A little about DG Dunbar Insurance - Crane Rental … little about DG Dunbar Insurance •Have been...

20

1

Transcript of A little about DG Dunbar Insurance - Crane Rental … little about DG Dunbar Insurance •Have been...

1

A little about DG Dunbar Insurance

•Have been insuring the crane, rigging, machinery moving and heavy hauling industry for

over 40 years.

•The brokerage started by creating a crane insurance program

•We have clients from coast to coast throughout Canada and represent over 300

independent crane rental companies

•Our program is designed specifically for mobile cranes, tower cranes, pile drivers and

related operations

•Our home base is in London, ON and we have an office in Calgary and looking to expand to

the East coast later this year

2

Aaron Casey

•Over 13 years in the commercial insurance business

•Spent 10 years on the Underwriting side of the business as a manager for a large insurer

•Last few years with DG Dunbar Insurance

•Handle our Crane Insurance program and cover the entire Canadian territory

Mike Schott

•Over 16 years in the commercial insurance business

•Have been with DG Dunbar the entire time

•Handle our crane insurance program and also cover the Canadian territory

3

This presentation was designed to offer a simple, yet detailed look at some of the most

important components of crane insurance.

Agenda:

1. An overview of what makes your businesses unique – Crane Rental companies have

several unique exposures that need to be addressed

2. Review types of losses we see on our program and where we see the most claims

3. Review a short list of the most common policy exclusions that exist in nearly every

policy that directly impact your businesses if not properly addressed

4. Overview of the main core insurance coverage’s so you know what to look for in your

own policies

4

Crane Insurance IS Specialized.

The first mistake some insurance brokers will take when insuring a crane rental company is

treating them like any other contractor.

•Cranes often carry a very high value that can, for larger cranes, be in the millions. Insurers

and brokers need to have expertise in the field to help value the equipment and properly

insure it using the right policies and the right limits.

•Older equipment generally gets market value replacement, while newer equipment

might have a replacement cost endorsement

•Another unique coverage is Hook Liability – which is the coverage responsible for covering

your customers goods while on the hook.

•Insurance policies will either refer to this coverage as “Hook” or “Installation

Floater” or “Riggers Liability”

•For companies with larger cranes, that are more difficult to find and replace, a physical

damage loss will result in loss of profits since the crane cannot work and a replacement

cannot be found. This is referred to as Business Interruption insurance or also referred to

as downtime insurance. (discussed in another slide)

•Finally, insurance policies are known for their “Fine Print”. They contain several standard

exclusions that, if not properly addressed can severely impact your business. (discussed in

another slide)

5

This leads us to the Hard Truth….

Crane accidents draw large crowds

The accidents are generally very expensive. We don’t see many claims on our program,

however when we do they are often hundreds of thousands of dollars or even millions.

Most insurers do not know cranes, which is also the first reason why crane accidents are so

expensive to settle

If you select the right broker, they can find you the proper market that knows your business

and has experience with crane claims

6

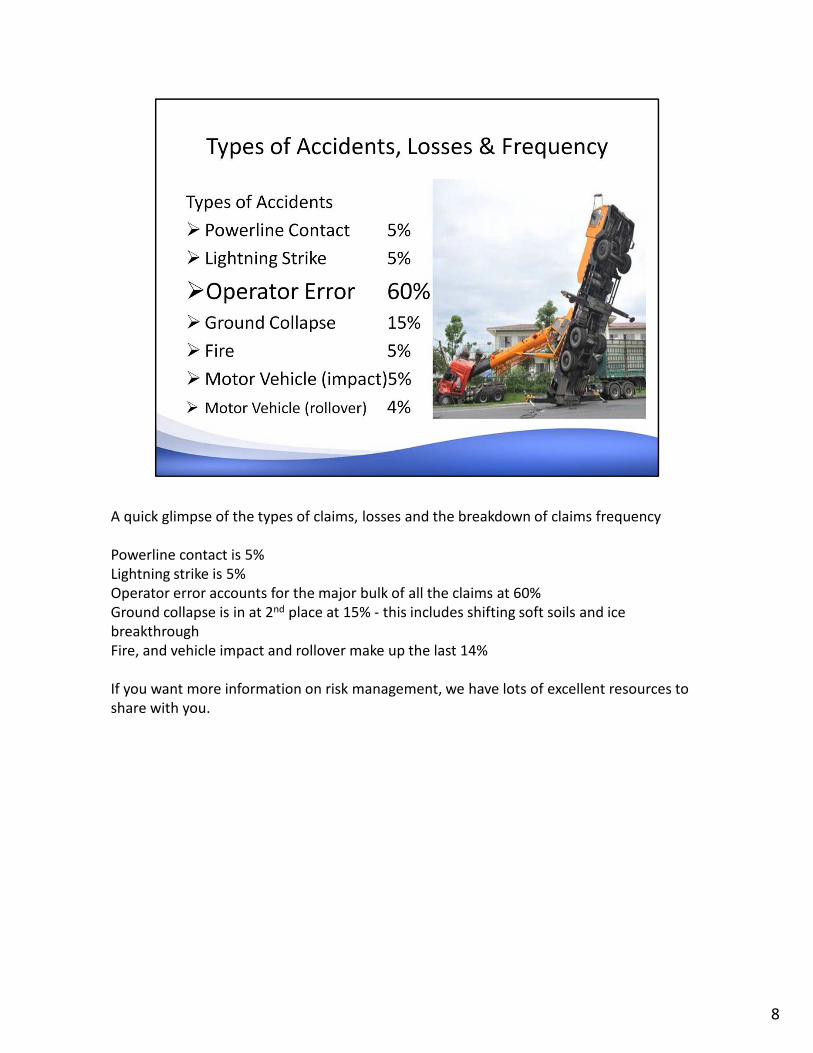

Review of the types of accidents, losses and frequency that we have seen on our program

over the last 20 years.

In those 20 years, we have paid over $15 Million in claims, so the following statistics are an

accurate representation of the crane insurance industry.

7

A quick glimpse of the types of claims, losses and the breakdown of claims frequency

Powerline contact is 5%

Lightning strike is 5%

Operator error accounts for the major bulk of all the claims at 60%

Ground collapse is in at 2nd place at 15% - this includes shifting soft soils and ice

breakthrough

Fire, and vehicle impact and rollover make up the last 14%

If you want more information on risk management, we have lots of excellent resources to

share with you.

8

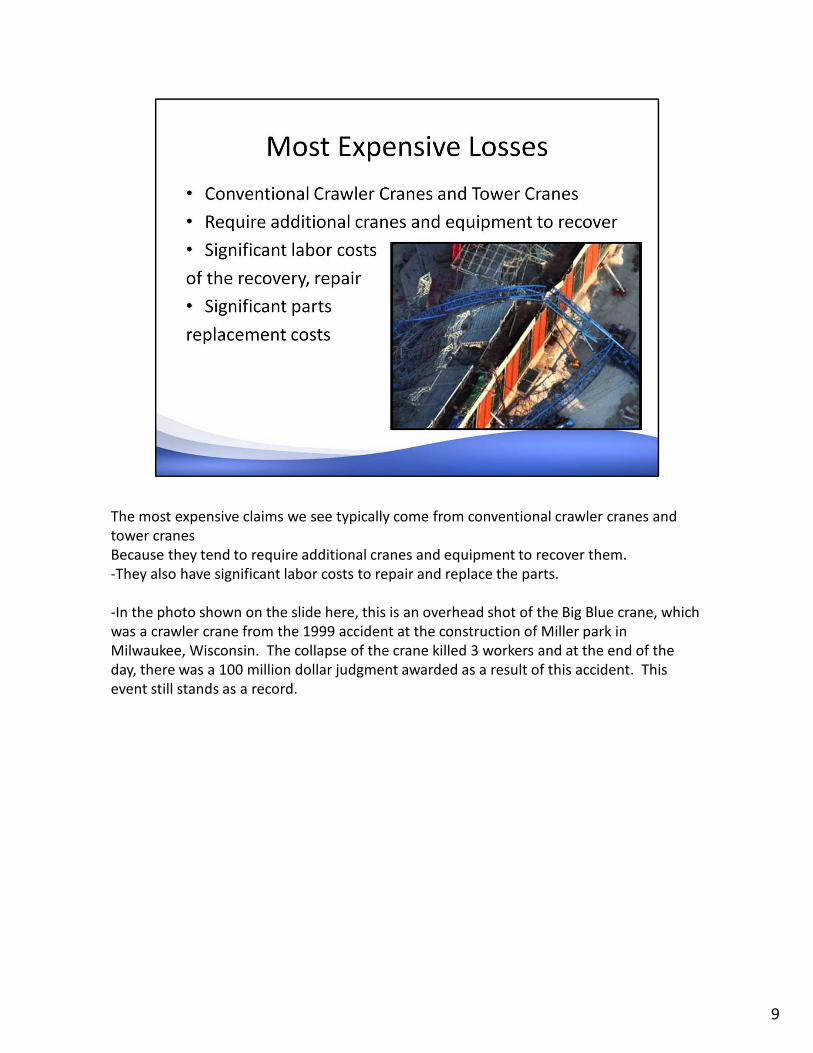

The most expensive claims we see typically come from conventional crawler cranes and

tower cranes

Because they tend to require additional cranes and equipment to recover them.

-They also have significant labor costs to repair and replace the parts.

-In the photo shown on the slide here, this is an overhead shot of the Big Blue crane, which

was a crawler crane from the 1999 accident at the construction of Miller park in

Milwaukee, Wisconsin. The collapse of the crane killed 3 workers and at the end of the

day, there was a 100 million dollar judgment awarded as a result of this accident. This

event still stands as a record.

9

And the Least expensive losses are typically seen from All terrain cranes, hydraulic truck

cranes, RT’s and Boom trucks.

For all the opposite reasons of the tower and crawler cranes, they typically require:

Minimal amounts of recovery equipment

Minimal labor costs

And lower repair and component part costs

10

The simplest way to explain an insurance policy is to think of it as a contract – which is

exactly what it is. A contract between the insurer and you, and it specifically describes how

it will respond to any losses that you may have and ….. And as with any contract, they

contain fine print.

We are going to review a few of the major policy exclusions and fine print that we believe

will significantly impact a crane rental business if not properly addressed.

11

This is what we consider to be the biggest fine print item in the entire business.

When reviewing the list of your equipment, you may notice on the policy summary page

that you have, for example a $2,500 deductible. When you investigate the policy a little

more closely, you may notice in the actual policy an example as shown on the screen.

This is a clause that stipulates that while you do show a $2,500 deductible, if your

equipment is over $300,000 it is actually 5% of the value of the equipment. So you may be

under the impression your million dollar crane carries a $5,000 or $10,000 deductible but

in realty it is $50,000.

Options exist to remove this clause completely so it is in your best interest to ask.

*DG Dunbar Crane program does NOT contain this clause.

12

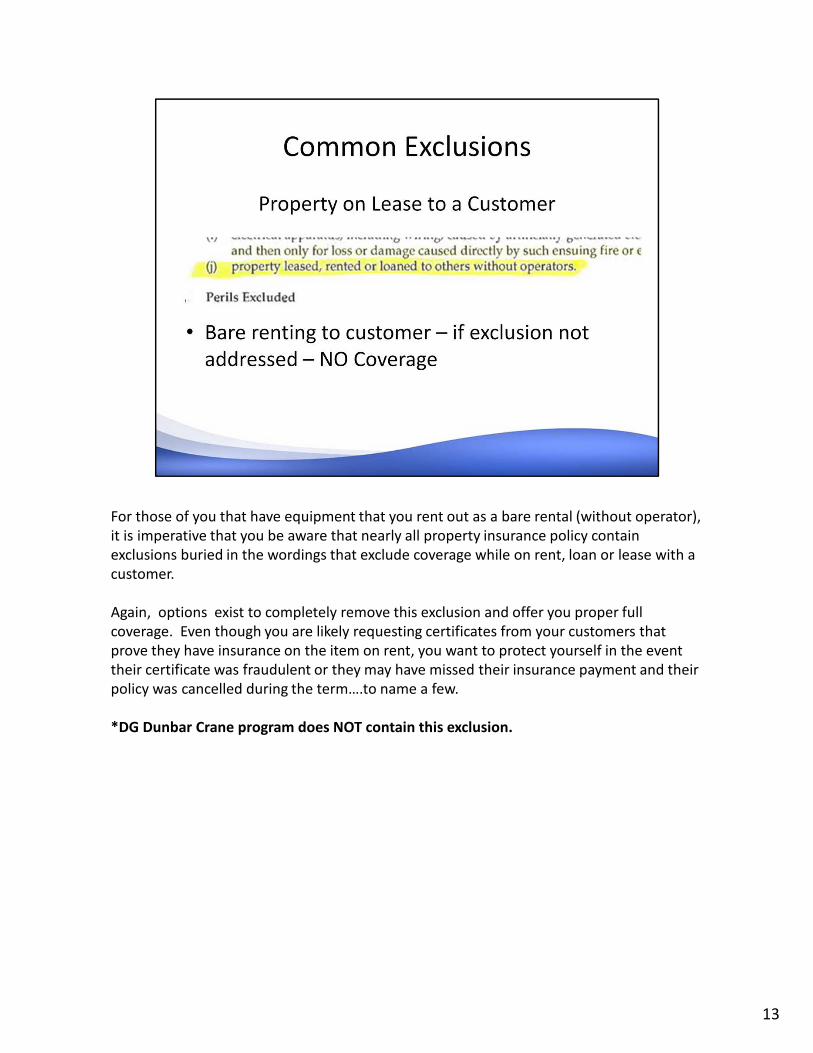

For those of you that have equipment that you rent out as a bare rental (without operator),

it is imperative that you be aware that nearly all property insurance policy contain

exclusions buried in the wordings that exclude coverage while on rent, loan or lease with a

customer.

Again, options exist to completely remove this exclusion and offer you proper full

coverage. Even though you are likely requesting certificates from your customers that

prove they have insurance on the item on rent, you want to protect yourself in the event

their certificate was fraudulent or they may have missed their insurance payment and their

policy was cancelled during the term….to name a few.

*DG Dunbar Crane program does NOT contain this exclusion.

13

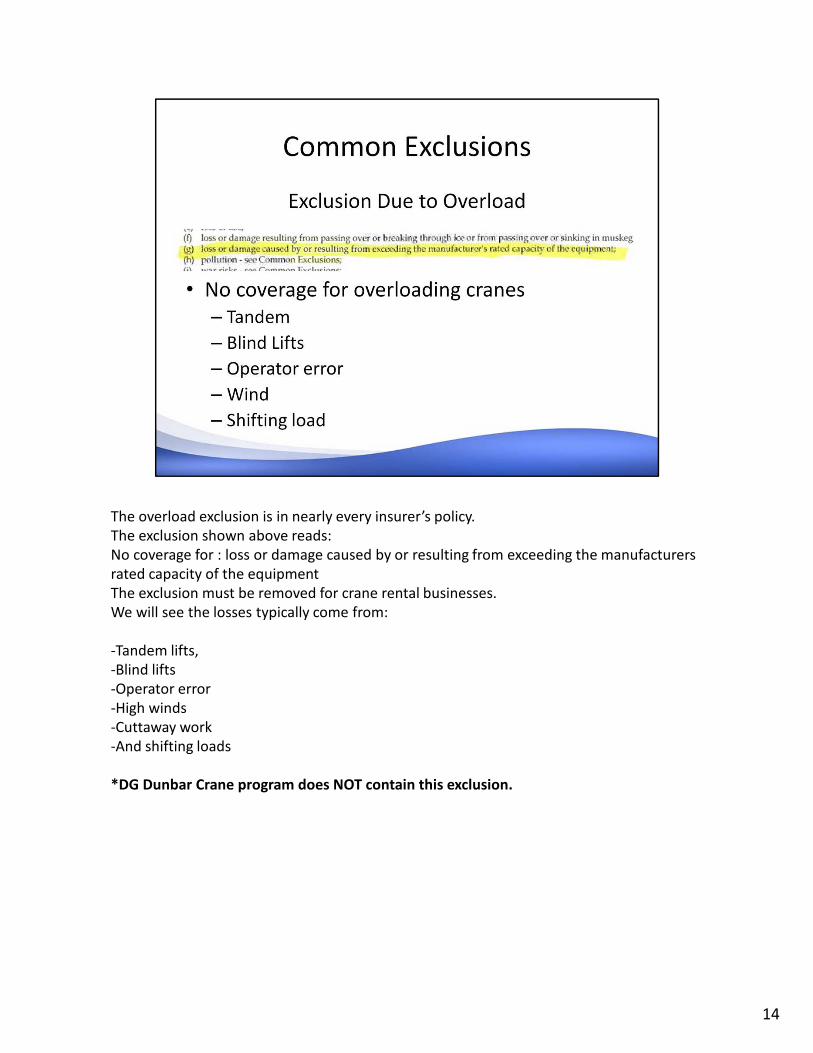

The overload exclusion is in nearly every insurer’s policy.

The exclusion shown above reads:

No coverage for : loss or damage caused by or resulting from exceeding the manufacturers

rated capacity of the equipment

The exclusion must be removed for crane rental businesses.

We will see the losses typically come from:

-Tandem lifts,

-Blind lifts

-Operator error

-High winds

-Cuttaway work

-And shifting loads

*DG Dunbar Crane program does NOT contain this exclusion.

14

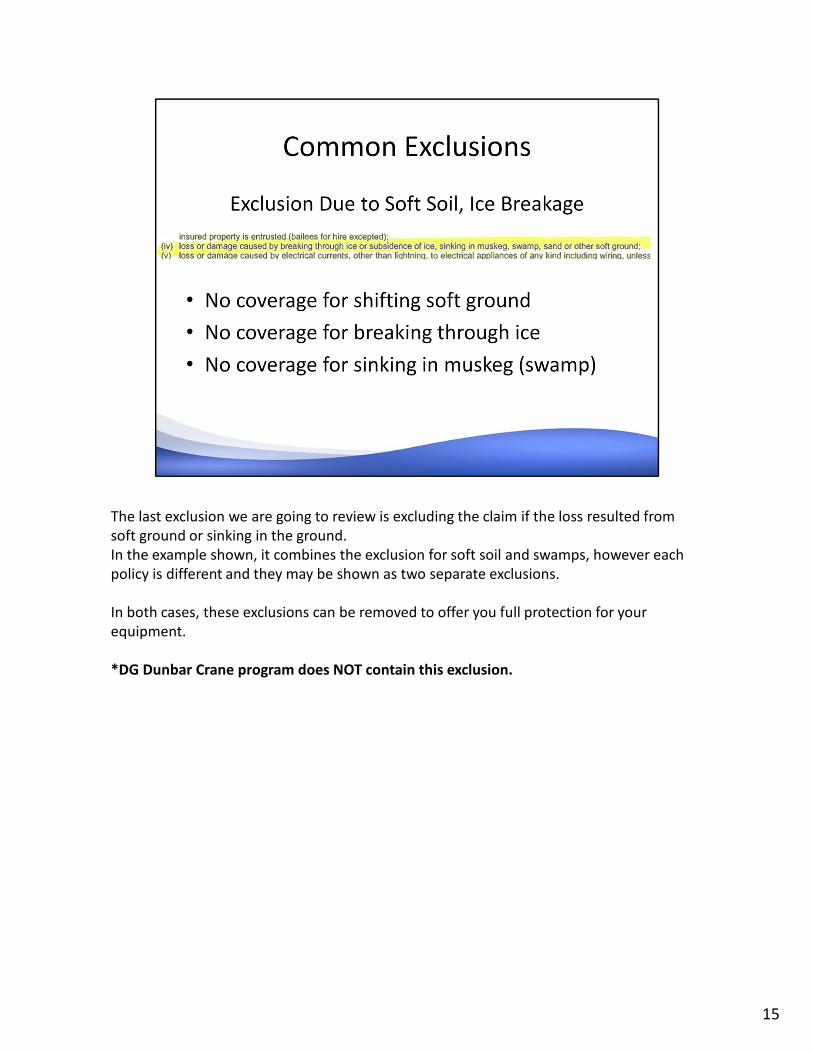

The last exclusion we are going to review is excluding the claim if the loss resulted from

soft ground or sinking in the ground.

In the example shown, it combines the exclusion for soft soil and swamps, however each

policy is different and they may be shown as two separate exclusions.

In both cases, these exclusions can be removed to offer you full protection for your

equipment.

*DG Dunbar Crane program does NOT contain this exclusion.

15

Brief review of what we consider the 4 major lines of coverage, which are:

1. The crane equipment

2. Business interruption insurance

3. Your General liability insurance

4. And Hook Liability

16

For your crane equipment and other contractor’s equipment

-The physical damage of the equipment can be insured under the property policy or under

the automobile policy. We prefer to list all of the equipment and boom trucks physical

damage under the property policy as contractor’s equipment because there are several

added benefits vs. an auto policy which include:

-Access to rental reimbursement – which is a coverage that provides you with

insurance to rent a replacement crane while your damaged crane is being repaired

our replaced so you can continue to work. Traditional limits on an auto policy for

this coverage are up to $5,000 while limits of $50,000 to $500,000 can be

purchased for relatively low costs under a property policy

-You also get access to Business Interruption insurance – which we will address on

the next slide

-Finally, your deductibles can be kept low and reasonable under a property policy,

vs. an automobile policy where they typically use the 5% rule of the original

purchase price

17

Business Interruption Insurance – can also be referred to as Downtime insurance

This can be a extremely valuable, especially for those of you with larger cranes in your fleet

that cannot be easily replaced with a rental.

Business interruption pays for loss of profits while your crane is down due to an insured

event

All policies are different and some may not offer this at all, others may show a small limit

and others show unlimited.

18

We will cap things off by offering a simply comparison of your General Liability versus Hook

Liability.

General Liability protects you and pays for injury and property damage that you are held

liable for to third parties.

Versus hook liability which pays for your customers goods while on hook, should something

happen during the lifting and rigging process. This coverage is for your customers goods

while they are in your care, custody and control.

To illustrate the difference using examples.

At a job site. You rig up a fiberglass pool to lift it over the house and into the customers

backyard. During the lift, right while over the house, the crane overloads and tips, sending

the fiberglass pool and boom right through the roof. In this example:

-You have damaged the pool, in which your Hook Liability will respond for this coverage

- You have also damaged the house, which is going to be paid for under your General

Liability insurance

- and finally, you have also damaged your own equipment – which will of course be paid for

under your property or automobile policy

19