A painful road forward Utilities in Central Europe -...

26

A painful road forward Utilities in Central Europe A white paper from the Economist Intelligence Unit sponsored by Oracle

Transcript of A painful road forward Utilities in Central Europe -...

A painful road forwardUtilities in Central Europe

A white paper from

the Economist Intelligence Unit

sponsored by Oracle

© The Economist Intelligence Unit 2004 1

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

A painful road forward: utilities in Central Europe is an

Economist Intelligence Unit white paper, sponsored

by Oracle.

The Economist Intelligence Unit bears sole

responsibility for the content of this report. The

Economist Intelligence Unit’s editorial team

conducted the interviews, executed the survey and

wrote the report. The findings and views expressed in

this report do not necessarily reflect the views of the

sponsor.

Our research drew on two main initiatives:

● We conducted in-depth interviews with power and

water industry executives in Estonia, the Czech

Republic, Poland and Slovakia, as well as with

regulators and with utility sector specialists in

banks, research institutes and international

organisations.

● We conducted an online survey in July/August 2004

of power and water industry executives distributed

throughout the EU accession and candidate

countries.

The author of the report was Nicholas Spiro and the

editor was Denis McCauley. Mike Kenny was

responsible for design and layout.

Our sincere thanks go to the interviewees and survey

participants for sharing their insights on this topic.

October 2004

Preface

2 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

After nearly 15 years of post-communist

transition, Central Europe’s network utilities

remain only part of the way through their

transformation from monolithic monopolies

to unbundled, competitive and consumer-oriented

firms. The 32 utility sector managers and specialists

interviewed and surveyed for this Economist

Intelligence Unit white paper, sponsored by Oracle,

agree that more wrenching change is needed if they

are to survive and grow amid the tougher competition

in an enlarged European Union.

In the electricity and water industries, the focus of

this paper, the reform agenda is dictated by three

pressing requirements: compliance with EU directives

on market-opening and environmental standards;

boosting efficiency and competitiveness; and

establishing a sound regulatory framework that

supports private investment. Integral to the

achievement of the first two and a key outcome of the

third is the ability of utilities to reduce and control

costs.

In addressing these imperatives, Central Europe’s

governments and utilities would do well to heed the

key messages of this report:

● Forget about California. There are plenty of

reasons to be wary of energy liberalisation, but

botched deregulation in other parts of the world

should not be one of them. Governments will need to

push ahead with deregulation at a time when its

proponents in the EU are few and far between.

Moreover, without independent watchdogs in place,

reforms are bound to falter.

Executive summary

● Going green will involve tough tradeoffs. To meet

stringent EU environmental regulations, Central

European utilities must become more efficient. This

means raising tariffs to cover more of their costs and,

in the power sector, diversifying their fuel sources

away from expensive and dirty coal. Despite fierce

opposition from ecologists, the case for retaining

cheap nuclear generation will become more

compelling.

● Private investors can help. To comply with EU

regulations, Central Europe’s utilities need to invest

on a colossal scale, requiring broader recourse to

private investment. Yet political resistance to private

participation remains strong. In both the power and

water sectors, private participation can help to speed

up utilities’ commercialisation. For this to happen,

however, national and local governments need to

become more trusting of private investors.

● Governments should be flexible on PPAs. They

may be anti-competitive, but long-term power

purchase agreements (PPAs) are a necessary evil to get

private investors and banks to fund environmental and

capacity upgrades. Governments would be foolhardy

to annul the contracts without providing adequate

compensation.

● Size isn’t everything. Governments should not get

carried away with building national champions.

Although Central Europe’s utilities need to bulk up in

order to compete with Western Europe’s vertically

integrated power giants, state-driven consolidation,

especially when it involves debt-laden and inefficient

companies, is doomed to fail.

© The Economist Intelligence Unit 2004 3

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

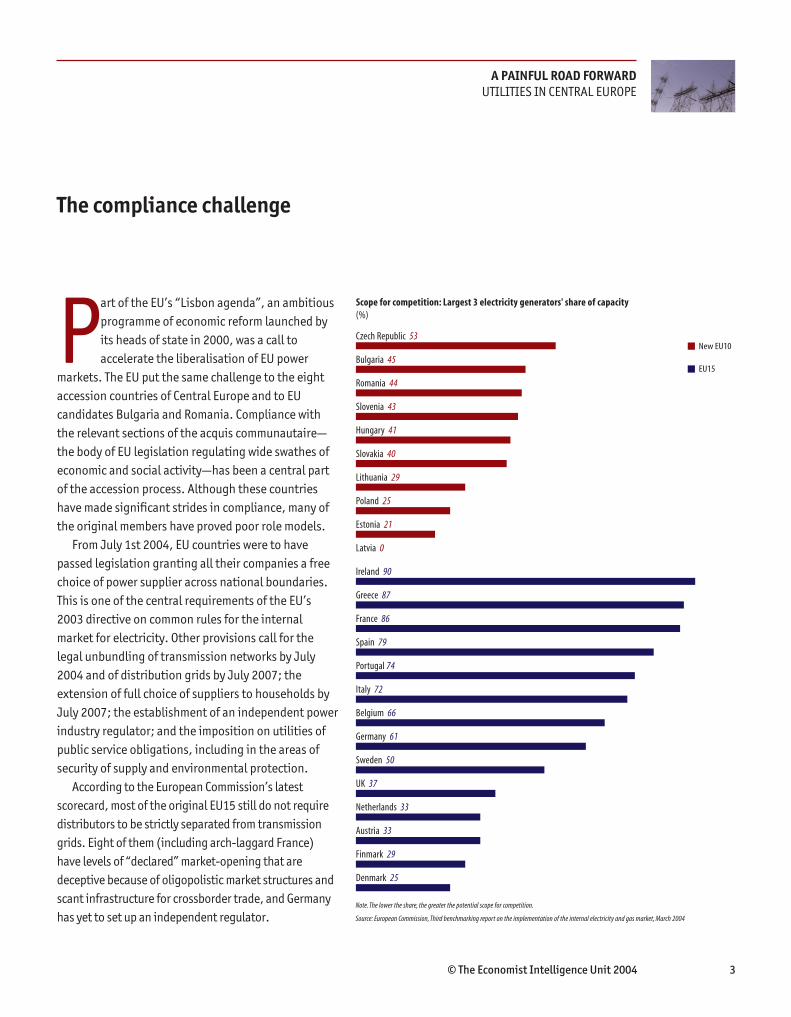

Part of the EU’s “Lisbon agenda”, an ambitious

programme of economic reform launched by

its heads of state in 2000, was a call to

accelerate the liberalisation of EU power

markets. The EU put the same challenge to the eight

accession countries of Central Europe and to EU

candidates Bulgaria and Romania. Compliance with

the relevant sections of the acquis communautaire—

the body of EU legislation regulating wide swathes of

economic and social activity—has been a central part

of the accession process. Although these countries

have made significant strides in compliance, many of

the original members have proved poor role models.

From July 1st 2004, EU countries were to have

passed legislation granting all their companies a free

choice of power supplier across national boundaries.

This is one of the central requirements of the EU’s

2003 directive on common rules for the internal

market for electricity. Other provisions call for the

legal unbundling of transmission networks by July

2004 and of distribution grids by July 2007; the

extension of full choice of suppliers to households by

July 2007; the establishment of an independent power

industry regulator; and the imposition on utilities of

public service obligations, including in the areas of

security of supply and environmental protection.

According to the European Commission’s latest

scorecard, most of the original EU15 still do not require

distributors to be strictly separated from transmission

grids. Eight of them (including arch-laggard France)

have levels of “declared” market-opening that are

deceptive because of oligopolistic market structures and

scant infrastructure for crossborder trade, and Germany

has yet to set up an independent regulator.

The compliance challenge

Scope for competition: Largest 3 electricity generators' share of capacity(%)

Czech Republic 53

Bulgaria 45

Romania 44

Slovenia 43

Hungary 41

Slovakia 40

Lithuania 29

Poland 25

Estonia 21

Latvia 0

Ireland 90

Greece 87

France 86

Spain 79

Portugal 74

Italy 72

Belgium 66

Germany 61

Sweden 50

UK 37

Netherlands 33

Austria 33

Finmark 29

Denmark 25

Note. The lower the share, the greater the potential scope for competition.

Source: European Commission, Third benchmarking report on the implementation of the internal electricity and gas market, March 2004

New EU10

EU15

4 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

A good start, but no cause for complacence

Bearing in mind that they were mainstays of central

planning a mere 14 years ago, Central Europe’s power

industries have made considerable progress in

complying with the acquis. Hans Haider, the head of

Eurelectric, the European power industry association,

stated earlier this year that the new EU members “are

well on the way to smooth implementation of EU

laws”. Most of the new members have created legally

independent transmission system operators (TSOs),

and all of them have set up nominally independent

watchdogs that oversee third-party access to

distribution grids. Although the dominance of

erstwhile incumbents constrains competition to a

greater extent than in Western Europe, Central

Europe’s power markets potentially offer more scope

for competition, since a great deal of fragmentation

has resulted from the unbundling of networks.

Hungary has been the most successful to date in

opening its electricity market to competition. After its

first stage of liberalisation kicked in in January 2003,

scores of large customers with annual consumption

levels exceeding 6.5 gwh (gigawatt hours) switched

suppliers, quickly raising the share of purchases on

the free market to 20% of total consumption by the

end of the year. “It was a much-needed

breakthrough,” notes Peter Kaderjak, the former head

of Hungary’s energy watchdog and now director of the

Regional Centre for Energy Policy Research in

Budapest.

Yet even in Hungary, competition is constrained by

a parallel “public service” market in which 80% of

generation and 40% of crossborder capacity is

contracted by Magyar Villamos Muvek (MVM), the

state-owned dominant wholesaler, under fixed-price

long-term power purchase agreements (PPAs). In

order for deregulation to become entrenched in

Central Europe’s electricity markets, contentious

issues such as PPAs need to be resolved in a

consensual and transparent manner.

Power industry reform is at much earlier stages

further east. In Russia, a series of reforms passed in

2003 call for the large-scale unbundling of the Unified

Energy System (UES) networks and the creation of

independent generation, transmission and

distribution companies, all by 2007. Given the vast

scale of the existing network and the lack of clarity

surrounding regulation and pricing reform, it can be

expected that Central Europe’s deregulation pains will

be greatly magnified in Russia.

A costly affair

An enormous challenge for utilities will be to comply

with EU environmental regulations. Central Europe’s

power sectors are hobbled by inefficient use of energy,

obsolete technologies and extensive use of carbon-

rich coal in generation. According to Eurelectric,

roughly 75% of the electricity produced in Central

Europe comes from conventional coal-fired thermal

plants, compared with 50% in the original EU15. In

Poland, coal (including lignite) provides a whopping

0 20 40 60 80 100

Sources of power generation in EU-15 and new EU members(%) Nuclear

Conventional thermal

Hydro

Total other renewables

EU15

New EU10

Source: Eurelectric

© The Economist Intelligence Unit 2004 5

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

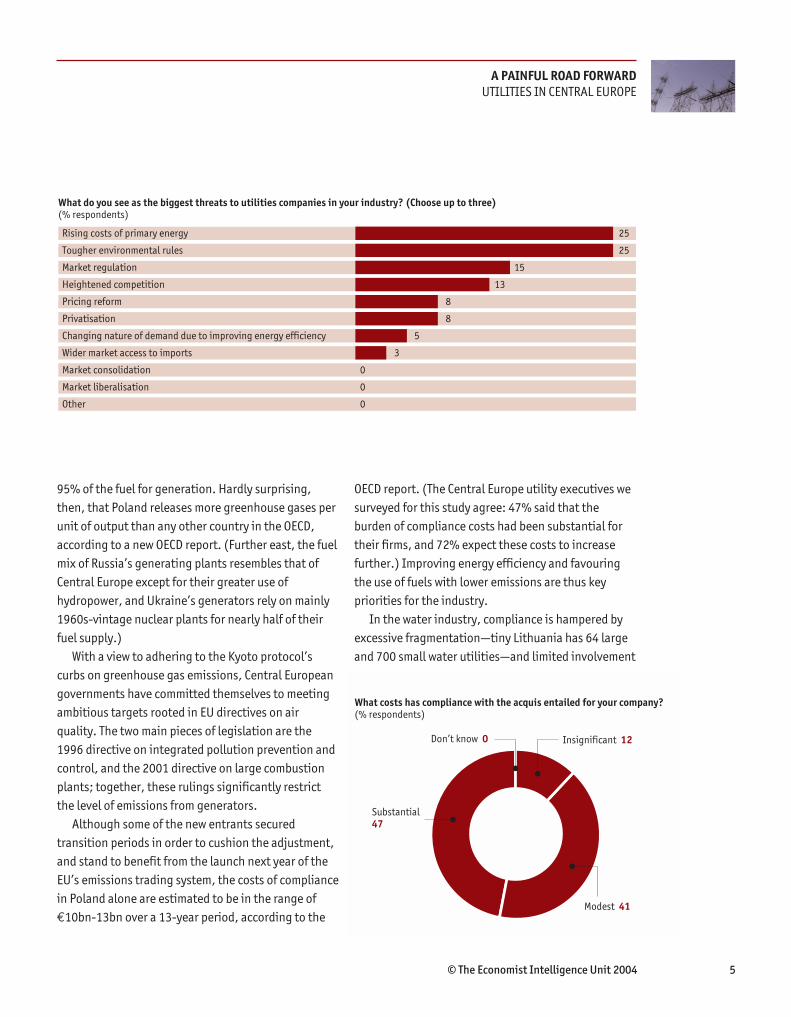

95% of the fuel for generation. Hardly surprising,

then, that Poland releases more greenhouse gases per

unit of output than any other country in the OECD,

according to a new OECD report. (Further east, the fuel

mix of Russia’s generating plants resembles that of

Central Europe except for their greater use of

hydropower, and Ukraine’s generators rely on mainly

1960s-vintage nuclear plants for nearly half of their

fuel supply.)

With a view to adhering to the Kyoto protocol’s

curbs on greenhouse gas emissions, Central European

governments have committed themselves to meeting

ambitious targets rooted in EU directives on air

quality. The two main pieces of legislation are the

1996 directive on integrated pollution prevention and

control, and the 2001 directive on large combustion

plants; together, these rulings significantly restrict

the level of emissions from generators.

Although some of the new entrants secured

transition periods in order to cushion the adjustment,

and stand to benefit from the launch next year of the

EU’s emissions trading system, the costs of compliance

in Poland alone are estimated to be in the range of

€10bn-13bn over a 13-year period, according to the

OECD report. (The Central Europe utility executives we

surveyed for this study agree: 47% said that the

burden of compliance costs had been substantial for

their firms, and 72% expect these costs to increase

further.) Improving energy efficiency and favouring

the use of fuels with lower emissions are thus key

priorities for the industry.

In the water industry, compliance is hampered by

excessive fragmentation—tiny Lithuania has 64 large

and 700 small water utilities—and limited involvement

What do you see as the biggest threats to utilities companies in your industry? (Choose up to three)(% respondents)

Rising costs of primary energy 25

Tougher environmental rules 25

Market regulation 15

Heightened competition 13

Pricing reform 8

Privatisation 8

Changing nature of demand due to improving energy efficiency 5

Wider market access to imports 3

Market consolidation 0

Market liberalisation 0

Other 0

What costs has compliance with the acquis entailed for your company? (% respondents)

Insignificant 12Don’t know 0

Substantial 47

Modest 41

6 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

of the private sector in both the ownership of assets

and their rights of operation. Apart from the Czech

Republic, where multinationals such as Veolia

Environnement (France) built up a strong presence

following a “mass privatisation” drive in the early

1990s, most of Central Europe’s water utilities are

municipally owned providers that are still in the

process of being commercialised. “Local governments

are the regulator, owner and consumer all at once,”

notes Thomas Maier, director for municipal and

environmental infrastructure at the European Bank for

Reconstruction and Development (EBRD) in London.

The main regulatory driver for Central Europe’s

water industry over the past several years has been the

1991 urban wastewater treatment directive, which

requires that cities and towns meet minimum

wastewater collection and treatment standards. The

2000 water framework directive expands the scope of

protection to all waters, sets up a system of

management within river basins and prescribes tariff

regimes that ensure that polluters pay.

Sewerage and wastewater infrastructure are the areas

most in need of investment. Even in Slovenia, the

wealthiest of the new Central European members, only

53% of the population is connected to a sewerage

system, and 57% of wastewater is not (adequately)

treated, according to a new study by the EBRD. Given the

vast investment needs of the sector, big improvements

in efficiency—preferably through increased private-

sector participation—are indispensable.

How will your company’s compliance costs change over the next three years?(% respondents)

Compliance costs will fall sharply 6

Compliance costs will fall slightly 0

Compliance costs will remain the same 22

Compliance costs will rise slightly 56

Compliance costs will rise sharply 17

Coverage of water supply, sewerage and wastewater treatment in selected countries

(%)

Population with Population with Wastewater

Country water connection sewerage treated

Lithuania 70 60 36

Slovenia 76 53 43

Poland 90 58 60

Bulgaria 81 42 42

Romania 58 50 47

Serbia & Montenegro 76 52 37

Russia* 84 70 91

Ukraine* 83 53 97

EU / OECD 80-100 55-98 50-90

* Urban areas only

Source: European Bank for Reconstruction and Development, Municipal and environmental infrastructure: Operations policy 2004 – 2008.

© The Economist Intelligence Unit 2004 7

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

Cost efficiency has overtaken competition as

the dominant theme in Central European

electricity. For utilities in the region’s poorer

countries, complying with stringent

environmental regulations while maintaining price

competitiveness and security of supply is an almost

insurmountable task in present conditions. According

to the International Energy Agency (IEA), for one,

improving energy efficiency will help to square the

circle. Although energy consumption in the region has

fallen since the start of the post-communist reforms

(mainly because of the steep fall in production by big

industrial end-users), energy intensity, or the ratio of

energy consumption to GDP, remains very high by

OECD standards.

The mastering of new technologies should help.

Central European utility executives surveyed for this

paper cited increased network automation as one of

The efficiency gap

Where will your company invest to achieve greater operational efficiency? (Choose all that apply) (% respondents)

Increased network automation 26

Integrated asset and financial management 23

More automation of customer contact centres 20

Acquisitions to achieve economies of scale 14

Mobile technology for improved field force management 9

More use of third party suppliers 9

Supply chain logistics 0

Other 0

In which areas of your business do you expect to see the greatest benefits from your investment in technology? (Choose three) (% respondents)

Increased efficiency of generation 22

Lower costs 18

Improved knowledge management 13

Better customer service 13

Increased efficiency of transmission 8

Better financial management 8

Improved sales and marketing 7

More successful customer relationship management 5

Enhanced back-office systems and networks 3

Easier collaboration with partners and suppliers 2

Increased productivity from mobile and remote workers 0

Other 0

8 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

the key areas of investment in their efforts to improve

operational efficiency. By far the two most important

benefits they seek from their technology investments

are better efficiency of generation and reduced

network costs. New electric and environmental

technologies—such as modern lighting systems, heat

pumps and boilers—will also help to reduce emissions.

Standing up for nuclear

The greatest savings for utilities, however, will come

from the use of cheaper and cleaner fuels. Unlike

Hungary and the Czech Republic, which have

diversified their primary energy sources, Poland still

relies heavily on dirty and expensive coal. “It’s our

Achilles heel in that it makes environmental

compliance all the more difficult,” laments Grzegorz

Gorski, the head of Polish operations of Electrabel

(Belgium). Clustered in the southern region of Silesia,

Poland’s heavily subsidised coal industry is still mired

in debt, despite considerable downsizing over the past

several years and the recent surge in global

commodity prices. As long as the sector’s combative

trade unions keep scotching plans to streamline the

industry, Poland’s emissions will remain high, the

government will struggle to price coal on a cost-

recovery basis and the long-awaited switch to natural

gas will make scant headway.

Seen in this light, Central European countries with

access to cheaper and cleaner nuclear energy—

Slovakia, the Czech Republic and Lithuania are the

main producers—are in a more fortunate position.

Although the anti-nuclear lobby in the EU still wields

considerable influence, fears of global warming caused

by greenhouse gases are prompting a reappraisal of

nuclear power. Slovakia’s government recently insisted

that bids for a 66% stake in Slovenske Elektrarne, the

country’s main power utility, which operates two base-

load nuclear plants generating over two-thirds of its

electricity, must include its nuclear assets (despite

attempts by Austria’s Verbund and Germany’s Eon to

cherry-pick its hydroelectric and thermal operations)

in order to guarantee security of supply.

According to a report by the Boston Consulting

Group (US), there are “long-term considerations that

argue for keeping the nuclear option open [if] Europe

remains committed to implementing Kyoto”. Slovakia

and the Czech Republic are likely to join other EU

countries, such as France, in championing nuclear

facilities on environmental and competitive grounds.

“Unless we suddenly come up with a new technology,

it’s not possible to meet emission reduction targets

without relying on nuclear,” insists Alan Svoboda, the

deputy head of Ceske Energeticke Zavody (CEZ), the

Czech Republic’s main power utility.

Tariff reform

One way to alleviate the seemingly intractable fuel

cost burden is to push ahead with tariff reform.

Although most Central European countries have made

significant progress in this area— according to the

EBRD, substantial tariff increases over the last several

years have allowed companies to attract the capital

needed to maintain and upgrade their networks (see

Coal 37

What do you expect will be the main sources of primary energy in your industry over the next five years? (Choose up to three) (% respondents)

Other 3

Oil 5

Natural gas 16

Nuclear power 18

Hydropower 21

© The Economist Intelligence Unit 2004 9

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

table)—sluggish unbundling of transmission grids is

hampering the phasing-out of cross-subsidies

between household and industrial customers.

According to the OECD, industrial end-user prices in

Poland in 2001 were only 0.3% above their 1991 levels

because of long-term contracts for coal. “In certain

cases, households are subsidising industry,” says

Tadeusz Staszewski, head of business development for

the Polish operations of Vattenfall (Sweden).

Central Europe’s water utilities have been much less

successful in implementing cost-reflective prices than

power suppliers. This is partly owing to the inherently

conflicting goals of tariff reform—although prices

should generate sufficient revenue to cover the cost of

supply, they should not be so high as to produce a

drop in consumption, requiring further tariff increases

to protect revenue, as was the case in Hungary,

Estonia and Latvia.

The main impediment to water pricing reform,

however, has to do with the political constraints of

municipal ownership and regulation. The municipal

water supply and sewerage company of Bydgoszcz, in

northern Poland, is struggling to raise its tariffs to an

acceptable affordability level of 2.9% of household

income as a condition for having received a coveted

ISPA grant from the EU (a pre-accession financial

package to assist with large-scale environmental and

transport projects). “We face constant criticism from

the city council,” says Stanislaw Drzewiecki, MWiK’s

general director. This is one of the reasons why the

involvement of the private sector is deemed essential.

Yet this is easier said than done.

In some countries, physical constraints also impede

water tariff reform. Less than 30% of the population in

Russia and Ukraine, for example, are metered,

according to the EBRD, whereas many OECD and other

developed countries have metering rates close to

100% of the population.

Electricity price trends in Central Europe, US ¢/kwh

Residential Non-residential

2000 2001 2002 2003 2000 2001 2002 2003

Czech Rep 5.40 6.70 8.10 8.77 5.40 5.22 6.60 7.01

Estonia 4.50 4.41 5.16 6.10 4.50 4.44 5.11 5.65

Hungary 6.62 6.78 7.98 10.35 4.95 5.08 5.97 7.44

Latvia 6.47 6.39 6.31 6.83 5.82 5.76 5.29 5.70

Lithuania 6.12 6.27 7.25 8.77 4.47 5.22 6.53 7.78

Poland 6.63 7.69 8.54 9.27 5.31 6.42 6.97 7.48

Slovakia 4.87 5.59 6.23 10.14 na na 7.19 10.71na = data not available

Source: EBRD

10 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

The global wave of infrastructure privatisation

and liberalisation in the 1990s has given way

to public disenchantment with sell-offs and

investor scepticism towards deregulation in

the absence of a sound regulatory framework. The new

reckoning pervades Central Europe’s electricity sector.

Political resistance to power sales, fuelled by trade

union intransigence and nationalist opposition to

selling the “family silver” to foreigners, is on the rise.

Even in the tiny Baltic states, where there should be

a premium on mergers and acquisitions to build scale,

privatisation is a touchy issue. “Politics gets in the

way,” says Gunnar Okk, the head of Eesti Energia,

Estonia’s main power utility, whose solitary bid earlier

this year for one of neighbouring Lithuania’s suppliers

was rejected by the government at the eleventh hour.

To make matters worse, Central Europe’s power

sector suffers from a dearth of prospective investors.

After years of aggressive expansion, international

utilities are in a period of deep retrenchment. As a

recent report from Pan Eurasian Enterprises, a North

Carolina-based consultancy specialising in east

European energy, notes: “The feeding frenzy for

investors in the power sector is over.” Local utility

executives seem to agree: when they were asked

about major opportunities for the sector,

privatisation ranked no higher than third as a

response, after export sales and well below further

market liberalisation.

Anthony Marsh, director for power and energy

utilities at the EBRD, says electricity is no longer a low-

risk business. In order to fund much-needed capital

investments in the sector, Central Europe’s

governments will have to address investors’

Coming to terms with private investment

What does your company see as its main competitive advantages? (Choose up to three) (% respondents)

Cost efficiency 13

Innovation 13

Quality of workforce 11

Access to finance 10

Access to primary energy sources 10

Access to new markets 8

Distribution network 8

Knowledge of local markets 8

Quality of product/service offering 8

Transmission network 7

Flexibility 7

Quality of customer service 7

Lean supply chain 3

Sales/marketing strength 0

Other 0

© The Economist Intelligence Unit 2004 11

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

grievances, particularly when it comes to the vexed

issue of long-term power purchase agreements (PPAs).

The PPA conundrum

In some of Central Europe’s power markets, competition

is restrained by PPAs, a product of the monopolistic

“single buyer” model of electricity under which the

incumbent grid operator purchases most of the power

from generators and resells it to distributors, all at a

fixed price. PPAs are invariably set at above-market

prices to cover investment costs for modernisation

work. In Hungary, Western strategic investors insisted

on PPAs as a condition for acquiring power plants.

“Nobody was really thinking about price liberalisation

back then, and the government needed to plug its

budget deficit,” notes Mr Kaderjak of the Regional

Centre for Energy Policy Research. Although Hungary

passed legislation in 2002 to resolve the “stranded

costs” problem—investments that suddenly become

uneconomic owing to liberalisation—MVM and the

generators are reluctant to renegotiate the contracts.

“The scheme is voluntary,” says Mr Kaderjak.

Poland’s government, on the other hand, has been

riling utilities and creditors by seeking to annul PPAs

in order to allow the transmission grid to exit the

trading business once and for all. The grid operator

was encouraged in the mid-1990s to sign long-term

contracts with generators as collateral for hefty bank

loans to finance environmental upgrades. For those

investors, such as PSEG Global (US), that took on

credit risk by doing PPA-backed project-finance deals,

cancellation of the contracts would result in banks

The Polish government’s scheme to scrap

long-term power purchase agreements

has set the cat among the pigeons. One

company that would stand to lose from a

forced annulment of the contracts is the

2,166-mw lignite-fired Elektrownia

Turow, Poland’s fourth-largest power

plant. In order to finance a mammoth

environmental upgrade, state-owned

Turow was encouraged by the government

in 1994 to sign a 22-year PPA with state

grid Polskie Sieci Elektroenergetyczne

(PSE). This allowed it to secure financing

for a €1.2bn investment programme—the

largest in the Polish electricity sector—

that included a high-profile international

bond issue. “Without the PPA, we would

not have had the leverage for huge

investments in de-sulphurisation,” insists

Jerzy Laskawiec, the veteran head of Elek-

trownia Turow.

Turow’s three-stage revamp has allowed

it to extend the lifespan of six of its ten

units to 2035, improve energy efficiency

and lower emissions to comply with EU

environmental standards. “We have

reduced emissions by some 60% over the

past decade. We are also one of the first

plants in Europe to use circulating

fluidised-bed technology (CFB) for our

boilers,” adds Mr Laskawiec. The upgrade is

nearly complete, with the last of its

modernised units due to be re-

commissioned early next year. “In

November, we’ll celebrate the completion

of the project. We’re in a much better

position than other plants, but we still have

to pay off the banks.”

Turow hopes that the compensation

formula in the government’s scheme—

staggered payments that are supposed to

cover the difference in the market value of

generators before and after the

cancellation of their PPAs—will prove

acceptable to its creditors. With debts of

over €900,000 at the end of last year,

Turow’s fortunes hinge on the goodwill of

its lenders. “I can’t envision a scenario

where banks would be wronged. They

provide the funds for modernisation,” Mr

Laskawiec says. Yet the government is

caught between a rock and a hard place:

whereas generators and creditors fear they

will not be adequately compensated, the

European Commission wants to restrict the

level of payments lest they fall foul of EU

rules on state aid.

Poland’s PPAs—A blessing for some

12 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

calling in their loans and potentially seizing control of

their assets.

If the Polish government rides roughshod over the

interests of investors and utilities, it could face legal

action. Yet it has the backing of the European

Commission, which wants Poland to dissolve its PPAs—

provided the compensation payments for annulling

the contracts do not breach EU rules on state aid—in

order to create a fully liberalised and unified wholesale

power market in Central Europe. “When you have

roughly half the trade in the largest market tied up in

PPAs, this won’t happen,” says a senior EU official.

Although Poland's govermment is moving in the

direction of a voluntary PPA-cancellation scheme, as

long as the uncertainty surrounding PPAs persists,

investors will shun Poland’s power market.

Add more P’s for potency

Private participation in Central Europe’s water and

waste treatment sectors is something of a rarity.

According to the EBRD study, public-private

partnerships, or PPPs (contractual agreements

between public agencies and private companies,

mainly in the form of management contracts and

leases) cover a paltry 4% of the region’s population,

compared with 42% in Western Europe. Although a

wariness on the part of local governments towards

private-sector involvement is partly to blame,

inadequate regulation is the main culprit. Even in

Bulgaria, which clinched the region’s first major PPP in

2000 when Sofia’s city council signed a 25-year

concession agreement with International

Water/United Utilities (UK), there have been

“concerns about transparency, the clarity of the

contract, the investment programme and the price

formulation,” according to a recent EU-commissioned

study on Central Europe’s water sectors. The EBRD

claims that only one-quarter of Central and East

European states have “adequate” concession laws.

Preoccupied with obtaining EU funds for

investments, Central European countries have devoted

fewer resources to the promotion of PPPs because of

their perceived complexity and popular fears

surrounding private investment in water. “Many local

governments prefer to keep ownership of poorly run

and inefficient companies rather than bring private

investors on board,” says Mr Drzewiecki.

According to the aforementioned EU-commissioned

study, the benefits of private participation/ownership

are being questioned because of concerns that

multinational companies—which have a strong

presence in the Czech Republic and, to a lesser extent,

in Hungary—are not fulfilling their investment

obligations. “Re-investment by utilities [with] private

sector involvement appears to be limited,” the report

notes. If anything, this puts more of a premium on

transparent and rigorous regulation—ideally

buttressed by the creation of independent watchdogs.

Number of PPPs in Central Europe's water sector

Czech Republic 16

Hungary 7

Poland 3

Russian Federation 2

Armenia 1

Bulgaria 1

Croatia 1

Estonia 1

Georgia 1

Romania 1

Slovakia 1

Slovenia 1

Source: EBRD, Municipal and environmental infrastructure: Operations policy 2004 – 2008.

© The Economist Intelligence Unit 2004 13

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

In order for Central Europe’s utilities to hold their

own in the EU, they will need to bulk up. Even in

some of the smaller markets, such as Hungary,

there has been little consolidation. In Poland’s

power sector there are still 17 large plants, 29

distributors and 19 combined-heat-and-power (CHP)

plants. Most of them lack the critical mass to

withstand competition from Western Europe’s

mammoth, vertically integrated firms.

Nowhere is the need for consolidation more

pressing than in the Baltic states. “We’re far too small

to go it alone. We have to grow—and grow together—

to be part of the Nordic market. Consolidation is not

science fiction. The only question is who will do the

consolidating: us or a German operator,” says Mr Okk

of Eesti Energia.

In Russia, dismantling of the vast UES network has

yet to begin, but if it goes to plan (a big if), more than

twenty new generating companies will be in operation

by 2007 and at least five distribution firms, along with

one national grid operator. Particularly in the

generation sector, a few regional companies will be

much weaker than others, and some degree of

consolidation with private-sector participation,

including from foreign sources, is likely.

In the water industry, although decentralisation

has accelerated the process of commercialisation,

some markets—notably Poland, Hungary and the

Czech Republic—are now overly fragmented,

hampering restructuring efforts. Many municipalities

are too small to raise financing for investments.

“There are ten water companies in the UK and 250 in

Poland. The excessive fragmentation results in

diseconomies of scale,” says Gerry Muscat, a senior

banker in municipal and environmental infrastructure

at the EBRD’s offices in Warsaw. Compliance with the

EU’s new framework water directive, which will require

integrated management at the river basin level, is

designed to encourage consolidation.

The allure of national champions

A flurry of domestic mergers and crossborder

takeovers over the past few years has turned Europe’s

electricity market into an elite club of six or seven

Strategies for growth

What approaches will your company take to drive growth over the next three years? Please rate the importance of the following approaches to your company's strategic goals on a scale of 1 to 5, where 1 is critically important and 5 is relatively unimportant. (Average)

Expanding transmission capacity 3.9

Entering new export markets 3.6

Achieving growth through mergers and acquisitions 3.3

Improving distribution channels 3.3

Improving transmission network 3.3

Entering new geographical markets domestically 3.1

Entering new alliance relationships 3.0

Increasing advertising and marketing spend 3.0

Expanding generation capacity 2.6

Building closer relations with existing customers 2.4

14 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

mega-utilities. This has not been lost on Central

Europe’s smaller companies. State-controlled CEZ

wants to become a regional powerhouse. It is already

Europe’s second-largest power exporter and is

aggressively pursuing crossborder deals to capture

more customers. It recently won a tender to purchase

a cluster of suppliers in Bulgaria, and it launched an

unsuccessful bid to buy a majority stake in

neighbouring Slovakia’s main utility. “We’re playing

the one game that’s left for us. Since we can’t be

leaders in Western Europe, we have to have a strong

presence in our region,” says its deputy head, Alan

Svoboda.

Poland is also keen on building national

champions. The government encouraged the creation

of two large generation groups that, together, account

for over 45% of production. One of the groups, BOT,

also includes coal mines and wants to acquire

distributors in order to become a vertically integrated

power company. “It was a big mistake not to

consolidate earlier. We need the critical mass to

compete on the European stage,” says Jerzy

Laskawiec, the head of Elektrownia Turow, the driving

force behind the creation of BOT. Yet unlike CEZ, which

cut costs and raised its efficiency, Poland’s national

champions are heavily indebted and overstaffed.

Although mergers may be necessary, consolidation in

Poland is often perceived as a craven alternative to

These are thrilling times for Ceske Energet-

icke Zavody (CEZ), the Czech Republic’s

main power utility. Eager to cement its

position as Central Europe’s largest elec-

tricity company, CEZ is giving foreign oper-

ators in the region a run for their money by

bidding for coveted assets in neighbouring

Slovakia and Bulgaria. “We’re able to stand

up to the big Western operators in this

region—particularly in the Balkans where

power markets are only just beginning to

open,” says Alan Svoboda, the deputy head

of CEZ. Yet one of the company’s main com-

petitive edges—its thriving export business

which last year accounted for one-third of

its production, making it Europe’s second-

largest power exporter after EdF (France)—

is under threat because of perennial

bottlenecks in crossborder trade.

Despite the adoption of a new EU

directive in 2003 aimed at facilitating

crossborder trade in electricity, there has

been limited progress in establishing fair

and transparent rules for market-based

allocation of transmission capacity.

Although this is partly owing to meagre

infrastructure for crossborder trade, many

utilities point the finger at obstructive

behaviour from national transmission

system operators (TSOs)—often condoned

by regulators. CEZ said earlier this year

that it expected its exports in 2004 to fall

by 15%, partly because of problems

obtaining crossborder capacity from

neighbouring Germany and Austria. “Last

year, things were moving in the right

direction. The [crossborder] auctions were

set up and the power was flowing. But this

year, after the black-outs, the German and

Austrian TSOs have reduced the capacity.

It’s hard to prove that their technical

worries are exaggerated. At the very least,

there needs to be an EU-wide authority to

oversee the operations of TSOs,” says Mr

Svoboda.

CEZ: Trading woes

© The Economist Intelligence Unit 2004 15

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

privatisation. Far better, experts say, to let private

investors do the consolidating themselves.

Size isn’t everything

Although the national champion model is all the rage

in Central Europe, large-scale consolidation is no

panacea. For one thing, the European Commission,

which now regrets having taken a relaxed attitude to

big energy mergers in Western Europe, is loth to let

Central Europe’s power market go down the same

route. “We wouldn’t want investors to think they will

be getting a captive market,” one EU official says.

Moreover, if market-opening is to become

entrenched, Central Europe’s fledgling energy

watchdogs and antitrust agencies will have to show

their teeth. Hungary’s regulator, for example, was set

up a decade ago, but it still lacks the power to set

prices. One of the main regulatory dilemmas over the

coming years, as consolidation—including of the

crossborder variety—inevitably gathers pace, will be to

strike a balance between national champion

arguments and competition concerns.

Since liberalisation no longer carries the promise of

cheaper power, cynics argue that consumers are

bound to lose out. However, this need not be the case.

Hungarian businesses have enjoyed cheaper prices

since they switched suppliers last year, and Poland set

up the region’s first power exchange in an effort to

spur competition once its PPAs are dissolved. These

developments augur well for market-opening.

Appendix: survey results

In July/August 2004, the Economist Intelligence Unit conducted an online survey of 20 power and water industry execu-

tives located throughout the EU accession and candidate countries. Our sincere thanks go to everyone who took part in the

survey.

Please note that not all answers add up to 100%, because of rounding or because respondents were able to provide multiple

answers to one question.

Demographics

In which country are you located? (% respondents)

Bulgaria 44

Poland 39

Romania 11

Czech Republic 6

In which country is your company’s global headquarters located? (% respondents)

Bulgaria 29

Poland 21

France 14

Germany 7

Sweden 7

Italy 7

Romania 7

Belgium 7

16 © The Economist Intelligence Unit 2004

A PAINFUL ROAD FORWARD

UTILITIES IN CENTRAL EUROPE

Which of the following titles best describes your job? (% respondents)

CEO/COO/Chief executive/Managing director 26

Director/VP of marketing 16

Other director/VP 11

Other manager 5

Other 42

© The Economist Intelligence Unit 2004 17

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

What percentage of your company’s turnover comes from your domestic market?(% respondents)

Will EU enlargement benefit your company?(% respondents)

Yes 76

25%-50% 6

75%-90% 6

Over 90% 89

No 24

What branch of the utilities industry does your company represent?(% respondents)

Power generation 58

Power distribution 21

More than one of the above 11

Water and sewerage 5

Power transmission 0

Power delivery, metering, billing 0

Other 5

How many employees does your company have across all locations?(% respondents)

Under 500 0

100-1,000 44

1,000-5,000 28

5,000-10,000 17

10,000-20,000 0

20,000-50,000 6

More than 50,000 6

18 © The Economist Intelligence Unit 2004

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

What does your company see as its main competitive advantages? (Choose up to three) (% respondents)

Cost efficiency 13

Innovation 13

Quality of workforce 11

Access to finance 10

Access to primary energy sources 10

Access to new markets 8

Distribution network 8

Knowledge of local markets 8

Quality of product/service offering 8

Transmission network 7

Flexibility 7

Quality of customer service 7

Lean supply chain 3

Sales/marketing strength 0

Other 0

What does your company see as its greatest vulnerabilities? (Choose up to three) (% respondents)

Cost efficiency 19

Flexibility 16

Sales/marketing strength 16

Access to finance 9

Distribution network 9

Innovation 9

Quality of customer service 9

Quality of workforce 9

Access to new markets 6

Access to primary energy sources 6

Transmission network 3

Lean supply chain 3

Knowledge of local markets 0

Quality of product/service offering 0

Other 3

© The Economist Intelligence Unit 2004 19

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

What are your company’s strategic priorities after EU enlargement? Please rate the importance of each of the following on a scale of 1 to 5, where 1 is critically important and 5 is relatively unimportant. (Average)

We will seek to expand beyond the EU 4.0

We will seek to expand into West European EU member states 3.8

We will seek to expand into other Central European EU member states 3.5

We will seek to expand into other domestic markets 3.1

We will seek to consolidate our position in our home market 2.0

What approaches will your company take to drive growth over the next three years? Please rate the importance of the following approaches to your company's strategic goals on a scale of 1 to 5, where 1 is critically important and 5 is relatively unimportant. (Average)

Expanding transmission capacity 3.9

Entering new export markets 3.6

Achieving growth through mergers and acquisitions 3.3

Improving distribution channels 3.3

Improving transmission network 3.3

Entering new geographical markets domestically 3.1

Entering new alliance relationships 3.0

Increasing advertising and marketing spend 3.0

Expanding generation capacity 2.6

Building closer relations with existing customers 2.4

How do you expect primary energy costs in your industry to change over the next three years?(% respondents) They will fall

dramatically 0

How do you expect regulatory control over wholesale and retail prices in your industry to change over the next three years?(% respondents)

It will stay the same 44

They will rise dramatically 0

They will rise modestly 58

They will stay the same 26

They will fall modestly 16

It will tighten dramatically 0

It will loosen dramatically 0

It will tighten modestly 39

It will loosen modestly 17

20 © The Economist Intelligence Unit 2004

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

What are your company’s investment priorities over the next three years? (Choose all that apply) (% respondents)

Human resources/training 18

Generating plant and equipment 17

Customer servicing 13

General management 13

Sales and marketing 13

Transmission network 13

Finance and accounting 7

Product development 5

Supply chain/logistics 0

Other 0

Where will your company invest to achieve greater operational efficiency? (Choose all that apply) (% respondents)

Increased network automation 26

Integrated asset and financial management 23

More automation of customer contact centres 20

Acquisitions to achieve economies of scale 14

Mobile technology for improved field force management 9

More use of third party suppliers 9

Supply chain logistics 0

Other 0

In which areas of your business do you expect to see the greatest benefits from your investment in technology? (Choose three) (% respondents)

Increased efficiency of generation 22

Lower costs 18

Improved knowledge management 13

Better customer service 13

Increased efficiency of transmission 8

Better financial management 8

Improved sales and marketing 7

More successful customer relationship management 5

Enhanced back-office systems and networks 3

Easier collaboration with partners and suppliers 2

Increased productivity from mobile and remote workers 0

Other 0

© The Economist Intelligence Unit 2004 21

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

In your view, which of the following technologies are most important for the utilities sector? Please rate the importance of each of the following technologies on a scale of 1 to 5, where 1 is critically important and 5 is relatively unimportant. (Average)

Supplier self-service access to orders and payment systems 3.5

Moving from in-house IT to use of global service providers 3.5

Ability to transmit maps and diagrams to field staff 3.4

Customer self-service access to bills 3.3

Continuous Internet access from the field to corporate systems 2.8

Automation of cross-departmental processes 2.5

Increased use of standard packages and business processes 2.4

What do you see as the biggest opportunities for utilities companies in your industry? (Choose up to three)(% respondents)

Market liberalisation 24

Access to export markets 13

Privatisation 11

Tougher environmental rules 9

Pricing reform 9

Heightened competition 9

Expansion of primary energy sources 7

Market consolidation 7

Changing nature of demand due to improving energy efficiency 7

Market regulation 2

Other 0

What do you see as the biggest threats to utilities companies in your industry? (Choose up to three)(% respondents)

Rising costs of primary energy 25

Tougher environmental rules 25

Market regulation 15

Heightened competition 13

Pricing reform 8

Privatisation 8

Changing nature of demand due to improving energy efficiency 5

Wider market access to imports 3

Market consolidation 0

Market liberalisation 0

Other 0

22 © The Economist Intelligence Unit 2004

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

Coal 37

What do you expect will be the main sources of primary energy in your industry over the next five years? (Choose up to three) (% respondents)

Other 3

Oil 5

Natural gas 16

Nuclear power 18

Hydropower 21

When will your firm be in compliance with the relevant areas of EU legislation—the acquis communautaire (excluding areas where transition periods apply)(% respondents)

We are already fully compliant 29

We will be in compliance this year 12

We will be in compliance next year 18

We will be in compliance in 2006 24

We will be in compliance later than 2006, but within five years 6

We will not be in compliance within five years 0

Don’t know 12

What areas of the acquis have posed the biggest challenges for your company? (Choose up to three)(% respondents)

Environmental protection 33

Competition rules 18

Customs and excise 12

Workplace health and safety 12

Taxation 9

Consumer protection 6

Corporate governance/reporting 6

Don't know 3

Product liability 0

Workforce representation 0

Other 0

© The Economist Intelligence Unit 2004 23

APPENDIX: SURVEY RESULTS

A PAINFUL ROAD FORWARD: UTILITIES IN CENTRAL EUROPE

What costs has compliance with the acquis entailed for your company? (% respondents)

Insignificant 12Don’t know 0

Substantial 47

Modest 41

How will your company’s compliance costs change over the next three years?(% respondents)

Compliance costs will fall sharply 6

Compliance costs will fall slightly 0

Compliance costs will remain the same 22

Compliance costs will rise slightly 56

Compliance costs will rise sharply 17

What is your company’s main source of information on EU compliance issues?(% respondents)

General business press 46

Local industry associations 23

EU 15

Consultancies 15

Government 0

Country-based EU delegations 0

Trade press 0

How do you access information on EU compliance issues?(% respondents)

An even mix of print and online sources 35

Mainly through print media 12

Mainly online 6

Through third parties (e.g. legal firms) 6

An even mix of both 0

A combination of all of the above 41

Whilst every effort has been taken to verify the

accuracy of this information, neither The Economist

Intelligence Unit Ltd., Oracle nor their affiliates can

accept any responsibility or liability for reliance by any

person on this white paper or any of the information,

opinions or conclusions set out in the white paper.

LONDON

15 Regent Street

London

SW1Y 4LR

United Kingdom

Tel: (44.20) 7830 1000

Fax: (44.20) 7499 9767

E-mail: [email protected]

NEW YORK

111 West 57th Street

New York

NY 10019

United States

Tel: (1.212) 554 0600

Fax: (1.212) 586 1181/2

E-mail: [email protected]

HONG KONG

60/F, Central Plaza

18 Harbour Road

Wanchai

Hong Kong

Tel: (852) 2585 3888

Fax: (852) 2802 7638

E-mail: [email protected]