A CRISIS IN C: CORONA, CONSUM PTION, CURRENCY, CONTRACTS · March 2020 – issue 159 A CRISIS IN C:...

12

March 2020 – issue 159 A CRISIS IN C: CORONA, CONSUMPTION, CURRENCY, CONTRACTS... OPINION 2 The purpose of this editorial is to present an overview of the main impacts of Covid-19 on the Brazilian electricity sector and to discuss general principles for the sector to address this challenge. REGULATORY In this section, we discuss the new measures approved by ANEEL due to the Covid-19 pandemic and other relevant issues that moved during the month. WATER RESOURCES AND EVIRONMENT This section presents an analysis of the market and technological mechanisms for reducing greenhouse gas (GHG) emissions to combat climate change. INTERNATIONAL In this section, we analyze the impacts of the socio-economic crisis caused by the coronavirus on the global electrical markets, especially on the behavior of demand and electricity prices. INNOVATION In this section, we discuss the innovative adaptation of technologies to face the Covid-19 crisis, exemplified by the temperature measurement. STRUCTURAL SUPPLY ANALYSIS It presents the updated balance of demand and structural energy supply for the coming years and our traditional delay meter. ABOUT THE ENERGY REPORT 12 The Energy Report is a PSR publication exclusively for subscribers. Suggestions and comments can be sent to [email protected]. Seeking to contribute more information to the intense debate about the impacts of the new Coronavirus pandemic on the electricity sector and due to its socioeconomic consequences, PSR decided to make this month’s editorial available for free to society, which discusses this topic and general principles for the sector to address this challenge. The remaining sections are available exclusively to subscribers. More information about subscription and access in the “About the Energy Report” section.

Transcript of A CRISIS IN C: CORONA, CONSUM PTION, CURRENCY, CONTRACTS · March 2020 – issue 159 A CRISIS IN C:...

March 2020 – issue 159

A CRISIS IN C: CORONA, CONSUMPTION, CURRENCY, CONTRACTS...

OPINION 2

The purpose of this editorial is to present an overview of the main impacts of Covid-19 on the Brazilian

electricity sector and to discuss general principles for the sector to address this challenge.

REGULATORY

In this section, we discuss the new measures approved by ANEEL due to the Covid-19 pandemic and

other relevant issues that moved during the month.

WATER RESOURCES AND EVIRONMENT

This section presents an analysis of the market and technological mechanisms for reducing greenhouse

gas (GHG) emissions to combat climate change.

INTERNATIONAL

In this section, we analyze the impacts of the socio-economic crisis caused by the coronavirus on the

global electrical markets, especially on the behavior of demand and electricity prices.

INNOVATION

In this section, we discuss the innovative adaptation of technologies to face the Covid-19 crisis,

exemplified by the temperature measurement.

STRUCTURAL SUPPLY ANALYSIS

It presents the updated balance of demand and structural energy supply for the coming years and our

traditional delay meter.

ABOUT THE ENERGY REPORT 12

The Energy Report is a PSR publication exclusively for subscribers. Suggestions and comments can be

sent to [email protected].

Seeking to contribute more information to the intense debate about the impacts of the new Coronavirus pandemic on the electricity

sector and due to its socioeconomic consequences, PSR decided to make this month’s editorial available for free to society, which

discusses this topic and general principles for the sector to address this challenge. The remaining sections are available exclusively to

subscribers. More information about subscription and access in the “About the Energy Report” section.

All rights reserved © PSR 2

OPINION

Very often, lectures and motivational texts claim that the word "crisis" in Mandarin is composed of the

ideograms for “danger (or risk)” - wēi (危) - and “opportunity” – jī (机). Just as often, this statement

is contested by those who know the language.1 The bone of contention is the second ideogram, which

instead of "opportunity" means "a crucial point when something important starts to change". In other

words, a tipping point.2

In the "day after", will the immense social, political, and economic changes that are taking place abruptly

around the world, unprecedented in recent history, be a total disaster?

The first Black Swan:3 the new Coronavirus

The pandemic of the new Coronavirus, or Covid-19, placed the world before the most severe test of

public health and economic resilience in the contemporary era and led to measures unprecedented in

modern history. Examples include the ongoing lockdown in several nations, as well as the synchronized

actions taken by central banks in major economies to ensure liquidity, reduce volatility in the capital

market, and the smooth functioning of the global financial system. The easing of monetary policy

around the world, with interest rates falling to historically low levels, the reduction of compulsory

deposit rates, in addition to fiscal stimulus measures to support families, self-employed and informal

workers and companies, are also being adopted to try to absorb the most severe impacts of this pandemic

on the economy.

Another characteristic of the pandemic is the immense uncertainty about crucial information, such as:

mortality rate; speed of contagion; whether infected persons, in particular asymptomatic ones, become

immune; when will a vaccine and/or treatment be available etc. Consequently, any scenario built at this

time about the intensity that the public health crisis will have on the macroeconomic dynamics around

the world and in Brazil is necessarily speculative.

Obviously, the same uncertainty about the overall impacts of the pandemic exists in the case of the

electricity sector. There is currently much speculation about the magnitude of these impacts, which will

be the main agents affected, how and what will be the ways to resolve the issues. The truth is that we

don't even know if we have reached the well’s bottom on economic impacts, or if the well is deeper.

Aiming to contribute to the debate with information, analysis, and rationality, PSR made a preliminary

analysis of the impact of Covid-19 with an extraordinary edition of its EnergyCast4, which created strong

1 https://en.m.wikipedia.org/wiki/Chinese_word_for_%22crisis%22 2 https://en.wikipedia.org/wiki/The_Tipping_Point 3 It is worth mentioning that the mathematician, statistician and author Nassim Taleb and creator of the expression “black

swan”, used to define great events that are unexpected and that bring great consequences (good or bad), do not consider

Coronavirus a “black swan”. In fact, he considers it to be predictable, especially after other pandemics caused also by

coronaviruses, such as SARS and MERS. In other words, it was not a question of "if", but of "when". 4 Available ( only in Portuguese) on major streaming platforms, such as Spotify:

https://open.spotify.com/episode/6qKzJoWGd3d2RT5al2FsMB

In PSR’s view, this interpretation of crisis as a “danger that leads to a tipping point” is perhaps the

most adequate to analyze the simultaneous impacts of two “black swans”: the Covid-19 pandemic

and the collapse of oil prices.

All rights reserved © PSR 3

interest, with more than 1200 auditions in the first week. More recently, we made a new edition that

discusses, in conversation with the strategic consultancy MacroPlan, possible scenarios for Brazil in

2020.

The second Black Swan: Fuels

“It's the End of the World as We Know It”, by the rock band R.E.M., can be a good title for the hellish

prospects of the crisis. However, the full title has an additional expression in parentheses - “(And I Feel

Fine)”, which can help explain the oil price crisis, which occurred almost simultaneously with Covid-

19. As will be seen below, the resulting crisis is a perfect example of the “Law of unintended

consequences”5.

Demand collapse (surprise)

With the adoption of social isolation measures, including travel restrictions, as well as a slowdown in

the global economy due to the uncertainties of the Coronavirus crisis, the demand for oil has collapsed.

By the beginning of 2020 the world consumed an average of 100 million barrels of oil per day. With the

crisis, this consumption fell 20% in February 2020.

Price war (on purpose)

Additionally, the dynamics of the oil market worldwide changed in recent years due to two factors: (i)

the rise of the shale oil industry, which transformed the United States from an importer to an

increasingly important exporter of fossil fuels (third largest in the world); and (ii) the alliance between

Saudi Arabia and Russia, the two largest oil exporters, to contain the growth of the American shale

industry. However, Russians and Saudis, who since 2016 had agreed to jointly manage the oil market,

disagreed at the beginning of March this year. After a round of OPEC discussions in Vienna, Russia did

not agree with the Saudi proposal to cut production by 1.5 million barrels per day, arguing that such a

move would only serve to support further growth in oil production by the United States. Saudi Arabia

decided to double the bet and start an unexpected war: it retaliated against the Russian attitude by

lowering its prices and promising to release its unused capacity in the oil market.

Price collapse (unintended consequence)

The combination of (purposeful) increased supply and (involuntary) reduced demand was lethal: the

price of Brent (international reference for oil price) went from about $ 50 to $ 20 in a few weeks (see

figure below), a price level not seen in decades6.

5 https://en.wikipedia.org/wiki/Unintended_consequences 6 If corrected by American inflation, this is the lowest price observed for Brent since 1973, the year of the oil crisis.

The purpose of this edition of the Energy Report is to continue the discussion of these EnergyCasts,

presenting an overview of the main impacts of Covid-19 in the electricity sector, and discussing

general principles for the sector to address this challenge.

All rights reserved © PSR 4

Global impact of the price collapse

The impacts of the new oil price scenario are severe: on the investment side, it affects the competitiveness

of oil production from new deep-water fields, such as the Brazilian Pre-Salt. On the side of existing

supply, it affects the production of American shale oil (and gas), in addition to increasing inventories7

and contributing to an even greater reduction in price. And this “shock” will affect the geopolitics of oil.

At this time (end of March), the global demand8 for oil is about 25% lower than the values forecasted

for this time of year. The transportation sector is responsible for about 60% of the demand for oil;

currently, the demand for fuels in strategic sectors such as aviation has fallen by more than 70%.

Consequently, excess production has been stored and has caused the occupation of the entire American

crude oil storage infrastructure; this has been occurring around the world. There are physical markets

trading oil below $ 10 a barrel (depending on quality), with exceptional cases of negative prices in the

United States.

Obviously, there are many doubts about future oil prices. In PSR's view, the current price is

unsustainable in the medium and long term for many members of OPEC, including the Saudis

themselves,; like many other countries, they are heavily dependent on revenue from the sale of their oil.

The price recovery will depend on a combination of three factors: a change in OPEC's stance, which

could cut global production; an automatic cut in the production of American shale oil due to its

unfeasibility at this price level; and the recovery in demand, now depressed by the Covid-19 pandemic.

However, the reality is that the current oil price level, if it persists, will affect the electricity sector, as

discussed below.

Other impacts and the electricity sector

Many other impacts describe the current global crisis in the electricity sector: consumption, climate,

fuels, capex, foreign exchange, credit, cost of debt, reliability, and investor behavior.

7 Currently, there is a problem even for the storage of the world production of crude oil. 8 World oil consumption is in the order of 100 million barrels per day, with the transportation sector accounting for 60% of

this volume.

Returning to the R.E.M. song, in the oil industry we arrived at “the end of the world”, but there are

countries that still “feel fine”.

All rights reserved © PSR 5

Consumption

The global economy is likely to enter a recession this year, the world GDP may drop by 3% in some

projections made by the financial market, caused by the likely North American recession, the significant

activity reduction in China and a sharp GDP drop in rope.

Therefore, the first and natural impact of Covid-19 in the energy sector (and in particular in the

electricity sector) is the reduction in consumption due to the global lockdown. Numerous analyzes have

been carried out internationally on these

impacts.

The graph on the right illustrates one of them,

prepared from ENTSO-e data: the reduction in

the average daily demand of 6 European

countries compared to the 2019 values. The

reduction in electricity consumption has been

very strong. This panorama has also been

observed in other energy sources, such as oil,

gas, etc.

Climate

The reduction in consumption immediately

affects global emissions of CO2 and

particulates, which in turn improve local

pollution. Statistics on these impacts are still being compiled. However, some information from

satellites is available.

The following figures illustrate, from satellite images, emissions of

nitrogen dioxide (NO2), an important pollutant, observed in

Wuhan, China, France and Italy (source: NASA):

The relative competitiveness of sources

The impact of reduced oil prices discussed above occurs in several ways: on the competitiveness of

electric cars against fossil fuel vehicles (the latter becoming more competitive); on the attractiveness of

energy efficiency (most of the time aiming at replacing energy sources); and on the price of natural gas.

All rights reserved © PSR 6

The global reduction in energy demand has pushed Henry Hub natural gas prices to very low levels,

around 1.6 USD / MMBtu, a level not seen since 1995. This price, if sustainable, will naturally increase

the economic competitiveness of natural gas power plants.

Capex and Currency

Another important impact affects long-term energy prices: the investment cost (or “Capex”) of new

infrastructure projects, in particular generation and transmission. This will possibly decrease, due to

excess equipment caused by the reduction in global demand. This reduction can be offset by the

exchange rate in the case of imported equipment: risk aversion coupled with low levels of interest rates

in the world continue to produce an appreciation of the dollar against other currencies, especially those

of emerging countries.

Credit and cost of debt

The financial crisis will impact companies' cash flow, increasing default risks (credit), and with

repercussions in the credit market. Even if the current scenario is of a very low, or even negative, global

interest rate, the global economic behavior resulting from the strong financial injections by United

States and Europe, aiming to keep the economy alive, is uncertain.

Reliability and behavior

The drop in electricity consumption should lead to lower wholesale electricity prices, causing a repricing

of assets. In turn, confinement and logistical restrictions may affect the operation and maintenance of

generating units. The resulting effect on supply reliability has been a concern by system operators in

several countries. In general, the Covid-19 crisis will increase the investors’ risk aversion, causing a

search for less risky assets.

In summary...

The previous list of impacts is not exhaustive and only illustrates the countless possibilities of severe

economic impacts due to the Covid-19 lockdown. It is not possible yet to make any credible conjecture

about how these impacts will affect the market fundamentals after the end of the crisis, precisely because

the path of recovery is still uncertain.

Impacts on the Brazilian electricity sector: “Wake up Dead”?

“Wake up dead”, by the heavy metal band Megadeth, tells the story of a person who was in a pleasant

dream and afraid to wake up from it. This dream became a nightmare, and the fear of “waking up dead”

became real. Similarly, 2020 started very promisingly for the sector: bills with excellent approval

prospects in the Senate and the Chamber signaled that the long-awaited modernization was underway.

The question is whether Covid-19 turned this dream into a nightmare.

These items are discussed below.

In PSR's opinion, the two biggest impacts will result from reduced demand and default. In addition,

the effects of the fuel and foreign exchange market will impact tariffs and prices, and confinement

and travel restrictions may also affect construction and maintenance schedules. Finally, the regulatory

and legislative agenda will have another dynamic.

All rights reserved © PSR 7

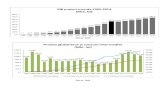

Market reduction impacts

Due to confinement,

consumption in Brazil

already is significantly lower

than that of previous weeks,

as shown in the figure.

Moreover, given that a

significant part of retail and

electro-intensive industries

only started their lockdown

in the last week of March, further reductions are expected. From the physical point of view, any demand

reduction will be “stored” in the reservoirs, improving the supply situation. However, there are

numerous relevant commercial impacts:

• The decreased load reduces the need for thermoelectric dispatch, which impacts the PLD, and in

turn affects the sale of energy and consumer tariffs.9

• It also impacts the GSF, increasing hydraulic displacement, which also affects sales and tariffs.10 But

in this case, the economic effect on GSF will depend on its combination with PLD, that is, the increase

in exposure to the short-term market for hydroelectric plants caused by the greater hydraulic

displacement can be offset by a lower PLD.

• The market reduction increases the uncertainty in the volumes of the generation and transmission

auctions. And, mainly, it impacts the distributors' financial situation, caused by the potential over-

contracting. As the excess contract is "sold" at a reduced PLD, there is a financial loss. This situation

also affects free consumers.

• Even in the case of distributors, the load reduction affects the revenues of everything that is

remunerated by MWh billed, such as the CDE account. Because many of the costs covered by CDE

are fixed, this account will become financially unbalanced.

An important uncertainty factor is the recovery curve for load after the crisis, and, above all, what the

"new economy" will look like. It may redefine growth vectors, consumption profiles, econometric

relations, forecast models etc.

Default and force majeure in contracts

The economic situation creates the threat of "force majeure" in contracts. Initially, it can occur due to

the over-contracting of consumers, who can ask for a review of the volumes. But it can also occur due

to the inability to pay, increasing the risk of default in the value chain altogether. The halt in the import

of goods necessary for the feasibility of projects can also cause construction delays, with associated

penalties. Additionally, the lockdown itself is already causing problems, such as municipal decrees that

forbid plants in some locations to operate. We expect many requests to classify events as “fortuitous” or

“force majeure” in order to inhibit the application of contractual fines for non-compliance to

generators, transmitters, and distributors.

9 The availability contracts pass on to the consumer the purchases in the short-term market when the thermals are not activated. 10 The contracts for quotas of physical guarantee of energy pass the hydrological risk to the consumer.

70

61

45

55

65

75

85

14/mar 15/mar 16/mar 18/mar 19/mar 21/mar 22/mar 24/mar 25/mar

Dem

adna SIN [GW]

Fonte: Operador Nacional do Sistema

Demanda horária em março Demanda

Média sem. 2

Média sem. 3

All rights reserved © PSR 8

Exchange rate and energy prices

Higher exchange rates and lower energy prices (oil and gas) impact the variable unit cost (CVU) of

thermal plants, which in turn affects the economic merit order for the dispatch of generating units. This

will affect thermal dispatch and PLD, with impacts on the supply chain, tariffs to final consumers and

“availability contracts” of thermal plants. A lower oil price also affects the profitability of pre-salt oil,

and a lower gas price improves the economic competitiveness of gas-fired power plants for renewables.

The extreme uncertainty in the above factors creates great difficulty for investors to prepare their bids

for the auctions. In addition, bids made under extreme uncertainty are more likely to be economically

unbalanced and cause problems in the future. Finally, there is an increased risk of over-investments

caused by uncertainty in demand growth, with tariff impacts for the consumer. For these reasons,

postponing auctions is a prudent decision11.

Legislative agenda

The agendas of the Chamber and the Senate are currently, and correctly, centered on the release of

resources for the health system and to minimize the damage to those economically affected by Covid-

19. The parliamentary recess begins in about three months, and we will have a second semester centered

on municipal elections. So, unfortunately, but objectively, we see little room for any progress to be made

on the first half of the reforms that were under accelerated discussion before the Covid-19 crisis, such

as PLS 232 and the bill to settle past GSF debts.

PSR’s immediate concern about legislative actions is as follows: there are already initiatives that seek to

forbid the interruption of electricity, telephone, gas, and water and sewage services to consumers. Some

refer specifically to the current situation of the COVID-19 epidemic, others deal widely with pandemics

or a public calamity situation. These measures are an understandable reaction in times of crisis, but they

can have a significant impact on the distributors if approved without a proper impact analysis. Measures

that provide for the use of R&D resources and energy efficiency to fund subsidies in the energy tariff for

three months are also being discussed, easing the pressure from the states that seek to prevent the power

cut, which would favor default, thus affecting revenues.

Regulatory agenda

Similar to the Legislative agenda, PSR believes that ANEEL's regulatory agenda will deal mostly with

issues associated with Covid-19, especially in articulation with the MME and the legislature in the

preparation of bills that may be needed to resolve the crisis.

11 On March 28th, 2020, the Ministry of Mines and Energy published Ordinance No. 134, postponing, for an indefinite period,

the A-4 and A-5 auctions of existing energy, the A-4 and A-6 of new energy, transmission auctions scheduled for 2020, 2021

and 2022 (according to MME Ordinance No. 15, of January 13th, 2020), and supply auctions for isolated systems.

In PSR's opinion, defaults are the most worrying factor. The possibility of non-payment in cascade

can impact the financial health of the sector, affecting payments to the various counterparties within

the commercialization segment. In turn, the default in the distribution segment can affect the

payments of generators and transmitters.

All rights reserved © PSR 9

So far, ANEEL has approved several measures to guarantee the continuity of the energy distribution

service, protecting consumers12 and employees. The measures will be valid for 90 days, may be extended,

and have commercial impacts.

ANEEL, however, has not yet begun to discuss the major commercial impacts on companies, such as

defaults, over-contracting, delays, penalties, etc. This agenda should overlap with the one mentioned

above, consequently postponing the decision on important issues such as the revision of Normative

Resolution No. 482.

Looking ahead: “Oh no, no ... please God help me”

"Oh no, no ... please God help me", by Black Sabbath, is a phrase that many sector agents, without

knowing this song, have been saying . In PSR's view, this sentence illustrates the extent of the confusion

about the above business consequences to the sector.

The distribution segment will be the most affected due to demand reduction, defaults, and a brutal drop

in tax collection and tariff increases of an already high tariff. The transmission sector, which is not

vulnerable to market risks, is now vulnerable to the risk of default. This risk also affects generation,

which will be impacted by a repricing of its energy value.

This crisis will also create opportunities in some areas. For example, the wholesale and retail price

differential will increase, making the free market and distributed generation more competitive.

However, this can hasten the “death spiral” of distribution companies and, thus, increase the

responsibility for an orderly opening of the market. Those topics will be discussed in a next Energy

Report.

Returning to the impacts on the sector, the most relevant question is: and what can be done?

The range of solutions “out there”

Firstly, it is worth looking at what is happening "out there", where the situation is just as serious. The

reality is that, so far, no country has stopped to think of a structural solution for its electricity sector; the

absolute priority has been patient care at Covid-19. The companies' cash has been used in this moment

of emergency and, until now, the range of solutions discussed to recover the sector includes: (i) Europe:

Treasury contributions or state intervention, with potential nationalization of assets; (ii) United States:

government support and use of the financial market, taking advantage of lower interest rates. In both

places, a strong wave of mergers and acquisitions is expected.

The range of solutions “in here”

PSR does not currently have a set of proposals to manage the factors mentioned in this report. Even

because these solutions depend on knowing the size of the consequences of the crisis, which is still

unknown. The fact is that the crisis is still under way and the size of its impact cannot yet be estimated.

12 The main measure with a commercial impact is that which prohibits the suspension of supply due to default by urban and

rural residential consumer units, including low income, in addition to services and activities considered essential, cf. legislation.

The most immediate problem in the sector is the cash position of agents, especially distributors,

which needs to be addressed quickly for minimum operation.

All rights reserved © PSR 10

The solution of this item is fundamental, it requires a quick execution and illustrates that the sector will

demand a package of solutions in the very short term, separated from another of short and medium

term, and of complex articulation. The BNDES, which can be an important player, has its own deadlines

for action. The Treasury, from where resources could come more quickly, is focused on addressing the

country's social and economic problems. Because of the possibility of economic and social disruptions,

the electricity sector needs strong and fast attention and priority, due to the importance of electricity

supply to the population at this time.

Looking at short and medium-term solutions, PSR believes that a systemic approach with some level of

coordination is essential, without preventing individual actions and solutions by associations and

companies.

PSR has been intensely discussing several alternative strategic paths. The sector will have a (natural)

conflict between proposed solutions that preserve companies, segments and/or the electricity sector

itself. There will also be proposals which require different degrees of government interference in

business environments. In other words, the situation is complex, the sector needs to find systemic

solutions, consistent with the current overall business environment.

In general, PSR believes that the “export” of risks from one segment to another should be avoided, and

that the range of solutions possibly includes: (i) a solution for immediate cash infusion to the sector

aiming at its sustaintability; (ii) application of existing regulatory mechanisms (MCSD, MVE,

assignment of contracts, etc.) to mitigate as much as possible the risks of demand reduction to the

distributor (we recognize, however, that these mechanisms are likely to be insufficient); (iii) financing

the allocation of residual impacts along the value chain in the most equitable way possible; (iv) (re)

financing of debts arising from situations of commercial default in the ACR.

For the free market (ACL), this is a moment, in principle, of respect for contracts, which have force

majeure and arbitration clauses for the treatment of disagreements. In this environment, this crisis can

be discussed bilaterally, with market solutions, leaving the government to act where it must, in the

regulated market. The sector institutions, however, may play an important role, at first, in investigating

and monitoring operations, in order to avoid abuses and commercial arbitrage that are wrongly justified

by the Coronavirus pandemic. However, a worsening of the crisis, with failures along the supply chain,

may require government interference, which could take the form of ensuring liquidity for the fulfillment

of commitments.

The current crisis and the 2001 rationing crisis

It is natural is to compare the current crisis to the 2001 rationing. In our view, the current scenario is

much more complex due to the current size of the free market (nonexistent in 2001), the plurality of

agents, the number of trading relationships, and more disputes by specific interests, illustrated by the

high number of associations.

The 2001 energy crisis had significant commercial impacts on companies, culminating in a “general

sector agreement” and the elaboration of regulatory improvements. The agreement was constructed to

preserve the financial health of the segments, sharing losses between them and the consumer. An

Extraordinary Tariff Review (RTE) was applied with increases of 2.9% for residential and rural low

voltage consumers and 7.9% for the others13.

13 These differentiated increases were aimed at equalizing the energy cost between the consumption classes.

All rights reserved © PSR 11

PSR, which at the time served directly in the Energy Crisis Management Chamber, believes that the main

lesson of the 2001 crisis that would apply today is the need to have a forum that centralizes the discussion

and proposes solutions, led by government and with authority to implement the measures that are

necessary to resolve its various aspects. Rationing has also shown us that: (i) the sector's “collective

intelligence” can devise a solution; but that (ii) the design of solutions to short-term problems can affect

the long-term development of our industry.

Finally, in 2001 the Electric Sector was the focus of the crisis; but in 2020 it is only a small part of it.

Even so, it is up to the government and agents to propose viable solutions. Otherwise, in the event

of a worsening of the crisis, the sector's functioning may become unfeasible.

All rights reserved © PSR 12

ABOUT PSR ENERGY REPORT

Energy Report is a monthly newsletter developed by PSR with the main objective of analyzing relevant

issues in the electricity sector in Brazil. It has been published electronically for five years in Portuguese,

and observes the following standardized structure:

Opinion – this section highlights a current and relevant issue in the electricity sector, selected

by PSR for further study and discussion. A list of subjects addressed in recent issues is available

below.

Regulatory – analyzes the recent activity of the government in the electricity sector and

presents executive comments on other relevant topics on the monthly regulatory agenda.

Water Resources and Environment – addresses recent environmental issues related to the

electricity sector, with emphasis on monitoring of the licensing processes.

International – analyzes events of the last month in the international electric markets and

presents PSR's view on measures taken.

Innovation – addresses the technological innovations of the month related to the electric

sector.

Supply – it presents an overview of the electrical system for the coming years, with the energy

supply and structural demand balance and the delay meter.

Subscription and access

The annual subscription of Energy Report comprises twelve (12) monthly electronic editions and can

be made by calling (21) 3906 2100, or by the e-mail: [email protected];

Access to our issues is restricted, and the subscriber must register at the PSR service portal. Whenever a

new edition is published, the registered readers will be notified by email and, by accessing the PSR

website, they can download the files. Previous editions are permanently available on the PSR service

portal.

Subjects discussed in previous editions

Issue 158 – February 2020: Reform of the electric sector in Colombia: The transformation of the transforming

country

Issue 157 – January 2020: CNPE defines new supply guarantee criteria… Or maybe not?

Issue 156 – December 2019: Water-energy nexus: precifying water when it is scarce

Issue 154 – October 2019: Improving the navigation of future of consumers and distribution companies.

Issue 153 – September 2019: Everything you wanted to know about the separation between ballast and energy.

Issue 152 – August 2019: Opening of electricity market: Coordinated or stampede?

Issue 151 – July 2019: Energy purchase strategy in ACR: back to the drawing board.

Issue 150 – June 2019: Working between two limits: public audience of PLD’s floor and cap.

Issue 149 – May 2019: Pumped storage is pumped up?

![Raport de Practica La Cooperativa de Consum Din Orrezina Consum Coop.[Conspecte.md]](https://static.fdocuments.us/doc/165x107/577c84641a28abe054b8bd37/raport-de-practica-la-cooperativa-de-consum-din-orrezina-consum-coopconspectemd.jpg)