A market leader in retail logistics and business activity performance 8 Continued strong growth in...

27

A market leader in retail logistics Logistics evolved: Agility and Ability 2017 Full Year Results Presentation 28 July 2017

Transcript of A market leader in retail logistics and business activity performance 8 Continued strong growth in...

A market leader in retail logistics

Logistics evolved: Agility and Ability

2017 Full Year Results Presentation

28 July 2017

2

Disclaimer

This presentation includes statements that are, or may be deemed to be, “forward-looking statements”. These forward-looking

statements can be identified by the use of forward-looking terminology, including the terms “believe”, “estimates”, “plans”, “projects”,

“anticipates”, “expects”, “intends”, “may”, “will”, or “should” or, in each case, their negative or other variations or comparable

terminology. These forward-looking statements include matters that are not historical facts and include statements regarding the

Company’s intentions, beliefs or current expectations.

Any forward-looking statements in this presentation reflect the Company’s current expectations and projections about future events. By

their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could cause actual results or

events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and

assumptions could adversely affect the outcome and financial effects of the plans and events described herein. Forward-looking

statements contained in this presentation regarding past trends or activities should not be taken as a representation that such trends or

activities will continue in the future. You should not place undue reliance on forward-looking statements, which speak only as of the

date of this presentation. No representations or warranties are made as to the accuracy of such statements, estimates or projections.

Please note that the Directors of the Company are, in making this presentation, not seeking to encourage shareholders to either buy or

sell shares in the Company. Shareholders in any doubt about what action to take are recommended to seek financial advice from an

independent financial advisor authorised by the Financial Services and Markets Act 2000.

3

Agenda

Highlights 1

2

Operational review

o Operational update

o Brand Health

3

Summary and Q&A 4

Financial review

o Financial update

o Post year end acquisitions

Highlights 1

Highlights – financial*

5

* The highlights are for the 12 months ended 30 April 2017, as compared to the 12 months ended 30 April 2016.

1 Group EBIT is defined as operating profit, including the Group’s share of operating profit in equity-accounted investees,

before amortisation of intangible assets arising on consolidation and any exceptional or non-recurring items.

Group revenue growth of 17.2% to £340.1m (2016: £290.3m), driven by strong growth in all divisions.

Group EBIT1 growth of 21.8% to £17.9m (2016: £14.7m):

o E-fulfilment & returns management services – EBIT of £10.2m, up 23.4% (2016: £8.3m).

o Non e-fulfilment logistics – EBIT of £12.4m, up 15.7% (2016: £10.7m).

o Commercial vehicles – EBIT of £2.3m, up 3.5% (2016: £2.3m).

EPS of 12.5p, up 20.5% (2016: 10.3p).

Proposed final dividend of 4.8p per share giving total dividend of 7.2p per share, up 20.0% (2016:

6.0p).

Cash generated from operations: growth of 25.2% to £25.7m (2016: £20.5m).

Financial review 2

7

Summary income statement

Headline financials

Strong top-line performance in the year in all

business segments.

EBIT is the key metric, and saw further strong

growth driven in particular by continued contract

evolution in the logistics business.

Increase in finance costs driven by investment in

fixed asset base in order to service new contracts

(predominantly open book).

Dividends

Interim dividend of 2.4 pence per share, paid

December 2016.

Final proposed dividend 4.8 pence per share,

giving total dividend of 7.2 pence per share (6.0

pence year to 30 April 2016).

£m Year to 30 April Change

2017 2016 %

Revenue 340.1 290.3 +17.2%

Cost of sales (241.1) (205.7)

Gross profit 99.0 84.6

Other net gains 0.4 0.2

Admin expenses (81.9) (70.3)

Operating profit before share of equity-

accounted investees, net of tax 17.5 14.5

Share of equity-accounted investees, net of tax 0.2 -

Operating profit 17.7 14.5

EBIT 17.9 14.7 +21.8%

Less: amortisation of other intangible assets (0.2) (0.2)

share of tax and finance costs of equity-accounted

investees (0.0) -

Operating profit 17.7 14.5

Net finance costs (1.6) (1.4)

Profit before income tax 16.1 13.1

Income tax (3.6) (2.8)

Profit for the financial year 12.5 10.3 +20.6%

Basic earnings per share (p) 12.5 10.3 +20.5%

Diluted earnings per share (p) 12.3 10.3

Segmental and business activity performance

8

Continued strong growth in Logistics:

o Organic growth and new business activities on

existing contracts including ASOS, John Lewis

pre-retail activities, Morrisons, Wilko and Zara.

o Full year benefit of prior year contract wins

including Browns, M&Co, Pep&Co and Ireland’s

largest retailer.

o Part-year impact of wins in the year including

Halfords, Inditex, Links of London, Kidly, Pretty

Green, Silkfred, Smiffys and Westwing.

o Significant increase in Click and Collect

revenues through the collaboration with John

Lewis.

Steady growth in commercial vehicles driven by new

vehicle sales and aftersales.

£m Year to 30 April Change

2017 2016 %

E-fulfilment & returns management services 129.9 97.6 +33.0%

Non e-fulfilment logistics 121.9 108.4 +12.5%

Total value-added logistics services 251.8 206.0 +22.2%

Commercial vehicles 91.5 85.6 +6.9%

Inter-segment sales (3.2) (1.3)

Group revenue 340.1 290.3 +17.2%

£m Year to 30 April Change

2017 2016 %

E-fulfilment & returns management services 10.2 8.3 +23.4%

Non e-fulfilment logistics 12.4 10.7 +15.7%

Central logistics overheads (4.8) (4.7)

Total value-added logistics services 17.8 14.3 +24.6%

Commercial vehicles 2.3 2.3 +3.5%

Head office costs (2.2) (1.9)

Group EBIT 17.9 14.7 +21.8%

Revenue

EBIT

9

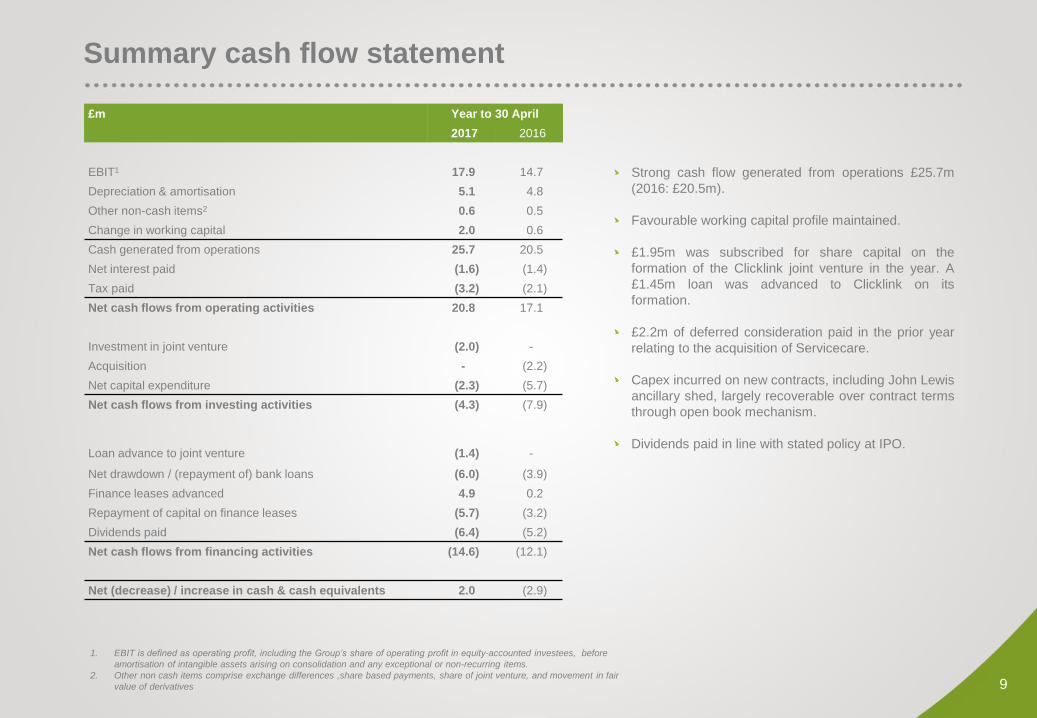

Summary cash flow statement

Strong cash flow generated from operations £25.7m

(2016: £20.5m).

Favourable working capital profile maintained.

£1.95m was subscribed for share capital on the

formation of the Clicklink joint venture in the year. A

£1.45m loan was advanced to Clicklink on its

formation.

£2.2m of deferred consideration paid in the prior year

relating to the acquisition of Servicecare.

Capex incurred on new contracts, including John Lewis

ancillary shed, largely recoverable over contract terms

through open book mechanism.

Dividends paid in line with stated policy at IPO.

£m Year to 30 April

2017 2016

EBIT1 17.9 14.7

Depreciation & amortisation 5.1 4.8

Other non-cash items2 0.6 0.5

Change in working capital 2.0 0.6

Cash generated from operations 25.7 20.5

Net interest paid (1.6) (1.4)

Tax paid (3.2) (2.1)

Net cash flows from operating activities 20.8 17.1

Investment in joint venture (2.0) -

Acquisition - (2.2)

Net capital expenditure (2.3) (5.7)

Net cash flows from investing activities (4.3) (7.9)

Loan advance to joint venture (1.4) -

Net drawdown / (repayment of) bank loans (6.0) (3.9)

Finance leases advanced 4.9 0.2

Repayment of capital on finance leases (5.7) (3.2)

Dividends paid (6.4) (5.2)

Net cash flows from financing activities (14.6) (12.1)

Net (decrease) / increase in cash & cash equivalents 2.0 (2.9)

1. EBIT is defined as operating profit, including the Group’s share of operating profit in equity-accounted investees, before

amortisation of intangible assets arising on consolidation and any exceptional or non-recurring items.

2. Other non cash items comprise exchange differences ,share based payments, share of joint venture, and movement in fair

value of derivatives

10

Summary balance sheet

Investment in fixed assets mainly incurred on new

open book contracts.

Net current liabilities position affects continuing positive

working capital model.

Net debt: EBITDA < 1.1

Unused bank facility as at 30 April 2017 £28.0m.

£m As at 30 April

2017 2016

Intangible assets 24.8 24.9

Property, plant & equipment 38.9 25.6

Interest in equity-accounted investees 2.2 -

Non-current financial assets 1.4 -

Deferred tax assets 0.3 -

Non-current assets 67.6 50.5

Inventories 30.0 26.2

Trade & other receivables 47.7 39.9

Cash & cash equivalents 0.9 0.7

Current assets 78.6 66.8

Trade & other payables 85.1 72.2

Borrowings 7.4 6.6

Short term provisions 0.1 0.1

Current tax liabilities 2.2 1.7

Current liabilities 94.8 80.6

Borrowings 20.0 12.9

Long term provisions 1.3 0.8

Deferred tax liabilities - 0.2

Non-current liabilities 21.3 13.9

Net assets 30.1 22.8

Net debt 25.1 18.8

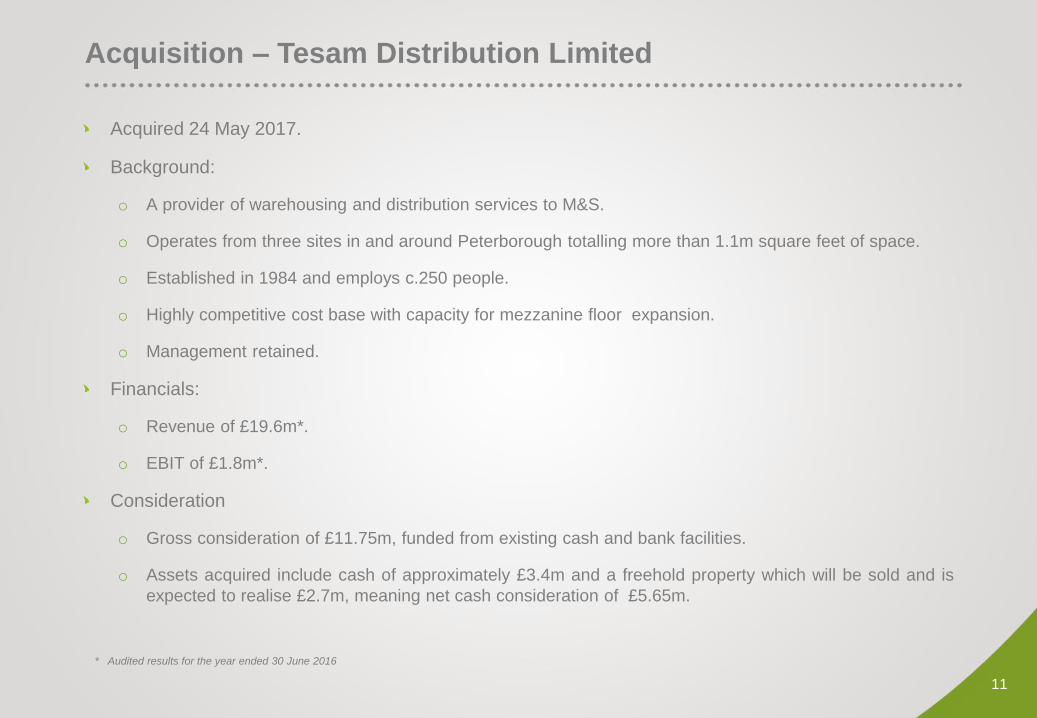

Acquisition – Tesam Distribution Limited

11

Acquired 24 May 2017.

Background:

o A provider of warehousing and distribution services to M&S.

o Operates from three sites in and around Peterborough totalling more than 1.1m square feet of space.

o Established in 1984 and employs c.250 people.

o Highly competitive cost base with capacity for mezzanine floor expansion.

o Management retained.

Financials:

o Revenue of £19.6m*.

o EBIT of £1.8m*.

Consideration

o Gross consideration of £11.75m, funded from existing cash and bank facilities.

o Assets acquired include cash of approximately £3.4m and a freehold property which will be sold and is

expected to realise £2.7m, meaning net cash consideration of £5.65m.

* Audited results for the year ended 30 June 2016

Acquisition – RepairTech Limited

12

Acquired 15 June 2017.

Background:

o Specialist provider of consumer electronic repair services based in Southam, Warwickshire.

o Complementary to Servicecare and Boomerang service offerings.

o Enhances the range of services available to existing Clipper customers, as well as attracting new

RepairTech clients to the Group.

o Management retained.

Financials:

o Revenue of £3.2m*.

o EBIT of £644k*.

Consideration

o Gross consideration of £3.0m, £2.5m funded from existing cash and bank and £0.5m deferred.

o Assets acquired include cash of £0.3m, meaning net cash consideration of £2.7m.

* Unaudited results for the year ended 31 March 2017

Operational review 3

E-fulfilment update

14

Additional e-comm capability created for further M&S product groups

Record volumes for Zara e-fulfilment during summer sale

Secret Sales go-live

Pretty Green go-live

Full start up of 5 Inditex brands

Set up fulfilment solution for BAT Vype

Set up fulfilment solution for PML NicoCigs

SilkFred go-live

Non e-fulfilment update

BAT warehouse & transport contract extended to end 2020.

Transport services extended to a sole supply agreement (ex

DHL).

Philip Morris – supplementary contract to encompass NicoCigs

– to 2020.

Morrisons Nutmeg – womenswear launched and in addition we

have increased capability to support 20% volume growth.

Crosswater – new transport operation.

TAPA (Transported Asset Protection Association) – Top tier

accreditations attained for FSR (Freight) and TSR (Truck) – only

UK operator to be awarded both accreditations at the top tier.

Further developments to support Halfords – pick & pack and

pre-retail.

15

16

Clicklink

Full onboarding of Urban Outfitters – all store replen & Clicklink.

Onboarding of Pull & Bear (Inditex brand) – trial to assess benefit to wider group.

Trial to full roll out for another major fashion player – store replen & Clicklink.

Ted Baker in John Lewis with full roll out being explored.

We now have 12 retail customers using the service with another 12 actively engaged.

The carton volume forecast for the key Autumn/Winter retail trading period shows a circa 25% uplift

when compared to 2016. Furthermore the non-JLP volumes are expected to be circa 17% of the total

by Christmas – demonstrating penetration into the wider sector.

New marketing initiative created to demonstrate the value of interlinking Clicklink & Boomerang – not

only for e-fulfilment but also for store replenishment – a 7 day service creates opportunities for store

inventory reductions.

John Lewis returns management now fully embedded in the ADC.

National Returns Centre in development for large UK retailer.

Returns trial underway for UK fashion retailer.

Record volumes for ASOS Boomerang.

Boomerang

17

New developments

Automation/Infrastructure

“Carrypick” pilot scheme being developed for major fashion customer.

“Autostore” concept development – working closely with 3 existing customers on evaluation.

ASOS Boomerang operation undergoing expansion of operational capability to support growth in

volumes.

Sorter developments underway to support the Clicklink extensive customer growth.

Mezzanine expansion underway at the new Northampton site to support shared use growth.

Ollerton mezzanine expansion underway to accommodate Wilko e-fulfilment growth.

Solutions Design/IT

Developed an e-comm/retail template solution in conjunction with JDA to create rapid roll out

capability for new customers.

Continuous Improvement Programme enhanced - introduction of “The CI Framework”, “The Process

Excellence Model” & “The Clipper Way” – sharing of best practice & collaboration.

Driving training enhanced with Virtual Reality simulator systems.

Servicecare

Commenced bicycle refurbishment for Amazon.

Attained accreditation from Morphy Richards to add to our manufacturer portfolio.

Enlarged our small domestic appliance refurbishment capability.

Rebuilt the Genesis eBay store.

Clipper Brand Health 2017

Clipper continues to enhance visibility, innovate and boost capabilities

• ClickLink

• Boomerang roll out – with extended services via

Servicecare & RepairTech

• “Now is History” campaign – thought leadership

• Future Forum – thought leadership events

• Investment in IT capabilities

• JDA developments

• Processes in place to benefit Tier 2 clients

• New Ops Board appointments: o Emma Dempsey (COO)

o Ant Everett (Engineering & Technology)

o Paul Thirkell (Senior Operations)

Speed and efficiency are important but retailers say chasing Amazon isn't the way

We’re getting carried away thinking that we

need to provide what Amazon do – none of us

have the investment capability they do and in

many cases, speed isn't always what the

customer wants

I don’t

actually

think

people

want next

day!

Next day is important

as an option, but it

doesn't stack up to

be the default

65% of customers expect delivery in 2-3

days, only 15% want it next day

Omnichannel: The future of department store retailing

Extracts from Clipper Brand Health 2017

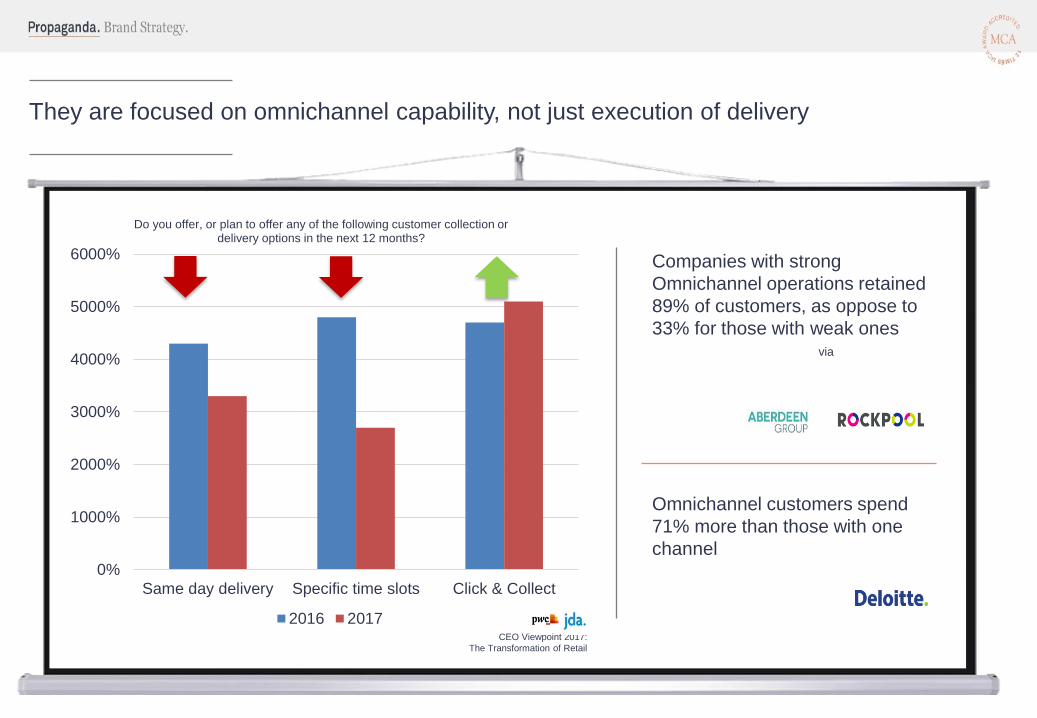

They are focused on omnichannel capability, not just execution of delivery

0%

1000%

2000%

3000%

4000%

5000%

6000%

Same day delivery Specific time slots Click & Collect

Do you offer, or plan to offer any of the following customer collection or delivery options in the next 12 months?

2016 2017CEO Viewpoint 2017:

The Transformation of Retail

Companies with strong

Omnichannel operations retained

89% of customers, as oppose to

33% for those with weak ones via

Omnichannel customers spend

71% more than those with one

channel

Smaller players don’t have the luxury of investment – a concern

• 68% of retailers have started to join the dots, but have

a long way to go to build an integrated omnichannel

view of the customer journey*

• 74% of retailers say returns are eroding profits**

• 33% plan to raise online order prices to cope with

demand**

• 74% of firms reported that they did not expect to have

robotics and automation introduced into their supply

chain for six or more years**

We can’t make automation pay

We need a single pool of stock first and

that’s a long way off

Returns are an issue but

they are a long way down

the list Having staff in store

prepare product doesn't

make sense but it’s our

best bet at the moment

* & , Mastering the culture of click and expect,

featured in ‘The future of E-commerce’, raconteur.net

** & , CEO Viewpoint 2017: The Transformation of Retail

*** &MHI, Accelerating Change: How innovation is driving digital

“always-on” supply chains Extracts from Clipper Brand Health 2017

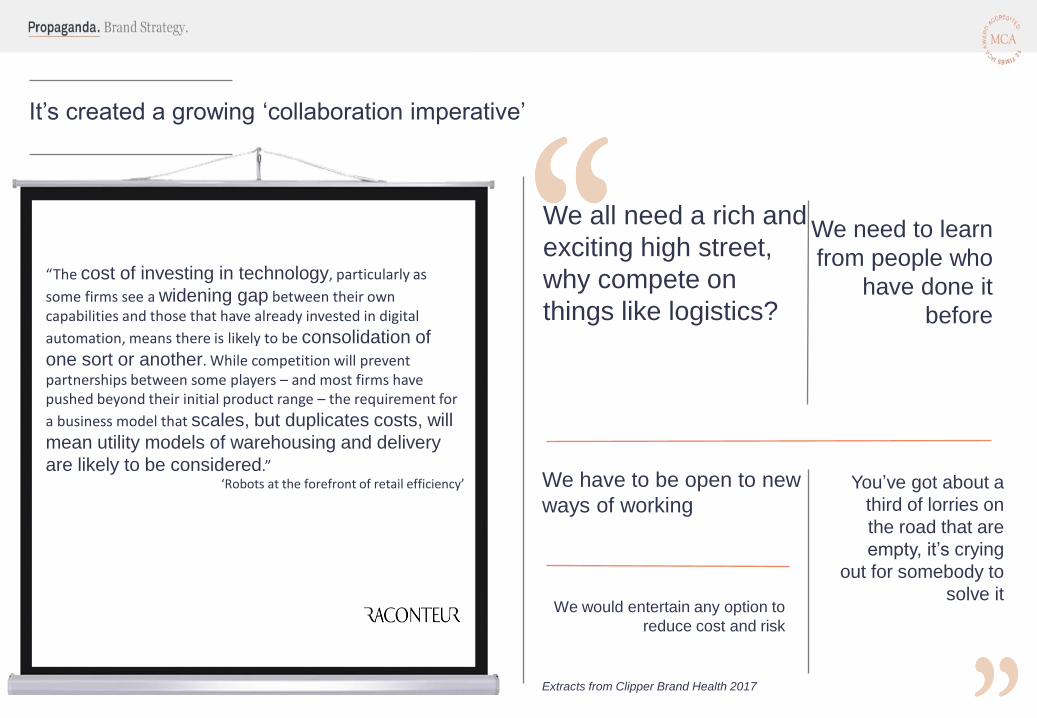

“The cost of investing in technology, particularly as

some firms see a widening gap between their own capabilities and those that have already invested in digital

automation, means there is likely to be consolidation of

one sort or another. While competition will prevent partnerships between some players – and most firms have pushed beyond their initial product range – the requirement for

a business model that scales, but duplicates costs, will

mean utility models of warehousing and delivery

are likely to be considered.” ‘Robots at the forefront of retail efficiency’

It’s created a growing ‘collaboration imperative’

We need to learn

from people who

have done it

before

We all need a rich and

exciting high street,

why compete on

things like logistics?

We have to be open to new

ways of working

We would entertain any option to

reduce cost and risk

You’ve got about a

third of lorries on

the road that are

empty, it’s crying

out for somebody to

solve it

Extracts from Clipper Brand Health 2017

The bigger picture – the need to innovate and upskill workforces

The winners will be those who are able to participate fully in innovation-driven ecosystems by

providing new ideas, business models, products and services, rather than those who can offer

only low-skilled labour or ordinary capital.

Klaus Schwab

‘The Fourth Industrial Revolution’

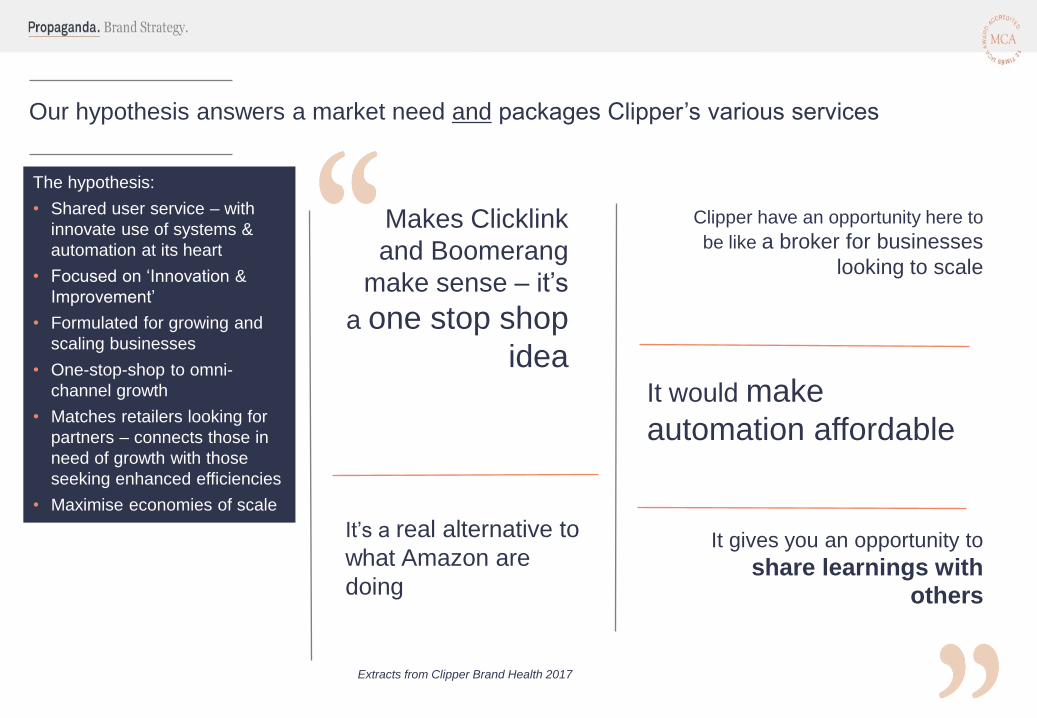

Our hypothesis answers a market need and packages Clipper’s various services

It gives you an opportunity to

share learnings with others

It’s a real alternative to

what Amazon are

doing

Makes Clicklink

and Boomerang

make sense – it’s

a one stop shop

idea

Clipper have an opportunity here to

be like a broker for businesses

looking to scale

It would make

automation affordable

The hypothesis:

• Shared user service – with

innovate use of systems &

automation at its heart

• Focused on ‘Innovation &

Improvement’

• Formulated for growing and

scaling businesses

• One-stop-shop to omni-

channel growth

• Matches retailers looking for

partners – connects those in

need of growth with those

seeking enhanced efficiencies

• Maximise economies of scale

Extracts from Clipper Brand Health 2017

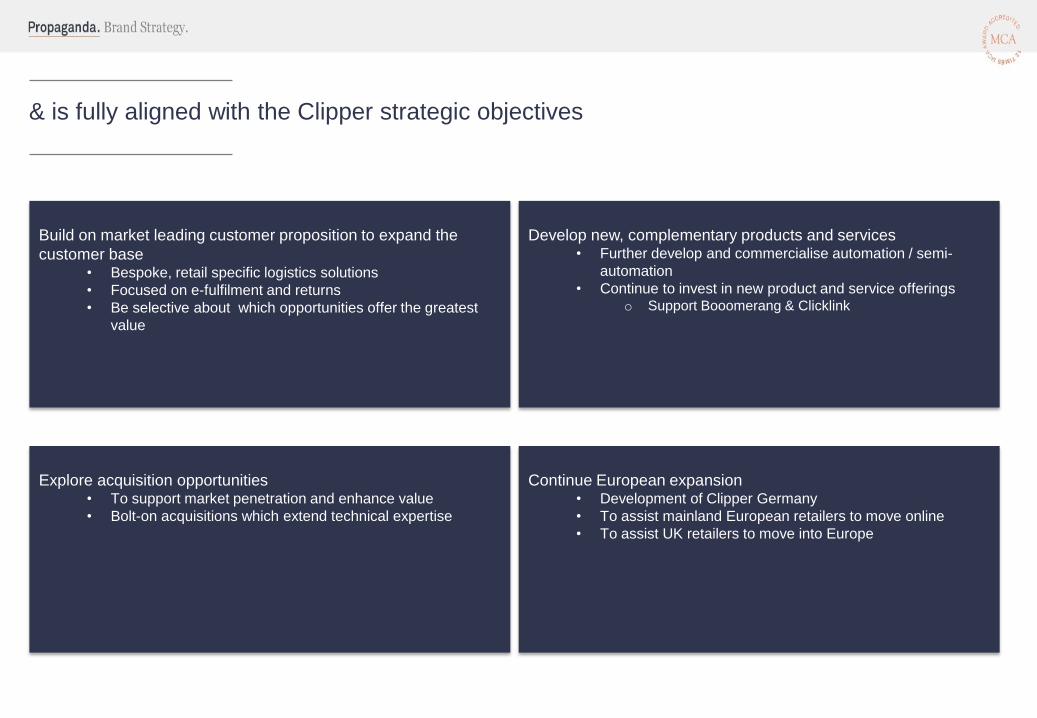

Build on market leading customer proposition to expand the

customer base • Bespoke, retail specific logistics solutions

• Focused on e-fulfilment and returns

• Be selective about which opportunities offer the greatest

value

Develop new, complementary products and services • Further develop and commercialise automation / semi-

automation

• Continue to invest in new product and service offerings o Support Booomerang & Clicklink

Explore acquisition opportunities • To support market penetration and enhance value

• Bolt-on acquisitions which extend technical expertise

Continue European expansion • Development of Clipper Germany

• To assist mainland European retailers to move online

• To assist UK retailers to move into Europe

& is fully aligned with the Clipper strategic objectives

Summary and Q&A 4