9/17/2015 1 How Do Foreign Financial Actors Vote in Developing Democracies? Research Concepts,...

40

03/27/22 03/27/22 1 How Do Foreign Financial Actors Vote in Developing Democracies? Research Concepts, Frameworks, Evidence & Prospects Paul M. Vaaler John and Bruce Mooty Chair in Law & Business Department of Strategic Management & Entrepreneurship Carlson School of Management & Law School University of Minnesota SNIE Annual Conference ng Lecture Series day, May 21, 2015 se Institute of Scientific Studies se, Corsica, FRANCE Copyright © Paul M. Vaaler, 2015. All rights reserved.

-

Upload

letitia-golden -

Category

Documents

-

view

215 -

download

2

Transcript of 9/17/2015 1 How Do Foreign Financial Actors Vote in Developing Democracies? Research Concepts,...

04/19/2304/19/23 1

How Do Foreign Financial Actors Vote in Developing

Democracies?Research Concepts, Frameworks, Evidence & Prospects

Paul M. Vaaler

John and Bruce Mooty Chair in Law & BusinessDepartment of Strategic Management & Entrepreneurship

Carlson School of Management&

Law SchoolUniversity of Minnesota

14th ESNIE Annual ConferenceMorning Lecture SeriesThursday, May 21, 2015Cargèse Institute of Scientific StudiesCargèse, Corsica, FRANCE Copyright © Paul M. Vaaler, 2015. All rights reserved.

04/19/23 2

The Presentation in a Nutshell

Competitive Elections and Foreign Lending and Investment Have Become (Generally Positive) Facts of Life In Most of the Developing World, But We Lack Theories and Evidence to Guide Our Understanding About How They Are Related: In Business, Substantial Research on “Political Risk” But Not When Politics Are “Up for Grabs” at

Election Time In Political Economy, Substantial Research on Policy Manipulations Associated With Elections, But Not

For Their Impact on Foreign Financial Actors

We Can Guide that Understanding With Political Business Cycle (PBC) Theories and Empirical Methods: Theoretically, We Can Integrate Opportunistic and Partisan PBC Model Assumptions To Gain Novel

Insight on the Attractiveness of Countries for Foreign Lending and Investment During Elections Empirically, We Can Document Broad-Sample Evidence Measuring Variation in Election-Period

Lending and Investment Across A Broad Range of Foreign Financial Actors

There Are Rich Research Prospects for Newcomers…Like You: Explaining The Impact of Elections on New Foreign Financial Actors in New Regions Explaining the Impact of “Elections” on Foreign Financial Actors in Developing Non-Democracies Explaining the Impact of Foreign Financial Actors on Domestic Political Actors: Private Regulation

04/19/23

Brazil, January 2003:

A Peaceful Partisan Transfer of the Brazilian Presidency Under Civilian Rule…

√Lula: 61.3%Serra: 38.7%

The October 2002 Vote:

A Brazilian Vignette…

04/19/23 4

But Six Months Earlier in June 2002….

“RECOMMENDATION: WE CONTINUE TO RECOMMEND CLIENTS REDUCE EXPOSURE AHEAD OF THE ELECTION…The sovereign spread (or risk premium) on Brazilian USD debt gapped out from 1250 basis points (bp) on Monday (June 17) to 1700 bp by the close on Friday (June 21)…Bond investors are clearly worried about the outcome of the presidential elections in October. “

Excerpt from Credit Suisse Private Banking

Newsletter to Investors June 26, 2002

√Lula: 61.3%Serra: 38.7%

A Brazilian Vignette…

04/19/23 5

Russia, July 1996:

Rocking-and-Rolling Right-Wing Incumbent President Boris Yeltsin Heading to Electoral Victory…Finally

Dour and Defeated Left-Wing Challenger Gennady Zyuganov

√Yeltsin: 53.7%, Zyuganov: 40.4%

…And A Russian Vignette

04/19/23 6

Russia in the 1990s:

Foreign Lenders and the Composition of Bank Lending to Russia in the Run-Up and Aftermath of this Watershed Election…

.3.3

5.4

.45

.5%

Sho

rt-T

erm

Len

ding

(<

1 Y

ear)

1994 1995 1996 1997 1998Year

Foreign Loans to Russia

…And A Russian Vignette

04/19/23 7

New Class of (Re-)Democratizing Developing Countries Since the 1980s:

Electoral Politics Providing (Sometimes Starkly Contrasting) Choices to Domestic Voters and Incentives to Engage in Election-Period (Budgetary) Policy Manipulations With Potentially Substantial Effects

What These Vignettes Suggest

04/19/23 8

New Class of Foreign Financial Actors in the1980s:

Foreign Lenders and Investors Observing Election-Period Manipulations With a Lens Differing Substantially From Domestic Voters, And “Voting” (Lending, Investing) Differently During Election Periods

What These Vignettes Suggest

04/19/23 9

How Are They Related?

What AreThe Risks?

And Opportunities?

•For Foreign Financial Actors•For Local Politicians•For Us

What These Vignettes Suggest

04/19/23 10

“A Government Is Not Supported a Hundreth Part so Much by the Constant, Uniform, Quiet Prosperity of the Country as by those Damned Spurts which [British Prime Minister William] Pitt Used to Have Just in the Nick of Time.”

Henry Brougham on Pitt the Younger (1814) The “All-Time Hero of Political Business Cycles…”

Ken Rogoff on Richard Nixon (1988)

Political Business Cycle (“PBC”) Concepts

Economic Policies Follow the Electoral Calendar

Opportunistic (Expansionary) PBCs Partisan (Left-Right) PBCs Models and Evidence To Date

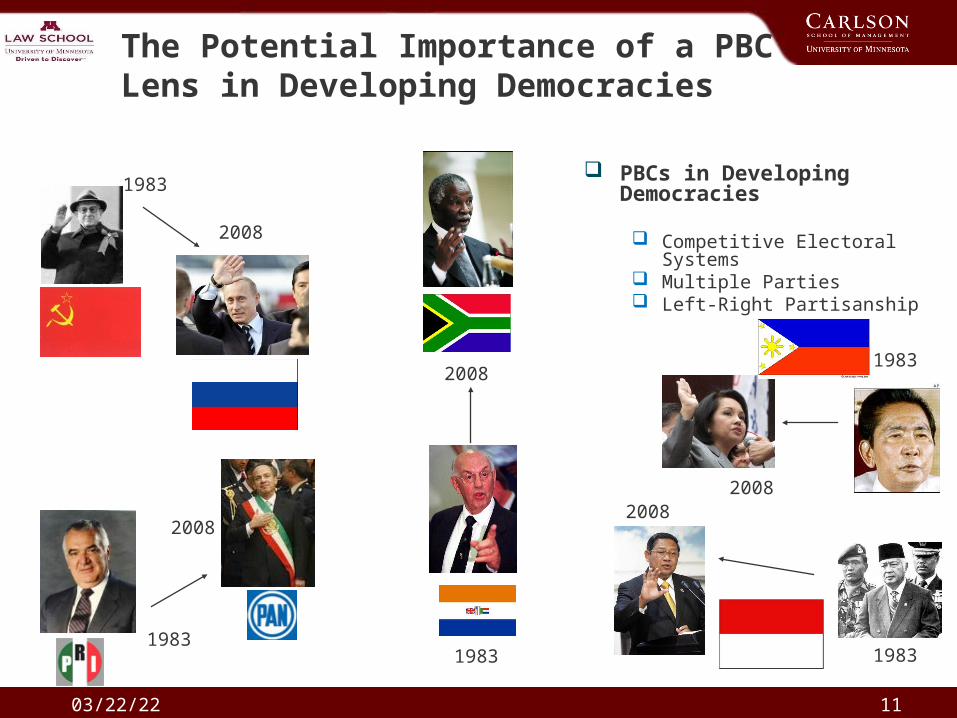

A Political Business Cycle Lens

04/19/23 11

1983

2008

1983

2008

1983

2008

1983

2008

1983

2008

PBCs in Developing Democracies

Competitive Electoral Systems

Multiple Parties Left-Right Partisanship

The Potential Importance of a PBC Lens in Developing Democracies

04/19/23 12

PBCs in Emerging Markets

Growing Economies Growing Financial Markets Growing Foreign Investor

Interest• Portfolio Investors• Direct Investors• Related Actors…Like

The Potential Importance of a PBC Lens in Developing Democracies

04/19/23 13

Incumbent Partisan Orientation Investor Electoral Expectation

Right-Wing Orientation

Left-Wing Orientation

Right-Wing Expected to Win ( 1)

(0,0) Right-Wing Base Case.

(++,--)Compared to Left-Wing Base Case and Left-Wing Close Call Case.

Closely Balanced Expectations ( 0.5)

(-,-) Compared to Right-Wing Base Case.

(+,-) Compared to Left-Wing Base Case.

Left-Wing Expected to Win ( 0)

(--,--)Compared to Right-Wing Base Case and Right-Wing Close Call Case.

(0,0) Left-Wing Base Case.

Conceptual Framework Development: Election-Period Confidence and Related Lending and Investment Behaviors Among Foreign Financial Actors Will Reflect Partisan and Opportunistic PBC Considerations If (0 ≤ ≤ 1) Represents the Likelihood of a Right-Wing Victory on Election Day, and (+)

Represents More ((-) Less) Confidence, Then Election Year Willingness to Lend and Invest Will Trend…

…For Right-Wing Incumbents, Negatively (Less Confidence) as the Likelihood Of Re-Election Decreases

…For Left-Wing Incumbents, Positively (More Confidence) as the Likelihood Of Re-Election Decreases (Partisan PBCs Dominate)

OR…For Left-Wing Incumbents, Negatively (Opportunistic PBCs Dominate)

Integrating PBC Lenses

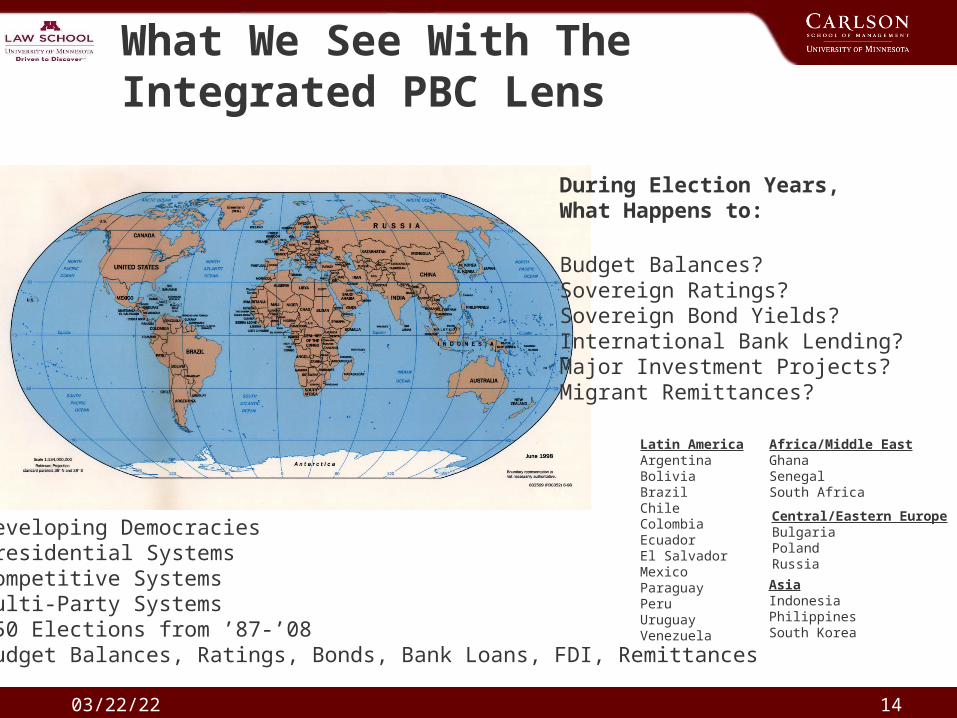

04/19/23 14

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorEl SalvadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastGhanaSenegalSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

•Developing Democracies•Presidential Systems•Competitive Systems•Multi-Party Systems•+50 Elections from ’87-’08•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

During Election Years,What Happens to:

Budget Balances?Sovereign Ratings?Sovereign Bond Yields?International Bank Lending?Major Investment Projects?Migrant Remittances?

What We See With The Integrated PBC Lens

04/19/23 15

“Standard & Poor’s today lowered its long-term local and foreign currencysovereign credit ratings on Brazil…given the worsening domesticdebt profile and heightening market concerns over political uncertaintiespresently and after the October presidential elections…”

Excerpt from Standard & Poor’s RatingsDirect, July 2, 2002

What We See With The Integrated PBC Lens: Budget Balances

04/19/23 16

-10

-50

5Y

ear-

to-Y

ear

Change in

Budget

Bala

nce

(%

of

GD

P)

-50 0 50Election Day Margin of Victory ( + ) or Defeat ( - ) ( % of Vote )

Right-Wing IncumbentElection Trend Line (x)

Left-Wing IncumbentElection Trend Line ()

1B

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•45 Elections from ’90-’04•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

Going Into Election Years,What Happens to:

Budget Balances?

Budget Balances As a % of GDP Go More Negative (Deficits) As the Likelihood of Right- or Left-Wing Incumbent Re-Election Diminishes.

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

What We See With The Integrated PBC Lens: Budget Balances

Bernhard, Chorzempa, Riley, & Vaaler (2015)

04/19/23 17

“Standard & Poor’s today lowered its long-term local and foreign currencysovereign credit ratings on Brazil…given the worsening domesticdebt profile and heightening market concerns over political uncertaintiespresently and after the October presidential elections…”

Excerpt from Standard & Poor’s RatingsDirect, July 2, 2002

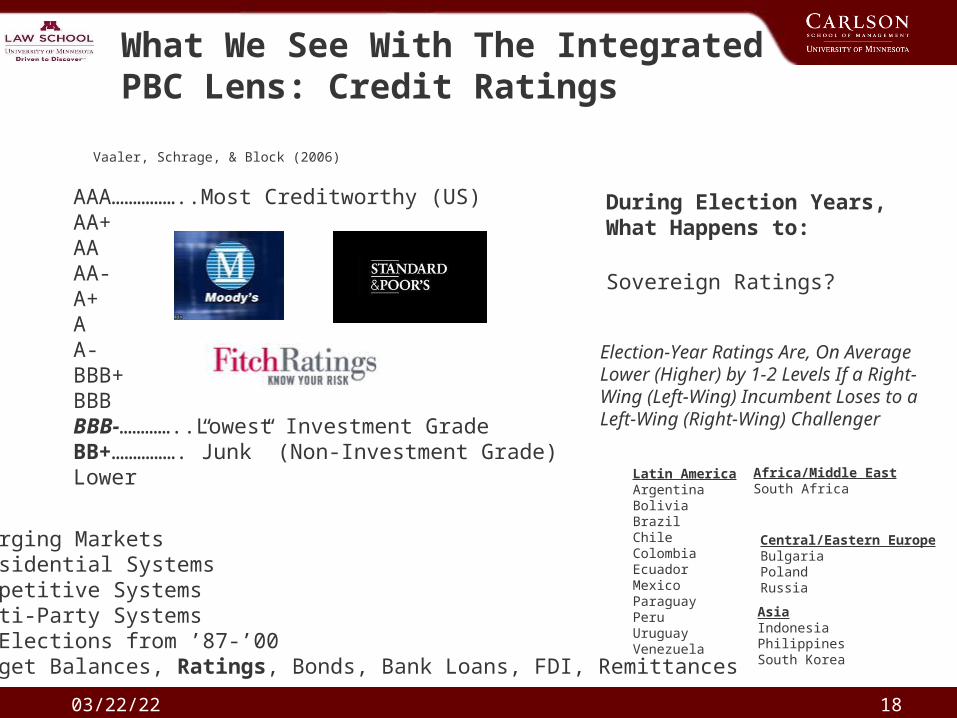

What We See With The Integrated PBC Lens: Credit Ratings

04/19/23 18

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

During Election Years,What Happens to:

Sovereign Ratings?

AAA……………..Most Creditworthy (US)AA+AAAA-A+AA-BBB+BBBBBB-…………..Lowest Investment GradeBB+…………….”Junk” (Non-Investment Grade)Lower

Election-Year Ratings Are, On Average Lower (Higher) by 1-2 Levels If a Right-Wing (Left-Wing) Incumbent Loses to a Left-Wing (Right-Wing) Challenger

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•36 Elections from ’87-’00•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

What We See With The Integrated PBC Lens: Credit RatingsVaaler, Schrage, & Block (2006)

04/19/23 19

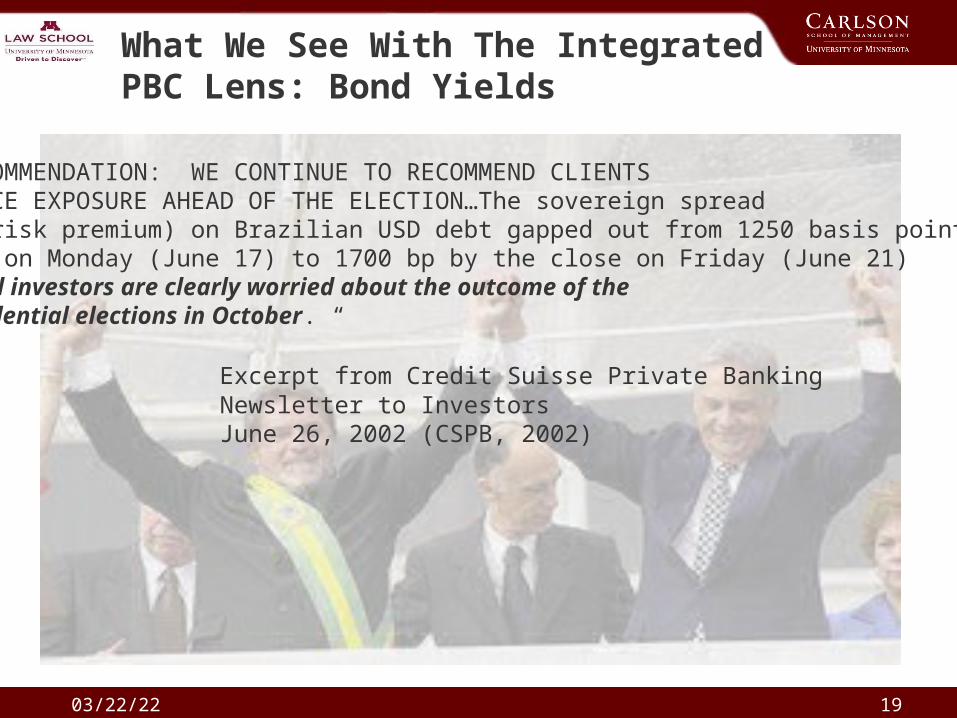

“RECOMMENDATION: WE CONTINUE TO RECOMMEND CLIENTS REDUCE EXPOSURE AHEAD OF THE ELECTION…The sovereign spread (or risk premium) on Brazilian USD debt gapped out from 1250 basis points (bp) on Monday (June 17) to 1700 bp by the close on Friday (June 21)…Bond investors are clearly worried about the outcome of the presidential elections in October. “

Excerpt from Credit Suisse Private Banking Newsletter to Investors June 26, 2002 (CSPB, 2002)

What We See With The Integrated PBC Lens: Bond Yields

04/19/23 20

Latin AmericaArgentinaBrazilChileColombiaMexicoPeruUruguayVenezuela

Central/Eastern EuropeBulgariaPolandRussia

AsiaPhilippines

During Election Years,What Happens to:

Sovereign Bond Yields?

Argentina Presidential Election May 14, 1995: Sovereign Bond Yields and Relative Spreads

10%

15%

20%

25%

30%

35%

15 - Nov - 94 15 - Dec - 94 15 - Jan - 95 15 - Feb - 95 15 - Mar - 95 15 - Apr - 95 15 - May - 95 15 - Jun - 95 15 - Jul - 95 15 - Aug - 95 15 - Sep - 95 15 - Oct - 95 15 - Nov - 95 0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Domestic Yield, Argentina (Left Y - Axis) Relative Spreads (Right Y - Axis) Predicted Slope of Relative Spreads

90 days

Election Day

Argentina: Right, D High Slope: - 0.00139 p - value < 0.01

Pre-Election Bond Yields Increase from 180-90 Days Before Election, then Decrease (Stay Steady) As Likelihood of Right-Wing Candidate Victory Increases

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•19 Elections from ’94-’00•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

What We See With The Integrated PBC Lens: Bond Yields

04/19/23 21

“We lost credit lines equal to 5% of our [GDP]…The [Brazilian presidential] elections lurked behind it all.”

BCB President Henrique MeireillesDescribing International Bank Lending to Brazil in 2002Financial Times, May 5, 2004

What We See With The Integrated PBC Lens: Bank Lending

04/19/23 22

During Election Years,What Happens to:

International Bank Lending?

Lending As a % of GDP Decreases (As the Likelihood of Right-Wing Incumbent Re-Election Diminishes.

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•45 Elections from ’90-’04•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

Bernhard, Chorzempa, Riley, & Vaaler (2015)

What We See With The Integrated PBC Lens: Bank Lending

04/19/23 23

“We are putting the Rio (hydro-electric power) project on hold until current political uncertainties get sorted out…”

Excerpt from Project Investment, August 23, 2002

What We See With The Integrated PBC Lens: FDI

04/19/23 24

During Election Years,What Happens to:

Major Investment Projects?

The Number of Major Investment Projects Announced Decreases (Increases) As the Likelihood of Right-Wing (Left-Wing) Incumbent Re-Election Diminishes

-50

51

01

5D

iffe

ren

ce i

n N

um

ber

of

Pro

ject

s A

nno

unce

d A

nnu

ally

-50 0 50 100Election Day Margin of Victory ( + ) or Defeat ( - )

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

What We See With The Integrated PBC Lens: FDI

Vaaler (2008)

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•36 Elections from ’87-’00•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

04/19/23 25

“For the 2002 presidential election, registration increased to 69,937 electors—almost 45 per cent more than four years before. The presidential election had to be decided in a second round of voting; in the first round, 38,618 external electors voted (55.5 per cent) and in the second round 36,043 (51.7 per cent).”

Excerpt from Administration and Cost of Elections (“ACE”) ProjectDescribing Rates of Voting in 2002 By Nearly 1,000,000 Brazilian Migrants Worldwide…Remitting $2.2 Billion in 2002

What We See With The Integrated PBC Lens: Remittances

04/19/23 26

What We See With The Integrated PBC Lens: Remittances

050

100

150

Ann

ual R

emitt

ance

s (P

er C

apita

)

-50 0 50Election Day Margin of Victory ( + ) or Defeat ( - ) ( % of Vote )

Left-Wing Incumbent Trend Line

Right-Wing Incumbent Trend Line

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•42 Elections from ’00-’08•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

During Election Years,What Happens to:

Migrant Remittances?

Remittances Per Capita (of Home-Country Population) Peak In Election Years Where the Outcomes Are Close, Indicative of Transnational Political Activation Cues Rather than More Conventional PBC Considerations

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorEl SalvadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastGhanaSenegalSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

Vaaler (2015)

04/19/23 27

PBC Considerations Matter in Developing Democracies Local Politicians Are

Given to Budgetary Spending Sprees to Gain Domestic Votes at Election Time

Most Foreign Financial Actors Also “Vote” Consistent with Integrated PBC Lens

Partisan PBC Considerations Are Especially Important in Such “Voting”

What We See With The Integrated PBC Lens: Overall

04/19/23 2828

What About Foreign Financial Actors in Established Democracies of the Industrialized World?

Electoral Transparency, Voter Experience (and Wariness)?

Who Are “Foreign” Actors

Surprises, Lags May Matter More

Research Extensions: OECD States

04/19/23 29

What About Foreign Financial Actors in When These Democracies Were Establishing?

Cross-Country and Within-Country (Over Time) Variation in Percentage of Enfranchised

Maybe Foreign Financial Actors Fear PBCs Less When the Enfranchised Are Fewer, More Privileged, Domestic Elites

Research Extensions: Historically

3-6%

18-22%

6-9%

0-2%

04/19/23 30

“Shanghai Gang”1992-2002

“Communist Youth League”2002-2012

“?”2012-…

Research Extensions: One-Party States

What About Foreign Financial Actors in During “Elections” in Non-Democracies?

Even Stalin Held Plebiscites

Single Parties Often Have Competition Among Factions

Incumbent Government Factions Have PBC Incentives When Party Leadership Is Up for Renewal

Mechanisms for Voting and “Voting” May Differ

04/19/23 31

Research Extensions: Reverse Relationships

If you think deficit-reduction is being driven by John Boehner or Harry Reid, think again. The biggest driver right now is Standard & Poor’s.

Robert Reich (2011)

There are two superpowers in the world today in my opinion. There's the United States and there's Moody's Bond Rating Service. The United States can destroy you by dropping bombs, and Moody's can destroy you by downgrading your bonds. And believe me, it's not clear sometimes who's more powerful.

Tom Friedman(1996)

AAA……………..Most CreditworthyAA+AAAA-A+AA-BBB+BBBBBB-…………..Lowest Investment GradeBB+…………….”Junk” (Non-Investment Grade)Lower

04/19/23 32

Research Extensions: Reverse Relationships

Research Proposition: Private, Transnational Agencies “Regulate” National Politicians and Their PBC Tendencies:

– PBCs Meet Transnational Regimes, Both Affecting Foreign Financial Actors…and Local PoliticiansPBCs Meet Transnational Regimes, Both Affecting Foreign Financial Actors…and Local Politicians

– Regime TheoryRegime Theory: Behavior By States In International Financial System Is Governed by Agency Norms : Behavior By States In International Financial System Is Governed by Agency Norms Favoring Budgetary Rectitude, That Is, Smaller Budget Deficits and Borrowing Limited to Funding Favoring Budgetary Rectitude, That Is, Smaller Budget Deficits and Borrowing Limited to Funding Projects That Promote Long-Term Economic Development and Enhanced Creditworthiness Projects That Promote Long-Term Economic Development and Enhanced Creditworthiness

– Implications for Agency Ratings and State Budget BalancesImplications for Agency Ratings and State Budget Balances : H1) Higher Ratings Are Associated With : H1) Higher Ratings Are Associated With Larger Budget Deficits (to Fund Projects Promoting Long-Term Economic Development); H2) Larger Budget Deficits (to Fund Projects Promoting Long-Term Economic Development); H2) Election-Years Are Associated With Larger Budget Deficits (to Fund Projects Promoting Short-Term Election-Years Are Associated With Larger Budget Deficits (to Fund Projects Promoting Short-Term Economic Growth and Re-Election); and H3) Higher Ratings Are Associated With Smaller Budget Economic Growth and Re-Election); and H3) Higher Ratings Are Associated With Smaller Budget Deficits During Election Years (Because No Additional Borrowing Then Funds Meritorious Projects)Deficits During Election Years (Because No Additional Borrowing Then Funds Meritorious Projects)

Completing the Sorely Needed Suramadu BridgeConnecting Java and Madura, Indonesia (2009)

Increasing “Social” Spending From Oil andGas Revenues In Anticipation of 2012 (2011)

In Non-Election Years,Ratings Permit More Negative Budget But…Balances For “Good”Reasons

In Election Years, Opportunistic PoliticiansExercise Are ConstrainedBy Threat of DowngradeFrom Spending Sprees

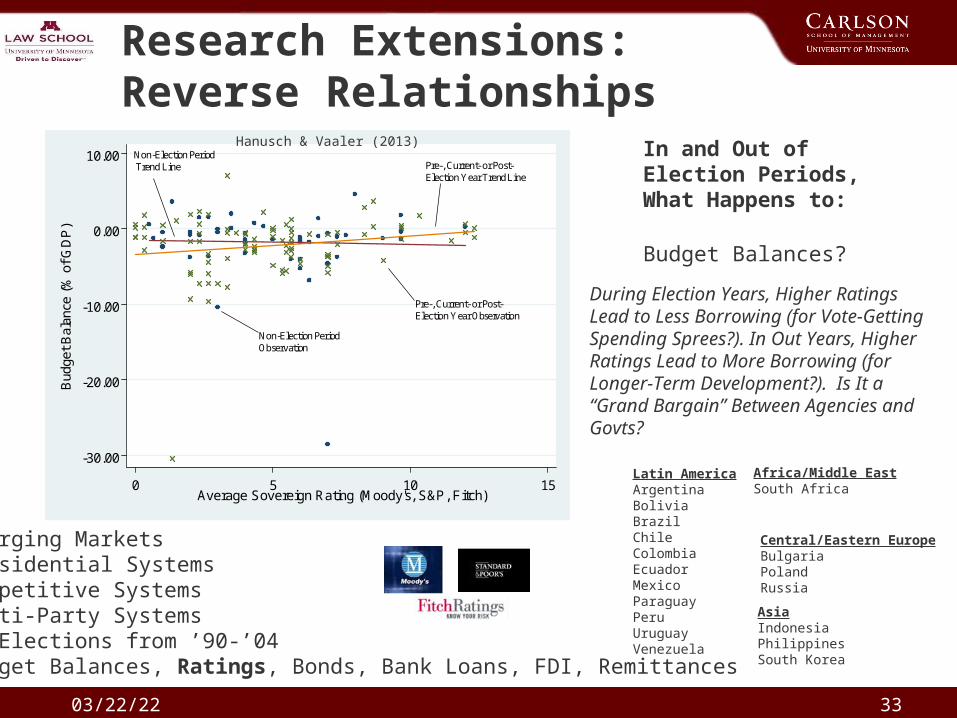

04/19/23 33

Research Extensions: Reverse Relationships

-30.00

-20.00

-10.00

0.00

10.00

Bud

get

Bal

ance

(%

of

GD

P)

0 5 10 15Average Sovereign Rating (Moody's, S&P, Fitch)

Pre-, Current- or Post-Election Year Observation

Non-Election Period Observation

Pre-, Current- or Post-Election Year Trend Line

Non-Election PeriodTrend Line

Latin AmericaArgentinaBoliviaBrazilChileColombiaEcuadorMexicoParaguayPeruUruguayVenezuela

Africa/Middle EastSouth Africa

Central/Eastern EuropeBulgariaPolandRussia

AsiaIndonesiaPhilippinesSouth Korea

In and Out of Election Periods,What Happens to:

Budget Balances?

During Election Years, Higher Ratings Lead to Less Borrowing (for Vote-Getting Spending Sprees?). In Out Years, Higher Ratings Lead to More Borrowing (for Longer-Term Development?). Is It a “Grand Bargain” Between Agencies and Govts?

•Emerging Markets•Presidential Systems•Competitive Systems•Multi-Party Systems•32 Elections from ’90-’04•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

Hanusch & Vaaler (2013)

04/19/23 34

Moody's downgrades Minneapolis' credit rating (Star Tribune, July 30, 2013)

“Moody's Investors Service downgraded Minneapolis's credit rating Monday night, delivering a blow to one of Mayor R.T. Rybak's signature achievements.”

S&P Downgrade: Ex-Obama Adviser Christina Romer Says U.S. “Pretty Darn F**ked” (Huffington Post,August 6, 2011)

"If France loses its AAA, I'm dead…“Le Canard Enchaine, October 21, 2011

How Do Agencies Ratings How Do Agencies Ratings Matter for Politicians Here?Matter for Politicians Here?

– Threatened Downgrades Threatened Downgrades Discipline Politicians from Discipline Politicians from Borrowing With Threat of Borrowing With Threat of Higher Future Borrowing Higher Future Borrowing CostsCosts

– Threatened Downgrades Threatened Downgrades Discipline Politicians from Discipline Politicians from Borrowing Lest They Be Borrowing Lest They Be Identified as “Bad Economic Identified as “Bad Economic Stewards” in the PresentStewards” in the Present

– Both Matter at Election TimeBoth Matter at Election Time

Research Extensions: Reverse Relationships

04/19/23 35

If “On Negative Watch” (for Downgrade)Then No Additional Election-Year Borrowing

…If Not “On Negative On Watch” Then Election-Year Borrowing Increases

-1-.

50

.51

Non-negative outlook Negative outlook

Me

an

ann

ua

l diff

ere

nce

in th

e p

rim

ary

bu

dg

et b

ala

nce

Likelihood of LosingAn Election AfterDowngrade IncreasesBy About 15 PercentagePoints If Downgraded YearBefore Re-Election

Research Extensions: Reverse Relationships

•63 Countries Globally•Presidential and Parliamentary Systems•Competitive Systems•Multi-Party Systems•111 Elections from ’01-’11•Budget Balances, Ratings, Bonds, Bank Loans, FDI, Remittances

Hanusch & Vaaler (2015)

52% 48%

04/19/23 36

Strategic Managers Should Look Past Party Names and Pins to Talk to Politicians In and Out of Power

Local Politicians Should Learn How to Talk “Finance,” How to Find Credible Representatives to Court Foreign “Voters”

Developing A Common Language, Norms, Meeting Places

Don’t Expect Help From the Embassy or Consulate

“It worries me that people think this [2010] election doesn’t matter. People are getting carried away.” Jim O’Neill, Chief Economist, Goldman Sachs

Practice and Policy Implications for Foreign Actors and Local Politicians

04/19/23 37

Some Opportunities: Arbitrage Opportunity for Bond Investors Temporary Domestic Credit Crunch

Hurting (Helping) Domestic (Foreign) Firms Electorally-Induced “Panic” in FDI Project

Terms When There Is Right-To-Left Swing

Argentina Presidential Election May 14, 1995: Sovereign Bond Yields and Relative Spreads

10%

15%

20%

25%

30%

35%

15 -Nov -94 15 -Dec -94 15 -Jan -95 15 -Feb -95 15 -Mar -95 15 -Apr -95 15 -May -95 15 - Jun -95 15 -Jul -95 15 -Aug -95 15 -Sep -95 15 -Oct -95 15 -Nov -95 0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Domestic Yield, Argentina (Left Y -Axis) Relative Spreads (Right Y -Axis) Predicted Slope of Relative Spreads

90 days

Election Day

Argentina: Right, D High Slope: -0.00139 p -value < 0.01

Buy into the Bubble

Sell out of the Bubble

Practice and Policy Implications for Foreign Actors and Local Politicians

04/19/23 38

A Closing Benediction

Politicians Then and Now Have Incentives to Implement Election-Year Economic Policies Consistent with PBC Considerations. Foreign Financial Actors Will Respond…And Sometimes Push Back on Politicians.

You Have the Opportunity to Explore These Relationships in Depth and in Real Time Around a World With Longer-Term Trends of Political and Economic Openness…With the Occasional Step Backwards.

That Exploration Will Give You Academic Career Choices –Economics, Political Science, Public Policy, Business Faculty Appointments– and Let You Weigh on Debates That Cross These Boundaries.

Very ESNIE-Esque

Make a Difference!

04/19/23 39

How Do Foreign Financial Actors Vote in Developing Democracies?

Research Concepts, Frameworks, Evidence & Prospects

Paul M. Vaaler

John and Bruce Mooty Chair in Law & BusinessDepartment of Strategic Management & Entrepreneurship

Carlson School of Management&

Law SchoolUniversity of Minnesota

Copyright © Paul M. Vaaler, 2015. All rights reserved.

Thanks

04/19/23 40

References Bernhard, W., Riley, S. & Vaaler, P. 2015. How Do International Bankers Vote in Developing Democracies?

Working Paper. University of Minnesota, Minneapolis, MN.

Block, S. & Vaaler, P. 2004. The Price of Democracy: Sovereign Risk Ratings, Bond Spreads and Political Business Cycles in Developing Countries. Journal of International Money and Finance, 23: 917-946.

Hanusch, M. & Vaaler, P. 2013. Credit Rating Agencies and Elections in Emerging Democracies: Guardians of Fiscal Discipline? Economics Letters, 119: 251-254.

Hanusch, M. & Vaaler, P. 2015. How Do Credit Rating Agencies Moderate Political Business Cycles? Working Paper. University of Minnesota, Minneapolis, MN.

Snowden, B. & Vane, H. 2005. Modern Macroeconomics: Its Origins, Development and Current State. Edward Elgar: Cheltenham, UK, 517-578 (“Chapter 10: The New Political Macroeconomics”).

Vaaler, P. 2008. How Do MNCs Vote in Developing Country Elections? Academy of Management Journal, 51: 21-43.

Vaaler, P. 2015. Elections and Migrant Remittances: New Evidence on the Insurance-Investment Debate. Working Paper. University of Minnesota, Minneapolis, MN.

Vaaler, P., Schrage, B., & Block, S. 2005. Counting the Investor Vote: Political Business Cycle Effects on Sovereign Bond Spreads in Developing Countries. Journal of International Business Studies, 36: 62-88.

Vaaler, P. Schrage, B. & Block, S. 2006. Elections, Opportunism, Partisanship and Sovereign Ratings in Developing Countries. Review of Development Economics, 10: 154-170.

Sources for this Presentation