A Project Report on Credit Risk Rating Analysis at SBI Commercial Branch

193

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch EXECUTIVE SUMMARY The State Bank of India has been, over the years, the flagship of Indian banking. State Bank of India is the largest bank in India with deposits of Rs 3,67,000 crores as on March 31, 2005. It dominates the Indian banking sector with a market share of around 20% in terms of total banking sector deposits. The increasing focus on upgrading the technology back-bone of the bank will enable it to leverage its reach better, improve service levels, provide new delivery platforms, and improve operating efficiency to counter the threat of competition effectively. SBI will maintain a good earnings profile in the medium term despite high pressure on yields due to the increasing competition in the banking sector. SBI’s earning profile is characterised by consistency in the return on assets (PAT/Average Assets), at around 1% per annum for the past three years, and diverse income streams. To maintain yields and pursue credit growth, the bank is aggressively targeting retail finance and small and medium enterprises (SMEs). The project was being undertaken at State Bank of India Commercial Branch, Belgaum. A study on Organisation, operations, products & services of State Bank of India was done. The project focuses upon the credit rating risk assessment practiced by State Bank of India. A brief study on M/s Margale Foundries was done. The Credit risk rating Babasabpatilfreepptmba.com Page 1

-

Upload

babasab-patil -

Category

Documents

-

view

239 -

download

0

description

Â

Transcript of A Project Report on Credit Risk Rating Analysis at SBI Commercial Branch

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

EXECUTIVE SUMMARY

The State Bank of India has been, over the years, the flagship of Indian banking. State

Bank of India is the largest bank in India with deposits of Rs 3,67,000 crores as on March

31, 2005. It dominates the Indian banking sector with a market share of around 20% in

terms of total banking sector deposits. The increasing focus on upgrading the technology

back-bone of the bank will enable it to leverage its reach better, improve service levels,

provide new delivery platforms, and improve operating efficiency to counter the threat of

competition effectively. SBI will maintain a good earnings profile in the medium term

despite high pressure on yields due to the increasing competition in the banking sector.

SBI’s earning profile is characterised by consistency in the return on assets

(PAT/Average Assets), at around 1% per annum for the past three years, and diverse

income streams. To maintain yields and pursue credit growth, the bank is aggressively

targeting retail finance and small and medium enterprises (SMEs).

The project was being undertaken at State Bank of India Commercial Branch, Belgaum.

A study on Organisation, operations, products & services of State Bank of India was

done. The project focuses upon the credit rating risk assessment practiced by State Bank

of India. A brief study on M/s Margale Foundries was done. The Credit risk rating

assessment mechanism, financial statements like Balance Sheet, Ratio Analysis of

Margale Foundries was studied. The area covered for the study of credit Rating Risk

Assessment of Margale Foundries by State Bank of India are the industrialists in and

around Belgaum who have availed loan facilities from State Bank of India. The Title of

the project is “A Study on Credit Risk Assessment of M/s Margale Foundries in State

Bank of India” The important findings of the study are during the year 2004-2005, the

current ratio was at 1.00 as against the estimate of 1.10. This is due to locking up of

receivables with SAME deutz Fahr India P. Ltd. The delay in realization of receivables

hindered the unit from producing upto the mark and selling more.

Some of the suggestions are the unit’s Current Ratio is 1, it should be improved by

infusing long term funds. As there was delay in realisation of receivables the unit should

take steps to stop supplying to default customers & try to acquire new customers. Banks

Babasabpatilfreepptmba.com Page 1

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

must have a MIS to enable them to manage and measure the credit risk inherent in all on

and off-balance sheet activities.

CONCLUSION

The banking system must be prepared to deal with the opportunities of higher growth,

and the challenges of ensuring more equitable growth. In dealing with the needs of rural

enterprises and of small and medium enterprises in urban areas, banks have to look for

new delivery mechanisms. These must economise on transaction costs and provide better

access to the currently under-served. To serve new rural credit needs, innovative channels

for credit delivery will have to be found. The State Bank of India is India's largest

commercial bank and is ranked one of the top five banks worldwide. It serves 90 million

customers through a network of 9,000 branches and it offers -- either directly or through

subsidiaries -- a wide range of banking services.

RISK MANAGEMENT

Risks are inherent in any financial intermediation and hence the bank is exposed to

certain risks that arise from its business and the environment within which it operates.

The bank has developed and is implementing various guidelines for managing risks like

setting up exposure limits, systematic internal controls and risk management systems

with consistent approach.

In order to manage risks, organizations need to be able to measure those risks

prospectively. They need to know, based on their current position, how much risk are

they taking. Organizations are addressing this challenge with statistical risk measures.

Babasabpatilfreepptmba.com Page 2

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

OVERVIEW OF BANKING SECTORThe first bank in India, though conservative, was established in 1786. From 1786 till

today, the journey of Indian Banking System can be segregated into three distinct phases.

They are as mentioned below:

Early phase from 1786 to 1969 of Indian Banks

Nationalisation of Indian Banks and up to 1991 prior to Indian banking sector

Reforms.

New phase of Indian Banking System with the advent of Indian Financial &

Banking Sector Reforms after 1991.

HISTORICAL PERSPECTIVE

Bank of Hindustan, set up in 1870, was the earliest Indian Bank . Banking in India on

modern lines started with the establishment of three presidency banks under Presidency

Bank's act 1876 i.e. Bank of Calcutta, Bank of Bombay and Bank of Madras. In 1921, all

presidency banks were amalgamated to form the Imperial Bank of India. Imperial bank

carried out limited central banking functions also prior to establishment of RBI. It

engaged in all types of commercial banking business except dealing in foreign exchange.

Reserve Bank of India Act was passed in 1934 & Reserve Bank of India (RBI) was

constituted as an apex bank without major government ownership. Banking Regulations

Act was passed in 1949. This regulation brought Reserve Bank of India under

government control. Under the act, RBI got wide ranging powers for supervision &

control of banks. The Act also vested licensing powers & the authority to conduct

inspections in RBI. In 1955, RBI acquired control of the Imperial Bank of India, which

was renamed as State Bank of India. In 1959, SBI took over control of eight private

banks floated in the erstwhile princely states, making them as its 100% subsidiaries. RBI

was empowered in 1960, to force compulsory merger of weak banks with the strong ones.

The total number of banks was thus reduced from 566 in 1951 to 85 in 1969. In July

1969, government nationalised 14 banks having deposits of Rs.50 crores & above. In

1980, government acquired 6 more banks with deposits of more than Rs.200 crores.

Nationalisation of banks was to make them play the role of catalytic agents for economic

growth. The Narsimham Committee report suggested wide ranging reforms for the

Babasabpatilfreepptmba.com Page 3

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

banking sector in 1992 to introduce internationally accepted banking practices.The

amendment of Banking Regulation Act in 1993 saw the entry of new private sector

banks.Banking Segment in India functions under the umbrella of Reserve Bank of India -

the regulatory, central bank. This segment broadly consists of:

1. Commercial Banks

2. Co-operative Banks

Nationalisation Of Banks In India

The nationalisation of banks in India took place in 1969 by Mrs. Indira Gandhi the then

prime minister. It nationalised 14 banks then. These banks were mostly owned by

businessmen and even managed by them. Before the steps of nationalisation of Indian

banks, only State Bank of India (SBI) was nationalised. It took place in July 1955 under

the SBI Act of 1955. Nationalisation of Seven State Banks of India (formed subsidiary)

took place on 19th July, 1960.

INTRODUCTION TO BANKING

Banks safeguard money and valuables and provide loans, credit, and payment services,

such as checking accounts, money orders, and cashier's checks. With the passage of the

Financial Modernization Act in 1999, banks also may offer investment and insurance

products, which they were once prohibited from selling. As a variety of models for

cooperation and integration between the financial services industries have emerged, some

of the traditional distinctions between banks, insurance companies, and securities firms

have diminished. In spite of these changes, banks continue to maintain and perform their

primary role in the financial system—accepting deposits and lending funds from these

deposits

TYPES OF BANKS

Babasabpatilfreepptmba.com Page 4

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

BANKS 1998-99

State Bank of India and Associates 08

Nationalized Banks 19Domestic Private Sector Banks 25

New Domestic Private Sector Banks 09

Foreign Banks 29

TYPES OF BANKING SERVICES

There are several types of banks, which differ in the number of services they provide and

the clientele they serve. Although some of the differences between these types of banks

have lessened as they begin to expand the range of products and services they offer, there

are still key distinguishing traits. Commercial banks, which dominate this industry, offer

a full range of services for individuals, businesses, and governments. These banks come

in a wide range of sizes, from large global banks to regional and community banks.

Global banks are involved in international lending and foreign currency trading, in

addition to the more typical banking services. Regional banks have numerous branches

and automated teller machine (ATM) locations throughout a multi-state area that provide

banking services to individuals. Community banks are based locally and offer more

personal attention, which many individuals and small businesses prefer. In recent years,

online banks—which provide all services entirely over the Internet—have entered the

market, with some success. However, many traditional banks have also expanded to offer

online banking, and some formerly Internet-only banks are opting to open branches.

The Indian Banking System:Under the Reserve Bank of India Act, 1934, banks were classified as scheduled banks

and non-scheduled banks. The scheduled banks are those, which are entered, in the

Babasabpatilfreepptmba.com Page 5

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Second Schedule of RBI Act, 1934. Such banks are those, which have a paid-up capital

and reserves of an aggregate value of not less than Rs.5 lacs and which satisfy RBI that

their affairs are carried out in the interest of their depositors. All commercial banks-

Indian and Foreign, regional rural banks and state co-operative

banks-are Scheduled banks. Non-Scheduled banks are those, which have not been

included in the Second Schedule of the RBI Act, 1934. The organized banking system in

India can be broadly divided into three categories:

(i) Commercial banks, (ii) Regional Rural Banks and (iii) co-operative banks. The

Reserve Bank of India is the supreme monetary and banking authority in the country and

has the responsibility to control the banking system in the country. It keeps the reserves

of all commercial banks and hence is known as the “Reserve Bank”. Commercial Banks

has been in existence for many decades. Commercial banks mobilize savings in urban

areas and make them available to large and small industrial and trading units mainly for

working capital requirements. After 1969 commercial banks are broadly classified into

nationalised or public sector banks and private sector banks.

COMMERCIAL FINANCING

The commercial financing model in Indian banking can be broadly categorized into project finance and working capital finance. These two segments form the pivot around which banks operate.

PROJECT FINANCE

Banks offer long term and short terms loans to business houses, corporations to set up their projects. These loans are disbursed after the approval from the banks’ core credit validating committee. In India, there are 11 national level land 46 state level financial and investment institutions that cater to long term funding requirements of the industry. The project finance segment is highly competitive with various players offering innovative schemes to entice corporate.WORKING CAPITAL

Babasabpatilfreepptmba.com Page 6

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

In order to meet the diverse needs and requirements of the business community, banks

offer working capital funds to corporate. Working capital finance is specialized line of

business and is largely dominated by the commercial banks. The Indian banking saw

dramatic changes in the last decade or so ever since the advent of liberalization and

India’s integration with the world economy. These economic reforms and the entry of

private players saw nationalized banks revamp their service and product portfolio to

incorporate new, innovative customer-centric schemes. The Indian banking finally woke

up to the surging demands of the ever-discerning Indian consumer. The need to become

highly customer focused (generated by high competitive levels) forced the slow-moving

public sector banks to adopt a fast track approach. Taking a leaf out of the private sector

banks, the public sector banks too went for major image changes (including corporate

brand building exercises) and customer friendly schemes. Marketing and brand building

programs were also given a new thrust in the new liberalized banking scenario.

Promotional budgets were hiked to cater to the new and large discerning target audience.

Banks were now keen on marketing their products and service though various mediums

to reach their core customers. Direct marketing, Internet marketing, hoarding, press ads,

television sponsorships, image makeovers etc. became an integral part of a bank’s

marketing mix. To meet the personalized needs of the customer and in order to

differentiate its services, banks repositioned themselves in specialized fields, like housing

loans, car finance, educational loans etc. to optimally service the customer. Permission

marketing became the new strategy that banks began to propound i.e. feeding the

customer (with his or her consent) with product and service information and thereby

enticing him towards the bank’s product service portfolio.

NEW GENERATION BANKING

The liberalize policy of Government of India permitted entry to private sector in the banking, the industry has witnessed the entry of nine new generation private banks. The major differentiating parameter that distinguishes these banks from all the other banks in the Indian banking is the level of service that is offered to the customer. Verify

Babasabpatilfreepptmba.com Page 7

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

the focus has always been centered around the customer – understanding his needs, preempting him and consequently delighting him with various configuration of benefits and a wide portfolio of products and services. These banks have generally been established by promoters of repute or by ‘high value’ domestic financial institutions. The popularity of these banks can be gauged by the fact that in a short span of time, these banks have gained considerable customer confidence and consequently have shown impressive growth rates. Today, the private banks corner almost four per cent share of the total share of deposits. Most of the banks in this category are concentrated in the high-growth urban areas in metros (that account for approximately 70% of the total banking business ). With efficiency being the major focus, these banks have leveraged on their strengths and competencies viz. Management, operational efficiency and flexibility, superior product positioning and higher employee productivity skills. The private banks with their focused business and service portfolio have a reputation of being niche players in the industry. A strategy that has allowed these banks to concentrate on few reliable high net worth companies and individuals rather than cater to the mass market. These well-chalked out integrates strategy plans have allowed most of these banks to deliver superlative levels of personalized services. With the Reserve Bank of India allowing these banks to operate 70% of their businesses in urban areas, this statutory requirement has translated into lower deposit mobilization costs and higher margins relative to public sector banks.

FUNCTIONING OF A BANK

Banking Regulation Act of India, 1949 defines Banking as "accepting, for the purpose of lending or investment of deposits of money from the Babasabpatilfreepptmba.com Page 8

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

public, repayable on demand or otherwise and withdrawable by cheques, draft, order or otherwise."

Banks essentially perform the following functions:

Accepting Deposits from public/others (Deposits) Lending money to public (Loans)

Transferring money from one place to another (Remittances)

Acting as trustees

Keeping valuables in safe custody

Government business

BANKING PRODUCTS

Banks in India have traditionally offered mass banking products. Most common deposit

products being

Savings Bank

Current Account

Term deposit Account

Lending products being

Cash Credit

Term Loans.

In view of several developments in the 1990s, the entire banking products structure has

undergone a major change. IT revolution has made it possible to provide ease and

flexibility in operations to customers. Rapid strides in information technology have, in

fact, redefined the role and structure of banking in India. Further, due to exposure to

global trends after Information explosion led by Internet, customers - both Individuals

and Corporates - are now demanding better services with more products from their banks.

Financial market has turned into a buyer's market. Banks are also changing with time and

Babasabpatilfreepptmba.com Page 9

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

are trying to become one-stop financial supermarkets. Market focus is shifting from mass

banking products to class banking with introduction of value added and customised

products. Products like debit cards, flexi deposits, ATM cards, personal loans including

consumer loans, housing loans and vehicle loans have been introduced by a number of

banks.

COMMERCIAL BANKING IN INDIA

India has a well developed banking system. Most of the banks in India were founded by

Indian entrepreneurs and visionaries in the pre-independence era to provide financial

assistance to traders, agriculturists and budding Indian industrialists. Indian banks have

played a significant role in the development of Indian economy by inculcating the habit

of saving in Indians and by lending finance to Indian industry.

The commercial banking structure in India consists of: Scheduled Commercial Banks and

Unscheduled Banks. Scheduled commercial Banks constitute those banks, which have

been included in the Second Schedule of Reserve Bank of India (RBI) Act, 1934. RBI

includes only those banks in this schedule, which satisfy the criteria laid down vide

section 42 (6) (a) of the Act.Indian banks can be broadly classified into nationalised

banks/public sector banks, private banks and foreign banks.

The commercial banking structure in India consists of:

Scheduled Commercial Banks Unscheduled Banks

Scheduled Banks in India constitute those banks which have been included in the Second

Schedule of Reserve Bank of India(RBI) Act, 1934. RBI in turn includes only those

banks in this schedule which satisfy the criteria laid down vide section 42 (6) (a) of the

Act.As on 30th June, 1999, there were 300 scheduled banks in India having a total

network of 64,918 branches.The scheduled commercial banks in India comprise of State

bank of India and its associates (8), nationalised banks (19), foreign banks (45), private

sector banks (32), co-operative banks and regional rural banks.

Babasabpatilfreepptmba.com Page 10

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

"Scheduled banks in India" means the State Bank of India constituted under the State

Bank of India Act, 1955 (23 of 1955), a subsidiary bank as defined in the State Bank of

India (Subsidiary Banks) Act, 1959 (38 of 1959), a corresponding new bank constituted

under section 3 of the Banking Companies (Acquisition and Transfer of Undertakings)

Act, 1970 (5 of 1970), or under section 3 of the Banking Companies (Acquisition and

Transfer of Undertakings) Act, 1980 (40 of 1980), or any other bank being a bank

included in the Second Schedule to the Reserve Bank of India Act, 1934 (2 of 1934), but

does not include a co-operative bank".

STATE BANK OF INDIAINTRODUCTION OF BANK

The Bank is actively involved since 1973 in non-profit activity called Community

Services Banking. All the branches and administrative offices throughout the country

sponsor and participate in large number of welfare activities and social causes. Its

business is more than banking because it touches the lives of people anywhere in many

ways.

SBI’s commitment to nation-building is complete & comprehensive

State Bank of India (SBI) was nationalised in July 1955 under the SBI Act of 1955.

Seven banks of SBI formed subsidiary and was nationalised on 19th July, 1960.

The State Bank of India is India's largest commercial bank and is ranked one of the top

five banks worldwide. It serves 90 million customers through a network of 9,000

branches and it offers -- either directly or through subsidiaries -- a wide range of banking

services.

HISTORY OF STATE BANK OF INDIA

The Imperial Bank of India

The origins of the State Bank of India go back to the early years of the nineteenth century. To Calcutta, then the capital of British India and a bustling city with an active mercantile community. It was in this environment that the Bank of Calcutta was established in 1806. Later renamed the Bank of Bengal, it was the first of the three Presidency

Babasabpatilfreepptmba.com Page 11

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Banks. The second, the Bank of Bombay, followed in 1840 and the third, the Bank of Madras, in 1843. Created out of the needs of the mercantile community the three Presidency Banks, nevertheless, introduced the banking habit to others and so helped to lay the foundation of a modern banking system in India. In 1921, the three Presidency Banks were merged to form the Imperial Bank of India. Inevitably, the Imperial Banks role expanded. It became the premier bank in India .And till the creation of the Reserve Bank o India in 1935; it was entrusted with certain Government banking functions.

Including the cash work of the Government. However, its growth was confined to commercial centers leaving almost three fourths of India untouched. In banking terms, while urban India progressed, rural India stagnated

The State Bank of India

In 1947 came Independence. And with the era of economic planning began. The development of industry, the building of the vast dams, giant steel plants, and essential thermal power plants heralded a shift from what, till then, had been traditionally an agriculture and trade based economy.With the metamorphosis of the economy, banking had even more of a key role to play. For if the industrialisation of the country was to keep in step with the upliftment of agriculture there

was a need for a bank that could serve both.In 1955, by an Act of Parliament, the Imperial Bank of India was reconstituted. And so was born the State Bank of India. With a new sense of social purpose and over 130 years of banking experience.In 1959, eight banks of the former princely states became associates of the State Bank. And the

State Bank Group was now poised for a dynamic thrust forward in

Babasabpatilfreepptmba.com Page 12

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

India’s banking scene. The first step was reaching more people. Especially in rural India. Though, by 1960, the State Bank had almost doubled the number of its offices to 882, the real breakthrough was not in the Bank’s size. There was a sea change in the very concept of banking; from banking for the classes to banking for the masses. It was a change that started a surge of growth that made the State Bank even more relevant in the context of the national economy. It was a change that evolved as a result of State Bank’s growing awareness of the problems that beset a developing nation’s economy. Through all

this, of course, the Bank continued to be the premier banking institution in the country. For instance, as it did in its days as the Imperial Bank of India, the State Bank continues to conduct Government banking business. It acts as the agent of the Reserve Bank of India in places where the Reserve Bank has no offices. The State Bank also maintains currency chests in over 2000 offices all across the country to ensure an adequate and continuous circulation of currency notes and coins. And because of its vast and ever expanding domestic and global network, the Bank offers services that have few parallels

.ABOUT STATE BANK OF INDIA

The State Bank of India has been, over the years, the flagship of Indian banking. State Bank of India is the largest bank in India in terms of profits, assets, deposits, branches and employees. With a network of over 9,000 branches in India and 51 foreign offices in 32 countries, the Bank commands about one-fifth of the total deposits and loans in all scheduled commercial banks in the country. State Bank of India is the successor to Imperial Bank of India. The latter was established in 1921 with the amalgamation of three Presidency

Babasabpatilfreepptmba.com Page 13

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Banks of Bombay, Bengal and Madras. State Bank of India came into being on 1.7.1955 through the State Bank of India Act, 1955. The Banks of erstwhile princely states of India joined the State Bank Group as subsidiaries under the State Bank of India (Subsidiary Banks) Act 1959. Over the years, the Bank has expanded rapidly. The Reserve Bank of India is the single largest shareholder of the Bank (with 59.73% stockholding followed by 14.1% NRI/FIIs, 11.8% financial institutions, 11.1% individuals and remaining with mutual funds and corporates). SBI's shares and bonds are listed for trading on all the major Indian stock exchanges. Its GDR is listed on the Luxembourg Stock Exchange. With a view to inculcating transparency in banking transactions and for providing information to customers, the Bank launched a Citizen's Charter in the form of the Code of Fair Banking Practices together with the General Terms and Conditions of Service. Appropriately named, 'Towards Excellence' Code reflects the Bank's commitment to provide service of the highest order and serves as a document of self-discipline.

ASSOCIATE BANKS State Bank of India has the following seven Associate Banks (ABs) with controlling interest ranging from 75% to 100%.

1. State Bank of Bikaner & Jaipur (SBBJ)2. State Bank of Hyderbad (SBH)

3. State Bank of Indore (SBIR)

4. State Bank of Mysore (SBM)

5. State Bank of Patiala (SBP)

6. Sate Bank of Saurashtra (SBS)

Babasabpatilfreepptmba.com Page 14

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

7. Sate Bank of Travancore (SBT)

Branch Network

Interactive branch locator allows to establish contact with any of the over 8900 SBI branches in India.

Worldwide network of SBI Bank

SBI Bank India has 52 Foreign Offices in 34 countries. SBI India serves the international needs of its foreign customers, in addition to conducting retail operations. The focus of the offices of SBI is India-related business.

LocationHeadquartered in Mumbai, SBI has hundreds of branches all over the country. It also has 52 foreign offices in 34 countries

Sharing Social responsibilities

Be it victims of earthquake at Lathur or Bhuj or the Tsunami State Bank of India

has contributed to the Prime Minister and Chief Minister’s Relief Funds.

Funded socially oriented projects for health & education.

Conducted camps for blood donation, adult literacy, medical check up

Initiated awareness programmes for AIDS, Cancer, TB, Anti Drug-addiction and

supported more than 100 organisations on an average, every year

SHAREHOLDING PATTERN FORM - AName of the Company: State Bank of India

Babasabpatilfreepptmba.com Page 15

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Scrip Code - 112 Quarter Ended - 30.09.2005

Category Code Category

No. of Shares

held% of

Shareholding

I CONTROLLING / STRATEGIC HOLDINGSA BASED IN INDIA1 Indian Individuals/HUFs & Relatives 2 Indian Corporate Bodies/Trusts/Partnerships

3 Persons acting in Concert (also include Suppliers/Customers) 314338700 59.73

4 Other Directors & Relatives ( other than in I above )

5 Employee Welfare Trusts/ESOPs (already converted into shares)

6 Banks/ Financial Institutions 7 Central / State Govt. 8 Central / State Govt. Institutions 9 Venture Funds / Private Equity Funds

Sub Total A 314338700 59.73

B BASED OVERSEAS

10 Foreign Individuals ( including FDI ) 11 Foreign Corporate Bodies ( including FDI ) 12 Non Resident Indians (individuals) 13 Non Resident Indians Corporate Bodies

Sub Total B NIL NIL

C GDR,s/ADRs/ADSs

Sub Total C NIL NIL

D OTHERS ( Please specify here )

Sub Total D NIL NIL

E ANY OTHER SHARES LOCKED-IN ( except covered above)

Sub Total E NIL NIL

SUB TOTAL I 314338700 59.73

Category Category No. of Shares % of

Babasabpatilfreepptmba.com Page 16

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Code held ShareholdingII FREE FLOATA BASED IN INDIA1 Indian Individuals/HUFs 29886541 5.682 Indian Corporate Bodies/Trusts/Parterships 9107916 1.733 Independent Directors & Relatives 0 0.004 Present Employees (Physical shareholdings ) 4095183 0.785 Banks/Financial Institutions 28089406 5.346 Central / State Govt. 469514 0.097 Central / State Govt.Institutions 0 0.008 Insurance Companies 4145516 0.799 Mutual Funds 31823315 6.0510 Venture Funds/Private Equity Funds 0.0011 Customers 0.0012 Suppliers 0.00

Sub Total A 107603244 20.45

B BASED OVERSEAS

13 Foreign Individuals 0 0.0014 Foreign Corporate Bodies 175206 0.0315 Foreign Institutional Investors (SEBI - registered ) 62443178 11.8616 Non Resident Indians ( Individuals ) 256565 0.0517 Non Resident Indian Corporate Bodies 0.00

Sub Total B 62874769 11.95

C GDRs/ADRs/ADSs 41468018 7.88

Sub Total C 41468018 7.88

D OTHERS ( Please specify here )

Sub Total D

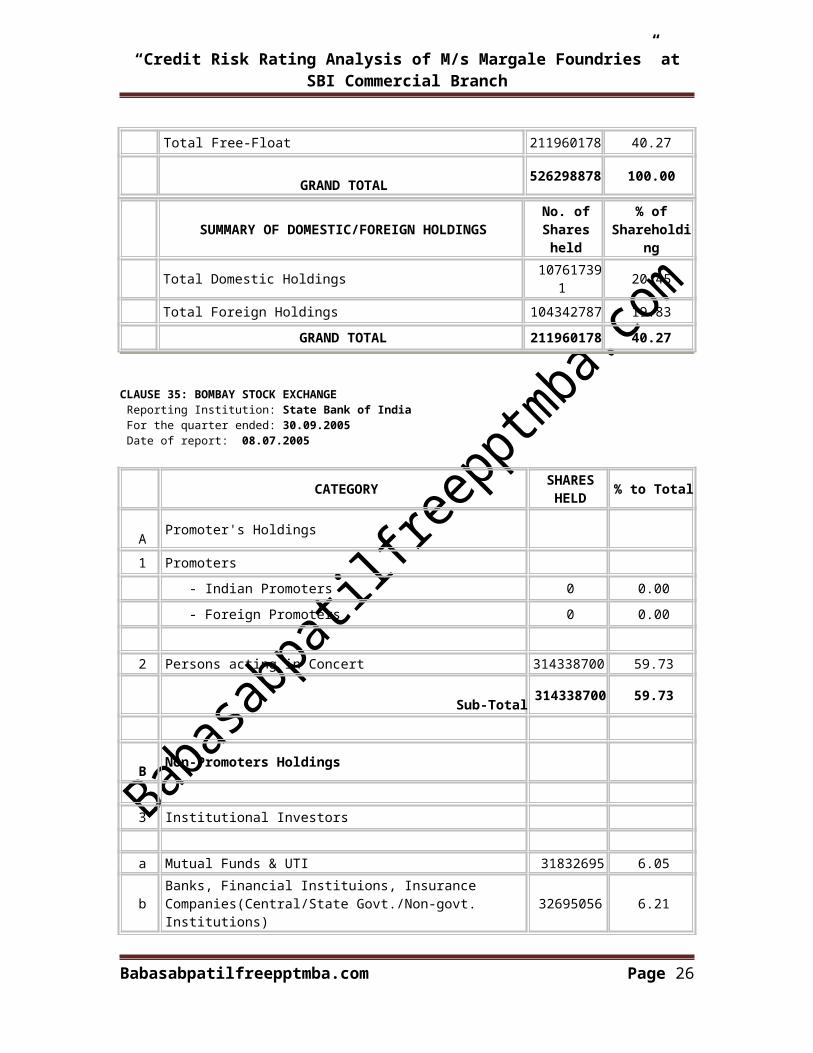

Sub Total II 211960178 40.27 GRAND TOTAL 526298878 100.00

BROAD SUMMARY OF HOLDINGSNo. of Shares

held% Of

Shareholding

Total Controlling / Strategic Holdings 314338700 59.73

Total Free-Float 211960178 40.27

GRAND TOTAL 526298878 100.00

Babasabpatilfreepptmba.com Page 17

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

SUMMARY OF DOMESTIC/FOREIGN HOLDINGSNo. of Shares

held% of

Shareholding

Total Domestic Holdings 107617391 20.45

Total Foreign Holdings 104342787 19.83

GRAND TOTAL 211960178 40.27

CLAUSE 35: BOMBAY STOCK EXCHANGE Reporting Institution: State Bank of India For the quarter ended: 30.09.2005 Date of report: 08.07.2005

CATEGORY SHARES HELD % to Total

A Promoter's Holdings

1 Promoters - Indian Promoters 0 0.00

- Foreign Promoters 0 0.00

2 Persons acting in Concert 314338700 59.73

Sub-Total 314338700 59.73

B Non-Promoters Holdings

3 Institutional Investors a Mutual Funds & UTI 31832695 6.05

b Banks, Financial Instituions, Insurance Companies(Central/State Govt./Non-govt. Institutions) 32695056 6.21

c FIIs 62443178 11.86

Sub-Total 126970929 24.13

4Others

a Private Corporate Bodies 8952860 1.70b Indian Public 33981724 6.46c NRIs 256565 0.05

Babasabpatilfreepptmba.com Page 18

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

d OCBs 175026 0.03e TRUST's 155056 0.03f OTHERS ( GDR'S) 41468018 7.88

Sub-Total 84989249 16.15

GRAND TOTAL 526298878 100.00

FORM C: FREE-FLOAT HOLDERS (DISCLOSE ONLY HOLDINGS OF 1% & ABOVE) (List of holders categorywise) Reporting Institution: State Bank of India Scrip Code - 112 Quarter Ended - 30.09.2005

SL NO HOLDER NAME

No. of Shares HELD

% of Shareholding

Category Code

Relationship, if any with anyone in I

1 The Bank Of New York 41468018 7.88

2 Life Insurance Corporation Of India 28199611 5.36

3Fidelity Management & Research Co. A/CFidelity Investment Trust - Fidelity

7200000 1.37

GRAND TOTAL 77713732 14.77

STATE BANK FOREIGN OFFICESThere are 52 Foreign Offices in 34 countries service the international needs of the bank's

foreign customers, in addition to conducting retail operations. The focus of these offices

is India-related business.

PROFILE The SBI’s powerful corporate banking formation deploys multiple channels to

deliver integrated solutions for all financial challenges faced by the corporate universe.

The Corporate Banking Group and the National Banking Group are the primary delivery

channels for corporate banking products. The Corporate Banking Group consists of

dedicated Strategic Business Units that cater exclusively to specific client groups or

specialize in particular product clusters. Foremost among these specialized groups is the

Corporate Accounts Group (CAG), focusing on the prime corporate and institutional

clients of the country’s biggest business centers. The others are the Project Finance unit

Babasabpatilfreepptmba.com Page 19

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

and the Leasing unit. The National Banking Group also delivers the entire spectrum of

corporate banking products to other corporate clients, on a nationwide platform.

PRODUCTS AND SERVICES

INDUSTRIAL SECTORWorking Capital Financing

SBI offers working capital finance to meet the entire range of short-term fund

requirements that arise within a corporate’s day-to-day operational cycle.The SBI

working capital loans can help your company in financing inventories, managing internal

cash flows, supporting supply chains, funding production and marketing operations,

providing cash support to business expansion and carrying current assets. SBI’s working

finance products comprise a spectrum of funded and non-funded facilities ranging from

cash credit to structured loans, to meet the different demands from all segments of

industry, trade and the services sector. Funded facilities include cash credit, demand loan

and bill discounting. Demand loans are considered also under the FCNR (B) scheme.

Non-funded instruments comprise letters of credit (inland and overseas) as well as bank

guarantees (performance and financial) to cover advance payments, bid bonds etc.

Project Finance

The SBI has formed a dedicated Project Finance Strategic Business Unit to assess credit

proposals from and extend term loans for large industrial and infrastructure projects.

Apart from this, project term loans for medium sized projects and smaller clients are

delivered through the CAG and the NBG.In general, project finance covers industrial

projects, capacity expansion at existing manufacturing units, construction ventures or

other infrastructure projects. Capital intensive business expansion and diversification as

well as replacement of equipment may be financed through the project term loans. Project

finance is quite often channeled through special purpose vehicles and arranged against

the future cash streams to emerge from the project. The loans are approved on the basis

of strong in-house appraisal of the cost and viability of the ventures as well as the credit

standing of promoters.

SBI deferred payment guarantee

Babasabpatilfreepptmba.com Page 20

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

SBI can extend deferred payment guarantees to industrial projects for obtaining imported

equipment. The DPG is a standby credit guaranteeing deferred payments, usually for

payments for capital goods, turnkey contracts etc.

Corporate Term Loan

The SBI corporate term loans can support your company in funding ongoing business

expansion, repaying high cost debt, technology upgradation, R&D expenditure,

leveraging specific cash streams that accrue into your company, implementing early

retirement schemes and supplementing working capital.Corporate term loans can be

structured under the FCNR (B) scheme as well, with the option of switching the currency

denomination at the end of interest periods. This will help you take advantage of global

interest rate trends vis-à-vis domestic rates to minimize your debt cost. The bank’s

corporate term loans are generally available for tenors from three to five years,

synchronized with your specific needs.SBI corporate term loans may carry fixed or

floating rates, as befits the exact requirement of the client and the risk context. Again,

these rates will be linked to the bank’s prime lending rate.SBI corporate term loans can

have a bullet or periodic repayment schedule, as required by the client. The repayment

mode may be linked to the cash accruals of the company.The Bank’s expert credit crew

gauges the applicant’s particular fund requirements and evaluates the company’s credit

worthiness, factoring in the cash flows generated by it.

Structured Finance

SBI structured finance involves assembling unique credit configurations to meet the

complex fund requirements of large industrial and infrastructure projects. Structured

finance can be a combination of funded and non-funded facilities as well as other credit

enhancement tools, lease contracts for instance, to fit the multi-layer financial

requirements of large and long-gestation projects.

SBI advantage in structured finance

Being India’s largest bank and with the rich experience that it brings with it, SBI

commands formidable expertise in engineering financial packages that address complex

requirements with minimum risk. Further, SBI has firm relationships across the financial

Babasabpatilfreepptmba.com Page 21

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

map of the world, which can be leveraged to structure solutions that may necessitate the

participation of several credit agencies.

Dealer Financing

SBI extends financial support to the corporate distribution networks, by providing both

working capital finance and term loans to select dealers of identified companies. This

gives dealers to leverage their business relationship with major corporates to avail low

cost credit. Also, this type of financial solutions allows the corporate negotiate a better

price with dealers. Dealer financing may be extended in the bill discounting form or

simply as cash credit.

Channel Financing

Channel financing is an innovative finance mechanism by which the bank meets the

various fund necessities along your supply chain at the supplier’s end itself, thus helping

you sustain a seamless business flow along the arteries of the enterprise. Channel finance

ensures the immediate realization of sales proceeds for the SBI client’s supplier, making

it practically a cash sale. On the other hand, the corporate gets credit for a duration

equaling the tenor of the loan, enabling smoother liquidity management.SBI has the

world’s largest banking network of over 9,000 branches and this enables it to deliver the

financial solution at your suppliers’ doorsteps, across the span of the country.

Equipment Leasing

The SBI’s has deployed a dedicated Strategic Business Unit for lease financing that is

richly experienced in arranging lease contracts for procuring expensive equipment for

your project or plant. At SBI, we arrange lease agreements as stand alone contracts or as

part of a structured package.

Loan Syndication

The SBI leverages its vast network of relationships to arrange syndicated credit products

for corporate clients and industrial projects. With its rich experience and strong

reputation, SBI’s syndication desk can assemble large loan packages involving a ring of

reputed financial entities, domestic and international, that match the large credit

requirements of infrastructure projects.

TRADE and SERVICES SECTOR

Babasabpatilfreepptmba.com Page 22

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Eligibility Profit making Corporates/Non-corporates (surface transport operators) owning more than 10 well-maintained vehicles (including the proposed).

Quantum of finance

Minimum Rs. 10 lacs and maximum Rs. 10 crores.

RepaymentTerm Loan: Maximum 5 years.

Repayment will be in Equated Monthly Installments (EMI), starting two months after disbursement. Cash Credit: Repayable on demand, renewal every year.

Eligible amount of finance

Term Loan: 100 % of the cost of the chassis, inclusive of excise duty. Other expenses are to be borne by the borrower. Where body building is not required, 80 % of the cost of the vehicle will be financed. An additional Term Loan limit, subject to a maximum of 20% of the original limit may be sanctioned for repair of the vehicle, on or after the 3rd year if the loan account is regular.Cash Credit : 80% of receivables.

PrepaymentTerm Loan: Maximum 1% p.a. on the pre-paid amount, for the residual period.

Rate of Interest

Babasabpatilfreepptmba.com Page 23

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

For Term loans, 8.50% p.a. with monthly rests and for Cash Credit, 11.75% p.a. with monthly rests.

Security Primary: Hypothecation of vehicles financed as well as book debts. Collateral:

i) At least 50% of the loan amountii) Personal guarantee of promoters and two third-party

guarantors.

Applicability Metro/urban/semi-urban centers

Bill Finance

The bank’s bill finance product helps you bridge the fund gap between the date of sale of products to the receipt of payments. The bank purchases the bill of exchange your company receives against a product sale, at a discount, thus doing away with the delay in realizing the receivables.The extent of discounting would amount to the interest calculated till the payments for the original sale are realized, and will be determined on the basis of market interest rates as well as the credit rating of the borrower.

Cash Credit for Traders

SBI cash credit can be in the form of a running account, similar to an overdraft secured by a charge on current assets, that meets the frequent cash requirements of your trading cycle.

Babasabpatilfreepptmba.com Page 24

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Term Loan for Asset Acquisition

The specialized product has been designed to help you purchase plant, machinery, land or other physical assets required during the growth and expansion of the your company.

Letters of Credit

The SBI offers Letters of Credit to facilitates your purchases of goods in trading operations, both domestic and international. Backed by the SBI’s strong reputation, you will be able to build better trust in trade and forge business relationships faster.The bank’s vast network of branches and correspondent banks enables your enterprise to sustain a seamless flow of business on a wide platform.Further, the bank’s informed trade finance crew can provide you with sophisticated credit and trade information and market knowledge, helping you extract more value from business.

Bank Gaurantees

The SBI guarantees the creditworthiness or the business capacity of its clients through its financial and performance guarantees.

Small and Medium EnterprisePROJECT UPTECHSBI extends consultancy services through PROJECT UPTECH for technology upgradation of small-scale industries. The bank's Consultancy Cells are trained for comprehensive techno-managerial studies and the bank offers financial packages as follow-up support for implementation of the upgradation ventures.

Babasabpatilfreepptmba.com Page 25

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Management Consultancy Services The Bank's Consultancy Services Cells are established in the Bank's Local Head Offices and offer support to clients by:

Counseling young entrepreneurs Organizing short-term Entrepreneurial Development and

Industrial Management Programmes

Techno economic feasibility reports; project appraisals; short market survey

Techno managerial studies of individual firms for enhancing their competitiveness in key areas like marketing, costing and pricing, MIS and corporate delivery systems.

Technology Upgradation

As an extension of its Management Consultancy Services and for supporting client's efforts for modernization, the bank has set up an Industrial Technology Group engaged in the following tasks:

Enhancing technology awareness among industrialists Catalyzing a step-up in quality, productivity and cost

effectiveness

Disseminating technological/market information

GENERAL PURPOSE TERM LOANS

State Bank of India grants term loans to small scale industries for meeting general

commercial purposes like substitution of high cost debt, research and development,

shoring up net worth and funding business expansion.The tenor of the loan is normally

is 3 years, and the pricing is fine-tuned to suit the risk profile of the borrower. The

Babasabpatilfreepptmba.com Page 26

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

repayment is structured in monthly or quarterly installments, according to the cash

generation cycle.

Eligibility criteria for these term loans

The SSI unit that takes the loan should not have any history of defaults in payment of

interest or installments of the principal. The unit should have a strong performance record

and a respectable credit rating as per the bank’s own credit assessment scales ( In case of

loan above Rs. 25 lakhs )

Type of security/guarantee required for the loan

Extension of hypothecation charge over the current assets and fixed assets is required as

primary security. Further, the borrower whose aggregate loans with the Bank exceed Rs 5

lakh may explore the possibility of collateralizing tangible security such as immovable

property and third party guarantee. In all cases, personal guarantees of

proprietors/partners/promoters have to be furnished.

Margins applicable

A minimum margin of 25 per cent is applicable for acquisition of land and building,

building construction, renovation of offices, showrooms, godowns, purchase of

equipment, vehicles etc. In other words, the quantum of the loan will be restricted to 75

per cent of the total expenditure.

LIBERALIZED CREDIT FOR SSI

State Bank of India extends production-linked credit facilities to small-scale industries,

ancillary industrial units and village and cottage industrial units on liberal terms and

conditions.

Under this scheme, the quantum of advances is not linked to the security

furnished, but the genuine requirements of the unit. The pricing of the loan is based

on credit assessment, and the units with strong ratings may be given finer rates.

No collateral security is required for loans up to Rs 5 lakh. Composite term loans

can be sanctioned up to Rs 25 lakh combining term loan and working capital.

Types of financial assistance under the Liberalized scheme

Babasabpatilfreepptmba.com Page 27

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

A. The Liberalized scheme offers a range of financial products including the following:

1. Term loans for acquisition of fixed assets

2. Working capital loans financing current assets

3. Letter of credit for acquisition of machinery and purchase of raw materials

4. Bank guarantee in lieu of security deposits to be made with government

department/other departments for execution of orders.

5. Deferred payment guarantees for purchase of machinery on deferred payment

basis.

6. Bill facility for purchase of raw materials and for sale of finished goods.

7. Composite loans (term loans plus working capital) up to Rs 25 lakh.

Margins applicable

For requirements up to Rs 25,000, no margins are involved. For limits ranging from Rs

25,000 to Rs 5 crore, the margin is set at 20 per cent. For credit limits above Rs 5 crore, a

25 per cent margin may be applied.

ENTREPRENEUR SCHEME

State Bank of India grants financial assistance to technically qualified, trained and

experienced entrepreneurs for setting up new viable industrial projects. Loans are

extended to technocrats who are unable to meet the normal margin requirements under

the liberalized schemes.

Eligibility criteria for the Entrepreneur schemeThe borrower has to be a technically

qualified person (a degree/diploma holder in engineering or technology), a craftsman

with adequate experience or training or a person possessing a degree in business or

industrial management, a chartered accountant or a cost accountant with relevant

experience.

Types of financial assistance under the Entrepreneur scheme

The bank provides:

Babasabpatilfreepptmba.com Page 28

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

term loans,

working capital and

equity fund finance

Margins applicable

For requirements up to Rs 5 lakh, no margins are involved. For needs ranging from Rs 5

lakh to Rs 20 lakh, the margin is set at 10 per cent.

EQUITY FUND SCHEME

Under the Equity Fund scheme, the SBI grants financial assistance to entrepreneurs who

are not able to meet their share of equity fully, by way of interest-free loans repayable

over a long period.This type of assistance fills in the gap between the margin

requirements in the project and the capital contributed by the promoter. The Equity Fund

assistance can be normally repaid over 5 to 7 years after the moratorium period.

Eligibility criteria for the Equity Fund scheme

The bank extends Equity Fund assistance only to new projects, which are also eligible

for the SBI’s Liberalized scheme and the Entrepreneur scheme. The project cost has to

be more than Rs 25,000. Type of security is required for the equity fund assistance

Security available for other loans should be extended to cover equity assistance also.

STREE SHAKTI PACKAGE

The Stree Shakti Package is a unique scheme run by the SBI, aimed at supporting

entrepreneurship among women by providing certain concessions. An enterprise should

have more than 50% of its share capital owned by women to qualify for the scheme.

The concessions offered under the Stree Shakti Package are:

1. The margin will be lowered by 5% as applicable to separate categories.

2. The interest rate will be lowered by 0.5% in case the loan exceeds Rs 2 lakh.

3. No security is required for loans up to Rs 5 lakh in case of tiny sector units

BUSINESS ENTERPRISES

Babasabpatilfreepptmba.com Page 29

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

An individual or a firm (partnership or proprietorship) who has established a business

venture for the purpose of providing any services like restaurants, Xerox copy centers,

computer centers, STD Booths are eligible for this scheme. Original cost of the

equipments (including land, building, machinery, furniture and fixture, etc. should not

exceed Rs.10 lakh.Extent of assistance is normally capped at Rs 10 lakh out of which

working capital limit sanctioned can be up to Rs 5 lakh. For requirements of up to Rs

25000, the margin is nil. For requirements between Rs 25000 and Rs 50000 the margin is

20 per cent. For requirements more than Rs 50,000 the margin is 50 per cent. For loans

up to Rs 25000 and more than Rs 25000, the primary security is the charge over the

assets purchased out of the Bank's finance. The collateral for loans up to Rs 25000 is nil,

for more than Rs 25000, it is the charge over the immovable or movable assets or third

party guarantee.

STATE BANK OF INDIA

COMMERCIAL BRANCH

BRIEF INTRODUCTION

The industrialists and big customers felt difficult to transact in small

banks and also much attention was not being paid to customers. Hence for easy

transaction and personal care to the customers they started the commercial branch on 14-

11-98. this bank deals mainly with big customers who want to borrow Rs25 lakhs and

above come here.

COMPANY PROFILE

Area profile Belgaum

District population About 10.00 lakhs

Major Industries

Foundries

Machine shops

Babasabpatilfreepptmba.com Page 30

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Hydraulics

Textiles (sarees)

Dairy

Sugar

Financial Institutions

Total Nationalised branches in Belgaum 432

District

State Bank of India

Branches in Belgaum district 24

SBI Branches in Belgaum City 12

Branch details

Location Halgekar Building

Goaves Hindwadi

Belgaum-590011

Premises Leased

Area: 8740 SQFT

Rent:@Rs.5.85 per Sq ft

Monthly Rent: Rs. 51,000/-

Date of opening 14-11-98

Incumbany SMG V

Facilities 1. Fully Computerised

2. Trade Finance

3. Forex – “B” category

4. SWIFT / SFMS

Inspection Rating A + (December 2003)

Staff Strength

Field officers 6

Babasabpatilfreepptmba.com Page 31

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Foreign Exchange 1

Bill Transaction 1

Accountant 1

In 1st Floor Advances Department

2nd Floor Accounts & Foreign Exchanges

Department

Important Customers

1. M/s Vishwanath Sugars

2. M/s Shri Renuka Sugar Ltd

3. M/s Ashok Iron Works Group

4. M/s Jinabakul Group

5. M/s Manickbag Group

6. Gudi Family

7. M/s Polyhydron Group

8. Vega Group

9. M/s Hind Group

Top 10 Depositors

1. M/s Vishwanath Sugars

2. M/s BT Patil & Sons

3. M/s Oilgear Towler Polyhydron (PVT)

4. M/s Shri Renuka Sugar Ltd

5. M/s Jinabakul Group

6. M/s Reliance Industries

7. M/s Hind Auto Cranks (Pvt)

8. M/s Fiarfield Atlas (PVT)

9. M/s Ashok Iron Works

10. M/s KLS Society

ORGANISATION STRUCTURE

Babasabpatilfreepptmba.com Page 32

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Chief Manager is overall incharge of all the bank transactions. He also

handles the Foreign Exchange. Under him comes the Manager Credit who manages and

controls all the credit related transactions.

In absence of chief Manager the Manager Credit is incharge of all the

bank related activities. Under him are three deputy managers. Each deputy Manager

handles 20 to 25 customers & 80 to 100 accounts among which some maybe

manufacturers or traders or builders. Individually they manage their work. The work is

allotted equitably to each Deputy Manager.

RESEARCH METHODOLOGY

Project Idea

The purpose of the project is to study and understand Credit Risk Assessment and Rating

Mechanism of State Bank of India, Commercial Branch, Belgaum.

The study focuses on credit Rating Analysis of M/s Margale Foundries, which is in

the line of activity of castings and also manufacturers of auto components. As loans are

subject to default in their repayment. SBI tries to assess the repayment capacity of

various firms through a tool called Credit Risk Assessment and Rating. Credit rating is

Babasabpatilfreepptmba.com Page 33

Chief Manager Narendra.D.Tele

Dileep A. Bankapur

Deputy Manager(Advances)

Ashok. Patvardhan

Deputy Manager(Advances)

NarasimhanDeputy Manager

(Advances

Sheena MathurConcurrent

Auditor

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

necessary for loans and advances of high volume to ensure their prompt repayment and to

minimize NPA’s.

Title of the Project: “Credit Risk Rating Analysis of M/s Margale Foundries”

Objectives

Main objective –

Assess the credit rating of M/s Margale Foundries

To study the comparative analysis of Balance sheet of the company and the credit

risk rating summary of the company for the financial year 2004-05.

Sub objectives –

Organization study of State Bank of India, its products, achievements, and future

trends in the company.

To understand Indian banking sector in general and commercial banking in

particular.

To understand the Credit Risk Assessment and Rating methodology practiced by

State bank of India.

To find out whether it is safe to lend high volume loan of more than Rs.25 lacks

to M/s Margale Foundries.

Conduct analysis of Balance Sheet, Ratio analysis, risk assessment verification to

arrive at rating.

To understand in brief the SMERA (Small & Medium Rating Agency) agency

guidelines followed by SBI

Sample area

The area covered for the study is Belgaum district’s State Bank of India where Industries

in & around Belgaum city have availed loan facilities from State Bank of India.

Duration of the Project is 60 days. (15th May to 14th July 2006)

Scope of the project

Babasabpatilfreepptmba.com Page 34

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

1. To interact with employees and understand the working of State bank of India,

Commercial Branch, Belgaum.

2. Detailed in depth interaction with credit managers to understand the risk

assessment and rating mechanism of SBI.

3. To Work Within SBI And Study Financial Statements, Reports, Etc.,

4. To study the performance of the client company and SBI’s credit rating Model

based on the nature of activities of company.

5. Assess the credit rating of Margale Foundries through credit rating analysis

with the use of financial results and calculated ratios.

Data collection Data obtained for the first time and used specifically for the particular

Primary Data: Primary data is the data obtained for the first time and used specifically

for the research study.

Primary data is collected through in depth interview and discussion with SBI credit

managers. This will help me to get qualitative information for analysis of credit rating.

Secondary Data: Secondary data are the data that have already been collected by and are readily available from other sources

Secondary data is collected through:

Magazines, Books and literature study

Internet and websites.

SBI’s Manuals, Reports, and circulars.

This will help be useful to collect quantitative data required for analysis of performance

and rating.

Project methodology

The study is mainly based on risk assessment, ratio analysis and Balance sheet and other

financial statements analysis. The data of quantitative nature such as financial statements,

ratios etc., are collected from State Bank of India Belgaum Branch’s Records and Reports

submitted to SBI by Margale Foundries. Techniques used for quantitative analysis are,

Babasabpatilfreepptmba.com Page 35

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

1. Comparative Financial Statements: The comparative analysis of financial statements

is a process of evaluating the relationship between component parts of financial

statements to obtain a better understanding of the firm’s position and performance.

2. Common sized Statements: Common sized Statement expresses assets and liabilities

as

per cent of total assets and expenses and profits as per cent of sales.

3. Ratio Analysis: Ratio Analysis is a systematic use of ratios to interpret/assess the

performance and status of the firm.

Qualitative data is collected through questionnaire filled by credit managers of bank to

understand the rating mechanism and other qualitative facts and their effects on CRA

model and ratings.

Limitations

Restrictions regarding disclosure of financial information from banks.

Detailed analysis was not possible due to limitation on project time.

Limited exposure to banking sector in our course module and related topics.

Statistical analysis tools could not be used.

There were time constraints.

Credit Risk ManagementWhat is Risk?

The word risk is derived from an early Italian word “resicare” which means “to dare”

Risk can be defined as emanating from a situation as something which throws a

challenge to a person to act or not to act with regard to an event or happening. These

challenges (or risks) under the different walks of life may take various forms. A soldier

may run the risk of life in a battle and a traffic police may run the risk of being hit by an

automobile on the road. Thus, the concept of risk is synonymous with the uncertainties in

a preposition and the degree of risk may be computed in terms of probability of an

outcome that is not desired. Every event or situation has some element of associated

risks. It is possible to reduce them to a manageable level but these cannot be wiped out

together. In short we cannot think of a zero-risk situation, whether in our work

environment or in our personnel lives.Risk taking is a deliberate action in the process of

Babasabpatilfreepptmba.com Page 36

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

financial decision making. The action results from an optimal choice made by the

decision maker, which in turn,

emanates from a systematic analysis of the various alternatives available. Risk taking is

calculated decision and phrases like outcome of “fate” or “come what may” etc do not

find a place in the process of risk assessment.

Subjective vs objective assessment of risk

Though lending bankers have traditionally been taking decisions only after weighing all

the inherent risks in credit proposal, there is a renewed thrust today on the importance of

laying down a structured system of assessment and management of risk in banks. The

credit analysts have indeed been assessing all the underlying risks as perceived by a

banker through the process of assessing all the underlying risks as perceived by a banker

though the process of assessment was highly subjective. As a result, lending bankers used

to denote the risk content in a credit proposal by using statements such as fair banking

risk, high banking risk or acceptable banking risk etc. on the basis of which credit

decisions were taken. However subjective evaluation of risk serves a limited purpose.

The fast changing economic scenario which has perhaps affected the banking system the

most, has generated the new kinds of risks, besides bringing about a sea change in the

concept of risk management. In order to manage these risks, we need to set a limit for

ourselves for risk absorption. In financial parlance, this limit is known as risk appetite.

This can be done only if the various elements of risks in a preposition are quantified and

aggregated. The new age risk assessment process therefore relies heavily on objective or

quantified assessment of risk. In a risk management process, today’s lending banker does

not stop with his findings that a credit proposal has an acceptable or fair banking risk. He

goes a step further and finds out the degree of acceptability of such risk elements.

Thereafter, he may then take a credit decision in favor of the proposal if the degree of

acceptability lies within his risk appetite limit.

CREDIT RISKThe degree of credit risk is the probability that a loan lent to a borrower may not be

repaid. The extent of repayment likely to be made and the time taken in the process are

important factors in the computation of probability of default. Probability of the

Babasabpatilfreepptmba.com Page 37

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

occurrence of counterpart default determines the extent of credit risk in a business

preposition.

Credit risk of an activity has a dual perspective- business specific and

management specific. The business specific risk may further be bifurcated into systematic

and non-systematic risk components. System risks are those posed to the business

proposition by factors like recession or depression in the business, government

regulation, political unrest, environmental issues etc. over which the management of the

business may not have control. Thus though an enterprise is healthy and efficient in

operation, the extraneous risk factors, may, at times prove to be significantly challenging.

Fortunately, these risks have historically been around 25% to 30% of the entire risk

spectrum, the rest 70% to 75% emanating from the enterprise specific risk elements. The

non-system risks i.e. the enterprise specific risk components are therefore the most vital

factors in the evaluation and assessment of credit risks in a credit appraisal proposal.

The term credit risk is defined, “as the potential that a borrower or counter-

party will fail to meet its obligations in accordance with agreed terms”.

In simple terms it is the probability of loss from a credit transaction.

Loans are the largest and most obvious source of credit risk. Loans are given by banks in

the form of corporate lending, sovereign lending, project financing and retail lending.

However other sources of credit risk exists throughout the activities of banks, including

in the banking book and in the trading book and both on and off the balance sheet. Banks

are increasingly facing credit risk in various instruments other than loans, including

acceptances, interbank transactions, trade financing, foreign exchange transactions,

financial futures, swaps, bonds, equities, options and in the extension of

commitments and guarantees, and the settlement of transactions.Credit risk encompasses

both default risk and market risk. Default risk is the objective assessment of the

likelihood that counterparty will default. Market risk measures the financial loss that will

be experienced should the client default.

Credit risk includes not only the current replacement value but also the potential loss

from default.

The components of credit risk are:

Babasabpatilfreepptmba.com Page 38

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

Credit growth in the organization and composition of the credit folio in terms of

sectors, centers and size of borrowing activities so as to assess the extent of credit

concentration.

Credit quality in terms of standard, sub-standard, doubtful and loss-making assets.

Extent of the provisions made towards poor quality credits.

Volume of off-balance-sheet exposures having a bearing on the credit portfolio.

According to Reserve Bank of India, the following are the forms of credit risk:

Non-repayment of the principal of the loan and/or the interest on it. Contingent liabilities

like letters of credit/guarantees issued by the bank on behalf of the client and upon

crystallization – amount not deposited by the customer. In the case of treasury operations,

default by the counter-parties in meeting the obligations. In the case of securities trading,

settlement not taking place when it is due. In the case of cross-border obligations, any

default arising from the flow of foreign exchange and/or due to restrictions imposed on

remittances out of the country.

Credit risk-rating framework:A credit risk-rating framework deploys a number/alphabet/symbol as a primary summary

indicator of risks associated with a credit exposure. These rating frameworks are logic-

based, utilize responses made on a specified scale and promote the accuracy and

consistency of the judgement exercised by the banks. For loans to individuals or small

businesses, credit quality is typically assessed through a process of credit scoring. Prior

to extending credit, a bank or other lender will obtain information about the party

requesting a loan. In the case of a bank issuing credit cards, this might include the

party's annual income, existing debts, whether they rent or own a home, etc. A standard

formula is applied to the information to produce a number, which is called a credit score.

Based upon the credit score, the lending institution decides whether or not to extend

credit. The process is formulaic and highly standardized. Many forms of credit risk—

especially those associated with larger institutional counterparties—are complicated,

unique or are of such a nature that that it is worth assessing them in a less formulaic

manner. The term credit analysis is used to describe any process for assessing the credit

Babasabpatilfreepptmba.com Page 39

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

quality of counterparty. While the term can encompass credit scoring, it is more

commonly used to refer to processes that entail human judgement. One or more people,

called credit analysts, review information about the counterparty. This might include its

balance sheet, income statement, recent trends in its industry, the current economic

environment, etc. They may also assess the exact nature of an obligation. For example,

secured debt generally has higher credit quality than does subordinated debt of the same

issuer. Based upon their analysis, they assign the counterparty (or the specific obligation)

a credit rating, which can be used for making credit decisions.

Credit risk limits:

For managing credit risk, a bank generally sets an exposure credit limit for each

counterparty to which it has credit exposure. This is standard procedure in many contexts.

It could be a corporate loan, individual loan or a derivative dealer transacting with

counterparties. All entail credit risk. All are contexts where credit exposure limits are

used. A bank may also use aggregate credit exposure limits. A bank might set credit

exposure limits by industry. It might also set a total exposure credit limit for all its

corporate lending activities. Exposures are calculated with the help of credit risk models.

Depending on the assessment of the borrower (commercial as well as retail) a credit

exposure limit is decided for the customer, however, within the framework of a total

credit limit for the individual divisions and for the company as a whole. Also within the

limit as per RBI, i.e. not more than 20% of capital to individual borrower and not more

than 40% of capital to a group borrower.

Threshold limit is set depending on the:

Credit rating of the borrower

Past financial records

Willingness and ability to repay

Borrower’s future cash flow projections.

RBI GUIDELINES ON CREDIT RISK MANAGEMENTA counterparty risk arising from non-performance of trading partners is, however the

most important factor significantly contributing towards credit risk. The non performance

Babasabpatilfreepptmba.com Page 40

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

generally arises from refusal or inability to perform by the counterparty due to adverse

price movements or from external constraints that were not anticipated by the principal.

The steps in the process of management of credit risk include the following. It is

necessary that the process of credit risk management and the following steps are

articulated in the approved loan policy of a lending bank.

Steps:

1. Measurement of risk through credit rating/scoring;

2. Quantification of risk through;

Estimating expected loan losses over a chosen time horizon (through

tracking portfolio behavior over 5 or more years), and

Unexpected loan losses i.e. the amount by which actual losses exceed the

expected loss (through statistical measurement tools like standard

deviation of losses etc.

3. Pricing the risk on a scientific basis; and

4. Controlling the risk through effective Loan Review Mechanism and portfolio

management.

SETTING UP PRUDENTIAL LIMITSAn important aspect of instituting a framework of credit risk management is the process

of laying down the prudential limits on various aspects of credit, which itself is a

mechanism to restrict the magnitude of credit risk. The process may involve the

following:

I. Setting up benchmarks on liquidity ratios (viz Current Ratio), gearing ratios

(viz Debt Equity Ratio), Profitability ratios, Debt Service Coverage Ratios or

other ratios, with flexibility for deviations. The necessary conditions in which

deviations may be permitted and the approving authority for such deviations

should be clearly spelt out in the loan policy of the banks.

II. Setting up of single group borrower limits, which maybe lower than the limits

prescribed by the RBI to provide a filtering mechanism.

Babasabpatilfreepptmba.com Page 41

“Credit Risk Rating Analysis of M/s Margale Foundries” at SBI Commercial Branch

III. Setting up of exposure limit ie. sum total of exposures assumed in respect of

those single borrowers enjoying credit limits in excess of a threshold limits,

say 10% to 15% of capital funds. The substantial exposure limit may be

fixed at 600% or 800% of capital funds, which depends on the degree of

concentration risk to which the bank is exposed.

IV. Setting up of maximum exposure limits to industry, sector etc. Proper systems

for evaluation of the exposures at reasonable intervals is necessary in this

regard. The limits may also require adjustments especially when a particular

sector or activity faces slow down or encounters specific problems, other

sector/industry specific problems. The exposure limits to sensitive sectors,