A SnApShot of EuropEA n plAtformS - Fund Platform...

45

A SNAPSHOT OF EUROPEAN PLATFORMS Today and in the future This paper has been prepared by: Luxembourg, February 2013

-

Upload

truongkiet -

Category

Documents

-

view

213 -

download

0

Transcript of A SnApShot of EuropEA n plAtformS - Fund Platform...

A SnApShot of EuropEAn plAtformS

Today and in the future

this paper has been prepared by:

Luxembourg, February 2013

About The AuthorsThis report was commissioned by the Fund Platform Group (FPG). The survey was carried out by Cerulli and The Platforum conducted follow-up interviews and wrote the report.

The survey was conducted over a four week period throughout October 2012 among some of the most influential platform groups, fund buyers and fund sellers across Europe. It sought the opinions of key players in the platform industry regarding future development opportunities, challenges and growth outlook.

The Fund Platform Group (FPG)The Fund Platform Group was established in 2011 in Luxembourg as a trade association made up of the largest fund platform providers with a European reach to build relationships and promote understanding between all stakeholders in the global fund distribution platform business.

Through the promotion and development of our industry, the FPG aims to establish high professional standards and facilitate the efficient and secure distribution of investment funds to end investors.

www.fundplatformgroup.com

Cerulli AssociatesCerulli Associates is a Boston headquartered independent asset management research firm with international offices in London and Singapore. The firm was established 20 years ago, and produces actionable research on asset management markets in over 45 countries around the world. For more information on Cerulli and the research we undertake, please visit www.cerulli.com. The Platforum The Platforum is a London-based specialist research firm with a focus on European investment platforms. In 2012 we published our first report on European platforms and distribution, imaginatively named The European Platform Guide.

Our extensive and senior external network supports our research which is principally qualitative. Drawing on data and interviews, our research paints a picture today but also provides opinion on how changes to distribution, products and regulation will shape the landscape moving forward.

Our clients include global fund managers, life companies, platforms, distributors and IFAs – anyone who wants to understand how retail distribution works in Europe and how to develop the best products and strategy for these markets. Excerpts of our research can be seen at www.theplatforum.com/research

Images © Istock: (chapter openers) Black Ink Designers, Corp. and pp19 Bruno Passigatti. Shutterstock: pp 6 Bedrin.

3 A Snapshot of European Platforms

forEword

When a handful of fund distribution platforms started to meet informally in Luxembourg back in 2010, we all shared the belief that the dynamics at play in our industry were about to produce some very important consequences in our respective businesses. We all wanted to be active participants in the process, and to benefit from these new dynamics by aligning our business models to the changing environment.

Despite all our differences in terms of business models, we knew that common global themes were forcing dramatic changes across the whole value chain of retail financial services. One of the protagonists at the heart of these changes is the platform, sitting between the manufacturers of financial products and the distributors of these financial products. Interestingly enough, despite this unique position, prior to establishing this Group, fund platforms had not been able to collectively express their views, share their experiences with other market participants and offer suggestions on how to address these new challenges.

This was the main reason for the creation of the FPG back in 2011 with the ultimate objective of facilitating the efficient and secure distribution of investment funds to end investors.

Across Europe there are many different platform models, servicing a large variety of distributors from independent advisers to banks. This diversity is one of the strengths we want and hope to grow within the FPG through a broad membership base across Europe and the quality of the initiatives we launch together.

After having completed our first year of activity, we at FPG felt it would be beneficial for all industry participants if we commissioned and produced research on the future of platforms. We have chosen to team up with two very well respected research companies for this project, Cerulli Associates and The Platforum. They have both produced some outstanding contributions to make this piece of work what it is today. We are very grateful to both of them and honoured by their support for our initiative.

As we go to press, those in the UK are in the final stages of preparing for the RDR and the final details of MiFID II are still being actively discussed in Europe. The only certainty in our businesses is that more changes are waiting at the door!

We do hope this piece of work will help our readers to enrich their thinking when planning ahead for the future.

The FPG Board of Directors, Luxembourg, February 2013.

A Snapshot of European Platforms 4

IntroductIon to thE SurvEy

In June 2012, the Fund Platform Group (FPG) decided to conduct some research with the aim of identifying some of the key challenges and changes faced across Europe by those working in retail financial services.

The survey questions were agreed between the FPG, Cerulli and The Platforum and administered via Cerulli’s bespoke survey platform. Subsequent interviews were conducted by The Platforum who wrote the report with input from the Fund Platform Group members and Cerulli.

In total, 70 participants took part in the survey with a mix of fund buyers (13%), fund sellers (51%) and fund platforms (26%) as well as a selection of other industry players including trade associations and service providers. The views were representative of a broad range of European countries including the five major markets (UK, Spain, Italy, France and Germany).

The survey participants

The Platforum also conducted more detailed interviews with distributors, platforms and fund managers across Europe. Our thanks to the following people in particular for their contributions:

Edouard Bokuetenge, Chairman of the Fund Platform GroupEd Dymott, Head of Business Development at Fidelity FundsNetwork Mark Elliot, Managing Director at BlackrockOlivier Huby, CEO at MFEXRichard Lepere, CEO, Fund Channel Paul Malpas, Head of UK Wholesale Distribution at Nordea Asset ManagementJohn Martin, Managing Director at PraemiumStephen Mohan, MD of Operational Services at CofundsJohn Pauly, CEO of Moventum SAJohn Salmon Partner at Pinsent Masons Tina Soderlund-Boley, Head of Northern European Institutions and Intermediaries at GAMFrank Wagner, Product Manager at attrax SA

* Others include transaction networks, trade associations, data/documents service providers, global custodians, universal bank, retail banks and brokerage firms.

Fund buyer 12.9%

Fund seller 51.4%

Fund platform 25.7%

Others 10.0%*

5 A Snapshot of European Platforms

SECTION 1 7OPEN ARCHITECTuRE AND FuNDS 8

1.1 If you offer fund distribution services, what type of architecture do you use? 81.2 What will happen to the demand for open architecture solutions across Europe over the next three years? 91.3 In your opinion what proportion in open architecture European platforms will be held by the top 10 managers (by AUM) in 2015? 121.4 If you are a fund buyer, have you seen an increase in the number of markets a fund is being distributed in compared to two years ago (2010)? 13

SECTION 2 14CHANGES TO DISTRIBuTION 15

2.1 Please rank the following distribution channels based on their growth potential in the next 3 years to 2015. 15

SECTION 3 20PLATFORM SERvICES 21

3.1 Platform services today and in 2015 ranked by fund buyers. 213.2 Platform services today and in 2015 ranked by fund sellers 223.3 Platform services ranked in order of importance today and in 2015 23

SECTION 4 24REvENuE, REBATES AND THE P&L 25

4.1 Based on the upcoming regulations, will European platforms be paid by fund manager rebate as opposed to via an explicit fee in 2015? 254.2 By 2015, which participant on the fund distribution value chain will pay for services provided by European platforms? 274.3 Which regulations will have the biggest impact of your cost base? 284.4 Which regulations will have the biggest impact on your revenue generating potential? 294.5 Based on the additional cost and expected revenue on regulations, how do you expect your profit margins to change at the end of 2012 and going forward to 2013? 30

SECTION 5 32GROWTH AND CHANGE 33

5.1 How do fund sellers expect the number of global agreements with platforms to change in 2015? 335.2 Which type of arrangements do fund buyers prefer to set up with platforms and is this expected to change in 2015? 345.3 How many markets will a fund typically be sold in by 2015? 345.4 Do you expect further fund consolidations/closures in the industry? 355.5 How much do you expect the number of funds to fall by at the end of 2013? 365.6 Do you think European platform assets will grow or stay at similar levels 385.7 What, in your opinion, will we see happen to the European platform market over the next three years? 395.8 If you are a European platform, which other markets are you considering expanding to? 415.9 What are the platform opportunities in Asia 42

SECTION 6 43CONCLuSIONS 44

contEntS

6

ExEcutIvE SummAry

• 68% of platforms believe that the demand for open architecture solutions across Europe will continue to increase

• 56% of fund buyers do not think that demand for open architecture solutions will increase by 2015 whereas 72% of fund sellers think it will. Fund buyers are largely satisfied with the amount of product and the number of managers they have available today

• 67% of platforms believe that more than 60% of funds will be held by 10 managers in 2015, whereas just 33% of fund buyers believe they will see these levels of concentration. The global reality of purchasing behaviour is more common than individual fund buyers and distributors believe

• The distribution channel thought most likely to represent growth across Europe is the retail bank, although private banks top the polls in the Nordics, Switzerland, Central Eastern Europe and Continental Europe. In the UK, funds-of-funds are thought to represent the best growth opportunity

• Today, fund manager rebate negotiations are the most valued service provided to fund buyers by platforms. In just three years this is expected to be the least important

• Fund sellers consider the role of transaction, execution and settlement services to be core to the function of a platform both now and in 2015

• Fund buyers and fund sellers are almost twice as likely as fund platforms to believe that platforms will be paid by rebates in 2015. Only 29% of platforms believe they will be paid by fund managers in 2015

• 52% of fund managers anticipate lower margins in 2013 with 51% of all respondents predicting an impending margin squeeze

• Without exception, MiFID II is seen as the most expensive piece of regulation to implement

• 71% of respondents believe that European platform AUA will grow in the future

• 53% believe that the European platform market will consolidate around a few champions

• Globalisation is in the air with 47% of asset managers anticipating that global agreements with platforms will rise

• 42% of platforms are looking to other European markets for growth, whilst 38% are looking to Asia

opEn ArchItEcturE And numbEr of fundS

1

A Snapshot of European Platforms 8

opEn ArchItEcturE And fundS

Our first area for analysis was around open architecture. Just how important is the concept, what does the concentration of funds look like and are we seeing more cross-border activity?

1.1 If you offer fund distribution services, what type of architecture do you use? 82% of platforms and 58% of fund sellers operate in an open architecture environment today.

The vast majority of European platforms operate in an open architecture environment with 82% offering full open architecture. This is consistent with global trends we have seen over the last decades. The customer demand for open architecture has been one of the primary accelerants of platform growth.

Richard Lepere, CEO of the international platform Fund Channel comments, “Open architecture is here to stay. Any investor is going to look for a broad choice of product, not just the ‘in-house’ product.”

Similarly, Frank Wagner, Product Manager at attrax S.A. feels that “Open architecture will remain very important for the whole market and platforms will continue to offer the full range of products. On the other hand single distribution units such as banks will focus more and more on a small guided or closed universe in order to cut costs, driven by increasing statutory regulations such as training, documentation etc.”

Unsurprisingly, more fund managers than platforms today operate in a closed architecture environment. Some fund managers have been naturally hesitant to embrace this trend, fearing loss of market share and the ‘guaranteed’ distribution offered by proprietary channels.

9 A Snapshot of European Platforms

Although the term ‘guided architecture’ can have negative connotations, it is also true that we see great concentration across the platform market in terms of which fund managers customers actually invest in. Despite the thousands of funds on offer, Fund Channel tells us that just 26% of all active funds on the platform represent 90% of the volume of their total business.

Nonetheless, natural selection leading to a common choice of manager is NOT the same as operating within a limited guided architecture market. So the message is that customer choice is here to stay – even if the reality is that very consistent decisions are made by fund buyers across Europe.

We take more detailed look at how concentrated the market is on p12.

1.2 What will happen to the demand for open architecture solutions across Europe over the next three years?

56% of fund buyers do not think that demand for open architecture solutions will increase by 2015 whereas 72% of fund sellers think it will. Is this the triumph of hope over experience, from an army of fund managers keen to sell – or does it tell a story of largely satisfied fund buyers today?

This is the first area where we identify some key difference in opinions between the fund buyers, the platforms in the middle and the fund sellers, or fund managers.

The majority of fund buyers do not anticipate increase in demand for open architecture solutions. Interestingly, they are also the only group not to envisage any decrease in demand. This is a fairly clear indicator that many fund buyers are happy with the number of managers and funds they have access to - they are comfortable with the status quo.

It is a well-documented fact that the European fund market is saturated. There are too many funds. So why do some think there will be more appetite for open architecture in the future?

opEn ArchItEcturE And fundS

A Snapshot of European Platforms 10

The following chart confirms that there were more than 28,000 funds in the European market as at August 2012. Although the number of funds has remained fairly static over the last five years, market growth has been as a result of a higher balance per fund, rather than yet more fund proliferation.

We also know that every single platform operating anywhere in the globe today will point to a plethora of funds on the platform which are not well supported. Although a sensitive area and so difficult for us to be specific, many platforms tell us that more than 50% of their assets are with just 10 fund managers. So although the practical voice of logic suggests that we have an excess of funds and unsupported product, when it comes to the general demand for open architecture, platforms anticipate growth continued demand for the service.

European Mutual Funds by Number and Average Size, 2008-August 2012

Source: Cerulli Associates in association with Lipper FMI

Why might we see an increased demand for open architecture solutions in Europe, when in practice, the same fund manager brands tend to dominate a concentrated European platform market (with some local brand exceptions?)

It is easy to understand why fund sellers want to believe we will see more open architecture. For those boutique managers, without large brands and wide distribution support, platforms are a lifeline they need in order to survive in a lower-margin, increasingly competitive environment. For any fund manager, a platform offers the opportunity to outsource some non-core activity and get access to important distributors.

67% of platforms believe they will see more demand for open architecture solutions. One could argue that this is a self-serving belief but global experience does suggest that the gradual march away from a closed architecture distribution model is inevitable, and will be accelerated by changing regulation, consumer expectations and more explicit charging models.

opEn ArchItEcturE And fundS

11 A Snapshot of European Platforms

We can clearly see the green shoots of change as the general global consumer trends of choice and transparency are driving change through some bank-dominated markets where those delivering product to the consumer have not always been the best at making those products.

However, not everyone believes that demand for open architecture will continue apace. John Pauly, CEO of platform Moventum, believes that changes in charging structures may in fact reduce demand for open architecture from fund buyers. He identifies four categories of fund buyers:

• Funds of funds and their custodians – “they will most likely support open architectures as a gateway to products for as long as market inefficiencies remain”

• Retail investors advised by banks – “this channel is the most likely to become a closed rather than an open architecture environment due to pressures on margins and disclosures”

• Retail investors advised by IFAs – “this is difficult to call - my take is that they will continue to look for open architecture solutions, but at the same time, I do not see their market share increasing”

• Self-directed retail investors – “they will continue to feed business to open architecture internet B2C platforms, but by the same token, I do not see their market share increasing”

These are controversial opinions and ones driven by the economic realities of delivering products and solutions profitably, rather than a more utopian view of what customers might want (but not necessarily want to pay for).

The UK leads the way in 2013 with new revenue models which ban advisers from being paid by product providers. The UK is yet to assess the full impact but we have seen banks pull out of the mass affluent market and offer closed architecture solutions directly to clients; we have seen great consolidation in the IFA market and the adoption of model portfolios which are arguably guided architecture; and the anticipated growth in the self-directed market is anticipated by some to feed into packaged products from fund managers and life companies, rather than the “pick a fund from a list of 1000” models so common today. All of this points to a narrower fund universe, not the broader one anticipated by many.

So the speculated reduction in appetite for open architecture is a controversial one, but not one without some early evidence from the market most affected by new and emerging revenue models.

This debate is not over yet and will be re-assessed against the fluid regulatory backdrop for years to come.

opEn ArchItEcturE And fundS

For those boutique managers, without large brands and wide distribution support, platforms are a lifeline they need in order to survive in a lower-margin, increasingly competitive environment.

A Snapshot of European Platforms 12

1.3 In your opinion, what proportion of funds in open architecture European platforms will be held by the top 10 managers (by AuM) in 2015?

Platforms and fund sellers anticipate more concentration than fund buyers

• 67% of platforms believe that more than 60% of funds will be held by 10 managers in 2015

• 60% of fund managers believe that more than 60% of funds will be held by 10 managers in 2015

• Just 33% of fund buyers believe they will see these levels of concentration.

The Managing Director for Europe at a leading global asset manager told us, “If the platform is truly open architecture and used by independent advisers then maybe 50% will go to the top 10 groups. This would be higher if the platform was being used by a distributor as a purely a trading platform for their guided architecture partners.” This is a more conservative view than the consensus but still points to a highly concentrated market.

Fund platforms have consistently reported concentration of fund manager flows, despite the appetite for open architecture shown earlier. The international platform, Fund Channel, reports having 400 fund managers on the platform – 50% of these managers represent less than 1% of total volumes. There are clear questions about the sustainability of every fund manager in the market today.

Earlier in the report we heard that 56% of fund buyers did not anticipate any changes in the levels of demand for open architecture solutions in Europe. This, combined with the chart above, tells us that the platform customers (ie the fund buyers) believe

opEn ArchItEcturE And fundS

Fund buyers are more alike in their selection behaviour than they might realise and their perceptions of the depth of open architecture across Europe don’t quite match the aggregated reality seen by the platforms and the fund managers.

13 A Snapshot of European Platforms

that there will be less concentration than fund managers do– but also suggests that they are happy with current access provided to fund managers. This seems to indicate that fund buyers are more alike in their selection behaviour than they might realise and their perceptions of the depth of open architecture across Europe don’t quite match the aggregated reality seen by the platforms and the fund managers.

Most platforms point to growing concentration of product. One platform CEO told us, “If I look at the top 10 funds used by my clients, they’re typically all the same. This is in part down to natural selection and in part down to the herd mentality. Our clients are institutions and pride themselves on fund research and selection BUT the top 10 managers are always the same. It comes down to brand, performance, customer experience and relationship management.”

1.4 If you are a fund buyer, have you seen an increase in the number of markets a fund is being distributed in compared to two years ago (2010)? We asked this question to the fund buyers in the survey to ascertain whether the anticipated ‘globalisation’ is happening.

67% of fund buyers are seeing an increase in the number of markets any one fund is being distributed in

Holly Mackay, CEO of The Platforum, observes, “We see substantial growth in this area. Patterns of behaviour are being influenced by improving platform capability and increasingly international models. Platforms such as Allfunds, RBC Investor Services, MFEX and Fund Channel are all working with clients in a number of different domestic markets with significant common denominators in the fund range. Although we’re still some way off a true ‘pan-European’ platform, both fund buyers and sellers report seeing more cross-border activity.” As we will see in Section 5, these considerations are also expanding to Asia as more platforms assess potential in these markets.

opEn ArchItEcturE And fundS

No 33.3%

Yes 66.7%

2chAngES to dIStrIbutIon

15 A Snapshot of European Platforms

chAngES to dIStrIbutIon

We have been through a period of difficult markets, changing consumer expectations and substantial regulatory change. Distribution is changing across many European markets and we track here participants’ views on which distribution channels will see most growth across key European countries and regions.

2.1 Please rank the following distribution channels based on their growth potential in the next three years to 2015. Survey respondents were asked to rank 6 different distribution channels according to perceived growth potential and to allocate a score between 1 and 7. Separate countries and regions were identified and respondents asked to rank growth potential by region and channel.

Below are the aggregate findings across Europe. Retail banks are clearly out in front in terms of perceived growth opportunity – and the independent adviser channel is felt to represent the least growth potential. Interestingly, execution-only is thought to be the third most appealing distribution channel in growth terms across Europe.

1=least significant, 7= most significant

Clearly responses differed across the board depending on the region. As we will go on to see, in Central Eastern Europe it’s all about retail banks. In Switzerland, growth is anticipated in the private banking sector whereas the UK expects to see a jump in funds-of-funds. Continental Europe and the UK are the most bullish about the growth of execution-only.

Overleaf, we share charts specific to each region and assess perceived growth potential by individual distribution channels.

A Snapshot of European Platforms 16

2.1.1 uK

Compared to European countries with bank-dominated distribution, fund-of-funds have not historically been as popular with the UK IFA as in other markets. This is expected to change in the new charging environment in the RDR.

Most IFAs report that they will find it difficult, in a fee-charging environment, to service lower value portfolios in any way which does not involve a multi-manager or fund-of-funds product. Smaller clients will only pay a finite amount which doesn’t leave much time to create a bespoke investment strategy any more. Those clients who move to a non-advised environment are also likely to consider a ‘solution’ rather than a ‘product’.

As for retail banks, what can we say? The Brits just don’t like their banks and big brands such as HSBC and Barclays have all pulled out of giving advice to the mass market, typically customers with less than £100,000.

The impact of all of the above is a gap in the middle market which many think will be filled by growth in execution-only platforms.

chAngES to dIStrIbutIon

The Brits just don’t like their banks and big brands such as HSBC and Barclays have all pulled out of giving advice to the mass market

17 A Snapshot of European Platforms

2.1.2 Continental Europe

Continental Europe is still a bank-dominated arena with continued growth forecast in the private banking channel in particular. We are particularly interested in the emerging independent financial adviser market which is predicted here to offer higher growth potential than the retail bank and fund-of-fund models. That is change!

2.1.3 Central Eastern Europe

For Central Eastern Europe, it’s all about banks. One of the only IFAs in Hungary, who we interviewed for this report, told us that “across Europe as a whole there is great room for improvement in what we offer customers. There is still too much product sold – with high initial commissions – and not enough service offered. Even in the German market, where there is a relatively established IFA community, most observers say that these advisers are commission-focussed and salesmen. Although there are circa 100,000 registered IFAs in Germany, we are told that only circa 30,000 of these advisers are giving credible investment advice. The remaining 70,000 are described as salesmen.”

chAngES to dIStrIbutIon

A Snapshot of European Platforms 18

Despite this fairly damning view, he was clear that this was still much better than the general environment in Central Eastern Europe where advice was bank-led, commission-led, in-house investment product-led and – in his opinion – of generally poor quality.

2.1.4 Switzerland

Those respondents with experience of the Swiss market identified private banking and fund-of-funds as the principal channels for growth, with execution-only bucking the general trend and sitting at the bottom of the pile.

Switzerland has historically been a market dominated by the big local players (UBS and Credit Suisse). There is plenty of reported local demand from private banks in particular for alternative service providers to bring additional transparency and efficiencies to the distribution chain. It remains to be seen how new entrants will be able to capture a piece of the action and which type of business model will eventually prevail: one-stop shopping or an unbundled approach.

chAngES to dIStrIbutIon

19 A Snapshot of European Platforms

2.1.5 Nordics

The principal areas of anticipated growth in the Nordics are private banks and funds-of-funds. Sweden in particular is named by many global fund managers as a retail market of growing interest.

chAngES to dIStrIbutIon

There is plenty of reported local demand from private banks in particular for alternative service providers to bring additional transparency and efficiencies to the distribution chain.

3plAtform SErvIcES

21 A Snapshot of European Platforms

plAtform SErvIcES

Let’s turn the spotlight onto the platforms. What services are they providing and what do their customers value?

3.1 Platform services today and in 2015 ranked by fund buyers. Today, fund manager rebate negotiations are the most valued service provided to fund buyers by platforms. In just three years this is expected to be the least important.

1=least important, 7=most important.

Perhaps one of the most interesting findings from this report is that today, fund buyers feel that the most important service provided by a platform is fund manager rebate negotiations. In just three years’ time, it is felt that this will be the least important service provided. That’s a dramatic change.

In the Italian market, most distributors today (even those using a platform) will still negotiate directly with the fund managers. This is a bank-dominated market with concentrated, big distributors who are big enough to negotiate direct with the managers.

Curiously, the least important service was the transaction, execution and settlement. This was once the very reason why a fund buyer would engage with a platform. Today, this has become such a commodity that it is the ‘value added’ services which really resonate with customers. Fund databases were second in importance today and felt to be of most importance in 2015.

Stephen Mohan, Managing Director of Operational Services at Cofunds, was surprised by some of these findings. “Economic theory tells you power flows toward the end customer in maturing markets. For this reason, it is logical that platforms will lose some of their negotiating power other than as scale representatives of small distributors. Consequently, one would expect large distributors, e.g. banks, to expect little value from platforms in this area, but small brokers, e.g. UK IFAs, to want to retain and support it.

A Snapshot of European Platforms 22

To me the surprise is the low level of value placed upon custody – particularly amongst buyers. In early 2008, I would have expected this, but the safety of client assets is increasingly of concern to regulators and more obviously fragile.”

Let’s now look at what the fund sellers, or the fund managers, value from platforms.

3.2 Platform services today and in 2015 ranked by fund sellers

1=least important, 7=most important.

Once again we see the fascinating tension between what fund buyers want from a platform – and what fund sellers want. For the fund managers, it’s all about effectively sourcing transaction, execution and settlement to an aggregator. Whilst this excites the fund managers, it has become a pure commodity for the distributors, or fund buyers.

Echoing the view that transaction services are the most important ones, Mark Elliot Managing Director and Head of EMEA Sales Strategy at Blackrock ranks the importance of the various platform services as follows, “Transaction execution and settlement, custody service, reporting and MI, fund documentation, fund manager rebates, then the fund database”.

Most fund managers we talk to cite good MI as a key function of any platform. In a world where fund managers are feeling increasingly disintermediated from the end customers, they rely on platforms to supply this management information which helps them understand distributor and end-customer behaviour.

In Section 4 we assess the revenue chain and just who will be responsible for paying the platforms. The UK regulator has mandated that platforms will need to be paid by customers – not by fund

plAtform SErvIcES

23 A Snapshot of European Platforms

manager rebates – in future. This has a subtle impact on who the customer is, and in turn, what will drive a platform’s development agenda.

In the past, platforms have been paid for by the fund managers. If they are increasingly paid for by the end customer then the development agenda will likely change and be less about keeping the fund managers happy, and all about keeping distributors and importantly, the end customer happy. In such an environment, databases, documentation and reporting will likely become more important services for platforms to do well.

3.3 Platform services ranked in order of importance today and in 2015

1=least important, 7=most important.

If we add the opinion of the fund buyers to that of the fund sellers, the above chart highlights the difference in opinion about what the most important jobs a platform does actually are.

• Sellers consider the role of transaction, execution and settlement services to be core to the function of a platform both now and in 2015.

• Current buyers consider rebate negotiations to be of paramount importance but this falls away by 2015

Frank Wagner, product manager for attrax shares his view on why the importance of rebate is diminishing: “In our opinion the decrease of the platforms rebate negotiation role is a result of two key impacts.” We cite these below.

• MiFID II could lead to the ban of commissions and therefore the negotiation of rebates would be obsolete• As platforms across Europe reach critical size and their percentage part of the administration fees just

can’t go any higher, we see less differentiation in the deals which platforms can cut and it becomes harder to make price a competitive advantage.

In the next section, we explore this issue of rebates and revenues in some more detail.

plAtform SErvIcES

4rEvEnuE, rEbAtES And thE p&l

25 A Snapshot of European Platforms

rEvEnuE, rEbAtES And thE p&l

Having seen the role which platforms play and the services they provide, there remains some doubt about the impending regulatory changes and exactly how platforms will be paid for the services which they provide.

4.1 Based on the upcoming regulations, will European platforms be paid by fund manager rebate as opposed to via an explicit fee in 2015? Fund buyers and fund sellers are almost twice as likely as fund platforms to believe that platforms will be paid by rebates in 2015

This chart is very interesting and we see significant disparity in the platforms’ interpretation of the regulatory direction of travel and the fund buyer and sellers’ view of the future.

The UK is the obvious market where the introduction of the RDR in 2013 will mean that platforms cannot be paid by fund manager rebate.

From 2013, all platforms will operate an unbundled charging model and will be paid directly by the client. Most platforms have a centralised cash account which will collect distributions and contributions, and pay the platform and the adviser charges. Any rebates which are paid by fund managers to platforms must be reimbursed to clients in the form of unit rebates. Cash rebates have been banned.

This is game changing for fund managers. Speaking at The Platforum conference in London in October 2012, JP Morgan MD, Head of UK Retail, Jasper Berens, noted that “for years, fund managers have paid for platforms and paid for distribution. Not anymore. Our performance will be assessed net of the costs of platforms and advisers.”

A Snapshot of European Platforms 26

In regards to a potential RDR which would span all European fund markets, there are already isolated cases (like the Dutch market for insurance products) but whilst some argue this is undoubtedly the end goal, Europe is still a long way away from giving up on the lucrative world of commission-based distribution. And when combining the current state of banks controlling distribution and the regulators having already imposed a tsunami of different regulatory changes (EMIR, CSDR, etc.), many tell us they believe it is unlikely that a pan-European RDR type of regulation will be treated as a pressing urgency. Despite changes to the UK market, 56% of fund sellers canvassed believe that European platforms will still be paid by rebate in 2015.

Paul Malpas, Head of UK Wholesale Distribution at Nordea Asset Management does not believe that the changes we have seen in the UK will be rolled out to the rest of Europe.

“Clearly RDR is changing the platform business landscape in the UK, however I do not see RDR-like legislation being rolled out across the rest of Europe any time soon. I would go as far as to say there are jurisdictions where an attempt to open the market in the same way as in the UK will more likely lead to less choice and higher costs to the end investor, a fact that is not lost on European regulators.”

Stephen Mohan, Managing Director of Operational Services at Cofunds, believes that platforms will still be able to charge fund managers for some elements of the administration services provided.

“The UK is catching its breath before resuming the fight for flab. The next round will be signalled by the post CP12/12 policy statement expected at year end from FSA. Platforms will either be able to charge fund managers for some of the administrative costs which they have removed from in-house or third party administrators or they will force a lower cost share class on the firms which are attempting to use the FSA as a bulwark to their margins. The interpretation favoured by the regulator will require the administration charge – of perhaps 5bps - to be passed (potentially through multiple nominees) in units to bemused end investors.

“Europe still has some German Greens attempting to make MiFID replicate UK and Dutch regulation, but is likely to go for disclosure over protecting producers. In such circumstances, I cannot believe that platforms will be unable to charge the fund managers for administration and distribution.”

John Salmon, Partner at legal firm Pinsent Masons helps make the important distinction between the two areas of commission which are under scrutiny. Firstly, payments to independent financial advisers by way of commission and secondly, payment of platforms by way of fund manager rebate.

Recent comments from Europe do suggest that there may be a ban on the payment of independent financial advisers by commission. However the banning of rebates from fund manager to platforms is not yet on the agenda of MiFID II.

“The current draft of MiFID II that is currently being negotiated would mean that product providers are excluded from paying fees, commission or any non-monetary benefits to IFAs that provide investment advice to clients. The current draft makes it clear that an independent adviser shall not accept and retain fees, commissions or any monetary and non-monetary benefits paid or provided by any third party or a person acting on behalf of a third party in relation to the provision of the service to clients. It also makes

rEvEnuE, rEbAtES And thE p&l

27 A Snapshot of European Platforms

it clear that where an adviser receives fees, commissions or any monetary and non-monetary benefits from a third party while providing the service of portfolio management or independent investment advice, it must pass on in full any monetary benefit received by a third party to a client.

MiFID II does not currently refer to payments or rebates made by platforms and it is not clear whether this is an issue which the EU will tackle in the near future.”

With this backdrop it is interesting that only 29% of platforms believe they will be paid by fund managers in 2015. Visionaries with pragmatic crystal balls? Or pessimists?

4.1 By 2015, which participant on the fund distribution value chain will pay for services provided by European platforms? We then broke this question down into a little more detail about who exactly will be paying for platform services in the future.

There are very different views on this topical question. Interestingly it is the platforms which feel most sure that their services will be paid for by consumers.

Although the majority of platforms believe that the days of platforms being paid for by the fund managers are limited, opinion is divided about who will actually pay for platform services.

rEvEnuE, rEbAtES And thE p&l

A Snapshot of European Platforms 28

• 39% of platforms believe that the end customer will pay for the platforms

• 33% of fund buyers, or distributors, believe that the end customers will pay for the platforms

• 36% of fund sellers, or fund managers, believe that platform costs will be shared by fund buyers and fund sellers

In the past, platforms have been paid for by the fund managers. Although the final requirements of regulators across Europe are not yet clear on this specific point, we note that only 12% of fund managers today believe that they will pay a platform’s fees moving forward. 60% of fund managers thought that the fund buyers would have some part to play in paying for a platform’s fees moving forward.

4.2 Which regulations will have the biggest impact of your cost base? Without exception, MiFID II is seen as the most expensive piece of regulation to implement

1=least important, 7=most important

MiFID II gets a clean sweep across the board, followed by UCITs IV for fund buyers and fund platforms, and Solvency II for fund sellers. FATCA is also felt to be a significant concern by the platforms, in terms of the impact it will have on their cost base.

Ed Dymott, the Head of Business Development at Fidelity FundsNetwork is confident in his view that “MIFID II will certainly have the biggest impact on platforms across Europe, although the RDR is possibly a good indication of what may be coming down the line. FATCA, although increasingly being simplified, will also have a significant impact on platforms. Increasingly we are seeing regulators targeting the record keeping services, rather than asset managers. RDR, MIFID II, FATCA are examples where those firms closest to the customer are finding the changes most challenging. This is a trend we see continuing as regulators increasingly focus on consumer protection.”

rEvEnuE, rEbAtES And thE p&l

29 A Snapshot of European Platforms

4.3 Which regulations will have the biggest impact on your revenue generating potential?

1=least important, 7=most important

Again, it is MiFID II and UCITS IV which are generally felt to have the greatest impact of revenue generating potential.

Edouard Bokuetenge, Chairman of the FPG considers that “the above chart is quite logical in terms of the priority given by the respondents, knowing that a great majority of regulatory changes will likely have a negative financial impact on the fund distribution value chain. Some of the changes will decrease revenues, others will make providers change their risk profiles and increase their counterparty risk management and other regulatory changes will increase all of our costs. The only one that represents a positive hope in terms of revenue generation is UCITS IV as we all expect that it will not only preserve but increase the fantastic success of this brand.”

Ed Dymott, Head of Business Development at Fidelity, thinks that some of the above regulatory developments are in fact positive news for platforms as it can mean that fund managers play a smaller role in retail distribution and pass some of the work (and revenue opportunity) to platforms.

“With regulations increasingly forcing many asset managers to become ‘institutional’, this is good news for European fund platforms. The RDR in the UK, is a good example of the opportunity for platforms, as this regulation has seen many fund managers exit retail distribution, simply to pass this responsibility to the fund platform. We see regulation acting as a further catalyst for this trend.”

rEvEnuE, rEbAtES And thE p&l

A Snapshot of European Platforms 30

4.4 Based on the additional cost and expected revenue on regulations, how do you expect your profit margins to change at the end of 2012 and going forward to 2013? It is a consistent story of falling margins, although the majority anticipate a stable year in 2012, with the fund managers the most confident about maintaining margin.

2011-12

2012-13

Our final question in this section related to profit margins at the end of 2012 and 2013.

It is a consistent story of falling margins, although the majority anticipate a stable year in 2012, with the fund managers the most confident about maintaining margin. 50% of fund buyers anticipate lower margins this year.

Although the question focussed on the impact of the changing regulatory environment, there are other factors at play which alter expectations of profit margins.

rEvEnuE, rEbAtES And thE p&l

31 A Snapshot of European Platforms

Looking to 2013 and expectations of margin decrease are consistent across the board. 50% of fund buyers, for a second consecutive year, anticipate falling margins and fund managers have lost 2012’s seeming immunity with 52% anticipating poorer figures come 2013.

It is a time of widely documented margin squeeze for fund managers. Tina Soderlund-Boley, Head of Northern European Institutions and Intermediaries at GAM predicts that costs of running business will increase and these costs cannot be passed on to the end customer. “Margins will decrease. We will not be able to pass on increased costs to the end client.”

50% of fund platforms also anticipate smaller profit margins in 2013.

The response to this from the platforms is clearly to try and increase revenues or cut costs. In terms of increasing revenues, with basis point pressure, the only route is to grow AUA or to offer other services. Expansion into other markets is seen by some as the route to increased profitability and we explore this more on page 41. A return to vertical integration is on the cards for others.

Richard Lepere, CEO at Fund Channel, is not convinced that vertical integration from his platform perspective is the way forward. “If I do fund selection, well, I have not seen any evidence of this being economically viable for a platform. How do I get customers to pay for this? And the people I would need to deliver this service are entirely different from the team I have today. I tend to view a platform as quasi-industrial business and we cannot be good at everything.”

Those 25% of platforms which anticipate greater profit margins point to the benefits of scale, global expansion and cost control as the mechanism by which they will achieve this. There is also general consensus that at a time of margin pressure for all, many more groups are looking to outsource non-core functions and so the order book and pipeline for many platforms is looking healthy.

Olivier Huby, CEO at MFEX, feels confident as the platform moves into 2013.

“We expect fund managers’ margins to decrease except for a few funds with high demand and high performance that will retain some pricing power while their performance lasts.

We believe our margins will actually increase in 2013 and after because of the scalability of our systems. Platform business is driven by technology and scalability. Also important is the ability to offer a high quality product which will require only minor adaptations to serve new clients, hence the scalability and the rising margins. More fee generating assets with a stable cost structure.

We expect some price war from some platforms that are only able to compete on price and not on quality, technology or services. We expect the number of platforms to decrease over time as some business models based on offering the lowest price are clearly not viable over the long term. 2013 will see the beginning of the consolidation of the market”.

The continental European platform market feels more buoyant than the UK platform market which, with over 30 providers, is saturated, competitive and highly retail compared to her more institutional continental cousins.

rEvEnuE, rEbAtES And thE p&l

5growth And chAngE

33 A Snapshot of European Platforms

growth And chAngE

Platforms have arguably changed the nature of fund distribution and, with more platforms now offering services to more than just one market, we are seeing an increase in global agreements between fund managers and platforms and funds being sold in more and more jurisdictions.

5.1 How do fund sellers expect the number of global agreements with platforms to change in 2015? Nearly half of all fund sellers believe that global agreements with platforms are on the rise

As platforms take on a more international flavour and start to operate in multiple jurisdictions, 47% of fund managers anticipate seeing an increase in the number of global agreements they have. This can be a mixed blessing. Yes, it allows focus on key global accounts, a centralised approach and fewer, typically lengthy legal agreements. But it can also put pressure on margins given the disparity in TERs and rebate expectations globally.

Mark Elliot, Managing Director and Head of EMEA Sales Strategy at Blackrock has become “aware of an increase in the number of requests for global agreements with platforms and we continue to work with these platforms to ensure that the agreement we have in place reflects both the local and global relationship as well as local market conditions.”

One Managing Director, Europe, of a leading global fund manager was cautious and asked for his comments to be non-attributable. “I would expect the number of global agreements to increase slightly as platforms try to expand. The pricing is the hot issue as we fund groups need to be able to set the price client by client.”

Stay the same 47.4%

Decrease 5.3%

Increase 47.4%

A Snapshot of European Platforms 34

5.2 Which type of arrangements do fund buyers prefer to set up with platforms and is this expected to change in 2015?

From the perspective of the fund buyer, somewhat unsurprisingly, they prefer a global agreement. This is about ease and convenience and negotiating with as many assets as they can find across multiple countries. The difficulty for platforms is that different markets have funds with very different TERs, and very different rebate expectations. Giving away up to 70% in Italy might be OK, but it could kill your business in the UK. As we saw above, fund managers are very hesitant to lose any pricing control with individual, institutional clients.

5.3 How many markets will a fund typically be sold in by 2015? The consensus view is that a fund will be sold across 5-10 different markets by 2015. It is the fund sellers who believe most strongly that a fund will be sold in more than 10 different markets

1= least likely; 5 = most likely

growth And chAngE

Global agreements 83.3%

Single country/domicile agreements 16.7%

35 A Snapshot of European Platforms

Edouard Bokuetenge, Chairman of the FPG thinks that increasing globalisation is in line with one of the expected outcomes of UCITS IV, but warns of the costs of such expansion. “… the costs of penetrating new markets and sustaining a “speed to market” strategy remain very high and asset managers will continue to need support and partnership to achieve their bold ambitions. Any asset managers that have not had experience of selling their funds in multiple markets will need the support of global cross-border distribution players to facilitate their desired expansion.”

In line with fund managers selling a fund in more than one market, we have also observed a gradual increase in the number of international platforms ie those platforms not just focussing on one domestic market. Oliver Huby, CEO of MFEX, provides platform services in both Sweden and France today. He expects that global asset managers will sell their funds in at least 10 countries but smaller firms will focus on fewer markets. “Smaller managers will likely target two to five markets, as there are still many administrative burdens to distribute funds on a wider basis and it is costly to start selling abroad”.

5.4 Do you expect further fund consolidations/closures in the industry? Although respondents expect to see funds being sold in more market, there is also general consensus that both fund closures and consolidation are inevitable.

Future expectations, illustrated above, are reinforced by actual fund closures that have been happening over recent years. The chart on the following page shows the number of mutual fund closures that have taken place in the industry in the last five years, and is reproduced with permission from Cerulli.

growth And chAngE

A Snapshot of European Platforms 36

European fund closures from 2008 to August 2012

The latest available data confirms that 1,130 funds had been closed year to date as at August 2012. So funds are clearly being closed and expectations are that more will follow. But how quickly did survey participants anticipate the number of funds to fall?

5.5 How much do you expect the number of funds to fall by at the end of 2013?

Across all respondents, 62% anticipate a 10%-30% reduction in the number of funds in Europe over the next 12 months. Most respondents expect to see a reduction of 10-20% in the number of funds.

growth And chAngE

37 A Snapshot of European Platforms

Unsurprisingly it is the fund sellers, or fund managers, who anticipate the smallest amount of closures.

Paul Malpas, Head of UK Wholesale Distribution at Nordea Asset Management thinks that the number of funds will inevitably fall. “I believe cost reduction is a major driver for asset managers when it comes to rationalising their product range. This is invariably linked to the implementation of UCITS requirements and the associated administrative burden, so yes I believe numbers will continue to fall. In contrast to the industry as a whole, we continue to focus on launching both internally and externally managed funds as part of our multi-boutique strategy, so investors can expect to see an increasing product palette from Nordea.” This comment reinforces the paradox we hear about the number of funds in the industry. Whilst we might logically see that there are too many funds, not many want to be the ones to actually cull their product range.

Some believe that the number of funds will fall as we see consolidation of the fund managers themselves – and also cite UCITS IV as a driver of this trend . “Although new fund launches remain a key driver of growth in the investment funds industry, the continued consolidation at level of the asset managers is likely to result in a net reduction in the number of funds in the medium term. The UCITS IV Directive provides for the proper legal framework to avoid the current and future replication of an asset management firm’s funds offered across different markets”.

However not everyone we talked to thinks that a further fall in the number of funds is inevitable.

Edouard Bokuetenge Chairman of the FPG argues that “…some of the new regulations should have the effect of increasing the number of ISIN codes (e.g. RDR).” Edouard believes that a lot of rationalisation has already taken place as a result of the crisis of 2008 and the impact on the markets and returns. “From my perspective, the funds closures or consolidations in the coming months will not be driven by ‘product strategy’ but by the positive or negative evolution of the worldwide economy.”

Having assessed respondents’ opinions on the likely changes in the funds market, we then turned the focus onto platforms and asked whether growth in the platform space is anticipated. The majority view is that platform assets will grow, with only 21% of all respondents thinking assets would stay the same. No-one thought that platform assets were likely to fall.

growth And chAngE

It is believed that M&A activity and some fund management firms closing down will contribute to an overall reduction in the number of funds in Europe

A Snapshot of European Platforms 38

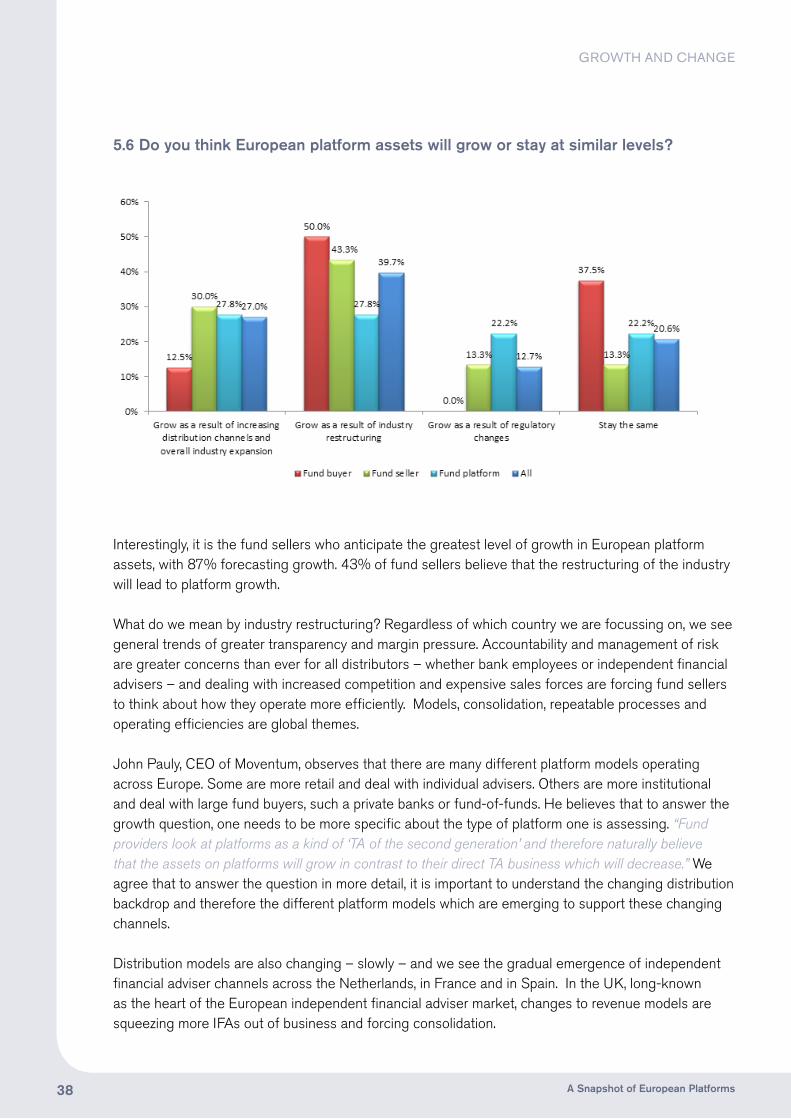

5.6 Do you think European platform assets will grow or stay at similar levels?

Interestingly, it is the fund sellers who anticipate the greatest level of growth in European platform assets, with 87% forecasting growth. 43% of fund sellers believe that the restructuring of the industry will lead to platform growth.

What do we mean by industry restructuring? Regardless of which country we are focussing on, we see general trends of greater transparency and margin pressure. Accountability and management of risk are greater concerns than ever for all distributors – whether bank employees or independent financial advisers – and dealing with increased competition and expensive sales forces are forcing fund sellers to think about how they operate more efficiently. Models, consolidation, repeatable processes and operating efficiencies are global themes.

John Pauly, CEO of Moventum, observes that there are many different platform models operating across Europe. Some are more retail and deal with individual advisers. Others are more institutional and deal with large fund buyers, such a private banks or fund-of-funds. He believes that to answer the growth question, one needs to be more specific about the type of platform one is assessing. “Fund providers look at platforms as a kind of ‘TA of the second generation’ and therefore naturally believe that the assets on platforms will grow in contrast to their direct TA business which will decrease.” We agree that to answer the question in more detail, it is important to understand the changing distribution backdrop and therefore the different platform models which are emerging to support these changing channels.

Distribution models are also changing – slowly – and we see the gradual emergence of independent financial adviser channels across the Netherlands, in France and in Spain. In the UK, long-known as the heart of the European independent financial adviser market, changes to revenue models are squeezing more IFAs out of business and forcing consolidation.

growth And chAngE

39 A Snapshot of European Platforms

John Pauly identifies two main drivers for the growth of platforms.

First, he describes the demand from institutional clients which look for efficiency gains that they can obtain by replacing multiple, complex and un-coordinated fund ordering routes, with a single gateway. For them, a platform is a standardised set of ordering pipelines, a single point of consolidation and an outsourced management of distribution agreements. “This demand will remain for as long as the market inefficiencies remain. But we have also seen in the past that market inefficiencies do not last forever.”

Secondly he points to the demand from retail clients via advisers which is very country specific and strongly driven by regulation and changes in market structure. He cites the recent growth of UK platform assets as being exclusively attributable to RDR.

“Overall, there is no uniform picture of the future of platforms. Depending on their offering and where they sit in the value chain and depending on what regulation does to this value chain, some of them will win whilst other will lose, but for all of them together, I believe that there will not be much growth in Europe.”

We asked respondents to share some views on what was likely to happen to the European platform market over the next three years.

5.7 What, in your opinion, will we see happen to the European platform market over the next three years?

Richard Lepere, CEO at Fund Channel, believes that consolidation is inevitable. “I am deeply convinced that the financial services industry will go through significant consolidation across all areas. The golden days are over and the overall size of the pie will shrink because profitability will revert to the mean. We will all see the consequences of changing remuneration models and those platforms without scale will be in a difficult position.”

growth And chAngE

A Snapshot of European Platforms 40

His views are echoed by Ed Dymott, Head of Business Development at Fidelity FundsNetwork who points to capital requirements and falling margins as key drivers of this trend.

“The platform market, both in the UK and across Europe is likely to see consolidation over the next five years. The significant levels of capital required to invest in these businesses, whilst seeing shrinking margins, will make the market difficult for many players. Like the research suggests, we see then development of global platforms, more challenging. Our experience suggests that areas such as asset servicing and fund custody can be done on a global basis, with similar core requirements across different jurisdictions. However, local record keeping and tax rules, typically require more focussed solutions, creating challenges in developing global wealth management capabilities. Although undoubtedly there is a growth in competition from new entrants, but also a number of technology and outsourcing providers, we believe very few will be long term players. Only those with very deep pockets will take any meaningful market share. We see the technology and outsourcing market the most challenging. If only three or four players can take any meaningful market share, this means this market for either a technology or outsourcing provider is limited, unless they can provide services on a global scale.”

Although we might believe that consolidation is inevitable, how in practice might this happen? It is our experience that actually attempting to merge two disparate platform technologies can be a very difficult exercise. Some platforms point to the opportunities of mergers with counterparties active in different territories, thereby accessing growth opportunities which may otherwise be elusive. Other simply say that smaller platforms without requisite scale may not be able to survive.

Some opinions are that globalisation is not that likely for platforms given some of the barriers to conducting business in multiple jurisdictions. Paul Malpas, Head of UK Wholesale Distribution at Nordea Asset Management believes that “The European platform business is highly fragmented with banks playing a major role in most jurisdictions via proprietary systems. Other than M&A activity I see little on the horizon that will break this status quo. It’s also no surprise to see market globalisation as the least likely outcome, when one considers barriers such as language, regulation and differing local market practices.”

Frank Wagner, Product Manager at attrax S.A thinks that talk of consolidation has been exaggerated. “Market consolidation around a few champions of fund platforms has been predicted for the last decade but we haven’t seen it yet. We believe that there is still enough space for a wider range of platforms to be profitable, mostly down to the by poor services provided by the CSDs (e.g. trailer fee negotiation, fund documentation etc.) If market regulation bans the payment of commissions, market consolidation will speed up and only platforms with additional services und earnings will remain.”

The jury remains out, although just 28% of respondents agreed with the view that there would be new entrants and infrastructures.

growth And chAngE

The platform market, both in the UK and across Europe is likely to see consolidation over the next 5 years.

41 A Snapshot of European Platforms

5.8 If you are a European platform, which other markets are you considering expanding to?

42% of European platforms think that growth opportunities are presented by other European markets, with Asia the next most appealing option

The source of growth for European platforms is largely felt to come from other European markets, although the UK is often mentioned in a separate breath as being a very different market. This is a story about growth and expansion in continental Europe.

Allfunds Bank is an example of an international platform which has expanded its operations from original parent Santander’s Spanish roots to operate in other juristrictions, including the UK, Italy, Luxembourg, Chile and Dubai.

Outside of Europe, 38% of participants in the survey pointed to Asia as providing opportunities. Asia is a great seductress, promising tales of opportunity and expansion, but she is seen by some as a fickle mistress. Everyone believes that Asia is a great opportunity but Asia is like Europe…it is a very fragmented market and so arguably doesn’t exist as a single concept. You have to look at each different market because China is so different to Malaysia, Singapore so different to Japan etc.

Singapore is generally reported to be the most interesting opportunity because of the private bank market there – this is the core target market of many European platforms. Additionally, SICAVs are sold in Singapore so the product environment is arguably more familiar.

Olivier Huby, CEO of MFEX, reports being interested in other European markets including Switzerland, the UK and Germany. He also sees potential in Asia, but he is less interested in the Middle East “as fund companies show some reluctance to distribute their funds in this area for compliance reasons. We would also not look to the USA for regulatory reasons.”

growth And chAngE

Asia is a great seductress, promising tales of opportunity and expansion, but she is seen by some as a fickle mistress.

Other European markets 41.7%

US 4.2%

Asia 37.5%

Latin America 16.7%

A Snapshot of European Platforms 42

5.9 What does it take to think about a platform in Asia?

A current trend on our radar is the expansion of more international platforms to the Asian markets1. Australian platform Praemium, with operations in the UK and Guernsey, has recently acquired Hong Kong based adviser software group Wealthcraft, and sees great potential for growth in these markets.

John Martin, CEO of Praemium, shares his views on the Asian opportunity.

“The market, in places platforms will focus, is broadly split between the international lifestyle investors (people who are working for global companies, living an expat life in a new country, or simply move countries on their career journey) and affluent/wealthy locals. That isn’t the case for mainland US, Australia, UK etc. where there is a very domestic focus and platforms will be domestic, running possibly on imported technology. Some main centres in Asia fit this profile well.”

Asset types and currency are slightly different - “if you include locals and expats, Asia likes equities as much as funds, plus local currency accounts not just Sterling, Euros and Dollars.”

Custody - “in Asia we have been asked for custody to be in Asia not in Europe. At the least they require an international “off-shore” centre such as Jersey.”

Regulation - “is getting stronger across the region but it is naturally different by country. A platform may need to seek authorisation in one jurisdiction but not another, it may restrict access to certain funds in Singapore but not in Hong Kong. In less regulated areas there may be no restrictions but covering AML requirements will be more complex.”

Commission v.s. fees - many advisers are running their business on up-front commission and some are moving to taking more regular commission as trail. However some are moving from commission to fees (the term RDR is often heard in Asia from advisers of expats). Whichever model, all want their fees or their commission from the platform, so rebates/retrocessions may go to the adviser or the investor.

“In summary, to think about the Asian market, I’d say you need flexibility in custody, currency, asset types and remuneration.”

1 The Platforum will be publishing The Asian Platform Guide in 2013

growth And chAngE

6concluSIonS

A Snapshot of European Platforms 44

concluSIonS

The common theme we heard from both the data and our interviews was a story of a continued need for open architecture solutions. Having said that, concentration of funds is getting more pronounced with the majority of platforms predicting that 70% of assets would flow to just 10 fund managers by 2015.

A great difficulty when writing any paper with a generic platform focus is that there are a varying number of platform models in Europe, which have all evolved in response to the different distribution dynamics of each market. Italy is very bank-dominated and the platforms are correspondingly highly institutional. The UK’s IFAs have been historically very fragmented and so platforms have been much more retail focussed. Looking to the future, each different European country has a slightly different focus. Switzerland, for example, is felt to offer great opportunity for those supporting the private banks. In continental Europe, insurance is felt to offer appealing growth potential.

As funds are sold in more countries, and as global agreements become more commonplace, the challenge for platforms is to deliver similar (or the same) underlying product in different jurisdictions with varying distribution channels at play.

Against the difficult backdrop of falling margins, fee pressure and the green shoots of increasing transparency, some believe that consolidation in the number of European platforms is inevitable. Scale continues to be a primary concern and platforms are looking to other European markets as well Asia for growth potential.

Although MiFID II has not made any pronouncements about banning rebates from fund managers to platforms, most platforms told us they believe this is an inevitable development. Although the fund buyers and sellers felt this would be less likely, there is a gradual reassessment from the platform clients about exactly what it is that they value from a platform. Today, rebate negotiations top the tables. In just three years’ time, expectations are that this will be least important feature. The redefines the value proposition for European platforms.

With an enormous amount of regulatory change across Europe, this is dominating development agendas and costs. MiFID II is seen as the most expensive piece of regulation to implement although we heard several interviewees cite UCITs IV as something which can support growth and additional revenues.

As we go to press, the UK regulator is on the brink of implementing the RDR, which has irrevocably altered the relationships between advisers, platforms and fund managers, with every piece of the value chain to be explicitly paid for by the customer. Opinion across Europe is divided about whether continental Europe will follow suit. We will be following with interest.

Thank you for reading this paper, we hope you have found it interesting and welcome feedback or comments.

Luxembourg, February 2013

The European Platform GuideReleased in March 2012, this report identifies the principal platforms in the major European markets. Whilst a pan-European platform is still in the making, more distributors and fund managers are seeking to make decisions at a European level. To date, there has not been one source of information about platforms in Europe.

This first guide identifies the major players, assess distribution in each specific country, positions each platform in its own sub-category (e.g. D2C, IFA, bank) and confirms their requirements from fund managers.

The European Platform Guide is available to purchase at £6,500 +VAT ($10,400, €7,900).

This report was published in March 2012. We are currently conducting research for the next edition, due to be published in March 2013.

Please contact Carmel Dickinson for more details: [email protected]

Founded in 1992, Cerulli Associates is a Boston-, London-, and Singapore-based research firm specializing in asset management and distribution trends worldwide. Cerulli Associates blends original research and data analysis to bring perspective to current market conditions and forecasts for future developments. Via a suite of research publications, Cerulli provides financial services firms with guidance in strategic positioning and new business development.

Cerulli’s repeatable, two-pronged proprietary research process (interviews and surveys) serves as the foundation of their published research and provides subscribers with the necessary context, intelligence, and key implications to navigate today’s and tomorrow’s market environment. Core product lines are complementary and subscription-based and include the Cerulli Report Series, and the Cerulli Edge series.

CONTACT uS

www.cerulli.com