A Hedonic Analysis of Retail Milk and Oatmeal Attributes...

145

A Hedonic Analysis of Retail Milk and Oatmeal Attributes in Québec Jun Xiao Department of Agricultural Economics McGill University, Montreal March 2012 A thesis submitted to McGill University in partial fulfillment of the requirements of the degree of Master of Science © Jun Xiao, 2012

Transcript of A Hedonic Analysis of Retail Milk and Oatmeal Attributes...

A Hedonic Analysis of

Retail Milk and Oatmeal Attributes in Québec

Jun Xiao Department of Agricultural Economics

McGill University, Montreal March 2012

A thesis submitted to McGill University in partial fulfillment of the

requirements of the degree of Master of Science

© Jun Xiao, 2012

i

ABSTRACT

This study analyzes price differentials attributable to observable characteristics of

retail milk and oatmeal using the hedonic pricing methodology. Aggregated 2010

Nielsen retail scanner data were matched with 2011 primary data on front-of-

package product claims and Nutrition Facts table information in order to evaluate

the implicit prices of front-of-package labels, store characteristics and regional

characteristics associated with food products. Estimates indicate that retail prices

of milk and oatmeal were significantly influenced by product characteristics,

product labels and store characteristics. In particular, nutrient content claims that

can be verified with the Nutrition Facts table were associated with small

discounts, while labels containing non-verifiable information tended to be

associated with statistically significant price premiums. At the store level, there

were significant differences in the price premiums associated with product

attributes for all nine types of stores considered. Results also indicated that the

price of products was not significantly influenced by whether stores were located

in urban and rural areas. However, results revealed both price-regulated and non-

regulated milk were priced differently according to regions defined by the Régie

des marchés agricoles et alimentaires du Québec. The data also suggest that

consumers consider a brand‘s province of origin and the regionality of local brand

names when purchasing retail milk.

ii

RÉSUMÉ

Cette étude analyse les écarts de prix attribuables à des caractéristiques

observables de lait et de gruau vendu au détail par la méthodologie des prix

hédoniques. L‘évaluation des prix implicites des allégations sur le devant des

emballages, des caractéristiques de magasins et des caractéristiques régionales

associés aux produits alimentaires s‘est effectuée par le traitement de données.

Pour ce, deux sources de données ont été appariées, à savoir les données

scanographiques agrégées de Nielsen datant de 2010 et des données primaires sur

l‘étiquetage nutritionnel des produits préemballés, recueillies durant l‘automne

2011, comprenant les allégations nutritionnelles et les tableaux de valeur nutritive.

Les résultats indiquent que les prix de vente au détail de lait et de gruau sont

considérablement influencés par les caractéristiques des produits, les étiquettes

des emballages et les caractéristiques des magasins. En particulier, les allégations

nutritionnelles qui peuvent être vérifiées par les tableaux d‘étiquetage nutritionnel

ont été associées à des prix marginaux négatifs, tandis que les étiquettes contenant

des informations non-vérifiables ont tendance à avoir des effets positifs sur la

valeur du produit. À l‘échelle des magasins, des différences significatives ont été

associés aux prix implicites des composantes des produits pour les neuf types de

magasins d‘alimentation considérés. Selon les estimations des modèles

hédoniques, l‘emplacement d‘un magasin, soit dans une zone urbaine ou rurale,

n‘influence pas le prix des produits de manière significative. Par contre, les prix

du lait réglementé et non-réglementé diffèrent selon les régions définies par la

Régie des marchés agricoles et alimentaires du Québec. Les résultats de l‘analyse

suggèrent également que les consommateurs considèrent la province d‘origine

d'une marque ainsi que la régionalité des noms de marques locales lors de l'achat

du lait au détail.

iii

ACKNOWLEDGEMENTS

This thesis grew from a series of discussions with my supervisor, Dr. Paul

J. Thomassin, and I would like to underline my genuine appreciation for his

guidance which took the shape of freedom to pursue this research topic and room

to work my own way, balanced with concise advice and direction when obstacles

were met.

One of the lessons I learned throughout this endeavour is that data is not

passively gathered, but tracked and hunted down. The analysis of milk labels

would not have been possible without Québec dairies openly sharing their data

and answering my questions; many thanks to Zuzana Janacova and Shafia El-

Zammar of Saputo, Vicky Lapointe of Laiterie de la Baie, Sylvie Larouche of

Laiterie Chagnon, Judy MacDonald of Northumberland Dairy, Valérie Rousseau

of Laiterie Chalifoux, Sonia Tremblay of Nutrinor, and Anne Roy and her brother

of Laiterie Royala. I would also like to thank Dr. Laurette Dubé of the Desautels

Faculty of Management for access to the Nielsen data. Additionally, I am

indebted to Dr. Yu Ma for explaining the Nielsen data with kindness and patience,

and to Dr. John Henning for discussing data analysis and for his continued

guidance since my undergraduate years.

Equally, I would like to thank my classmates for their constructive

criticism, the administrative staff of the Department of Natural Resource Sciences

for their helpfulness, the Social Sciences and Humanities Research Council for

financial support, and my friends for offering encouragements and a shoulder to

lean on.

Most importantly, I wish to acknowledge my parents who have always

unhesitatingly offered emotional, moral and financial support. For their self-

sacrifices and dedication a mere expression of thanks does not suffice.

iv

TABLE OF CONTENTS

ABSTRACT ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

RÉSUMÉ ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i i ACKNOWLEDGEMENTS ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i ii TABLE OF CONTENTS ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv LIST OF TABLES ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vi LIST OF FIGURES ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vi

CHAPTER I: INTRODUCTION ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.1 OVERVIEW AND PROBLEM STATEMENT..................................................... 1 1.2 OBJECTIVES ............................................................................................... 2

1.3 STRUCTURE OF THESIS .............................................................................. 3

CHAPTER II: LITERATURE REVIEW .... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.1 OVERVIEW ................................................................................................ 4 2.2 CANADIAN FOOD LABELLING POLICY ....................................................... 5 2.3 U.S. FOOD LABELLING POLICY ................................................................. 7

2.4 FOOD LABELLING HISTORY AND PREVALENCE ......................................... 8 2.5 FOOD LABELLING AND CONSUMER PURCHASING DECISIONS .................... 10

2.5.1 Experimental Studies ...................................................................... 11 2.5.2 Economics ....................................................................................... 13 2.5.3 Stated Preference Literature ............................................................ 13

2.5.4 Revealed Preference Literature: Hedonic Pricing Method ............. 15

2.6 CHOICE OF METHODOLOGY ..................................................................... 18

2.7 HEDONIC THEORY ................................................................................... 19 2.7.1 Three Central Considerations ......................................................... 22

2.7.2 Selection of the Good ...................................................................... 22 2.7.3 Selection of Attributes .................................................................... 23 2.7.4 Functional Form .............................................................................. 28

CHAPTER III: DATA AND MODEL SPECIFICATION ... . . . . . . . . 32

3.1 DATA....................................................................................................... 32 3.1.1 Product Characteristics ................................................................... 33 3.1.2 Store Characteristics ....................................................................... 33

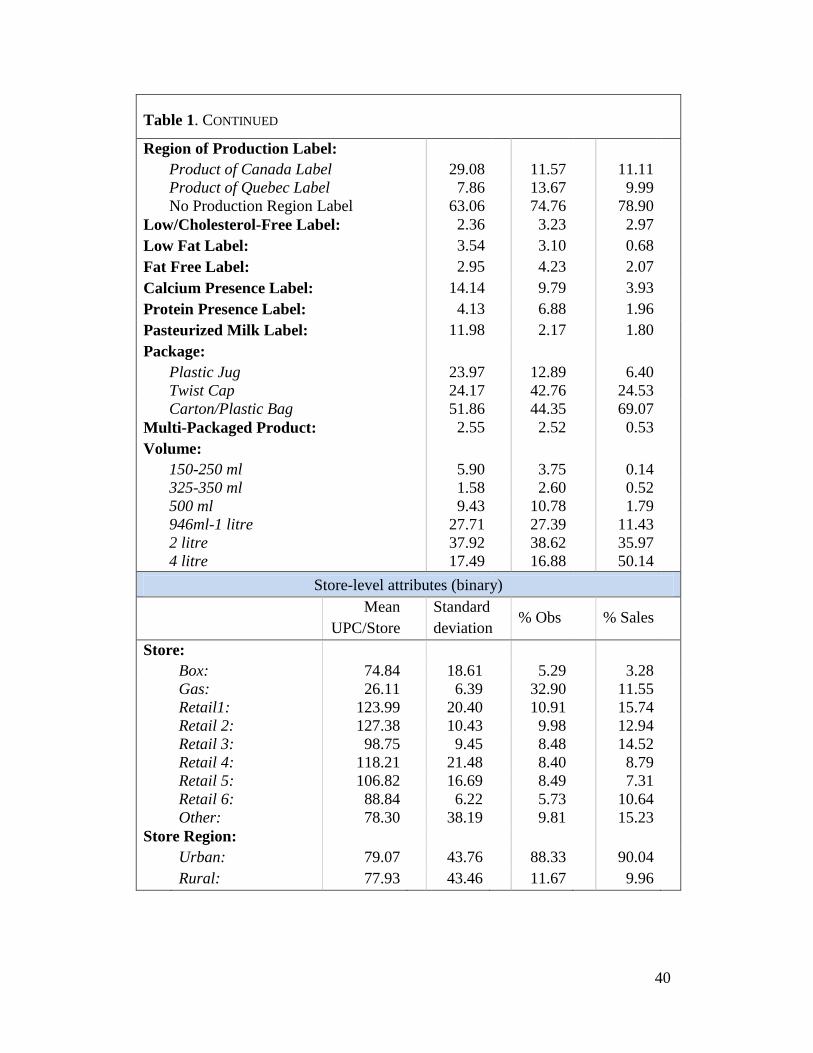

3.2 DESCRIPTIVE STATISTICS ........................................................................ 34

3.2.1 Descriptive Statistics of Retail Milk Products ................................ 34

3.2.2 Descriptive Statistics of Retail Oatmeal Products .......................... 41 3.3 LARGE SAMPLE SIZE ............................................................................... 45 3.4 MODEL SPECIFICATION ........................................................................... 46

3.4.1 Hedonic Pricing Model for Milk ..................................................... 47 3.4.2 Hedonic Pricing Model for Oatmeal ............................................... 50

v

CHAPTER IV: RESULTS AND DISCUSSION ... . . . . . . . . . . . . . . . . . . . . . . . 53

4.1 RETAIL MILK RESULTS ........................................................................... 53 4.1.1 Product Characteristics ................................................................... 54 4.1.2 Product Labels ................................................................................ 55 4.1.3 Store Characteristics ....................................................................... 57 4.1.4 Discussion ....................................................................................... 60

4.2 RETAIL OATMEAL RESULTS .................................................................... 61 4.2.1 Product Characteristics ................................................................... 61 4.2.2 Product Labels ................................................................................ 63 4.2.3 Store Characteristics ....................................................................... 64

4.3 HYPOTHESIS TESTING ............................................................................. 67

4.3.1 Objective 1: Front-of-Package Labels ............................................ 67 4.3.2 Objective 2: Store-Level Differences ............................................. 71

4.3.3 Objective 3: Regional Market Differences ..................................... 84

CHAPTER V. SUMMARY AND CONCLUSIONS ... . . . . . . . . . . . . . . . . . . 97

5.1 RESULTS .................................................................................................. 98 5.2 DISCUSSION ............................................................................................. 99 5.3 LIMITATIONS ......................................................................................... 101

5.4 FUTURE RESEARCH ............................................................................... 102

BIBLIOGRAPHY ... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

APPENDIX I. Règlement sur les prix du lait de consommation .. 114

APPENDIX II. Region I Fluid Milk Retail Prices .. . . . . . . . . . . . . . . . . . . . . 115

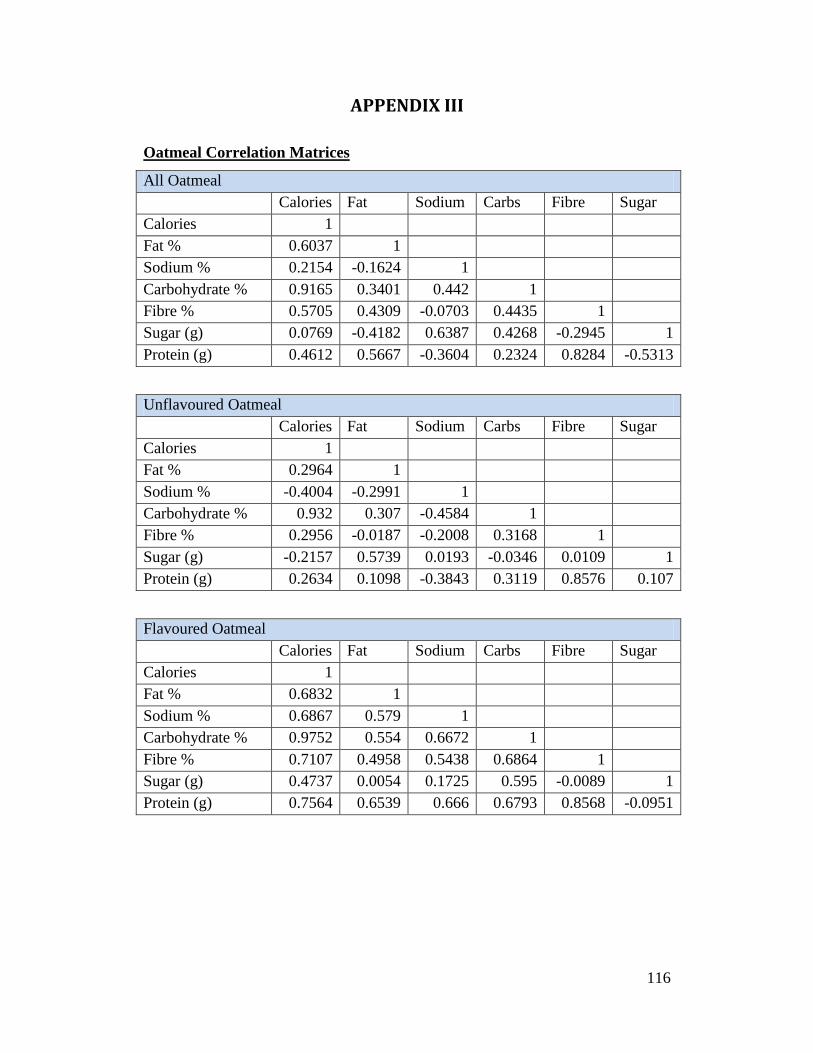

APPENDIX III. Oatmeal Correlation Matrices .. . . . . . . . . . . . . . . . . . . . . . . . . 116

APPENDIX IV. Summary Statistics of Standardized Nutri tional

Information of Oatmeal Model by Flavour Category .. . . . . . . . . . . . . . . . . 117

APPENDIX V. Store-Level Regression Results for Milk ($/L) .. . 119

APPENDIX VI. Store-Level Regression Results for Milk ($/L) .. 120

APPENDIX VII. Store-Level Regression Results for Oatmeal

($/350g) .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126

APPENDIX VIII. Price per Litre of Milk by Volume ... . . . . . . . . . . . . . . 130

APPENDIX IX. OLS Estimates of Retail Milk Model for Québec

and Gatineau, with Brand Base ($/L) .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

APPENDIX X. OLS Estimates of Retail Milk Model by Price -

Regulated Markets, with RMAAQ-based Regions, Brand Base and

Local Brand Regions ($/L) .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 135

vi

LIST OF TABLES

Table 1. Descriptive Statistics of Retail Milk UPCs by Attributes ...................... 39

Table 2: Descriptive Statistics of Retail Oatmeal UPCs by Attributes ................ 43

Table 3. Definitions of Variables for the Hedonic Price Model for Milk ............ 48

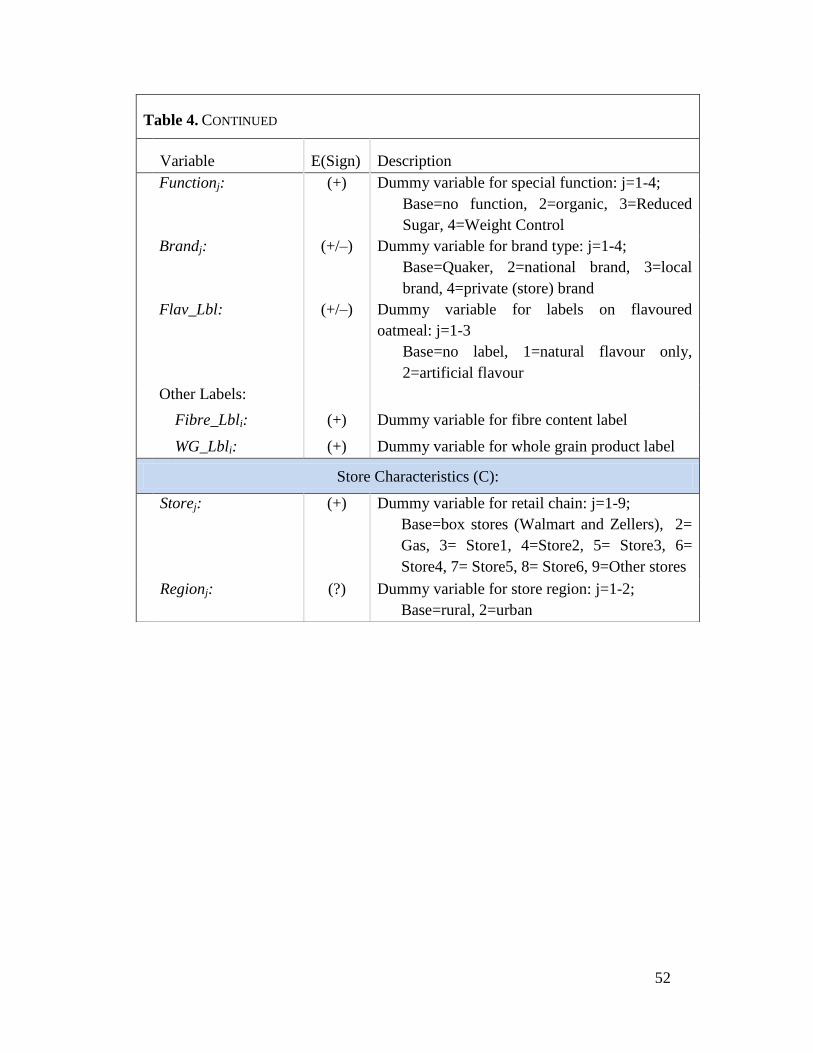

Table 4. Definitions of Variables for the Hedonic Price Model for Oatmeal ...... 51

Table 5. OLS Estimates of the Linear Hedonic Model for Milk ($/L) ................ 58

Table 6. OLS Estimates of the Semi-log Hedonic Model for Oatmeal ($/350g) 65

Table 7. Store-Level Results for Milk ($/L) ........................................................ 76

Table 8. Store-Level Results for Oatmeal ($/350g) ............................................. 82

Table 9. OLS Estimates for Retail Milk by Price-Regulated Markets, with

RMAAQ-based Regions ($/L) .............................................................................. 87

Table 10. Predicted Values for Price-Regulated Milk ......................................... 90

Table 11. Classification of Local Brands According to Brand Name .................. 94

LIST OF FIGURES

Figure 1: Front-of-Package and Back-of-Package Food Labels (CFIA, 2010) ..... 7

1

CHAPTER I: INTRODUCTION

Overview and Problem Statement 1.1

Today‘s consumer, shopping in the average supermarket, faces a choice set

of over 38,000 items (FMI, 2010). In this competitive environment, one of the

ways firms distinguish and advertise their products is through front-of-package

labels. As with any decision, firms which maximize profits should ensure that the

marginal revenue from each additional label equals or exceeds its associated

marginal cost (Golan et al., 2010). These decisions are set within a policy and

socio-economic context which provides constraints and opportunities for firms.

For instance, the Canadian Food Inspection Agency regulates claims found on the

front of product packages as well as the elements contained within the Nutrition

Facts Table. On the other hand, consumer trends clearly influence firms‘ labelling

decisions. The U.S. sales in 2010 of products with health claims related to

production methods and nutrient content health attributes, such as ―organic,‖

―natural‖ and indications of the presence of fat and fibre, ranged from $56.6

million for foods with plant steroid claims to $46.6 billion for product with fat

claims (Nielsen, 2010). Front-of-package labels constitute an element driving

consumer purchasing decisions by providing information that is beyond tangible

product attributes such as package type and volume.

The hedonic pricing method can be used to quantify the level at which

front-of-package information influences consumer decisions. This method is

based on the consumer demand theory of Lancaster (1966) which argues that

consumer demand is for the attributes of a good rather than the physical good as a

whole. By dividing a commodity into its characteristics, a good‘s price can be

decomposed into the sum of the marginal yield of each attribute multiplied by its

marginal implicit price (Ladd and Suvannunt, 1976). Using this approach,

researchers have assessed the implicit value of food attributes including the value

of food safety claims (Li and Hooker, 2009), beef steak brands (Schulz et al.,

2010) and the organic attribute for baby food (Smith, et al. 2009).

2

Store type can also influence product price. Consumers can control their

choice set according to where they shop because different retail chains carry

different products. For example, box stores (supercenters) constitute the latest

advancement in food retailing (Stiegert and Hovhannisyan, 2009) by offering a

combination of food retailing, general merchandising and pharmacies.

Additionally, the development of private (store) labels has enabled retailers to

assume a more active role in the food marketing system (Berge‘s Sennou, 2006).

A cross-store analysis can provide insight into consumer preferences for store

type and front-of-package labels. Within-chain analysis of the location of retail

chains can also provide insights into differences in pricing strategy: as the

consumer base and level of competition differ between urban and rural stores,

retail chains may adjust product prices accordingly.

Given the prevalence of front-of-package labels in today‘s market

(LeGault et al., 2004), this study used the hedonic pricing method to estimate the

implicit values for food product attributes, focusing on characteristics identified

on product labels.

Objectives 1.2

Although several studies have examined the relationship between a particular

food attribute and product price, there is a gap in the literature regarding the

implications of different types of labelling claims, which advertise the presence or

absence of food attributes, on food choice. Beyond the Nutrition Facts table, food

manufacturers incorporate composition, quality, quantity, nutrient content and

health claims on the front of food packages (CFIA, 2010). This study uses Nielsen

MarketTrack data to examine whether there were implicit values attributed to

front-of-package labelling statements, and whether food attribute values vary

according to retail and regional markets. Regulations concerning the display and

content of front-of-package claims can also influence product price. The product,

fluid milk, was chosen to evaluate how regulations set by the Régie des marchés

agricoles et alimentaires du Québec impacted the hedonic price models. Product

attributes for a second relatively homogenous good, oatmeal, were also analyzed

3

to potentially uncover cross-product trends. Specifically, the objectives of the

study were:

1) To evaluate whether there are significant implicit prices for labelling

statements that advertise the presence, absence, or level of an attribute in

food products;

2) To estimate whether implicit prices for food product characteristics,

including labelling statements, differ by store type;

3) To estimate whether implicit prices for food product characteristics,

including labelling statements, differ by store location;

4) To determine the presence of cross-product trends by comparing results

for the previous objectives for two food products.

Structure of Thesis 1.3

The second chapter consists of a literature review which is separated into

two parts. First, an introduction to food labelling familiarises the reader with

Canadian labelling policy and reviews the literature of food labelling and its

impact on consumer purchasing decisions. The second half of Chapter II reviews

hedonic theory, the proposed methodology for analysing the implicit prices

associated with food product attributes.

Chapter III presents the Nielsen MarketTrack data by outlining the

descriptive statistics of milk and oatmeal. Also, the hedonic pricing models are

specified in preparation for hypotheses testing.

Chapter IV presents the regression results for the empirical models and

discusses the interpretation of their coefficients. A first step in the analysis was to

conclude whether there were significant implicit prices associated with product

labels, based on the model estimates. Next, retail chains were grouped together to

test whether implicit prices were identical at the store level. Subsequently,

regional differences were investigated in a similar manner.

The final chapter summarizes findings of this study. The initial objectives

are revisited and limitations to this research project are discussed. Suggestions for

further research are also made in this chapter.

4

2 CHAPTER II: LITERATURE REVIEW

Overview 2.1

The literature review is divided in two parts. Part I reviews food labelling

policy and previous literature on consumer purchasing decisions. An emphasis is

placed on how economists use stated and revealed preference methodologies to

determine consumers‘ willingness to pay (WTP) for food attributes by using

labelling claims as proxies for the presence or absence of these attributes.

Although claims such as ―pesticide-free,‖ ―organic‖ and ―lactose-free‖ only

appear on front-of-packages, consumers can verify several nutrient content claims

with the Nutrition Facts panel on the back of packages. If nutrient content claims

are accounted for, but information on the Nutrition Facts panel is omitted, the

values consumers place on labelling statements and information on the back of

food packages are implicitly aggregated. Thus, both nutrient content information

and claims were accounted for in this study to examine whether buyers

differentiate between front-of-package labels and information found on the

Nutrition Facts table, and whether different types of front-of-package labels elicit

different responses.

In Part II, the choice of methodology is identified and hedonic theory is

presented. Empirical estimations of hedonic models in the food labelling literature

demonstrate varying uses of functional form, choice of variables and data sources

amongst researchers. In addition to labelling statements, several attributes for

product brand, origin and retail store type are considered.

5

PART I: PREVIOUS LITERATURE

Canadian Food Labelling Policy 2.2

In Canada, the 2003 Guide to Food Labelling and Advertising (Guide)

establishes guidelines for food claims, including alcoholic beverages, in order to

meet with the requirements set by acts and regulations within the Canadian

legislative framework: the Food and Drugs Act, the Food and Drug Regulations,

the Consumer Packaging and Labelling Act and the Consumer Packaging and

Labelling Regulations. The Guide was developed to assist industry to comply

with legislation and protect consumers, and outlines the basic labelling

requirements, advertising requirements and the mandatory and voluntary elements

within the Nutrition Facts table (CFIA, 2010).

The Nutrition Facts table is a mandatory food label that is displayed on a

product package, along with its common name, net quantity, dealer name and

address, list of ingredients and durable life date. A Nutrition Facts table should

contain information regarding serving size, calories and 13 core nutrients. In

addition, there are conditions under which food manufacturers must declare

additional nutrients beyond ―core‖ information contained in the Nutrition Facts

table, and regulations surrounding how the table should be presented on the

product. For example the table must be positioned on a continuous surface, and

mustn‘t be placed in an area where it will be destroyed when consumers open the

food package (CFIA, 2008).

In terms of voluntary labelling statements, the Guide defines three types of

claims (CFIA, 2010):

(1) Composition, quality, quantity and origin claims include statements with

words such as ―fresh,‖ ―homemade,‖ ―true,‖ ―real,‖ ―organic,‖ and

―reconstituted.‖ The main requirements set for food manufacturers are to

refrain from misleading impressions, misleading descriptions and to

provide accurate information to consumers. Overall, the Guide does not

6

provide specific definitions in terms of the context in which terms

regarding food composition and quality are used, but approaches the issue

in a more pragmatic way by providing examples of good practices.

(2) Nutrition content claims are statements that describe the level of a

nutrient in a food product. Regulations concerning this type of claim aim

to provide consumers with consistent information in order to compare

foods easily. For example, the Guide establishes conditions that must be

met when making comparative claims involving similar foods. Unlike

labelling policies in the United States, Canadian policy prohibits implied

nutrition content claims made on their own, and they must immediately

precede or follow an expressed nutrient claim. For instance, an implied

statement such as ―semi-salted‖ must be accompanied by an approved

statement for foods defined as low in sodium or salt, such as ―low in

sodium‖, which is an indirect claim on the level of sodium in a food, or

―contains less than X mg salt per serving‖, which is a direct claim on the

level of sodium in a food (DoJ, B.01.501, 2010).

(3) Health claims state or imply a relationship between the consumption of

food, or an ingredient in the food, and health. The Guide classifies health

claims into three categories: disease risk reduction claims, function

claims and general health claims. Function claims describe how the

consumption of food, or component of a food, has an impact on the

normal functions or biological activities of the body, and should be

distinguished from the structure/function claims category in U.S.

labelling policy.

Since claims are usually displayed on the front of a product‘s package, while

the Nutrition Facts table is generally positioned on the back, the two elements are

sometimes referred to as front-of-package and back-of-package labels,

respectively (Figure 1).

7

Figure 1: Front-of-Package and Back-of-Package Food Labels (CFIA, 2010)

U.S. Food Labelling Policy 2.3

In the United States, two principal federal laws govern food products

under the Food and Drug Administration‘s (FDA) jurisdiction: the Federal Food,

Drug, and Cosmetic Act and the Fair Packaging and Labeling Act. Food claims

are separated into three broad categories (FDA, 2008):

(1) Nutrient content claims explicitly or implicitly characterize the level of a

nutrient found in a food product. An expressed nutrient content claim is

any direct statement about the level (or range) of a nutrient in the food,

e.g., ―low sodium‖ or ―contains 100 calories.‖

(2) Health claims on food labels may express or imply a relationship between

the consumption of a food or one of its components and a disease or

health-related condition. For example, implied health claims include

symbols, such as a heart symbol, that suggest a relationship between

consumption and health.

(3) Structure/Function claims are reserved for dietary supplements, and

describe the role of a nutrient or dietary ingredient in terms of how it

The Nutrition Facts table is

also referred to as ―back-of-

package‖ information

―Front-of-package‖ labels

must meet requirements set

by the CFIA

8

affects or maintains structure or functions in humans. The label statement

cannot bear a disease claim, in which case the marketed product will be

subject to regulation as a drug, unless it qualifies as an authorized health

claim.

The FDA does not govern all food labelling policies: foods that contain

organic labelling statements fall under the jurisdiction of the U.S. Department of

Agriculture (USDA). The National Organic Program (NOP) regulates the

standard to any producer who wants to sell an agricultural product as organically

produced. Also, certain labels remain unchecked by both agencies. Currently,

there are no restrictions surrounding the use of ecological- or sustainable-type

food labels, such as ―no drugs or growth hormones used,‖ ―free range,‖ or

―sustainably harvested‖ (USDA, 2008). Moreover, the FDA Food Labeling

Guidance and Regulations do not cover issues such as microbial food safety,

pesticide residues and the use of preservatives (FDA, 2008).

In general, Canadian laws and regulations concerning front-of-package

claims are more stringent than those in the United States. These standards are

sustained by ensuring that foreign foods displaying claims are evaluated by the

CFIA‘s Label and Recipe Registration Unit prior to being exported to Canada.

Typically, Canada does not permit imported meat and poultry products containing

claims such as ―natural‖, ―antibiotic free‖, ―hormone free‖ and ―chemically free‖

(CFIA, 2011).

Food Labelling History and Prevalence 2.4

Since the enactment of the Pure Food and Drug Act in 1906, food

labelling laws and regulations have evolved in the 20th

century to ensure the

provision of true and non-misleading claims to consumers. In 1990, the Nutrition

Labeling and Education Act (NLEA) was passed to: standardize the Nutrition

Facts panel and serving sizes, make its presence mandatory on processed goods,

and strictly regulate labelling statements (Geiger, 1998). Benefits of mandatory

labelling include product reformulation, product innovation and changed

consumer behaviour, and costs of labelling are mostly borne by consumers who

9

pay for government management and regulation (Drichoutis et al., 2006). Whether

mandatory labelling has led to net benefits or costs to society has been debated.

On one hand, Zarkin et al. (1993) estimated that the NLEA resulted in savings of

up to $100 billion in medicare costs in two decades, and the FDA (1993) affirmed

that the benefits of improved food labelling brought forth by the NLEA

outweighed the cost of implementation and compliance. On the other hand,

researchers have found that consumer preferences and purchasing patterns for

frozen meals (Mojduszka, 2001) and their search for nutritional information

(Balasubramanian and Cole, 2002) did not change significantly after the

implementation of the NLEA.

As of 1976, the FDA has studied the prevalence of labelling for processed

and packaged foods in the United States through the Food Label and Package

Survey (FLAPS). The agency‘s 12th

survey was conducted with 2000-2001 data

from Information Resources Inc. (IRI), and found that almost 100% of sampled

packaged products displayed a nutrition label. Survey results indicated that

approximately 5% of packaged food products in the United States displayed a

health claim and/or a structure/function claim, while one third of products sold

displayed nutrient content claims. The study also included information pertaining

to the prevalence of health claims by product group (such as hot cereals, seafood,

meat/poultry substitutes), and nutrient content claims by type of claim and by

product group. However, the average number of claims per product group isn‘t

specified (LeGault et al., 2004). Surprisingly, the survey showed that the

percentage of products with nutrient content claims for total fat, saturated fat,

cholesterol, dietary fibre and sugar decreased from 1997 to 2001. A subsequent

study found that 12% of products now contain nutrient content claims about the

level of trans fats (Brandt et al., 2009). The authors propose that changes in the

prevalence of front-of-package claims are due to industry responding to changes

in consumer tastes and preferences for low-fat and fat-free foods (LeGault et al.,

2004). However, the following sections indicate that current research suggests it

is still unclear whether consumers optimize their search for food attributes

through the use of labelling statements.

10

Food labelling and consumer purchasing decisions 2.5

Neoclassical economists traditionally justify government intervention in

order to correct market failures, which may be caused by imperfect market

competition, externalities and imperfect information. Since nutritional and health

claims cannot be verified during or after consumption, consumers can not search

for the bundle of attributes that maximizes their utility. Thus, food labelling

policies are a means for governments to provide consumers with information

pertaining to nutritional and health characteristics of foods to transform credence

attributes into search attributes, and help prevent ―lemons‖ in the market

(Drichoutis et al., 2006).

Both consumers and producers face trade-offs when using food labels:

consumers who engage in information search behaviours face a search/time trade-

off; consumers who read nutritional labels face a taste/nutrition trade-off

(Drichoutis et al., 2006). For instance, consumers may balance the immediate

gratification offered by a tasty chocolate with the long-run benefits of a nutritious

banana. For food manufacturers, the cost of displaying labels on food packages

has to be balanced against additional revenue; deciding what labels to display is a

complex decision given the number of potential attributes and differences in

consumer preferences (Golan et al., 2001).

The study of consumer‘s use of labelling statements is broad, and contains

detailed research on topics such as the profiles of consumers likely to use

nutritional information, and the relationship between label use and dietary change.

Articles can be found in marketing journals, food science journals as well as

economics journals. The following two sections reviews evidence of the impact of

food labelling on consumer purchasing decisions, and categorises results as either

experimental evidence or economics studies.

11

2.5.1 Experimental Studies

In experimental design settings, the study of the impact of labelling

statements on consumers may be divided into six categories: (1) consumer

knowledge and awareness of dietary issues; (2) sources of information and trust;

(3) consumer perception, attitudes and beliefs of claims; (4) communication

framing and context; (5) consumer reactions to disease-reduction or health

enhancement and; (6) consumer purchase decisions. Pothoulaki and

Chryssochoidis (2009) explain how the first five components ultimately influence

consumer purchase decisions: a consumer‘s purchase decision is a function of the

communication framing and context as well as the disease/risk prevention claims

that alter the impact of health claims. The weight consumers place on health

claims is a function of consumer knowledge and awareness of dietary issues,

sources of information and trust, and a consumer‘s perceptions, attitudes and

beliefs.

Alfieri and Byrd-Bredbenner (2000) conducted a study with 150 women

who were the principle food purchasers in their household to assess how labelling

statements impact purchasing decisions. Through 15-minute face-to-face

interviews, the researchers evaluated whether the participants could locate and

manipulate data on the Nutrition Facts table as well as assess nutrient content

claims and health claims. They found that over 60% of women regularly read

Nutrition Facts labels and that over 90% of surveyed women stated that the

Nutrition Facts table always or sometimes impacted their food purchasing

decisions. However, participants performed poorly in terms of their understanding

of health claims: they could not determine which of five health claims could

appear on a pasta mix with a Nutrition Facts label. The authors proposed that

consumers may find health claims hard to validate because there are no concrete

data available to verify the accuracy of health claims and that certain consumers

may be sceptical of health claims on product packages.

Alternatively, Lee et al. (2007) provided evidence for the taste-health or

taste-nutrition trade-off consumers experience when purchasing food (Drichoutis

12

et al., 2006). The authors conducted focus groups to study the impact of health

claims on the taste of breakfast cereals. They found that certain health and

nutrient content claims, specifically the promotion of soy as a healthy ingredient,

may be undermined by taste stigmas. The conclusions from these experiments

also indicated that health claims may play dual roles: first, indicating the presence

of a nutrient to consumers, and second, informing them about the potential health

impacts of consuming the nutrient or food product. This means that studies on

labelling statements need to be attentive to the role of both nutrient content claims

and health claims; ignoring health claims potentially biases observations.

Garretson and Burton (2000) collected data from 382 primary household

grocery shoppers through a mail survey to compare how consumers value two

different sources of information, in terms of two nutrients (fat and fibre), on mock

frozen dinner food package. In particular, the authors aimed to understand how

statements on the front (health and nutrient claims) and back (Nutrition Facts

table) of a product‘s package influenced consumers‘ attitudes and purchase

intentions, perceived disease-related risks and trust of information. Results from

their multivariate analyses of variance indicated that front-of-package claims

about fat and fibre, as well as Nutrition Facts table information concerning fibre

levels, did not positively affect brand attitude and purchase intent. However,

information on the Nutrition Facts table regarding fat affected consumers‘

decision-making. The study concluded that consumers tend to rely on Nutrition

Facts tables rather than nutrient claims and health claims. Also, when the

information on claims and Nutrition Facts tables diverge, consumers tend to trust

claim information less.

Teratanavat et al. (2004) used a marketing approach and also found that

consumers rely primarily on the Nutrition Facts table, rather than on health and

nutrition information on the front of food packages. In an experimental setting,

over three hundred undergraduate students were shown one of several versions of

front and back panels of a box of wheat crackers on a computer monitor, and were

subsequently asked a series of questions concerning the effect of the information

on their attitudes, understanding and buying intention. A univariate analysis of

13

variance was conducted, and results suggested, similar to Garretson and Burton

(2000), that the presence of claims on the front of food packages does not lead

consumers to evaluate product quality more carefully and that students are able to

distinguish healthy from unhealthy products whether claims are present or absent.

Although consumers tend to prefer products with claims than products

without claims (Teratanavat et al., 2004), the role of these claims on consumer

purchasing behaviour is unclear. Research indicates that consumers who use

labels tend to shop by comparing the Nutrition Facts table of similar types of

products and to focus on the components of fat, energy and carbohydrates within

the label (Higgingson et al., 2002a and 2002b). Worsley (1996) surveyed

supermarket shoppers in Australia and found that consumers were mostly

interested in information concerning additives, health impacts and fat.

2.5.2 Economics

In the economics literature, studies are undertaken to investigate the role

of information, either on front-of-package claims or Nutrition Facts tables, on

consumer choice. One method to estimate this impact is with the stated preference

approach, which relies on answers to carefully designed surveys to elicit

consumer choices and values. An alternative way to measure the values

consumers place on this information is through revealed preference methods,

which are based on actual market behaviour. The economics literature is rich on

research pertaining to consumer demand for food characteristics, but relatively

sparse in terms of consumer valuation of nutrient content labelling statements.

2.5.3 Stated Preference Literature

Hu et al. (2006) explain that when analyzing the utility consumers derive

from different bundles of goods, ―the random utility model assumes that

individuals make choices based on the attributes of the alternatives and that

overall utility is decomposed into systematic and random (or error) components‖

14

(p. 1034). The explainable components may be parameterised as attributes that

pertain to choice options, characteristics that pertain to individual s, interactions

of choice option attributes with the individual characteristics and interactions of

individual characteristics with choice option intercepts (Louviere, 2001).

For example, Teratanavat and Hooker (2006) found a positive demand for

health attributes for a novel functional food. Data were collected from over 1700

households in Ohio through a mail survey using a choice experiment design,

where subjects chose among 3 products (conventional tomato juice, tomato juice

plus, tomato juice plus with soy) and an opt-out option in each of four scenarios.

Products were described according to four attributes: health benefits (zero, single

or multiple), organic/conventional ingredients, natural or fortified nutrients, and

four price levels. The different levels of health benefits were presented in a format

similar to health claims found on fronts of packages, such as ―rich in nutrients

that may reduce the risk of prostate cancer,‖ rather than as a percentage increase

or decrease to human health, such as ―5% increase in the risk to your health‖ used

in the surveys of Yen (2009) and Roy (2009). The authors developed two random

utility models (a mixed and conditional logit model) to analyze their discrete

choice data. They discarded the conditional logit model as it incorrectly assumes

homogenous preferences across respondents, and determined that consumers, on

average, prefer a single health benefit to multiple health benefits, and natural to

fortified nutrients.

While some researchers argue that labelling regulation transforms

credence attributes into search attributes (Drichoutis et al., 2006), there is

evidence that certain claims are regarded as credence attributes to consumers. A

choice experiment study by Olynk et al. (2010) showed that consumers were

willing to pay a premium for verification of livestock production process

attributes, such as animal rearing, handling and housing practices. Consumers‘

WTP varied across attributes verified, but also according to verifying entity. For

example, the WTP for pasture access was highest for verification by the USDA,

followed by verification by the producer, consumer groups and private third

15

parties. This is a clear example of how sources of information and trust

(Pothoulaki and Chryssochoidis, 2009) affect consumer valuation of food labels.

Many researchers who use stated preference methods consistent with

random utility theory implicitly assume that all differences in consumers‘ choices

are due to the explainable components listed above. However, research suggests

other factors besides unobserved taste heterogeneity, such as context effects,

reference point effects, availability effects and superstition effects, influence

consumer purchasing decisions (Hu et al., 2006). For instance, Hu et al. (2006)

studied how context effects and consumers‘ reference points on product price and

genetically modified ingredients influence purchasing behaviour in the case of

packaged, sliced bread. The authors surveyed 437 consumers by distributing three

different surveys with different labelling contexts (mandatory labelling, voluntary

labelling, and no specific labelling requirement) and asked them to choose

between two products (plus an opt-out option) characterized by four attributes

(brand name, type of bread, ingredients, price). Their results indicate that both

context effects and reference dependence are factors, besides taste heterogeneity,

that influence consumer decision-making. This is in line with findings outside

economics that suggest that communication framing and context influence

consumer purchase decisions (Pothoulaki and Chryssochoidis, 2009).

2.5.4 Revealed Preference Literature: Hedonic Pricing Method

The use of labelling statements in hedonic pricing models is used

primarily as a proxy for the presence, absence or level of an attribute in food

products, in order for researchers to determine the implicit price of selected food

attributes. When front-of-package statements can not be cross-examined with

information on the Nutrition Facts panel, then the implicit price consumers place

on the food attribute and on the labelling statement coincide.

For example, Li and Hooker (2009) analyzed food safety claims and their

influence on supply-side (agribusiness) price. They examined cross-category

valuation of claims for two product categories (spoonable yogurts, meat and

16

poultry products) using parametric and non-parametric hedonic models. Unlike

most researchers who assume a perfect competition market structure, the authors

included a product innovation level variable to proxy for product differentiation

and uniqueness. For spoonable yogurts, preservative free and organic claims were

associated with significant price premiums, while Kosher-certified and pesticide

free claims were not. For meat and poultry products, the authors tested the

significance of E. Coli free, natural and antibiotic free claims, and found that only

the latter two were statistically significant. Since none of these claims can be

verified with the Nutrition Facts panel, purchasers must rely on front-of-package

statements that indicate attribute presence or absence. For the statistically

insignificant Kosher-certified claim, the authors suggest that, while the claim had

no impact on product price, it may have marketing advantages. Li and Hooker

also propose that the incidence at which claims are found on products relates to its

statistical significance: the pesticide free and E. Coli free claims were featured on

a limited number of yogurts and meats, respectively, and firms may have had a

limited ability to monitor them.

Alternatively, Chang et al. (2010) estimated the marginal implicit prices

consumer placed on the production methods of retail eggs. Using retail scanner

data of quarterly egg sales across the entire U.S., and of weekly sales from two

regional markets, the authors‘ semi-log hedonic price model estimated that

production attributes such as cage-free, free-range and organic command a

significant price premium. Although Chang et al.‘s (2010) model controlled for

egg color, size, packaging, brand label and time, results from a Chow test

indicated strong regional differences in price premiums for production attributes.

While several studies on consumer preferences focus on relatively

unprocessed foods such as retail beef (e.g. Ward et al. 2008; Parcell and

Schroeder, 2007; Schulz et al., 2010), Ahmand and Anders (2011) studied

Canadians‘ preferences of highly processed chicken and seafood products. Retail

price ($/lb) per item per store was explained according to four categories of

dummy variables: brand, package size, meat cut (for chicken) or species (for fish),

and process form (such as barbecue and souvlaki). In discussing their results,

17

Ahmand and Anders suggested two additional variables that may account for

differences in relative pricing across processed seafood products: store-level

characteristics and front-of-package labels.

When front-of-package claims can be verified with back-of-package

information, it is important to distinguish between both effects. An example

where consumer valuation of labelling statements and valuation of nutrients are

not differentiated is Muth et al.‘s (2009) study of breakfast foods and cereals. The

authors used Nielsen Scantrack data and built a semi-log hedonic price regression

model to determine whether labelling statements were associated with increases in

consumer WTP. The explanatory variables used in the regression analysis

included: package size, store brand, product brand and labelling statements. By

omitting to control for differences in the nutrient composition of foods, Muth et

al.‘s conclusions do not pertain solely to consumers‘ preferences for front-of-

package information, since labelling statements may reflect characteristics of the

Nutrition Facts table. For example, the authors‘ regression results suggested that

consumers positively value carb-conscious labelling statements. Without

controlling for differences in the nutrient composition of breakfast foods and

cereals, their results may suggest that consumers value certain foods that are low

in carbohydrates and fat, rather than labelling statements about carbohydrates and

fat.

In contrast, Gulseven and Wohlgenant (2010) built a hedonic metric model

to estimate the values of product attributes for fluid milk. They matched Nielsen

Homescan Data with information about food attributes using the USDA Nutrient

Database to construct a dataset of front-of-package claims and nutrient

information (back-of-package information) for each product. Among the authors‘

findings are that lactose-free, cholesterol-free, organic and soy attributes are

highly influential on product price.

For products with relatively homogenous nutrition characteristics, it may

not be necessary to control for nutrient information. While Gulseven and

Wohlgenant (2010) used continuous variables to represent elements found on the

Nutrition Facts table, Ward et al. (2008) analysed the implicit value of ground

18

beef by categorizing packages according to levels of fat (lean percentage), and

categorize steak products by USDA quality grade, thus assuming away other

nutritional differences. The price per pound of retail beef was modeled using both

linear and semi-log functional forms, and front-of-package explanatory variables

included: ―no antibiotics added,‖ ―no hormones added,‖ ―all natural,‖ ―source

verified‖ and ―guaranteed quality.‖ Label results were inconsistent across the two

product groups considered (ground beef and roast/steak products) and functional

form. Additionally, the sign on certain significant variables was counterintuitive:

a statistically significant negative price premium was associated with the ―no

hormones added‖ and ―all natural‖ claims. Ward et al. (2008) suggest the discount

associated with these claims may have been attributable to the fact that the model

already controlled for brand name, and the combined consideration of both

variables would lead to nonexistent price premiums for products displaying those

labels.

Choice of Methodology 2.6

The survey of evidence from experimental studies in the food science and

marketing arena, as well as from economics research using the stated preference

approach, shows considerable variation in the way consumers react to food labels,

and suggests consumers may not positively value information claims. Cowburn

and Stockley (2004) conducted a literature review of consumer understanding of

nutrition labelling, and concluded that most of the evidence is based on

experiments that take place in non-realistic settings and employ subjective

measures. In their search for information, the authors considered only 9 out of 103

studies to be of high or medium-high quality, and stated that there exists a lack of

evidence to ―build up a picture that accurately reflects consumers‘ habitual use of

nutrition labelling‖ (p.26). Consequently, one way to study consumers‘ value of

front-of-package labelling statements is through the revealed preference approach,

which studies actual consumer choices rather than their answers to survey

questions or their actions in experimental settings. The approach also circumvents

framing effects of surveys, as described in Hu et al. (2006).

19

In terms of methodology, the review of previous work suggests discrete

choice models are generally used to determine consumers‘ stated preference for

food attributes, while the hedonic pricing methodology is preferred in the revealed

preference literature. Each model is based on a different set of assumptions;

central to hedonic models is the concept of a continuous function relating the

price of a good to its attributes. Conversely, the discrete choice approach suggests

individuals maximize their utility given a set of products and their attributes

(Mason and Quigley, 1990). Cropper et al. (1988) conducted a comparison of both

approaches by simulating equilibia in housing markets, and found both models‘

performance similar in estimating the marginal value of an attribute. However,

their multinominal logit model was better suited to estimate non-marginal changes

in attribute levels.

The hedonic pricing method was chosen as it better responds to the

objectives of evaluating the existence of positive implicit prices for front-of-

package labels, and determining whether these implicit prices differ by store and

region. The appropriateness of the hedonic price model as the chosen

methodology is supplemented in the following section, where hedonic theory is

presented along with three general issues related to its use: selection of the good,

selection of its attributes and choice of functional form.

Part II: Hedonic Theory

Hedonic Theory 2.7

Lancaster‘s (1966) new theory of consumer demand, in which he

postulates that consumers derive utility not from goods themselves but their

characteristics, responds to limitations within neoclassical utility theory: it

explains why consumers derive utility from commodities, and provides a way of

predicting demand for new commodities (Smith et al., 2009). The use of the

hedonic method in economics can be divided into two general fields: the first

group analyzes and adjusts observed prices for changes in product quality, while

20

the second group analyzes the relationship between individual attributes and their

implicit prices (Hulten, 2003).

Building on Lancaster‘s theory, Rosen (1974) developed the hedonic

model in the case of a perfect competition market structure with a continuum of

products. In his seminal paper, he considers a good Z, such as an individual food

product, composed of n attributes represented by the vector .

Bundled together, the characteristics are priced at the unit price of the product:

( ) ( ) . Rosen shows that the marginal implicit price for an

attribute zi, represented by ( ) ( )

, characterises optimal consumer and

producer behaviour.

On one side, consumers maximize their utility through the purchase of a

unit of the food product and a composite good x, subject to a budget constraint

(where y represents income):

( ) ( ) ( )

By normalizing the price of the composite good and assuming a perfectly

competitive market, the first-order condition of the utility maximization problem

is:

This means that the marginal rate of substitution between an attribute of the food

product and the composite good is equal to the marginal price of the attribute.

Hence, given their income level, consumers reveal through their purchase of the

good Z that their marginal willingness to pay for an attribute is equal to its

marginal price.

On the other hand, producers maximize their profit by producing an

amount M of the product Z. Their total revenue assuming perfect competition is

( ), and costs of production are represented by ( ) where β represents

the firm‘s variables in the cost-minimizing problem, such as factor prices. Firms

maximize their profits by choosing the amount M to produce:

21

( ) ( )

A condition derived from the cost-minimization problem is that the

marginal cost of producing an attribute is equal to its marginal price:

Thus, from the condition where the market clearing price paid for a

product is a function of its associated attributes and the marginal implicit price

paid per attribute, Rosen (1974) demonstrates that the marginal implicit price

represents optimal behaviour by both sides of the market, where the relative value

of the attributes to consumers is equal to the marginal cost of production of that

attribute:

In this equilibrium condition between optimal producer and consumer

decisions, the amount of attributes demanded by the consumer is met by the

amount supplied by the producer. From this point, the demand and supply

schedules for different attributes may be derived, which is generally referred to as

second stage analysis. The papers reviewed and the discussions below pertain to

the estimation of consumer attribute values rather than deriving Rosen‘s second

stage structural supply and demand equations.

Hulten (2003) notes the distinction between Rosen‘s interpretation of

marginal implicit prices with the utility-based interpretation associated with

Lancaster‘s (1966) new theory of consumer demand. Rosen (1974) considers the

price of a good to be an envelope linking equilibriums between consumers and

producers - tangencies between consumers‘ demands for, and firms‘ supplies of,

product characteristics. Lancaster‘s consumer-based view maintains that implicit

prices relate to consumers‘ WTP for attributes and overlooks producer behaviour.

22

2.7.1 Three Central Considerations

There are three general issues related to the use of the hedonic regression

model (Hulten, 2003). The first and second topic deal with the selection of the

good and the selection of its attributes, while the third issue relates to the choice

of functional form.

2.7.2 Selection of the Good

Product differentiation models are subject to the problem of distinguishing

goods as products in their own right, in contrast to goods as a subclass of a given

product category. For instance, does one treat a particular brand of ice cream as a

good and consider the different flavours offered as characteristics, or does one

include near-substitutes and treat ice cream as a good regardless of the brand? Is

it reasonable to also include further substitutes such as popsicles and frozen

desserts? Theory indicates that a common hedonic function should apply for all

items in the class of goods considered, which is reasonable when the range of

items is small. However, this benchmark is violated whenever dummy variables

are included (Hulten, 2003). Overall, the choice of food product depends on the

range available in the data as well as other constraints that may be imposed, such

as the selection of a homogeneous good, the selection of a functional food, or the

selection of a packaged product with several close substitutes.

The two retail commodities chosen to study cross-product preferences in

front-of-package labelling were milk and oatmeal because they are relatively

homogenous products in terms of nutrient composition. This minimizes the

number of explanatory variables employed for back-of-package information and

directs attention towards the information found on font-of-package food labels. In

addition, fluid milk and oatmeal have few direct substitutes and can be reasonably

defined as goods in their own right.

23

2.7.3 Selection of Attributes

Drawing on the definition of implicit marginal price provided by Rosen

(1974), attributes selected should influence both consumer and producer

behaviour. Although labelling statements that pertain to elements in the Nutrition

Facts panel can be considered to be elements of consumer and producer decision-

making, other labelling statements such as disease-reduction health claims are less

obvious (Hulten, 2003). This is perhaps why a large branch of applied

econometrics ignores the interaction between producers and consumers and

restricts analysis to the price faced by consumers, and consumer welfare (Diewert,

2003).

Assuming consumers are not identical, the implicit prices obtained from

hedonic regression are not fixed parameters but a weighted average that may

change over time due to changing preferences and changing mix of consumers.

The implicit prices may also change over time because of non-separability: if

attributes defining good A cannot be dissociated with attributes defining good B,

which are outside the hedonic function, the implicit marginal price may change

due to changes in the relation between goods A and B. Missing attributes within

the hedonic function create a similar problem (Hulten, 2003). For these reasons,

econometric models are most successful when applied to goods that have additive

and non-conflicting attributes (Drichoutis et al., 2006).

While there are conventional characteristics used in hedonic pricing

models for houses, where variables such as lot size, living area, number of

bathrooms and neighbourhood attributes are recurrent from study to study, food

products are heterogeneous goods with differing attributes. Thus, there is no

combination of attributes that applies to all food products. Researchers using

scanner data deal with large databases with thousands of observations and hence

thousands of degrees of freedom, and thus have a tendency to use a relatively

large number of variables in hedonic pricing models. Hidano (2002) suggests

three categories of explanatory characteristics to estimate a hedonic price function

for housing markets: (1) characteristics of the commodity itself; (2) attributes that

24

affect the quality of the commodity from the outside and (3) the general

environment. Similarly, attributes of retail food products can be categorized as

product characteristics, store characteristics and those concerning the general

environment.

2.7.3.1 Product Characteristics:

While product characteristics are commodity-dependent, recurring attributes are

described below:

Package size/Servings per package: A continuous variable may be used when

the differentiated products come in different sized packages.

Bulk: Muth et al. (2009) used a dummy variable to capture price discounts

associated with multi-packaging for granola and yogurt bars, and found a

significant negative implicit price.

Package Type: Consumer may distinguish food products according to the way

they are packaged; for example, eggs are sold in cardboard, plastic or

Styrofoam packages (Chang et al., 2010).

Nutritional Attributes: Nutritional attributes such as labelling statements are

best represented as dummy variables. Otherwise, nutritional information on

Nutrition Facts panels such as protein, carbohydrate and fat content, as well as

percentage daily recommended intake of cholesterol, sodium and vitamins and

minerals may be captured by continuous or binary variables.

Child Product Attribute: Li and Hooker (2009) included a binary variable to

capture the implicit price of spoonable yogurts which are positioned towards

children. However, the attribute was found to be statistically insignificant.

Production Method Attributes: Several credence attributes can be attributed to

this category, which include organic ingredient claims, pesticide-free claims,

antibiotic-free claims, as well as claims pertaining to production methods

according to particular religious frameworks, such as kosher foods.

Region of Origin: Steiner (2004) performed a hedonic pricing analysis on

Australian Wines and included explanatory variables for the different regions

25

of origin. Region of production can also be a production method attribute, and

several studies, reviewed in Hu et al., (2011) support that foods with region of

origin labels, such as ―locally produced,‖ command a price premium over

products without such claims.

Brand: Diewert (2003) developed arguments for and against using brand

dummy variables as independent variables. Those who argue against including

brand dummy variables believe that if all the important attributes of the food

product are included in the regression, the brand variable is superfluous and

increases multicollinearity. Conversely, proponents deem that brand dummies

capture attributes that are hard to specify, such as reliability, degree of

consumer knowledge about the product through advertising, and availability.

Recent research on pork and beef prices suggests brand premiums exist

(Parcell and Schroeder, 2007; Schulz et al., 2010). Schulz et al. (2010)

categorized beef brands according to three dimensions: longevity, prominence

and positioning. Brand longevity captures consumer recognition, while brand

prominence signals whether the product is distributed locally, regionally or

nationally. The authors used four categories for brand positioning: special

brands, program brands, store brands and other. Brand prominence captured

price premiums associated with local claims, while brand positioning captured

the implicit price of special production practices.

Additionally, brands may implicitly signal the presence of nutrients, as

shown by Huffman and Jensen‘s (2004) study on margarines. In valuing the

implicit price of nutritional enhancements in margarine, the authors employed

a dummy variable for a specific brand of margarine to signal for the presence

of plant stenol esters and unsaturated sterols.

Brand-specific effects can also be regrouped by using a dummy variable

per brand. For instance, Maguire et al. (2004) restricted their data to

observations of four prominent brand-name baby foods, with a dummy

variable to represent each. This decreases multicollinearity in contrast to

Schulz et al.‘s (2010) approach. Another method is to regroup brands in

simpler categories, such as store brand and major brand (Chang et al., 2010).

26

This alternative captures the price premiums and discounts associated with

private labels and well-known brands, and allows variables that account for

explicit label claims to capture price premiums associated with labelling

information.

2.7.3.2 Store Characteristics

Akin to including neighbourhood characteristics when determining

housing prices, hedonic pricing models for retail food products can incorporate

store attributes. As stated by Ward et al. (2008), this implies that store

characteristics are associated with a consumer‘s overall shopping experience.

Food products are sold in different store types. Categories include grocery

stores, discount stores, specialty shops, ethnic shops, convenience stores, co-ops

and markets. Each store type may be represented with its own dummy variable, or

a single dummy variable may be used to separate purchases from grocery stores

from all other types of specialty shops. Studies have shown that store

characteristics capture a portion of a product‘s price. For instance, Maguire et al.

(2004) used both a continuous variable for square footage of grocery stores and

dummy variables for other types of food outlets to estimate the price premium for

organic baby food. Parcell and Schroeder (2007) found that different store types

explain the price of different pork cuts: for example, supercenters have a

significant impact on the price of steak while warehouses command a positive

price premium for pork chops, ribs and roast. In general, one can expect, as per

Ward et al.‘s (2008) results, that products are priced lower in discount stores and

warehouse club stores than in grocery supermarkets and specialty shops.

The product itself may give an indication as to which types of outlets are

significant explanatory variables. For example, convenience stores sell baby food

at a higher price than other store types, and thus convenience stores are a

significant variable in Maguire et al.‘s (2004) study. On the other hand,

convenience stores do not often sell meat, and that store type was not a significant

variable for Parcel and Schroeder‘s (2007) hedonic model for retail pork cuts.

27

2.7.3.3 Other attributes:

Region: There may be regional differences to the general environment in

which products are bought and sold. For instance, Ward et al. (2008) gathered

data from three metropolitan areas to study the implicit value of beef product

attributes and assigned dummy variables for each city to account for cost-of-

living differences. An alternative way to analyze retail differences is to run

regressions per region of interest. Chang et al. (2010) ran two regressions of

their hedonic model per metropolitan area and conducted a Chow test to reject

the hypothesis that the implicit prices of retail egg attributes were equal across

locations.

Price Index/Time of Year: Hidano (2002) argues that the hedonic approach

must be based upon cross-sectional data according to the theory of

capitalization hypothesis: if a good‘s price is a function of its attributes, that

price can differ over time, such as in the stock market, or over space, such as

in the housing market. Hedonic theory is based on price differentials of a good

at one time in the market, and, as such, is based upon cross-sectional

capitalization rather than time-series capitalization. In practice, there may not

be sufficient data for one time period to perform a hedonic analysis and

therefore, time adjustments should be performed.

If the product studied may be subject to seasonal pricing patterns, monthly

or seasonal dummy variables may be used to capture these variations.

Alternatively, a market price indicator can be used to adjust for changing price

levels over time. For instance, Schulz et al. (2010) used data that spanned over

a 5-year period to study retail steak price. To account for changing prices over

time, the authors calculated weekly weighed average steak prices based on

their scanner data. Temporal variables are mostly used in the case of fresh

produce and meats, whose prices are known to vary. Packaged food prices, on

the other hand, don‘t tend to change during the study period.

28

2.7.4 Functional Form

Theory provides little guidance regarding the functional form to choose

when performing hedonic regressions (Steiner, 2004; Malpezzi, 2002). In general,

the functional form for a hedonic pricing model is not known a priori and

consequently, some researchers argue that the choice of functional form for the

hedonic price function should remain an empirical matter.

In light of the growing number of researchers who chose the functional

form of hedonic models using goodness of fit criterion, Cropper et al. (1988)

designed a study to provide some a priori indication of the functional form that

would most accurately estimate marginal attribute prices. The authors aimed to

identify the optimal choice of functional form for hedonic price functions in the

housing market context. Six forms of the hedonic price function were tested:

linear, semi-log, log-log, quadratic, linear and quadratic functions of Box-Cox

transformed variables. These results were compared with known utility function

bids for houses with given attributes. Cropper et al.‘s conclusions are divided into

two contexts: when all attributes are observed, linear and quadratic Box-Cox

forms perform best. However, in the case where product attributes in the

statistical analysis were incomplete or proxy measures for the quality of the

product were used, the linear, semi-log, log-log and linear Box-Cox functions

performed better than quadratic and quadratic Box-Cox functions. Lastly, the

authors suggested, based on the results of their simulations, that the linear Box-

Cox and linear forms were best suited for hedonic pricing analysis.

With respect to the analysis of food attributes, the choice of functional

form for hedonic pricing models is predominantly linear or semi-log. Since

dummy variables are often used to identify the presence or absence of attributes,

the log-log form is an unsuitable option. Semi-log and linear functional forms

each have strengths and weaknesses and the Box-Cox transformation model can

help steer the selection of either functional form.

29

2.7.4.1 Linear model

The linear model links a good with its attributes by representing price as a

function of its characteristics plus a random error term:

The linear model is considered by some to be unrealistic because it implies

that an attribute‘s implicit price is independent of other characteristics and

displays zero variance across sample observations (Rosen, 1974). Also, when

dealing with empirical issues, a non-linear form is preferred when potentially

dealing with heteroskedasticity (Steiner, 2004). However, linear specifications are

easy to interpret, as a unit increase in an attribute causes the price to rise by the

amount equal to the attribute‘s coefficient.

An example where a linear regression model is used (and justified) is

Schulz et al.‘s (2010) hedonic analysis of the value of beef steak branding using

retail scanner data. The authors considered that the attributes of steak are

separable and additive, estimated the implicit prices of retail steak characteristics

using a linear and log-linear model, and obtained quantitatively similar results.

Likewise, Maguire et al. (2004) estimated the price premium for organic

baby food using a linear hedonic model by arguing that the characteristics of baby

foods, such as stage, type and flavour, can be found and purchased in any

combination of attribute bundles. In proposing that the attributes of baby foods

vary independently from each other, the authors utilized a linear model to perform

their analysis. Their choice of functional form also insinuates that the assumption

of constant implicit marginal price is applicable for the food attributes in their

study and that consumers are unlikely to experience diminishing marginal utility

through the use of the food product or over the total quantity of baby food

consumed. In contrast, Steiner (2004) chose the semi-log functional form to

perform a hedonic price analysis of Australian wines because it was considered

that the marginal implicit prices were non-linear and bundling constraints were

present for wine attributes.

30

2.7.4.2 Semi-log model

The semi-log model is represented by the log of the price of a good as a

function of its defining attributes and a random error term:

One property of the semi-log form in the food labelling context is that the

coefficient measures the percent change in the price of food as a result of a unit

change in a continuous variable attribute (Steiner, 2004). However, where