a historical approach of change in management accounting topics

22

Accounting and Management Information Systems Vol. 10, No. 3, pp. 375–396, 2011 A HISTORICAL APPROACH OF CHANGE IN MANAGEMENT ACCOUNTING TOPICS PUBLISHED IN ROMANIA Mădălina DUMITRU 1 , Daniela Artemisa CALU and Cătălina GORGAN The Bucharest Academy of Economic Studies, Romania Adriana CALU University of Bucharest, Romania ABSTRACT The change in management accounting is a topical issue in international research in management accounting. We analysed the change in the management accounting from an international perspective. We also want to see which the situation in Romania is. In order to analyse it, we studied the articles published in management accounting in Romania since 1908 in top journals. We considered four time ranges established on historical and academic changes. In the final section of the paper we presented a few directions to be considered for the future research in management accounting in Romania. The conclusion was that from 1990 until 2004 the articles presented modern cost calculation methods and the trends identified in other countries. After 2005 the research topics in the Romanian journals were traditional as compared with the research topics in MAR. Management accounting, change, economic journals, evolution, history INTRODUCTION One way to study the nature of change is exploring the stability and continuity of the inherent continuous processes of life. Veblen was the first to build a parallel with biology, emphasizing the pass of the relevant information in time (Veblen, 1898, 1914). The same parallel was used by Hodgson (1993) and Calu (2005) in their studies. Stability and change are not independent: even though the biggest part of life 1 Correspondence address: Mădălina Dumitru, Faculty of Accounting and Management Information Systems, The Bucharest Academy of Economic Studies, Piaţa Romană nr. 6, Bucharest, Romania, Tel. +40 21.319.19.00, E-mail. [email protected]

Transcript of a historical approach of change in management accounting topics

Accounting and Management Information SystemsVol. 10, No. 3, pp. 375–396, 2011

A HISTORICAL APPROACH OF CHANGEIN MANAGEMENT ACCOUNTING TOPICS

PUBLISHED IN ROMANIA

Mădălina DUMITRU1, Daniela Artemisa CALU and Cătălina GORGANThe Bucharest Academy of Economic Studies, Romania

Adriana CALUUniversity of Bucharest, Romania

ABSTRACT

The change in management accounting is a topical issue in internationalresearch in management accounting. We analysed the change in themanagement accounting from an international perspective. We also wantto see which the situation in Romania is. In order to analyse it, we studiedthe articles published in management accounting in Romania since 1908in top journals. We considered four time ranges established on historicaland academic changes. In the final section of the paper we presented afew directions to be considered for the future research in managementaccounting in Romania. The conclusion was that from 1990 until 2004 thearticles presented modern cost calculation methods and the trendsidentified in other countries. After 2005 the research topics in theRomanian journals were traditional as compared with the research topicsin MAR.

Management accounting, change, economic journals, evolution, history

INTRODUCTION

One way to study the nature of change is exploring the stability and continuity of theinherent continuous processes of life. Veblen was the first to build a parallel withbiology, emphasizing the pass of the relevant information in time (Veblen, 1898,1914). The same parallel was used by Hodgson (1993) and Calu (2005) in theirstudies. Stability and change are not independent: even though the biggest part of life

1 Correspondence address: Mădălina Dumitru, Faculty of Accounting and Management InformationSystems, The Bucharest Academy of Economic Studies, Piaţa Romană nr. 6, Bucharest, Romania,Tel. +40 21.319.19.00, E-mail. [email protected]

Accounting and Management Information Systems

Vol. 10, No. 3376

is stable, people are characterized by a curiosity searching for alternatives to thepresent situation. So, there is always potential for change. The change in this area is acontinuous process, of interest in the international research (Scapens, 2006). Therecent social, economical and juridical changes forced the appearance of innovationsin the management accounting. These changes sent the old theories into the shadow,questioning their opportunity, but also the capacity of the new ones to succeed indifficult moments. The analysis of the change in management accounting supposes theanalysis of the way in which a theory is chosen instead of another.

We ask ourselves which factors are determining the change in the managementaccounting of the entities in the public and private area, at international level, butespecially in Romania, where taxes frequently prevent the decision making persons tofocus on other aspects of the entity they work in. Even more, in Romania theapplication of the management accounting was poorly understood in 1990 (as beingoptional), which stopped its progress.

The social and economical environment, including culture, have a collateral impact inthe change appearance in the financial accounting, the immediate impact beingmanaged by the financing system of the firms, to which the political factor is added.By observing in time the political-economical-accounting correlation in Romania, wecan distinguish the following general ideas: the enforcement of socialism hasgenerated the incitement of an accounting which uses adequate mechanisms, and theglobalization is currently generating the aggregation of standards regarding theconvergence, concluded between IASB and FASB (Baker & Barbu, 2007). In themanagement accounting, the elements which determine the change are represented byexternal factors (such as, normalized factors in the case of Romania, in the nineties)but mostly by the internal factors – the culture of the firm, the management, the sizeof the firm, the activity area, the form of ownership of the capital etc. (Burns &Scapens, 2000).

“We live in a changing world!” But do we live in a changing country? At least fromthe point of view of the management accounting. Let’s see an example. A studypublished in 2010 (Jinga et al., 2010) showed that as far as the cost methods employedby surveyed managers, 20.51% apply the global absorption method, 25.64% apply thejob costing, 7.69% apply direct-costing, 12.82% use ABC costing, 5.13% use target-costing and 17.95% do not know the name of the method or they do not use anymethod for cost computation.

However, global absorption and job costing methods (the two most used costingmethods in Romania according to the previous study in 2009) were the ones usedmore than thirty years ago. That is, before the Relevance lost of the managementaccounting.

Nowadays, the continuous change is a constant, the organizational environment beingconstrained to align to the new trends and technologies, and even to a whole

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 377

redefining as an organization. In order to survive, the entities must change, mustreinvent their operation of dependence towards the movements and trends of themarket. For a considerable period of time, the management was regarded as true art,an acquired talent through the practice of attempts and errors. A variety of individualtechniques, often based on creativity, human reasoning, intuition and experience wereused for solving problems of the same type and this against the quantitative methodsand the scientific approaches. The complexity of businesses and their activityenvironment has increased considerably in the last decades (Quattrone & Hopper,2001).

The international researchers admitted the need for a change in managementaccounting. In this article we try to assess the situation in Romania. In order to do this,we organize the rest of this research paper as it follows: We analyze the change in the management accounting from the international

perspective; We analyze the change in the management accounting in Romania from the

point of view of the research works published; We analyze the change in the management accounting in a future perspective.

1. THE ANALYSIS OF CHANGE IN THE MANAGEMENT ACCOUNTING– THE INTERNATIONAL PERSPECTIVE

Management accounting change in organizations has to be seen as an evolutionary,path dependent process in which existing ways of thinking (institutions), circuits ofpower and trust in accountants can all have an impact on the way in which the actorswithin the organization respond to external institutional and economic pressures. It isthis complex process of inter-related influences which shapes management accountingpractices and explains the diversity we see in the practices of individual companies.Understanding management accounting change requires an understanding of variousorganisational and historical contingencies (Scapens & Roberts, 1993). In the lastthirty years there has been a change in the management accounting research topics:from explaining the diversity of practices in a population, to making sense of thepractices in individual companies. In management accounting research the 1970s wasan era of economic oriented mathematical models. Going into the 1980s, managementaccounting researchers began to recognise that there was a gap between theory andpractice, and that research to describe practice was urgently needed. Into the 1990s avariety of theories and a number of different methodological approaches started to beused to study management accounting practices. This change is reflected in the shift inthe research methods – from quantitative survey work to qualitative case studies(Scapens, 2006). But the challenge for current (and future) work is to use thetheoretical perspectives which the researchers have developed to provide insights thatare relevant and helpful for practitioners. This is the case especially when academicworks theorise issues closer to managers’ daily lives such as accounting change (e.g.Burns & Scapens, 2000), and accounting in inter-organizational relationship (e.g.Mouritsen & Thrane, 2006).

Accounting and Management Information Systems

Vol. 10, No. 3378

The success of the changes in the accounting system depends on the manner in whichthe behavioural and organizational implications are managed. The appropriateimplementation of these changes is less successful if they are seen as simple technicalinnovation. Most of the studies are focused especially on the users’ perceptions(managers), while the perceptions of information providers were often ignored (Pierce& O’Dea, 2003).

The recent financial crisis and corporative scandals without precedent, the markets’globalization and the competitiveness without precedent, the continuous change of thenational and international regulations together with the opportunities offered by theinformational advanced technologies have forced the appearance of innovations in themanagement accounting. In the specialized literature, we can find manyunderstandings of the term “innovation” (Alter, 2000; Rogers, 1995; Moisdon, 1997).This problem was studied also in the past by the specialty authors for the entities fromthe public sector (Lapsley & Wright, 2004; ter Bogt & van Helden, 2000) and theprivate sector (Albu & Albu, 2008; Alcouffe, 2002; Alcouffe et al., 2003). A relevantfeature is that when a product which solves a practical problem with a theoreticalinterest is obtained and that product works, that means we have constructed a theoryin the management accounting (Malmi et al., 2004). When it comes to innovations,the following have to be described: the theoretical framework of the research, themethodology used, the causes of implementing the innovation, the elements whichhave influenced the implementation and further on the process of implementation fordifferent innovations will be analyzed by comparison, the degree of spreading forthese innovations in Romania will be discussed, the results obtained will besynthesized and proposals will be interpreted and defined for running the innovationsin the management accounting.

After the seventies, the research in the international management accounting has beencharacterized through an obvious disciplinary opening (Bollecker & Azan, 2009). It isknown that the theoretical borrowings are meant to diversify the analysis and enlargethe research. From this point of view, Rojot (2005) was highlighting that in the currentstatus of the management sciences, the capacity of conservation of the plurality ofapproaches must be supported, in an independent manner from the disciplinaryfrontier and to be chosen depending on the needs. A researcher has great chances toinnovate, by moving away from the traditional cores of its discipline, in order toadvance towards the frontier areas, because the progress appears in a greater degree atthe meeting point of the disciplines (Dogan & Pahre, 1991). By studying theinternational specialized literature, we can see that the articles are influenced more bythe management sciences (43.39% from citations) than by sociology (33.96%).

The management accounting system, as a way of organizational control being at thedisposal of managers, is by its nature dependent of the organization (Bouquin, 2004).By analyzing the specialized literature, we have identified features of the entities fromthe private sector which operate in production, services, distribution, constructions,agriculture (Băviţă et al., 2008; Maurel, 2008) etc. In the last years, with the advent of

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 379

the philosophy New Public Management, the research of the entities from the publicsector grew considerably. Concerning the public sector, in the specialized literature,we have identified organizational features for education, health, public administrationetc. (Nor-Aziah & Scapens, 2007; Brignall & Modell, 2000; Lapsley & Pllot, 2000).As well, we may identify the features of those who activate as freelancers (notary –Cappellatti & Kouthra, 2008, individual offices of accounting etc.).

Nowadays, the accounting activity is automated. The main issues of the accountingsystem from the point of view of the management are not technical or structural butrefer to the need of an efficient management accounting from the management’s pointof view. The IT system is at the basis of this process, supplying the information.

Caglio (2003) was stating that usually the external factors are significant for thosewho work in the domain of management accounting. Other studies cannot providesuch an assurance and state that the impact is collateral, through control (Scapens &Jazayeri, 2003; Granlund & Malmi, 2002). As influences of the informationaltechnologies upon the management accounting, we mention the following: the joint ofthe management accounting systems to strategy and action (Boitier, 2007); thetransition from the management accounting system based on numbers generated byaccounting to a system based on nonfinancial, operational numbers (Dechow &Mouritsen, 2005); the remodelling of the mission of the management accountants,which focus mostly on analytical duties (Davis & Albright, 2000); the remodelling ofthe knowledge which the management accountants must acquire (Azan, 2009); theincrease of the flexibility of the information processing, in this way integrating theaccounting information. In the last three decades the role of the managementaccountant was to improve the competitiveness and the profitability of the firmthrough a speech of logical analysis and a rational decision-taking process. Still, themanner in which the speech is designed has been modified through time – from thepresentation of the relevant information in the 1980’s, to the working with themanagers for finding the information needed in the 1990’s, to disciplining theorganization through the measurement systems of performance in 2000 (Balvinsdottiret al., 2009).

2. THE ANALYSIS OF THE RESEARCH IN MANAGEMENTACCOUNTING IN ROMANIA

Many studies have chosen to investigate the role of academic journals in thedissemination of accounting knowledge because they have proven to be the primarymeans for the diffusion of research knowledge in the social sciences (Nederhof & vanRaan, 1993; Gray et al., 2002, quoted by van Campenhout & van Caneghem, 2010).Even though Schneider (1995) argues that it is not only the publication of a piece ofresearch that matters, but also its ability to boost further research, current evaluationmethods still mainly focus on the former.

For individuals, publications are crucial because their number and quality aregenerally the main criteria for hiring, tenure and promotion decisions (Brinn et al.,

Accounting and Management Information Systems

Vol. 10, No. 3380

1996; Mathieu & McConomy, 2003), even in institutions which have little interest inresearch (Hopwood, 2008). For universities, recognition as a research-intensiveinstitution creates a favourable image that may attract the best postgraduate studentsand provide financial resources, especially since several governments have undertakenresearch assessment exercises to guide the allocation of public funds (Raffournier &Schatt, 2010).

In Romania, the term of quality ratio was introduced to include in the universitiesfinancing methodology a stimulating and corrective component. The National Councilof Research in Higher Education (ro. Consiliul Naţional al Cercetării Ştiinţifice dinInvăţământul Superior - CNCSIS) computes IC6 since 2006, using the data from 2005(previously, IC8 was computed). This quality ratio, involved in the assessment of theperformances level in the university scientific research, has a complex structure and adistinct computation formula as to other quality ratios. It allows the budgetaryallocations covering the basic needs of the universities in students’ preparation (wagesand materials) to be correlated with the way in which they are satisfied, both fromfunds allocated from the state and from other revenues (http://www.cncsis.ro/Public/cat/25/Prezentare.html).

The criteria imposed on the universities by this quality ratio have as effect requestsregarding the research results of the academics. The relevance and visibility of theresults of the scientific research activities is measured according to: Articles, proceedings paper, review published in ISI indexed journals;

b) Scientific papers published in foreign journals in the main journals stream,indexed in international databases; c) Scientific papers published in thevolumes of the international conferences ISI indexed and/or the onesorganised by international professional bodies;

Articles published in journals recognised at a national level, by CNCSIS – Band B+ categories;

Books published by national printing houses recognised by CNCSIS orprestigious international printing houses (on paper or electronic).

Raffournier and Schaff (2010) study the content of 18 major academic journals inaccountingi over five years (2000–2004) and the set of papers presented at the EAAcongress in 2003, 2004 and 2005. We notice in their study that no paper of aRomanian author appears in any of the journals and only 2 papers are presented atEAA congresses. However, these papers are not part of the evaluation process inRomania. Thus, we consider that the researches of the Romanian authors are mainlypublished in Romanian journals. The result is convergent with the one of Popa et al.(2009).

2.1. Research methodology

The research methodology used was of a qualitative type. We made a historicalanalysis of the articles presented in the top journals since 1908, identifying significanttime ranges.

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 381

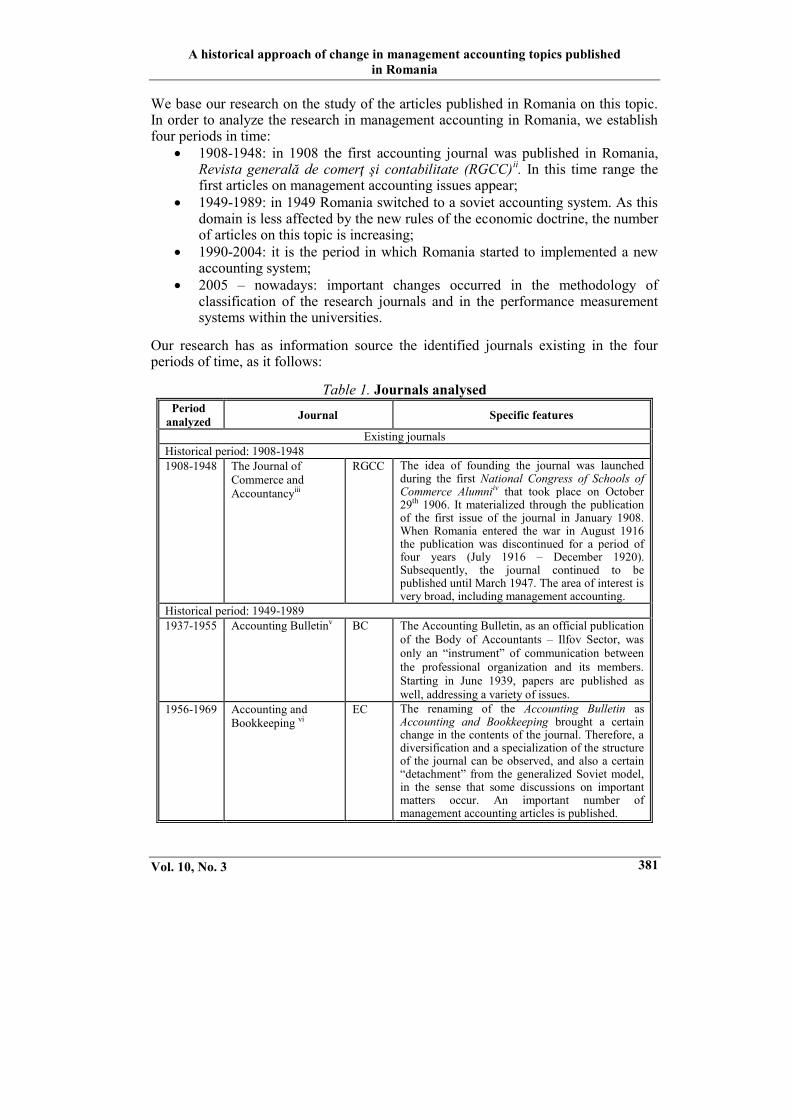

We base our research on the study of the articles published in Romania on this topic.In order to analyze the research in management accounting in Romania, we establishfour periods in time: 1908-1948: in 1908 the first accounting journal was published in Romania,

Revista generală de comerţ şi contabilitate (RGCC)ii. In this time range thefirst articles on management accounting issues appear;

1949-1989: in 1949 Romania switched to a soviet accounting system. As thisdomain is less affected by the new rules of the economic doctrine, the numberof articles on this topic is increasing;

1990-2004: it is the period in which Romania started to implemented a newaccounting system;

2005 – nowadays: important changes occurred in the methodology ofclassification of the research journals and in the performance measurementsystems within the universities.

Our research has as information source the identified journals existing in the fourperiods of time, as it follows:

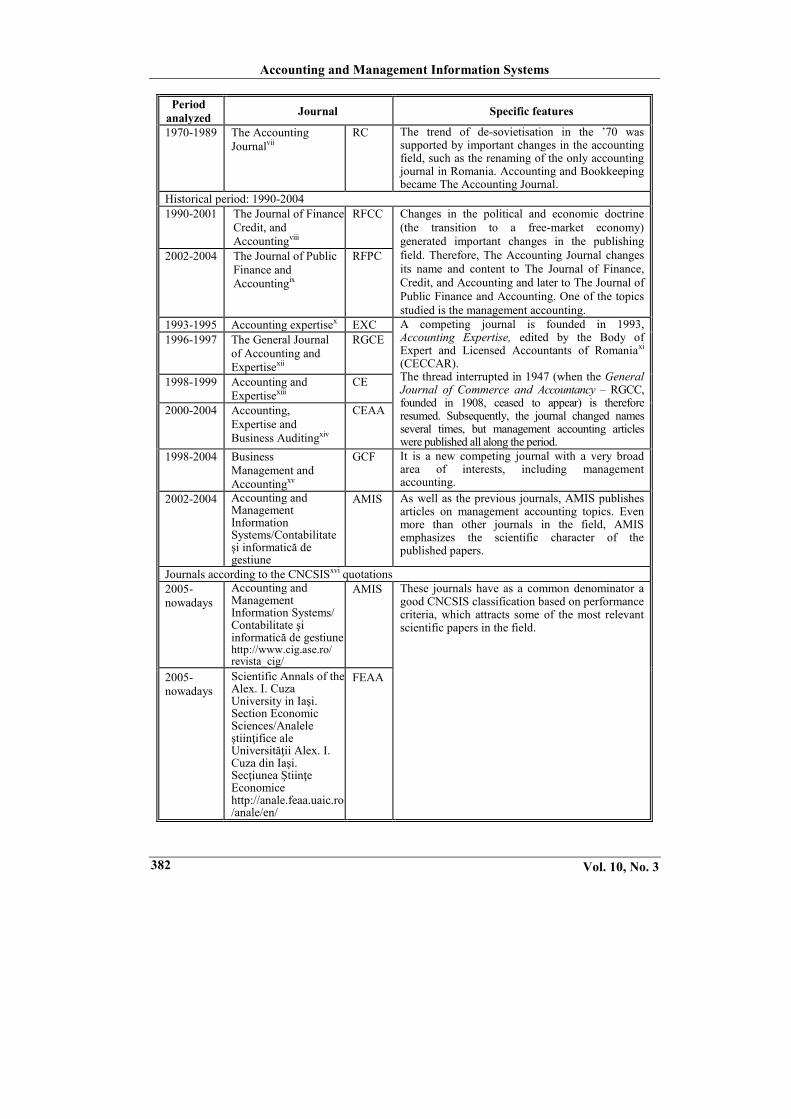

Table 1. Journals analysedPeriod

analyzed Journal Specific features

Existing journalsHistorical period: 1908-19481908-1948 The Journal of

Commerce andAccountancyiii

RGCC The idea of founding the journal was launchedduring the first National Congress of Schools ofCommerce Alumniiv that took place on October29th 1906. It materialized through the publicationof the first issue of the journal in January 1908.When Romania entered the war in August 1916the publication was discontinued for a period offour years (July 1916 – December 1920).Subsequently, the journal continued to bepublished until March 1947. The area of interest isvery broad, including management accounting.

Historical period: 1949-19891937-1955 Accounting Bulletinv BC The Accounting Bulletin, as an official publication

of the Body of Accountants – Ilfov Sector, wasonly an “instrument” of communication betweenthe professional organization and its members.Starting in June 1939, papers are published aswell, addressing a variety of issues.

1956-1969 Accounting andBookkeeping vi

EC The renaming of the Accounting Bulletin asAccounting and Bookkeeping brought a certainchange in the contents of the journal. Therefore, adiversification and a specialization of the structureof the journal can be observed, and also a certain“detachment” from the generalized Soviet model,in the sense that some discussions on importantmatters occur. An important number ofmanagement accounting articles is published.

Accounting and Management Information Systems

Vol. 10, No. 3382

Periodanalyzed Journal Specific features

1970-1989 The AccountingJournalvii

RC The trend of de-sovietisation in the ’70 wassupported by important changes in the accountingfield, such as the renaming of the only accountingjournal in Romania. Accounting and Bookkeepingbecame The Accounting Journal.

Historical period: 1990-20041990-2001 The Journal of Finance,

Credit, andAccountingviii

RFCC Changes in the political and economic doctrine(the transition to a free-market economy)generated important changes in the publishingfield. Therefore, The Accounting Journal changesits name and content to The Journal of Finance,Credit, and Accounting and later to The Journal ofPublic Finance and Accounting. One of the topicsstudied is the management accounting.

2002-2004 The Journal of PublicFinance andAccountingix

RFPC

1993-1995 Accounting expertisex EXC A competing journal is founded in 1993,Accounting Expertise, edited by the Body ofExpert and Licensed Accountants of Romaniaxi

(CECCAR).The thread interrupted in 1947 (when the GeneralJournal of Commerce and Accountancy – RGCC,founded in 1908, ceased to appear) is thereforeresumed. Subsequently, the journal changed namesseveral times, but management accounting articleswere published all along the period.

1996-1997 The General Journalof Accounting andExpertisexii

RGCE

1998-1999 Accounting andExpertisexiii

CE

2000-2004 Accounting,Expertise andBusiness Auditingxiv

CEAA

1998-2004 BusinessManagement andAccountingxv

GCF It is a new competing journal with a very broadarea of interests, including managementaccounting.

2002-2004 Accounting andManagementInformationSystems/Contabilitateşi informatică degestiune

AMIS As well as the previous journals, AMIS publishesarticles on management accounting topics. Evenmore than other journals in the field, AMISemphasizes the scientific character of thepublished papers.

Journals according to the CNCSISxvi quotations2005-nowadays

Accounting andManagementInformation Systems/Contabilitate şiinformatică de gestiunehttp://www.cig.ase.ro/revista_cig/

AMIS These journals have as a common denominator agood CNCSIS classification based on performancecriteria, which attracts some of the most relevantscientific papers in the field.

2005-nowadays

Scientific Annals of theAlex. I. CuzaUniversity in Iaşi.Section EconomicSciences/Analeleştiinţifice aleUniversităţii Alex. I.Cuza din Iaşi.Secţiunea ŞtiinţeEconomicehttp://anale.feaa.uaic.ro/anale/en/

FEAA

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 383

Periodanalyzed Journal Specific features

2005-nowadays

Virgil MadgearuReview of EconomicStudies and Research/Revista de Studii şiCercetări EconomiceVirgil Madgearu/http://www.econ.ubbcluj.ro/rvm/en/

VM

2008-nowadays

Studia UniversitatisBabeş Bolyai.Oeconomicahttp://studiaoeconomica.ubbcluj.ro/

SUBB

2.2. Research results

a) Publishing the research results in management accounting in 1908 – 1949

According to the research conducted by Calu (2005), management accounting(costing) issues began to attract the interest of accounting specialists; many articleswere published in the RGCC, in 1908-1948. Accordingly, specialized articles werepublished on a particular segment, such as the division of general administrativeexpenses or an overview of the calculation of costs in different economic sectors:industry, trade. The problem of distribution methods of the expenses was alsopresented in the pages of journals; in this regard, the appearance of procedures(methods) in the Romanian literature is noticed: the division method, the additionalmethod, equivalent figures method, coupling method etc.

Issues related to budgeting cost were also if interest; in this respect we recall a chapterin Evian’s book “Accounting Industry” (The budget is “a projection into the future ofthe enterprise’s activity”) and an article published in BC (1948).

The period under review is characterized by the concerns displayed by the academicsfor choosing, defining and clarifying specific terms for cost calculation. Accordingly,there were discussed and defined the following terms: price cost, the recovery price:“price cost, meaning the purchase (procurement) price, the recovery price – aminimum sale price”xvii, general administration overheads – “all the expensesconnected with rent, salaries, light and heating, various taxes etc.”xviii, procurementcosts for sale – “all the general expenses made with the purchasing of goods and notincluded in paragraph a) [the cost price]”xix, selling expenses – “all the expensesincurred in the sale such as advertisement, displays, placement agencies etc.”xx. Theseconcepts were debated in CECCAR and were published in RGCC (1936).

At the same time, different aspects of industry experience in other countries arepresented as examples, such as standardization and cost calculation in Germany(RGCC, 1937). Another idea found in the pages of the publications of that time is thecomputation of the industrial recovery cost using extra accounting techniques.

Accounting and Management Information Systems

Vol. 10, No. 3384

Therefore, “... technical or extra accounting recovery costs are established usingsheets prepared for each item produced and columns containing the quantity and thecost of the raw materials employed, wages and manufacturing overheads reportedpercent”xxi (RGCC, 1940).

b) Publishing the research results in management accounting in 1949 – 1989

Post calculation was the part of the management accounting on which no substantialchanges were generated by the new economic doctrine. Given the possibility of awider exercise of the professional judgment, the cost calculation is one of the topicscovered in the pages of the journals EC and BC.

According to Calu (2005) the first research subjects that made reappearance in BC(after the June 11th 1948 moment) were those addressing the issue of costing. Themain topics were: costing in coal mines; cost calculation in the manufacturingindustry; post calculation in publishing houses; post calculation in cotton mills. Giventhat the accounting standard-setting process was developed at the industry level, therecan be noticed that most authors attempted to point out various features in the field ofmanagement accounting as well.

Changing the name of the journal from Buletinul contabililor (BC) to Evidenţacontabilă (EC) in 1956 only brought formal changes. Costing is as in the previousperiod, one of the main subjects addressed in the pages of this journal. According toCalu (2005), the subjects addressed in EC can be divided into two categories: (1) thepresentation of classical costing methods, using different companies as examples andproviding suggestions for improvement and (2) suggestions regarding the use of newmethods (direct-costing), from the “industrialized countries”. In the first category ofmethods, full-costing, process costing and job order costing were discussed, asmethods used assess costs in various industries. The second category, of modernmethods, began to be presented in the literature in the late ‘60s, initially in the form ofa book review, and subsequently in some articles addressing the issues of: recordingand calculation of production costs using THM method (machine-hour rate), the costcalculation concepts under standard costing method, GP (George Perrin) costcalculation method, direct-costing method.

Together with the “object” of accounting, the cost calculation was the subject ofarticles published in RC in the period 1970-1972. It was defined as it follows: “theobject of the cost calculation is, on one hand, the production and selling expenses ofthe enterprise, and on the other hand, the production of material goods, works andservices conducted in a given organizational framework and expressed quantitativelyby certain units of measurement” (RC, 1971).

In the late socialist period, in an article published in RC (1988), Ristea discussed theneed to organize “the management accounting as an autonomous function”xxii. Thisarticle expressed the view that “accounting cannot be limited to costing and thecomputation of the results only through the carriers of value”xxiii, requiring “a separateaccounting information structure ... called «management accounting», the central

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 385

problem of which is to calculate the production costs and results”xxiv and using “thespecific instruments ... costing, internal budgets and internal financial control”xxv.

c) Publishing the research results in management accounting in 1990 – 2004

Following the Revolution of 1989, which resulted in the fall of communism and thetransition to a free market economy, the publishing environment has undergone asignificant transformation. Therefore, a transition occurred, from the existence of amonopoly on specific accounting journals to a plurality of options. An analysis wasperformed of articles published during this period in the field of managementaccounting according to topic.

The duality in the post-revolutionary Romanian accounting system involves distinctapproaches regarding the problems of management accounting and costing. In theearly ‘90s, “the benchmark treatment” was represented by full costing, matched by theaccounting technique of using the Class 9 accounts form the Chart of accounts torecord costing activities. These accounts were called Management Accounts andprovided under the regulations issued by the Ministry of Finance.Switching from a monistic accounting to a dualistic accounting system resulted in theappearance of original articles presenting the appropriate technical solutions for thenew realities, such as introducing a practical choice for the organization ofmanagement accounting (EXC, 1993). The issues raised were not only technical, butthey also raised questions: is there a boundary between financial and managementaccounting? (EXC, 1996). Subsequently, management accounting began to be moreand more the subject of articles that relate to a modern approach. In this respect wemention the following: activity-based costing (RFCC, 1999; CEAA, 2003; RFPC,2003; GCF, 2003; AMIS), target costing (AMIS), the relevance of accountinginformation in making decisions on cost management within a company (GCF, 1999;AMIS, 2004), approaches concerning the limits of the management accounting system(GCF, 2000), the conceptual boundaries of the management accounting in thedevelopment worldwide (RFCC, 2001), considerations of influence of the costcalculation on the profit or loss (RFCC, 2001), comparative management accounting(CEAA, 2002), management accounting using marginal costs (AMIS, 2004), culturalaspects (AMIS, 2003) etc.

Linked to the management accounting issue is the management control, defined as“the process by which managers ensure that resources are obtained and used withefficiency, effectiveness and relevance for the objectives of the organization” (Ionaşcuet al., 2001). Some particular aspects of management control began to be addressed inspecialized journals. In this respect, we note the overall approach of this domain:restructuring the company and management control (RFCC, 1999), managementcontrol for activities generating fixed overheads (GCF, 2003), internal transfer pricingpractices (CEAA, 2001, 2002), inventory management models, the concept ofmanagement control (AMIS, 2004), budgets (AMIS, 2004), concept of performance(AMIS, 2002, 2004), project management (AMIS, 2003), quality control and qualitycosts (AMIS, 2004).

Accounting and Management Information Systems

Vol. 10, No. 3386

d) Publishing the research results in management accounting in 2005 – 2011

In 2005 the Ministry of Education established new criteria for holding teachingpositions in higher education and for achieving academic titles. Consequently, somemutations occurred regarding the publication of scientific papers. According to thenew regulations, the most relevant criteria for holding teaching positions in highereducation and for achieving academic titles are: the number of ISI articles (A journalsin CNCSIS classification), the number of international databases indexed articles (B+journals in CNCSIS classification), holding the position of director or member of aresearch team working on a research project financed through a national competition.Thus, the most relevant papers were published in journals classified by CNCSIS as A(ISI) and B + (indexed in international databases).

In the same year, CNCSIS established new criteria for the evaluation of journals (A,B, C, and D). In 2007, the B+ subcategory was introduced to stimulate the visibility ofRomanian journals on the Web. In 2008 the B+ subcategory became the category ofRomanian journals indexed in international databases, and complying with all theconditions of the B category journals (http://www.cncsis.ro/articole/1901/Arhiva-2005-2010.html).

To classify the articles published in the four journals we did as it follows: weidentified the articles with other topics than accounting, articles with financialaccounting topics, management accounting articles and other types of accounting. Toclassify the management accounting articles we adapted a classification published bythe Management Accounting Review (MAR) to analyze the articles published in thelast two decades (Management Accounting Research, 21 (2010) 278–284). However,the classification of these articles is the result of our work and is inevitably subjective.Thus, the articles were classified according to two criteria: topic studied and researchsettings. After analyzing the abstracts of the articles published, the criteria weredetailed as it follows:

Table 2. Criteria usedCRITERIA

Topic studied Traditional costing techniquesAdvanced costing techniquesPricing; including transfer pricingManagement accounting practicesManagement accounting changeManagement and organisational controlPerformance measurementStrategic managementRisk managementInter-organisational management controlOthers

Research settings GenericManufacturingSpecific industriesServicesSpecific countriesOther

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 387

The results obtained are the following in table 3.

Table 3. Classification of articlesITEMS TOTAL AMIS FEAA VM SUBB

u % u % u % u % u %Total number of articles,of which:

731 100 531 100 49 100 61 100 90 100

Number of articles inother domains

391 53.49 251 47.27 11 22.45 53 86.89 76 84.44

Number of articles inaccounting, of which:

340 46.51 280 52.73 38 77.55 8 13.11 14 15.56

Number of articles infinancial accounting

138 40.59 115 41.07 18 47.37 1 12.5 4 28.57

Number of articles inmanagement accounting

70 20.59 55 19.64 8 21.05 3 37.5 4 28.57

Number of articles inother types of accounting

132 38.82 110 39.29 12 31.58 4 50 6 42.86

We notice that the average percentage of papers in management accounting is 20.59%in these journals (from 19.64% in AMIS to 37.5% in VM).

Table 4. First criteria: topics studiedITEMS MAR

2000-2009(%)

TOTALROMANIA AMIS FEAA VM SUBB

u % u % u % u % u %Traditional costingtechniques

9 12.86 7 12.73 2 25

Advanced costingtechniquesxxvi

15 16 22.86 12 21.82 2 25 1 33.33 1 25

Pricing; includingtransfer pricing

2 4 5.71 4 7.27

Managementaccounting practices

8 6 8.57 4 7.27 1 12.5 1 33.33

Managementaccounting change

15 5 7.14 5 9.09

Management andorganisationalcontrol

17 5 7.14 3 5.45 2 50

Performancemeasurement

14 2 2.86 2 3.64

Strategicmanagement

3 5 7.14 3 5.45 1 33.33 1 25

Risk management 3 2 2.86 2 25Inter-organisationalmanagement control

6 1 1.43 1 1.82

Othersxxvii 17 15 21.43 14 25.45 1 12.5Total 100

(205 papers)70 100 55 100 8 100 3 100 4 100

Accounting and Management Information Systems

Vol. 10, No. 3388

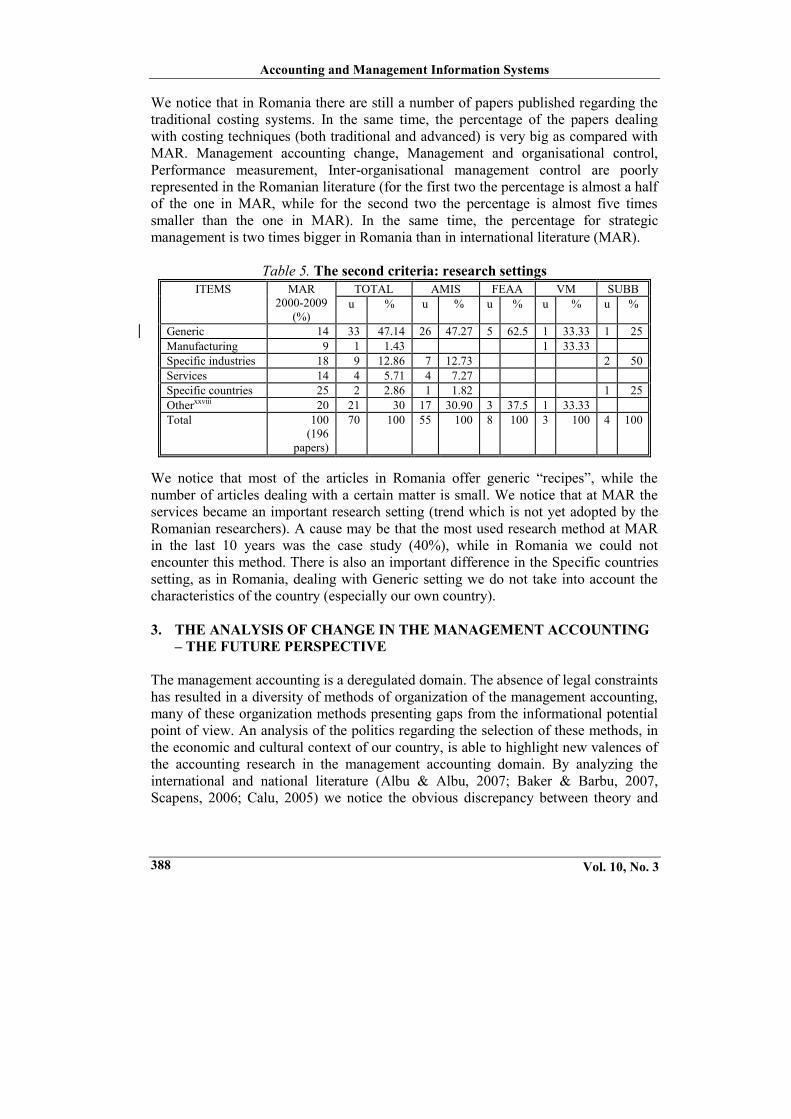

We notice that in Romania there are still a number of papers published regarding thetraditional costing systems. In the same time, the percentage of the papers dealingwith costing techniques (both traditional and advanced) is very big as compared withMAR. Management accounting change, Management and organisational control,Performance measurement, Inter-organisational management control are poorlyrepresented in the Romanian literature (for the first two the percentage is almost a halfof the one in MAR, while for the second two the percentage is almost five timessmaller than the one in MAR). In the same time, the percentage for strategicmanagement is two times bigger in Romania than in international literature (MAR).

Table 5. The second criteria: research settingsITEMS MAR

2000-2009(%)

TOTAL AMIS FEAA VM SUBBu % u % u % u % u %

Generic 14 33 47.14 26 47.27 5 62.5 1 33.33 1 25Manufacturing 9 1 1.43 1 33.33Specific industries 18 9 12.86 7 12.73 2 50Services 14 4 5.71 4 7.27Specific countries 25 2 2.86 1 1.82 1 25Otherxxviii 20 21 30 17 30.90 3 37.5 1 33.33Total 100

(196papers)

70 100 55 100 8 100 3 100 4 100

We notice that most of the articles in Romania offer generic “recipes”, while thenumber of articles dealing with a certain matter is small. We notice that at MAR theservices became an important research setting (trend which is not yet adopted by theRomanian researchers). A cause may be that the most used research method at MARin the last 10 years was the case study (40%), while in Romania we could notencounter this method. There is also an important difference in the Specific countriessetting, as in Romania, dealing with Generic setting we do not take into account thecharacteristics of the country (especially our own country).

3. THE ANALYSIS OF CHANGE IN THE MANAGEMENT ACCOUNTING– THE FUTURE PERSPECTIVE

The management accounting is a deregulated domain. The absence of legal constraintshas resulted in a diversity of methods of organization of the management accounting,many of these organization methods presenting gaps from the informational potentialpoint of view. An analysis of the politics regarding the selection of these methods, inthe economic and cultural context of our country, is able to highlight new valences ofthe accounting research in the management accounting domain. By analyzing theinternational and national literature (Albu & Albu, 2007; Baker & Barbu, 2007,Scapens, 2006; Calu, 2005) we notice the obvious discrepancy between theory and

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 389

practice, among the studies undertaken in diverse geographical areas but also amongthe addressed research methods.

The research in the change in the management accounting in Romania may be basedon the evolution theory, whose potential was not fully described or used in theaccounting research (Johansson & Siverbo, 2009; Coad & Cullen, 2006). The analysisof change in management accounting should follow two axes: the trend at theconceptual level and the methodological one.

From the conceptual point of view, theories in a social sciences field such asmanagement accounting research should provide explanations that are useful for thosewe study – managers, organizations and society (Malmi & Granlund, 2009). Theultimate reason for developing a theory is to be able to use this understanding, ortheory, in creating better management accounting practices, both in terms of contentand use (Chenhall, 2003; Ittner & Larcker, 2001). An important criterion for atheory’s success is the value of the theory to users. As well, there is a need formanagement accounting theories addressing what systems or techniques to use, howand in which circumstances (Kaplan, 1998). Not in the last time, we need theoriesexplaining how to change management accounting practices (Malmi & Granlund,2009). Studies should address the performance implications of various practices.Another avenue is to develop existing practice theories to more complete theories byspecifying constructs, relationships and underlying mechanisms more clearly andaddressing their limitations (Malmi & Granlund, 2009). One of the most used theoriesin the management accounting change is the framework suggested by Burns &Scapens (2000).

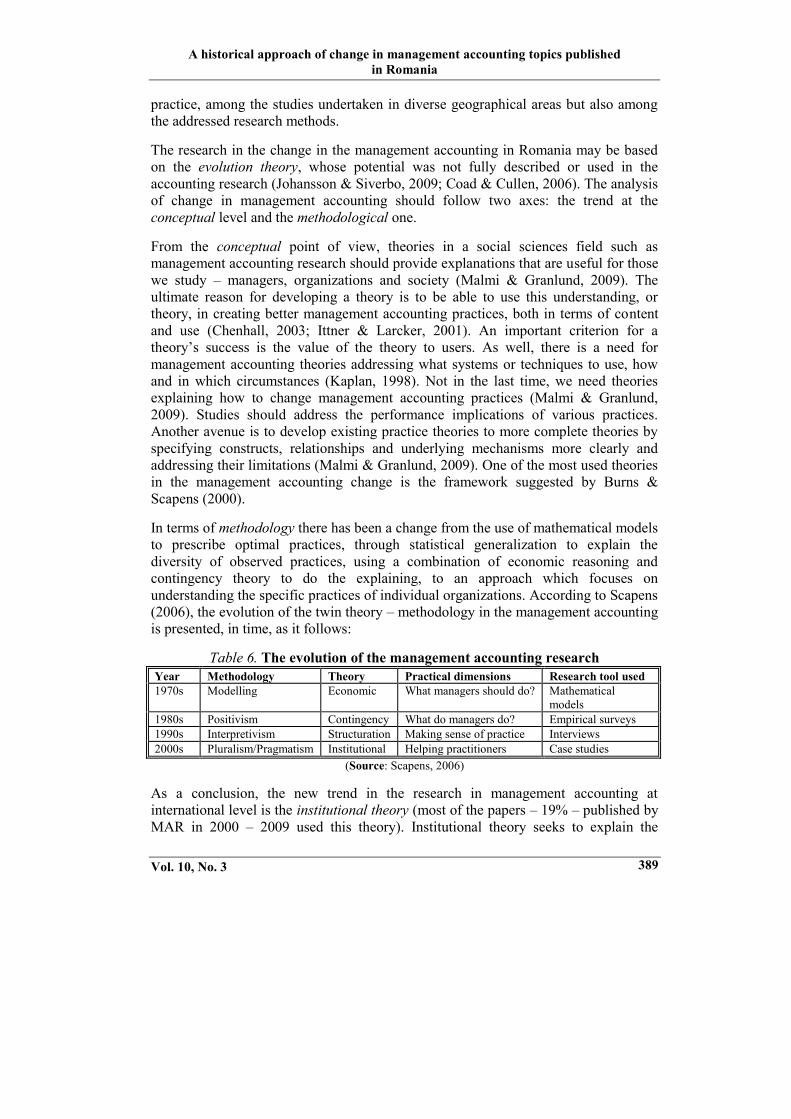

In terms of methodology there has been a change from the use of mathematical modelsto prescribe optimal practices, through statistical generalization to explain thediversity of observed practices, using a combination of economic reasoning andcontingency theory to do the explaining, to an approach which focuses onunderstanding the specific practices of individual organizations. According to Scapens(2006), the evolution of the twin theory – methodology in the management accountingis presented, in time, as it follows:

Table 6. The evolution of the management accounting researchYear Methodology Theory Practical dimensions Research tool used1970s Modelling Economic What managers should do? Mathematical

models1980s Positivism Contingency What do managers do? Empirical surveys1990s Interpretivism Structuration Making sense of practice Interviews2000s Pluralism/Pragmatism Institutional Helping practitioners Case studies

(Source: Scapens, 2006)

As a conclusion, the new trend in the research in management accounting atinternational level is the institutional theory (most of the papers – 19% – published byMAR in 2000 – 2009 used this theory). Institutional theory seeks to explain the

Accounting and Management Information Systems

Vol. 10, No. 3390

development of institutions and organizations and the way that organizations competefor political and social power and institutional legitimacy. DiMaggio & Powell (1983)label the process through which institutions and organizations tend to adopt similarstructures and practices, as institutional isomorphism. Institutional isomorphism is aprocess that causes a particular organizational unit within a population to resembleother units in the population facing similar sets of environmental conditions and it canbe coercive, normative and mimetic.

From the research methodology point of view the newest existing trend atinternational level is the pluralism/pragmatism, which supposes using a mixing ofmethods, both qualitative and quantitative. The latest method is the triangulation.Triangulation represents an original abstract of different research methods (e.g. casestudies and survey methods). Within the survey methods the questionnaires and theinterviews may be used. The triangulation between the case studies and the empiricalinvestigation methods (Modell, 2005) offers the means for assessing the degree ofconvergence and, in the same time, offers the means for the presentation ofdifferences between the results obtained (Brewer & Hunter, 1989; Sieber, 1973). Theempirical surveys can improve the level of understanding the impact of a certainphenomenon and/or the form and intensity of the conceptual relationships noticed inthe case studies. On the other hand, the case studies increase the understanding leveloffered by the results of the empirical investigations, offering a holistic vision and, inthe same time, help explaining the obvious problems or the problems that can appearin the future.

CONCLUSIONS

We started from the idea of presenting the national historical perspective regarding themain topics in management accounting in time (1908-2005). Our conclusion was thatuntil 1989 most of the papers described the classical cost calculation methods. From1990 until 2004 the articles presented modern cost calculation methods and the trendsidentified in other countries. After 2005 (when a major change occurred regarding theassessment of the academic journals), we compared the research published in fourimportant Romanian academic journals on management accounting topics. Ourobjective was to establish the trend of the management accounting research inRomania. The small number of articles published made us believe that this was notrelevant. So, we compared the total number of articles published in these journals withthe articles published in MAR. We came to the conclusion that the research topics inthe Romanian journals are traditional as compared with the research topics in MAR.

A limit of our research is that due to the lack of tradition in publishing managementaccounting papers in academic journals, we could not make a comparison in time ofthe results obtained. Another limit is that we only selected 4 journals, while there arelots of other economic journals in Romania classified B+ by CNCSIS which publisharticles on this topic. Another limit is that in some journals the number of articlespublished on management accounting topics is very small. Another limit is that we

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 391

could not use the entire classification presented in MAR, namely the theory used, asmany articles had only a literature review part. We also didn’t present the regions oforigin of these papers, as in more than 90% of the cases (100% for the journals exceptAMIS) this is Romania.

The differences in percentages show us that there is a need for a change in themanagement accounting research in Romania. We notice that in Romania theresearchers are more concerned with the costing techniques than with the managementcontrol. In the same time, the target of management accounting is to help managers intheir decision making process. This cannot be achieved since our research focuses ongeneric settings and not on specific industries or services. We must pay more attentionto the accounting and management practices in the successful organizations (Malmi &Granlund, 2009). For our country most of the researchers are also the professors.Since their concerns are related to the costing techniques mostly, this is what theytransmit to their students, and their students will implement in their companies. This iswhy we believe that a change in the management accounting research topics will alsolead to a change in the management accounting practice. The target is to find the wayin which the challenges of the economic, social and legal environment are transformedin opportunities through the changes in the management accounting.

ACKNOWLEDGEMENTS

This work was supported by CNCSIS –UEFISCSU, project number ID 1779 Romaniafacing a new challenge: accessing the structural funds for the sustainable developmentin agriculture. The convergence of financial reporting of the native entities with theEuropean realities, PNII – IDEI 1779/2008.

REFERENCES

Albu, C. & Albu, N. (2007) „Le contrôle de gestion en Roumanie - un essaid’identification des pratiques et propositions de recherché”, 28ème Congrèsde l’Association Francophone de Comptabilité, Poitiers, France

Albu, C. & Albu, N. (2008) “Transformation and Hybridization within the accountingprofession: some evidence from Romania”, The European AccountingAssociation 31st Congress, Rotterdam, the Netherlands

Alcouffe, S. (2002) “La diffusion de l’ABC en France: une etude empirique utilisantla theorie de la diffusion des innovations”, Actes du 23e congres de l’AFC

Alcouffe, S., Berland, N. & Levant, Y (2003) “Les facteurs de diffusion desinnovations manageriales en comptabilite et controle de gestion: une etudecomparative”, Comptabilite – Controle – Audit / Numero special – Numerospecial – Mai: 7-26

Almăşan, A. & Grosu, C. (2008) „Managers’ awareness of the accounting informationusefulness”, Accounting and Management Information Systems, no. 24: 56-71

Alter, N. (2000) L’innovation ordinaire, Paris: PUF Sociologies

Accounting and Management Information Systems

Vol. 10, No. 3392

Azan, W. (2009) “Management Control Competences and ERP: An EmpiricalAnalysis in France”, European Accounting Association 32nd Congress,Tampere, Finland

Baker, R. & Barbu, E.M. (2009) “The Evolution of Research on InternationalAccounting Harmonization: An Historical and Institutional Perspective”,European Accounting Association 32nd Congress, Tampere, Finland

Baker, R. & Barbu, E.M. (2007) “Trends in research on international accountingharmonization”, The International Journal of Accounting, vol. 42: 272-304

Baldvinstottir, G., J. Burns, H. Nørreklit & R.W. Scapens, 2009, The Image ofAccountants: From Bean Counters to Extreme Accountants, AccountingAuditing & Accountability Journal, vol. 22, no. 6: 858-882

Băviţă, I., Dumitru, M., Calu, D., Pitulice, C. & Popa, A. (2008) “Contabilitatea înagricultură – abordări teoretice şi practice”, Bucureşti: Editura Contaplus

Boitier (2007) “L’influence des systems de gestion integers sur l’integration dessystems de controle de gestion”, Comptabilite – Controle – Audit, Tome 14,vol. 1, Juin: 33- 48

Bollecker & Azan (2009) “L’importation de cadres theoriques dans la recherché encontrole”, Comptabilite – Controle – Audit / Tome 15, vol. 2, Decembre 2:61-86

Bouquin, H. (2004) “Comptabilite De Gestion”, EconomicaBrewer, J. & Hunter, A. (1989) Multimethod research: A Synthesis of styles. Newbury

Park: SageBrignall, T.J. & Modell, S. (2000) “An institutional perspective on performance

measurement and management in the new public sector”, ManagementAccounting Research, vol. 11, no. 3: 281-306

Brinn, T., Jones, M.J. & Pendlebury, M. (1996) “UK Accountants’ Perceptions ofResearch Journal Quality”, Accounting and Business Research, vol. 26, no. 3:265-278

Burns, J. & Scapens, R.E., (2000) “Conceptualizing management accounting change:an institutional framework”, Management Accounting Research, vol. 11, no.1:3-25

Caglio, A. (2003) “Enterprise Resource Planning systems and accountants: towardshybridization?”, European Accounting Review, vol. 12, no. 1: 123-153

Calu, D. (2005) Istorie şi dezvoltare privind contabilitatea din România, Bucureşti:Editura Economică

Cappellatti, L. & Kouthra, D. (2008) “L’implantation d’un systeme de controle degestion au sein d’entreprise liberals: cas des offices de notaries”,Comptabilite- Controle - Audit, Tome 15, vol. 1, Juin: 79-104

Chenhall, R.H. (2003) “Management control system design within its organizationalcontext: Findings from contingency-based research and directions for thefuture”, Accounting, Organizations and Society, vol. 28, no. 2-3: 127-168

Coad A.F. & Cullen J. (2006) “Inter-organisational cost management: Towards anevolutionary perspective”, Management Accounting Research, vol. 17, no. 12:342-69

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 393

Davis, S. & Albright, T. (2000) „The Changing Organizational structure andIndividual Responsabilities of Managerial Accountants: A Case Study”,Journal of Managerial Issues, vol. 12, no. 4: 446- 468

Dechow, N. & Mouritsen, J. (2005) Enterprise resource planning systems,management control and the quest for integration, Accounting, Organizations& Society, vol. 30., no. 7-8: 691-733

DiMaggio, P.J. & Powell, W.W. (1983) „The iron cage revisited: institutionalisomorphism and collective rationality in organizational fields”, AmericanSociological Review, vol. 48, no.4: 147- 160

Dogan, M. & Pahre, R. (1991) L’innovation dans les sciences sociales, PUFGlăvan, M., Brăescu (Dumitru), M., Dumitru, V., Jinga, G. & Lapteş, R. (2007) “The

Relevance and Quality of the Accounting Information”, Accounting andManagement Information Systems, Supplement: 103-114

Granlund, M. & Malmi, T. (2002) “Moderate impact of ERPs on managementaccounting: a lag or permanent outcome?”, Management AccountingResearch, vol. 13, no. 3: 299-321

Hodgson, G. (1993) “Economics and Evolution”, Cambridge: Polity PressHopwood, A.G. (2008) “Changing Pressures on the Research Process: On Trying to

Research in an Age when Curiosity is not Enough”, European AccountingReview, vol. 17, no. 1: 87- 96

Ittner, C.D. & Larcker, D.F. (2001) “Assessing empirical research in managerialaccounting: A value-based management perspective” Journal of Accountingand Economics, vol. 32, no 1-3: 349-410.

Jinga, G., Dumitru, M., Dumitrana, M. & Vulpoi, M. (2010) “Accounting systems forcost management used in the Romanian economic entities”, Accounting andManagement Information Systems, vol. 9, no. 2: 242-267

Johansson, T. & Siverbo, S. (2009) “Why is research on management accountingchange not explicitly evolutionary? Taking the next step in theconceptualisation of management accounting change”, ManagementAccounting Research, vol. 20, no. 2: 146- 162

Kaplan, R. S. (1998) “Innovation action research: Creating new management theoryand practice, Journal of Management Accounting Research, vol. 10: 89-118

Lapsley, I. & Pallot, J. (2000) “Accounting, management and organizational change:A comparative study of local government”, Management AccountingResearch, vol. 11, no. 2: 213- 229

Lapsley I. & Wright (2004) “The diffusion of management accounting innovations inthe public sector: a research agenda”, Management Accounting Research vol.15, no. 3: 355-374

Malmi, T., Järvinen, P. & Lillrank, P. (2004) “A Collaborative Approach forManaging Project Cost of Poor Quality”, European Accounting Review,vol. 13, no. 2: 293-317

Malmi, T., & Granlund, M. (2009) “In Search of Management Accounting Theory”,European Accounting Review, vol.18, no. 3: 597- 620

Accounting and Management Information Systems

Vol. 10, No. 3394

Mathieu, R., & McConomy, B. (2003) “Productivity in “top-ten” academic accountingjournals by researchers at Canadian universities”, Canadian AccountingPerspectives, vol. 2, no. 1: 43-76

Maurel, C. (2008) “Les caracteristiques du controle de gestion au sein des societiescooperatives de production”, Comptabilite- Controle- Audit, Tome 14, Vol. 2,Decembre: 155- 172

Modell, S. (2005) “Triangulation between case study and survey methods inmanagement accounting research: An assessment of validity implications”,Management Accounting Research, vol. 16, no. 2: 231-254

Moisdon, J.C. (1997) “Du monde d’existence des outils de gestion”, Paris: EditionsSeli Arslan

Mouritsen, J. & Sof T. (2006) “Accounting, network complementarities and thedevelopment of inter-organisational relations. Review of Accounting andnetwork”, Accounting, Organizations and Society, vol. 31, no.3: 241-275

Nederhof, A.J. & van Raan, A.F.J. (1993) “A bibliometric analysis of six economicsresearch groups: a comparison with peer review”, Research Policy, vol. 22:353-368

Nor-Aziah, A.K. & Scapens, R.W. (2007) “Corporatisation and accounting change.The role of accounting and accountants in a Malaysian public utility”,Management Accounting Research, vol. 18, no. 2: 209- 247

Pierce, B. & O'Dea, T. (2003) “Management accounting information and the needs ofmanagers: Perceptions of accountants and managers compared”, The BritishAccounting Review, vol. 35, no. 3: 257-290

Popa A., Barbu E. M. & Farcane N. (2009) “A Neo-Institutional Explanation ofAccounting Evolution in Romania”, European Accounting Association 32nd

Congress, Tampere, FinlandQuattrone, P. & Hopper, T. (2001) “What does organizational change mean?

Speculations on a taken for granted category”, Management AccountingResearch, vol. 12: 403- 435

Raffournier, B. & Schatt, A. (2010) “Is European Accounting Research FairlyReflected in Academic Journals? An Investigation of PossibleNon-mainstream and Language Barrier Biases”, European AccountingReview, vol. 19, no.1: 161-190

Rogers, E.M. (1995) “Diffusion of Innovations”, New York: Free PressRojot, J., (2005), Theorie des organisations, ESKA: ParisScapens, R.W. & Jazayeri, M. (2003) “ERP systems and management accounting

change: opportunities or impacts? A research note”, European AccountingReview, vol. 12, no. 1: 201-233

Scapens, R.W. & Roberts, J., (1993) “Accounting and control: a case study ofresistance to accounting and change”, Management Accounting Research,vol. 4, no.1: 1-32

Scapens, R.W. (2006) “Understanding management accounting practices: A personaljourney”, The British Accounting Review, vol. 38, no.1: 1- 30

A historical approach of change in management accounting topics publishedin Romania

Vol. 10, No. 3 395

Schneider, A. (1995), “Incidence of Accounting Irregularities: An Experiment toCompare Audit, Review, and Compilation Services”, Journal of Accountingand Public Policy, vol. 14, no. 4: 293-310

Sieber, S.D. (1973) “The integration of fieldwork and survey methods”, AmericanJournal of Sociology, vol. 78: 1335- 1359

ter Bogt, H. & van Helden, J. (2000) “Accounting Change in Dutch Government:Exploring the Gap between Expectations and Realizations”, ManagementAccounting Research, vol. 11, no. 2: 263-279

van Campenhout, G. & van Caneghem, T. (2010) '”Article Contribution andSubsequent Citation Rates: Evidence from European Accounting Review”,European Accounting Review, vol. 19, no. 4: 837- 855

Veblen, T. (1898) “Why is economics not an evolutionary science?” QuarterlyJournal of Economics vol.12: 373–397

Veblen, T. (1914) “The Instinct of Workmanship and the State of the Industrial Arts”,New York: McMillan

http://www.cncsis.ro/Public/cat/25/Prezentare.html, accessed on March 1st 2011*** Revista de contabilitate, 1970-1989 [RC]*** Expertiză contabilă, 1993-1995 [EXC]*** Contabilitatea, expertiza şi auditul afacerilor 2000-2003 [CEAA]*** Gestiunea şi contabilitata firmei [GCF]*** Revista Finanţe, Credit, Contabilitate [RFCC]*** Revista Finanţe publice şi contabilitate [RFPC]

i The journals studies were: Accounting and Business Research; Accounting, Organizations andSociety; European Accounting Review; Journal of Accounting and Economics; Journal ofAccounting Research; The Accounting Review; Journal of Practice and Theory; InternationalJournal of Auditing; Accounting, Auditing and Accountability Journal; Critical Perspectives onAccounting; Accounting Business and Financial History; Accounting History; The AccountingHistorians Journal; Journal of International Accounting, Auditing and Taxation; Journal ofInternational Financial Management and Accounting; The International Journal of Accounting;Journal of Management Accounting Research; Management Accounting Research.

ii Commerce and Accounting General Journaliii Ro. Revista Generală de Comerţ şi Contabilitateiv Ro. Congresul absolvenţilor şcolilor comerciale din ţarăv Ro. Buletinul Contabililorvi Ro. Evidenţa contabilăvii Ro. Revista de contabilitateviii Ro. Revista de Finanţe, Credit, Contabilitateix Revista Finanţe publice şi contabilitatex Ro. Expertiză contabilăxi Ro. Corpul Experţilor Contabili şi Contabililor Autorizaţi din Româniaxii Ro. Revista generală de contabilitate şi expertizăxiii Ro. Contabilitate şi expertizăxiv Ro. Contabilitatea, expertiza şi auditul afacerilorxv Ro. Gestiunea şi contabilitatea firmeixvi There is an ISI journal in Romania in the economic field (Amfiteatru Economic) and several journals

where economic research can be published (Economic Forecasting, Transylvania Research, Studii şi

Accounting and Management Information Systems

Vol. 10, No. 3396

Cercetări de Calcul Economic and Cibernetică Economică). However, the number of studies inaccounting is too small for a statistical regrouping. Given the above considerations, we believe thatthe relevant research in Romanian accounting can be found in the journals quoted as B+ byCNCSIS. For the purposes of this study, four journals were selected where accounting articles arefound, published by the most important universities in the country (see Table 1).

xvii Ro. „preţul de cost, adică preţul de cumpărare (procurare), preţul de revenire – preţ minim devânzare”

xviii Ro. „toate cheltuielile în legătură cu scopul urmărit de întreprinderea comercială cum sunt: chirii,salarii, luminat şi încălzit, impozite diverse etc.”

xix Ro. „toate cheltuielile generale făcute cu procurarea mărfii şi care nu intră în punctul a) [preţul decost – n.a.]”

xx Ro. „toate cheltuielile făcute pentru realizarea vânzării cum sunt: reclame, vitrine, agenţii de plasareetc.”

xxi Ro. „se stabilesc ... preţuri de revenire tehnice sau extracontabile cu ajutorul unor fişe întocmitepentru fiecare obiect fabricat şi cuprinzând coloane pentru cantitatea şi costul materiei primeîntrebuinţate, pentru costul mânei de lucru şi pentru cheltuielile de fabricaţie raportate la sută”

xxii Ro. „ca funcţie autonomă a unei contabilităţi de gestiune interne”xxiii Ro. „contabilitatea nu se mai poate limita la calculaţia costurilor şi determinarea rezultatelor numai

prin prisma purtătorilor de valoare”xxiv Ro. „o structură informaţională contabilă distinctă... denumită de noi <<contabilitate de gestiune

internă>>, a cărei problemă centrală este calcularea costurilor şi stabilirea rezultatelor producţiei”xxv Ro. „instrumentele caracteristice... sunt: calculaţia costurilor, bugetele interne şi controlul financiar

preventiv”xxvi Here we cumulated ABC (7% in MAR) and Other advanced techniques (7% in MAR) in MAR.xxvii In Other we cumulated Other in MAR (3%) and also the topics that didn’t appear in Romanian

journals, as it follows: Capital Budgeting (1% in MAR); Budgeting, standard costing and varianceanalysis (5% in MAR); Cost accounting systems and techniques (4% in MAR); EVA and residualincome (1% in MAR); Governance (3% in MAR).

xxviii In Other we cumulated Public sector (9% in MAR), Multinationals (5% in MAR) – because noarticle was published in this research setting in Romania, and Other.