A Playbook for Contending with the Medical Devices Excise Tax

5

A Playbook for Contending with the Medical Devices Excise Tax Research shows that few device makers have offset the excise tax they began paying in January 2013; here’s how to reduce costs in targeted areas of SG&A in order to maintain profit margins. • Cognizant 20-20 Insights Executive Summary By now, you have probably read that in March 2013, the U.S. Senate voted 79-20 to repeal the new excise tax on gross sales of medical devices, which includes everything from CT scans and replacement knees to tongue depressors. While the move appears encouraging for device manufacturers, there’s a catch: For the repeal to go through, lawmakers must identify an alter- native tax source to replace the $29 billion the excise tax is expected to generate over 10 years. 1 Sound futile? Exactly. Given that the tax is likely here to stay, how have medical device makers reduced their costs to compensate for the 2.3% duty they began paying on January 1? A review of manufactur- ers’ SEC 10-K filings reveals that they haven’t. To avoid margin erosion, however, the offsetting cost reductions must happen soon. An objective, disciplined approach to SG&A cost reduction can help manufacturers meet the margin squeeze and result in healthier businesses. How the Tax Affects the Medical Devices Industry The tax comes at a difficult time for the industry. High unemployment and the economy’s uncertain recovery have caused prospective patients to defer elective medical procedures such as knee and hip replacements. Moreover, because the manufacturers typically draw from an older demographic already covered by Medicare, they expect minimal new business from the Affordable Care Act’s pool of newly insured patients. Unlike other excise taxes — such as the gasoline tax that funnels funds to road repairs — the device makers’ tax has no mitigating industry benefit. Estimating the excise tax’s effect on companies is complex. For one thing, the tax applies only to U.S. sales. For another, it excludes associated services, such as education and consulting. As a result, calculating the tax’s impact on individual orga- nizations depends on the company’s geographic revenue mix, as well as the mix of device and services revenues. Major device manufacturers generate roughly 46% of their revenues outside the U.S. (see Figure 1). Least affected by the excise tax are those companies with large non-U.S. revenues and lucrative services revenues. For example, Becton Dickinson and St. Jude Medical earn less than half of their revenues from the U.S. On the other cognizant 20-20 insights | june 2013

Transcript of A Playbook for Contending with the Medical Devices Excise Tax

A Playbook for Contending with the Medical Devices Excise Tax Research shows that few device makers have offset the excise tax they began paying in January 2013; here’s how to reduce costs in targeted areas of SG&A in order to maintain profit margins.

• Cognizant 20-20 Insights

Executive SummaryBy now, you have probably read that in March 2013, the U.S. Senate voted 79-20 to repeal the new excise tax on gross sales of medical devices, which includes everything from CT scans and replacement knees to tongue depressors.

While the move appears encouraging for device manufacturers, there’s a catch: For the repeal to go through, lawmakers must identify an alter-native tax source to replace the $29 billion the excise tax is expected to generate over 10 years.1

Sound futile? Exactly.

Given that the tax is likely here to stay, how have medical device makers reduced their costs to compensate for the 2.3% duty they began paying on January 1? A review of manufactur-ers’ SEC 10-K filings reveals that they haven’t. To avoid margin erosion, however, the offsetting cost reductions must happen soon. An objective, disciplined approach to SG&A cost reduction can help manufacturers meet the margin squeeze and result in healthier businesses.

How the Tax Affects the Medical Devices IndustryThe tax comes at a difficult time for the industry. High unemployment and the economy’s uncertain

recovery have caused prospective patients to defer elective medical procedures such as knee and hip replacements.

Moreover, because the manufacturers typically draw from an older demographic already covered by Medicare, they expect minimal new business from the Affordable Care Act’s pool of newly insured patients. Unlike other excise taxes — such as the gasoline tax that funnels funds to road repairs — the device makers’ tax has no mitigating industry benefit.

Estimating the excise tax’s effect on companies is complex. For one thing, the tax applies only to U.S. sales. For another, it excludes associated services, such as education and consulting. As a result, calculating the tax’s impact on individual orga-nizations depends on the company’s geographic revenue mix, as well as the mix of device and services revenues.

Major device manufacturers generate roughly 46% of their revenues outside the U.S. (see Figure 1). Least affected by the excise tax are those companies with large non-U.S. revenues and lucrative services revenues. For example, Becton Dickinson and St. Jude Medical earn less than half of their revenues from the U.S. On the other

cognizant 20-20 insights | june 2013

2

hand, Stryker and C. R. Bard earn approximately two-thirds of their revenue in the U.S., making them more vulnerable to the tax’s impact.2

Equipment titan Thermo Fisher Scientific predicts little impact on its business because the majority of its sales are laboratory devices, which are not subject to the tax. The company estimates its exposure to result in a tax of only $20 million to $25 million.3

Breaking out revenues of devices vs. services adds an administrative burden to pricing and accounting activities, and there’s no doubt it will impact the way companies write future pricing agreements. Bundled pricing of products and services is likely to change.

It should be noted that the tax burden is especially high for startup companies. Because the tax applies to total device sales rather than profits, young organizations with nascent profits pay dis-proportionate shares of their profits toward the tax. In addition, startups tend to earn a higher percentage of revenues from U.S. domestic sales and typically earn less service revenue. The result is that the new tax may lead to increased industry consolidation and discourage the innovation and creativity that is often the hallmark of young businesses.

Attempts to Offset the Tax Data shows that in the three years between the Affordable Care Act’s enactment and the date the tax went into effect, device makers have taken

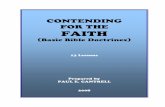

some steps to offset the tax, such as aggressively pursuing new business outside the U.S. From 2009 to 2012, the industry grew non-U.S. revenues from 41.5% to 45.5% of total revenues — a surprisingly large and rapid shift in such a short timeframe (see Figure 2, next page).

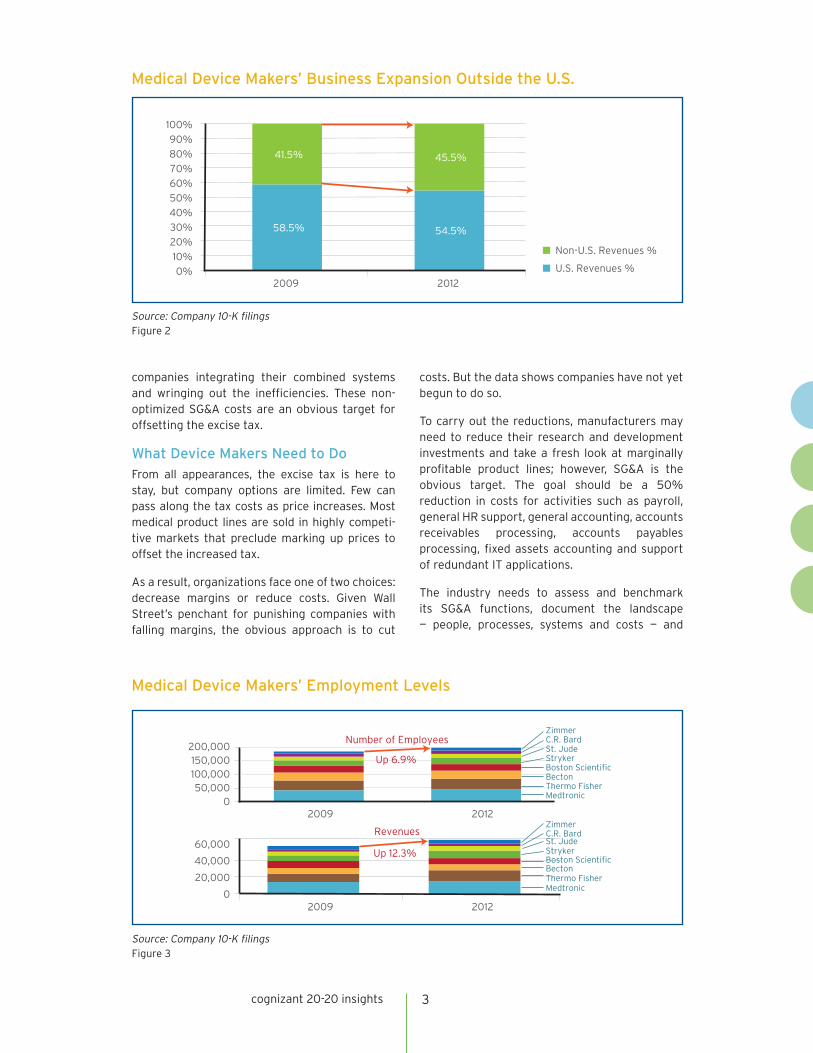

In addition, empirical evidence shows device makers putting the brakes on hiring. According to a review of corporate 10-K filings, total employment among the largest device manufac-turers reached 183,298 in 2009, the year before the Affordable Care Act was signed into law. By 2012, the companies’ employment had risen by 6.9% to 195,965. Revenues grew an even healthier 12.3% (see Figure 3, next page). Revenue growth that outpaces hiring should result in produc-tivity gains that appear in improved SG&A as a percentage of sales.

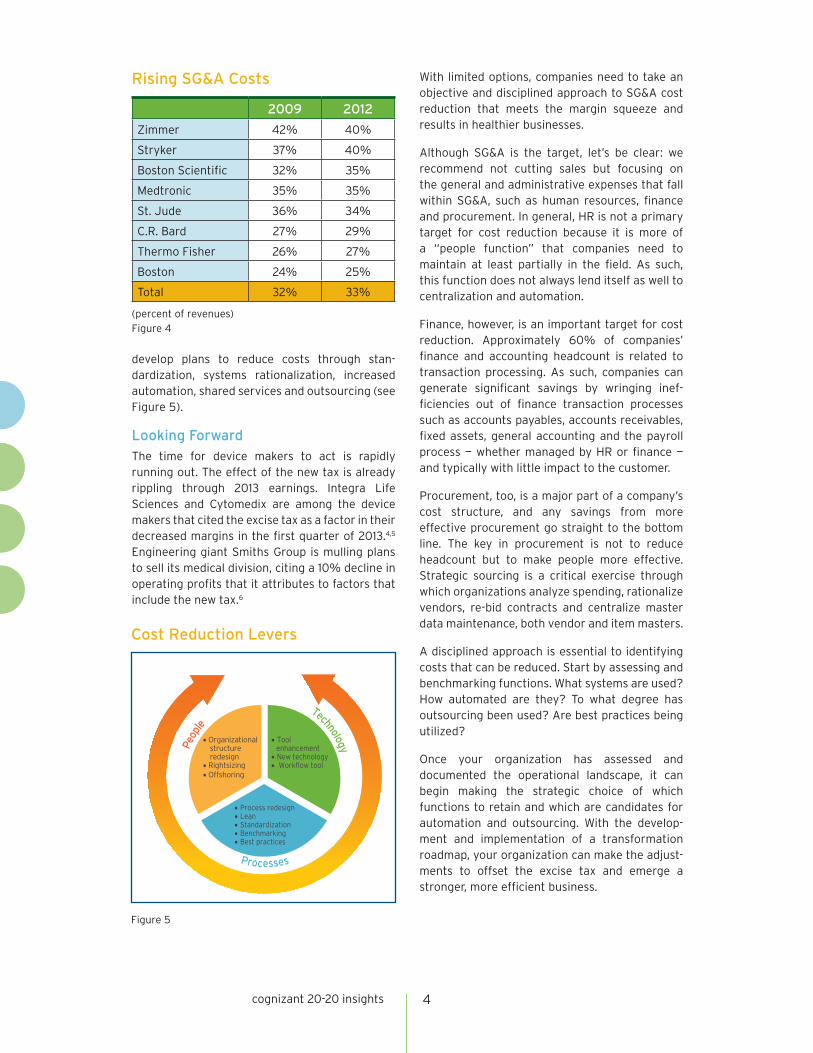

Yet among medical device makers, SG&A as a percentage of revenues has worsened (see Figure 4, page 4). The industry’s decline in SG&A perfor-mance between 2009 and 2012 may in part reflect the expansion overseas. It also suggests that the productivity gains are showing up elsewhere in the corporation, most likely in manufacturing.

Device makers’ sagging SG&A cost efficiency also clearly indicates that the industry’s expansion through mergers and acquisitions has produced multiple redundant back-office functions that are decentralized, nonstandardized and fragmented. Despite the abundant M&A activity, we don’t see the SG&A efficiency gains that would indicate

cognizant 20-20 insights

Source: Company 10-K filingsFigure 1

Medical Device Makers’ Non-U.S. Revenues

U.S. Revenues %

Non-U.S. Revenues %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Becto

n

St. Jude

Therm

o

Fish

er

Boston

Scientif

ic

Med

tronic

Zimm

er

Stryke

r

C.R. B

ard

companies integrating their combined systems and wringing out the inefficiencies. These non-optimized SG&A costs are an obvious target for offsetting the excise tax.

What Device Makers Need to Do From all appearances, the excise tax is here to stay, but company options are limited. Few can pass along the tax costs as price increases. Most medical product lines are sold in highly competi-tive markets that preclude marking up prices to offset the increased tax.

As a result, organizations face one of two choices: decrease margins or reduce costs. Given Wall Street’s penchant for punishing companies with falling margins, the obvious approach is to cut

costs. But the data shows companies have not yet begun to do so.

To carry out the reductions, manufacturers may need to reduce their research and development investments and take a fresh look at marginally profitable product lines; however, SG&A is the obvious target. The goal should be a 50% reduction in costs for activities such as payroll, general HR support, general accounting, accounts receivables processing, accounts payables processing, fixed assets accounting and support of redundant IT applications.

The industry needs to assess and benchmark its SG&A functions, document the landscape — people, processes, systems and costs — and

3cognizant 20-20 insights

Medical Device Makers’ Business Expansion Outside the U.S.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

U.S. Revenues %

Non-U.S. Revenues %

58.5% 54.5%

41.5% 45.5%

2009 2012

Source: Company 10-K filingsFigure 2

Medical Device Makers’ Employment Levels

58.5% 54.5%

41.5% 45.5%

2009 2012

2009 2012 0

50,000100,000150,000

200,000Number of Employees

Medtronic Thermo Fisher Becton

Stryker St. Jude

Zimmer C.R. Bard

Boston Scientific

Boston Scientific

0

20,000

40,000

60,000Revenues

Medtronic Thermo Fisher Becton

Stryker

C.R. Bard Zimmer

St. Jude

Up 6.9%

Up 12.3%

Source: Company 10-K filingsFigure 3

cognizant 20-20 insights 4

develop plans to reduce costs through stan-dardization, systems rationalization, increased automation, shared services and outsourcing (see Figure 5).

Looking ForwardThe time for device makers to act is rapidly running out. The effect of the new tax is already rippling through 2013 earnings. Integra Life Sciences and Cytomedix are among the device makers that cited the excise tax as a factor in their decreased margins in the first quarter of 2013.4,5 Engineering giant Smiths Group is mulling plans to sell its medical division, citing a 10% decline in operating profits that it attributes to factors that include the new tax.6

With limited options, companies need to take an objective and disciplined approach to SG&A cost reduction that meets the margin squeeze and results in healthier businesses.

Although SG&A is the target, let’s be clear: we recommend not cutting sales but focusing on the general and administrative expenses that fall within SG&A, such as human resources, finance and procurement. In general, HR is not a primary target for cost reduction because it is more of a “people function” that companies need to maintain at least partially in the field. As such, this function does not always lend itself as well to centralization and automation.

Finance, however, is an important target for cost reduction. Approximately 60% of companies’ finance and accounting headcount is related to transaction processing. As such, companies can generate significant savings by wringing inef-ficiencies out of finance transaction processes such as accounts payables, accounts receivables, fixed assets, general accounting and the payroll process — whether managed by HR or finance — and typically with little impact to the customer.

Procurement, too, is a major part of a company’s cost structure, and any savings from more effective procurement go straight to the bottom line. The key in procurement is not to reduce headcount but to make people more effective. Strategic sourcing is a critical exercise through which organizations analyze spending, rationalize vendors, re-bid contracts and centralize master data maintenance, both vendor and item masters.

A disciplined approach is essential to identifying costs that can be reduced. Start by assessing and benchmarking functions. What systems are used? How automated are they? To what degree has outsourcing been used? Are best practices being utilized?

Once your organization has assessed and documented the operational landscape, it can begin making the strategic choice of which functions to retain and which are candidates for automation and outsourcing. With the develop-ment and implementation of a transformation roadmap, your organization can make the adjust-ments to offset the excise tax and emerge a stronger, more efficient business.

Rising SG&A Costs

(percent of revenues)Figure 4

Figure 5

Cost Reduction Levers

2009 2012

Zimmer 42% 40%

Stryker 37% 40%

Boston Scientific 32% 35%

Medtronic 35% 35%

St. Jude 36% 34%

C.R. Bard 27% 29%

Thermo Fisher 26% 27%

Boston 24% 25%

Total 32% 33%

• Process redesign

• Lean

• Standardization

• Benchmarking

• Best practices

• Tool enhancement

• New technology

• Workflow tool

• Organizational structure redesign

• Rightsizing

• Offshoring

Processes

Peop

le

Technology

About CognizantCognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process out-sourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and approximately 162,700 employees as of March 31, 2013, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world. Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

World Headquarters500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 20 7297 7600Fax: +44 (0) 20 7121 0102Email: [email protected]

India Operations Headquarters#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2013, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About the AuthorsPaul Nowacki, CFA, is Leader of Finance & Accounting, Transformation Consulting, within Cognizant’s Business Process Services Group. In this role, Paul oversees all F&A consulting activities. He also serves as a thought leader in F&A and helps identify market trends and shape new Cognizant offerings. He is a frequent conference and webinar speaker and author of numerous articles and whitepapers on various finance and accounting topics. By combining his industry experience in IT and finance leadership roles with a background in transformational consulting, Paul looks holistically at finance and accounting orga-nizations and blends process and systems with organizational design perspectives. He has a B.S. in quan-titative business analysis and an M.B.A. with a concentration in operations research. Paul also holds the Chartered Financial Analyst professional designation. He can be reached at [email protected].

Moses Mallela, CPA, is a Principal Consultant within the Finance and Accounting Practice of Cognizant’s Business Process Services Group. In this role, Moses engages with clients on strategic assessments and identifying opportunities for value creation. Moses has extensive experience in offshore service delivery and has led global consolidation and standardization of F&A processes across multiple countries and languages into offshore and near-shore delivery centers. He holds a master’s degree in commerce and is a gold medalist from Osmania University, Hyderabad, India. He also holds the Cost and Management Accounting professional designation. He can be reached at [email protected].

Footnotes1 “Description of H.R. 436, The ‘Protect Medical Innovation Act of 2011,’” Joint Committee on Taxation,

Publication JCX-45-12, May 29, 2012.

2 U.S. Securities And Exchange Commission, Form 10-K.

3 Ibid.

4 “Disappointing 1Q Earnings for IART,” Zacks Equity Research, May 10, 2013.

5 “Cytomedix’s CEO Discusses Q1 2013 Results - Earnings Call Transcript,” SeekingAlpha, May 10, 2013.

6 “Smiths in Talks Over Medical Sale,” Midland News Express & Star, May 31, 2013.