A Conceptual Framework and Survey

51

American Economic Association The Role of Boards of Directors in Corporate Governance: A Conceptual Framework and Survey Author(s): Renée B. Adams, Benjamin E. Hermalin and Michael S. Weisbach Source: Journal of Economic Literature, Vol. 48, No. 1 (MARCH 2010), pp. 58-107 Published by: American Economic Association Stable URL: http://www.jstor.org/stable/40651578 . Accessed: 29/10/2013 04:14 Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at . http://www.jstor.org/page/info/about/policies/terms.jsp . JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. . American Economic Ass ociation is collaborating with JSTOR to digitize, preserve and extend access to Journal of Economic Literature. http://www.jstor.org

-

Upload

chumba-museke -

Category

Documents

-

view

219 -

download

0

Transcript of A Conceptual Framework and Survey

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 1/51

American Economic Association

The Role of Boards of Directors in Corporate Governance: A Conceptual Framework andSurveyAuthor(s): Renée B. Adams, Benjamin E. Hermalin and Michael S. WeisbachSource: Journal of Economic Literature, Vol. 48, No. 1 (MARCH 2010), pp. 58-107Published by: American Economic Association

Stable URL: http://www.jstor.org/stable/40651578 .

Accessed: 29/10/2013 04:14

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of

content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms

of scholarship. For more information about JSTOR, please contact [email protected].

.

American Economic Association is collaborating with JSTOR to digitize, preserve and extend access to Journal

of Economic Literature.

http://www.jstor.org

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 2/51

Journal fEconomicLiterature010,48:1,58-107

http:www.aeaweb.org/articles.php?doi=10.1257/jel.48.1.58

TheRoleofBoardsofDirectorsnCorporate overnance: Conceptual

FrameworkndSurveyRenée Β.Adams, enjamin . Hermalin, nd Michael S.Weisbach*

Thispaper s a surveyf he iteraturen boards fdirectors, ith n emphasisn

research onesubsequento theBenjamin . Hermalin nd MichaelS. Weisbach(2003)survey. he twoquestionsmost sked about boards re whatdeterminestheirmakeupndwhat eterminesheir ctions? hese uestionsre undamentallyintertwined,hich omplicateshe tudy fboards ecausemakeupnd actions rejointly ndogenous.focus f his urveys how he iterature,heoreticals well sempirical,eals or on occasionsails o deal with his omplication. e uggestthatmanytudiesfboards an best e nterpreteds oint tatementsbout oth hedirector-electionrocessnd the ffectfboard ompositionn board ctions ndfirm erformance.JELG34,L25)

1. Introduction

Peopleoften uestionwhetherorporate

boardsmatter ecause their ay-to-dayimpacts difficultoobserve. utwhenhingsgowrong,heyanbecome he enterf tten-tion.Certainlyhiswas trueof theEnron,Worldcom,ndParmalatcandals. hedirec-tors fEnron ndWorldcom,nparticular,wereheld iablefor hefraud hat ccurred:Enrondirectors ad topay$168milliono

*Adams: University f Queensland and ECGI.Hermalin:UniversityfCalifornia, erkeley.Weisbach:Ohio StateUniversity.he authors ish o thank i-WoongChung,Rüdiger ahlenbach, liezerFich,JohnMcCon-nell,Léa Stern,René Stulz,and Shan Zhao forhelpfulcomments n earlierdrafts. he authors re especiallyappreciativefthecomments eceived rom hree nony-mousrefereesnd theeditor, ogerGordon.

investorlaintiffs,fwhich 13million asout fpocketnot overedy nsurance);ndWorldcomirectors ad topay$36million,ofwhich 18million as outofpocket.1 sa consequencef hese candals ndongoingconcernsbout orporateovernance,oardshavebeen at thecenter fthepolicy ebateconcerningovernanceeformndthefocusof considerablecademic esearch. ecauseof thisrenewednterestnboards, reviewofwhatwe have nd havenot earned rom

researchncorporateoards stimely.Much of the research n boards ulti-matelyouches n thequestionwhat s therole ofthe board?"Possible nswers angefrom oards'being implyegalnecessities,

1MichaelKlausner,Bernard S. Black,and Brian R.Cheffins2005).

58

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 3/51

Adams,Hermalin,ndWeisbach: heRoleofBoards fDirectors 59

somethingkinto thewearing fwigs nEnglish ourts, o theirplayingn active

partntheoverall

managementnd control

of thecorporation.o doubt he truthiessomewhereetween hese xtremes;ndeed,therereprobably ultipleruths hen hisquestions asked fdifferentirms,ndiffer-ent ountries,r ndifferenteriods.

Given hat ll corporationsaveboards,thequestion f whether oardsplay rolecannot e answeredconometricallys thereis no variationn theexplanatoryariable.Instead, tudies ook at differencescrossboardsand ask whether hesedifferencesexplain ifferencesn thewayfirms unc-tion nd howthey erform.he boarddif-ferenceshat newouldmost ike ocaptureare differencesn behavior. nfortunately,outsidefdetailed ieldwork,t sdifficultoobserve ifferencesnbehavior nd harderstill oquantifyhemna way seful or ta-tisticaltudy. onsequently,mpirical orkin thisarea has focused n structuralif-ferencescross oards hat represumedocorrelate ithdifferencesn behavior. or

instance,commonresumptions that ut-side nonmanagement)irectors illbehavedifferentlyhan nsidemanagement)irec-tors.One can then ook at theconduct fboards e.g.,decision o dismiss heCEOwhenfinancial erformances poor)withdifferentatios f outside o insidedirec-tors o see whetheronduct ariesn a sta-tisticallyignificantannercross ifferentratios.When onducts notdirectlybserv-able e.g., dvice o theCEO about trategy),one an ook ta firm'sinancialerformanceto see whetheroard tructure atterse.g.,theway ccountingrofitsary ith heratioof utsideo nside irectors).

Oneproblemonfrontinguch nempiri-cal approachs that here s no reason osuppose board structure s exogenous;indeed,herereboth heoreticalrgumentsand empirical videnceto suggest oardstructuresendogenoussee,e.g.,Hermalin

and Weisbach 988,1998,and2003).Thisendogeneityreates stimationroblemsf

governancehoices remadeon thebasisof

unobservablesorrelatedith he rror ermintheregressionquations eing stimated.Infact,neof urmain ointsn his urveysthe mportancefendogeneity.overnancestructuresriseendogenouslyecause eco-nomic ctors hoose hemnresponseo thegovernancessues hey ace.2

Beyondhe mplicationsndogeneityoldsfor conometricnalysis,t also has mplica-tions or ow oview ctual overnancerac-tice. n

particular,henwe observewhat

appears o be a poorgovernancetructure,weneed o skwhyhat tructureas hosen.Althought s possible hat hegovernancestructure as chosen ymistake,ne needstogive t east omeweighto thepossibilitythattrepresentsheright,lbeit oor, olu-tion othe onstrainedptimizationroblemtheorganizationaces.Afterll,competitioninfactor,apital,ndproductmarketshouldlead, n Darwinian ashion,o thesurvivalof hefittest. hile dmittedlyfittest"oes

notmean optimal,"nythinghatwas sub-optimal orknown easonswouldbe unfitinsofarstherewould epressureo addressthese reasonsforsuboptimality.n otherwords, xistinguboptimalitys unlikelyolend tselfoquick robvious ixes.

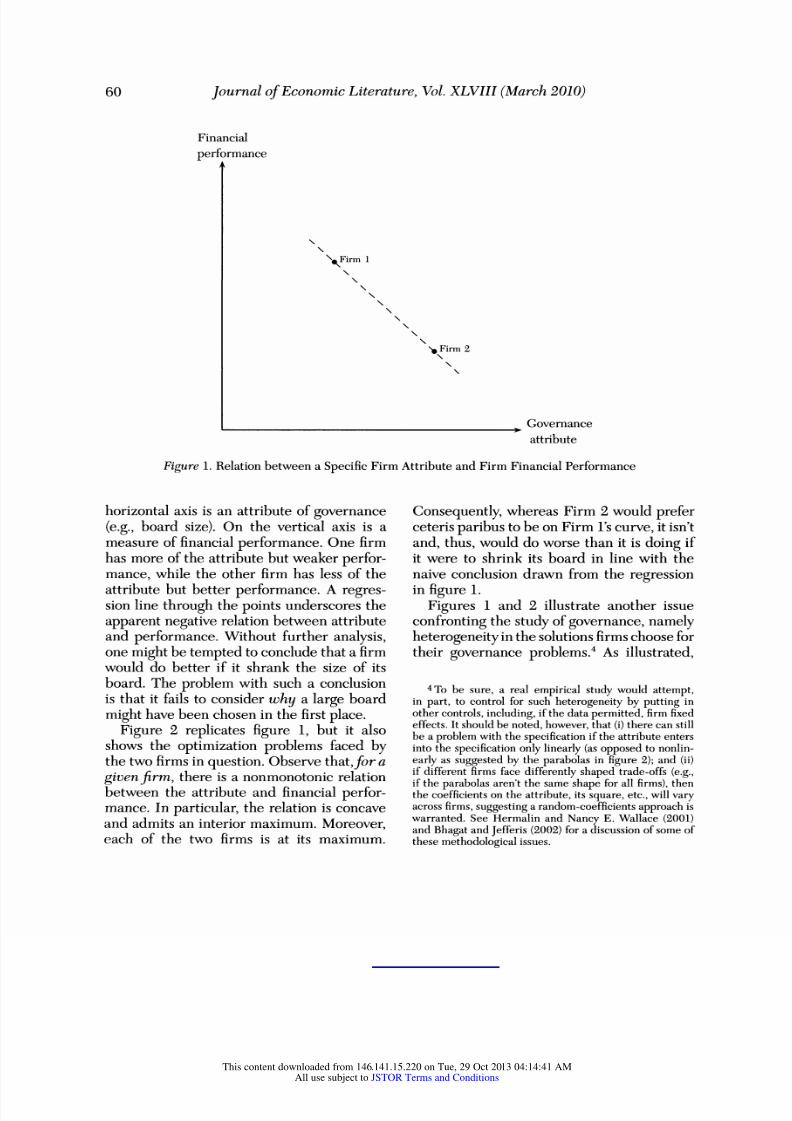

This nsightbout ndogeneitys,however,easyto forgetn the face of data.Figureshows plotof two data points.3 n the

2Harold Demsetz and Kenneth Lehn (1985) were

among he firsto make hegeneral oint hat overnancestructures re endogenous.Otherswho have raised itincludeCharles P. Himmelberg, . GlennHubbard, ndDarius Palia (1999), Palia (2001), and Jeffrey. Coles,MichaelL. Lemmon, ndJ.FelixMeschke 2007). Thepointhas also been discussed n various urveys f theliterature; onsider, .g., Sanjai Bhagatand Richard H.Jefferis2002) and MarcoBecht, atrick olton,nd AilsaRöell 2003),among thers.

3Figure 1 is presented or llustrativeurposesandshouldnot be read as a critique fanyexisting esearch.In particular, oneofthestudiesdiscussedbelow are asnaive s figure .

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 4/51

60 JournalfEconomic iterature,ol.XLVIII March 010)

Financialperformance

' ''Firm 1

''

''

''

''

''

^ Firm 2'

'

Governanceattribute

Figure .Relation etween Specific irmAttributendFirmFinancialPerformance

horizontalxis s an attributefgovernance(e.g.,boardsize).On the vertical xis s ameasure ffinancialerformance.nefirmhas more f he ttributeutweaker erfor-mance,while he other irm as less of theattributeutbetter erformance.regres-sion ine hroughhepoints nderscoresheapparent egativeelation etween ttributeandperformance.ithout urthernalysis,onemightetemptedoconclude hat firmwoulddo betterf t shrank hesize of tsboard.Theproblem ith uch conclusion

isthat t fails oconsider hy largeboardmightavebeenchosennthefirstlace.Figure2 replicates igure , but it also

shows heoptimizationroblems acedbythe wo irmsnquestion. bservehat,/orgiven irm,here s a nonmonotonicelationbetween heattributendfinancialerfor-mance.nparticular,herelations concaveand admits ninterior aximum. oreover,each of the twofirmss at its maximum.

Consequently,hereas irm wouldpreferceterisaribusobe onFirm 'scurve,t sn'tand, hus,woulddo worse han t sdoingfitwereto shrinkts board n line with henaive onclusion rawn rom heregressioninfigure.

Figures1 and 2 illustratenotherssueconfrontinghe tudyfgovernance,amelyheterogeneityn he olutionsirmshoose ortheirgovernanceroblems.4s illustrated,

4To be sure,a real empirical tudywould attempt,in part,to control or uchheterogeneityy puttingnother ontrols,ncluding,f he datapermitted,irm ixedeffects.t should e noted,however,hat i) there an stillbe a problemwith hespecificationf he attributentersinto hespecificationnly inearlyas opposedto nonlin-early s suggested ytheparabolas n figure ); and (ii)ifdifferentirms acedifferentlyhapedtrade-offse.g.,iftheparabolas ren't he sameshapefor ll firms),henthe coefficientsn theattribute,ts quare, tc.,willvaryacrossfirms,uggestingrandom-coefficientspproachswarranted. ee Hermalin nd NancyE. Wallace (2001)andBhagat ndJefferis2002) for discussion f ome ofthesemethodologicalssues.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 5/51

Adams,Hermalin,nd Weisbach: heRoleofBoards fDirectors 61

Figure . The Real DecisionsFacedby he Firms

Firms1 and 2 facedifferentovernanceproblemsnd,notsurprisingly,re drivento differentolutions.lmostverymodel fgovernancehows hat heequilibriumut-come s sensitiveo ts xogenousarameters;consequently,eterogeneityn those aram-eterswill ead toheterogeneitynsolutions.Moreover,nce onetakes nto ccount ari-ous sources fnonconvexity,uch as thosearisingn optimal ncentivechemes, nemayfind hat trategiconsiderationsead

otherwisedentical irms o adoptdifferentgovernanceolutionssee, e.g., Hermalin1994).

Somehelpwiththeheterogeneityssuecouldbe forthcomingrommore heoreti-cal analyses. lthough common and notnecessarilynaccurateperception f theliteraturencorporateovernance,articu-larly elatedo boards fdirectors,s that tis largelympirical,uch viewoverlooks

largebodyofgeneral heoryhat s readilyapplied o thespecific opic f boards.Forinstance,monitoringy the board wouldseem to fit ntothe general iteraturenhierarchiesnd supervisione.g.,OliverE.Williamson975;Guillermo . Calvo andStanislawWellisz1979;Fred Kofman ndJacquesLawarrée1993,JeanTirole1986;Tirole1992).As a second xample,ssues fboard collaboration ouldseem to fit ntothegeneraliteraturenfree-ridingnd the

teamsproblemsee,e.g.,BengtHolmstrom1982).The teams-problemxampleserves to

illustrateproblemhat an arise napply-ing off-the-shelf"heoryoboards.t s wellknownhat, s a member'share f team'soutputalls, e or he uppliesess ffort.orboards, owever,hequestions not singledirector'sffort,ut whathappens o totalefforte.g.,are larger oards ess capable

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 6/51

62 JournalfEconomic iterature,ol.XLVIII March 010)

monitors ecause of the teamsproblem)?Yet,here, heoryannot rovide definitiveanswer whether otal

equilibriumffort

increases r not withboard size dependscriticallyn assumptionsbout functionalforms.5 hile"anythingoes"conclusionscan be acceptablenan abstractheoreticalmodel,heyreofteness han atisfactorynappliedmodeling.he ack f lear efinitivepredictionsn much f the related eneraltheorys,therefore,hindrance o model-inggovernancessues.Conversely,fa spe-cificmodel makesa definitiverediction,then necan often e leftwonderingf t s

an artifactfparticularssumptionsatherthan reflectionf robust conomicruth.

A second, elated oint s that,n a sim-ple, ndthus ractable, odel,heoryan betoostrong;hat s,by applicationfsophis-ticated ontracts r mechanisms,hepar-ties e.g., irectorsndCEO) canachievemore ptimalutcomehan ealityndicatesispossible. oanextent,hat roblemanbefinessed;ornstance,fonerestrictstten-tion o incompleteontracts. ut as others

havenoted, he assumptionf incompletecontracts an fail to be robust o minorperturbationsf the informationtructure(Hermalinnd Michael . Katz1991) rtheintroductionf a broader lass of mecha-nismsEricMaskin ndTirole 999).

A furtherssue s thatcorporationsrecomplex, et, o haveany raction,modelmust bstractwayfrommany eaturesfreal-lifeorporations.hismakes t difficulttounderstandhe omplexnd multifaceted

solutionsirms se to solve heir overnanceproblems. or instance, he optimalgov-ernance tructuremightnvolve certain

5For instance, f a team's total benefit s Σ^=1 en,whereen is the effort f agentn, each agent gets 1/Nof thebenefit,nd eachagentn'sutilitys (Σ^=1 em)/N(e,T+I)/(7 1), then totalequilibrium fforts N{l/N)l/'which s increasingn Ν if 7 > 1, decreasing n Ν if7 € (0, 1),and constantf7 = 1.

type fboard, peratingna certain ashion,having mplemented particularncentive

package,nd

respondingncertain

wayso

feedback romherelevantroductnd api-tal markets.o include ll thosefeaturesna model s infeasible,ut an weexpect heassumptionf eteris aribus ith espectothenonmodeledspects f he ituationobereasonable? heconstrainednswer rrivedatbyholdingll elseconstant eed notrep-resent heunconstrainednswerccurately.

Yet another oint,relatedbothto thepreviouspoint and to our emphasisonissuesofendogeneity,s that,motivatedyboth desire osimplifynd to conformoinstitutionaletails, he modeler s oftentemptedotakecertain spects f thegov-ernance tructure s given.The problemwith his s thatthegovernancetructureis largelyndogenous;t is, in itsentirety,thesolution eached yeconomic ctors otheir overnance roblems. fcourse, er-tainfeatures,uch s thenecessityfhavinga boardofdirectors,an largelye seen asexogenous althought shouldbe remem-

bered hat he decisiono make companya corporationatherhan, ay, partnershipis itselfndogenous).urthermore,hetim-ingofevents, articularlynthe short un,can make treasonableo treat ome spectsof hegovernancetructuresexogenousorthepurposes f nvestigatingertain ues-tions heoretically.

Inthis urvey,e focus rimarilyn workthat llustrateshe sorts fchallenges is-cussedabove,papersthathelp clarifyhe

nature fboardbehavior,r thatuse novelapproaches. e alsoattemptoput heworkunder the same conceptualmicroscope,namelyow houldheresults e interpretedin light fgovernancetructureseing hesecond-bestolutionothegovernancerob-lemsfaced y hefirm. ur focus s also onmore ecent apers, ven f hey re notyetpublished, ecauseprior urveys y KoseJohn nd Lemma W. Senbet 1998) and

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 7/51

Adams,Hermalin,ndWeisbach: heRoleofBoards fDirectors 63

Hermalin nd Weisbach2003)covermanyestablishedapersnthis ield. lthougheaim obe

comprehensive,twould e

impos-sibleto discuss very aper n light f therecentxplosionnthe iteraturenboards.6Of necessity, e omitmany nterestingpapersnthis rea andweapologize o theirauthorsn advance. For a more detaileddiscussion f theevent-studyvidence ur-roundingoard ppointments,e refer hereader o DavidYermack2006).M.AndrewFields ndPhyllis .Keys 2003)review hemonitoringoleoftheboard, s well s theemergingiteraturen boarddiversityseealso David A. Carter, etty .Simkins,ndW.Gary impson003;Kathleen . FarrellandPhilipL. Hersch 005; and RenéeB.Adams nd Daniel Ferreira 009 on boarddiversity).e do notdirectlyiscuss irec-tor urnover;ermalinndWeisbach2003)review ome of the relevantiteraturenthis opic.7or he ake fbrevity,e do notdiscuss he iteraturen boards f financialinstitutions.ecausethis s a surveyfcor-porateboards,we also do not discuss he

literaturenboards forganizationsuch snonprofitandcentral anks. artlyecauseofthedifficultyn obtainingata,this it-eratures lessdevelopedhan he iteratureon corporate oards WilliamG. Bowen1994 discusses omeof thesimilaritiesnddifferencesetweencorporate nd non-corporateoards).8imilar ata limitationsrestricts to a discussionfboards fpub-licly raded orporations.inally, e do not

6Afterearchinghe iterature,e estimate hatmorethan 200 working aperson boards were writtenn thefirstive ears ince Hermalin nd Weisbach2003) pub-lished heir oard urveynocausal ink s mplied).

7See also Eliezer M. Fich and Anil Shivdasani2007),TodPerrynd Shivdasani2005),and Yermack2004),forsomerecentworknthis rea.

8Also see Hermalin 2004) for discussion f howresearch n corporate oardsmay nform he study funiversityndcollegeboards.James . Freedman 2004)discusses he relation etweenuniversitiesnd colleges'boards nd their residents.

consider tudies hatcomparegovernanceinternationally.

Althoughhis

survey rimarilyonsid-

ers the economics nd financeiteratures,boards are a subjectof interestn manyother isciplines,ncludingccounting,aw,management, sychology,nd sociology.9While heres anoverlapntheseiteratures,there re alsodifferences.or nstance,heeconomics nd financeiterature'socus astraditionallyeen on theagency roblemsboards olve r,nsomenstances,reate.ncontrast,hesociologicalnd managementliteratureslso emphasize hatboardscan(i)play role nstrategyettingnd ii)pro-vide critical esourceso thefirm,uch asbuildingetworksndconnectionssee, .g.,Sydney inkelstein, ambrick,nd AlbertA.Cannella 009).Someof he opics revi-ouslynthedomain fother isciplinesrebeginningo be of nterestnthe econom-ics and financeiterature.orexample,hisliteratureasbegun o ncorporatessues fexpertise,rust, iversity,ower, nd net-worksnto heirnalyses.10

The next ection onsiders hequestionofwhatdirectors o. The section ollowing,section , considersssuesrelated o boardstructure.ection4 discusseshow boardsfulfill heirroles. Section5 examines he

9Some examplesof this broader iterature ncludeLucian A. Bebchuk ndJesseM. Fried 2004),Ada Demband F. FriedrichNeubauer 1992),AnnaGrandori2004),Donald C. Hambrick, heresa Seung Cho, and Ming-JerChen (1996),JayW. Lorsch 1989),MylesL. Mace

(1971),Jeffreyfeffer1972),MarkJ.Roe (1994),JamesD. Westphal ndEdwardJ. ajac (1995),Westphal1999),andZajac andWestphal1996).

10 orresearch rom n economic erspectiven direc-tordiversity,ee Carter,Simkins, nd Simpson 2003),Farrell and Hersch (2005), and Adams and Ferreira(2009).Director xpertises discussednfransection .3.Someaspectsofpowerrelated o boards are capturednHermalin nd Weisbach 1998); see RaghuramG. Rajanand Luigi Zingales 1998) for moregeneral conomicanalysis fpower norganizations.ee Asim jaz Khwaja,AtifMian and AbidQamar 2008) forwork n thevalue oa firm reated y tsdirectors' ocial networks.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 8/51

64 JournalfEconomie iterature,ol.XLVIII March 010)

literaturen whatmotivates irectors.Weendwith ome oncludingemarks.

2. WhatDo Directors o?

To understand orporateboards, oneshould eginwith hequestion fwhatdodirectorso?11

2.1 Descriptivetudies

Oneway o determine hatdirectors oisto observe irectors;hats,do field ork.There s a large

descriptiveiterature n

boardse.g.,Mace1971;Thomas . Whisler1984; Lorsch1989; Demb and Neubauer1992, ndBowen 994).

The principalonclusionsfMace werethat directorserve s a sourceofadviceandcounsel,erve s some ort fdiscipline,and act in crisis ituations"fa change nCEO becomes ecessaryp.178). henatureof their adviceand counsel" s unclear.Mace suggestshat board serves argelyas a soundingoard for he CEO andtopmanagement,ccasionallyrovidingxper-tisewhen firmaces n issue boutwhichone ormore oardmembersreexpert. etDemb and Neubauers urvey esults indthatapproximatelywo-thirdsf directorsagreed hat settinghe trategicirectionfthecompany" asone of the obsthey id(p. 43, emphasis dded).12 ighty ercentofthedirectorslso agreed hat heywere

11 his question s distinct rom hequestion fwhatshoulddirectors o? This secondquestion s answered,inpart, ythe egalobligationsmposedbycorporateaw(both tatute ndprecedent), aving o do withfiduciaryobligationssee, e.g.,Robert C. Clark 1986, especiallychapters and4).

12 t s mportanto note hat heDemb andNeubauersurveys nd questionnairesampleveryfewAmericandirectors4.2percent). hetopfour ationalitiesurveyedby hem reBritish29.6percent), erman11.3percent),French11.3percent),ndCanadian 9.9percent). verall43.7percent f heir espondentsome fromommon-lawcountries.

"involvedn setting trategyor he com-pany" p.43).Seventy-fiveercentfrespon-dents o another fDemb and Neubauersquestionnaireseporthat heyset trategy,corporateolicies,verall irection, ission,vision"p.44). Indeedfarmore espondentsagreedwith hat escriptionf heirobthanagreedwiththe statementshattheirobentailedoversee[ing],onitor[ing]opman-agement, EO" (45 percent); succession,hiring/firingEO and top management"(26percent);r servings a "watchdogorshareholders,ividends"23percent).

Thedisciplinary

ole of boards s alsounclearfromdescriptivetudies.Perhapsreflectingheperiodhe studied,Mace sug-gests hatdisciplinetemsargelyromheCEO and other op managementnowing"that eriodicallyheymustppear eforeboardmade p argelyf heir eers"p.180).Lorsch akes n evendimmeriew,uggest-ing hat oards re sopassive hat hey fferlittle yway fdisciplinesee,especially,.96). Demb and Neubauers tatisticseembroadlyonsistentith his iew,s ess han

half of theirrespondentsgreethattheirjob is to"oversee,monitoropmanagement,CEO" and less than a quarter greethattheirob s toserve s a "watchdogor hare-holders,ividends"p.44).

On theother and,thas beensuggestedthat he boardpassivityescribed yMaceand Lorsch s a phenomenonfthepast.For nstance, aul W. MacAvoyndIra M.Millstein1999) suggest hat boardshaverecentlyecome esspassive; hat s, theyhave volvedromeingmanagerialubber-stampso active nd ndependent onitors."MacAvoynd Millstein rovide tatisticalevidence nsupportf hat onclusion,ind-ing hatCalPERS' gradingf firm'soardprocedures s positivelyorrelatedwithaccounting-basedeasures fperformance.Another iece ofevidence onsistent iththeviewthatboardshavebecome ougheris thatCEO dismissal robabilitiesave

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 9/51

Adams,Hermalin,ndWeisbach: heRoleofBoards fDirectors 65

beentrendingpwardseeMarkR. Huson,Robert arrino,ndLauraT.Starks001forevidence ver he

period1971to 1994 and

see StevenN. Kaplanand Bernadette .Minton006 formore ecentvidence).2.2 TheHiring, iring,nd Assessmentf

ManagementOne role that is typicallyscribed to

directors s control of the process bywhich opexecutivesre hired, romoted,assessed, nd, fnecessary,ismissedsee,e.g.,Richard . Vancil 987for descriptiveanalysisnd LalithaNaveen 006 for tatis-tical vidence).

Assessmentan be seen as having wocomponents,neismonitoringfwhat opmanagementoes nd he thers determin-ing he ntrinsicbility f opmanagement.Themonitoringfmanagerialctions an,inpart, e seen as part f board's bliga-tion o be vigilantgainstmanagerialmal-feasance. et,beingrealistic,t is difficultto see a boardactually eing n a positionto detectmanagerialmalfeasance irectly;atbest, boardwould eemdependentnthe actions f outside uditors,egulators,and, in some instances,he news media.Indirectly, board mightguard againstmanagerialmalfeasancehroughts choiceof auditor, ts oversight ver reportingrequirements,nd tscontrolver ccount-ingpractices.

The principal ocusof the literaturenassessment,t east t a theoreticalevel, asbeenon the uestionfhow heboard eter-

minesmanagerialbilityndwhat tdoeswiththatnformation.13ne strategyor tudyingthequestion fabilityssessment as beenthe daptationfHolmstrom's1999)model,whichnalyzes gencyndmonitoringhen

13Typically,he CEO is a member f the board. Instatinghe CEO is atodds with theboard,"we are, ikethe iterature,sing heboard as shorthand or he boardminus heCEO.

agentsave areeroncerns,oboards.Withinthat pproach,uthors avefocusedn howthe ssessmentf

bilityelates o the

poweroftheCEO (e.g.,Hermalin ndWeisbach1998); othe electionfprojectsnd trategy(e.g.,SilviaDominguez-Martinez,tto H.Swank,ndBaukeVisser008); o he rocessofselectinghe CEO (e.g.,Hermalin005);amongtherssues.

2.2.1Assessment,argainingower,ndCEO Control

The first rticleto applyHolmstrom'sframeworko boardswas Hermalin nd

Weisbach1998). In theirmodel, here san initial eriod ffirmerformancenderan incumbent EO. Based on thisperfor-mance, he boardupdates tsbeliefs boutthe CEO's ability.n light ftheseupdatedbeliefs,heboardmay hoose o dismissheCEO and hire replacementrom hepoolofreplacementEOs or tmay argain iththe ncumbentEO with egardochangesinboardcompositionnd his futurealary.Theboard, hen, hooseswhethero obtain

an additional,ostly ignal boutCEO abil-ity eitherhat f theoriginalncumbentfretainedr hereplacementfhired).14asedon this ignal,fobtained,he board gainmakes decisionboutkeepingrreplacingthe CEO. If replaced, (another) EO isdrawn rom hepoolofreplacementEOs.Finally,econd-andfinal-)eriod rofitsrerealized, ith he xpectedalue f heprof-itsbeing positive unctionf the then-in-charge EO's ability.

The board's nclinationo obtain n addi-tional ignals a functionf ts ndependence

14An alternative, ut essentially quivalent,model-ing strategyor his tagewouldbe to assume the boardalwaysreceives he additional ignal,but the board hasdiscretion ver the informativenessf the signal,withmore nformativeignalsbeing ostlier o theboard thanless informativeignals.See the discussionn Hermalin(2005) on thismatter.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 10/51

66 JournalfEconomic iterature,ol.XLVIII March 010)

fromheCEO.15 heboard'sndependencetthat tagewilldepend n theoutcomef he

bargainingamebetween heboard ndthe

incumbentEO ifhe isretained.16ecausetheacquisitionf the additionalignal anonlyncrease herisk fbeing ismissedndthe CEO enjoys noncontractibleontrolbenefit,heCEO prefersless ndependentboard; hat s,a board ess ikelyoacquirethis dditionalignal. he board,however,preferso maintaints ndependence. henthe CEO has bargaining ower specifi-callywhenhe has demonstratedhathe's a"rare ommodity"y performingell theboards independenceeclines. ntuitively,a CEO whohas shown imselfo be aboveaveragebargains n two dimensions: ecan bargainfor morecompensationnd,because he preferso remainCEO ratherthan efired,hedegree f heboard inde-pendence. tanymomentntime, iventsmarginalateof substitutionetween irmperformancenddisutilityfmonitoring,boardviews tself s optimallyndependent(i.e., he directorsiew ny hangentheir

compositionhatmayeadtomore r essdil-igencenmonitoringsmovingt way romthe ncumbent oard'soptimum).17ence,a local change n independence epresentsa second-ordeross for he board thetopofthehill s essentiallylat), hereas s anincreasenthe CEO's salarys a first-orderloss themarginalostof a dollar s alwaysa dollar). heboard, herefore,s morewill-

15Independences a complexoncept.With especttomonitoringheCEO,one magineshat irectorshohave lose ies o theCEO (e.g., rofessionally,ocially,or because heCEO haspower ver hem)would indmonitoringimmoreostlyhan irectorsith eweries(althougheeWestphal999for nopposingiew).Wediscussndependencet engthnfra.16HermalinndWeisbachssume here s sufficientcompetitionmongpotential eplacementEOs forthepositionhat replacementEO hasnobargainingpower. heirmodelwould e robustogiving replace-ment EO some argainingowers long s itwas essthan hatnjoyedy n ncumbentEO who s retained.

ingtobudgeon the ssue of ndependence(willingnessomonitor)han alary,t least

initially;ence, here s movementninde-

pendence.o a CEO who erformsell ndsup facing less ndependentoard.Theflipside s that CEO whoperformsoorlysvulnerableoreplacement.

MalcolmBaker and Paul A. Gompers(2003),AudraL. Boone et al. (2007),andHarley . Ryan ndRoyA.Wiggins2004)each find vidence onsistent ith he deathat uccessful EOs are able tobargain orless independentoards.Boone et al. findthat ariables hat rereasonablyssociatedwithbargainingower ither or he boardor the CEO are significantnd have theright ign. n particular, easures f CEObargaining ower, enure, nd the CEO'sshareholdings,renegativelyorrelated ithboardndependence.he tenure indings,nparticular,reprecisely hat he Hermalinand Weisbach model predicts.Measuresthat ndicate hat heCEO hasrelativelyessbargainingower,ncludingutside irectorownershipnd thereputationfthe firm's

investmentanker tthe ime f ts PO, areallpositivelyorrelated ith oard ndepen-dence.Similarly,aker nd Gompers indthatmeasures hatreflect he CEO's bar-gaining ower,ncludingn estimatef theCEO'sShapleyalue nd he eputationf hefirm'sentureapitalists,ave hepredictedsigns negativeor heformerndpositiveorthe atter) ith especto thepercentagef

17 or instance,f the board's ctions re deter-minedby a median-voter odel, hen the incum-bent median director voter)knows that moni-toringwill be optimalfrom her perspectivefthere s no change n boardcomposition.f, how-ever, ompositionhangeso that he s no ongerhemedian irector,hen he evelofmonitoringill nolongerbe optimalfromher perspective.rovided,though,hat he tastes f the new mediandirectorrangeon a continuumrom he incumbent ediandirector's,henhaving new mediandirector ithonly slightly ifferentastes than the incumbentrepresents second-ordeross for the incumbent.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 11/51

Adams,Hermalin,ndWeisbach: heRoleofBoards fDirectors 67

non-insideirectorsn theboard.At oddswith heHermalin ndWeisbachmodel ndunlike oone tal.,Baker nd

Gompersind

apositive albeit tatisticallynsignificantrelationshipetween EO tenure ndper-centagefnon-insideirectors.inally, yanandWigginsind hat CEO's paybecomesless inked oequity erformanceshis on-trol ver heboard ncreasesproxied yhistenurendtheproportionf nsiders).heseauthorsnterprethese indingss consistentwith heHermalinndWeisbachargainingframework,ecause t uggestshat s CEOsbecomemore

owerful,heyse this

owerto improveheirwell-beinge.g., s here,where his ower llows hem o reduce hevolatilityf heirompensation).

Baker and Gompers, oone et al., andRyanndWigginsre ll ensitiveo he ssuethat overnancetructuresreendogenous.Baker ndGompers,nparticular,rovideconvincingolutiono theproblem y den-tifyinglausiblenstrumentsor he ndoge-neous ariablentheirpecification,enturecapitalfinancing,hese nstrumentseingthe tate f perationnd time ummyhatcaptures xogenous apital nflows o ven-ture apital unds. etnoneofthesepaperssheds ightn whetheruccessful EOs areable tobargain or less ndependentoardwithin hesamefirm,ecausethey ll relyon analyses f repeated ross-sectionsfdata rather hanpaneldatawith irmixed-effects.heddingmore irectmpiricalighton thedynamic ature f theCEO -boardrelationshipithin irms emains n inter-

esting opic or uture esearch.2.2.2 AssessmentndProjectelection

Dominguez-Martinez,wank, nd Visser(2008) is a model imilar o Hermalin ndWeisbach1998).A keydifferenceetweenthe two is that, n Dominguez-Martinez,Swank,ndVisser,t s theCEO whodeter-mineswhat nformationhe board earns.An interpretationfDominguez-Martinez,

Swank, nd Visser'smodel s that here retwopossible ypes fCEO, goodand bad.In each of two

productiveeriods,CEO

draws project trandom rom distribu-tion of differentrojects conditionalnCEO ability,achperiod's raw s an inde-pendentvent). hink f achproject eingsummarizedy tsnetpresentalue NPV).The differenceetween he twotypesofCEOs is that the distributionfprojects(distributionfNPVs o beprecise)sbetterfor hegood type han the bad type e.g.,thegood type's istributionominateshebad

type'snthe ense ffirst-ordertochas-

ticdominance).The CEO sees the stamped" PV on the

project e draws,whereas he board doesnot. n the econd final) eriod, heCEO'sincentivesre suchthathe implementsheproject e drawsf ndonlyf thas positiveNPV. n thefirsteriod, owever,heCEO'sincentivesrepossiblymisaligned ith hatof he hareholders:heCEO valueskeepinghis ob. If hisfirst-periodctions rperfor-mance ead thedirectorso infer e is the

badtype nd theboard s not ommittedoretain im, henhe willbe dismisseds it sbetter o draw gainfrom hepoolofCEOsthan o continue o the secondperiodwitha CEO who s known o be bad.TheCEO'sconcern boutretaining is job makes ttempting,herefore,or im o avoid isk ohisreputationynotpursuingvenpositiveNPVprojectsnthefirsteriod.

One potentialolution ouldbe for heboard to commit o retain hefirst-periodCEO for he econd eriod.With hat om-mitment,EOs would hooseonly ositiveNPVprojectsnthefirsteriod. his,how-ever,s notnecessarilyptimal ecausethedirectorsre throwingway heoption oreplace heCEO if heynfer e islikelyobe bad. That s, s is also notednHermalinandWeisbach,heabilityoreplace CEOa board nferssprobablyadcreates valu-able realoption or hefirm.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 12/51

68 JournalfEconomic iterature,ol.XLVIII March 010)

Figure . IllustrationftheDominguez-Martinez,wank, ndVisser2008) Model

Notes:TheprobabilityensityunctionsverNPV are shown or he two ypes. rom n informationaler-spective,heCEO should e retainedf ndonlyf he realizedvalue of projects aboveυ1. f,however,°denotes heprojectwith nNPV= 0,then heboard, o imit irst-periodosses,maywish o commit oretaintheCEO if ndonlyf he realizedvalue s above somecutofftrictlyetween l and u°.

Given thatgood-type EOs are morelikelyohave ositive PVprojectshan adtypes,n alternativetrategyor he boardwould be to commit o dismiss he CEOonlyfhedoesn't ndertakeproject. his,however,s notwithoutostbecause nowCEO couldbewillingoundertakenega-tiveNPVprojectf t snot o bad that hedisutilityesultingromursuingheprojectoutweighsisutilityrometainingis ob.18

Underhis overnanceule, omenumber fnegative PVprojects illbepursued.A third trategy ight e for he board

to commit o keep the CEO only f he

18Dominguez-Martinez,wank, nd Visser ssume aCEO's first-periodtilityunctions π + λχ,whereπ isthe returnsrom hefirst-periodroject, > 0 is his ben-efit fkeeping is ob,andχ € {0,1) ndicateswhether eloses orkeepshis ob, respectively.

undertakes positiveNPV project.Thismighteemoptimal,nsofars it voids eg-ativeNPVprojectsnd allows ome earn-ing,but couldneverthelesse suboptimal:howmuch s learned bout he CEO's abil-ity epends ntherelativeikelihoodfthetwotypeshaving rojects ith particularNPV. t s possible,herefore,hatf givenNPV is more ikely rom good type hana bad type, hen tcould be worth aving

thatproject ndertakenven ftheNPVisnegativeecause eeing heproject rovidesvaluable nformationbout heCEO's abil-ity. onversely,f givenNPV s moreikelyfrom bad type han goodtype, hen tcould be worthwhileismissinghe CEOfollowingherealizationftheprojectvenif ts NPV is positive. igure3 illustrates.Purelyromheperspectivef ptimalnfer-ence,the board hould etain CEO ifhe

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 13/51

Adams,Hermalin,nd Weisbach: heRoleofBoards fDirectors 69

hasa projectwith nNPVabovevl and dis-miss im therwise.f,however 1 0 = υ°,thenthis cutoff

mplies irst-periodosts.

Trading ff hesefirst-periodostsagainstthe value of information,he boardmaywish o set a cutoff,c,between 1 nd ν ;thats, CEO keepshis obif ndonlyfheundertakes project nd thatproject aysofft eastvc.

Dominguez-Martinez,wank,nd Visserobserve hat heirmodeloffers possibleexplanationorwhy vidence f poordeci-sionmaking" oes not lwaysead toCEOdismissal. ometimest is optimal o let aCEO pursuea bad strategyather hanstick o the status uo (i.e.,better opur-sue a negative PVproject atherhandonothing) ecause the nformationevealedfrom hat ourse f ction llows heboardtoupdate ositivelybout heCEO's ability.Admittedly,s formulatedere, he samemodelwouldalso explain he dismissal fa CEO aftermoderateuccess fmoderatesuccess s more ssociatedwith owabilitythanhighability.19ominguez-Martinez,Swank,nd Visser'smodel lso suggestsnexplanationorwhy ewCEOs rarelyeemto be ridingwithtrainingwheels whenit comes to managing heircompanies.LimitingCEO's range f ction, hile er-haps way o avoid iskymistakes,lso im-itshowmuch heboard an earn bouthisability. specially arlyn hiscareer,whenrelativelyittle sknown,he xpected alueof nformationan outweighheexpectedcostofmistakes.

2.2.3 Assessmentnd CEO SelectionHermalin2005) is concernedwith he

fact hatnformations more aluablewhena board s seeking o infer heability f a

19Dominguez-Martinez,wank,and Visser do notmake hispoint. his s one of heways ur nterpretationof theirmodel could be said to differ rom heir ctualmodel.

relativelynknownCEO than that of amore stablished eteran.he reasonsthatthe

optiono dismiss

poorly erformingCEO andhire newone s ike nexchangeoption.Consequently,ts value is greater,ceteris aribus, hegreaters the amountof uncertainty.ermalinbuilds on thisinsightoexamine herelationshipetweena board's tructurend tspropensityohirea new CEO from he outside an externalhire)versusfrom he inside an internalhire).Presumablyn internal ire s a bet-ter-knownommodityhan nexternalire,meaninghat n external ire ffersreateruncertaintynd, thus, a greateroptionvalue.An external ire s,therefore, orevaluable eteris aribus.How muchmorevaluable, owever,epends n thedegree owhich he boardwill monitorhe CEO (itsdegree fdiligence).iketheHermalin ndWeisbach1998)model, he boardmakesdecision s tohow ntensivelytwillmonitortheCEO, which s reflectedntheprobabil-itytwillget nadditionalignal orrelatedwith is bility.20ithouthe ignal,heres

nooption alue.Consequently,hevalueofuncertaintybout newCEO isgreaterhemore iligentheboard i.e., hemoreikelyit s toacquire hesignal) nd,therefore,more iligentoard smorewillingo tradeoff ther ttributesorgreater ncertaintythan is a less diligentboard. Hermalinargues hat his nsightffers n explana-tion orwhyhere as been a growingrendtoward othmore xternal ires nd horterCEO tenures:Due to increasedpressure

from nstitutionalhareholders, oregov-ernmentregulations, reaterthreatsoflitigation,nd newexchange equirements,boardshavebecomemorendependentnd

20Alternatively,ndessentially quivalently,hesignalis always bserved, ut tsprecisions an increasingunc-tionof the board'seffortstmonitoring.ee section ofHermalin.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 14/51

70 JournalfEconomic iterature,ol.XLVIII March 010)

MoreCEO

CompensationMore ceo nsk ^r I 1^S^ required or=> moreCEO >^ À Moré? sk ^^ greater ffortincentive S^ ^ more ^N*.

ySGreater '

incentive ^V^^ value f ι 1 ^^

More I I Greater I °Ption externalM°K

, I Greater. . ^ externalindependent -^* propensity > ceoboards to monitor ^ compensation

^^^ I Moreuncertainty ^^^^^. I =>.more

^^^ceo more ^^^ Τ likelyired ^^^likely o be ^^^ ▼

^^^ Compensationdiscovered low

^^^ Shorter J^^ requiredforability avemge fesjofe

ceo securitytenures

Figure . AGraphical ummaryf he Hermalin2005) Model

diligent.21ence,boards re morewillingto monitor,hich aises he ikelihoodheyhire xternallyor heCEO position.22oremonitoringirectlyaises helikelihood fCEO dismissalnd indirectlyaises t if tleadsfirmso hireCEOs aboutwhom ess sknown.

OneresponsefCEOs to his reater on-itoringressures for hem oworkharder"(which ouldbe interpreteds takingessperquisites).othbecausethey re led towork arder nd theirobs are lesssecure,

21See Huson,Parrino nd Starks2001) and Stuart .Gillanand Starks 2000) for vidence on trends owardgreater oard independencetechnically,oards with agreater roportionfoutsidedirectors)nd the rise ofinstitutionalnvestors.

22See KennethA. Borokhovich, arrino, nd TeresaTrapani 1996), Huson,Parrino, nd Starks 2001), andJayDahya,JohnJ.McConnell, ndNickolaosG. Travlos(2002) for vidence hat heproportionfnewCEO hiresthatare externalhas been increasing;he lastprovidesevidencefor his rend utside heUnited tates.

CEOs willdemand reater ay ncompen-sation.Hence, consequencefmore nde-pendent oards ver ime ouldbe upwardpressurenCEO compensation.23iguresummarizesermalin's odel.24

23AsHermalinnotes, hepositive orrelationetweenboard independence nd CEO pay in time series neednot mply positive orrelationn thecross ection tanypointntime.Hermalin ketches nextension fhismodelthatwouldpredict negative orrelationncross ection,despite positive orrelationver ime. ee his section .

24 t s worth otinghatHermalin s not heonly heo-

reticalexplanation orthe trendtowardmore externalhires and greater EO compensation. evinJ.Murphyand JánZábojník 2006); Murphy nd Zábojník 2004)offer non-boards-basedmodel that takes as its mainpremisethat there has been a declinein the value ofmanagers' irm-specificnowledge elative o thevalue oftheir eneralknowledge. s they how, hiswill ncreasethewillingness ffirms o hireCEOs externally. ivenMurphyndZábojníksmodeling f theCEO labor mar-ket, hisgreaterwillingnessogooutside ranslatesntorise n CEO compensation. ermalindiscusseshow hismodelcan be extended o incorporateheMurphy ndZábojníkmodel, ee hissection .

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 15/51

Adams,Hermalin,ndWeisbach: heRoleofBoards fDirectors 71

2.2.4 OtherAssessmentodels

A number f otherpapers

examine hemechanismsssociatedwith the board'sassessment f the CEO. Clara Grazianoand AnnalisaLuporini 2005) also has aboard hat eeks o determineEO ability.Criticalo theirnalysiss thepresence flarge hareholdern theboard, newho swilling obear thecost ofmonitoring,utwho alsogainsprivate enefitsfthecom-panypursues ertain trategiesprojects).Because onlythe large shareholder illmonitor,

heyind here an be advantages

to a dual-boardysteme.g., s inmuch fcontinental urope) because it may beadvantageousodivorcehemonitoringolefromhepower ohave sayover hecom-pany'strategy.avidHirshleiferndAnjanV.Thakor1994) ssume hat oards lwaysreceiveignals seful oassessingheCEO'sability,utboards iffernsofars some relax and someare vigilant. igilant oardsmay hoose ofire he CEO on thebasisofa badsignal. he situationn Hirshleifernd

Thakorscomplicatedy hepossibilityftakeoveridbyan outside artywith nde-pendentnformationboutthe firm; on-sequently,tmaybehoove vigilant oardnotto acton its own nformation,utwaitto see what nformationanbe learned ythepresenceornot)of a takeoverid andtheprice id.This rticlelsoexemplifieshefacthat oard overnancesonly ne ourceofmanagerialisciplinend,more pecifi-cally,tcaptureshenotionhat nternalnd

externalmonitoringan serve s substitutesorcomplements.incent . Warther1998)presentsnothermodel nwhich he boardacquiresnformationboutmanagerialbil-ity. ere,unlike heothermodelswe'vedis-cussed, ach director etsa private ignaland ggregationf nformationscostlynso-far s a director ho ndicates e receivednegativeignal s at risk f osing is boardseat fheprovesobe in theminority.

A recentstrandof the literature asrecognized hat he board'smonitoringfthe CEO can create, n effect,

dangerofopportunismrholdupbytheboard.25Theabilityodismiss heCEO after e hasmadefirm-specificnvestments eanstheboardcan appropriateomeofthe CEO'sreturns,hereby iminishingis originalinvestmentncentives.wopapers n thisstrandare AndresAlmazan and JavierSuarez 2003) andVolker aux (2008). Inboth, wo riticalssumptionsre i) initialcontractsetween oardand CEO canberenegotiatednd (ii) at least somekinds

of boards strongnAlmazan nd Suarez,independentnLaux)cannot ommito notbehaving pportunisticallyr aggressivelyinrenegotiation.

In AlmazanndSuarez, fter eing ired,a CEO can, tpersonalost, ake discreteaction hat aises, ya discretemount,heprobabilityhat given trategyrprojectwill ucceed. his ctions observabley heboard,butnotverifiable,hich reates nopportunityor ater oldup. fterheCEO

takes sinks) is action, profitableppor-tunityor hefirmmay rise hat equiresnew CEO toexploit.f the board s strongenough o fire he ncumbentEO infavorof newCEO, then heboard an usethatpossibilityoobtain alary oncessionsromthe ncumbentecause osing is obmeanshe oses privateenefit.he threat fbeingforced omake uch oncessionsan under-mine heCEO's initialncentiveo take hecostlyction.

To be more oncrete,onsider variationon Almazan and Suarez's dea:26 upposethat the new opportunityas the same

25Opportunismand holdup problemshave beenstudied n a largenumber f areas of economics inceWilliamson1975,1976).

26The actual Almazan and Suarez (2003) model ismorecomplex han what we presenthere. While thosecomplicationseadto a richernd morenuanced nalysis,they re notnecessaryoget he basic dea across.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 16/51

72 Journal fEconomicLiterature, ol. XLVIII (March 2010)

expectedpayoff s keepingthe incumbentCEO if he took the action and, thus, a

higher xpected payoffhan

keepinghim if

he didn't take the action. Suppose a weakboard will never fire the CEO when theexpectedvalue ofkeepinghimequals thatof the new opportunity,ut can fire himwhen the latter s greater.A strong oard isalways capable offiring he CEO. Assumeit s possible,whenthe threat odismiss heCEO is credible,for he board to capture,in renegotiation,he CEO's privatebenefitof control ndpushtheCEO to some reser-vationutilitycall it0). Hence, a CEO with

a strong oardhas no incentive o take theaction: f the newopportunityoesn'tarise,he retainshis job no matterwhat he did,there s no renegotiation f his compensa-tion, nd he enjoysthe controlbenefit.Butifthe newopportunityoes arise he gets0regardlessof his action; either he is fired,thus denied both pay and privatebenefit,or through enegotiations forceddown toa 0 reservation tilitypayoff). ecause hisultimate ayoffs independent fhis action,

he has no incentive o incur the cost oftak-ingit. The storys,however, ifferentorCEO who faces a weak board. Now, he isstrictlyetteroff fhe has taken the actionand the new opportunityrises: the boardcannotthreaten o firehim,so he contin-ues tocapturerentswage plus privateben-efit). f he didn't take the action and thenew opportunityrose,then he would losebothwage and privatebenefit. f the newopportunityriseswith owfrequency,o it

is efficient or he incumbentCEO to taketheaction, henhaving weak boardwillbebetter hanhaving strong oard.

In Almazan and Suarez, the distinctionbetween strong nd weak boards is a dis-tinctionabout theirbargaining power. InLaux (2008), the board alwayshas all thebargaining owerat therenegotiationtage(can make a take-it-or-leave-itffer o theCEO), but boards differ n theirdegree of

independence.This variation n degree ofindependence acts, however,like a shiftin

bargaining power. Consequently,for

reasons similar to those in Almazan andSuarez, a firm an be betteroffwith a lessindependentboard than a more indepen-dent board.

2.2.5 AdditionalEmpiricalAnalyses fAssessment

There is both anecdotal and statisticalevidence that boards dismiss poorly per-forming EOs. Based on interviews,Mace

(1971) and Vancil (1987) conclude thatboards fire, lbeit oftenreluctantly, oorlyperformingCEOs. There are numerousstatistical nalyses that show poor perfor-mance, measured either as stock returnsor accounting profits, ositively redictsachange nthe CEO.27 Simply ocumentingrelationship etweenpoor performancendan increasedprobabilityf a CEO turnover,although uggestive f board monitoring,snonetheless arfrom onclusive.After ll, a

sense offailure rpressurefrom harehold-ers could explainthisrelationship. o bet-ter identify he role played by the board,Weisbach (1988) interactsboard composi-tionand firm erformancen a CEO turn-over equation. His results indicate thatwhen boards are dominated by outsidedirectors,CEO turnover s more sensitiveto firm erformancehan t s in firmswith

27A problem acing mpiricalwork s thatfirms ftenoffer face-savingationale or change n CEO (e.g.,hewishes to spendmoretime withhis family) ather hanadmit he CEO was forced utfordoinga bad job. SeeJeroldB. Warner,Ross L. Watts, nd Karen H. Wruck(1988),Weisbach 1988),Parrino1997),and DirkJenterand Fadi Kanaan (2008) forfurther iscussions f thisissue and strategies ordealingwith it. To the extentnon-performance-basedEO turnover s random, tsimplydds noiseto turnover egressions,husreducingthe powerof suchtests,but leaves them unbiased andconsistent.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 17/51

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 18/51

74 Journal fEconomicLiterature,Vol. XLVIII (March 2010)

performanceaverageTobin'sQ) is increas-ing in board size for ertaintypesoffirms,

namelythose thatare

highlydiversified r

that rehigh-debt irms.Perry 1999) breaks down the cross-sec-

tional relationship etween CEO turnoverand firm erformance ywhether he out-side directors re paid using ncentives.Hefindsthat the relationship etween CEOturnover nd firmperformances strongerwhen boards have incentives.This findingsuggeststhat providing explicit ncentivesto directors eads them to be morevigilant(actmore ndependently). eyond ncentive

reasons, nother otential xplanations thefollowing:n firms hat make use of incen-tivepay fordirectors, he directorshave aprofessionalather han a personalrelation-shipwith the CEO and, thus, re relativelyindependentf him.

To conclude thissection, t is worthnot-ingthat fewanalysesofCEO turnover on-trol for firm-specific eterogeneity singfirm ffects. s increasinglyongpanel-datasets become available,futureresearchwill

be able to shed more lighton within-firmchanges nCEO turnover.

2.3 Setting fStrategyIn addition o makingdecisions concern-

ing the hiring nd firing f CEOs, boardsmayalso be involved n the setting f strat-egyor,somewhat quivalently,he selectionofprojects.Certainly urveys f directorssee the discussionof Demb and Neubauer(1992)above indicate hatdirectors elieve

themselves o be involvednsettingtrategy.2.3.1 Theory

To anextent,many f hemodelsdiscussedabove could be modified to make themaboutboards' oversightf strategy.nsteadof replacingthe CEO, the board compelshimto changestrategy.n an adaptationofAlmazan and Suarez (2003) or Hermalinand Weisbach (1998), the CEO could be

assumedto have an intrinsic reference orthe ncumbenttrategyersus replacement(the ncumbent

trategyrovides, .g.,more

opportunityo consumeperquisites). n anadaptationof Laux (2008), similar resultswould follow f one assumed the financialreturns o thereplacement trategyre inde-pendent f the CEO's initial ctions.

An alternativemodeling approach is toinvestigatehe choice of strategys a gameof informationransmission: he CEO (ormanagementmore generally)has differentpreferenceshanthe boardconcerning roj-ects (strategies). numberofobservers re

comingto the view that nformationrans-mission between the board and the CEOis important orgood governance see, e.g.,Holmstrom 005). This is particularlyruewhen the CEO has payoff-relevantrivateinformation,nsofar s an agency problemarises because the CEO can influence heboard'sdecision hroughhestrategiceleaseof nformation.

Adams and Ferreira (2007) build amodel based on four broad assumptions:(i) the CEO dislikes limits on his actions(loss of control); ii) advice from he boardraises firmvalue without imiting CEO'sactions; iii) the effectivenessf the board'scontrol nd the value of its advice are bet-ter the more nformed heboardis; and (iv)the board depends cruciallyon the CEOforfirm-specificnformation.n the Adamsand Ferreiramodel,the board can learn theamount, G [0,1],bywhich project houldbe optimally djusted e.g.,what the appro-

priate level of investment n it should be).The board can do this,however, nly ftheCEO has informed hem bouttheproject. tis assumed the CEO canwithhold hat nfor-mation,but if he chooses to share it,thenhe mustdo so honestlyi.e.,usingthe stan-dardterminologyfthe contractsiterature,the informations "hard").The CEO has abias, b > 0, such that he likes to increasethe size ofprojects e.g., nvestmore than s

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 19/51

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 20/51

76 JournalfEconomic iterature,ol.XLVIII March 010)

lossfrom he size of theprojectometimesbeingdistortedi.e., n those stateswhenthe CEO retains ontrol).he Adams ndFerreiramodel lso implies hat tmaybeoptimal oseparate headvisoryndmoni-toringoles f theboard; hat s,to have adual board ystems inmany ountriesnEurope.

Milton Harris and ArturRaviv 2008)is similarn spirit o Adams nd Ferreira.Harris nd Raviv ssume hat heCEO andthe nsider irectors,ike he outside irec-torsnAdams ndFerreira,ave nformationrelevanto thequadraticoss. The payoffs,net offixed erms ndadditivelyeparableaspects f heir espectivetilities,re

Uo - -(s - ao - ö7)2 and

Ui = -(s - ao- aI- b)2,

where he ubscripts and denote utsid-ers and insiders,espectively,ndat is theinformationhatthe t groupof directorshave about heoptimal ize oftheproject.Observe, ow,hat he ptimalizefromheshareholders'erspectives = ao + a7.Thevalueof tis theprivatenformationf thet group f directors. nlike nAdams ndFerreira,ow t could be suboptimal,romthe hareholders'erspective,ogive ontrolover to theoutsiders:lthoughhe nsiderswillalmost urely otchoose heoptimalgiven ontrol,heymight etcloserftheirinformationsparticularlyaluablei.e., hevariance fal is relativelyig).Harris nd

Raviv onsiderwo oard tructures:utsidercontrol nd insider ontrol.Whengrouphas control,t has the choiceofchoosingordelegatinghechoice o theother roup.Whengroup makes he choice t receivesa message romhe other roup bout hatother roup information.sinAdams ndFerreira,heequilibria f thesecheap-talkgamesdo notpermit ull nformationev-elation.Whenthe insiders' nformations

sufficientlyaluablerelativeo the outsid-ers' i.e.,Var(ö7)/Var(öo)κ > 1,κ a con-stant hat

ependsnparameter

alues) ndinformations valuable elativeothe gencyproblemspecifically,ar(#7)/fo2ω > 1,ωa constant hatdepends n parameteral-ues), hen nsider ontrols superioro out-sider ontrol.fthose onditionsren'tmet,then utsiderontrolssuperior.

Like Adams nd FerreirandHarris ndRaviv,Charu G. Raheja (2005) wishes ounderstandoard tructuren he ightf heboard's eed oobtainnformationbout hefirm'srojects r strategies.nlikeAdams

andFerreira, here ll boardmembersreequally gnorant,r Harris ndRaviv, hereboth nside ndoutside irectorsespectivelyhaveprivatenformation,aheja assumesthat nly he nside irectorsossess rivateinformation.ncontrasto most f he itera-ture,Rahejadeparts rom he dea that henon-CEOnside irectorsnd heCEO havecoincidentncentives.nsiders ontrol heCEO throughhe hreatf ratting"im utto theoutsiders,howill henoinwith he

insidersnfiringheCEO, should heCEOmisbehave.Although clevermodel, t is difficult

to reconcileRaheja'smodelwiththe evi-dence in Mace (1971) or Vancil (1987).Insubordinationy a CEO's managementteam seems exceedinglyare. Moreover,what vidence here s aboutwhistle-blow-ers rats)s hardly ncouragingorRaheja'smodel.Anecdotalvidence,t east, uggeststhat whistle-blowersend to suffer,more

than e rewarded,or heirctionssee, .g.,Joann . Lublin, 002).Evidence fwhistle-blowers oing o outside irectorss rarethe mostprominentecentwhistle-blower,Enron's herronWatkins,ornstance entto theCEO (KenLay)with er oncerns.

FenghuaSong and Thakor 2006) alsoconsidernformationransmissionelevanttoprojectelection. ike ome therworknthis rea, hey uild n thecareer-concerns

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 21/51

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 22/51

78 JournalfEconomic iterature,ol.XLVIII March 010)

option hat s never xerciseds worthless;hence,fthesignalwere omplete oise, swouldbe the case ifboardhad zero

qual-ityrecall hesignal's ariance s 1/q),herewould eeffectivelyooption. s the ualityof heboard nd, hus,nformationmproves,the more valuable this optionbecomesand,therefore,he morevaluable hefirmbecomes.

It is not, however,ostless o increaseboard uality ithout ound. irst,t seemsreasonablehat igher uality irectorsom-mand premiumr that rovidingboardwith ufficientncentivesodo a high-qualityjob is expensive.o thecostofboardqual-ity s increasingn quality.Under uitableassumptionsbout this costfunctione.g.,thatmarginalostbe risingnq),therewillbe anoptimal inite aluefor . In addition,if heCEO labormarketeacts o the ignalso that heCEO's futurealarys an ncreas-ingfunctionfthesignal, hen he CEO isexposed o more uturealary isk hemoreinformativehe signal s (i.e.,the greaterisq). Intuitively,heposteriorstimate f he

CEO's abilitys a weighted verage f theprior, hichs fixed,nd thesignal,whichis noisy. hemore nformativehesignal sknown obe,themoreweightsassignedhesignal. his ncreaseshe CEO's riskmorethan he ower ariance f thesignal tselfreduces t seeHermalinndWeisbach 009for etails).A CEO willrequire ompensa-tion or hisgreaterisk,o his nitial alary(winexpression1))willhave o be greater.In light fthiscost,under uitable ondi-

tions,twill gainbe thecase that finiteisoptimal.Fromexpression1), the marginalnet

returnoq is

1 λ ( -rr' TT3/2 dw

2rq20'^Jλ _

~dq

(note '/H = -rr/y/H). hechangenthemarginal et return oq with espect or,

the measure f thecurrentconomic nvi-ronment,as the ame ign s

άφί=μ' < 0drY'y/Hj

where the inequality ollows ecause anincreasen r is a movefurthernto he efttail of thedensity.herefore,hemarginalnetreturn oq is fallingnr,whichmeansthat heoptimal ualityf heboard s owerwhen conomic onditionsregood i.e., shigh) hanwhen hey re bad (i.e., is low).Intuitively,hen imes regood, he boardwillwish to let mediocre EOs go aheadwith rojects,ut heywon'twhen imes rebad. Consequently,he value of mprovingthemonitoringfprojectss greater hentimes rebad thanwhen heyregood.

Nina Baranchuknd PhilipH. Dybvig(2009) is an interestingrticlen this reabecause t s notworriedbout nformationtransmissionetween EO andboard,butamong hevariousboard membershem-

selveswhich,npractice,ncludeheCEO).Each director has a belief,tGW1, s towhat he firmhould o. Similar oAdamsand Ferreira2007) and Harris nd Raviv(2008),a directorxpects o suffer qua-draticoss nthedistance etween isbeliefsas to what hefirmhould o and what hefirm'sctual ourse f ction, , is;thats,adirector'stilitys

- || a, - â ||

The directorsrrive t â accordingo a solu-tion oncepthat he uthorsall consensus.This solution oncepthas manydesirableproperties,ncludingxistence or ll suchgames. weaknessf he oncept,owever,sthat heres noexplicitxtensive-formametowhich t s a solutionconsensuss a coop-erativegame-theoreticoncept).Anotherissue s there s no scope fordirectors o

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 23/51

Adams,Hermalin,nd Weisbach: heRoleofBoards fDirectors 79

update heir eliefs asedonwhat heyearnof thers' eliefs. bsentiases n thepart fthedirectors,t s not lear

whyhedirectors

wouldnotfreelyhare heirnformationndarrive t a consensus eliefwhich n turnwould eadto a unanimoushoice s towhatthefirmhould o.

Bythe revelationrinciple,he nforma-tion-transmissionodels discussed herecould all be solvedby a direct-revelationmechanismf complete ontracting erepossible.34hat s, f theparties ouldfullycommitndmonetaryransfersfany evelamong hemwerefeasible,hen hepartiescould chieve n nformationallyonstrainedoptimumvia contracting.here would,therefore,e noneed toworryboutboardcompositionr control. ence,as is com-mon fmanymodels eekingoexplain heinstitutionseobserve,here s a reliance,tsome evel, nthe ssumptionhat ontract-ing is necessarilyncomplete.n particu-lar, ither oards annot ommitullys tohowtheywilluse the nformationevealedto them r it is infeasibleontractuallyor

them opaythe CEO (orothers)na man-ner sufficiento induce fficientevelation.For nstance,nHarris ndRaviv 2008),direct-revelationechanism oulddo bet-terthantheequilibriumutcomes onsid-eredprovidedhat hepartiesould ontractdirectlyn the izeof heprojects a func-tion ftheir nnouncementsndthey ouldmake transfers. lthough his literaturetendsnot oexplore ully hy ontractsreincomplete,asual empiricism ouldsug-

gestthat here re, ndeed, imits o bothcommitmentsnd transfers.o,realistically,organizationsre necessarilyn a second-or third-bestituation. onsequently,he"law ofthe secondbest" often pplies toremedy,n part, hesecond- r third-bestproblem,hepartiesangainby ntroducing

34Note Song and Thakor is not an information-transmission odel.

another,artiallyffsettingroblem.35ntheliteraturenboards,he ffsettingproblem"is

havingless

diligent/lessontrolling/lessindependentoard.Having "lax" oard s away fpartiallyommittingo how nforma-tionwillbeused, hereby imicking,npart,thecommitmenthat contractualolution,were nefeasible, ould rovide.2.3.2 EmpiricalndExperimental

Evidence

Ann B. Gillette, homas H. Noe, andMichaelJ.Rebello2003);Gillette, oe andRebello 2008)perform series f nterest-

ingexperimentsesignedoget t the ssueof nformationransmissionithinheboard-room.n Gillette, oe,and Rebello 2003),they onsider laboratoryettingnwhichinformednsiders re groupedwith unin-formed utsidersn a simulated oardroomsetting.hey ind hat he nclusionf utsid-ers mproves elfarey makingndesirableequilibriaess ikely.illette, oe, ndRebello(2008) compare, gain n a laboratoryet-ting, ingle-tieredoards,wo-tieredoards,

insider-controlledoards, and outsider-controlledoards. heyfind hat wo-tieredboards end o be overlyonservativentheirchoices nd thatoutsider-controlledoardstend o ead othemost fficientayoffs.

The class of modelsbased on strategicinformationransfermplicitlyelies ontheassumptionhatoutsider irectorsreless well informedhan are inside direc-tors. nrichetta avina nd PaolaSapienza(forthcoming)dopta clever pproach o

testingthis assumption.These authorsexamine he relative rofitabilityf tradesintheirompanies'tocksmadeby utsiders

35An exampleof the law of the second best is, forinstance, ncouragingomedegreeof cartelization f apolluting ndustry: y reducing ompetition, ricewillbe driven above privatemarginal ost; hence, societymayhopetoget pricecloser o socialmarginal ost i.e.,cost inclusive f the negative xternalityaused bythepollution).

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 24/51

80 JournalfEconomic iterature,ol.XLVIII March 010)

and insiders nd find hat bothtypesofdirectors arn abnormal rofits,ut thatinsiders arnbetter eturnshando outsid-ers.These resultsuggesthat oth ypes fdirectors ave access to inside nformationbut that outsiders' nformations strictlyworse han nsiders'. hus thefindingup-portsthe underlyingssumption f theinformation-basedodels fboards.

Breno Schmidt2008) considers situ-ation n which advice could be particu-larly aluable, amely uringmergersndacquisitions.n the basis of the social tiesbetween he CEO and otherdirectors,e

classifiesoards s "friendly"ties xist) nd"unfriendly"a continuousmeasure s alsoemployed).When t is likelyhatdirectorspossess aluable nformationbout nacqui-sitionan ndexmeasure),hereturnsftheacquirerrehighern announcementf heacquisitionorbidderswithmorefriendlyboards.Conversely,hen he need to disci-pline hemanagers a greateroncern,ocialtiesprove o be a negative.

Althoughheres a growingmpiricalit-

eratureeekingo estimateherole fdirec-torsnstrategyetting,t s safe osay hatthis s an area nwhichmuchwork emainsto be done.

3. How are Boards fDirectorsStructured?

We havediscussedomeexplanationsorwhy here re boards, ndwhy ne mightexpect ndogenously-chosenoards opro-

videmonitoringfmanagement,espitehefact thatmanagementypically as somesayover the board's omposition.ut thetheories imply rovide stylized escrip-tion f heunderlyingensionsntherole fthe board n corporate overnance. ctualgovernances much icher han hesebare-bones haracterizations.

There are a number f questions hatcan onlybe answered y looking t data

on real-worldoards fdirectors. ow areboards structuredn practice?Does thisstructureoincide ith he arlier-discussedtheories? owhas t hangedver ime, othinresponseochangesntheeconomyndregulatorynvironments?

3.1 SomeFacts

Observersypicallyividedirectorsntotwo groups: nside directors nd outsidedirectors.Generally, directorwho is afull-timemployeef thefirmn questionis deemed o be an insidedirector,hiledirector hoseprimarymployments not

with hefirms deemed to be an outsidedirector. utside irectorsre often aken obe independentirectors,et he ndepen-dence f ome irectors homeet hedefini-tion f noutsidersquestionable.xamplesof uchdirectorsre awyersrbankers hodo businesswith hecompany.utsidersfdubiousndependenceresometimesut na third ategorynempirical orksee,e.g.,HermalinndWeisbach988): affiliated"r"gray"irectors.nrecent ears, ublic res-sure and regulatoryequirementsave edfirmso havemajority-outsideroards.

The characteristicsfboards f argeU.S.corporationsave eendescribedn numberof tudies. or xample,ich nd Shivdasani(2006)considersample f 08of he argestU.S. corporationsetween 989 and 1995.They indhat,naverage,utsiders ake p55 percentfdirectors,nsiders0 percent,and affiliated irectors he remaining5percent. he average oard ontains welve

directors, ach receiving approximately$36,000 nfees plus tock ptions),nd has7.5meetingsyear. numberf hedirectorsserved nmultipleoards; heoutside irec-torsnthese irmsveragedver hree irec-torships. hile hese ata reforarge ublicfirms,ames . Linck, effry. Netter,ndTinaYang2008)consider larger ample f8,000 necessarily)mallerirms,ith imilarpatternsnthedata.

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 25/51

Adams,Hermalin,nd Weisbach: heRoleofBoards fDirectors 81

While the existence nd basic structureofboardshaveremainedelativelyonstantover ime, he

waynwhich

heyre com-

posedhaschanged. ehn, ukesh atro,ndMengxinhao 2009)considersample f 1firmshat ave urvivedspublic ompaniesfrom935until 000.Survivorshipias om-plicates he nterpretationf their indings,neverthelesshey eflectomebasic trendsthathaveaffected oards.First, oard izeappears o have hump atternver ime;taverages1 n1935, eaks t 15 n1960, nddeclines o11 n2000.However,oard izehas becomemore niformver ime s thestandard eviation fboard izedrops rom5.5 n 1935 o 2.7 n2000. These ompanies'boardshave become more outsider-domi-nated s well; nsider epresentationropsfrom 3 percentn 1935 to ust13percentin2000. Part fthisdrop an be explainedbythetypicalife ycle f firms. s found-ingfamilies xit and firms ecome moreprofessionallyanaged, gency problemscan becomeworse s thosencontrolre nolonger ignificantwners.n response,irms

willwish oadd outside irectorso counter-act he ncreasedgency roblems.Since2000, therehave been significant

changes. arbanes-Oxleyontained num-berofrequirementshat ncreased hework-loadof ndthedemand or utside irectors(see Linck,Netter,nd Yang2009 foradescriptionf theserequirements).n addi-tion, he scandals t Enron nd Worldcomhave ed o ubstantiallyncreasedubliccru-tinyfcorporate overnance.onsequently,

boardshave become arger,more ndepen-dent,have morecommittees, eet moreoften,ndgenerallyave more esponsibil-ity nd risk againsee Linck,Netter,ndYang2009).Thesechanges oth ncreasedthedemand or irectorsnd decreased hewillingnessf directorso serve or givenprice. t is not surprising,herefore,hatdirectorayand liabilitynsurance remi-umshave ncreasedubstantially.rom he

shareholders'erspective,heneteffect fthisregulations notclear;future esearchwillneed to address heextent o which headditionalmonitoringffsetshe ncremen-talcostsmposed ySarbanes-Oxley.3.2 FactorsnBoardCompositionhat

PotentiallyffectBoard'sActions

We havealready iscussedmuchoftheliterature elating oard compositioninterms f the insider-to-outsideratio) ndboard ize to board ctions egardingver-sight ftheCEO, as well as to overall irmperformancesee section .2). Yetbeyondthe nsider-to-outsideratio nd board ize,other oard ttributeso doubt lay role.Each boardof directorss likelyo have tsowndynamics, function fmany actorsincludinghepersonalitiesndrelationshipsamong hedirectors,heir ackgroundsndskills,nd their ncentivesnd connections.Some ofthesefactorsrereadilymeasuredwhileothers re not.Therehas been con-siderable esearch hat eeks o estimateheimpact f various oard characteristicsn

board onduct ndfirmerformance.3.2.1 CEO-ChairmanDuality

Many EOs alsohold he itle fChairmanof theBoard;thisduality olds n almost80 percent f largeU.S. firmssee PaulaL. RechnerndDan R. Dalton1991).Thisstructures viewed ymanysgiving EOsgreaterontrol t theexpense f other ar-ties,ncludingutside irectors.omitigatethe onsequent roblems, anybserversf

corporateovernanceave alled or prohi-bition n theCEO servings chairmansee,e.g.,Michael . Jensen993).

Anumberfrecent apers ave xaminedtheuse ofdual itlesncorporateovernanceempirically. ames A. Brickley,Coles,and GreggA. Jarrell1997) estimates heperformanceffectsf ombineditles. heseauthors ind ittle vidence hat ombiningor separatingtitles affects corporate

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 26/51

82 JournalfEconomic iterature,ol.XLVIII March 010)

performance.hey onclude hat hesepa-ration nd combinationf titles s partofthe natural uccession

rocessescribed

yVancil 1987). n contrast, oyaland Park(2002)findhat he ensitivityfCEO turn-over operformances lowerwhen itles recombined,onsistent iththe notion hatthe combinationf titles s associatedwithincreased ower verthe board.Similarly,Adams, eitor lmeida,nd Ferreira2005)find vidence onsistentith he viewthatCEOs alsoholdinghe hairmanitleppeartohold reaternfluencever orporateeci-sionmaking.

Overall,hese tudies re consistentiththeview hat ombineditles reassociatedwithCEOs havingmore nfluencen thefirm.However,his relation s not neces-sarily ausal. nfluencenside n organiza-tion rises ndogenously,nd with nfluencegenerallyomefancieritles. heGoyal ndPark and Adams, Almeida, nd Ferreirafindingsotentiallyeflect EO power hatcame bout ndogenouslyhroughmannersimilaro hat escribedntheHermalinnd

Weisbach1998)model. n otherwords,CEO whoperformsellwould e rewardedbyhisbeing ivenhe hairmanitle s well.Sucha process, speciallyfthe ncreasenpower rises ecause f demonstratedighability, ouldnotnecessarilymply erfor-mance hanges ollowinghiftsntitles,on-sistent ith heBrickley,oles,andJarrellfindings.

Even f t strue hat ombininghe itles fCEO andchairman eans hat n ndividual

has, naveragemore nfluencever isfirm,it does not follow hatmandatingeparatetitles ouldmproveorporateerformance.In fact,Adams,Almeida, nd FerreirasimilaroBrickley,oles, ndJarrellfindthatmeasures fCEO powerrenot ystem-aticallyelated ofirmerformance.his sconsistent ithour overarchingrgumentthatactual corporate-governanceracticeneeds to be seen as partof the solution o

the onstrainedptimizationrogramhat scorporategovernanceesign. ence,mpos-

ing separateitleswould ither

ieldless

optimalolution r ead toa,possiblyneffi-cient, ork-aroundhatmaintainedheopti-mal amount f CEO power.36 oreover,snoted arlier,makinghe CEO's job worselikelymeans noffsettingncreasenpay scompensation.onsequently,s withmostpolicyprescriptionsn the area of gover-nance, olicymakershould ewary f allsfor rohibitingheCEO servings chairman.

3.2.2 Staggeredoards

A common, et ontroversial,overnancearrangements known s "staggeredoards."When firm as a staggeredoard,nsteadofholdingnnual lections or ach direc-tor, irectorsre electedformultiple earsat a timeusuallyhree),ndonly fraction(usually third) fthedirectorsre electedin a givenyear.This practice s typicallyadopted s a wayofshielding firm romtakeover ecause a potential cquirer an-notquicklyakecontrol f the firm's oard

even it controls 00 percent f the votes.This rrangements more ommon han nemightmagine in theFaleye 2007) sam-ple,roughlyalf fthefirms ave lassified(staggered)oards.

While the consequence f the separa-tionof the CEO and chairman ositionson firmperformances ambiguous,essambiguityxistswithrespect o staggeredboards; the empirical vidence ndicatesthisarrangements not n the sharehold-

ers' nterestsalthough,s withmuch ftheempiricalwork, aution s warranted ueto joint-endogeneityssues). Both Jarrelland Annette . Poulsen 1987) andJamesM.MahoneyndJoseph .Mahoney1993)

36Recallthat,n a number fmodels fboards, edingsome ontrol omanagementsoptimalseee.g.,Almazanand Suarez2003; Laux 2008; Adams nd Ferreira 007;and Harris nd Raviv 008).

This content downloaded from 146.141.15.220 on Tue, 29 Oct 2013 04:14:41 AMAll use subject to JSTOR Terms and Conditions

8/14/2019 A Conceptual Framework and Survey

http://slidepdf.com/reader/full/a-conceptual-framework-and-survey 27/51

Adams,Hermalin,nd Weisbach: heRoleofBoards fDirectors 83

find egativeeturns henfirms nnouncethey re classifyingheir oards although

Jarrellnd Poulsen's

indings notstatisti-

cally ignificant).ebchuk, ohn . Coates,and Guhan Subramanian2002) find hata classified oardalmost oubles heoddsthat firm emainsndependenthen acedwith hostileakeover.ecause omewould-be acquirersreno doubt cared ff ythestaggeredoard, heBebchuk, oates, ndSubramanianindingsikely nderestimatethe bilityf classifiedoard o resist ake-overs. ebchukndAlmaCohen 2005)findthat irms ith taggeredoardshave owervalue han ther irms,sing obin's as ameasure f alue. inally,aleye2007)findsthat staggeredoard owershe ensitivityofCEO turnoverofirmerformance.

An mplicationftheview hat taggeredboards entrenchmanagers nd decreasevalue s thatwhen irmsdestagger,"eturnto annualelections or ll directors,alueshould ncrease.Re-JinGuo, Timothy .Kruse, nd TomNohel 2008) considersample ffirmshat estaggernd find hat

the alue f hese irmsoes,nfact,ncrease.They lsofind hat estaggerings not ypi-cally nitiatedy managers,utbyactivistshareholders.ubsequento thedestagger-ing, nvestoreactionndicates hat thesefirmsre more ikelyo be takeoverargets.All ofthesefindingseinforceheview hatstaggeringoardss a mechanismhat ervestoprotectmanagementymakingakeoversdifficult.