

division that is responsible for developing its own

independent policies and strategies; however, it

maintains production, logistical and distribution

synergies with our beer lines.

Our soft drinks posted healthy growth during 2005.

Sales volumes increased 6%, somewhat higher than

the 5% rise we had expected for the year. We were able

to maintain our market share and further boosted the

EBITDA margin, which rose to 31.4% for the year, higher

than the 30% that had been estimated.

17%

2005 | Annual Report | AmBev .11

market share

Revenues per hectoliter were up 6.3%, driven by a

readjustment in prices over the year, management

initiatives and an increase in direct distribution.

We began to exploit new market opportunities, an

effort that will be given new emphasis in 2006.

The 2.5-liter PET bottle launch is a step in the right

direction in view of the fact that soft drinks sales in

larger bottles has grown faster than the market

average, revealing a consumer preference for this

type of packaging.

We are enthusiastic about the installation of flow

meters to monitor the output of soft drink companies,

which will become mandatory in September 2006.

Similar to what happened in the beer industry, this

equipment will encourage fairer competition in the

sector, reducing the pressure for competitors to offer

informal discounts.

We identified the major growth potential of the

Brazilian market, currently the third largest in the

world in terms of volume but one that still has a low

per capita rate of consumption (70 liters per year).

12. AmBev | Annual Report | 2005

With a young population – one-third under the age of 15

– Brazil represents an opportunity to supply innovative

products for different consumption occasions.

We have winning brands. Guaraná Antarctica is a

Brazilian symbol, with the unique taste of a fruit that

is grown in the Amazon region and that is being

reinforced with greater visibility during 2006 with

the brand sponsoring the Brazilian national soccer

team during a Soccer World Cup competition year.

Pepsi has a large product line with distinctive tastes and

notably introduced a new visual identity during 2005.

Gatorade quenches the thirst of sports practitioners

and replaces mineral salts. Those who prefer a

smoother, non-carbonated beverage will find Lipton

Ice Tea is an option that has distinctive flavors.

Soft Drinks Brazil

2005 | Annual Report | AmBev .13

Hispanic LatinAmerica (HILA)

Sustained growth inthe Southern Cone

Our operation in the region encompasses 12 countries

in South and Central America and the Caribbean,

of which in five – Argentina, Uruguay, Paraguay,

Bolivia and Chile – we operate through our strategic

partner Quinsa.

In 2005, revenues rose 8.2% to R$ 2.1 billion, although

the division had mixed results. Quinsa posted a strong

performance, with its EBITDA in dollars increasing by

32.2%. Consolidated volume grew 12.9%, with beer

increasing 7.1% while soft drinks rose 26%. Dollar

revenues per hectoliter increased 10.4% over 2004.

In the other countries, which we call HILA-ex,

revenues rose 1.5%, impacted negatively by the

tougher competitive environments in Central

America and the soft drink markets in Peru and the

Dominican Republic.

2005 | Annual Report | AmBev .15

12countries

Our operationsencompass

growth inrevenues

8.2%

Hispanic Latin America (HILA)

In Bolivia, we posted consistent growth, with actions

concentrated on adding value to the brand portfolio

and reinforcing the distribution network. In Chile,

sales grew by 66.2%, driven by the Brahma brand’s

launch in September, and our market share rose to

15.5% (a gain of four percentage points). In Paraguay,

we maintained the recovery that we began two years

previously, supported by a better mix of brands and

new distribution processes. In Uruguay, we also took

advantage of the recovery of the local market to

expand our operations, with soft drinks being the

highlight – displaying the highest growth within

AmBev in the segment in 2005.

Quilmes Industrial S.A. (Quinsa)Through a combination of product launches, brand

development, cost discipline, distribution restructuring

and point-of-sale execution, Quinsa’s results improved

in each country. Our share in the brewery, which is the

market leader in the Southern Cone countries,

contributed R$ 1,299.9 million to the company’s

consolidated revenues (up 12.7%). In December 2005,

our stake was the equivalent to 59.2% of Quinsa’s

capital (compared to 54.8% the previous year).

In Argentina, the strategy for expanding presence in

the premium segment was maintained. After the

successful Stella Artois long neck beer product launch

at the end of 2004, the brand gained a 1-liter bottle

version. In soft drinks, growth reflected the consumer

market recovery and greater market shares for the

company’s brands. Two actions were important:

the PepsiCo license to operate within the last region

of the country where Quinsa was not already present

and the introduction of H2Oh carbonated water.

We initiated the doubling of the Tres Arroyos malt

plant, a project that should be fully operational in the

first half of 2006.

16. AmBev | Annual Report | 2005

Hispanic Latin America (HILA)

The period was dedicated to reinforcing the project to

introduce the best financial discipline practices,

managing revenues and costs, distribution and

point-of-sale execution. We took advantage of

successful experiences in the Brazilian market,

striving to adopt efficient processes and practices

that are capable of adding value to the operations.

We are still in the initial stages of our activities in the

majority of the region’s countries, part of an

expansion strategy initiated in 2003. This year’s

performance reinforces our commitment to the

region, which has great potential and encouraging

prospects for the future.

Northern Latin America (HILA-ex)Revenues from our operations in Northern Latin

America, Central America and the Caribbean

increased 1.5%, totaling R$ 780.4 million. We reached

the milestone of 1 million hectoliters of beer in the

last quarter of 2005, making us proud of our

accomplishments in a short amount of time.

However, performances varied in each country in which

we operate. There was consistent growth in Venezuela,

with an increase in volume and market share; we began

to sell beer in Peru and the Dominican Republic;

celebrated the Brahma brand’s first sales year

anniversary in Ecuador. However, the stiffer competitive

environments in Central America and the soft drinks

markets in Peru and the Dominican Republic negatively

impacted our revenues.

2005 | Annual Report | AmBev .17

North America

New operating modelin a challenging

environment

Labatt’s operations in North America contributed

R$ 3,975.5 million to our consolidated revenues.

The pro forma comparison with the performance of

2004 resulted in a 1.2% decline in Canadian dollars.

However, we achieved efficiency gains: the EBITDA

rose 12%, reaching R$ 1,433.10 million.

Revenues were influenced by three factors: the

increase in the low-price brand segment; a decline in

exports to the United States due to competition from

wine and distilled spirits as well as Mexican,

European and Asian beers; and the reduction of

volumes produced on behalf of Guiness, a reflection

of our plan for rationalizing the production structure,

that included the closing of two brewing facilities

(New Westminster and Toronto).

2005 | Annual Report | AmBev .19

North America

We also introduced the Zero Base Budget (ZBB). More

than cutting and controlling costs, this is an entirely

new system of approaching the cost and expense

structure that determines a new and more

encompassing vision regarding all of our businesses.

A portfolio of more than 50 brands supports us in

Canada. Besides Labatt Blue, we produce and handle the

local distribution of Budweiser and Bud Light, licensed

from Anheuser-Busch, and InBev’s Stella Artois.

Budweiser continued to be the Canadian volume leader

and at year’s end we recorded a significant increase in

In this challenging environment, we adopted a number

of measures to ensure the prosperity of our operations

in the region. It was a year of intense inwards-looking

focus and changes to our management model. We

introduced a new organizational structure, reclassifying

job positions and variable compensation packages with

the objective being to align the interests of the

employees and the shareholders to the profitability

targets of our operations. This process was

accompanied by the difficult task of restructuring the

workforce, but it allowed us to rationalize the operating

structure and achieve cost efficiencies.

20. AmBev | Annual Report | 2005

ofCanada’s10 largestbrands

50brands in the portfolio

23%of AmBev’sEBITDA

Represents

Brahma will fill a gap in our product line – the

transparent bottle, a segment that represents

4.1% of the market.

Coupled with the complete restructuring of internal

operations and the sales team, our performance in 2005

has equipped us to be more personalized in our

approach, focusing attention on the priorities of each

market. This is the type of challenging environment

that, for us, represents an exceptional opportunity

for growth.

sales of Bud Light, Stella Artois and Alexander Keith’s,

the number one domestic specialty beer in Canada and

the main draft beer brand in Ontario, which is the

largest market in the country. This improvement

partially compensated lower sales of Labatt Blue and

the company’s other brands, which faced a more

aggressive competitive environment.

As a result, we ended the year with five of Canada’s ten

top brands. We also concluded a successful test-launch

of Brahma in the Alberta region in preparation for

selling the brand as of 2006 in selected markets.

2005 | Annual Report | AmBev .21

5

22. AmBev | Annual Report | 2005

Passion for Execution

Discipline and science fordelivering the best results

The greatest challenge and the biggest opportunity

for growth is in getting close to consumers and

winning their preference. This challenge propels us

each day and represents a true passion for execution.

It is a passion for the business that involves all stages

of our work – from the acquisition of the raw material

through to the delivery of our products to the end

consumer – and it is this that enables us to maintain

a consistent rise in earnings.

For us, execution is discipline and science. It is at the

point-of-sale, at the moment of purchase, when the

great majority of consumers decide which beverage

they are going to taste or take home. We need

to profoundly understand the point-of-sale and

consumers needs in order to most effectively deal

with the variables that interfere with our brands’

performance. This involves research, marketing,

merchandising, distribution, product exposure,

refrigeration and pricing – so that, in the view of

the consumer, our products are more competitive

than the competition’s.

2005 | Annual Report | AmBev .23

Passion for Execution

We also install coolers, specially developed

refrigerators designed to maintain beer at the ideal

temperature for consumption (-5ºC), which is a

strategic distinguishing characteristic in the

main markets.

People who Sell (“Gente que vende”)

Our passion for execution is transmitted to every

single person who works at AmBev, independent of

his or her job position. Since AmBev was created in

2000, all eemployees reach the points-of-sale to

participate in the People who Sell program, designed

to teach them to understand and learn how the

market works, how our products are sold and exposed

and what is the opinion of the point-of-sale’s owner.

Besides Brazil, in 2005, this initiative was run in five

other countries: Ecuador, Guatemala, Peru, the

Dominican Republic and Venezuela. The People who

Sell program not only strengthens the company’s

culture and practices – it also disseminates the

responsible consumption message.

Motivation and efficiencyOur sales staff visits each point-of-sale two times per

week on average. The workday begins with an

animated and motivational general meeting of the

teams when targets, strategies and tactics are

established for better point-of-sale execution.

The teams make their sales calls equipped with

palmtops, devices that connect them to a database

giving them valuable information about each client

establishment (order history, inventory, types of

packaging, average prices, etc.). Due to sale channel

diversity, this model makes the negotiation process

more effective and lets us present a sales proposal that

satisfies client requirements until a subsequent visit.

Our teams strictly follow a list of features that must

be observed in order to help the points of sale increase

their efficiency and the results of the sales of our beer,

soft drinks, teas, isotonics and water. This includes

product exposure and organization, inventory control,

posters and other publicity materials and sales

prices, among others.

24. AmBev | Annual Report | 2005

2005 | Annual Report | AmBev .25

BeersSkol – Brazil market leader (31.9% share in December 2005), where it has been produced since

1967, was the first beer in a can in the country and revolutionized the market again in 2002

through Skol Beats.

Brahma – Brazil’s most traditional brand, launched in 1888, which is the market leader in

Paraguay and present also in 23 countries of the Americas and Europe.

Antarctica – A classic Pilsen beer that has been produced since 1885, which combines

tradition and quality.

Bohemia – The first Brazilian beer, produced since 1853, which is the premium segment leader

and is also presented in the Bohemia Weiss and Bohemia Escura versions.

Original – A beverage with a memorable taste sold in the premium segment.

Serramalte and Polar – Brands whose distribution is concentrated in the south of Brazil.

Líber and Kronenbier – Non-alcoholic; they multiply the number of occasions for consuming beer.

Caracu – A dark stout-type beer.

Quilmes – Synonym for beer in Argentina, it is comes in more than 15 versions. It also is our main

brand in Chile, Bolivia and Uruguay.

Brands

A large and innovative portfolio We have one of the largest and most diversified beverage portfolios in the world, including three top selling

international beer brands: Skol, in third place ; Brahma, in sixth place; and Antarctica, in 20th place. The three

brands are market leaders in Brazil as is Quilmes in Argentina, while Labatt Blue is the top-selling Canadian beer

in the world. Moreover, the unique taste of our Guaraná Antarctica, made from an Amazonian fruit, is ranked 15th

in the world preference for soft drinks. We produce and sell products for different consumption occasions and

consumer profiles, with an extensive line of beers, soft drinks, isotonics, ready-to-drink teas and mineral water.

We have beverages to satisfy all preferences wherever people may be. We invest in the continuous development

of our brands in order to ensure that they remain in the spotlight over the long term. In order for the company to

establish the correct value of its brands, we strive to increasingly optimize the execution of price per channel,

packaging and consumption occasion as well as maintaining a competitive price for the consumer.

Our main brands, per product category, are:

Pilsen and Patrícia – Points of reference in the Uruguayan beer market.

Brahva – The brand we market in Central American countries.

Labatt Blue – The best selling brand of Canadian beer in the world, produced together with

another 50 brands in the country such as Kokanee and Alexander Keith’s.

Stella Artois – InBev’s international brand, a super premium beer with a balanced and memorable

taste that was introduced in Belgium in 1366 and now is also produced in Brazil and Argentina.

Soft DrinksGuaraná Antarctica – The second best selling soft drink in Brazil with the unique flavor of

the guaraná fruit that is grown in the Amazon region.

Pepsi-Cola – AmBev is the second largest PepsiCo bottler in the world. We produce and

distribute soft drinks in a number of companies in Latin and Central America with a product

line that includes the traditional Pepsi-Cola, Pepsi-Twist, with its innovative cola and lemon

taste, and Pepsi X, the first energetic soft drink in the world.

Among our other notable soft drink brands are Sukita, an orange-flavored beverage, Soda

Limonada and Tônica Antarctica.

Isotonics Gatorade – The best selling isotonic sports beverage in the world, also part of our alliance

with PepsiCo.

TeasLipton Iced Tea – Ready-to-drink tea segment world leader, produced under franchise

license in Brazil.

WaterFratelli Vita – Lightness is one of its main qualities, due to the low level of dissolved salts.

2005 | Annual Report | AmBev .27

Distribution

Competitive advantages incosts and services

Distribution is one of the beverage business’ most

complex aspects. We service approximately 1 million

points-of-sale in Brazil alone. To be able to do this, we

combine direct and outsourced distribution, through

exclusive resellers, comprising a multi-brand network

that ensures deep market penetration and

competitive advantages in costs and services.

We maintain an efficient and creative transportation

logistics structure for the products that are always at

hand for consumers. In order to reach little towns in

the Amazon region, for example, we make use of

boats and even small canoes in contrast to the latest

generation trailer trucks we use in large urban centers.

1

millionpoints-of-sale

2005 | Annual Report | AmBev .29

Distribution

costs through economies of scale because the sale and

delivery of different brands and products are carried

out by the same infrastructure. We also use a

computerized system for obtaining and crosschecking

data about each point-of-sale, which lets us more

effectively execute sales and delivery routes.

Our own distribution and outsourced network

represents a unique source of marketing and

distribution knowledge.

With a complete portfolio of products, we use the

strength of our brands to maximize our distribution

efficiency, enhancing our market leadership position.

The more products that are placed in point-of-sale,

the more efficient we are in achieving distribution

cost reductions.

Exclusive resellers and direct distribution in major

cities and for self-service make it possible to reduce

30. AmBev | Annual Report | 2005

The AmBev Excellence Program encourages constant

improvement through support of an operations

manual that establishes the standards of worldwide

performance quality and exchange of best practice

information. Distributors that achieve excellence

three years in a row receive the title of AmBev

Ambassadors, entering the company’s select group

of most admired and respected partners.

AmBev Ambassadors

32. AmBev | Annual Report | 2005

Cost Management

Commitment to results In order to ensure that AmBev continues to be one of

the world’s most efficient producers, cost

management is a true obsession for us. Our planning

is based on the Zero Base Budget (ZBB) system that,

each year, establishes stretched targets for controlling

expenses and cost in order to increase our margins.

Each team is responsible for the management of its

own budget and meeting targets is compensated for

through an aggressive variable compensation

program. Thus, we stimulate the commitment and we

direct all the teams to carry out strict cost control.

An example of our high level of cost control is the

management of the Distribution Center’s fleet of

vehicles. In 2005, two initiatives exemplified the series

of measures we adopted to ensure that the growth of

these costs was lower than the rise of our revenues:

vehicles were transformed to use natural gas as fuel

instead of gasoline, and we highlighted them with

colored stickers. As a result, we wound up not having

to pay more for cars that originally were painted in

the colors of our brands.2005 | Annual Report | AmBev .33

97%reutilization of solid wastes

4

liters ofwater perliter ofbeerproduced

34. AmBev | Annual Report | 2005

Cost Management

AmBev became a world benchmark in items

considered important for the composition of

production costs. Examples include the average of 4.2

liters of water per liter of beer produced – an index

that has hit an unprecedented 3.3 liters at our Curitiba

(PR) plant) – and 97% reutilization rate of solid wastes

stemming from the production process (malt bagasse,

residual ferment from beer production, pulp from

bottle labels, and similar items). These by-products are

treated as businesses and their sales contributed R$

59.5 million to 2005’s revenues, up 23% over the

previous year (R$ 46.6 million).

Another distinguishing management characteristic

was the Manufacturing Excellence Program. Made up

of a set of regulations, procedures, tools and

management methods, the program encourages each

unit to improve its results. The system rewards results

while identifying and disseminating the best

practices for meeting established targets. Using it, it is

possible to recognize and compensate the best

performances.

Within the AmBev, Labatt, Quilmes and InBev

universe, we have more than 70 manufacturing

plants, which opens up opportunities for exchanging

best practices, resulting in efficiency gains.

0

20

40

60

20

04

20

05

46

.6

59

.5

20

03

31

.8

Revenues from by-products and wastes R$ million

different items in inventory (versions of packaging

of different beverage brands) that identifies the

variables for sales forecasts, costs and regional

production and highlights the best alternatives for

satisfying client orders. For major freight shipments

and distances, we use railroad, waterway and coastal

shipping transportation modes.

This obsession for cost control was a determining

factor leading to Canadian EBTIDA growth in 2005,

a year when our volumes were impacted by

tough competition.

Within the strategy for achieving efficiency in costs

along with superior quality, we produce some raw

materials that we consume. AmBev is the owner of

five malt production facilities (one in Brazil, two in

Argentina and two in Uruguay), which supply part of

the malt consumed in the brewing of beer. We also

have a glass factory in Paraguay, a facility for making

metallic corks and another plant for PET bottle

pre-forms in Manaus (AM).

Furthermore, we have developed a proprietary system

for exchanging information between the plants, the

distribution centers and the distributors and the

2005 | Annual Report | AmBev .35

Financial Discipline

Management based oncreation of value

With a model that combines the growth of revenues,

efficient distribution, a passion for execution and

permanent attention to costs and expenses, financial

discipline is yet another one of our strong points.

Our management is based upon the Economic Value

Added (EVA®) tool that is extensively used in our

industrial and commercial facilities to support

decisions while always striving to create value.

EVA growth is related to our variable compensation

policy as a way of motivating and remunerating the

performance of AmBev’s People.

Our generation of cash comes from an EBITDA that

totaled R$ 6.3 billion in 2005, with an average

compound annual growth rate (CAGR) of 33.4% over

the past five years. The fact that we control our

investments and our cash flow the same way that we

control expenses contributed to this result.

36. AmBev | Annual Report | 2005

Financial Discipline

Net debt of R$ 6.1 billion in 2005 represented a multiple

of 0.97 of the EBITDA, which indicates an opportunity

to increase leveraging the company’s growth.

The Standard & Poors and Fitch rating agencies

recognized us as being in the Investment Grade

category, on the basis of our solid capital structure.

We were the first Brazilian company to receive this

classification, making it possible to obtain funds on

the international market at competitive costs as

investors become more aware of AmBev’s low risk.

We have assured a consistent rate of return for our

shareholders. All cash that is not invested in our

business is disbursed to shareholders in the form

of dividends or interest on own capital. In 2005,

shareholder compensation totaled R$ 1,692 million,

the equivalent to 109% of net income.

2005 | Annual Report | AmBev .37

6.3R$billion in2005

EBITDA

33.4%over the past5 years

CAGR

20

01

62%

43%

32%

71%

114%

20

02

20

03

20

04

20

05

1.3

00

99

8

33

7

20

01

29

2

50

2

Dividends and payout

Dividends (R$ million) Dividends (R$ million) * Payout (as percentage of Net Income)

(*) Value referring to the 2005 fiscal year, not provisioned in the 12/31/2005 balance sheet

109%

1.3

27

39

2

Culture

Our culturedistinguishes and

motivates talent

We have our own way of being and of doing things,

which have been determining factors in building the

AmBev Culture. Through a combination of values,

beliefs, practices and management principles that

guide our actions and our behavior, our culture makes

us different and shows who we are.

The fundamental purpose of our business – our

Mission – is to make available the best brands,

products and services to the market that make it

possible to create strong and long-lasting ties with

our consumers and our clients. Our dream – our

Vision – is to be the best beverage company in the

world in terms of quality, strength of brands and

recognition of clients as their best partner, to have the

highest profitability and the best and most

committed people. It means to dream the “impossible”

and execute boldly and courageously, to be ready to

propose, face and exceed targets that would be

impossible for others to meet.

38. AmBev | Annual Report | 2005

2005 | Annual Report | AmBev .39

Culture

We act like leaders – We lead by personal example.

We want to win, but always respecting ethical

practices. We adopt a zero tolerance policy with regard

to keeping our culture alive and we believe that our

diversity constitutes a fortress. We are present where

things happen together with our People, our clients

and our consumers. We use up shoe leather to get to

know the details of our business.

And it means to move forward and lead the changes

that are necessary to achieve the dream. It means to

be passionate about everything we do.

We have defined four values that guide our conduct:

The consumers come first – Consumers are the

reason for everything that we do and we are partners

with our clients and resellers in order to provide them

superior quality.

Our People make the difference – We attract, develop

and maintain the best people, we invest in our People,

we support their continuous training and we

reward success.

We make things happen – We dream big dreams.

We select challenging targets and pursue major

performances. We are focused on results. We work

hard and enthusiastically. We use our reserve tanks.

We act like and are recognized as owners.

40. AmBev | Annual Report | 2005

Culture

We think and act like owners – We must demonstrate

passion and responsibility, taking decisions and

acting in the company’s long-term interest as if it

were ours. We act to ensure that our investment –

our company – has growing and sustainable value.

We demonstrate leadership and we develop the best

people – We must lead our company in the midst

of changes that are occurring in order to achieve

extraordinary results and also to identify and develop

our future leaders. Having the right people in the

right places doing the right things will make a big

difference in our journey from the Largest to the Best.

Our CompetenciesWe challenge ourselves to achieve extraordinary

results – We propose challenging targets,

continuously striving to discover new ways for

growing our business and delivering exceptional

performances without compromising either

quality or integrity.

We have in-depth knowledge of our business –

We apply our knowledge about our businesses,

the industry and the company to create value for

our investors.

We build strong relationships and teams – Our capacity

for teamwork and the fact that we mutually trust and

respect each other and maximize all the resources

available to us represent the key to our success.

We meet our targets the AmBev way: simply, focused

and disciplined – We will be rewarded for simplifying

our business, for focusing our energy and our

resources on the company’s biggest priorities and

for building a culture of discipline.

2005 | Annual Report | AmBev .41

AmBev People

Competence to recruit, totrain, to motivate and to

retain the best professionals

28,214persons in 14 countries

42. AmBev | Annual Report | 2005

Our People are dynamic, creative, imbued with

entrepreneurial spirit and a thirst for success. They

identify with an informal workplace and are in search

of a brilliant professional career. At the end of 2005,

we were 28,214 persons – most of whom in Brazil

(19,042 professionals).

We encourage our people to give the best of

themselves, to work hard and defend the work that

they do. We have a variable compensation program

that, in some cases, can represent up to 70% annual

earnings. Through bonuses, prizes and a stock option

plan, all employees – from executive officers to those

on the factory floor – are compensated for meeting

targets and goals. High-potential professionals with

exceptional performances earn the right to use a

bonus as part of a Stock Option Acquisition Plan,

effectively becoming owners of the company.

AmBev People* – December 2005

Industrial 13,798Sales and distribution 9,773Administration 4,643Total 28,214* does not include Quilmes’ operations.

TraineesOne way for employees to enter AmBev is through its

Trainee Program, which we consider to be of strategic

importance for the permanent renovation of our

human talent. We already have trained more than

500 professionals since it was created in 1990 in the

former Brahma. Six individuals who were trainees

today are company directors while many others are

managers. The recruiting and selection process

involves the entire executive officer team, whose

members visit the main universities in the region’s

countries to present our program and our culture.

In 2005, we received 19,198 applications and we

selected 42 young professionals in the following

countries: Brazil (19), Peru (4), Ecuador (4), Venezuela

(3), Guatemala (6), Honduras (1), El Salvador (1),

Nicaragua (1) and the Dominican Republic (3).

2005 | Annual Report | AmBev .43

TrainingOur People are young (average age of 35, which rises

to 42 for those in executive positions) and have a good

educational background: 19% have college degrees and

92% graduated from high school.

We permanently invest in the development of our

employees through a continuous education process.

In 2005, 55% of our employees underwent training.

Some R$ 14 million was earmarked for the

development of Our People through the AmBev

University and undergraduate and post-graduate

scholarships offered by the Antonio and Helena

Zerrener Foundation (FAHZ), one of the company’s

controlling shareholders. Our corporate university

makes the training process democratic, with courses

adapted for all levels of job positions within the

company in different formats, and making extensive

use of information technology. For example, TV AmBev

process that also awakened the interest of AmBev

units outside of Brazil, such as in Ecuador and the

Dominican Republic.

We entered into partnership with a number of

companies and organizations specialized in recruiting

individuals with special needs and we adopted the

same selection and compensation criteria used for

people with no such needs. In December 2003, we had

143 professionals with special needs on the payroll. In

two years, a total of 264 persons were recruited and

our target is to reach 800 by the end of 2006.

Quality of LifeWe also kicked off the Great Life program

(“Vida Legal”) whose goal is to stimulate healthy

habits, foster preventive health actions and

encourage employees and their family members

to deal with chronic diseases. Besides improving

their quality of life, we will save 15% in the

annual cost of medical assistance – and this

money will be transformed into other benefits,

such as scholarships.

AmBev People

For example, TV AmBev by satellite is a tool for the

transmission of our knowledge as well as a

communication vehicle that is on the air during eight

different time slots. In this process, certified directors

and managers also are instructors. Since 2002, 32,000 of

our own and resellers’ employees participated in courses

and training sessions designed to boost their careers.

The AmBev MBA course already has graduated 210

professionals since 1998, the year the former Brahma

created it. The objective is to offer a systemic vision of

the company as well as provide opportunities for

comparing our processes, results and culture to the

best companies in Brazil and abroad.

DiversityIn 2005, we launched the Program for Hiring

Professionals with Special Needs. More than merely

complying with Brazilian legislation, which requires

that 5% of a company’s payroll be reserved for people

with deficiencies, the initiative was designed to

encourage diversity and social inclusion. The program

was accompanied by an awareness and mobilization

44. AmBev | Annual Report | 2005

2005 | Annual Report | AmBev .45

46. AmBev | Annual Report | 2005

Sustainability

Our work couplesdevelopment with

sustainability

The constant concern to achieve profitability and be

responsible – both legally and ethically – leads AmBev

along a path of business sustainability. We strictly

comply with our tax obligations, we encourage the

adoption of transparent standards of conduct among

our employees and we invest in consistent and

permanent social projects that are in step with our

core business.

We work in the present while looking towards the

future. Thus, we invest in social and environmental

counterpoints in the locations where we have

operations. This is a commitment that goes beyond

the creation of jobs and paying of taxes, which in

2005 totaled R$ 7.2 billion. We share knowledge and

management with the chain of production and we

invest in the training of our human talents, in

environmental preservation policies, in the fostering

of culture and cultural manifestations of the countries

in which we are present. Moreover, we are a pioneer

in the campaign for responsible consumption of

alcoholic beverages.

2005 | Annual Report | AmBev .47

Social Responsibility

Another action in this program was the sponsorship

of a booklet, “How To Speak with Your Children about

the Use of Alcohol,” prepared by the scientific advisers

to the Health and Alcohol Scientific Center (CISA),

initially distributed in schools in São Paulo.

Moreover, the AmBev People Who Sell (Gente que Vende)

initiative that introduces our employees to the points

of sale selected “Amigo da Vez” as its slogan in 2005,

with the idea being that groups of young people who

go out for a good time should select one of their group

as the designated driver who must not drink and can

take them all home. During this activity, the employees

– 14,000 participated in the event – distributed 35,000

brochures to establishments throughout the country

especially prepared for the occasion.

Responsible ConsumptionWe have been running the groundbreaking AmBev

Responsible Consumption Program since 2001,

which follows the premises of the World Health

Organization (WHO). It includes advertising materials

that warn about the risks of drinking and driving,

the distribution of billboards and banners with the

message “If You Drink, Don’t Drive” on highways and

airport access roads, and the “Ask for their ID”

campaign, which advises bar and restaurant owners

about the importance of not selling alcoholic

beverages to minors under the age of 18. This

campaign already has involved more than 250,000

establishments throughout the country.

In the events that are sponsored by our brands, such

as the Brahma Box and Skol Beats, we invest in

specific actions such as offering free transportation,

discounts for taxi service and distribution of material

(brochures, bandanas, automobile stickers) that

encourage participants not to drive after they have

been drinking. We also have already donated more

than 14,000 breath analyzers to the governments of

São Paulo, Rio de Janeiro, Rio Grande do Sul and the

Federal District, and we have placed the message

“If You Drink, Don’t Drive” on 340 outdoor digital

clocks installed in the streets of São Paulo.

48. AmBev | Annual Report | 2005

Social Responsibility

Latin America for studying and disseminating

recycling practices, created by the Rio de Janeiro-

Ecomarapendi NGO. Courses, workshops and

professional training programs are run at the center,

which also maintains the Recycling Ecospace gallery

for permanent display of the work of artists who use

recycled materials in their projects.

Recycling To encourage solutions for reducing losses and for

preserving the environment and natural resources, in

2005 we created the 1st AmBev Recycling Prize. Based

on the 4R formula – Reduce, Reuse, Recycle and

Renovate – initiatives that represent the perfect

balance between responsible use of natural resources

and innovation in the use of disposable materials

were recognized. More than 800 projects were

submitted and visual artists, designers and artisans

(Reuse), previously unpublished studies (Reduce),

cooperatives, associations and non-profit

organizations (Recycle) and journalists (Renovate)

received awards. The finalists in each category were

included in an exhibit put on at the São Paulo

Museum of Image and Sound (MIS).

We also contributed to the development and

improvement in the quality of life of a number of

communities of waste scavengers through the

Solidarity Recycling Program that assisted 27

cooperatives in five states and the Federal District in

2005. The action included the donation of hydraulic

presses – that compress packaging materials and add

value to the items that are commercialized – along

with support for the Recicloteca, the largest center in

2005 | Annual Report | AmBev .49

Social Responsibility

in the world where we develop high-productivity

seedlings that are immune to pests that we donate

to farmers. AmBev has organized Guaraná Day there

each year since 1998 during which the technological

practices adopted by the company for growing the

fruit are taught to the farmers and the development

projects for the region are introduced. In 2005,

we announced acquisition of the entire 2005/2006

harvest during the event, representing some 220 tons

of beans, at a value that was 44% higher than

the minimum stipulated by the official National

Supply Company (CONAB).

50. AmBev | Annual Report | 2005

The Maués ProjectThis initiative is part of the Green Free Zone Project –

developed by the Amazonas state government. It has

earmarked some R$ 60.9 million through 2013

designed to finance a series of actions for the

population of Maués to encourage the growing of

guaraná crops and to contribute to the local

community’s social and economic development.

Toward this end, we also operate the Santa Helena

Farm in the Maués region, which is a research center

that contains the largest guaraná plant genetic bank

Social Responsibility

Moreover, the FAHZ earmarks R$ 4 million through

undergraduate and postgraduate scholarships as an

investment in the development and continuous

learning of Ambev People.

Solidarity In 2005, we reinforced the humanitarian aid

campaign for the countries most affected by the

tsunami – Sri Lanka and Indonesia – with the

donation of 414 hectoliters of mineral water for

their populations.

In another demonstration that solidarity is embedded

in the company’s culture, our employees in Jaguariúna

(SP) ran a Solidarity Christmas campaign that

collected 3.2 tons of food and 1,200 liters of milk,

delivered to institutions in the municipality that help

needy children

Solidarity LiteracyAlso designed to contribute to social gains, we

sponsor a program to eradicate illeteracy in Brazil.

Initiated in 2001, our assistance already has made it

possible to help 9,500 students and to train 380

literacy teachers in eight municipalities in the states

of Amazonas (Anori, Maués and Manacapuru),

|Sergipe (Simão Dias), Maranhão (Belagua), Bahia

(Maragogipe), Piauí (Nossa Senhora dos Remédios)

and Mato Grosso (Nossa Senhora do Livramento).

The Fundação Antonio e HelenaZerrenner (FAHZ)One of AmBev’s controlling shareholders, the FAHZ is

a national charitable institution that, through

hospitals, schools and day care centers offers free

medical, educational and social assistance to the

company’s employees, their dependents and others,

involving a total of 50,000 lives. In São Paulo it

operates the 244-bed Santa Helena Hospital, which

offers medical treatment preferentially to the

beneficiaries, and the Walter Belian Vocational School,

which teaches grade and high school courses along

with vocational classes to over 1,000 students,

with courses in secretarial services, electronics,

graphic arts and industrial information technology.

2005 | Annual Report | AmBev .51

The Environment

Commitment to superioreco-efficiency standards

Our environmental policy establishes the

commitment to seek and apply technologies,

processes and industrial inputs that reduce the impact

of our operations on the environment. We have

created eco-efficiency indicators – such as the

consumption of water and energy and the recycling of

waste – that are systematically measured. Annual

targets per plant are established, designed to meet

internal and external benchmarks. These targets are

part of the Manufacturing Excellence that motivates

all AmBev People to continuously improve processes.

The management of water resources is one of our

priorities. We have adopted a series of measures to

rationalize water consumption, both to reduce costs as

well as to protect the environment. As a result, we

have become a national point of reference in the beer

industry, with average consumption of 4.2 liters of

water per each liter of beer we produced in 2005.

In 2001, our average was 5.62 liters.

52. AmBev | Annual Report | 2005

2005 | Annual Report | AmBev .53

5.6

2

5.3

6

4.8

8

4.3

7

4.2

1

Water consumption(liter/liter of beer)

20

01

20

02

20

03

20

04

20

05

93

.7

%

94

.9

%

95

.8

%

96

.5

%

96

.8

%

Reutilization of industrial wastes

20

01

20

02

20

03

20

04

20

05

9.5

1

9.3

5

9.1

3

8.7

6

8.7

3

Energy consumption (Kwh/HL)

20

01

20

02

20

03

20

04

20

05

The Environment

analyzed on a monthly basis both by our own

laboratories as well as a facility in São Paulo

that controls the water quality of all AmBev’s

plants in Brazil.

Through the adoption of biogas in a number of its

units, we seek to substitute sources of non-renewable

energy and reduce polluting emissions. AmBev’s

Brazilian plants already use biogas – produced from

the biological reactions in its effluent treatment

stations – for the production of steam used to

We have produced a primer, known in-house as the

Water Commandments, emphasizing practices such

as proper maintenance of equipment to avoid leaks

and constant referral to each facility’s indicators.

We ensure that our effluent treatment stations

maintain the proper conditions for allowing the

recycling of the water used for cleaning and

maintenance purposes. Furthermore, this water is

returned to the environment in a highly purified

form. Samples of water outflow from the stations are

54. AmBev | Annual Report | 2005

Furthermore, we recycled 97% of the solid industrial

wastes our facilities generated, reaching 99% at the

Nova Rio plant in Rio de Janeiro. Malt bagasse and

ferment were transformed into protein for animal

feed. Residual ferment from the beer brewing process

is used to make flavor cubes used in soups and broths

and as food supplements for people. The pulp

extracted from our packaging is sent to cardboard

manufacturers for recycling.

produce power. Through this technique, we have been

able to reduce the use of natural gas and, mainly, fuel

oil. We also have become more efficient in our

consumption of electricity: we went from 9.5 Kwh per

hectoliter in 2000 to 8.7 Kwh in 2005.

We also initiated the Biomass Project for the

reutilization of wood residues, sawdust, coconut husks

and reforestation wood to produce energy in four of

our plants. Through this program we were able to

avoid the burning of 26,000 tons a year of fuel oil.

2005 | Annual Report | AmBev .55

We have structured our corporate governance model in a manner that ensures transparency, appropriate

disclosure, efficient decision-making control processes and equal and fair treatment of all shareholders.

We have been increasingly improving our governance structure, reinforcing internal controls and fully taking into

account all features of the Sarbanes-Oxley Act. This law requires that international companies listed on U.S. stock

exchanges adapt themselves to a series of measures designed to protect investors by demanding more precision

and reliability regarding the business information they disclose.

We advanced further in the project that was initiated in 2004, surveying the risks and controls not only related to

the preparation and disclosure of financial information but also that involving operations, as well. The project has

involved all of top and middle management, who also have the help of outside consultants. The main risks were

mapped, addressed and tested in 2005. We are totally committed to concluding the work during 2006 in order

to obtain the certification required by the Act before year’s end.

At the 2005 Annual Shareholders’ Meeting, the Board of Directors elected independent members to sit on the

company’s Fiscal Committee, now a permanent body that also has assumed the Audit Committee’s duties.

With a one-year term of office, the Committee’s members include specialists in the Brazilian and U.S. financial

markets. No member of the Committee exercises a position on the Board of Directors or Executive Management.

56. AmBev | Annual Report | 2005

Enhancing the best practices on behalf of shareholders

Corporate Governance

Corporate Governance

2005 | Annual Report | AmBev .57

Our higher corporate governance standards are derived from some important principles, such as:

Transparent Communication: We understand that open and transparent communication is an excellent means

of creating value for shareholders. We offer detailed analyses to the market, including quarterly reports and

conference calls so that investors understand the fundamentals of our company and the main guidelines

of our businesses.

Decision-making processes: Our Board of Directors makes use of its members’ experience to guarantee that its

long-term objectives are met while short-term competitiveness is achieved. It works through the support of such

committees as:

• Executive Committee: the main link between the policies and decisions taken by the Board of Directors and

AmBev’s managers. Its responsibilities include analyzing, proposing and monitoring the company’s performance

goals and budgets to ensure compliance with objectives.

• Compliance Committee: it helps the Board of Directors monitor and analyze the company’s internal controls and

fiscal profile and its operations with stakeholders.

• Finance Committee: it analyzes and monitors the company’s annual investment plan and opportunities for

external growth, as well as the capital structure, cash flow and management of financial risks.

Simultaneously, the Board of Directors ensures that our values, ethics and culture are practiced and disseminated.

Our team of top executives includes very experienced professionals who have been with the company an average

of 10 years each. It is our policy to rotate job functions on a regular basis, which offers managers an extensive and

deep understanding of our businesses’ different facets.

58. AmBev | Annual Report | 2005

Alignment with objectives: In order to ensure that the objectives of the executives remain aligned with

shareholders’ expectations, the company has adopted a variable compensation system for all employees that is

linked to achieving stretched targets. Following the concept disseminated by our culture of thinking like owners,

the top 200 executives participate in a stock option plan tied in with their annual bonuses, making them

shareholders in the company and fostering a long-term relationship between the executives and the company.

Shareholders’ agreement: The controlling block is composed of two entities that in December 2005 together held

88.1% of the company’s voting capital and 64.3% of its total capital: InBev, with, directly or indirectly, 72.9% of its

voting capital and 56.1% of the total capital, and the Fundação Antonio e Helena Zerrenner (FAHZ), with 15.2% of its

voting capital and 8.2% of total capital. The Shareholders’ Agreement, which is valid until 2019, confers on FAHZ

the right to veto on questions related to a wide range of important matters, such as dividends, investments,

acquisitions and the issuance of new debt.

Shareholder composition (1)In thousands of shares Common % Preferred % Total %

Interbrew International B.V. (2) 22,280,277 64.60% 10,087,238 32.10% 32,367,515 49.10%Fundação Antonio e Helena Zerrenner INB 5,314,282 15.20% 103,203 0.30% 5,417,485 8.20%AmBrew S/A (2) 2,870,650 8.30% 1,435,611 4.60% 4,306,261 6.50%InBev Participações Societárias Ltda (2) 0 0.00% 296,900 0.90% 296,900 0.50%Total Controlling Block 30,465,209 88.10% 11,922,952 37.90% 42,388,161 64.30%Instituto AmBev de Previdência Privada 1,919 0.00% 9,595 0.00% 11,514 0.00%Others 1,888 0.00% 9,441 0.00% 11,329 0.00%Free Float 4,009,286 11.60% 18,574,615 59.20% 22,583,901 34.30%Share in Treasury 21,120 0.10% 860,048 2.70% 881,168 1.30%Total 34,499,423 100.00% 31,376,651 100.00% 65,876,074 100.00%

(1) On December 31, 2005(2) Controlled by InBev S.A. / N.V.

Corporate Governance

Our shares are traded on the São Paulo Stock

Exchange (ticker symbols AMBV3 and AMBV4) and,

as American Depositary Receipts (ADRs), on the

New York Stock Exchange (ticker symbol ABV).

On the Brazilian stock market, the company’s

preferred shares rose 42.7% in value in 2005, while the

Ibovespa increased by 27.7%, ending the year quoted

at R$ 898.00. Its shares were traded during 100% of

the exchange’s sessions, with 70,460 total

transactions involving 5.2 million shares and a

financial volume of R$ 8,983.3 million.

On the NYSE, our ADRs appreciated 55.4%, quoted

at US$ 38.05, compared to a 0.6% decline of the

Dow Jones Index. Total trading volume was

US$ 3,890.9 million.

AmBev’s market capitalization at the end of the year

was equivalent to R$ 53.6 billion, compared to a

market capitalization of R$ 40.4 billion in 2004.

Shares as an Investment

Jan-00

350%

300%

250%

200%

150%

100%

50%

0%

400%

450%

Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04 Jul-04 Jan-05 Jul-05 Dec-05

Stock performance on the Bovespa (1)

AMBV4 AMBV3 Ibovespa

(1) Historical series adjusted by the bonus occurred in May 2005. (2) Announcement of business combination with Interbrew

(2)

2005 | Annual Report | AmBev .59

Board of Directors

Co-chairmen

Victório Carlos De Marchi Carlos Alves de Brito – elected in 2006

Directors

Marcel Herrmann Telles Carlos Alberto da Veiga SicupiraJosé Heitor Attilio GraciosoRoberto Herbster GusmãoVicente Falconi CamposLuis Felipe Pedreira Dutra LeiteJohan M.J.J. Van Biesbroeck

Alternate Directors

Jorge Paulo Lemann Roberto Moses Thompson Motta

Fiscal Committee

Members

Alcides Lopes Tápias Álvaro Antônio Cardoso de SouzaAntônio Luiz Benevides Xavier

Alternate Members

Ary WaddingtonEmmanuel Sotelino SchifferleNilson José Bulgueroni

60. AmBev | Annual Report | 2005

The Team

2005 | Annual Report | AmBev .61

Executive Directors

Chief Executive Officer for Latin America

Luiz Fernando Edmond

Chief Executive Officer for North America

Carlos Alves de Brito

Executive Officer for Hispanic Latin America

Juan Manuel Vergara Galvis

Chief Financial and Investor Relations Executive Officer

João Castro Neves

Sales Executive Officer

Bernardo Pinto Paiva

Marketing Executive Officer

Carlos Eduardo Lisboa

Industrial Executive Officer

Cláudio Braz Ferro

Soft Drinks Executive Officer

Francisco de Sá Neto

Corporate Affairs Executive Officer

Milton Seligman

General Counsel

Pedro de Abreu Mariani

People and Management Executive Officer

Ricardo Wuerkert

Shared Services and IT Executive Officer

Jean-Yves Rotte-Geoffroy

Quinsa Executive Officer

Agustín García Mansilla

Financial Section

62. AmBev | Annual Report | 2005

2005 | Annual Report | AmBev .63

Contents

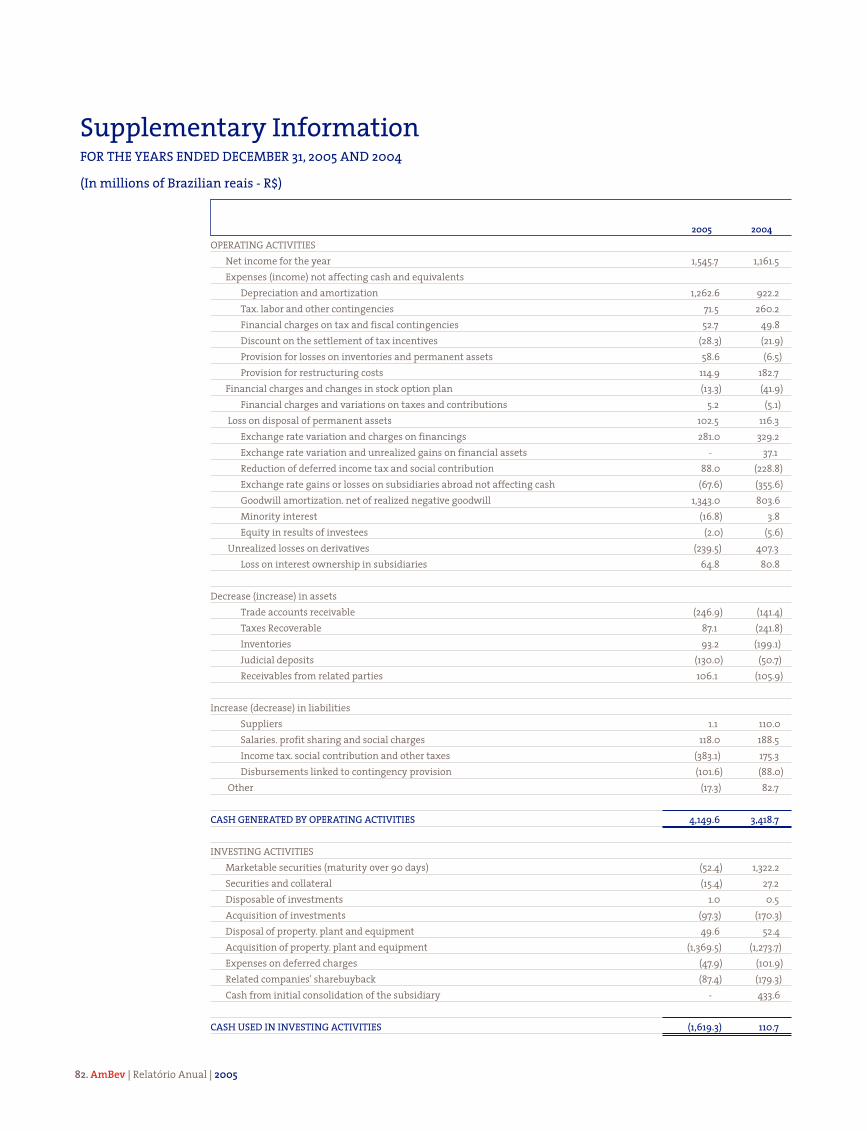

1. Management Report 642. Independent Auditor's Report 743. Fiscal Comittee Report 754. Balance Sheets 765. Income Statements 786. Statements of Changes in Shareholders' Equity 797. Statements of Changes in Financial Position 808. Supplementary Information 829. Note to Financial Statements 84

10. Investor Information 115

64. AmBev | Relatório Anual | 2005

Overview of Companhia de Bebidas das Américas – AmBevWith operations in 14 countries of the Americas, AmBev is the fifth world’s largest brewer and the leader in the LatinAmerica. Ambev’s operations consist of the production and trading of beer, draft beer, soft drinks, other non-alcoholicbeverages and malt and are divided into three business segments:• Brazil Operations, represented by sales of (i) beer (“Beer Brazil”); (ii) carbonated soft drinks (CSD) and non-alcoholic,

non-carbonated (Nanc) beverages; and (iii) malt and by-products;• Hispanic Latin America (HILA), represented by AmBev’s current stake of 59.2% in Quinsa (Argentina, Bolivia, Chile,

Paraguay and Uruguay), as well as the Company’s operations in Northern Latin America (El Salvador, Equator,Guatemala, Nicaragua, Peru, Dominican Republic and Venezuela); these last operations, grouped, are designatedby HILA-ex (HILA excluding Quinsa); and

• North America represented by Labatt Brewing Company Limited (“Labatt”) operations, including beer domesticsales in Canada and exports to the United States (“USA”).

Major AmBev’s brands include Skol (the third most consumed beer in the world), Brahma, Antarctica, Bohemia,Original, Quilmes, Labatt Blue, Brahva and Guaraná Antarctica. In addition, AmBev is PepsiCo’s largest bottlingcompany outside of the USA. Through a franchising agreement, the Company sells and distributes Pepsi productsin Brazil and other Latin American countries, including Pepsi, Lipton Ice Tea and Gatorade.

AmBev’s credit risk as debt issuer in domestic and foreign currency is investment grade according to Standard andPoor’s and Fitch Ratings.

Financial Highlights 2005The following financial and operational information, unless otherwise stated, is presented on a consolidated basisand in thousands of Reais, pursuant to the Brazilian Corporate Law. All comparisons, unless otherwise stated, refersto 2004.• AmBev’s consolidated EBITDA reached R$ 6,305.1 million in 2005, growing 39.0%.• According to ACNielsen, Ambev’s market share in Brazilian beer market in 2005 was 68.3% (2004: 66.2%). Beer

Brazil segment’s volume grew 8.2% and the revenue per hectoliter reached R$ 129.9.• CSD & Nanc EBITDA margin reached 31.4%, an increase of 210 basis points, which kept AmBev as an industry