A Guide of Federal Funding Disaster Relief for those affected by Super Storm Sandy

Upload

rafael-fisherCategory

view

25download

0description

A Guide of Federal Funding Disaster Relief for those affected by Super Storm Sandy

Monmouth County Division of Planning

Overlap in Funding Eligibility

1 - Individual Assistance

3 - Increased Cost of Compliance

5 - Hazard Mitigation

7 - Other Federally-funded Programs

(e.g. USDA, HHS,DOL, VA, SSA, USACE)

8 – Public Assistance

6 - Community Development Block Grant

– Disaster Recovery(CDBG-DR) (HUD)

4 - Small Business Administration Loans (SBA)

2 - National Flood Insurance Program

Disaster Relief Matrix - IndividualIndividual Property Owner/Homeowner/Renter

Secondary Home or Vacation Property

Primary Residence

In a Presidentially-declared Disaster Area

YESYESSecondary homes & vacation properties do not qualify for Federal Disaster Relief Aid

NO Federal Disaster Relief

Aid Not Applicable

In a Presidentially-declared Disaster Area

Register with FEMA Maintain Standard Flood Insurance Policy (SFIP)

Register with SBA Register with local government / community

Hazard Mitigation Assistance Program

Register with agency distributing CDBG-DR

funds

Non-Profit Organizations

YESYESMay qualify

for IHP grant program,

other FEMA disaster

assistance & to receive access to

other Federal Assistance program

NOOther sources for

compensation must be used to replace or repair

damaged building and personal

property including insurance policies dependent upon qualifications & limitations , any available private funding sources, personal funds,

etc.

YESYESFile claim with your insurance

company for settlement

NOAll costs come out of pocket

YESYES NOMay not

qualify for more

funding

YESYESMay be able to

obtain grant funding for elevation,

demolition or acquisition

NOMitigation projects handled privately

YESYESMay be able to obtain grant

funding for repair, re-habilitation relocation, acquisition

& other eligible

projects

NORepair, re-habilitation relocation, acquisition

& other eligible projects will be

handled privately

YESAble to

take advantage

of a valuable resource that may

be able to help with

your disaster recovery unmet needs

NOMissing out on a valuable resource to help

you with your

disaster recovery unmet needs

ApprovedApprovedLoan

money becomes

available for disaster -related

improve-ments

ICCMay qualify for the program if home is

found more than 50% substantially damaged

Not Approved

Sent back to FEMA for

review of applicable

grant funding

Will be required to get SFIP if FEMA

IHP grant is accepted

YESYESPrimary Residences do qualify for

Federal Disaster Relief AidSee below for available programs

NO Federal Disaster Relief

Aid Not Applicable

Failure to apply for SBA Assistance could disqualify

you from receiving CDBG-DR funding

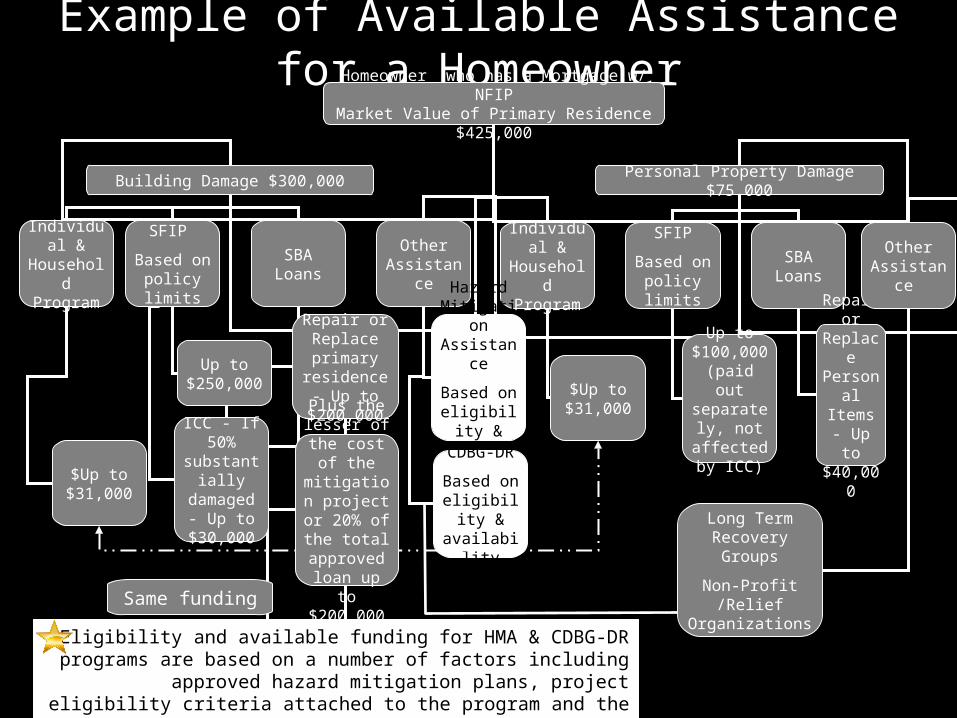

Example of Available Assistance for a HomeownerHomeowner who has a Mortgage w/ NFIP

Market Value of Primary Residence $425,000

Building Damage $300,000 Personal Property Damage $75,000

Individual & Household Program

SFIP

Based on policy limits

SBA LoansIndividual & Household Program

SFIP

Based on policy limits

SBA Loans Other Assistance

Hazard Mitigation

Assistance

Based on eligibility & availability

CDBG-DR

Based on eligibility & availability

Up to $100,000 (paid out

separately, not affected

by ICC)

Repair or Replace Personal

Items - Up to $40,000

$Up to $31,000

$Up to $31,000

Up to $250,000

ICC - If 50% substantially

damaged - Up to $30,000

Repair or Replace primary residence - Up

to $200,000

Eligibility and available funding for HMA & CDBG-DR programs are based on a number of factors including approved hazard mitigation plans, project eligibility criteria

attached to the program and the amount of funding available.

Other Assistance

Long Term Recovery Groups

Non-Profit /Relief Organizations

Plus the lesser of the cost of the mitigation project or 20%

of the total approved loan up to $200,000

Same funding

Connections between Federal Funding Options

2-NFIP/ SFIP

Insurance Programs

4-SBA Loans

3-Increased Cost of

Compliance

1-Individual Assistance

Grant

Individual & Individual & HouseholdsHouseholds

Other Needs &

Expenses/

Personal Property

Building PropertyCoverage

6-CDBG-DR

5-Hazard Mitigation

Grant (404)

7-Other Federally-

funded Projects

8-Public AssistanceGrant (406)

State & State & Local Local

Government Government & Nonprofit & Nonprofit

OrgsOrgs

Economic Revitalizatio

n

Acquisitions

Repairs/ Replacemen

t/ Rehabilitatio

n

Temporary Housing

Can be used as

non-Federal match funds

Hazard Mitigation Planning

HazardMitigatio

n Projects

Administrative/

Management CostsPersonal

PropertyCoverage

Debris RemovalEmergency Protective

MeasuresRoads & Bridges

Water Control FacilitiesBuildings & Equipment

UtilitiesParks, Rec. Fac, & Other

Fac.

House ElevationHouse RelocationHouse DemolitionFloodproofing

(non-residential or approved resident.

exception)

Home & Personal Property

Business Physical Disaster

Economic InjuryMil. Res. E.I.

1-Individual & Household Assistance Program Eligibility Eligible Participant

You are located in a federally declared disaster area.

You have filed your insurance claim or your property is not covered by insurance

It is your primary residence, where you live most of the year

You are not able to live in your home Your or someone you live with is a US citizen, non-

citizen national or qualified alien Ineligible Participant

The home is not a primary residence (i.e. it is a second home or vacation home)

You have refused assistance from your insurance provider

Your losses are business–related Your expense resulted from precautionary

evacuation activities – you were able to return home immediately after the incident

You have adequate rent-free housing that you can use

The damaged home is located in a community that does not participate in the NFIP – in this case the flood damage would not be covered, however you may qualify for rental assistance or other needs not covered by flood insurance (all Monmouth Co. towns participate except for Shrewsbury Twp.)

Eligible Costs/Uses – to help with critical expenses that cannot be covered in other ways Temporary Housing (e.g. rental assistance or

government provided housing unit) Repair damages not covered by insurance & to

make the damaged home safe, sanitary & functional.

To help homeowner with the cost of replacing their destroyed home

Other Need for necessary & serious expenses (e.g. medical, dental, funeral, personal property, transportation, moving/storage)

Limitations IHP will not cover all of your losses from damage to

your property. IHP is not intended to restore your damaged

property to pre-disaster condition – it is to return to a functional structure.

By law, IHP cannot provide you for losses that are covered by your insurance.

IHP does not cover business-related losses Appeals

You may appeal any decision (e.g. eligibility, amount or type of aid provided late applications, request to return money or questions regarding continuing help) postmarked within 60 days of FEMA decision letter date.

1-Individual & Household Assistance Program Eligibility Key Notes

If you do not use the money as explained by FEMA, you may not be eligible for any additional help & may have to give the money back

Disaster help is usually limited to up to 18 months from the date of the Presidentially-declared disaster

This is a grant which does not have to be repaid pending proper use of funds

The funds are tax-free The funds are not counted as income or a

resource for determining eligibility for welfare, income assistance or income-tested benefit programs funded by the Federal government

The funds may not be reassigned or transferred to another person

You must keep receipts or bills for 3 years to demonstrate how all of the money was used in meeting your disaster-related need

IHP and Flood Insurance If your insurance claim is delayed 30+ days

from the time you filed, FEMA may find you eligible to award you funds as an advance which would be paid back upon receiving your insurance settlement

If your maximum insurance settlement is insufficient to meet your disaster-related needs & you still have unmet disaster-related needs – you may write FEMA and request additional assistance

If you have exhausted your insurance settlement’s maximum Additional Living Expenses (ALE) & you still have unmet disaster-related needs – you may write to FEMA and request additional assistance

The FEMA Helpline is available to help you locate an available rental resources in the disaster area. 1-800-621-FEMA

Online housing resources: FEMA Housing Portal New Jersey Housing Resource Center Socialserve.com

2 - National Flood Insurance Program (NFIP) Eligible Participants

All owners of eligible property (a building and/or its contents) located in a community participating in the NFIP

Standard Dwelling (Single Family House) General Property (5 or more family

residential building & non-residential buildings)

Residential Condominium Building Association

Owners and Renters Standard Flood Insurance Policies (SFIP)

1-year term 2 types of Coverage

Building Property Personal Property

Ten percent of a dwelling’s building coverage may be applied to a detached garage.

Residential detached garages used, or held in use, for residential business or farming are not covered under the dwelling policy. These detached garages and other accessory structures must be insured under a separate policy.

Key Notes The National Flood Insurance Reform

act of 1994 requires individual in Special Flood Hazard Zones (SFHZ) who receive disaster assistance for losses to real or personal property to purchase & maintain flood insurance coverage for as long as the live in the dwelling

Identify the flood zone the structure is located in using Flood Rate Insurance Maps (FIRM)

Find out if your community participates in the NFIP

To determine if your property is in a SFHZ visit your local community planning or building permit department. Digital maps can be views on FEMA’s Region 2 website or FEMA’s Map Information Exchange.

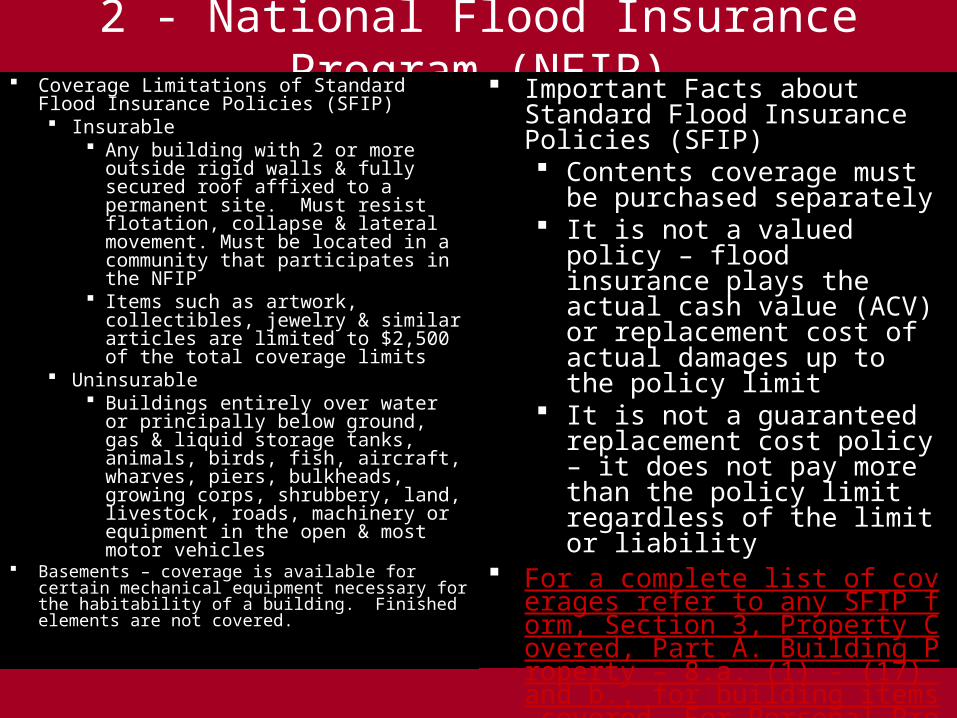

2 - National Flood Insurance Program (NFIP) Coverage Limitations of Standard Flood

Insurance Policies (SFIP) Insurable

Any building with 2 or more outside rigid walls & fully secured roof affixed to a permanent site. Must resist flotation, collapse & lateral movement. Must be located in a community that participates in the NFIP

Items such as artwork, collectibles, jewelry & similar articles are limited to $2,500 of the total coverage limits

Uninsurable Buildings entirely over water or

principally below ground, gas & liquid storage tanks, animals, birds, fish, aircraft, wharves, piers, bulkheads, growing corps, shrubbery, land, livestock, roads, machinery or equipment in the open & most motor vehicles

Basements – coverage is available for certain mechanical equipment necessary for the habitability of a building. Finished elements are not covered.

Important Facts about Standard Flood Insurance Policies (SFIP) Contents coverage must be purchased

separately It is not a valued policy – flood

insurance plays the actual cash value (ACV) or replacement cost of actual damages up to the policy limit

It is not a guaranteed replacement cost policy – it does not pay more than the policy limit regardless of the limit or liability

For a complete list of coverages refer to any SFIP form, Section 3, Property Covered, Part A. Building Property – 8.a. (1) - (17) and b., for building items covered. For Personal Property, refer to Section 3,. Property Covered, Part B. Personal Property – 4. a., b., & c.

3 - Increased Cost of Compliance (ICC) Eligible Participants

SFIP Policyholders who’s insured building meets 1 of 2 conditions:

1) Determined to be substantially damaged (damage exceeds more than 50% of the value of the building prior to damage occurring);

2) Meets the criteria of a repetitive loss structure

Eligible Costs/Uses ICC coverage only applies to flood-related damage Helps pay toward the cost to elevate, floodproof

(non-residential only), demolish or relocate the building

Basements can be floodproofed using ICC payments ONLY if the building is located in a community approved for residential basement exceptions by FEMA

FEMA allows NFIP policyholders to assign their ICC claim benefits to the community when they are participating in a FEMA-funded mitigation program. Coordination must be done through the community and the property owner. The ICC payment can be used to match a FEMA mitigation grant to cover the remaining costs.

Limitations The $30,000 maximum amount collected through

ICC is in addition to the amount the policy holder receive for physical damages by flood.

The total amount the policyholder receives for combined structural damage & ICC is always capped by the maximum limit of coverage established by Congress

Key Notes Helps pay for the cost to comply with state or

community floodplain management laws or ordinances from a flood even in which a building has been declared substantially damaged or repetitively damaged

ICC coverage is included in all Standard Flood Insurance Policies, however not all buildings are eligible (i.e. substantially damaged declaration). ICC is Coverage D in every SFIP.

ICC is only available for accessory buildings only when a separate flood insurance policy is written on that building (i.e. detached garage)

ICC does not extend to other remodeling or construction improvements that are not required to meet minimum floodplain management requirements

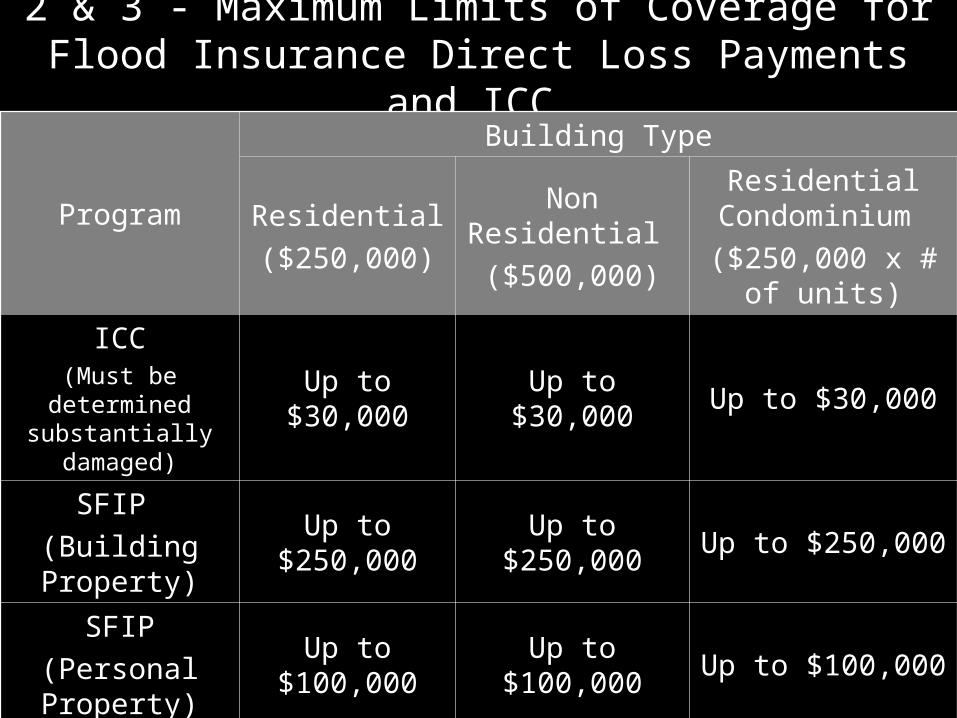

2 & 3 - Maximum Limits of Coverage for Flood Insurance Direct Loss Payments and ICC

Program

Building Type

Residential ($250,000)

Non Residential ($500,000)

Residential Condominium

($250,000 x # of units)

ICC(Must be determined

substantially damaged)Up to $30,000 Up to $30,000 Up to $30,000

SFIP (Building Property)

Up to $250,000 Up to $250,000 Up to $250,000

SFIP(Personal Property)

Up to $100,000 Up to $100,000 Up to $100,000

*Detached garages may be valued up to 10% of Building Property coverage; Other detached building must have own SFIP.

The maximum amount collectible under the SFIP for both the ICC payment and the direct loss payment (building claim) for flood cannot be greater than the maximum limits of coverage for that class of buildings authorized under the National Flood Insurance Act of 1968, as amended. Having an ICC claim does not affect a Personal Property claim which is paid separately.

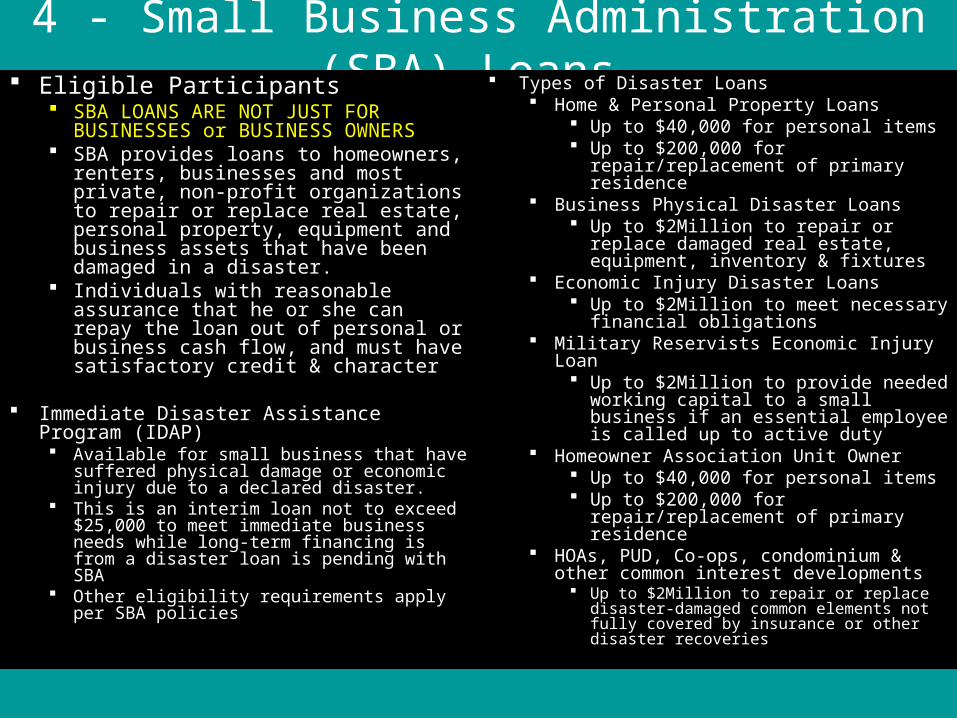

4 - Small Business Administration (SBA) Loans Eligible Participants

SBA LOANS ARE NOT JUST FOR BUSINESSES or BUSINESS OWNERS

SBA provides loans to homeowners, renters, businesses and most private, non-profit organizations to repair or replace real estate, personal property, equipment and business assets that have been damaged in a disaster.

Individuals with reasonable assurance that he or she can repay the loan out of personal or business cash flow, and must have satisfactory credit & character

Immediate Disaster Assistance Program (IDAP) Available for small business that have suffered

physical damage or economic injury due to a declared disaster.

This is an interim loan not to exceed $25,000 to meet immediate business needs while long-term financing is from a disaster loan is pending with SBA

Other eligibility requirements apply per SBA policies

Types of Disaster Loans Home & Personal Property Loans

Up to $40,000 for personal items Up to $200,000 for repair/replacement of

primary residence Business Physical Disaster Loans

Up to $2Million to repair or replace damaged real estate, equipment, inventory & fixtures

Economic Injury Disaster Loans Up to $2Million to meet necessary financial

obligations Military Reservists Economic Injury Loan

Up to $2Million to provide needed working capital to a small business if an essential employee is called up to active duty

Homeowner Association Unit Owner Up to $40,000 for personal items Up to $200,000 for repair/replacement of

primary residence HOAs, PUD, Co-ops, condominium & other

common interest developments Up to $2Million to repair or replace disaster-

damaged common elements not fully covered by insurance or other disaster recoveries

4 - Small Business Administration (SBA) Loans MOST DISASTER AID FROM THE

FEDERAL GOVERNMENT IS IN THE FORM OF LOANS FROM THE SMALL BUSINESS ADMINISTRATION (SBA)

ELIGIBILITY FOR OTHER DISASTER RELIEF FUNDS MAY BE AFFECTED IF YOU DO NOT FILL OUT AN APPLICATION FOR AN SBA LOAN

SBA loans can be used as non-federal matching cost share for hazard mitigation projects that individuals collaborate with local community on

Applying for a SBA loan does not require you to accept the funds, however not accepting the funds that you are eligible for may have an affect on other disaster relief funding

DO NOT miss the filing deadline by waiting for an insurance settlement

Key Points Under the Flood Disaster Protection Act of 1973 – a

loan recipient must obtain flood insurance if the proceeds of SBA financial assistance are used for property located in a special flood hazard area. This also applies to the business loan program regarding inventory, etc. contained in the building located in the special flood hazard zone.

In general SBA will not require collateral to secure a disaster home loan or physical disaster business loan of less than $14,000 or an economic injury loan of $5,000 or less. Even if you do not have the collateral, you will not be declined as long as the SBA is reasonably sure you can repay your loan

Misuse of SBA funds may result in criminal, civil or administrative action.

Loan Use Restrictions Restore or replace your primary home & your

personal or business property as nearly as possible to their pre-disaster condition, & within certain limits, to protect damaged or destroyed real property from possible future similar disasters

Secondary homes or vacation properties are not eligible for these loans

SBA cannot cover agriculture losses – contact USDA for recovery assistance

4 - Small Business Administration (SBA) Loan Categories

Home & Personal Property Loans

Business Physical Disaster Loans

Economic Injury Disaster Loan

Military Reservist Economic Injury Loan

Must be located in a declared disaster area & a victim of a disaster.

You don’t have to own a business. Non-primary properties are not

eligible. Can be a renter or homeowner

Business or NPO located in a declared disaster area & incurred

damage during the disaster.

Business or NPO located in a declared disaster area & incurred

damage during the disaster.

Provides funds to an eligible small business to meet operating expenses

because essential employee was called to active military duty.

Repair or replacement of primary residence to pre-disaster condition.

Repair or replace personal property (i.e. clothing furniture, cars, appliances, etc.).

Upgrades are not covered unless required by local building codes.

Repair or replacement of real property, machinery, equipment,

fixtures, inventory, leasehold improvements to pre-disaster

condition. Upgrades are not covered unless required by local building

codes.

Meet necessary financial obligations- expenses the business would have

paid if the disaster had not occurred. Not for refinancing long term debts or provide capital need prior to disaster.

Does not replace sales or lost profits.

Provide working capital needed until essential employee is released from

active duty. Lost income or profits are not covered. Not to be used in place of regular debt, refinance long-term

debt or expand business.

Credit/Collateral/InsurancePhysical loss loans over $14K must

be secured

Credit/Collateral /Insurance Physical loss loans over $14K must

be secured

Credit/Collateral /Insurance All EIDL loans over $5K must be

secured

Credit/Collateral /Insurance All MREIDL loans over $50K must be secured with reasonable assurance that a MREIDL will be repaid. Loans

over $50K must have proper insuranceInterest Rate: Unable to obtain credit

elsewhere -rate will not exceed 4%. Able to obtain credit elsewhere rate

will not exceed 8%.

Interest Rate: Unable to obtain credit elsewhere -rate will not exceed 4%. Able to obtain credit elsewhere rate

will not exceed 8%.

Interest Rate: Unable to obtain credit elsewhere -rate will not exceed 4%. Able to obtain credit elsewhere rate

will not exceed 8%.Interest Rate: 4%

Loan Terms & Amount Limits: Up to $40K for personal property; Up to

$200K to repair residence. Terms: up to 30 yrs; determined case-by-case.

Loan Terms & Amount Limits: Up to $2M. Repayment can be up to 30

years.

Loan Terms & Amount Limits: Up to $2M. Repayment can be up to 30

years.

Loan Terms & Amount Limits: Up to $2M, though if a major source of

employment SBA can waive limit..

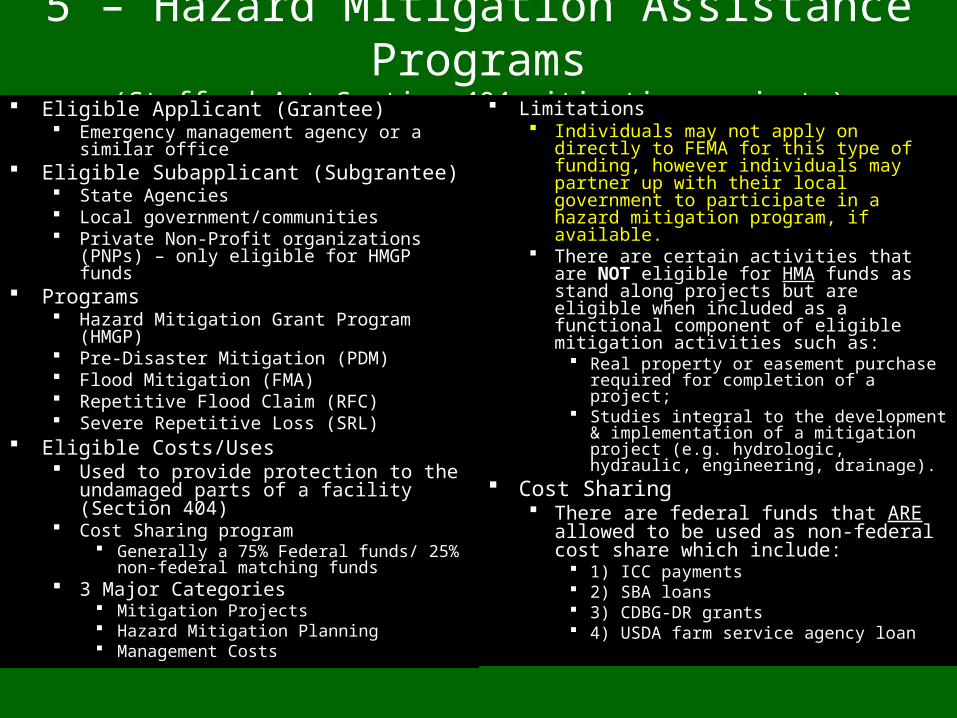

5 – Hazard Mitigation Assistance Programs(Stafford Act Section 404 mitigation projects)

Eligible Applicant (Grantee) Emergency management agency or a similar office

Eligible Subapplicant (Subgrantee) State Agencies Local government/communities Private Non-Profit organizations (PNPs) – only

eligible for HMGP funds Programs

Hazard Mitigation Grant Program (HMGP) Pre-Disaster Mitigation (PDM) Flood Mitigation (FMA) Repetitive Flood Claim (RFC) Severe Repetitive Loss (SRL)

Eligible Costs/Uses Used to provide protection to the undamaged

parts of a facility (Section 404) Cost Sharing program

Generally a 75% Federal funds/ 25% non-federal matching funds

3 Major Categories Mitigation Projects Hazard Mitigation Planning Management Costs

Limitations Individuals may not apply on directly to FEMA for

this type of funding, however individuals may partner up with their local government to participate in a hazard mitigation program, if available.

There are certain activities that are NOT eligible for HMA funds as stand along projects but are eligible when included as a functional component of eligible mitigation activities such as:

Real property or easement purchase required for completion of a project;

Studies integral to the development & implementation of a mitigation project (e.g. hydrologic, hydraulic, engineering, drainage).

Cost Sharing There are federal funds that ARE allowed to

be used as non-federal cost share which include:

1) ICC payments 2) SBA loans 3) CDBG-DR grants 4) USDA farm service agency loan

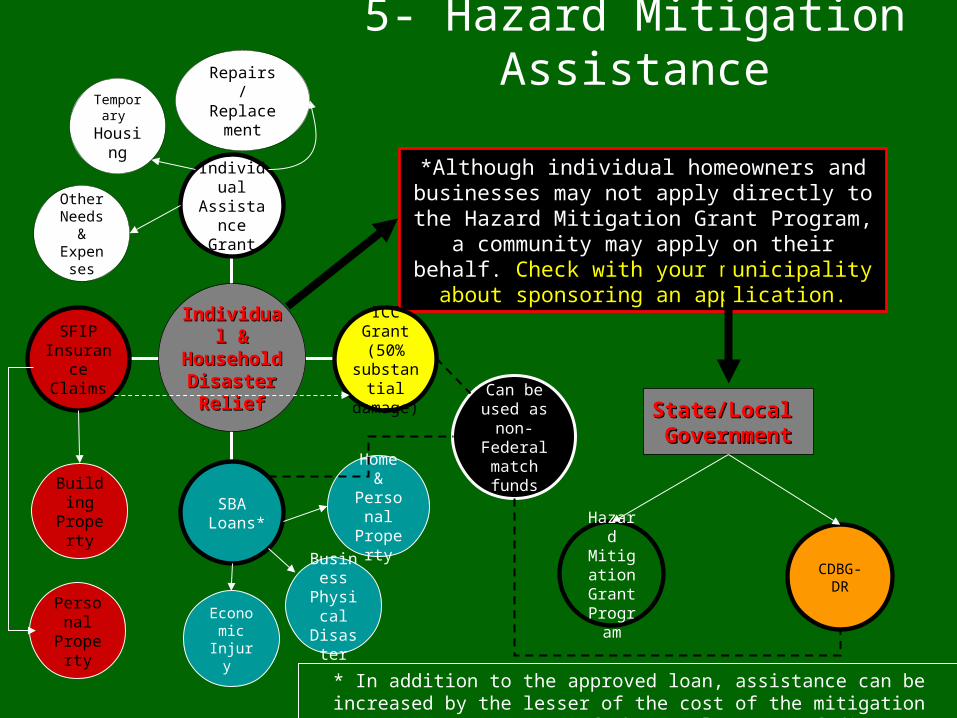

5- Hazard Mitigation Assistance

Business

Physical

DisasterEconomic Injury

Personal

Property

Temporary

Housing

*Although individual homeowners and businesses may not apply directly to the Hazard Mitigation Grant Program, a community may apply on their behalf. Check with your

municipality about sponsoring an application.

SFIPInsurance

Claims

SBA Loans*

ICCGrant (50% substantial damage)

Individual Assistance

Grant

Individual & Individual & HouseholdHousehold

Disaster Disaster ReliefRelief

Building Propert

y

Other Needs & Expense

s

Hazard Mitigation Grant Program

Can be used as

non-Federal match funds

CDBG-DR

Repairs/ Replacemen

t

State/Local State/Local GovernmentGovernment

Home & Personal Property

* In addition to the approved loan, assistance can be increased by the lesser of the cost of the mitigation measure or up to 20% of the total amount of disaster damage up to $200,000.

5 - Hazard Mitigation Funding available to help homeowners implement flood retrofitting projects

Hazard Mitigation Grant Program

Pre-Disaster Mitigation

Flood Mitigation Assistance

Repetitive Flood

Claims

Severe Repetitive

Loss

Projects fall into 3 basic categories: 1) Mitigation Projects, 2)Hazard Mitigation Planning & 3) Administrative Costs

5 - FEMA Hazard Mitigation Assistance Programs(Stafford Act Section 404 mitigation projects)

Hazard Mitigation Grant Program (HMGP)

Pre-Disaster Mitigation (PDM)

Flood Mitigation Assistance (FMA)

Repetitive Flood Claims (RFC)

Severe Repetitive Loss (SRL)

Ensure that the opportunity to take critical mitigation

measures to reduce the risk of loss of life & property from future disasters is not lost

during the reconstruction process following a

disaster.

Implement a sustained pre-disaster natural hazard mitigation

program to reduce overall risk to the

population & structures from future hazard

events

Reduce or eliminating claims under the National Flood Insurance Program

(NFIP).

Reduce flood damages to individual properties for which one or more

claim payments for losses have been made under flood insurance

coverage

Reduce flood damages to residential properties that have experienced

severe repetitive losses under flood insurance

coverage

Mitigations ProjectsHazard Mitigation Planning

Management Costs

Mitigations ProjectsHazard Mitigation Planning

Management Costs

Mitigations ProjectsHazard Mitigation Planning

Management Costs

Mitigations ProjectsManagement Costs

Mitigations ProjectsManagement Costs

Allocation is a sliding scale based on percentage of estimated total Federal

assistance under the Stafford Act excluding admin costs

Allocation based on consistency with applicable laws. FEMA will administer the program as directed by

Congress. Grants are competed for on a national

level

Allocation is based on the total number of NFIP insurance policies & total number or repetitive loss properties

FEMA will rank eligible mitigation project

subapplications on the basis of the greatest saving to the

NFIP

Allocation of funds based on the national percentage of

severe repetitive loss properties present within their

jurisdiction

5 - FEMA Hazard Mitigation Cost Share Requirements

ProgramsMitigation Activity

(% Federal/Non-Federal Share)

Management Costs (% Federal/Non-Federal Share)

Grantee Subgrantee

HMGP (Hazard Mitigation Grant Prog.) 75/25 100/0* -/-**

PDM (Pre-Disaster Mitigation) 75/25 75/25 75/25

PDM- subgrantee is a small impoverished community 90/10 75/25 90/10

FMA (Flood Mitigation Assistance) 75/25 75/25 75/25

FMA – severe repetitive loss property w/ Repetitive Loss Strategy 90/10 90/10 90/10

RFC (Repetitive Flood Claims) 100/0 100/0 100/0

SRL (Severe Repetitive Loss) 75/25 75/25 75/25

SRL – with Repetitive Loss Strategy 90/10 90/10 90/10

*Because available HMGP management costs are calculated as a percentage of the Federal funds provided, the non-Federal share is already accounted for. **Subapplicants should consult their State Hazard Mitigation Officer (SHMO) for the amount or percentage of HMGP subgrantee management cost funding their State has determined to be passed through to subgrantees.

6 – Community Development Block Grant – Disaster Relief (CDBG-DR) Eligible Grantee

States/local governments located in Presidentially-declared disaster areas. These communities must have significant unmet recovery needs and the capacity to carry out a disaster recovery program

Activities Funds must be used for: “…necessary expenses

related to disaster relief, long-term recovery & restoration of infrastructure, housing & economic revitalization…”

Each Activity must: Address a disaster-related impact (direct or indirect) in

a Presidentially-declared county for the covered disaster

Be a CDBG eligible activity (according to regulations and waivers)

Meet a National Objective 1. Benefit persons of low & moderate income, 2. aid in the prevention or elimination of slums or

blight 3. or meet other urgent community development

needs because existing conditions pose a serious & immediate threat to the health & welfare of the community where other financial resources are not available.

Funds can be used as the non-federal match for FEMA Public Assistance Projects, FEMA Hazard Mitigation Grant Program & USACE projects where not all funding has been fully appropriated to USACE or requires USACE to pay for the entire project.

Limitations Funds must supplement, NOT REPLACE, other

sources of federal disaster recovery assistance. Non-competitive, non-recurring Disaster Recover

grants that consider unmet needs by other Federal Disaster assistance programs

Examples of Eligible Costs/Uses Rebuild homes & infrastructure (i.e. [emergency]

reconstruction of essential water, sewer, electrical and telephone facilities) damaged by the disaster

Provide assistance to affected business owners (i.e. retain/create jobs)

Residential or commercial property buyouts/Buying damaged properties in a flood plain & relocating residents to safer areas

Floodplain mapping & landuse planning Elevating, floodproofing, outfitting with roof straps,

storm shutters, stronger materials Debris removal not covered by FEMA Code enforcement homeownership activities such as down payment

assistance, interest rate subsidies & loan guarantees for disaster victims;

Public services (generally limited to no more than 15 percent of the grant);

Planning & administration costs (limited to no more than 20 percent of the grant)

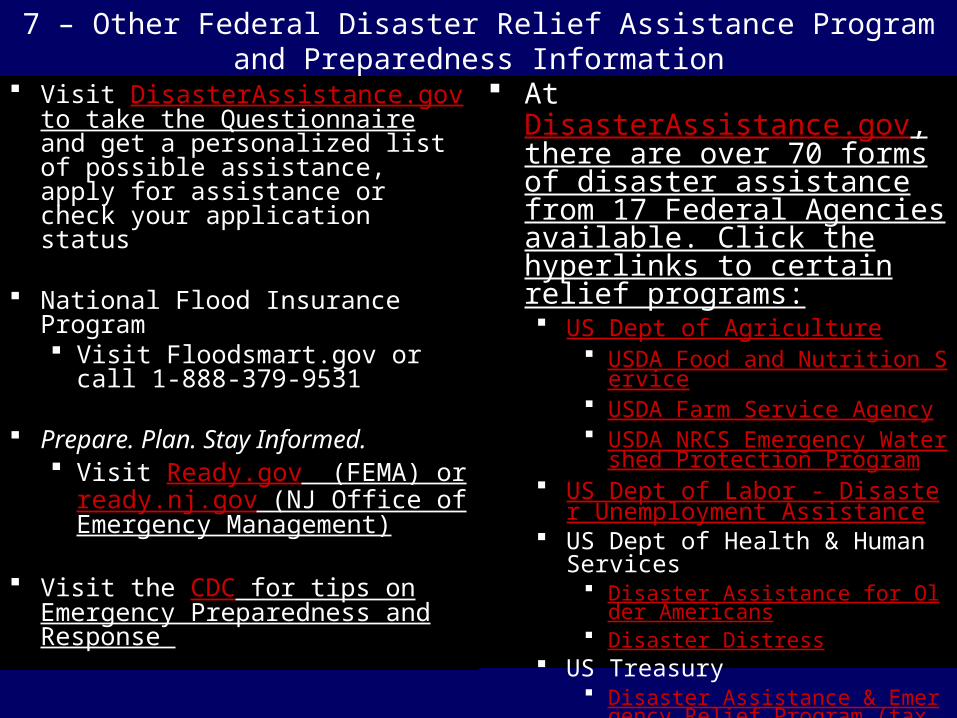

7 – Other Federal Disaster Relief Assistance Program and Preparedness Information

Visit DisasterAssistance.gov to take the Questionnaire and get a personalized list of possible assistance, apply for assistance or check your application status

National Flood Insurance Program Visit Floodsmart.gov or call 1-888-

379-9531

Prepare. Plan. Stay Informed. Visit Ready.gov (FEMA) or

ready.nj.gov (NJ Office of Emergency Management)

Visit the CDC for tips on Emergency Preparedness and Response

At DisasterAssistance.gov, there are over 70 forms of disaster assistance from 17 Federal Agencies available. Click the hyperlinks to certain relief programs: US Dept of Agriculture

USDA Food and Nutrition Service USDA Farm Service Agency USDA NRCS Emergency Watershed Pro

tection Program US Dept of Labor - Disaster Unemployment

Assistance US Dept of Health & Human Services

Disaster Assistance for Older Americans Disaster Distress

US Treasury Disaster Assistance & Emergency Relief Pr

ogram (tax counseling & assistance) Savings Bond Redemption & Replacement

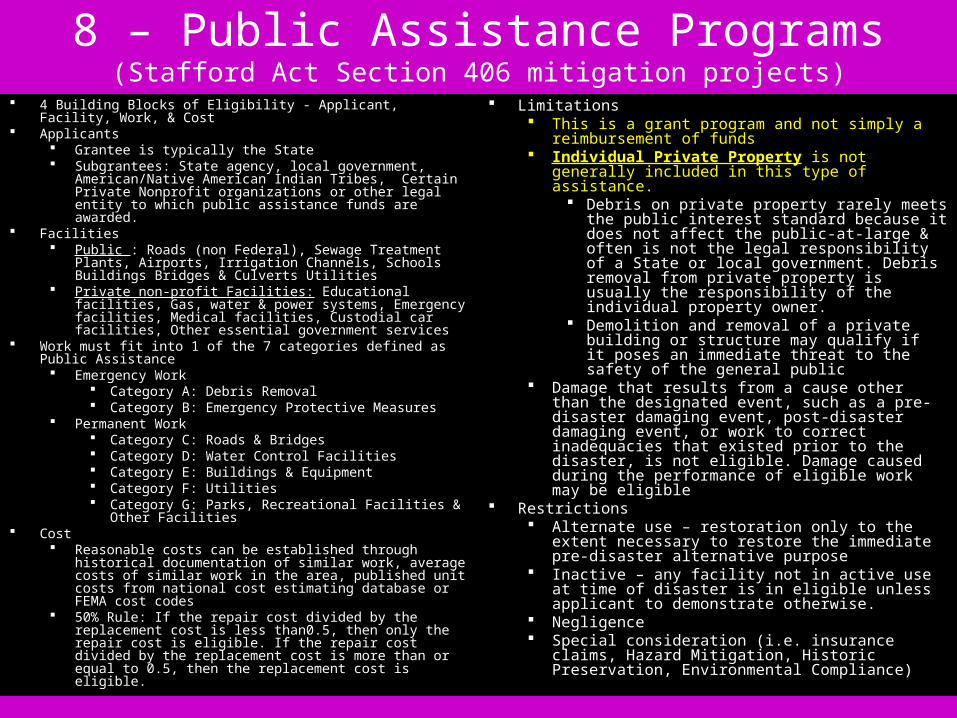

8 – Public Assistance Programs(Stafford Act Section 406 mitigation projects)

4 Building Blocks of Eligibility - Applicant, Facility, Work, & Cost Applicants

Grantee is typically the State Subgrantees: State agency, local government, American/Native

American Indian Tribes, Certain Private Nonprofit organizations or other legal entity to which public assistance funds are awarded.

Facilities Public : Roads (non Federal), Sewage Treatment Plants, Airports,

Irrigation Channels, Schools Buildings Bridges & Culverts Utilities Private non-profit Facilities: Educational facilities, Gas, water &

power systems, Emergency facilities, Medical facilities, Custodial car facilities, Other essential government services

Work must fit into 1 of the 7 categories defined as Public Assistance Emergency Work

Category A: Debris Removal Category B: Emergency Protective Measures

Permanent Work Category C: Roads & Bridges Category D: Water Control Facilities Category E: Buildings & Equipment Category F: Utilities Category G: Parks, Recreational Facilities & Other

Facilities Cost

Reasonable costs can be established through historical documentation of similar work, average costs of similar work in the area, published unit costs from national cost estimating database or FEMA cost codes

50% Rule: If the repair cost divided by the replacement cost is less than0.5, then only the repair cost is eligible. If the repair cost divided by the replacement cost is more than or equal to 0.5, then the replacement cost is eligible.

Limitations This is a grant program and not simply a reimbursement

of funds Individual Private Property is not generally included in

this type of assistance. Debris on private property rarely meets the public

interest standard because it does not affect the public-at-large & often is not the legal responsibility of a State or local government. Debris removal from private property is usually the responsibility of the individual property owner.

Demolition and removal of a private building or structure may qualify if it poses an immediate threat to the safety of the general public

Damage that results from a cause other than the designated event, such as a pre-disaster damaging event, post-disaster damaging event, or work to correct inadequacies that existed prior to the disaster, is not eligible. Damage caused during the performance of eligible work may be eligible

Restrictions Alternate use – restoration only to the extent necessary

to restore the immediate pre-disaster alternative purpose

Inactive – any facility not in active use at time of disaster is in eligible unless applicant to demonstrate otherwise.

Negligence Special consideration (i.e. insurance claims, Hazard

Mitigation, Historic Preservation, Environmental Compliance)

Sandy Affected ResidentsApril 1, 2013 APPLICATION DEADLINE!!!

For FEMA and SBA Assistance

Not filling out an SBA loan application may affect youreligibility for other Federal disaster relief programs

Register with FEMA – call 1-800-621-FEMA (3362)

*REMEMBER TO UPDATE YOUR CONTACT INFORMATION WITH FEMA AS NEEDED*

Register with SBA (Small Business Administration) in person @ a Disaster Recovery Center http://asd.fema.gov/inter/locator/home.htm or online https://disasterloan.sba.gov/ela/

IF YOU QUALIFY, YOU DO NOT HAVE TO ACCEPT THE LOAN

Some Federal Agencies use SBA information to determine your Community’s Disaster Needs

Sandy Affected Residents FEMA’s New Jersey Hurricane Sandy Website

http://www.fema.gov/disaster/4086

Wide Array Of Disaster Help Available http://www.fema.gov/disaster/4086/updates/wide-array-disaster-help-available

Hurricane Sandy Recovery Resource Listhttp://www.fema.gov/disaster/4086/updates/hurricane-sandy-recovery-resource-list

Hurricane Sandy Mitigation Resourceshttp://www.fema.gov/region-vi/hurricane-sandy-mitigation-resources

NJ Office of Emergency Management Sandy Recoveryhttp://www.ready.nj.gov/programs/sandy_recovery.html

Hurricane Sandy Advisory Base Flood Elevations (ABFEs) in New Jersey and New York

http://www.region2coastal.com/sandy/abfe

“What is my Advisory Base Flood Elevation (ABFE)?” Interactive Mapping Tool http://www.region2coastal.com/sandy/table

Presentation Sources Robert T. Stafford Disaster Relief & Emergency Act as amended, and Related Authorities, FEMA

592, June 2007 Biggert-Waters Flood Insurance Reform Act of 2012, HR 4348-512 Code of Federal Regulations

Title 44: Emergency Management & Assistance, Part 206 – Federal Disaster Assistance Title 44: Emergency Management & Assistance, Part 61 – Insurance Coverages & Assistance Title 13: Business Credit & Assistance, Parts 120 – Business Loans & 123 - Disaster Loan

Program FEMA Public Assistance Guide, FEMA 322, June 2007,

http://www.fema.gov/public-assistance-policy-and-guidance/public-assistance-guide Public Assistance Applicant Handbook, FEMA P-323, 2010 9500 Series Policy Publications, http://www.fema.gov/9500-series-policy-publications

National Flood Insurance Program (NFIP) – Answers to Questions About the NFIP, FEMA F-084, March 2011

NFIP, Increased Cost of Compliance Coverage – Guidance for State & Local Officials, FEMA 301, September 2003

Hazard Mitigation Assistance Unified Guidance (HMGP, PDM, FMA, RFC, SRL), FEMA, June 1, 2010

Engineering Principles & Practices for Retrofitting Flood-Prone Residential Structures (3rd Edition), FEMA P-259, January 2012

Hazard Mitigation Assistance (HMA) Tool for Identifying Duplication of Benefits, FEMA, October 2012

FloodSmart.gov. The official site of the National Flood Insurance Program (NFIP)