A Credit Providers Perspective PARLIAMENTARY HEARINGS ON CREDIT AMNESTY Cape Town 14 August 2012.

16

A Credit Providers Perspective PARLIAMENTARY HEARINGS ON CREDIT AMNESTY Cape Town 14 August 2012

-

Upload

abby-forward -

Category

Documents

-

view

216 -

download

3

Transcript of A Credit Providers Perspective PARLIAMENTARY HEARINGS ON CREDIT AMNESTY Cape Town 14 August 2012.

A Credit Providers Perspective

PARLIAMENTARY HEARINGS ON CREDIT AMNESTYCape Town 14 August 2012

Who are the CPA• CPA is a voluntary association of Payment Data Providers,• CPA members include:• Credit Providers,• Insurance companies,• Telco providers, and• Other.

• CPA creates a self regulatory framework for credit data to be submitted and shared among members,

• CPA manages the quality and format of the data being shared,• CPA is governed through an elected Management Committee,• Key principle of reciprocity in data sharing,• Historically only dealt with consumer data,• In the process of also facilitating SMME data.

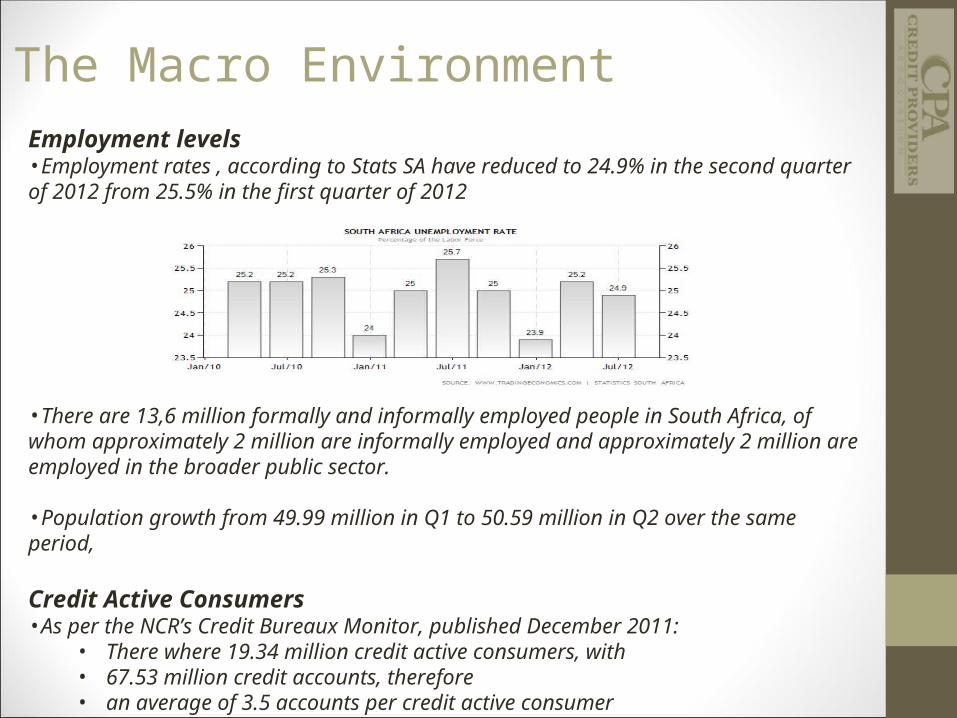

The Macro EnvironmentEmployment levels•Employment rates , according to Stats SA have reduced to 24.9% in the second quarter of 2012 from 25.5% in the first quarter of 2012

•There are 13,6 million formally and informally employed people in South Africa, of whom approximately 2 million are informally employed and approximately 2 million are employed in the broader public sector.

•Population growth from 49.99 million in Q1 to 50.59 million in Q2 over the same period,

Credit Active Consumers•As per the NCR’s Credit Bureaux Monitor, published December 2011:

• There where 19.34 million credit active consumers, with• 67.53 million credit accounts, therefore• an average of 3.5 accounts per credit active consumer

The Macro Environment

• The Role of Credit in the Economy,• Recession and Economic crisis,• Rising cost of living,• South Africa has different consumer groups with different

financial needs,• Credit is not a one shoe fits all.

Different Credit Products• National Credit Act defines different credit products:• Mortgages,• Credit Facilities,• Unsecured Credit Transactions,• Developmental Credit,• Short term credit,• Other Credit,• Incidental Credit.

• These credit products have different capped rates,• Credit products also has different loan performances,

STATS NPL %Mortgages Q4 2009 Q4 2010 Q4 2011

Current 85% 86% 88%

30 Days 3% 3% 3%

31 – 60 Days 2% 1% 1%

61 – 90 DYS 1% 1% 1%

91 – 120 Days 2% 2% 1%

120 + Days 7% 7% 6%

Facilities Q4 2009 Q4 2010 Q4 2011

Current 80% 86% 87%

30 Days 57% 5% 5%

31 – 60 Days 2% 2% 2%

61 – 90 DYS 1% 2% 2%

91 – 120 Days 1% 1% 1%

120 + Days 8% 4% 4%

Unsecured Q4 2009 Q4 2010 Q4 2011

Current 73% 77% 79%

30 Days 5% 5% 4%

31 – 60 Days 2% 2% 2%

61 – 90 DYS 2% 1% 1%

91 – 120 Days 1% 1% 1%

120 + Days 16% 14% 13%

Different Credit Products• National Credit Act defines different credit products:• Mortgages,• Credit Facilities,• Unsecured Credit Transactions,• Developmental Credit,• Short term credit,• Other Credit,• Incidental Credit.

• These credit products have different capped rates,• Credit products also has different loan performances,• Different credit providers focus on different credit products.• The allowed rate determines credit providers ability to absorb

poor performing debt.

Credit DataThe CPA•Members voluntarily share positive and negative credit data with each other on a monthly basis.

The NLR•Members voluntarily (historically compelled to share) share positive and negative credit data with each other within 48 hours.

Bureaux Specific Data•Credit bureaux clients (such as credit providers) submit their credit data to the bureaux.

Positive and Negative Data is shared (Gold List and Non-performing Data)•Information of all credit active consumers is shared, of which the majority of data relates to positive credit behaviour, and negative data in the event of defaults.

How do Credit providers Use Data•Generally credit providers perform two areas of analysis when taking a credit decision:

• An affordability asessment is done to determine the consumers ability to service the debt applied for, and

• A Credit Bureaux check to determine his/her propencity to pay the debt.•Different credit providers focus on different consumer groups and therefore have exposure to a variety of credit risk profiles,•Positive and negative data is used by credit providers to identify and evaluate prospective clients,•Negative credit data does not necessarily exclude a consumer from credit, only indicates a higher risk with access to a different credit product.

Credit Data (Cont.)

Credit Standing of Consumers

The % of Adverse listings have reduces from 15.6% in June 2010 to 12.9% in December 2011

Varying credit products to meet needsIntelligent / Niche Products

•Historically, lower income consumers were deemed to be a higher risk. The inclusion of payment behaviour information and the indicators which are submitted to bureaux have allowed for more advanced analytics. This has allowed for a refinement of consumer lending decisions.•Credit Providers can now determine good from bad based on the consumers individual behaviour rather than applying risk indicators to generalisations.

Bad Luck versus Bad Faith•Poor credit performance usually has one of two causes:

• Poor performance due to bad luck such as losing a job, or some other emergancy beyond the control of the consumer, or

• Poor performance due to the consumer acting in bad faith and not wanting to repay their debt.

•Bad luck consumers has the ability of improving their credit record once they are in a position to repay their debt and generally do so,•Every payment made improves a consumer credit rating,•Bad faith customers tend not to restore their credit performance, even if granted an amnesty,•An amnesty disables the ability to distinguish between bad luck and bad faith customers resulting in a generalisation.

• One of the important focuses of the National Credit Act (NCA) is that of protecting consumers (reckless lending provisions and debt counseling),

• If credit data does not give a true reflection of actual performance it would lead to an irresponsible credit environment,

• Reduced consumer protection, with a higer level of reckless lending,

• The reckless lending provisions in the NCA probably more restrictive for consumers to access credit than negative listings of non-paying consumers.

Implications of Incomplete data

Amnesty removes ability to distinguish between performing and non-performing credit behavior

• The inability to distinguish between good performing and poor performing consumers will lead to:• Credit providers following a more conservative approach when

granting credit, resulting in less access to credit,• Contraction of credit to lower income categories of consumers,• Good performing consumers will be prejudiced due to the

inability to distinguish between consumers,• If there is no sanction for consumers not repaying their debt, it

would make certain sectors of the credit market unattractive and credit providers will pull back on granting credit in higher risk sectors,

• Less consumers being able to acsess formal credit, and would need to borrow from the informal sector,

• Finmark survey indicates that there is a growing trend in consumers borrowing from informal lenders.

Healthy Credit Sector• It is important to have a well functioning and profitable Credit

Industry,• Credit plays a crucial role in the effective functioning of our

economy,• Profitable credit providers will attract investment,• The more investment attracted enables credit providers of

different forms and shapes to service a wider range of consumers,

• Credit providers making poor credit decisions due to a lack of sufficient data will increase bad debts, be unattractive investment destinations, and contract access to credit.

Thank you.

Questions?