A Longitudinal Investigation of Reading - University of Iowa

15

Financial Market Report Serbia In cooperation with AUSSENWIRTSCHAFT AUSTRIA. AUSSENWIRTSCHAFT AUSTRIA

Transcript of A Longitudinal Investigation of Reading - University of Iowa

Financial Market Report

Serbia

In cooperation with AUSSENWIRTSCHAFT AUSTRIA.

A U S S E N W I R T S C H A F T A U S T R I A

3

The Serbian Financial Market

1. The Economic and Political Situation in Serbia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2. Company Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

3. Taxation and Legislation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

4. Arbitration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

5. Subsidies and Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

6. Risk Hedging and Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

7. Payment and Account Services at Raiffeisen banka a.d. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

7. Raiffeisen banka a.d. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

8. Your International Business Specialists at Raiffeisen banka a.d.

and the Global Raiffeisen Network . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Important:

Despite thorough research and the use of reliable sources, we cannot accept responsibility or liability for the completeness or accuracy of this brochure’s contents. The purpose of this brochure is to give you initial, general information to help you develop business relationships in Serbia. The content of this brochure does not constitute any form of advice or offer or invitation to make an offer .

Prepared in cooperation with AUSSENWIRTSCHAFT AUSTRIA at WKÖ (the Austrian FederalEconomic Chamber).

Sources:Raiffeisen Bank International AGWKO: Serbia Country Report, of the AUSSENWIRTSCHAFT AUSTRIABibliography: Skok B., Gotwald A., Jungreithmeir T. (2008), Förderinstrumente für Südosteuropa (Subsidy and Support Instruments for Southeastern Europe). Vienna: Linde Verlag Wien.

Copy deadline: May 2017.

2

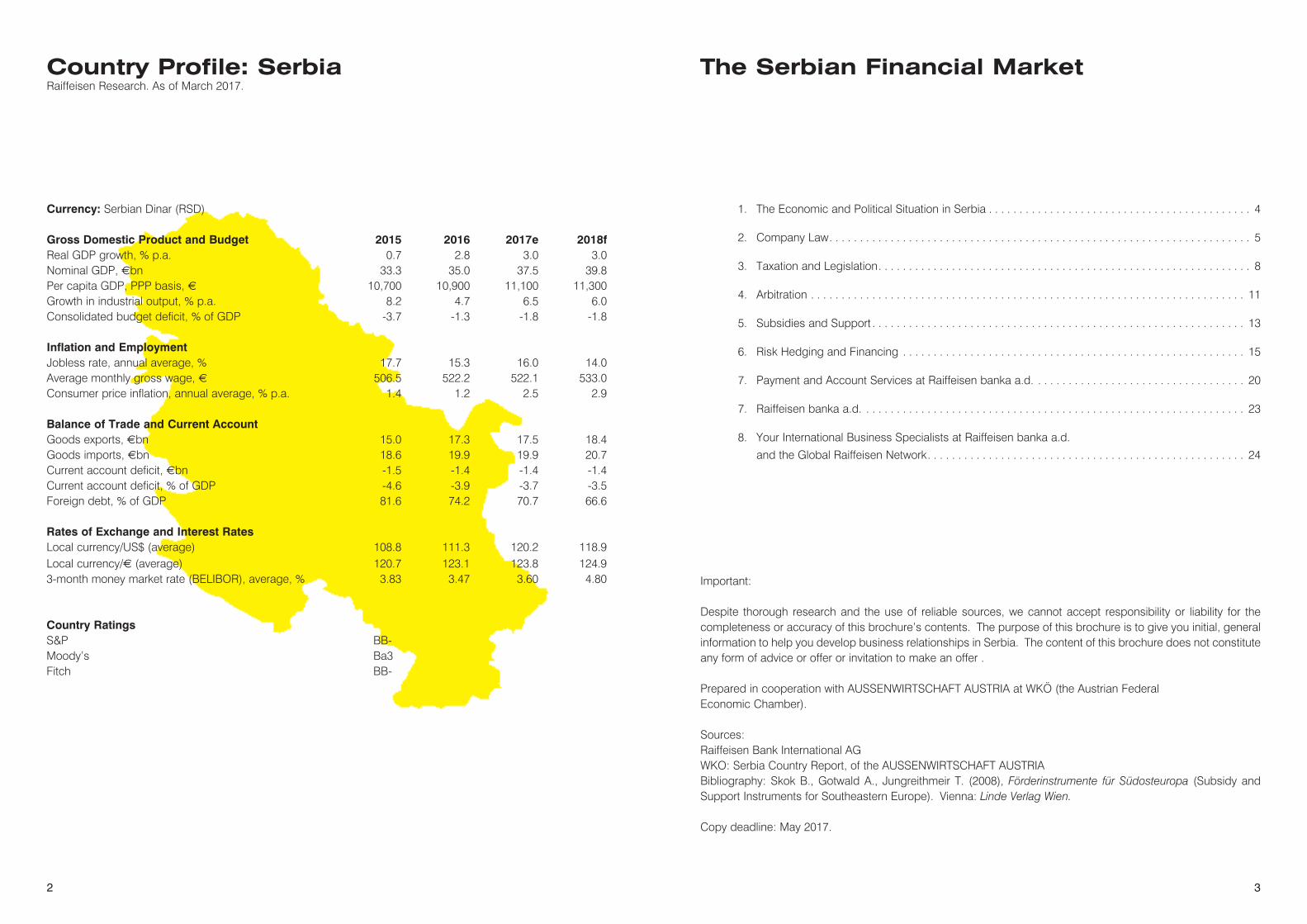

Country Profile: SerbiaRaiffeisen Research. As of March 2017.

Currency: Serbian Dinar (RSD) Gross Domestic Product and Budget 2015 2016 2017e 2018fReal GDP growth, % p.a. 0.7 2.8 3.0 3.0Nominal GDP, €bn 33.3 35.0 37.5 39.8Per capita GDP, PPP basis, € 10,700 10,900 11,100 11,300Growth in industrial output, % p.a. 8.2 4.7 6.5 6.0Consolidated budget deficit, % of GDP -3.7 -1.3 -1.8 -1.8 Inflation and Employment Jobless rate, annual average, % 17.7 15.3 16.0 14.0Average monthly gross wage, € 506.5 522.2 522.1 533.0Consumer price inflation, annual average, % p.a. 1.4 1.2 2.5 2.9 Balance of Trade and Current Account Goods exports, €bn 15.0 17.3 17.5 18.4Goods imports, €bn 18.6 19.9 19.9 20.7Current account deficit, €bn -1.5 -1.4 -1.4 -1.4Current account deficit, % of GDP -4.6 -3.9 -3.7 -3.5Foreign debt, % of GDP 81.6 74.2 70.7 66.6 Rates of Exchange and Interest Rates Local currency/US$ (average) 108.8 111.3 120.2 118.9Local currency/€ (average) 120.7 123.1 123.8 124.93-month money market rate (BELIBOR), average, % 3.83 3.47 3.60 4.80 Country Ratings S&P BB- Moody’s Ba3 Fitch BB-

5

2. Company Law

Limited Liability Companies (d.o.o.) A limited liability company is a company founded by one or several natural persons or legal entities to carry out a specific activity under a single trading name. Members take on liability for the company’s obligations up to the extent of the value of their contributions. The minimum equity of a limited liability company is RSD100.

Joint Stock Company (a.d.) A joint stock company is a company formed by one or more natural persons and/or legal entities to carry on a specific business activity under a single trading name. The company’s share capital is represented by and divided into shares.

The minimum amount of share capital has been increased to RSD3,000,000.

Limited Partnership (k.d.) A limited partnership is a company formed by way of an agreement between two or more natural persons and/or legal entities to carry on a specific business activity under a single trading name.

At least one of the members is liable without limitation (the general partner) for the company’s obligations. At least one person is liable with limitation to the extent of the value of their contributions. The registration fees (not the total costs of forming the company) amount to RSD6640.

Partnership company (o.d.)A partnership company is a company formed by way of an agreement between two or more natural per-sons and/or legal entities to carry on a specific business activity under a single trading name. Unless otherwise agreed with the creditors, the partners are jointly and severally liable for the company’s debts up to the extent of all their assets. Registration (not the total costs of forming the company) costs RSD6640.

Serbia has a GDP per capita equivalent to EUR 4,911, which is approximately 34% of GDP per capita in the Eurozone and corresponds to EUR 10,900 in purchasing power parity. GDP per capita has increased markedly in recent years. In 2016, GDP in Serbia grew by 2.8% compared to the previous year. Economic growth has therefore significantly increased again compared to the previous years. Economic growth was mainly driven by strong growth in exports, increased investments, and also rising public consumption. We expect an increase in GDP in 2017 and 2018 of 3.0% compared to the respective previous years. Exports and investments in infrastructure will encourage economic growth, a further reduction in the unemployment rate and a decrease in current account deficits. Even if interest rates have begun to go up, this correction is still too small to prevent growth in the loan cycle, which has been continuing since 2016. Average infla-tion for 2016 was 1.2% compared to the previous year. This was significantly below the long-term trend. Inflation moved into the target range of 3%+/- 1.5 pp and should remain around the middle of the forecast range in 2017. The unemployment rate in 2016 was 15.3%. We expect the unemployment rate to either stay the same or even increase slightly during 2017 and 2018. The budget deficit for 2016 amounted to 1.3% of GDP - significantly lower than in previous years. For 2017 and 2018, we expect the budget deficit to be slightly higher, but still low compared to the last 10 years. National debt in 2016 was high, at 71.6% of GDP. In view of the above described development in the budget deficit, we expect the national debt ratio to fall slightly in the coming years. Serbia’s current account had a deficit of 3.9% of GDP in 2016. With exports continuing to grow rapidly, we expect the current account deficit to stagnate or even fall in the coming years. Foreign debt amounts to 74.2% of GDP (2016) and has therefore seen a downwards trend in the last few years. The foreign debt ratio could fall further in the next few years. The local currency stabilised against the euro in 2016, but still got weaker. The National Bank has tried to keep the Serbian dinar stable by means of interventions; nevertheless, it is expected to weaken in the coming years. At the end of the year, the base rate was 4.0% and should remain stable during 2017.

Aleksandar Vucic, the head of the Serbian government, was voted as successor to President Tomislav Nikolic in the first round of the presidential elections. The large majority of Serbians therefore chose to con-tinue with reforms and move further towards the EU. However, Vucic is known for his good relationships with Russia and China. Very much so, the 47 year old said on Sunday night in Belgrade. The Prime Minister said that the election result shows the country to still be strong, stable and secure. Serbia is an official EU candi-date and has been in accession negotiations since 2012. EU accession talks were officially commenced in January 2014. The cabinet elected in April 2016 has set the preliminary (and very ambitious) goal to close all chapters by 2020. However, we consider it highly unlikely that all requirements will be fulfilled in the next four years. Because Serbia has fulfilled most of the quantitative goals under the Standby Agreement (SBA), the International Monetary Fund (IMF) has only planned two technical audits for 2017. The main obstacle to completing the deal is the reform/privatisation of state-owned enterprises, which is on the agenda. In addition, the government is reconsidering signing the new programme, which expires in 2018.

1. The Political and Economic

Situation in Serbia

4

76

Representative OfficeForeign persons pursuing an economic activity in banking, finance or insurance and certain international organisations can open a representative office for certain purposes. A representative office is not a legal entity. Activities are carried out on behalf of the founder. Several branches can be formed.

Branch Offices (“ogranak”)Under (new) Company Law (Official Gazette of the Republic of Serbia, No. 36/11), there is a provision for both Serbian and foreign legal persons forming branch offices (subsidiaries, in Serbian “ogranak”). Branch offices are not a legal entity. They can therefore only act on behalf of and for the account of the company’s main office, and are an integral part of the main office. Branch offices are formed following a decision by the governing bodies of the main office and must be entered in the business register.

Business RegisterBy founding the Serbian Business Registers Agency “agencija za privredne register” (APR), the process for forming a company, which can be conducted electronically, was considerably accelerated, and the costs minimised. In addition to the business register, APR runs numerous other public registers, such as a regi-ster of liens. These are run electronically and are publically viewable (www.apr.gove.rs). On the homepage, you can find all application forms, accompanying legislation and information on forming a company.

Investments And Joint VenturesForeign investors have the same rights and obligations with regard to their investments as Serbian inve-stors. National law also applies to companies with foreign participation. There are a few exceptions in law regarding foreign investments.

A foreign investment is understood as the acquisition by foreigners of any property rights which are linked to a business interest in Serbia, and the purchase of common stock and shares in Serbian companies. In general, foreign investors have full legal protection and legal certainty with regard to their investments. These may only be limited where there is a public interest under the law. In this instance however, compen-sation must be guaranteed at the current market value.

If there are more favourable bilateral or international agreements between Serbia and another country, these have precedence over national legal norms. There is an agreement for the support and protection of foreign investors. This provides, firstly, that each contractual party may not treat the investors of the opposite side less favourably than their own investors. It also guarantees both countries free transfers of all payments in a convertible currency for the investors of the other contractual party with regard to investments. In the case of legal disputes related to investments, the International Centre for Investment Disputes is competent.Joint Ventures are understood to be the establishment of a subsidiary company by two legally and econo-mically separate companies. The formation of a joint venture is allowed in Serbia and is a common form of economic collaboration.

Most frequently, collaborations occur between two private companies and between the state and a private company. It should be noted that collaborations with public authorities are subject to additional restrictions and conditions. When forming a joint venture, it is usual to choose the legal form of a company with limited liability or a joint stock company.

At this point, the new Public Private Partnerships and Concessions Act, which was adopted in November 2011, should be mentioned.

8 9

The new Serbian Minister of Finance, Mlađan Dinkić (in office since July 2012) has announced a possible rise in corporate profit tax from 10% to 15%. The Austrian Foreign Trade Centre in Belgrade will be happy to give you information about the current situation.

Unless a double taxation agreement (DTA) specifies otherwise (see below), 20% tax is levied on the ear-nings of foreigners without a residence in Serbia, as well as their dividends and other investment income, company profits, copyright income, interest, capital gains and rental income. Income from shares and divi-dends is not included in the tax base. Taxable persons that invest more than 600 million RSD (c. 6 million EUR) and also employ 100 people for an indefinite period, are exempt from paying corporate profit tax for ten years in proportion to their investment. Companies that invest more than 6 million RSD (c. 60,000 EUR) and employ at least 5 people in certain less-developed regions of the country are exempt from paying cor-porate profit tax for five years. The calculation is proportional to the investment amount.

Value Added Tax/ Vat NumberValue added tax was introduced in Serbia on 1 January 2005. VAT is levied on the supply of goods or ser-vices for payment within the Republic of Serbia, and on imports.

VAT is a general consumption tax that must be paid on all sales of goods and services at each stage in production. The basis of assessment is the price paid by the taxpayer for the supplied goods or services or the value of the imported goods as determined by the customs authorities.

The standard VAT rate is 20%. A reduced VAT rate of 10% is applicable to basic foods, medicines paid for by health insurance, computers, textbooks, municipal services and similar.

VAT must always be paid, but the tax already paid can be deducted from output tax (input tax deduction).

A special taxation regime is in place for small taxpayers (threshold of RSD2,000,000). This regime applies to farmers, travel agencies, works of art and antiques.

Humanitarian organizations, foreign donors and foreign citizens are either completely exempt from paying VAT or get it refunded in full. There is a practical problem for companies that only export, which is that the taxpayer is outside VAT system and has to correct the input tax on stock and fixed assets. The company must achieve a taxable domestic turnover of RSD2,000,000 plus VAT to remain in the system.

Companies established in a Serbian free trade zone can (at least temporarily) receive an exemption from paying VAT on imported goods and may, under certain circumstances, be completely exempted from paying VAT on exports.

3. Taxation and Legislation

For foreign traders there are particularities that must be observed. A foreign trader cannot register directly for VAT. The registration can only occur indirectly via a branch. The reverse charge rule, which passes on the obligation to pay VAT to the service beneficiary, applies. It is essential that the service is documented in order to avoid auditors refusing the input tax deduction.

Reverse Charge SystemThe reverse charge system applies in Serbia, where, when a foreign trader carries out deliveries or other services in Serbia, tax owed is transferred to the domestic service beneficiary. Foreign traders are also entitled to input tax deduction but only under more restricted conditions. From a VAT point of view, we recommend as much as possible carrying out activities in Serbia through a subsidiary company in order to avoid problems with the input tax deduction.

Double Taxation AgreementSince 1 January 2011, the double taxation agreement between Austria and Serbia has applied. It applies to persons who are resident in Austria and/or Serbia. For natural persons, this means the place of habitual residence. For legal entities, it depends on the country in which the management is based. Taxes on pro-perty and income are covered by the agreement. These are mainly income tax, corporation tax and land tax.There are two ways to avoid double taxation. One is the exemption with progression method, and the other is the credit method. It should be noted that in the double taxation agreement Austria applies the exemption method and Serbia the credit method.

Input Tax Rebate/ AccountingVAT must always be paid but the tax already paid can be deducted from output tax (input tax deduction). The input tax deduction can also be claimed for imported goods where import papers are fully provided in the deduction period. Input tax can also be claimed in later periods where the calendar year is not relevant. There is no system of yearly VAT. The tax return can be changed a maximum of twice in five years for the same tax period/ the same reporting period.

The refund occurs within 45 days (15 days for export companies) of the request. In the most heavily taxed regions, such as Belgrade, the refund occurs regularly, while in communities that are economically weaker there can be delays.

The refund of VAT for foreigners is limited to trade fair services. The refund can be requested on the official form until 30 June of the following year. In practice, there are problems with the processing of refunds by

1110

4. Arbitration

Serbia has ratified the Convention on the Recognition and Enforcement of Foreign Arbitral Awards (the New York Convention).

Unlike the judgements of state courts, arbitral awards can be enforced practically worldwide. For a dispute to be settled by a court of arbitration, its jurisdiction must have been agreed upon beforehand in writing. It is therefore advisable to include an arbitration clause in the contract with your foreign counterparty.

The Austrian Federal Economic Chamber offers institutional arbitration as a service through the International Arbitral Centre of the Austrian Federal Economic Chamber.

The arbitration clause of the International Arbitral Centre of the Austrian Federal Economic Chamber reads as follows (versions are also available in the languages that are most important for Austrian exporters):

‘All disputes arising out of this contract or related to its violation, termination or nullity shall be finally settled under the Rules of Arbitration and Conciliation of the International Arbitral Centre of the Austrian Federal Economic Chamber in Vienna (Vienna Rules) by one or more arbitrators appointed in accordance with these Rules.’

Useful agreements to supplement this arbitration clause:

• the number of arbitrators shall be .......................... (one or three); • the applicable law shall be ............................; • the language used during arbitration proceedings shall be ......................................

Detailed information:

Internationales Schiedsgericht der Wirtschaftskammer Österreich International Arbitral Centre of the Austrian Federal Economic Chamber Dr. Manfred Heider; Phone: +43-5-90 900-4398; Fax: +43-5-90 900-216. E-mail: [email protected]; Internet: wko.at/arbitration

The fact that you as an Austrian company are a member of the Federal Economic Chamber can in some circumstances be a cause for concern for a strong foreign counterparty. In this case we recommend that you agree on a different arbitral court, such as the one belonging to the International Chamber of Commerce. This has its headquarters in Paris and is represented in Austria by ICC Austria.

the authorities. The current application form in Serbian for refunding VAT without a permanent establishment in Serbia can be downloaded from the following link: http://www.poreskauprava.gov.rs/sr/pdv/Ref1.htm l.There is a translation available at the Austrian Foreign Trade Centre in Belgrade.

The necessary attachments to the application are:• Original confirmation from the tax authorities in Austria regarding registration as a trader (liable for VAT)• Translation into Serbian of the confirmation• Original supporting documents and copies of invoices for goods or services used in Serbia for which VAT

was calculated• Proof of full payment of the original tax

Accounting is based on the International Accounting Standards with specific modifications. In this way, it is possible to establish exchange rate differences by yearly regulation. It is also possible to have a finan-cial year that differs from the calendar year. Financial statements must be filed by the end of February and returns must be filed by 15 March. The tax return is determined from the financial statement through effective tax reconciliation. Additionally it is necessary to observe size classes for financial statements and tax returns, which are based on the balance sheet total, sales revenues and the number of employees. All entities are classified as small, medium or large companies. However, only medium and large companies are obliged to have audited accounts.

Income Tax An amendment to the ‘Income Tax Law’ was enacted on 14 July 2006 (Official Gazette of the Republic of Serbia, Nos. 24/01, 80/02, 135/04, 62/06, 65/06,31/2009,44/2009,18/2010). Tax is charged at a rate of 10% on income from agriculture and forestry and on self-employed income (July 2006). Income tax on copyright income, income from similar rights and from industrial property rights was reformed in 2005. Income tax is not charged on the following:

• incomes of up to RSD11.604; • termination payments upon retirement; • termination payments upon termination of employment on the grounds of unsuitability on the part of the

employee; • one-off compensation received by a person leaving employment on the grounds of redundancy (surplus

workforce) during restructuring, or preparations for an enterprise’s privatisation.

1312

5. Subsidies and Support

Therefore you have the following options:

• If your company has a strong starting position in contract negotiations or if you and your counterparty are roughly equal, we recommend you use the arbitration clause of the Austrian Federal Economic Chamber.

• If on the other hand your company holds a weaker position, or if your counterparty is of equal strength and will not agree to the Austrian Federal Economic Chamber’s arbitration clause, then we recommend that you agree on a different arbitral court, such as that of the International Chamber of Commerce (ICC).

The arbitration clause of the International Chamber of Commerce (ICC) reads as follows:

‘All disputes arising out of or in connection with the present contract shall be finally settled under the Rules of Arbitration of the International Chamber of Commerce by one or more arbitrators appointed in accor-dance with the said Rules.’ This arbitration clause is also available in other languages.

Detailed information:

ICC Austria, International Chamber of CommerceDr. Maximilian Burger-Scheidlin; Phone: +43-5-90 900-3701; Fax: +43-5-90 900-3703; E-mail: [email protected]; Internet: www.icc-austria.org.

EU cohesion policy / regional policy 2014-2020Initial situation / status quoThe various regions of Europe, especially Central and Southeastern Europe, exhibit large differences in economic and social development. To strike a balance between the regions, the EU has set the following targets as part of its Europe 2020 strategy:

• Creation of jobs• Strengthening companies’ competitive position• Promotion of economic growth and sustainable development• Improvement in EU citizens’ life quality

The cohesion / regional policy is aimed at all regions in the EU in order to create intelligent, sustainable and integrative growth. The cohesion policy is defined for a seven-year period (2014-2020). A budget of EUR 351.8 billion, i.e. almost one third of the entire EU budget, is set aside for achieving the above targets in the timeframe mentioned. Within the scope of this budget, funding is granted in the form of non-repayable grants.

Structure of the funding programmes / from the EU target to the national funding programmeThe individual EU member states use the EU targets set under the Europe 2020 strategy to define their national and regional priorities, from which the individual Operational Programmes (OPs) are derived.The Operational Programmes are structured according to region and topic. Within these programmes “priority axes” are defined, which are subject to guidelines approved by the European Commission. The following topics are priorities for the individual countries: Innovation, research & development, job creation, environmental protection, education, SMEs, transport and regional development.

Dedicated national funding agencies (ministries and investment agencies) are responsible for awarding the grants. While grants can be applied for continuously in framework programmes in Austria, they are mostly awarded in the context of “calls” (tender exercises) in Eastern Europe.

For each priority axis mentioned above, tender exercises are held once or twice a year and are open for one to three months. The main assessment criteria for company grants are company size, location, content and impact of the funding project.

How can your company obtain funding?Clearly defined projects can be submitted during the period when the tender exercise is open. Only complete applications (project description, approvals, budget,...) in the respective national language are accepted. The submitted projects are then evaluated by assessors using a points system based on the guidelines specified/defined in the program. All projects within a “call” take part in a competition. Only those with the highest score are shortlisted for funding commitments.

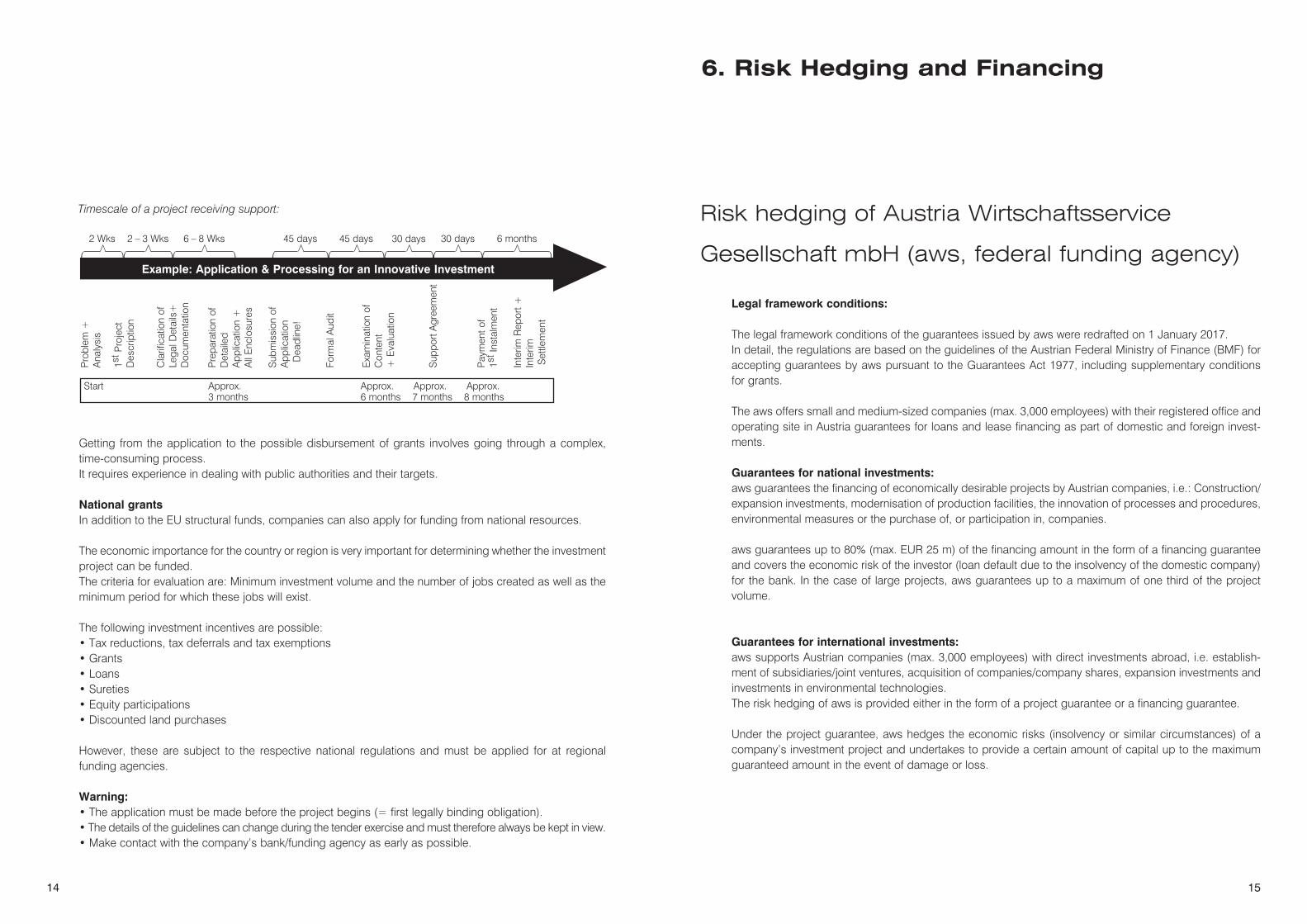

1514

Getting from the application to the possible disbursement of grants involves going through a complex, time-consuming process.It requires experience in dealing with public authorities and their targets.

National grantsIn addition to the EU structural funds, companies can also apply for funding from national resources.

The economic importance for the country or region is very important for determining whether the investment project can be funded.The criteria for evaluation are: Minimum investment volume and the number of jobs created as well as the minimum period for which these jobs will exist.

The following investment incentives are possible:• Tax reductions, tax deferrals and tax exemptions• Grants• Loans• Sureties• Equity participations• Discounted land purchases

However, these are subject to the respective national regulations and must be applied for at regional funding agencies.

Warning:• The application must be made before the project begins (= first legally binding obligation).• The details of the guidelines can change during the tender exercise and must therefore always be kept in view.• Make contact with the company’s bank/funding agency as early as possible.

Pro

blem

+A

naly

sis

1st P

roje

ctD

escr

iptio

n

Cla

rific

atio

n of

Lega

l Det

ails

+D

ocum

enta

tion

Pre

para

tion

ofD

etai

led

App

licat

ion

+A

ll E

nclo

sure

s

Sub

mis

sion

of

App

licat

ion

€ Dea

dlin

e!

Form

al A

udit

Exa

min

atio

n of

Con

tent

+ E

valu

atio

n

Sup

port

Agr

eem

ent

Pay

men

t of

1st I

nsta

lmen

t

Inte

rim R

epor

t +In

terim

Set

tlem

ent

Example: Application & Processing for an Innovative Investment( )

>

2 Wks

( )

>

2 – 3 Wks

( )

>

6 – 8 Wks

( )

>

6 months

( )

>

30 days

( )

>

30 days

( )

>

45 days

( )

>

45 days

Start Approx. Approx. Approx. Approx. 3 months 6 months 7 months 8 months

Timescale of a project receiving support:

6. Risk Hedging and Financing

Risk hedging of Austria Wirtschaftsservice

Gesellschaft mbH (aws, federal funding agency)

Legal framework conditions:

The legal framework conditions of the guarantees issued by aws were redrafted on 1 January 2017.In detail, the regulations are based on the guidelines of the Austrian Federal Ministry of Finance (BMF) for accepting guarantees by aws pursuant to the Guarantees Act 1977, including supplementary conditions for grants.

The aws offers small and medium-sized companies (max. 3,000 employees) with their registered office and operating site in Austria guarantees for loans and lease financing as part of domestic and foreign invest-ments.

Guarantees for national investments:aws guarantees the financing of economically desirable projects by Austrian companies, i.e.: Construction/expansion investments, modernisation of production facilities, the innovation of processes and procedures, environmental measures or the purchase of, or participation in, companies.

aws guarantees up to 80% (max. EUR 25 m) of the financing amount in the form of a financing guarantee and covers the economic risk of the investor (loan default due to the insolvency of the domestic company) for the bank. In the case of large projects, aws guarantees up to a maximum of one third of the project volume.

Guarantees for international investments:aws supports Austrian companies (max. 3,000 employees) with direct investments abroad, i.e. establish-ment of subsidiaries/joint ventures, acquisition of companies/company shares, expansion investments and investments in environmental technologies.The risk hedging of aws is provided either in the form of a project guarantee or a financing guarantee.

Under the project guarantee, aws hedges the economic risks (insolvency or similar circumstances) of a company’s investment project and undertakes to provide a certain amount of capital up to the maximum guaranteed amount in the event of damage or loss.

1716

aws guarantees up to 50% of the loan used (for large projects up to 1/3 of the project volume). The gua-rantee fee is dependent on the ratings result calculated when examining the respective project, as well as the term of the guarantee.

Under the international financing guarantee, aws guarantees the financing of Austrian companies for eco-nomically desirable projects abroad, i.e.: construction/expansion investments, modernisation of production facilities, the innovation of processes and procedures, environmental measures or the purchase of, or participation in, companies.

aws guarantees up to 80% (max. EUR 25 m) of the financing volume and thereby covers the economic risk of the investor for the bank.

Conditions of the aws guarantee:

National guarantees: • Processing fee: 0.25% (one-off) of the assessment basis (max. EUR 30,000)• Guarantee fee: The guarantee fee depends on the ratings result calculated when examining the

respective project as well as the term of the guarantee

International guarantees:• Processing fee: 0.25% (one-off) of the assessment basis (max. EUR 50,000)• Guarantee fee: The guarantee fee depends on the ratings result calculated when examining the

respective project as well as the term of the guarantee.

Austria

Abroad

BANK

OeKB (Oesterreichische Kontrollbank AG)In order to achieve sustainable success in the export business and for investments made abroad, com-panies need good risk management and attractive financing arrangements. With federal export guaran-tees and OeKB refinancing packages, the OeKB offers instruments via the respective house banks that strengthen Austrian companies and their partners in global competition. By processing export guarantees, the OeKB acts as the Export Credit Agency (ECA) of the Republic of Austria.

Export guarantees protect the entrepreneur against payment defaults (for economic or political reasons) related to export transactions. In the case of foreign investments, export guarantees provide protection against political risks.

Federal export guarantees also offer an attractive way to access financing for export and investment acti-vities. Export guarantees can be utilised by all large, medium and small companies whose guaranteed transactions have a positive impact on Austria’s current account balance or are in the national interest.

Companies can learn more about the ideal kinds of guarantee from the OeKB Export Service (www.export-service.at) or from their house bank. OeKB’s export financing process provides the possibility of refinancing exports and equity participations abroad. This export financing process is available as a source of refinan-cing at domestic and foreign commercial banks and is offered to companies via these banks within the scope of their export business and foreign investments.

The prerequisites for this type of financing are• A federal guarantee as required by the Export Funding Act (EFA), or• A guarantee from a credit insurer within the meaning of the EFA• A guarantee from aws, or• A guarantee of an international organisation within the meaning of the EFA.Furthermore, the financing of the underlying supplies/services must bring about a direct or indirect impro-vement in the Austrian current account balance or be in the Austrian national interest.

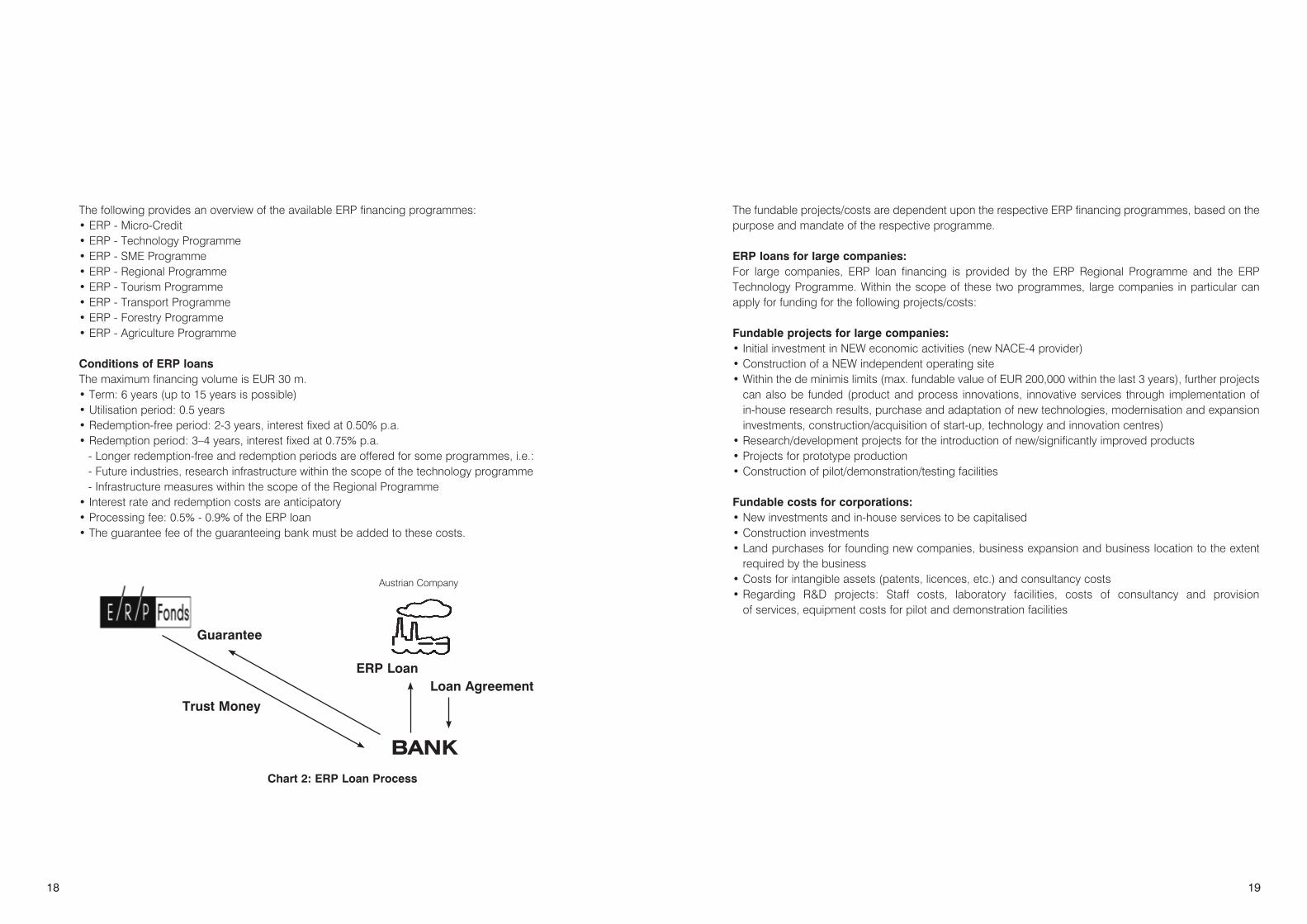

ERP fundThe ERP fund is a fund with its own legal personality, which was attached to aws in 2002. ERP loans are reduced-interest loans with multi-year redemption-free periods and multi-year redemption periods, and are collateralised by a guarantee from aws or a bank.

ERP financing programme Companies are eligible to apply which have their registered office and operating site in Austria and which are active in one of the following sectors: industrial or commercial production, research and development services, transport, processing of agricultural products, and trading companies.

1918

The following provides an overview of the available ERP financing programmes:• ERP - Micro-Credit• ERP - Technology Programme• ERP - SME Programme• ERP - Regional Programme• ERP - Tourism Programme• ERP - Transport Programme• ERP - Forestry Programme• ERP - Agriculture Programme

Conditions of ERP loansThe maximum financing volume is EUR 30 m.• Term: 6 years (up to 15 years is possible)• Utilisation period: 0.5 years• Redemption-free period: 2-3 years, interest fixed at 0.50% p.a.• Redemption period: 3–4 years, interest fixed at 0.75% p.a.

- Longer redemption-free and redemption periods are offered for some programmes, i.e.:- Future industries, research infrastructure within the scope of the technology programme- Infrastructure measures within the scope of the Regional Programme

• Interest rate and redemption costs are anticipatory• Processing fee: 0.5% - 0.9% of the ERP loan• The guarantee fee of the guaranteeing bank must be added to these costs.

Austrian Company

BANK

Guarantee

Trust Money

ERP LoanLoan Agreement

Chart 2: ERP Loan Process

The fundable projects/costs are dependent upon the respective ERP financing programmes, based on the purpose and mandate of the respective programme.

ERP loans for large companies:For large companies, ERP loan financing is provided by the ERP Regional Programme and the ERP Technology Programme. Within the scope of these two programmes, large companies in particular can apply for funding for the following projects/costs:

Fundable projects for large companies:• Initial investment in NEW economic activities (new NACE-4 provider)• Construction of a NEW independent operating site• Within the de minimis limits (max. fundable value of EUR 200,000 within the last 3 years), further projects

can also be funded (product and process innovations, innovative services through implementation of in-house research results, purchase and adaptation of new technologies, modernisation and expansion investments, construction/acquisition of start-up, technology and innovation centres)

• Research/development projects for the introduction of new/significantly improved products• Projects for prototype production• Construction of pilot/demonstration/testing facilities

Fundable costs for corporations:• New investments and in-house services to be capitalised• Construction investments• Land purchases for founding new companies, business expansion and business location to the extent

required by the business• Costs for intangible assets (patents, licences, etc.) and consultancy costs• Regarding R&D projects: Staff costs, laboratory facilities, costs of consultancy and provision

of services, equipment costs for pilot and demonstration facilities

2120

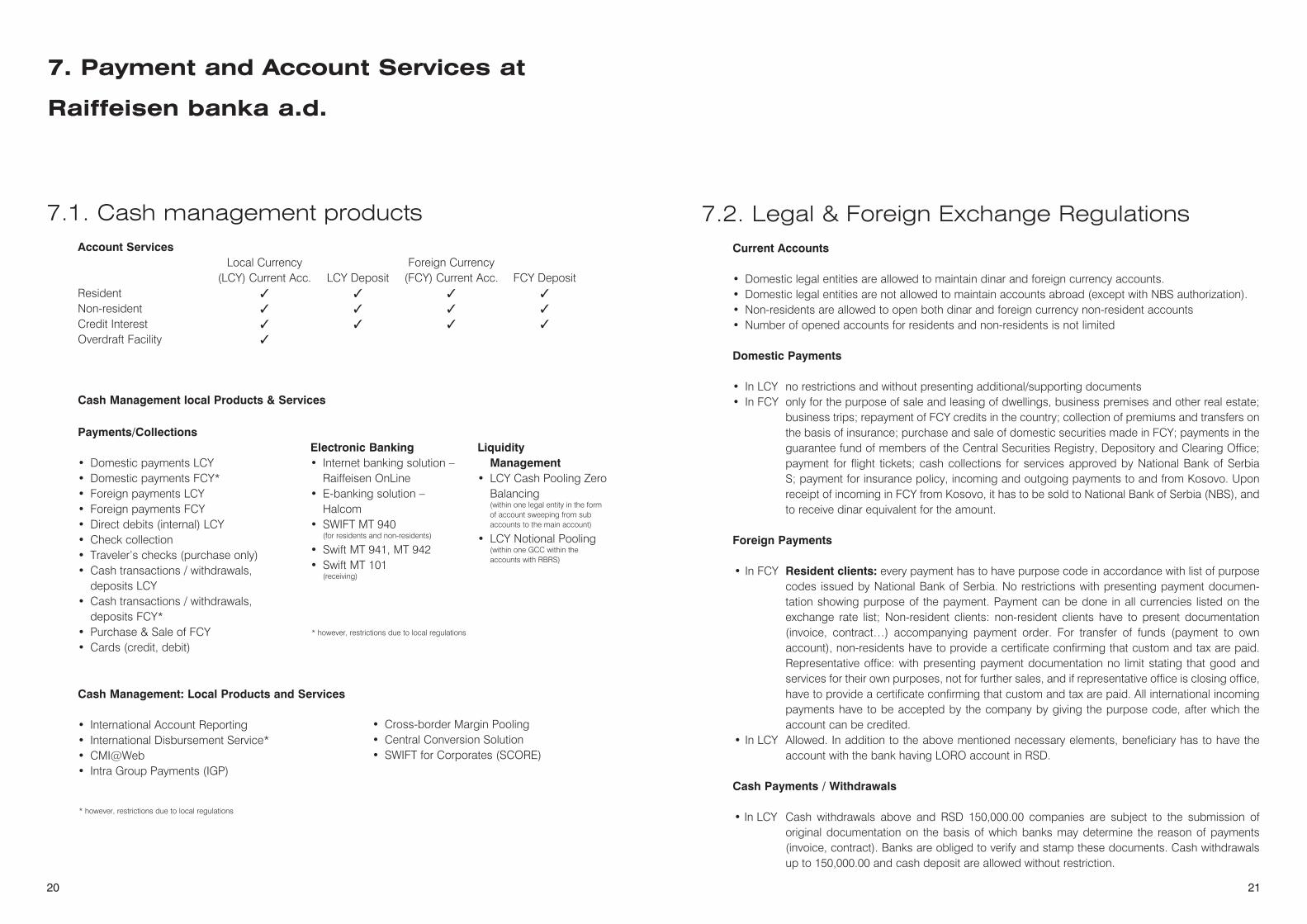

7. Payment and Account Services at

Raiffeisen banka a.d.

7.1. Cash management productsAccount Services Local Currency Foreign Currency (LCY) Current Acc. LCY Deposit (FCY) Current Acc. FCY DepositResident 3 3 3 3

Non-resident 3 3 3 3

Credit Interest 3 3 3 3

Overdraft Facility 3

Cash Management: Local Products and Services

• International Account Reporting• International Disbursement Service*• CMI@Web• Intra Group Payments (IGP)

Payments/Collections

• Domestic payments LCY• Domestic payments FCY*• Foreign payments LCY• Foreign payments FCY• Direct debits (internal) LCY• Check collection• Traveler’s checks (purchase only)• Cash transactions / withdrawals,

deposits LCY• Cash transactions / withdrawals, deposits FCY*• Purchase & Sale of FCY• Cards (credit, debit)

Cash Management local Products & Services

Electronic Banking• Internet banking solution –

Raiffeisen OnLine• E-banking solution –

Halcom• SWIFT MT 940 (for residents and non-residents)

• Swift MT 941, MT 942• Swift MT 101 (receiving)

Liquidity

Management • LCY Cash Pooling Zero

Balancing (within one legal entity in the form

of account sweeping from sub accounts to the main account)

• LCY Notional Pooling (within one GCC within the

accounts with RBRS)

* however, restrictions due to local regulations

* however, restrictions due to local regulations

• Cross-border Margin Pooling• Central Conversion Solution• SWIFT for Corporates (SCORE)

7.2. Legal & Foreign Exchange RegulationsCurrent Accounts • Domestic legal entities are allowed to maintain dinar and foreign currency accounts.• Domestic legal entities are not allowed to maintain accounts abroad (except with NBS authorization).• Non-residents are allowed to open both dinar and foreign currency non-resident accounts• Number of opened accounts for residents and non-residents is not limited Domestic Payments

• In LCY no restrictions and without presenting additional/supporting documents • In FCY only for the purpose of sale and leasing of dwellings, business premises and other real estate;

business trips; repayment of FCY credits in the country; collection of premiums and transfers on the basis of insurance; purchase and sale of domestic securities made in FCY; payments in the guarantee fund of members of the Central Securities Registry, Depository and Clearing Office; payment for flight tickets; cash collections for services approved by National Bank of Serbia S; payment for insurance policy, incoming and outgoing payments to and from Kosovo. Upon receipt of incoming in FCY from Kosovo, it has to be sold to National Bank of Serbia (NBS), and to receive dinar equivalent for the amount.

Foreign Payments

• In FCY Resident clients: every payment has to have purpose code in accordance with list of purpose codes issued by National Bank of Serbia. No restrictions with presenting payment documen-tation showing purpose of the payment. Payment can be done in all currencies listed on the exchange rate list; Non-resident clients: non-resident clients have to present documentation (invoice, contract…) accompanying payment order. For transfer of funds (payment to own account), non-residents have to provide a certificate confirming that custom and tax are paid. Representative office: with presenting payment documentation no limit stating that good and services for their own purposes, not for further sales, and if representative office is closing office, have to provide a certificate confirming that custom and tax are paid. All international incoming payments have to be accepted by the company by giving the purpose code, after which the account can be credited.

• In LCY Allowed. In addition to the above mentioned necessary elements, beneficiary has to have the account with the bank having LORO account in RSD.

Cash Payments / Withdrawals

• In LCY Cash withdrawals above and RSD 150,000.00 companies are subject to the submission of original documentation on the basis of which banks may determine the reason of payments (invoice, contract). Banks are obliged to verify and stamp these documents. Cash withdrawals up to 150,000.00 and cash deposit are allowed without restriction.

2322

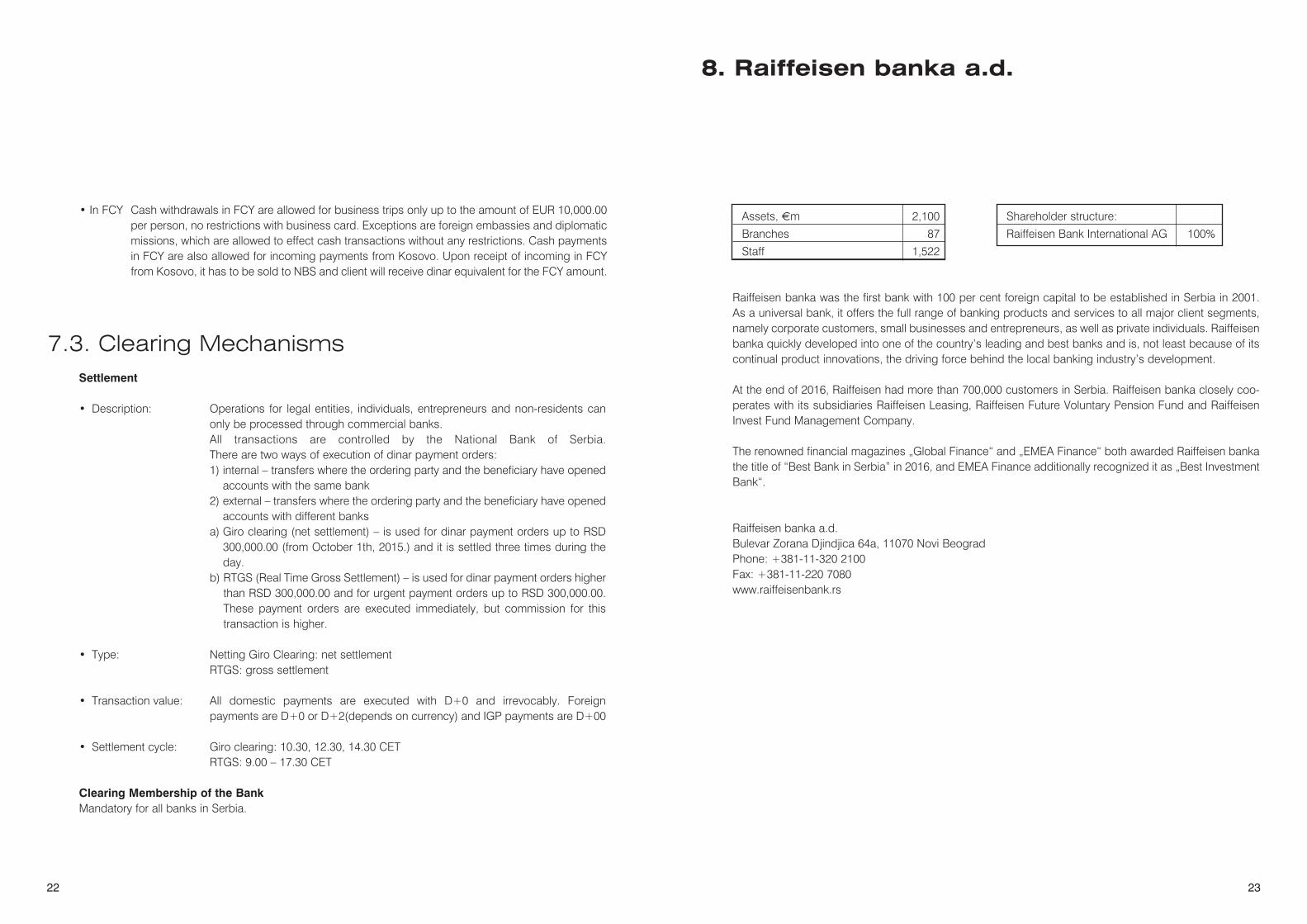

7.3. Clearing MechanismsSettlement • Description: Operations for legal entities, individuals, entrepreneurs and non-residents can

only be processed through commercial banks. All transactions are controlled by the National Bank of Serbia.

There are two ways of execution of dinar payment orders: 1) internal – transfers where the ordering party and the beneficiary have opened

accounts with the same bank 2) external – transfers where the ordering party and the beneficiary have opened

accounts with different banks a) Giro clearing (net settlement) – is used for dinar payment orders up to RSD

300,000.00 (from October 1th, 2015.) and it is settled three times during the day.

b) RTGS (Real Time Gross Settlement) – is used for dinar payment orders higher than RSD 300,000.00 and for urgent payment orders up to RSD 300,000.00. These payment orders are executed immediately, but commission for this transaction is higher.

• Type: Netting Giro Clearing: net settlement RTGS: gross settlement

• Transaction value: All domestic payments are executed with D+0 and irrevocably. Foreign payments are D+0 or D+2(depends on currency) and IGP payments are D+00

• Settlement cycle: Giro clearing: 10.30, 12.30, 14.30 CET RTGS: 9.00 – 17.30 CET

Clearing Membership of the BankMandatory for all banks in Serbia.

• In FCY Cash withdrawals in FCY are allowed for business trips only up to the amount of EUR 10,000.00 per person, no restrictions with business card. Exceptions are foreign embassies and diplomatic missions, which are allowed to effect cash transactions without any restrictions. Cash payments in FCY are also allowed for incoming payments from Kosovo. Upon receipt of incoming in FCY from Kosovo, it has to be sold to NBS and client will receive dinar equivalent for the FCY amount.

Assets, €m 2,100

Branches 87

Staff 1,522

Raiffeisen banka was the first bank with 100 per cent foreign capital to be established in Serbia in 2001. As a universal bank, it offers the full range of banking products and services to all major client segments, namely corporate customers, small businesses and entrepreneurs, as well as private individuals. Raiffeisen banka quickly developed into one of the country’s leading and best banks and is, not least because of its continual product innovations, the driving force behind the local banking industry’s development.

At the end of 2016, Raiffeisen had more than 700,000 customers in Serbia. Raiffeisen banka closely coo-perates with its subsidiaries Raiffeisen Leasing, Raiffeisen Future Voluntary Pension Fund and Raiffeisen Invest Fund Management Company.

The renowned financial magazines „Global Finance“ and „EMEA Finance“ both awarded Raiffeisen banka the title of “Best Bank in Serbia” in 2016, and EMEA Finance additionally recognized it as „Best Investment Bank“.

Raiffeisen banka a.d.Bulevar Zorana Djindjica 64a, 11070 Novi BeogradPhone: +381-11-320 2100 Fax: +381-11-220 7080www.raiffeisenbank.rs

8. Raiffeisen banka a.d.

Shareholder structure:

Raiffeisen Bank International AG 100%

24 25

9. Your International Business Specialists

at Raiffeisen banka a.d. and the Global

Raiffeisen Network

Your specialist at Raiffeisen banka a.d.Sofija [email protected]+381 11 220 7807

Your international business specialists Raiffeisen Bank International AGHerwig [email protected]: +43 / 1 / 717 07 – 1574

Raiffeisen Bank International AGRudolf [email protected]: +43 / 1 / 717 07 – 3537

Raiffeisenlandesbank NÖ-Wien AGNadja [email protected]: +43 / 5 / 1700 – 92426

Irene [email protected]: +43 / 5 / 1700 – 92157

Raiffeisen-Landesbank Steiermark AGFranz [email protected]: +43 / 316 / 4002 – 7110

Beatrix [email protected]: +43 / 316 / 4002 – 7141

Raiffeisenlandesbank Oberösterreich AGHelmut [email protected]: +43 / 732 / 6596 – 23113

Artem [email protected]: +43 / 732 / 6596 – 23161

Raiffeisenverband SalzburgBernhard [email protected]: +43 / 662 / 8886 – 14161

Raiffeisen-Landesbank Tirol AGAndrea [email protected]: +43 / 512 / 5305 – 12230

Raiffeisenlandesbank VorarlbergAlexandra [email protected].: +43 / 5574 / 405 - 528

Raiffeisenlandesbank BurgenlandWilhelm [email protected]: +43 / 2682 / 691 – 605

Raiffeisenlandesbank KärntenMichael Stegmü[email protected]: +43 / 463 / 99300 – 2280

Herbert Schö[email protected]: +43 / 463 / 99300 – 2269

26 27

Notes Notes

Received from: