9 Strategies to Raise Your Credit Score to 720 or Higher!!!

43

9 Strategies to RAISE Your Credit Score to 720 or HIGHER! Welcome To … Understanding Credit Scores! And …

-

Upload

gabriel-e-brown -

Category

Business

-

view

77 -

download

0

Transcript of 9 Strategies to Raise Your Credit Score to 720 or Higher!!!

9 Strategies to RAISE Your Credit Score

to 720 or HIGHER!

Welcome To …

Understanding Credit Scores! And …

Gabriel Brown is easily one of the nation’s leading credit score experts! He has years of experience as the CEO of Vivix Credit Solutions, a national recognized leader in the credit repair industry.

Gabriel Brown: “From Homeless to Black Cards!”

Started in 2006, Vivix Credit Solutions has successfully served THOUSANDS of credit repair clients and Vivix has recorded over 950,000 deletions from the credit reports of those clients.

For two and one-half years, Mr. Brown co-hosted a national talk radio show on KLAV called “Help Your Life!”

Mr. Brown’s rags to riches story is a tale of desperation to inspiration and as proof of his successful journey, he’ll be happy to send you his e-book “From Homeless to Black Cards” that tells of his climb out of his dire credit circumstances to his present day situation of dream come true lifestyle.

Through Vivix, Gabriel Brown’s passion and mission is to give millions of people a fresh credit start -- “a second chance at the credit dance!”

Vivix Credit Solutions is licensed and bonded by the Nevada Department of Business and Industry, accredited with the Better Business Bureau, member of Las Vegas Chamber of Commerce and founded in 2006! Member of the National Association of Credit Service Organizations (NASCO).

Vivix Credit Solutions: A Name You Can Trust!

Vivix Credit Solutions has successfully served THOUSANDS of credit repair clients and Vivix has recorded over 950,000 deletions from the credit reports of those clients thereby raising their credit scores!

All counselors are FICO 8 Certified Professionals!

100% Customer Satisfaction Guaranteed!

Vivix Credit Solutions has four business licenses and a NAIC Code: 523930 and a SIC Code: 628203 as an Investment Advice and Financial Advisory service!

Free Consultations: 702-434-4414

You’re thinking: What’s In It For Me?”

After this presentation, you’re more likely to get the home, mortgage, car, insurance rates, and lifestyle of your DREAMS! Now and for the FUTURE! That’s because higher FICO scores can lower monthly mortgage, insurance and credit card rates so much that a consumer has HUNDREDS of extra dollars monthly for investment accounts!

Credit Scores & Credit Reports:More Reasons to Care!

The FIRST problem is that most Americans are unwittingly being VICTIMIZED

(legally pick pocketed) because:

• They don’t understand how the credit reporting system works,

• How their credit is calculated, • The important ways in which credit reports and

scores can affect their financial well-being, • Or what they can do about it.

Credit Scores & Credit Reports:More Reasons to Care!

The SECOND problem is the potential for inaccuracy in the credit report data that are used to calculate credit scores.

“Is your credit report accurate?”

Credit Scores & Credit Reports:More Reasons to Care!

The THIRD problem is that IDENTITY THEFT, considered the nation’s fastest growing crime, poses a direct threat to the

accuracy and integrity of data in the credit reporting system.

Identity thieves typically steal an individual’s identifier’s, such as social security number, name,

address, date of birth, mother’s maiden name, and then use them to get credit in that person’s name.

The innocent victim’s credit report is polluted by highly negative info!

Cost of Bad Credit!

TWO EXAMPLES

AUTO LOAN: $20,000 car paid over 60 months will pay an

ADDITIONAL $8,593 for the car!

HOME MORTGAGE: $100,000 mortgage paid over 30 years will pay an

ADDITIONAL $130,000 for the SAME home! Even if you are in that mortgage for only 2-5 years,

it costs you more because of the rule of 78s!

CREDIT SCORINGBasics & History

What Is a Credit Score?

For most models, the higher the score, the better the risk.

A credit score is a three digit number that reflects your credit worthiness AT A GIVEN POINT IN TIME, it’s a snap shot!

The credit score is based on data in your credit report.

In a recent nationwide survey, 97% of consumers

could NOT name all 3 credit reporting agencies.

If you’re a mortgage lender, realtor or insurance professional, you have an opportunity to be of greater service by educating the consumer, adding value to your services and increasing customer loyalty.

A healthy blood pressure reading is important to your body and having a good FICO score is important to your financial health!

History of Credit Scoring

FICO = Fair Isaac Company Established in 1958 to Create a Scoring System

to Effectively Forecast Probable Repayment of Debts Strictly Marketed to the Banking Industry Held in Confidence by Lending Institutions Never Meant to be Seen or Understood by Average

Consumer 1994: Distributed Software to Agencies

CREDIT SCORESWhat Do They Mean?

• Predicts the statistical chance of a consumer becoming 90 days late or more on a particular loan obligation

• Each score is specific for each bureau

• The higher the scores the less the odds of default

• The scores are generated by analyzing the information contained in the consumer’s credit report at THAT particular moment in time

What Do The Scores Mean? (continued)

FICO Score Range by Credit Bureau

Equifax Score Range:

300 to 850

Experian Score Range:300 to 900

TransUnion Score Range:

336 to 843

Like the secret KFC recipe, the precise formulas that are used for calculating the

various scores are well-guarded trade secrets.

Consumer Default: What are the Odds?

QUALIFYING

Odds on Consumers Defaulting When 90 Days Late:

Scores OddsBelow 500 …………… FORGET ABOUT IT!500 to 619 …………… 8 to 1620 to 659 …………… 26 to 1660 to 679 …………… 38 to 1680 to 699 …………… 55 to 1700 to 719 …………… 123 to 1720 to 759 …………… 323 to 1760 to 799 …………… 597 to 1Above 800 …………… 1292 to 1

What are the determining factors?

CREDIT SCORING

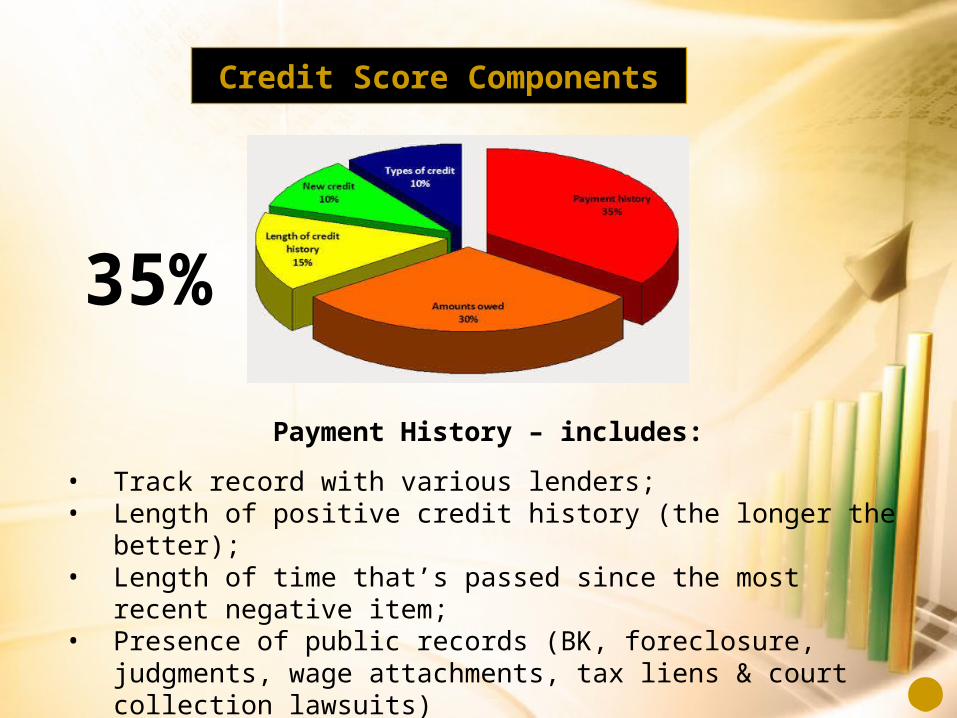

Credit Score Components

Credit Score Components

Payment History – includes:• Track record with various lenders; • Length of positive credit history (the longer the better); • Length of time that’s passed since the most recent negative item; • Presence of public records (BK, foreclosure, judgments, wage

attachments, tax liens & court collection lawsuits)

35%

Credit Score Components

Amount Owed (extent of indebtedness) –

includes:• Too many cards can lower a score; • Ratio of credit balance to credit limit; • The total amount owed on ALL accounts; • How much is owed on EACH type of account? • How much of a mortgage or other installment

loans are paid off?

30%

Credit Score Components

Length of Credit History (the longer the better) – includes:

• Overall length of credit history (in general); • How long have SPECIFIC credit accounts been established? • How long has it been since you USED certain accounts?

15%

Credit Score Components

How Much NEW Credit? – includes:• How many new accounts recently, especially credit cards? • How LONG has it been since you opened a new account? • How many RECENT requests for credit have you made, as

indicated by “inquiries” to the credit bureaus?• Length of time since credit report inquiries were made to lenders• Whether you have a good RECENT credit history following past

payment problems

10%

Credit Score Components

Type of Credit – includes:• Do you have a “healthy mix” of installment

(mortgages & loans) and revolving credit (credit cards)?• It’s not entirely clear what’s healthy and what’s not!• Loans from banks are considered positive, while

finance companies are not!

10%

Impact of Negative Items

• 1st Year = 93%

• 1-2 years = 60%

• 2-3 Years = 44%

• 3-4 Years = 33%

• Older than 5 Years = 22%

Time heals all wounds, but it still leaves a scar!

• Your credit scores are based entirely on the information in your credit reports on file at the big three credit bureaus: Equifax, Experian and TransUnion.

• If the information is wrong, your credit scores could suffer. Go to YouTube - 40 Million Mistakes: Is your credit report accurate? (posted by CBSnewsonline)

• You can get your reports once a year for free from the government run AnnualCreditReport.com; you can buy subsequent copies directly from the bureaus or from myFICO.com for about $20 EACH or call us and we’ll tell you how to get all three for $1. Just give us a call.

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

Strategy #1: Patrol your credit reports.

• Accounts that aren't yours.

• Reports of late payments when you paid on time.

• Bankruptcies older than 10 years or accounts that were wiped out in bankruptcy but are listed as still due.

You can dispute anyserious errors, such as:

• Other negative information that's older than seven years. (The seven year clock typically starts 180 days after the account first went delinquent.)

Even though you CAN dispute yourself, you probably won’t get satisfaction. Again, go to YouTube video referenced on previous slide!

• Retail cards and gas cards can help you build your credit history initially, but to get your scores into the 700 plus territory you'll want at least one traditional card: a Visa, a MasterCard, a Discover or an American Express.

Strategy #2: Get a Major Credit Card

• If you can't qualify for a regular card, consider a secured version, for which you make a deposit with an issuing bank. You can find offers at CardRatings.com, CreditCards.com, LowCards.com and Index Credit Cards, among other sites.

• Just make sure the card reports to all three bureaus, and try to get a card that converts to a regular credit card after 12 to 18 months of on-time payments.

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Credit scores are extraordinarily sensitive to whether you pay your bills on time, so don't let travel, a busy schedule or a simple brain cramp trash your scores.

Strategy #3: Arrange automatic payments for every card or loan.

• Most lenders will let you set up automatic payments that take an amount you specify -- the minimum payment, a set dollar amount or the full balance -- every month from your checking account.

• You should examine and pay your credit cards yourself, but as a back-up plan, set-up an automatic minimum payment (that way you still pay some interest so the “system” rewards you with a better score.

9 Strategies To Raise Your Credit Score to 720 or

HIGHER!

• Yes, your insurance should’ve covered that bill; no, you shouldn't have to pay for a broadband connection that doesn't work.

Strategy #4: Don't let disputes go to collections

• But if you let a commonplace problem like these escalate, your account will be turned over to collections and become a big black mark on your credit reports.

• Pay under protest and get your revenge in small claims court. (Don't get sued yourself, though: lawsuits and judgments are also major stains on your credit reports.)

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• More than a third of your FICO score depends on how much of your available credit you're using … your so-called “credit utilization ratio.”

Strategy #5: Pay down and spread out your debt.

• The FICO formula likes to see big gaps between your balances (whether you pay them off each month or not) and your limits, especially on credit cards. (You're rewarded for paying down installment debt, such as mortgages and auto loans, but your scores improve much more dramatically when you pay down revolving debt such as credit cards.)

• In short, it's better to have small balances on several cards than a big balance on one card.

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• You have to worry about your credit utilization ratio EVEN if you pay your balances in full each month.

Strategy #6: Make sure your “Paid in Full”

balance reports that way!

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Many consumers like to use credit cards to earn rewards and air miles and then automatically pay off the balance every month when the statement closes. You’d think that’s a great way to responsibly manage your credit, but if you’re thinking your lender is reporting a $0 balance every month, you might be wrong and it’s hurting you!

Strategy #6: Make sure your “Paid in Full”

balance reports that way!

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Lenders typically report your account performance to the credit bureaus once a month – but NOT necessarily at the time when you pay your bill.

• Consider this: by the 15th of the month, you’ve used your credit card to make $500 worth of purchases on a $1,000 limit card .......

Strategy #6: Make sure your “Paid in Full”

balance reports that way!

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• You have automatic payments set up to pay the balance in full on the closing date, but your credit card company reports your account information to the bureaus on the 20th of every month. That means the $500 balance STILL shows up on your credit report — NOT the $0 balance!

• So for purposes of calculating your credit utilization ratio, a reported balance of $500 on a $1,000 limit card makes your credit utilization ratio 50% which looks really, REALLY bad even though you paid off the balance in full. (You never want to be above 30%.) If your credit utilization is high every month and it’s reported to the bureaus, your FICO Score will likely decrease.

Strategy #6: Make sure your “Paid in Full”

balance reports that way!

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Your best option is to avoid using too much credit. If you’re really interested in having a $0 balance reported, contact your lender and see if you can find out when they report account data to the credit bureaus.

• Alternatively, if you sign up for credit monitoring, you’ll be alerted when this data is reported and thus be able to determine an approximate reporting date (just be sure to consider tip #1 mentioned earlier). Depending on the lender, you may be able to set up your automatic payments to process on a date BEFORE the balance is reported to the credit bureaus.

• The less of your available credit you use, the more FICO rewards you.

Strategy #7: Shoot for 10%

• Keeping your credit utilization below 30% on your cards is good; getting it below 10% is even BETTER.

• If you regularly use more, ask for a higher limit or spread out your charges on more than one card or make two payments every month -- one just before your monthly statement closing date to lower the balance reported to the credit bureaus and a second one just before the due date to avoid late fees.

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Overloading your cards is a bad thing for your scores, but so is not using them at all.

Strategy #8: Don’t let your cards gather dust

• The scoring formula prefers to see accounts that are being actively used rather than sitting on a shelf.

• Even a little activity is better than no activity and a little interest is better than no interest. So “use it or you’ll lose it.”

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• Credit card issuers are reducing limits right and left. In fact, one banking analyst noted that at the end of 2010, risk-averse companies had slashed in half the $5 trillion in credit limits that existed before the financial crisis.

Strategy #9: Push back against lower limits

• This might have been awful news for your credit scores. That’s because it automatically made your “credit utilization” ratio look worse.

• Now that you’re aware, you can, and should, try to push back by asking for a higher limit but ONLY if you’re a real 690 or higher. If you’re not at least a 690, they could cancel you!

9 Strategies To Raise Your Credit Score to 720 or HIGHER!

• …. you’ll probably become frustrated by the process and you will NOT get results in 35–60 days, it might even be impossible!

You Can TRY Do-It-Yourself

Credit Repair But …

• Go to YouTube.com and watch the short “60 Minutes” YouTube video: “40 Million Mistakes: Is your credit report accurate?” In this 13 minute video clip you’ll see what the producers of “60 Minutes” discovered. There is VAST potential for inaccuracy in the credit report data that are used to calculate credit scores AND it’s nearly impossible to fix yourself. And the mistakes can be crippling! Watch it!

• Credit score improvement takes time. If you have serious black marks, such as bankruptcies, short sales or foreclosures, you can see significant improvement in your scores as time passes, but you may have to wait YEARS for those negatives to drop off your credit reports before you can join the “700-Plus Club.”

You Can TRY Do-It-Yourself Credit Repair But … (continued)

• Well, first off, this isn’t for everybody. While we’re not lawyers, using FICO 8 certified professionals isn’t cheap, but it IS valuable!

(Need a different paradigm!)

• Second, the question REALLY should be what does this cost if I DON’T do this? If you want to buy a home in a market that’s appreciating, how many thousands MORE will the home cost if you have to wait 18 to 24 months or more to TRY to get your credit healthier?

• If you want to re-finance or get a first time mortgage on a property, how many TENS of thousands MORE will you pay in interest on that loan over the years because you DON’T get our help? This doesn’t cost, it PAYS!

What Will This Cost?

Now You Have Some Basic Knowledge and …

Knowledge Applied is

POWER!

For a special detailed report on this INCLUDING 5 BONUS strategies, just contact us or get back with

the person who led you to this webinar.

Ask for “9 Strategies to Raise Your Credit Score to 720 or

HIGHER!”

“9 Strategies To Raise Your Credit Score to 720 or HIGHER!”

Insider Secrets to Higher Credit Scores & Funding!