A. FINANCIAL RESULTS FOR THE YEARS ENDED DECEMBER31, … · local distribution grid of the Cagayan...

177

Transcript of A. FINANCIAL RESULTS FOR THE YEARS ENDED DECEMBER31, … · local distribution grid of the Cagayan...

1 | P a g e

MANAGEMENT REPORT

Brief Description of the General Nature and Scope of the Business of the Registrant and its Subsidiaries and Associates

First Gen Corporation (First Gen or the Parent company) is engaged in the business of power generation through the following operating companies:

(i) First Gas Power Corporation (FGPC) which operates the 1,000 MW Santa Rita natural gas-fired power plant;

(ii) FGP Corp. (FGP) which operates the 500 MW San Lorenzo natural gas-fired power plant; and (iii) FG Bukidnon Power Corporation (FG Bukidnon), via First Gen Renewables, Inc. (FGRI), which

operates the 1.6 MW FG Bukidnon mini hydroelectric power plant.

Equity in net earnings from associates include: (i) Energy Development Corporation (EDC), with an aggregate installed capacity of approximately 1,198.8 MW of geothermal power; and (ii) First Gen Hydro Power Corporation (FG Hydro) which operates the newly rehabilitated and upgraded 132 MW Pantabangan-Masiway hydroelectric power plants. The 225 MW Bauang bunker-fired power plant, which operated under Bauang Private Power Corporation (BPPC) under a Build-Operate-Transfer Agreement (BOT) with National Power Corporation (NPC), was turned over to the Government last July 25, 2010. Therefore, BPPC’s equity in net earnings contribution was only until July 31, 2010. First Gen’s 40% economic interest in EDC is indirectly held through Prime Terracota Holdings Corp. (Prime Terracota) and Red Vulcan Holdings Corporation (Red Vulcan), while its interest in FG Hydro is 40% held directly, and 60% held indirectly through EDC. As of December 31, 2010, the Parent company also directly owned 577.5 million shares in EDC. This is equivalent to a 3% economic interest in EDC. The following discussion focuses on the results of operations of First Gen and its power generating companies. As of December 31, 2010, First Gen's ownership interests in these operating companies are indirectly held through intermediate holding companies, with the exception of FG Hydro where First Gen directly holds a 40% interest. First Gas Holdings Corporation (FGHC) was incorporated on February 3, 1995 as a holding company

for the development of gas-fired power plants and other non-power gas related businesses. The company is 60% owned by First Gen and 40% owned by BG Consolidated Holdings (Philippines), Inc. FGHC wholly owns FGPC, the project company of the 1,000 MW Santa Rita Power Plant.

Unified Holdings Corporation (UHC) was incorporated on March 30, 1999 as the holding company of First Gen’s 60% equity share in FGP, the project company of the 500 MW San Lorenzo Power Plant. First Gen owns 100% of UHC.

FGRI, formerly known as First Philippine Energy Corporation, was established on November 29, 1978. It is tasked to develop prospects in the renewable energy market. FGRI has transformed itself from a supplier of solar products and systems to a power service provider in the countryside. First Gen owns 100% of FGRI. FG Bukidnon, a wholly-owned subsidiary of FGRI, was incorporated on February 9, 2005. Upon conveyance of First Gen in October 2005, FG Bukidnon took over the operations and maintenance of the FG Bukidnon hydroelectric power plant (FGBHPP). The run-of-river plant consists of two 800-kW turbine generators that use water from the Agusan River to generate electricity. It is connected to the local distribution grid of the Cagayan Electric Power & Light Company, Inc. (CEPALCO) via the National Grid Corporation of the Philippines (NGCP) line.

2 | P a g e

Prime Terracota was incorporated on October 17, 2007 as the holding company of Red Vulcan. Red Vulcan was incorporated on October 5, 2007 as the holding company for First Gen’s stake in EDC.

On November 22, 2007, First Gen, through Red Vulcan, was declared the winning bidder for Philippine National Oil Company and EDC Retirement Fund’s remaining shares in EDC, which consisted of 6.0 billion common shares and 7.5 billion preferred shares. Such common shares represented 40% economic interest in EDC while the combined common and preferred shares represented 60% of the voting rights in EDC. EDC is the Philippines’ largest producer of geothermal energy, operating 12 geothermal steamfields in the 5 geothermal renewable service contract areas where it is principally involved in the following: (i) the production of geothermal steam for sale to EDC-owned power plants; and (ii) the generation of electricity for sale to NPC and privately-owned distribution utilities. On May 12, 2009, Prime Terracota issued Class “B” voting preferred shares at par value to the Lopez Inc. Retirement Fund (LIRF) and Quialex Realty Corporation (QRC). Prime Terracota is the effective 60% voting / 40% economic owner of EDC through its subsidiary Red Vulcan. Prior to its issuance of preferred shares to LIRF and QRC, Prime Terracota was a wholly-owned subsidiary of First Gen. With the issuance of the preferred shares, First Gen’s voting interest in Prime Terracota is now reduced to 45%, with the balance taken up by LIRF (40%) and QRC (15%). This transaction triggered the deconsolidation of Prime Terracota, Red Vulcan, EDC and FG Hydro (collectively referred to as the Prime Terracota Group) in First Gen’s consolidated financial statements effective May 2009. Thereafter, First Gen’s investment in Prime Terracota is accounted for using the equity method in the consolidated financial statements of First Gen as it still retains significant influence over Prime Terracota through its 45%-voting interest.

FG Hydro was incorporated on March 13, 2006 as a wholly-owned subsidiary of First Gen. On September 8, 2006, FG Hydro emerged as the winning bidder for the then 100 MW Pantabangan and the 12 MW Masiway Hydroelectric Power Plants (PMHEPP). The then 112 MW PMHEPP was transferred to FG Hydro on November 18, 2006, representing the first major generating asset of NPC to be successfully transferred to the private sector. On October 15, 2008, First Gen’s Board of Directors approved the sale of 60% of FG Hydro to EDC and the divestment was completed in November 2008. As a result of the divestment, First Gen’s direct voting and indirect voting interest in FG Hydro after the transaction are 40% and 36%, respectively. Moreover, the completion of the rehabilitation and upgrade project of Pantabangan hydroelectric power plant’s Units 1 and 2 in 2010 increased the power generation capacity of PMHEPP to 132 MW.

First Private Power Corporation (FPPC) was established on November 27, 1992 primarily to engage in power generation. FPPC is 40%-owned by First Gen. FPPC owns a 93.25% interest in BPPC. BPPC was incorporated on February 3, 1993 and operated the Bauang power plant in Payocpoc Sur, Bauang, La Union, a 225 MW bunker-fired power plant which had a BOT with NPC for a period of fifteen (15) years from July 25, 1995 until July 25, 2010. BPPC’s BOT contract with NPC expired last July 25, 2010 and the Bauang power plant was turned-over to NPC on the same date. On November 15, 2010, BPPC and FPPC filed an application to be merged into one entity, with the former as the surviving entity. The application for merger was approved by the Securities and Exchange Commission of the Philippines on December 13, 2010, and the assets and liabilities of FPPC have been transferred to, and absorbed by, BPPC on December 15, 2010, the effectivity date of the merger.

3 | P a g e

In November 2008, First Gen completed the divestment of a 60% controlling stake in FG Hydro to EDC. In May 2009, with the investments of LIRF and QRC in the voting preferred shares of Prime Terracota, First Gen’s voting interest in Prime Terracota was reduced to 45%. Under Philippine Financial Reporting Standards (PFRS), a subsidiary is consolidated from the date on which the parent first achieves control up to the date on which control is lost. The operating results of controlled entities acquired or disposed of during the year are included in the consolidated statement of income from the date of acquisition and up to the date of disposal, as appropriate.

Deconsolidation of Prime Terracota, Red Vulcan, EDC and FG Hydro

As a result of the foregoing transactions, the consolidated financial statements of First Gen contained herein present the financial information of the Prime Terracota Group as follows:

the consolidated statements of income and the consolidated statements of cashflows for the year ended December 31, 2008 reflect the results of operations and cash flows of the Prime Terracota Group under the line item “Discontinued Operations”. However, in the consolidated statements of income and the consolidated statements of cashflows for the year ended December 31, 2009, the results of operations and cash flows of the Prime Terracota Group for the period ended April 30, 2009 is reflected under the line item “Discontinued Operations”. The consolidated statements of income and the consolidated statements of cashflows have been restated, as permitted under PFRS, and do not include the revenue and expense line items of the Prime Terracota Group for comparative purposes; and,

the consolidated statement of financial position as of December 31, 2009 does not consolidate the results of the Prime Terracota Group due to the divestment explained above. Beginning May 2009, First Gen’s investments in Prime Terracota and FG Hydro are shown as part of “Investments in associates” in the consolidated statement of financial position. Subsequent to the deconsolidation, the results of operations for the eight-month period ended December 31, 2009 and for the year ended December 31, 2010 are now accounted for using the equity method of accounting and are reflected in the “Equity in net earnings of associates” account in the consolidated statement of income.

Under PFRS, First Gen’s interests in the Prime Terracota Group are required to be reported under the equity method of accounting from the date on which control was lost, which occurred in May 2009, and restating the consolidated statement of income for the periods when Prime Terracota, Red Vulcan, EDC, and FG Hydro were still controlled and consolidated is permitted so as to provide some form of comparability with the new presentation. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS A. FINANCIAL RESULTS FOR THE YEARS ENDED DECEMBER 31, 2010, 2009 AND 2008

(Amounts in USD thousands) 2010 2009 2008 Statements of Income Data

Revenues $1,244,278 $1,022,116 $1,262,398 Income from continuing operations before income tax

$162,826

$91,157

$124,151

Net income attributable to Equity Holders of the Parent Company

$70,217

$16,754

$14,474

Statements of Financial Position Data 2010 2009 2008

ASSETS

Total current assets $377,889 $346,515 $665,541 Long-term receivables - net of current portion – – 652,831 Investments in associates 1,207,518 1,020,722 20,958 Property, plant and equipment 580,663 562,238 736,262 Intangible assets 17,370 17,972 1,301,651 Deferred income tax assets 3,794 10 71,794 Other noncurrent assets 154,159 213,566 248,840

4 | P a g e

Total Assets $2,341,393 $2,161,023 $3,697,877

LIABILITIES AND EQUITY

Total current liabilities $383,621 $282,566 $996,508 Bonds payable – net of current portion – 277,353 362,978 Long-term debt – net of current portion 729,502 700,324 1,073,285 Derivative liabilities – net of current portion 39,911 25,335 59,861 Retirement liability 722 167 24,899 Deferred income tax liabilities – net 10,479 18,609 30,036 Other noncurrent liabilities 29,189 49,632 131,899

Total Liabilities 1,193,424 1,353,986 2,679,466 Equity attributable to Equity Holders of the Parent Company 989,296 663,034 458,660 Non-controlling Interests 158,673 144,003 559,751

Total Equity 1,147,969 807,037 1,018,411

Total Liabilities and Equity $2,341,393 $2,161,023 $3,697,877

RESULTS OF OPERATIONS

December 2010 vs. December 2009 Results

CONSOLIDATED STATEMENTS OF INCOME Revenues Based on the audited consolidated financial statements for the year ended December 31, 2010, First Gen's revenues increased by $222.1 million or 21.7% to $1,244.3 million in 2010 from $1,022.1 million in 2009. The increase was due to higher revenues from sale of electricity by $159.2 million or 15.8% to $1,169.1 million in 2010 from $1,009.9 million in 2009, which resulted from higher fuel charges during the year as oil prices increased in the world market. Fuel revenues increased by $150.5 million with gas prices averaging at $9.6/GJ (or $10.2/MMBtu) in 2010 versus $8.6/GJ (or $9.1/MMBtu) in 2009. With the scheduled maintenance outage of the Malampaya platform in February and March 2010 and several gas curtailments that were experienced during the year, the Santa Rita and San Lorenzo power plants were required to operate on more expensive liquid fuel. The gas plants’ combined dispatch were slightly higher year-on-year at 82.7% capacity factor in 2010 compared to 82.3% in 2009. Another factor for the increase in total revenues was the mark-to-market (MTM) gain on derivatives in 2010 amounting to $5.4 million, as compared to the $0.9 million MTM loss in 2009. Derivative gains or losses recognized during the year pertain to MTM changes in the valuation of First Gen’s existing Convertible bonds and the call option to purchase EDC shares. First Gen has a call option over an aggregate of 585 million common shares of EDC exercisable up to April 2013 (see Note 13 of First Gen’s audited consolidated financial statements for the year ended December 31, 2010). The equity in net earnings of associates amounting to $47.7 million in 2010 significantly increased by $46.6 million as compared to $1.2 million in 2009 indicating the full year effect of the Prime Terracota Group as an associate. In 2009, equity in net earnings only included the share in net earnings of the Prime Terracota Group from the time of deconsolidation in May 2009 to December 2009. Earnings from the Prime Terracota Group for the periods January to April 2009 is reflected under “Net income from discontinued operations” in the consolidated statements of income for the year ended December 31, 2009.

5 | P a g e

Out of the total dollar increase in equity in net earnings, $39.8 million and $12.0 million are due to the higher equity in net earnings from EDC and FG Hydro, respectively. These were partly offset by the absence of equity in net earnings from BPPC as the Bauang BOT contract with NPC expired last July 2010. On a 12-month year-on-year comparison (adjusting for the attributable earnings from the Prime Terracota Group during the periods January to April 2009), net earnings from EDC is higher only by $21.5 million or 69.4%. The increase is due to higher revenues from Green Core Geothermal, Inc. (Green Core), a subsidiary of EDC which operates the Palinpinon-Tongonan power plants, following its full year operation in 2010 as compared to two months in 2009; net increase in miscellaneous income from the recovery of impairment loss on Input VAT claims amounting to P1,746.8 million, and absence of a deferred tax assets write-down due to implementation of the Renewable Energy (RE) law which amounted to P2,959.2 million in 2009 . Similarly, net earnings from FG Hydro is higher only by $8.4 million or 551.7% due to high WESM prices during the year and high volume of electricity sales during the first quarter of 2010. In addition, lower interest expense at Red Vulcan and Prime Terracota by $7.6 million and $3.2 million, respectively, also contributed to the higher contributions to earnings during the year. Total revenue was further increased by interest income amounting to $8.9 million in 2010, which increased by $1.9 million or 27.9% from $6.9 million in 2009. This resulted from higher ending cash balances at the Parent company level due to the new loans availed during the year and the remaining cash from the Rights Offer. The Parent company also received management fees amounting to $3.9 million in 2010, which improved by $0.4 million or 11.9% from $3.5 million in 2009. Moreover, there were additional reimbursements to cover employee costs of First Gen’s seconded employees that were charged to EDC during the year. Net Income

First Gen’s consolidated net income increased by $26.0 million or 27.4 % to $121.0 million in 2010 from $95.0 million in 2009. The significant change in consolidated net income was a result of the movements of the following items:

Consolidated Net Income

Net income from continuing operations increased by $68.0 million to $121.0 million resulting from:

• higher Equity in net earnings of associates by $46.6 million resulting from the recognition of equity in net earnings of the Prime Terracota Group covering the whole year of 2010 as compared to the eight months recognized in 2009; the higher net earnings from EDC was due to higher revenues from Green Core following its full year operation in 2010 as compared to two months in 2009, net increase in miscellaneous income from the recovery of impairment loss on Input VAT claims, and absence of a deferred tax assets write-down in 2010. Adding to this was the higher net earnings from FG Hydro due to high WESM prices during the year and high volume of electricity sales during the first quarter of 2010. In addition, lower interest expense at Red Vulcan and Prime Terracota by $7.6 million and $3.2 million, respectively, also contributed to the higher contributions to earnings in 2010;

• the recognition of MTM gain on derivatives of $5.4 million in 2010, a reversal from last year’s $0.9 million MTM loss on derivatives. Derivative gains or losses recognized during the year pertain to MTM changes in the valuation of First Gen’s existing Convertible bonds and the call option to purchase EDC shares;

• increased interest income by $1.9 million or 27.9% resulting from higher ending cash balances at

the Parent company level due to the new loans availed during the year and the remaining cash from the Rights Offer;

6 | P a g e

• interest expense and financing charges decreased by $7.9 million due to lower interest expense as a result of scheduled loan repayments of FGPC and FGP. Another factor adding to this decrease is the Parent company’s buy-back of its Convertible bonds and the maturity of the Peso-denominated bond in July 2010. The decrease was, however, partially offset by the higher interest expense at UHC by $2.8 million after recognizing a full year of interest expense on its P5.4 billion loan, which was drawn in March 2009;

• Other revenues were higher by $9.0 million as a result of the recognition of higher consultancy fees and reimbursements to cover employee costs of the First Gen’s seconded employees to EDC; and,

• Lower foreign exchange loss of $5.1 million in 2010 as compared to a $8.7 million foreign

exchange loss recognized in 2009 resulting from the payment of the Peso-denominated bond in July 2010, which reduced First Gen’s exposure to foreign exchange translation.

The increase in net income from continuing operations was offset by the absence of net income from discontinued operations during the year as compared to the amount recognized in 2009 of $42.0 million. This amount pertains to the net income of the Prime Terracota Group from January to April 2009, prior to the deconsolidation. Considering the absence of net income from discontinued operations, First Gen’s consolidated net income increased by $26.0 million or 27.4 % to $121.0 million in 2010 from $95.0 million in 2009.

Of the $121.0 million consolidated net income for the year ended December 31, 2010, net income attributable to the Parent company amounted to $70.2 million, which is $53.5 million or 319.1% higher than the $16.7 million net income attributable to the Parent company in 2009.

Net Income Attributable to Equity Holders of the Parent Company

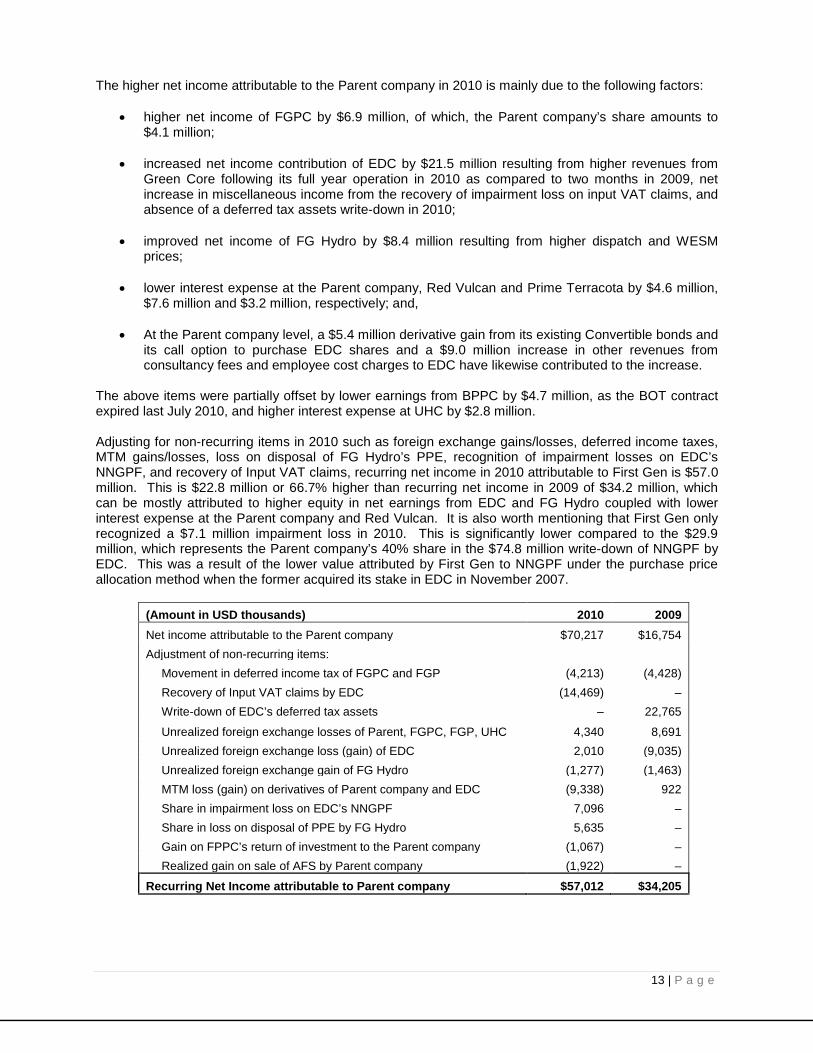

The higher net income attributable to the Parent company in 2010 is mainly due to the following factors:

• higher net income of FGPC by $6.9 million, of which, the Parent company’s share amounts to $4.1 million;

• increased net income contribution of EDC by $21.5 million resulting from higher revenues from Green Core following its full year operation in 2010 as compared to two months in 2009, net increase in miscellaneous income from the recovery of impairment loss on input VAT claims, and absence of a deferred tax assets write-down in 2010;

• improved net income of FG Hydro by $8.4 million resulting from higher dispatch and WESM prices;

• lower interest expense at the Parent company, Red Vulcan and Prime Terracota by $4.6 million, $7.6 million and $3.2 million, respectively; and,

• At the Parent company level, a $5.4 million derivative gain from its existing Convertible bonds and its call option to purchase EDC shares and a $9.0 million increase in other revenues from consultancy fees and employee cost charges to EDC have likewise contributed to the increase.

The above items were partially offset by lower earnings from BPPC by $4.7 million, as the BOT contract expired last July 2010, and higher interest expense at UHC by $2.8 million. Adjusting for non-recurring items in 2010 such as foreign exchange gains/losses, deferred income taxes, MTM gains/losses, loss on disposal of FG Hydro’s PPE, recognition of impairment losses on EDC’s NNGPF, and recovery of Input VAT claims, recurring net income in 2010 attributable to First Gen is $57.0 million. This is $22.8 million or 66.7% higher than recurring net income in 2009 of $34.2 million, which can be mostly attributed to higher equity in net earnings from EDC and FG Hydro, coupled with lower

7 | P a g e

interest expense at the Parent company and Red Vulcan. It is also worth mentioning that First Gen only recognized a $7.1 million impairment loss in 2010. This is significantly lower compared to the $29.9 million, which represents the Parent company’s 40% share in the $74.8 million write-down of NNGPF by EDC. This was a result of the lower value attributed by First Gen to NNGPF under the purchase price allocation method when the former acquired its stake in EDC in November 2007.

(Amount in USD thousands) 2010 2009 Net income attributable to the Parent company $70,217 $16,754 Adjustment of non-recurring items:

Movement in deferred income tax of FGPC and FGP (4,213) (4,428) Recovery of Input VAT claims by EDC (14,469) – Write-down of EDC’s deferred tax assets – 22,765

Unrealized foreign exchange losses of Parent, FGPC, FGP, UHC 4,340 8,691 Unrealized foreign exchange loss (gain) of EDC 2,010 (9,035) Unrealized foreign exchange gain of FG Hydro (1,277) (1,463) MTM loss (gain) on derivatives of Parent company and EDC (9,338) 922 Share in impairment loss on EDC’s NNGPF 7,096 – Share in loss on disposal of PPE by FG Hydro 5,635 – Gain on FPPC’s return of investment to the Parent company (1,067) – Realized gain on sale of AFS by Parent company (1,922) –

Recurring Net Income attributable to Parent company $57,012 $34,205

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

ASSETS

Major movements in the audited consolidated statements of financial position of First Gen Group from December 31, 2009 to December 31, 2010 resulted in a net increase of $180.4 million or 8.3% in First Gen Group’s consolidated total assets. The net increase is a result of the following major movements: Cash and cash equivalents increased by $75.7 million or 60.3% as a result of the remaining cash

proceeds from the Rights Offer, new loans availed, and cash accumulated from operations during the year.

Investments in associates increased by $186.8 million or 18.3% due to higher accumulated equity in

net earnings of the Prime Terracota Group, additional deposits for future stock subscriptions totaling $53.4 million, and the purchase of EDC shares directly by First Gen.

Other noncurrent assets decreased by $59.4 million or 27.8% as a result of the consumption of Prepaid gas during the latter part of 2010, use of spare parts following the scheduled major maintenance outage of the Santa Rita and San Lorenzo power plants in 2010, and payment by BG of its advances from FGPC in connection with the proceeds from the Santa Rita refinancing. These transactions decreased other noncurrent assets by $20.5 million, $36.5 million, and $5.0 million, respectively.

Receivables decreased by $33.8 million or 27.9% as a result of the early payment received from

Meralco covering the November 2010 billings in December 2010, which was otherwise due in January 2011.

8 | P a g e

LIABILITIES AND EQUITY Total liabilities decreased by $160.6 million or 11.9% to $1,193.4 million as of December 31, 2010 from $1,354.0 million as of December 31, 2009 due to the following major movements: Bonds payable decreased by $172.0 million resulting from the buy-back of Convertible bonds and the

payment of the P5.0 billion bonds by the Parent company amounting to $105.5 million. As of December 31, 2010, the Parent company bought back Convertible bonds with a total face value of $74.0 million for a total settlement amount of $83.2 million.

Other noncurrent liabilities decreased by $20.4 million or 41.2% due to the reduction in unearned revenues following the use of Prepaid gas during the latter part of 2010.

Scheduled principal payments during the year amounting to $21.7 million and $26.4 million were made on FGPC’s and FGP’s loans, respectively.

Deferred income tax liabilities decreased by $8.1 million due to lower deferred income tax liabilities of

FGPC, and FGP’s recognition of deferred income tax assets both resulting from the movements in foreign exchange rate of the Philippine Peso against the U.S. dollar in 2010.

Accounts payable and accrued expenses decreased by $5.8 million or 5.5% resulting from the

payment of FGP’s liquid fuel suppliers in February 2010. This decrease was partially offset by higher operations and maintenance (O&M) fees payable to Siemens Power Operations, Inc. (SPOI) following the effectivity of the new O&M agreement on August 1, 2010 and higher payables to the gas sellers as a result of the increase in gas prices.

The above reduction in liabilities was partly offset by the following movements: Availment of new loans by the Parent company in May 2010 amounting to $72.2 million and $11.4

million (or P500.0 million), which increased total outstanding debt by $83.6 million.

Derivative liabilities increased by $14.6 million due to higher derivative liabilities of FGPC resulting from lower LIBOR rates in 2010 as compared to the previous year. FGPC recognized a derivative liability as it entered into interest rate swap agreements to hedge the interest payments of its debt.

Total equity increased by $340.9 million or 42.2% to $1,148.0 million as of December 31, 2010 as compared to $807.1 million as of December 31, 2009 mainly due to the successful completion of the Rights Offer in January 2010 and income earned during the year. Likewise, equity attributable to equity holders of the Parent company increased to $989.3 million, or 49.2% higher, as compared to $663.0 million in 2009.

9 | P a g e

FIRST GEN MATERIAL CHANGES IN FINANCIAL CONDITION (2010 vs. 2009)

Horizontal and Vertical Analyses of Material Changes for the years ended December 31, 2010 vs. 2009

CONSOLIDATED STATEMENTS OF INCOME

HORIZONTAL ANALYSIS VERTICAL ANALYSIS

(Amounts in U.S. Dollars and in Thousands) Dec. 2010 Dec. 2009 2010 vs. 2009

2010 vs. 2009 2010 2009

REVENUE Sale of electricity 1,169,155 1,009,918 159,237 15.8% 94.0% 98.8% Mark-to-market gain on derivatives 5,395 – 5,395 0.0% 0.4% 0.0% Interest 8,881 6,942 1,939 27.9% 0.7% 0.7% Equity in net earnings of associates 47,729 1,167 46,562 3989.9% 3.8% 0.1% Others 13,118 4,089 9,029 220.8% 1.1% 0.4% TOTAL REVENUES 1,244,278 1,022,116 222,162 21.7% 100.0% 100.0%

Fuel cost (821,467) (669,832) (151,635) 22.6% -66.0% -65.5% Power plant operations & maintenance (40,220) (37,624) (2,596) 6.9% -3.2% -3.7% Depreciation and amortization (54,970) (53,932) (1,038) 1.9% -4.4% -5.3% Staff costs (16,582) (10,625) (5,957) 56.1% -1.3% -1.0% Other administrative expenses (38,664) (37,244) (1,420) 3.8% -3.1% -3.6%

Sub-total (971,903) (809,257) (162,646) 20.1% -78.1% -79.2% Interest expense & financing charges (104,222) (112,089) 7,867 -7.0% -8.4% -11.0% Foreign exchange loss - net (5,114) (8,691) 3,577 -41.2% -0.4% -0.9% Mark-to-market loss on derivatives – (922) 922 -100.0% 0.0% -0.1% Other charges (213) – (213) 0.0% 0.0% 0.0%

Total (1,081,452) (930,959) (150,493) 16.2% -86.9% -91.1%

INCOME FROM CONTINUING OPERATIONS BEFORE INCOME TAX

162,826

91,157 71,669 78.6% 13.1% 8.9%

Provision for (benefit from ) Income Tax Current 48,848 45,492 3,356 7.4% 3.9% 4.5% Deferred (7,022) (7,381) 359 -4.9% -0.6% -0.7%

41,826 38,111 3,715 9.7% 3.4% 3.7%

Net income from continuing operations 121,000 53,046 67,954 128.1% 9.7% 5.2%

Net income from discontinued operations – 41,961 (41,961) -100.0% 0.0% 4.1%

NET INCOME 121,000 95,007 25,993 27.4% 9.7% 9.3%

Attributable to:

Equity holders of the Parent Company 70,217 16,754 53,463 319.1% 5.6% 1.6% Non-controlling Interests 783 78,253 (27,470) -35.1% 4.1% 7.7%

Revenues

Revenues for the year ended December 31, 2010 increased by $222.1 million or 21.7% to $1,244.3 million from $1,022.1 million during 2009. The increase was due to the major movements in revenue items as explained in detail below:

10 | P a g e

Revenue from sale of electricity Revenues from the sale of electricity increased by $159.2 million or 15.8% to $1,169.1 million in 2010 from $1,009.9 million in 2009, as a result of higher fuel charges during 2010 as oil prices increased in the world market. With the scheduled maintenance outage of the Malampaya platform in February and March 2010 and several gas curtailments that were experienced during the year, the Santa Rita and San Lorenzo power plants were required to operate on more expensive liquid fuel. In addition, the price of natural gas in 2010 averaged at $9.6/GJ (or $10.2/MMBtu), 11.7% higher than the average price during 2009 of $8.6/GJ (or $9.1/MMBtu). Santa Rita and San Lorenzo also posted a slightly higher plant dispatch in 2010 at a combined average of 82.7% as compared to 82.3% during the same period last year. Mark-to-market (MTM) gain on derivatives The company recognized a $5.4 million MTM gain on derivative transactions in 2010 as the Company recognized $3.9 million gain on its call option to purchase EDC shares in the market and $1.5 million gain on First Gen’s Convertible bonds. First Gen has a call option over an aggregate of 585 million common shares of EDC exercisable up to April 2013 (see Note 13 of First Gen’s audited consolidated financial statements as of December 31, 2010). This is a reversal of the MTM loss on derivative transactions of $0.9 million that was recognized in 2009, which was classified under “Costs and Expenses” account of the Company’s consolidated statements of income. The gain/(loss) on derivatives results from the change in the price of the Convertible bonds in the market vis-à-vis the put option and from the movement of EDC’s share price in the market vis-à-vis the call option’s exercise price. Interest income Interest income increased by $1.9 million or 27.9% to $8.9 million in 2010 from $6.9 million in 2009 as a result of the higher cash balances at the Parent company after the successful completion of the Rights Offer in January 2010 and new loans availed during the year. Equity in net earnings of associates Equity in net earnings of associates amounting to $47.7 million in 2010 significantly increased by $46.6 million as compared to $1.2 million in 2009 showing the full year effect of Prime Terracota Group as an associate. In 2009, equity in net earnings only included the share in net earnings of the Prime Terracota Group from the time of deconsolidation in May 2009 to December 2009. Earnings from the Prime Terracota Group for the periods January to April 2009 is reflected under “Net income from discontinued operations” in the consolidated statements of income. Out of the total dollar increase in equity in net earnings, $39.8 million and $12.0 million are due to the higher equity in net earnings from EDC and FG Hydro, respectively. These were partly offset by the absence of equity in net earnings from BPPC of $4.7 million in 2009 as the Bauang BOT contract with NPC expired last July 2010. On a 12-month year-on-year comparison (adjusting for the attributable earnings from the Prime Terracota Group during the periods January to April 2009), net earnings from EDC is higher only by $21.5 million or 69.4%. The increase is due to higher revenues from Green Core following its full year operation in 2010 as compared to two months in 2009; net increase in miscellaneous income from the recovery of impairment loss on Input VAT claims amounting to P1,746.8 million and absence of a deferred tax assets write-down amounting to P2,959.2 million recognized in 2009 due to implementation of the RE law. Similarly, net earnings from FG Hydro is higher only by $8.4 million or 551.7% due to high WESM prices during the year and high volume of electricity sales during the first quarter of 2010.

11 | P a g e

Other revenues The $9.0 million increase is mainly due to consultancy fees received by First Gen from EDC, which was adjusted effective September 2009. The three-year consultancy services agreement took effect on September 1, 2008 and will end on August 31, 2011. Adding to the increase is the reimbursements to cover employee costs of the First Gen’s seconded employees that were charged to EDC during the year.

Costs and operating expenses for the year ended December 31, 2010 posted a net increase of $162.6 million or 20.1% to $971.9 million as compared to $809.3 million in 2009 as a result of the following movements:

Costs and Operating Expenses

Fuel cost Fuel charges of Santa Rita and San Lorenzo went up by $151.6 million or 22.6% to $821.5 million in 2010 from $669.9 million in 2009. The higher fuel cost was due to the consumption of liquid fuel during the scheduled Malampaya outage in February and March 2010, and during the gas curtailments that were experienced during the year. Both plants were required to operate using a more expensive liquid fuel during these periods. Moreover, the average price of natural gas increased by 11.7% to $9.6/GJ (or $10.2/MMBtu) in 2010 as compared to the average price in 2009 of $8.6/GJ (or $9.1/MMBtu).

Staff costs Staff costs increased by $6.0 million or 56.1% due to a lower weighted average foreign exchange rate in 2010 (P45.309:$1.00) compared to the rate in 2009 (P47.769:$1.00) that was used to convert the Peso-denominated expenses to its U.S. dollar equivalent. In addition, the amounts for the year ended December 31, 2010 already reflect the salary adjustments that were effected during the year. Other administrative expenses Other administrative expenses increased by $1.4 million or 3.8% in 2010 due to higher professional fees at the Parent company level in connection with various financing activities during the year.

Interest expense and financing charges decreased by $7.9 million or 7.0% to $104.2 million in 2010 from $112.1 million in 2009. Interest expense at FGPC and FGP decreased by $5.9 million due to the lower outstanding debt during the year after the scheduled principal payments were made. The Parent company also recognized lower interest expense by $4.6 million after paying down its P5.0 billion bond which matured in July 2010. This was offset by higher interest expense at UHC by $2.8 million after recognizing a full year interest expense on the P5.4 billion corporate notes, drawn in March 2009.

Interest expense and financing charges

In 2010, the Company recognized a MTM gain on derivative transactions of $5.4 million as compared to the MTM loss on derivative transactions of $0.9 million that was recognized in 2009. This MTM gain pertains to the gains in First Gen’s call option to purchase EDC shares and Convertible bonds, which were included as part of “Revenues” in the consolidated statements of income. The net derivative loss in 2009 was due to the change in the fair values of First Gen’s Convertible bonds.

MTM loss on derivatives

Foreign exchange loss amounted to $5.1 million in 2010. Although the peso appreciated, the foreign exchange loss decreased by $3.6 million or 41.2% compared to $8.7 million recognized in 2009 resulting from the payment of the Peso-denominated bond in July 2010, which reduced First Gen’s exposure to foreign exchange translation.

Foreign exchange loss - net

The First Gen group recognized a higher provision for income tax by $3.7 million or 9.7% to $41.8 million in 2010 as compared to $38.1 million in 2009. The increase was primarily due to the higher current income tax resulting from the full year effect of FGP’s income tax following the expiry of FGP’s income tax holiday in February 2009 and the higher taxable income of FGPC.

Provision for (benefit from) Income Tax

12 | P a g e

First Gen’s consolidated net income increased by $26.0 million or 27.4 % to $121.0 million in 2010 from $95.0 million in 2009. The significant change in consolidated net income was a result of the movements of the following items:

Net Income

Net income from continuing operations increased by $68.0 million to $121.0 million resulting from:

• higher Equity in net earnings of associates by $46.6 million resulting from the recognition of equity in net earnings of the Prime Terracota Group covering the whole year of 2010 as compared to the eight months recognized in 2009; the higher net earnings from EDC due to higher revenues from Green Core following its full year operation in 2010 as compared to two months in 2009, net increase in miscellaneous income from the recovery of impairment loss on Input VAT claims, and absence of a deferred tax assets write-down in 2010. Adding to this was the higher net earnings from FG Hydro due to high WESM prices during the year and high volume of electricity sales during the first quarter of 2010. In addition, lower interest expense at Red Vulcan and Prime Terracota by $7.6 million and $3.2 million, respectively, also contributed to the higher contributions to earnings in 2010;

• the recognition of MTM gain on derivatives of $5.4 million in 2010, a reversal from last year’s $0.9 million MTM loss on derivatives. Derivative gains or losses recognized during the year pertain to MTM changes in the valuation of First Gen’s existing Convertible bonds and the call option to purchase EDC shares;

• increased interest income by $1.9 million or 27.9% resulting from higher ending cash balances at

the Parent company level due to the new loans availed during the year and the remaining cash from the Rights Offer;

• interest expense and financing charges decreased by $7.9 million due to lower interest expense

as a result of scheduled loan repayments of FGPC and FGP. Another factor adding to this decrease is the Parent company’s buy-back of its Convertible bonds and the maturity of the Peso-denominated bond in July 2010. The decrease was, however, partially offset by the higher interest expense at UHC by $2.8 million after recognizing a full year of interest expense on its P5.4 billion loan, which was drawn in March 2009;

• Other revenues were higher by $9.0 million as a result of the recognition of higher consultancy fees and reimbursements to cover employee costs of the First Gen’s seconded employees to EDC; and,

• Lower foreign exchange loss of $5.1 million as compared to a $8.7 million foreign exchange loss

recognized in 2009 resulting from the payment of the Peso-denominated bond in July 2010, which reduced First Gen’s exposure to foreign exchange translation.

The increase in net income from continuing operations was offset by the absence of net income from discontinued operations during the year as compared to the amount recognized in 2009 of $42.0 million. This amount pertains to the net income of the Prime Terracota Group from January to April 2009, prior to the deconsolidation. Considering the absence of net income from discontinued operations, First Gen’s consolidated net income increased by $26.0 million or 27.4 % to $121.0 million in 2010 from $95.0 million in 2009.

Of the $121.0 million consolidated net income for the year ended December 31, 2010, net income attributable to the Parent company amounted to $70.2 million, which is $53.5 million or 319.1% higher than the $16.7 million net income attributable to the Parent company in 2009.

Net Income Attributable to Equity Holders of the Parent Company

13 | P a g e

The higher net income attributable to the Parent company in 2010 is mainly due to the following factors:

• higher net income of FGPC by $6.9 million, of which, the Parent company’s share amounts to $4.1 million;

• increased net income contribution of EDC by $21.5 million resulting from higher revenues from Green Core following its full year operation in 2010 as compared to two months in 2009, net increase in miscellaneous income from the recovery of impairment loss on input VAT claims, and absence of a deferred tax assets write-down in 2010;

• improved net income of FG Hydro by $8.4 million resulting from higher dispatch and WESM prices;

• lower interest expense at the Parent company, Red Vulcan and Prime Terracota by $4.6 million, $7.6 million and $3.2 million, respectively; and,

• At the Parent company level, a $5.4 million derivative gain from its existing Convertible bonds and its call option to purchase EDC shares and a $9.0 million increase in other revenues from consultancy fees and employee cost charges to EDC have likewise contributed to the increase.

The above items were partially offset by lower earnings from BPPC by $4.7 million, as the BOT contract expired last July 2010, and higher interest expense at UHC by $2.8 million. Adjusting for non-recurring items in 2010 such as foreign exchange gains/losses, deferred income taxes, MTM gains/losses, loss on disposal of FG Hydro’s PPE, recognition of impairment losses on EDC’s NNGPF, and recovery of Input VAT claims, recurring net income in 2010 attributable to First Gen is $57.0 million. This is $22.8 million or 66.7% higher than recurring net income in 2009 of $34.2 million, which can be mostly attributed to higher equity in net earnings from EDC and FG Hydro coupled with lower interest expense at the Parent company and Red Vulcan. It is also worth mentioning that First Gen only recognized a $7.1 million impairment loss in 2010. This is significantly lower compared to the $29.9 million, which represents the Parent company’s 40% share in the $74.8 million write-down of NNGPF by EDC. This was a result of the lower value attributed by First Gen to NNGPF under the purchase price allocation method when the former acquired its stake in EDC in November 2007.

(Amount in USD thousands) 2010 2009 Net income attributable to the Parent company $70,217 $16,754 Adjustment of non-recurring items:

Movement in deferred income tax of FGPC and FGP (4,213) (4,428) Recovery of Input VAT claims by EDC (14,469) – Write-down of EDC’s deferred tax assets – 22,765

Unrealized foreign exchange losses of Parent, FGPC, FGP, UHC 4,340 8,691 Unrealized foreign exchange loss (gain) of EDC 2,010 (9,035) Unrealized foreign exchange gain of FG Hydro (1,277) (1,463) MTM loss (gain) on derivatives of Parent company and EDC (9,338) 922 Share in impairment loss on EDC’s NNGPF 7,096 – Share in loss on disposal of PPE by FG Hydro 5,635 – Gain on FPPC’s return of investment to the Parent company (1,067) – Realized gain on sale of AFS by Parent company (1,922) –

Recurring Net Income attributable to Parent company $57,012 $34,205

14 | P a g e

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION Horizontal and Vertical Analyses of Material Changes as of December 31, 2010 and 2009

HORIZONTAL ANALYSIS VERTICAL ANALYSIS

Increase (Decrease)

(Amounts in U.S. Dollars and in Thousands) Dec-10 Dec-09 2010 vs. 2009 (Audited) (Audited) Amount % Dec-10 Dec-09 ASSETS Current Assets Cash and cash equivalents $201,251 $125,531 $75,720 60.3% 8.6% 5.8% Receivables 87,503 121,334 (33,831) -27.9% 3.7% 5.6% Inventories 51,013 65,072 (14,059) -21.6% 2.2% 3.0% Other current assets 38,122 34,578 3,544 10.2% 1.6% 1.6% Total Current Assets 377,889 346,515 31,374 9.1% 16.1% 16.0% Noncurrent Assets Investments in associates 1,207,518 1,020,722 186,796 18.3% 51.6% 47.2% Property, plant and equipment 580,663 562,238 18,425 3.3% 24.8% 26.0%

Intangible assets 17,370 17,972 (602) -3.3% 0.7% 0.8% Deferred income tax assets 3,794 10 3,784 37840.0% 0.2% 0.0% Other noncurrent assets 154,159 213,566 (59,407) -27.8% 6.6% 9.9% Total Noncurrent Assets 1,963,504 1,814,508 148,996 8.2% 83.9% 84.0%

TOTAL ASSETS $2,341,393 $2,161,023 $180,370 8.3% 100.0% 100.0%

LIABILITIES AND EQUITY Current Liabilities Accounts payable and accrued expenses $98,698 $104,451 ($5,753) -5.5% 4.2% 4.8% Income tax payable 5,253 7,543 (2,290) -30.4% 0.2% 0.3% Due to related parties 6,709 6,711 (2) 0.0% 0.3% 0.3% Convertible bonds redeemed 83,134 – 83,134 0.0% 3.6% 0.0% Convertible bonds not redeemed 130,149 – 130,149 0.0% 5.6% 0.0% Current portion of long-term debt 59,678 46,499 13,179 28.3% 2.5% 2.2% Philippine peso-denominated bonds – 107,984 (107,984) -100.0% 0.0% 5.0%

Obligations to Gas Sellers on Annual Deficiency – 9,378 (9,378) -100.0% 0.0% 0.4%

Total Current Liabilities 383,621 282,566 101,055 35.8% 16.4% 13.1%

Noncurrent Liabilities Convertible bonds – 277,353 (277,353) -100.0% 0.0% 12.8% Long-term debt – net of current portion 729,502 700,324 29,178 4.2% 31.2% 32.4% Derivative liabilities 39,911 25,335 14,576 57.5% 1.7% 1.2% Retirement liability 722 167 555 332.3% 0.0% 0.0% Deferred income tax liabilities – net 10,479 18,609 (8,130) -43.7% 0.4% 0.9%

Other noncurrent liabilities 29,189 49,632 (20,443) -41.2% 1.2% 2.3%

Total Noncurrent Liabilities 809,803 1,071,420 (261,617) -24.4% 34.6% 49.6%

TOTAL LIABILITIES 1,193,424 1,353,986 (160,562) -11.9% 51.0% 62.7% Equity Attributable to Equity Holders of the Parent Redeemable preferred stock 14,585 13,561 1,024 7.6% 0.6% 0.6% Common stock 74,697 45,915 28,782 62.7% 3.2% 2.1% Additional paid-in capital 590,193 320,455 269,738 84.2% 25.2% 14.8% Deposits for future stock subscriptions – 93,318 (93,318) -100.0% 0.0% 4.3%

15 | P a g e

Accumulated share in other comprehensive losses of associates (21,006) (78,516) 57,510 -73.2% -0.9% -3.6% Cumulative translation adjustments (16,309) (9,642) (6,667) 69.1% -0.7% -0.4% Retained earnings 400,123 330,930 69,193 20.9% 17.1% 15.3% Cost of common stock held in treasury (52,987) (52,987) – 0.0% -2.3% -2.5%

989,296 663,034 326,262 49.2% 42.3% 30.7%

Non-controlling Interests 158,673 144,003 14,670 10.2% 6.8% 6.7%

Total Equity 1,147,969 807,037 340,932 42.2% 49.0% 37.3%

TOTAL LIABILITIES AND EQUITY $2,341,393 $2,161,023 $180,370 8.3% 100.0% 100.0% Cash and cash equivalents This account consists mainly of cash on hand and in banks. Cash equivalents include cash investments with original maturities of less than three months. Cash and cash equivalents increased by $75.7 million or 60.3% to $201.2 million as of December 31, 2010 as compared to $125.5 million as of December 31, 2009. The increase is mainly due to accumulated cash from operations and the higher cash balances at the Parent company level due to the remaining proceeds from the Rights Offer that was completed in January 2010 and new loans availed during the year. Adding to the increase is the higher ending cash balances at FGPC and FGP since payments from Meralco for the November 2010 billing were received early, which were otherwise due in January 2011. Receivables Receivables decreased by $33.8 million or 27.9% to $87.5 million as of December 31, 2010 from $121.3 million as of December 31, 2009. The decrease mainly resulted from the early payment received from Meralco covering the November 2010 billings. Receivables from Meralco as of December 31, 2009 still include the November 2009 billings which were paid by Meralco in January 2010. Inventories The decrease in this account by $14.1 million or 21.6% was due to the use of liquid fuel during the scheduled 30-day maintenance outage of the Malampaya gas plant which started in February 2010. Other current assets This account increased by $3.5 million or 10.2% primarily due to higher balance of current maturing receivables from BG during the year and higher prepaid expenses. Investments in associates This account, which increased by $186.8 million or 18.3%, mainly includes the accumulated equity in net earnings of the Prime Terracota Group, the additional deposits for future stock subscription totaling to $53.4 million, and the cost of the EDC shares that were purchased directly by the Parent company through an ordinary block sale in the Philippine Stock Exchange (PSE). As of December 31, 2010, First Gen has a 3% direct ownership in EDC. It is worth mentioning that on April 19, 2010, First Gen executed a call option agreement over an aggregate 585 million common shares of stock in EDC within a period of three years or up to April 2013. Property, plant, and equipment – net This account slightly increased by $18.4 million or 3.3% mainly due to the prepaid major spare parts that were reclassified from “Other noncurrent assets” account as a result of the scheduled major maintenance outages of the Santa Rita and San Lorenzo power plants that were completed during the year. This increase was partially offset by the depreciation expenses for the year. Intangible assets This account decreased by $0.6 million or 3.3% due to amortization of FGP’s “Pipeline rights” for the year.

16 | P a g e

Deferred income tax assets This account increased by $3.8 million as a result of appreciation of the Philippine Peso against the U.S. dollar (i.e. from P46.20 in December 2009 to P43.84 in December 2010). In the case of FGP, this appreciation has led to higher difference between the carrying values of non-monetary assets and their related tax bases as of December 31, 2010 which resulted to a higher deferred income tax asset. Other noncurrent assets This account decreased by $59.4 million or 27.8% due to the consumption of Prepaid gas by FGPC and FGP during the latter part of 2010. Moreover, the cost of spare parts pertaining to turbine blades of the Santa Rita and San Lorenzo power plants, which were previously capitalized under “Prepaid major spare parts” account were now reclassified under “Property, plant, and equipment” account as these parts were used during the gas plant’s scheduled major maintenance outages during the year. Accounts payable and accrued expenses This account decreased by $5.8 million or 5.5% due to lower net trade payables of FGPC and FGP during the year. In February 2010, FGP settled its payments with its liquid fuel suppliers. This decrease was partially offset by the increase in FGPC’s O&M fees payable to SPOI following the effectivity of the new Operations O&M agreement on August 1, 2010. The increase in gas prices during the year likewise resulted in higher payables to the gas sellers. Income tax payable Income tax payable decreased by $2.3 million or 30.4% which resulted from higher creditable withholding taxes applied against the income tax payables of FGPC and FGP in 2010. Obligations to Gas Sellers on Annual Deficiency The $9.4 million decrease in this account pertains to the settlement of the Annual Deficiency claims for Contract Year 2006. The original balance of $9.4 million has been reduced to $2.1 million following the final settlement of the gas dispute which took effect in June 2010. Convertible bonds redeemed This account pertains to the total put value of the Convertible bonds that will be redeemed in February 2011. On February 11, 2011, holders of the First Gen’s Convertible bonds amounting to $72.5 million exercised their option to require the Parent company to redeem the Convertible bonds at a price of 115.6% of the face value. The total put value amounting to $83.8 million (with a face value of $72.5 million and carrying value of $83.1 million) was paid on February 11, 2011. Convertible bonds not redeemed After the redemption on February 11, 2011 as explained above, this account pertains to the carrying value of the unredeemed Convertible bonds amounting to $130.1 million (with face value of $113.5 million) which will now have a maturity date of February 11, 2013. As compared to the $277.4 million value in December 2009, the carrying value of the Convertible bonds decreased due to the buy-back of Convertible bonds during the year, with a face value of $74.0 million, by the Parent company for a total settlement amount of $83.2 million. Philippine peso-denominated bonds The decrease in this account pertains to the final maturity of the P5.0 billion bond, which matured on July 30, 2010. Derivative liabilities This account increased by $14.6 million or 57.5% due to higher derivative liabilities of FGPC resulting from lower LIBOR rates in 2010 as compared to the previous year. FGPC recognized a derivative liability as it entered into interest rate swap agreements to hedge the interest payments of its debt. Retirement liability The $0.6 million increase in this account was due to the effect of the revised actuarial valuation report across the First Gen group during the year.

17 | P a g e

Deferred income tax liabilities – net The decrease of $8.1 million or 43.7% was due to lower deferred tax liabilities of FGPC and FGP, as a result of the movements in foreign exchange rate of the Philippine Peso against the U.S. dollar (i.e. from P46.20 in December 2009 to P43.84 in December 2010). Other noncurrent liabilities – net of current portion This account decreased by $20.4 million or 41.2% resulting from the use of Prepaid gas by the gas plants during the latter part of 2010, which led to the decrease in “Unearned revenues” account by $20.5 million, though partially offset by the accretion of the asset retirement obligation amounting to $0.1 million. The settlement of the outstanding dispute with the gas sellers covering the Annual Deficiency claims for 2006 has likewise led to lower ending balances for this account. Redeemable preferred stock The $1.0 million or 7.6% increase in this account pertains to the stock dividends on Series “E” preferred shares that were declared in 2010. Common stock The $28.8 million or 62.7% increase in common stock was due to the Rights Offer that was successfully completed in January 2010. Additional paid-in capital The $269.7 million or 84.2% increase in this account pertains to the proceeds from the Rights Offer in excess of the par value of the stocks issued, net of transaction costs. Accumulated share in other comprehensive losses of associates The Company recognized a reduction in equity amounting to $21.0 million as of December 2010, which was $57.5 million or 73.2% lower compared to the $78.5 million in 2009. This account reflects First Gen’s share in the translation of the peso-denominated balances of the Prime Terracota Group into U.S. Dollar, which is First Gen’s functional currency, effective May 2009. The reduction in this amount is due to the appreciation of the Philippine peso against the U.S. dollar from P46.20 in December 2009 to P43.84 in December 2010. Cumulative translation adjustments This contra-equity account increased by $6.7 million or 69.1% to reflect First Gen’ share in the translation of the peso-denominated balances of the subsidiaries and the unfavorable movements in the MTM valuation of FGPC’s and FGP’s interest rate swaps. As noted above, the appreciation of the Philippine peso against the U.S. dollar and the lower LIBOR rates in 2010 as compared to the previous year has led to the change in this account. Retained earnings First Gen’s retained earnings increased by $69.2 million or 20.9% resulting from the earnings accumulated during the year. The increase was partially offset by the $1.0 million stock dividend to the Parent company’s preferred shareholders. Non-controlling Interests This account increased by $14.7 million or 10.2% as a result of higher earnings, net of dividends received, from FGPC and FGP accumulated during the year.

18 | P a g e

FIRST GEN MATERIAL CHANGES IN FINANCIAL CONDITION (2009 vs. 2008)

Horizontal and Vertical Analyses of Material Changes for the years ended December 31, 2009 vs. 2008

CONSOLIDATED STATEMENTS OF INCOME

HORIZONTAL ANALYSIS VERTICAL ANALYSIS

(Amounts in USD thousands) Dec 2009 (Audited)

Dec. 2008 (Audited)

2009 vs. 2008

2009 vs. 2008 2009 2008

REVENUE Sale of electricity $1,009,918 $1,212,016 ($202,098) -16.7% 98.8% 6.0% Interest 6,942 9,079 (2,137) -23.5% 0.7% 0.7% Equity in net earnings of associates 1,167 3,530 (2,363) -66.9% 0.1% 0.3% Mark-to-market gain on derivatives -net – 12,190 (12,190) -100.0% 0.0% 1.0% Foreign exchange gains - net – 24,011 (24,011) -100.0% 0.0% 1.9% Others 4,089 1,572 2,517 159.9% 0.4% 0.1% TOTAL REVENUES 1,022,116 1,262,398 (240,282) -19.0% 100.0% 100.0% Fuel cost (669,832) (863,874) 194,042 -22.5% -65.5% -68.4% Depreciation and amortization (53,932) (54,026) 94 -0.2% -5.3% -4.3% Power plant operations & maintenance (37,624) (37,320) (304) 0.8% -3.7% -3.0% Staff costs (10,625) (12,027) 1,402 -11.7% -1.0% -1.0% Other administrative expenses (37,244) (49,263) 12,019 -24.4% -3.6% -3.9%

Sub-total (809,257) (1,016,510) 207,253 -20.4% -79.2% -80.5% Interest expense & financing charges (112,089) (121,417) 9,328 -7.7% -11.0% -9.6% Foreign exchange loss - net (8,691) – (8,691) 0.0% -0.9% 0.0% Mark-to-market loss on derivatives - net (922) – (922) 0.0% -0.1% 0.0% Other charges – (320) 320 -100.0% 0.0% 0.0%

Total (930,959) (1,138,247) 207,288 -18.2% -91.1% -90.2%

INCOME FROM CONTINUING OPERATIONS BEFORE INCOME TAX 91,157 124,151 (32,994) -26.6% 8.9% 9.8% Provision for (benefit from ) income tax

Current 45,492 31,448 14,044 44.7% 4.5% 2.5% Deferred (7,381) 18,472 (25,853) -140.0% -0.7% 1.5%

38,111 49,920 (11,809) -23.7% 3.7% 4.0%

Net income from continuing operations 53,046 74,231 (21,185) -28.5% 5.2% 5.9% Net income from discontinued operations 41,961 19,237 22,724 118.1% 4.1% 1.5%

NET INCOME $95,007 $93,468 $1,539 1.6% 9.3% 7.4%

Attributable to: Equity holders of the Parent Company $16,754 $14,474 $2,280 15.8% 1.6% 1.1% Non-controlling Interests 78,253 78,994 (741) -0.9% 7.7% 6.3%

Revenues decreased by 19.0% or $240.3 million to $1,022.1 million in 2009 from $1,262.4 million in 2008. The decrease was due to the major movements in revenue items as explained in detail below:

Revenues

19 | P a g e

Revenue from sale of electricity Revenues from the sale of electricity decreased by $202.1 million or 16.7% to $1,009.9 million in 2009 from $1,212.0 million in 2008, which resulted from lower fuel charges during the year as oil prices declined in the world market. Fuel revenues decreased by $199.4 million with gas prices averaging at $8.6/GJ (or $9.1/MMBtu) in 2009 versus $11.6/GJ (or $12.3/MMBtu) in 2008. The gas plants’ combined dispatch was marginally higher at 82.2% capacity factor in 2009 compared to 81.6% in 2008, making Santa Rita and San Lorenzo the highest dispatched in the Luzon grid. Mark-to-market (MTM) gain on derivatives The $12.2 million decrease in this account pertains to the non-recurring MTM gain on derivative transactions of First Gen that was recognized in 2008. The Company recognized a MTM loss on derivative transactions of $0.9 million in 2009, which was classified under “Costs and Expenses” account of the Company’s audited consolidated statements of income. Interest income Interest income decreased by 23.5% or $2.1 million to $6.9 million in 2009 from $9.1 million in 2008 as a result of lower interest income on Annual Deficiency by $2.8 million following scheduled Annual Deficiency payments by FGPC and FGP to the Gas Sellers. In addition, the Parent company and FGP recorded lower interest income from its cash balances by $1.7 million and $0.7 million, respectively. These were partly offset by higher interest income of FGPC by $3.1 million due to interest earned on advances made to its non-controlling shareholder. Equity in net earnings of associates Equity in net earnings of associates decreased by $2.4 million with the deconsolidation effective May 2009. Beginning May 2009, equity in net earnings of associates include the combined share in net earnings from the deconsolidated subsidiaries; namely, Prime Terracota, Red Vulcan, EDC, and FG Hydro. The combined amount from the deconsolidated subsidiaries from May 2009 to December 2009 is a net loss of $3.5 million due to interest expenses at Red Vulcan and Prime Terracota, which offset earnings from EDC. Earnings from the deconsolidated subsidiaries for the periods January to April 2009 and the whole year of 2008 are reflected under “Net income from discontinued operations” in the consolidated statements of income. Prior to the deconsolidation, equity in net earnings only included share in net earnings from BPPC. The lower earnings from the deconsolidated subsidiaries, reflected in equity in net earnings of associates, were offset by the higher share in net earnings of BPPC by $1.2 million in 2009. Foreign exchange gains - net No unrealized foreign exchange gain was recognized in 2009 as compared to a $24.0 million foreign exchange gain recognized in 2008. The foreign exchange gain in 2008 was mainly due to the unrealized foreign exchange gain on the Peso bond as a result of the depreciation of the Philippine Peso against the US dollar. The Company recognized unrealized foreign exchange loss of $8.7 million in 2009 which was included as part of “Costs and Expenses” in the consolidated statements of income. Other revenues The $2.5 million increase in Other revenues in 2009 pertains to consultancy fees received by First Gen from EDC, which started in September 2008.

Costs and operating expenses for the year ended December 31, 2009 posted a net decrease of $207.3 million or 20.4% to $809.3 million as compared to $1,016.5 million in 2008 as a result of the following movements:

Costs and Operating Expenses

Fuel cost Fuel cost decreased by $194.0 million or 22.5% in 2009 due to lower gas prices in 2009.

20 | P a g e

Staff costs Staff costs decreased by $1.4 million or 11.7% due to a lower provision for retirement expenses in 2009 and higher weighted average foreign exchange rate in 2009 (P47.769:$1.00) compared to the rate in 2008 (P43.970:$1.00) that was used to convert the Peso-denominated expenses to its US dollar equivalent. Other administrative expenses Other administrative expenses decreased by $12.0 million or 24.4% in 2009 due to lower professional fees by $4.3 million and lower taxes and licenses by $6.7 million at the Parent company level. The higher professional fees and taxes and licenses in 2008 pertain to underwriting fees, legal fees, and documentary stamp taxes associated with various loans availed during the previous year. Taxes and licenses in 2008 also include the capital gains tax on the sale of First Gen’s 60% stake in FG Hydro.

Interest expense and financing charges decreased by $9.3 million or 7.7% to $112.1 million in 2009 from $121.4 million in 2008. The decrease was due to a decrease in interest expense on loans of the Parent company and FGP by $19.2 million and $3.0 million, respectively, after paying down debt during the year. In addition, interest expense on Annual Deficiency payable to the gas sellers decreased by $2.8 million following the scheduled payments made on the Payment Deferral Agreement. These were partly offset by higher interest expense in FGPC after the refinancing of its loans in November 2008 and the issuance of UHC’s P5.4 billion corporate notes, which increased interest and financing expense by $7.4 million and $6.9 million, respectively.

Interest expense and financing charges

The Company recognized an unrealized foreign exchange loss of $8.7 million in 2009 pertaining to unrealized foreign exchange loss on UHC’s P5.4 billion corporate notes and the Parent company’s Peso bond as a result of the appreciation of the Philippine Peso against the U.S. dollar.

Foreign exchange loss – net

The Company recognized a MTM loss on derivative transactions of $0.9 million in 2009 as compared to the MTM gain on derivative transactions of $12.2 million recognized in 2008, which was included as part of “Revenues” in the consolidated statements of income. The derivative loss was due to the change in the fair value of First Gen’s Convertible bonds.

MTM loss on derivatives

The Company recognized a lower provision for income tax by $11.8 million or 23.7% of $38.1 million in 2009 as compared to 2008. The decrease was primarily due to the recognition of a benefit from deferred income tax of $7.4 million in 2009 versus an $18.5 million provision that was recognized in 2008 resulting from the movements in foreign exchange rate of the Philippine Peso against the U.S. dollar. The benefit from deferred income tax was partly offset by higher current income tax of FGP by $13.5 million due to the expiry of its income tax holiday in February 2009.

Provision for (benefit from) Income Tax

First Gen’s consolidated net income increased by $1.5 million or 1.6% to $95.0 million in 2009 from $93.5 million in 2008. Of the total net income in 2009, $53.0 million is net income from continuing operations and $42.0 million pertains to the net income from January to April 2009 of the recently deconsolidated subsidiaries of First Gen. The relatively flat change in consolidated net income was a result of the offsetting movements of the following items:

Net Income

• Net income from discontinued operations which pertains to the net income of the Prime Terracota

Group for the months of January to April in 2009 and January to December in 2008 increased by $22.7 million in 2009. This is mainly due to lower interest expense at Red Vulcan level after reducing debt in 2009 and foreign exchange gains of EDC during the year.

• Administrative expenses were lower in 2009 by $13.4 million due to lower provision for retirement expenses, and lower professional fees and tax expenses. The Company incurred higher professional fees and tax expenses in 2008 from underwriting fees, legal fees, and documentary stamp taxes associated with various loans availed in 2008.

21 | P a g e

• The Company recognized lower provision for income tax by $11.8 million in 2009 as a result of changes in deferred tax liabilities due to the appreciation of the Philippine peso against the U.S. dollar in 2009.

• Interest expense and financing charges decreased by $9.3 million due to lower interest expense at the Parent company level as a result of the Company’s debt reduction program.

• Other revenues were higher by $2.5 million as a result of the recognition of consultancy fees from EDC.

The above gains were offset by the following: • First Gen group incurred a foreign exchange loss of $8.7 million in 2009, in contrast with the

foreign exchange gain of $24.0 million recognized in 2008. • The Parent company incurred a loss on derivative liabilities of $0.9 million resulting from the

change in the fair value of the Convertible bonds. This is a reversal of the MTM gain on derivative liabilities recognized in 2008 of $12.2 million.

• A $6.4 million gain was recognized in 2008 pertaining to monetized banked gas as compared to in 2009.

• Equity in net earnings decreased by $2.4 million due to the recognition in this account of Red Vulcan and Prime Terracota’s interest expense covering the months of May to December 2009.

• Interest income decreased by $2.1 million mainly due to lower interest on cash at the Parent company.

• Capacity charges slightly decreased by $2.3 million or 1.0% due to lower NDC of Santa Rita and San Lorenzo as a result of normal plant degradation.

Of the $95.0 million consolidated net income in 2009, net income attributable to the Parent company amounted to $16.8 million, $2.3 million or 15.8% higher than the $14.5 million net income attributable to the Parent company in 2008.

Adjusting for non-recurring items in 2009 such as foreign exchange gains/losses, deferred income taxes, and the write-down of EDC’s deferred tax assets, recurring net income in 2009 attributable to First Gen is $34.2 million. This is $15.5 million or 83.2% higher than recurring net income in 2008 of $18.7 million, which can be mostly attributed to lower interest expense at the Parent company and Red Vulcan.

(Amount in USD thousands) 2009 2008 Net income attributable to the Parent company $16,754 $14,474 Adjustment of non-recurring items:

Movement in deferred income tax of FGPC and FGP (4,428) 11,083 Monetized banked gas – (6,369) Arbitration gain of EDC – (32,515) Write-down of EDC’s deferred tax assets 22,765 – Unrealized foreign exchange losses (gains) of the

Parent company, FGPC, FGP, UHC 8,690 (23,999) Unrealized foreign exchange loss (gain) EDC (9,035) 70,378 Unrealized foreign exchange loss (gain) of FG Hydro (1,463) 5,658 MTM loss (gain) on derivatives of Parent company and EDC 922 (20,036)

Recurring Net Income attributable to Parent company $34,205 $18,674

22 | P a g e

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION Horizontal and Vertical Analyses of Material Changes as of December 31, 2009 and 2008

HORIZONTAL ANALYSIS

VERTICAL ANALYSIS

Increase (Decrease)

Dec-09 Dec-08 2009 vs. 2008

(Amounts in USD Thousands) (Audited) (Audited) Amount % Dec-09 Dec-08 ASSETS

Current Assets Cash and cash equivalents $125,531 $229,647 ($104,116) -45.3% 5.8% 6.2%

Receivables 121,334 244,996 (123,662) -50.5% 5.6% 6.6% Inventories 65,072 76,206 (11,134) -14.6% 3.0% 2.1% Available-for-sale (AFS) financial assets – 14,194 (14,194) -100.0% 0.0% 0.4% Derivative asset – 12,923 (12,923) -100.0% 0.0% 0.3% Other current assets 34,578 49,508 (14,930) -30.2% 1.6% 1.3%

346,515 627,474 (280,959) -44.8% 16.0% 17.0%

Noncurrent assets held for sale – 38,067 (38,067) -100.0% 0.0% 1.0% Total Current Assets 346,515 665,541 (319,026) -47.9% 16.0% 18.0% Noncurrent Assets

Investments in associates 1,020,722 20,958 999,764 4770.3% 47.2% 0.6% Property, plant and equipment 562,238 736,262 (174,024) -23.6% 26.0% 19.9% Intangible assets 17,972 1,301,651 (1,283,679) -98.6% 0.8% 35.2% Deferred income tax assets 10 71,794 (71,784) -100.0% 0.0% 1.9% Long-term receivables - net of current portion – 652,831 (652,831) -100.0% 0.0% 17.7% Other noncurrent assets 213,566 248,840 (35,274) -14.2% 9.9% 6.7% Total Noncurrent Assets 1,814,508 3,032,336 (1,217,828) -40.2% 84.0% 82.0%

TOTAL ASSETS $2,161,023 $3,697,877 ($1,536,854) -41.6% 100.0% 100.0%

LIABILITIES AND EQUITY Current Liabilities Loans payable $– $200,461 ($200,461) -100.0% 0.0% 5.4%

Accounts payable and accrued expenses 104,451 231,216 (126,765) -54.8% 4.8% 6.3% Income tax payable 7,543 1,836 5,707 310.8% 0.3% 0.0% Due to related parties 6,711 7,056 (345) -4.9% 0.3% 0.2% Obligations to Gas Sellers on Annual Deficiency 9,378 36,696 (27,318) -74.4% 0.4% 1.0% Current portion of:

Bonds payable 107,984 – 107,984 0.0% 5.0% 0.0% Long-term debt 46,499 518,101 (471,602) -91.0% 2.2% 14.0%

Derivative liabilities – 1,142 (1,142) -100.0% 0.0% 0.0%

Total Current Liabilities 282,566 996,508 (713,942) -71.6% 13.1% 26.9%

Noncurrent Liabilities Bonds payable – net of current portion 277,353 362,978 (85,625) -23.6% 12.8% 9.8% Long-term debt – net of current portion 700,324 1,073,285 (372,961) -34.7% 32.4% 29.0% Derivative liabilities - net of current portion 25,335 59,861 (34,526) -57.7% 1.2% 1.6% Retirement and other post-retirement liability 167 24,899 (24,732) -99.3% 0.0% 0.7% Deferred income tax liabilities – net 18,609 30,036 (11,427) -38.0% 0.9% 0.8%

Other noncurrent liabilities 49,632 131,899 (82,267) -62.4% 2.3% 3.6%

Total Noncurrent Liabilities 1,071,420 1,682,958 (611,538) -36.3% 49.6% 45.5%

TOTAL LIABILITIES 1,353,986 2,679,466 (1,325,480) -49.5% 62.7% 72.5%

Equity Attributable to Equity Holders of the Parent Company

23 | P a g e

Redeemable preferred stock 13,561 9,572 3,989 41.7% 0.6% 0.3% Common stock 45,917 20,624 25,293 122.6% 2.1% 0.6% Additional paid-in capital 320,453 319,530 923 0.3% 14.8% 8.6%

Deposits for future stock subscriptions 93,318 – 93,318 0.0% 4.3% 0.0%

Accumulated share in other comprehensive losses of associates (78,516) – (78,516) 0.0% -3.6% 0.0% Cumulative translation adjustments (9,642) (136,645) 127,003 -92.9% -0.4% -3.7% Accumulated unrealized gain on AFS financial assets – 382 (382) -100.0% 0.0% 0.0% Equity reserve – (28,383) 28,383 -100.0% 0.0% -0.8% Retained earnings 330,930 354,137 (23,207) -6.6% 15.3% 9.6% Cost of preferred and common stock held in treasury (52,987) (80,557) 27,570 -34.2% -2.5% -2.2%

663,034 458,660 204,374 44.6% 30.7% 12.4%

Non-controlling Interests 144,003 559,751 (415,748) -74.3% 6.7% 15.1%

Total Equity 807,037 1,018,411 (211,374) -20.8% 37.3% 27.5%

$2,161,023 $3,697,877 ($1,536,854) -41.6% 100.0% 100.0%

Cash and cash equivalents This account consists mainly of cash on hand and in banks. Cash equivalents include cash investments with original maturities of less than three months. Cash and cash equivalents decreased by 45.3% or $104.1 million to $125.5 million as of December 31, 2009 as compared to $229.6 million as of December 31, 2008. The decrease is mainly due to the higher cash balances of FGPC and FGP as of December 31, 2008 since payments to Gas Sellers on the November 2008 fuel charges were already made in January 2009. The decrease in this account was also due to the deconsolidation of cash and cash equivalents of EDC and FG Hydro amounting to $16.3 million and $3.9 million, respectively, as of December 31, 2008. Receivables Receivables decreased by 50.5% or $123.7 million to $121.3 million as of December 31, 2009 from $245.0 million as of December 31, 2008 after the deconsolidation of EDC’s and FG Hydro’s receivables amounting to $154.8 million. The decrease was partly offset by the higher trade receivables from FGPC and FGP by $28.5 million. Receivables from Meralco as of December 31, 2009 still include the November 2009 billings which were paid by Meralco in January 2010. Available-for-sale (AFS) financial assets The $14.2 million decrease in AFS financial assets was due to the deconsolidation of EDC. This account previously included EDC’s investments in dollar-denominated ROP bonds. Inventories The decrease in this account by 14.6% or $11.1 million was due to the deconsolidation of EDC’s inventories amounting to $32.2 million as of December 31, 2008. This was partly offset by higher fuel inventory of Santa Rita and San Lorenzo by $21.1 million due to liquid fuel purchases made during the year in preparation for the scheduled maintenance outage of the Malampaya gas plant in February 2010. Derivative asset The decrease of $12.9 million was primarily due to the deconsolidation of EDC and FG Hydro in May 2009. The balance in 2008 includes EDC’s freestanding derivative transactions, particularly the range bonus forward contracts and the foreign currency forward contracts; and FG Hydro’s embedded foreign currency options on the contract with Andritz Hydro, GmbH for the Pantabangan Refurbishment and Upgrade Project (PRUP). Other current assets The net decrease in other current assets by 30.2% or $14.9 million was primarily due to the deconsolidation of EDC’s current assets amounting to $12.6 million and the application of prepaid taxes against various taxes totaling to $4.8 million.

24 | P a g e