945 1035,fri-analytical insights

24

vv

-

Upload

summit-professional-networks -

Category

Documents

-

view

118 -

download

0

Transcript of 945 1035,fri-analytical insights

vv

Building the Foundation for Analytics

A Data Management Perspective Tracy A. Spadola CPCU, CIDM, FIDM V.P. Business Development – Insurance Data Management Association Practice Lead – Insurance – Teradata Corporation

Persistent Economic Turmoil, Market Uncertainty

Increased Frequency & Severity of Cat Events

Regulatory Environment Growing more Onerous

Tech Savvy, Demanding Customers Expensive & Hard to Manage

Distribution Channels

Increased Customer & Market Competition

Major Challenges in the Business Environment

Major Challenges in the IT Environment

Legacy Systems Upgrades Cyber Security

Big Data New Technologies

* Data Management Challenges

Insurers are Often Flying Blind

Each Discipline has its Own Data

No Common Understanding

No Complete View of Customer, Agent Decisions Based on Incomplete Information

BABEL

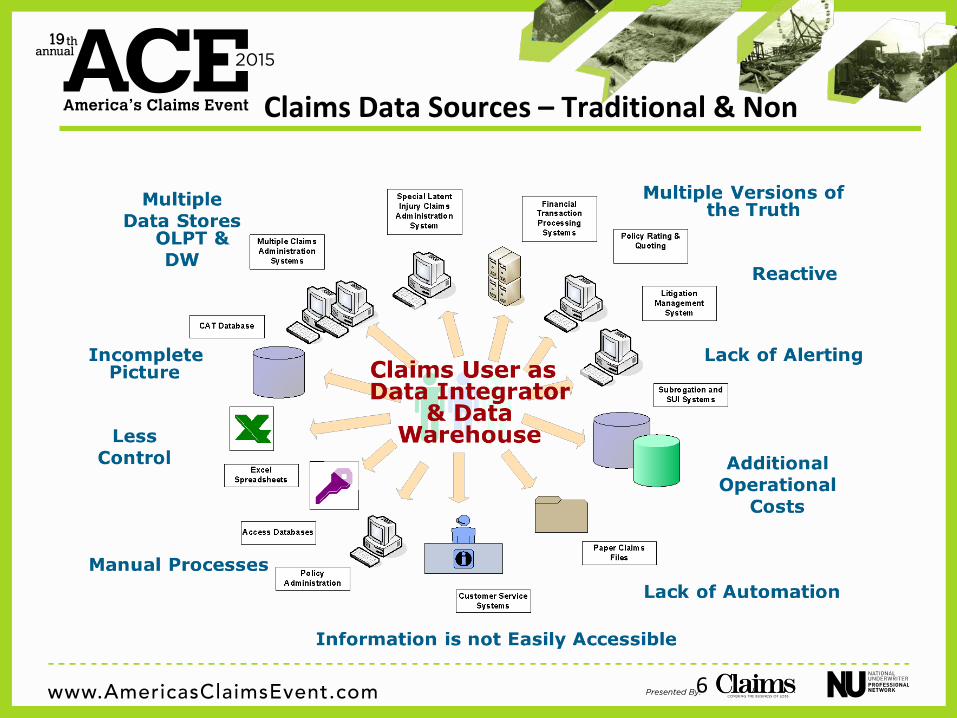

Claims Data Sources – Traditional & Non

6

Why Data Management in Claims is Important

• Data Silos – Claims data can include many information silos including subrogation,

litigation management, adjusting, financial, case management, vendor management and more.

• Data Management – assures better claims data integration for more accurate analytics and

information as well as faster claims investigations. – allows for more automation of processes including fraud detection. – enables better regulatory claims compliance and reporting – enables product development, reduction of costs and more.

7

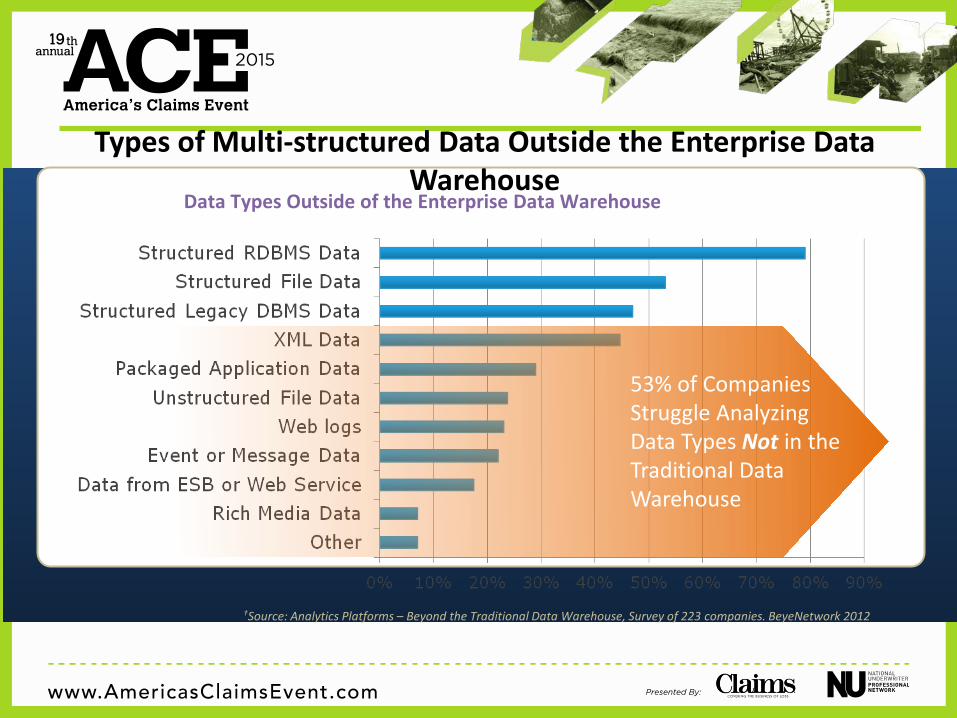

Types of Multi-structured Data Outside the Enterprise Data Warehouse

†Source: Analytics Platforms – Beyond the Traditional Data Warehouse, Survey of 223 companies. BeyeNetwork 2012

Data Types Outside of the Enterprise Data Warehouse

53% of Companies Struggle Analyzing Data Types Not in the Traditional Data Warehouse

Big Data, Analytics & Its Challenges

• “Non-Traditional” data sources – Web activity, telematics, weather, social media, etc. – 3rd Party data – Limited data standards

• Beyond structured – Unstructured and Multi-Structured data requiring new

technologies (hardware and software)

• Highly iterative analysis

Big Data Requires multiple Information Management strategies and new technologies.

Integration across the Analytic Ecosystem is critical

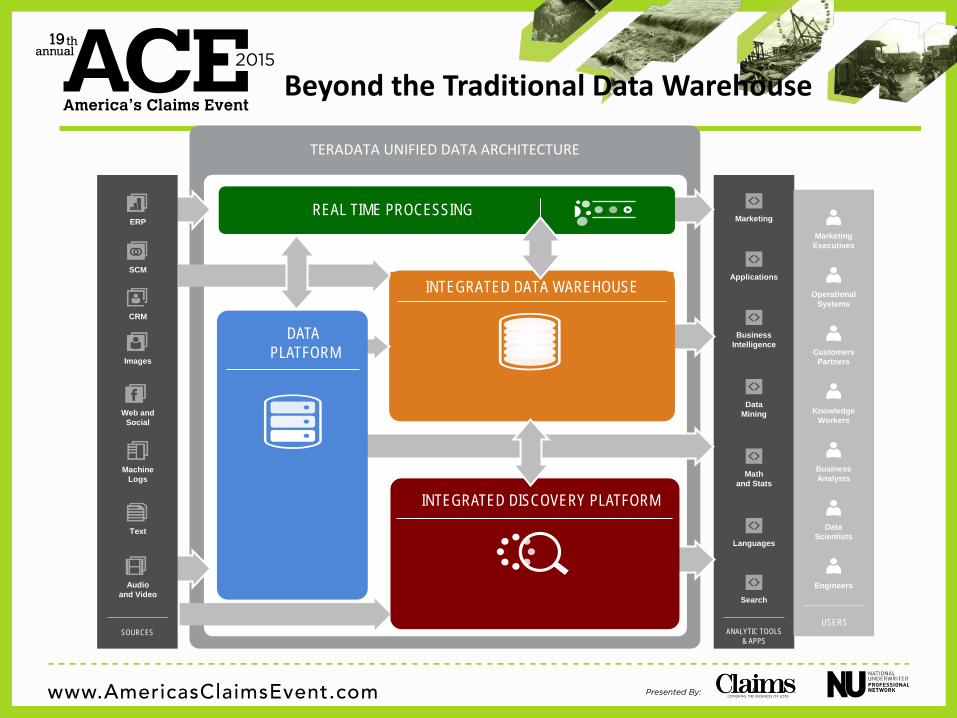

Beyond the Traditional Data Warehouse

TERADATA UNIFIED DATA ARCHITECTURE

Security, Workload Management ERP

SCM

CRM

Images

Audio and Video

Machine Logs

Text

Web and Social

SOURCES

Marketing Executives

Operational Systems

Frontline Workers

Customers Partners

Engineers

Data Scientists

Business Analysts Math

and Stats

Data Mining

Business Intelligence

Applications

Languages

Marketing

USERS

ANALYTIC TOOLS & APPS

Search

Marketing Executives

Operational Systems

Knowledge Workers

Customers Partners

Engineers

Data Scientists

Business Analysts

USERS

INTEGRATED DATA WAREHOUSE

DATA PLATFORM

INTEGRATED DISCOVERY PLATFORM

Security, Workload Management REAL TIME PROCESSING

Final Thoughts

• More and More Big Data is not traditional Insurance Data – Understand the Data Quality implications

• Identify the right platform for the particular data source

– Reporting, Analytics, File Storage, Discovery

• Implement solid Data Management practices for increased Business Value

vv

Making Data Important

Presented by: Stephanie Behnke, Innovation Director

Mercury Insurance Group

• Creating a Data Centric Culture – Begin with the

Executives – Meet with the claims

handlers – Remember that not

everyone realizes how sexy data is!

– Apply standard change management techniques

• What’s in it for me • Provide examples of

current data gaps • Walk the team through

the possibilities in a world of accurate data – automation, ease of use, predictive claims handling

• Follow Up is Key – Bring success stories to

the team – Share pitfalls or gaps

during audits – Always tie data integrity

to new reports, features, or automation

• Keep reminding the team that data and measurement matters

vv

Fraud Management

Presented by: Tamer Soliman Vice President

© Assurant, Inc. 2015 - This document is the property of Assurant, Inc. All information contained herein and any related material thereto is considered proprietary and confidential. The content cannot be duplicated, distributed, replaced, shared, or conveyed either in whole or in part, electronically or in hard copy to any third parties without the prior written consent of Assurant, Inc.

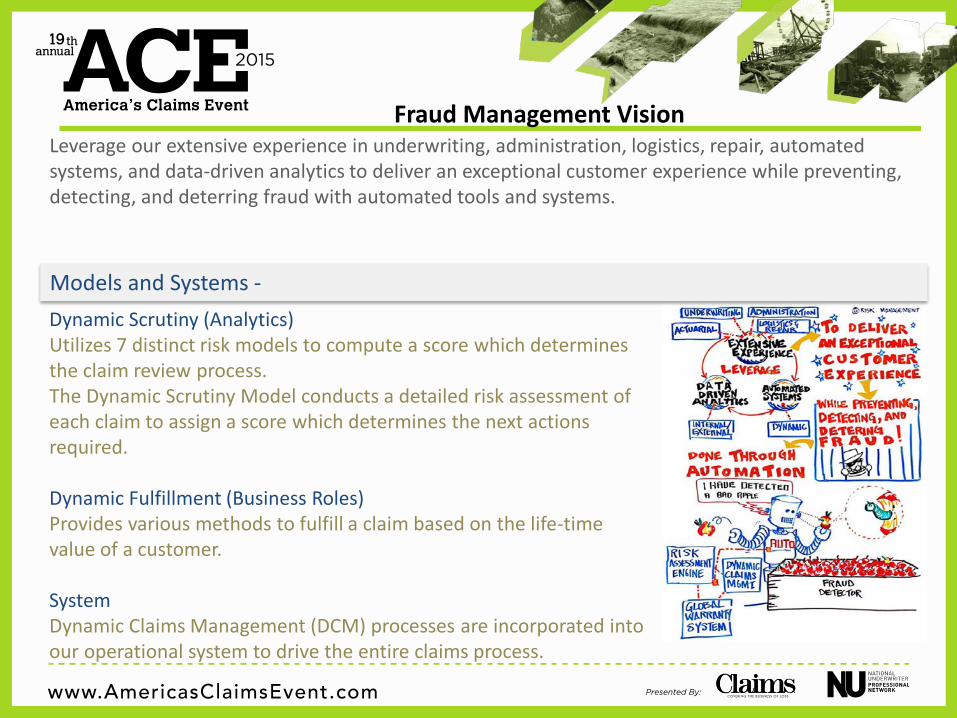

Fraud Management Vision Leverage our extensive experience in underwriting, administration, logistics, repair, automated systems, and data-driven analytics to deliver an exceptional customer experience while preventing, detecting, and deterring fraud with automated tools and systems.

Dynamic Scrutiny (Analytics) Utilizes 7 distinct risk models to compute a score which determines the claim review process. The Dynamic Scrutiny Model conducts a detailed risk assessment of each claim to assign a score which determines the next actions required. Dynamic Fulfillment (Business Roles) Provides various methods to fulfill a claim based on the life-time value of a customer. System Dynamic Claims Management (DCM) processes are incorporated into our operational system to drive the entire claims process.

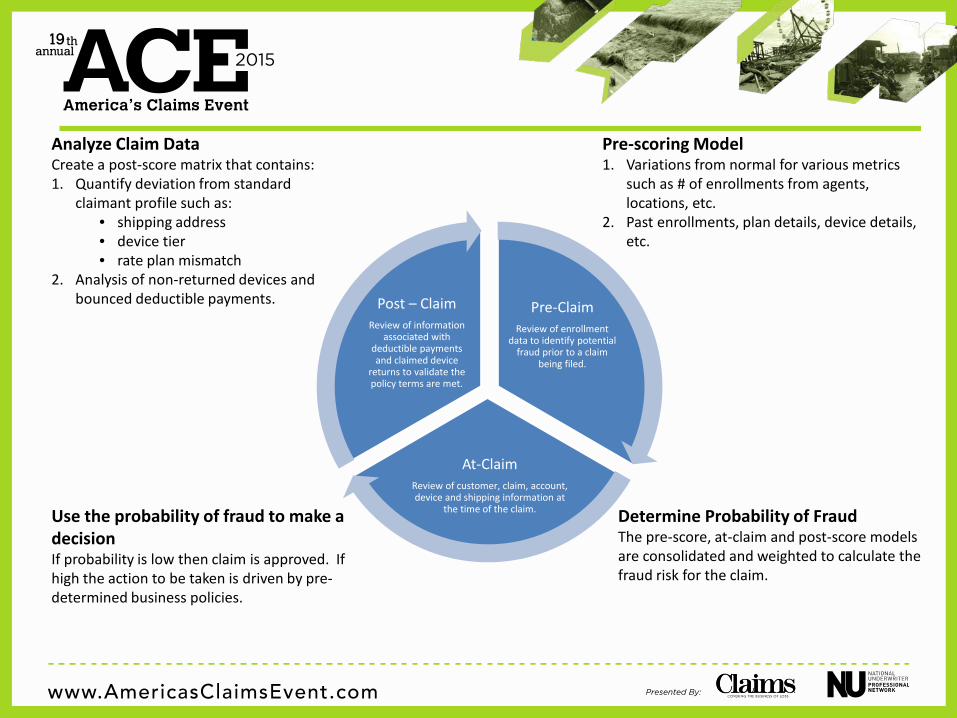

Models and Systems -

Pre-Claim Review of enrollment

data to identify potential fraud prior to a claim

being filed.

At-Claim Review of customer, claim, account, device and shipping information at

the time of the claim.

Post – Claim Review of information

associated with deductible payments and claimed device

returns to validate the policy terms are met.

Determine Probability of Fraud The pre-score, at-claim and post-score models are consolidated and weighted to calculate the fraud risk for the claim.

Analyze Claim Data Create a post-score matrix that contains: 1. Quantify deviation from standard

claimant profile such as: • shipping address • device tier • rate plan mismatch

2. Analysis of non-returned devices and bounced deductible payments.

Pre-scoring Model 1. Variations from normal for various metrics

such as # of enrollments from agents, locations, etc.

2. Past enrollments, plan details, device details, etc.

Use the probability of fraud to make a decision If probability is low then claim is approved. If high the action to be taken is driven by pre-determined business policies.

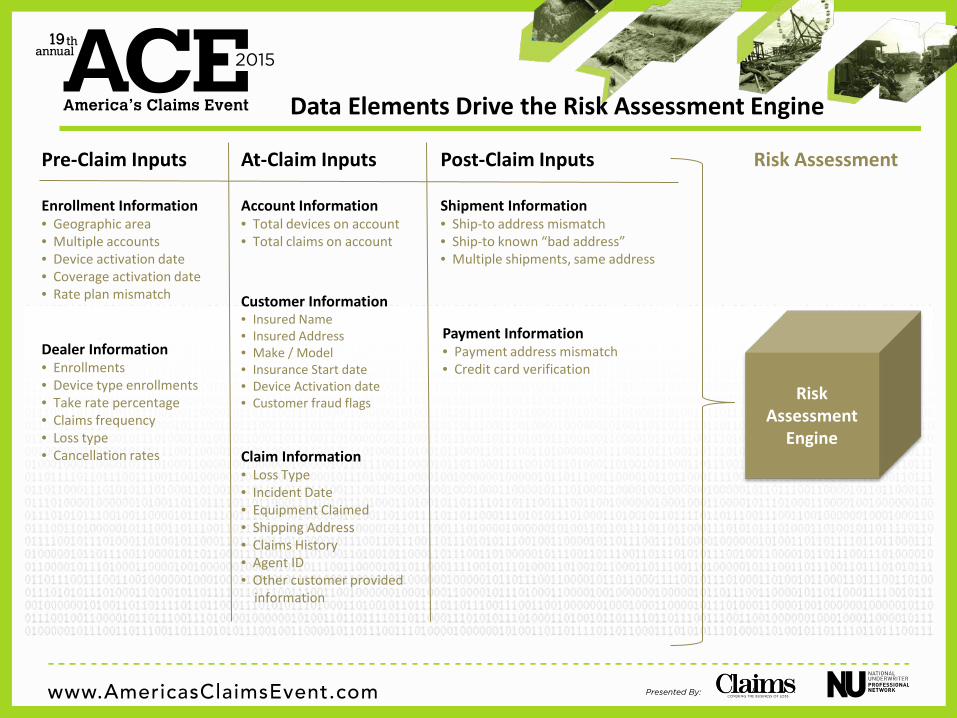

Customer Information • Insured Name • Insured Address • Make / Model • Insurance Start date • Device Activation date • Customer fraud flags

Claim Information • Loss Type • Incident Date • Equipment Claimed • Shipping Address • Claims History • Agent ID • Other customer provided information

Account Information • Total devices on account • Total claims on account

Pre-Claim Inputs At-Claim Inputs

Dealer Information • Enrollments • Device type enrollments • Take rate percentage • Claims frequency • Loss type • Cancellation rates

Enrollment Information • Geographic area • Multiple accounts • Device activation date • Coverage activation date • Rate plan mismatch

Risk Assessment Post-Claim Inputs

Payment Information • Payment address mismatch • Credit card verification

Shipment Information • Ship-to address mismatch • Ship-to known “bad address” • Multiple shipments, same address

Risk Assessment

Engine

Data Elements Drive the Risk Assessment Engine

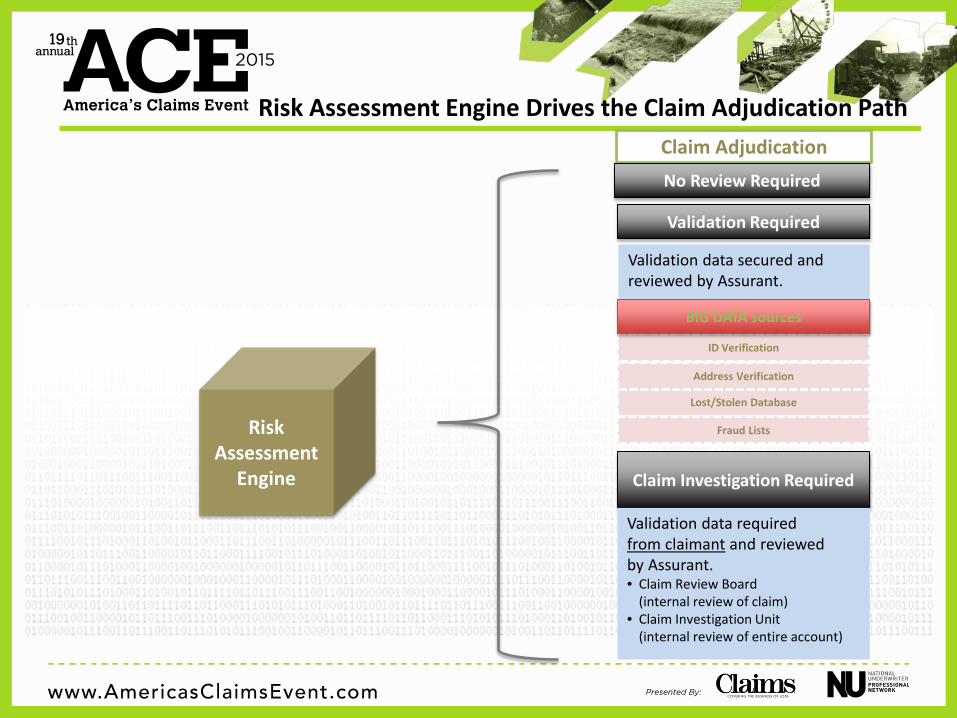

Validation data secured and reviewed by Assurant.

Claim Adjudication

Risk Assessment

Engine

No Review Required

Validation Required

Claim Investigation Required

Validation data required from claimant and reviewed by Assurant. • Claim Review Board (internal review of claim) • Claim Investigation Unit (internal review of entire account)

Lost/Stolen Database

Address Verification

Fraud Lists

ID Verification

BIG DATA sources

Risk Assessment Engine Drives the Claim Adjudication Path

Other Uses of Big Data “How do we validate the information provided by the customer during the claim interview is correct?”

• External address and identification databases. • External bad address and fraud lists.

“How do we predict the likelihood that a claim will result in a complaint to the DOI?”

• Use a web scraper for the claim files for key word matches to populate the Corrective and Preventive Action (CAPA) database.

• Use a web scraper on social media sites to collect customer comments.