9-1 Payroll Kirkwood Community College March 2, 2009 Presented by Sanh Tran, MBA, CPIM, CTL.

23

9-1 Payroll Kirkwood Community College March 2, 2009 Presented by Sanh Tran, MBA, CPIM, CTL

-

Upload

roxanne-ramsey -

Category

Documents

-

view

216 -

download

0

Transcript of 9-1 Payroll Kirkwood Community College March 2, 2009 Presented by Sanh Tran, MBA, CPIM, CTL.

9-1

Payroll

Kirkwood Community CollegeMarch 2, 2009

Presented by Sanh Tran, MBA, CPIM, CTL

McGraw-Hill/Irwin ©2008 The McGraw-Hill Companies, All Rights Reserved

Chapter 9

PayrollPayroll

9-3

• Define, compare, and contrast weekly, biweekly, semimonthly, and monthly pay periods

• Calculate gross pay with overtime on the basis of time

• Calculate gross pay for piecework, differential pay schedule, straight commission, variable commission scale and salary plus commission

Payroll#9#9Learning Unit ObjectivesCalculating Various Types of Employees’ Gross Pay

LU9.1LU9.1

9-4

• Prepare and explain the parts of a payroll register

• Explain and calculate federal and state unemployment taxes

Payroll#9#9Learning Unit ObjectivesComputing Payroll Deductions for Employees’ Pay; Employers’ Responsibilities

LU9.2LU9.2

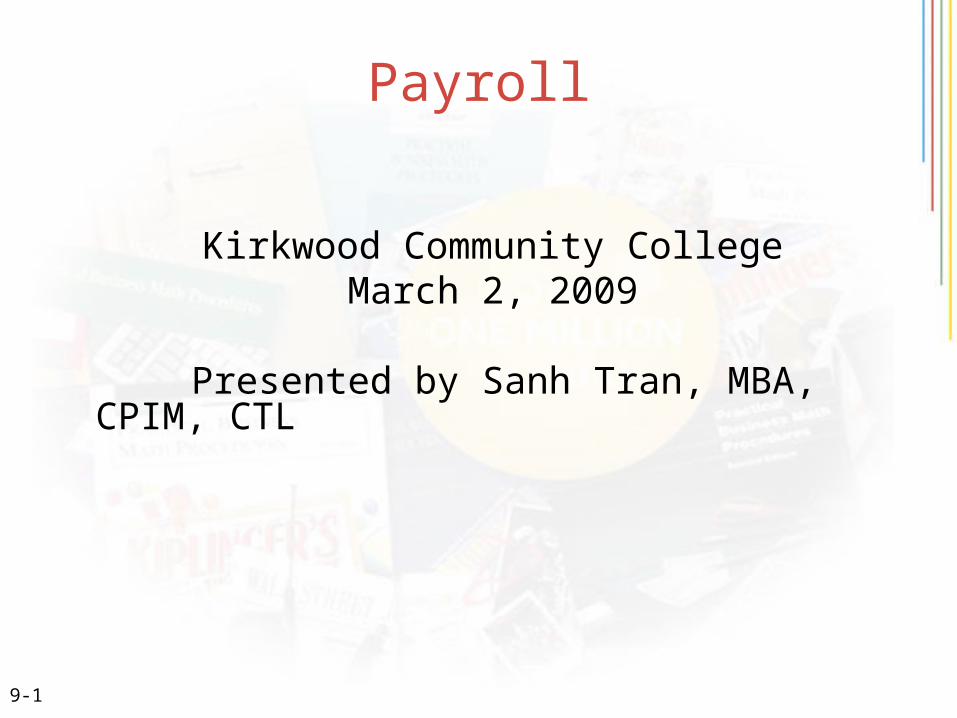

9-5

Payroll Cycles

Salary Paid Period (based on a year)

Weekly 52 times (once a week) $961.54 ($50,000/52)

Biweekly 26 times (every two weeks)$1,923.08 ($50,000/26)

Semimonthly 24 times (twice a month) $2,083.33 ($50,000/24)

Monthly 12 times (once a month) $4,166.67 ($50,000/12)

Earning per period

9-6

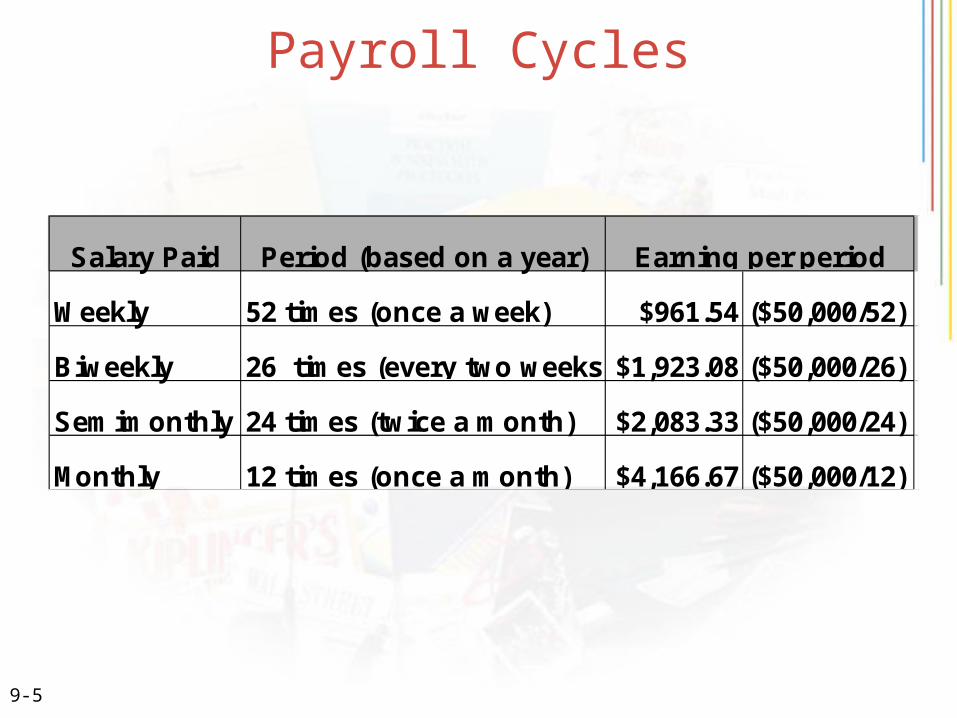

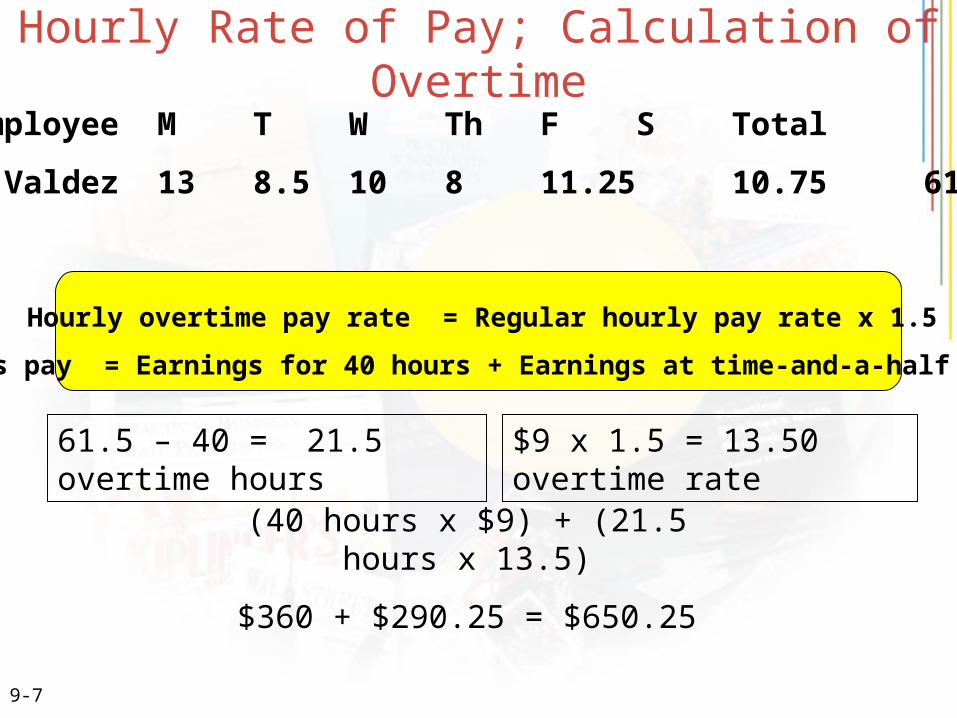

Hourly Rate of Pay; Calculation of Overtime

Gross pay = Hours Employee worked x Rate per hour

Hourly overtime pay rate = Regular hourly pay rate x 1.5

Gross pay = Earnings for 40 hours + Earnings at time-and-a-half rate

9-7

Hourly Rate of Pay; Calculation of Overtime

Employee M T W Th F S Total

R Valdez 13 8.5 10 8 11.25 10.75 61.5

Hourly overtime pay rate = Regular hourly pay rate x 1.5

Gross pay = Earnings for 40 hours + Earnings at time-and-a-half rate

(40 hours x $9) + (21.5 hours x 13.5)

$360 + $290.25 = $650.25

61.5 – 40 = 21.5 overtime hours $9 x 1.5 = 13.50 overtime rate

9-8

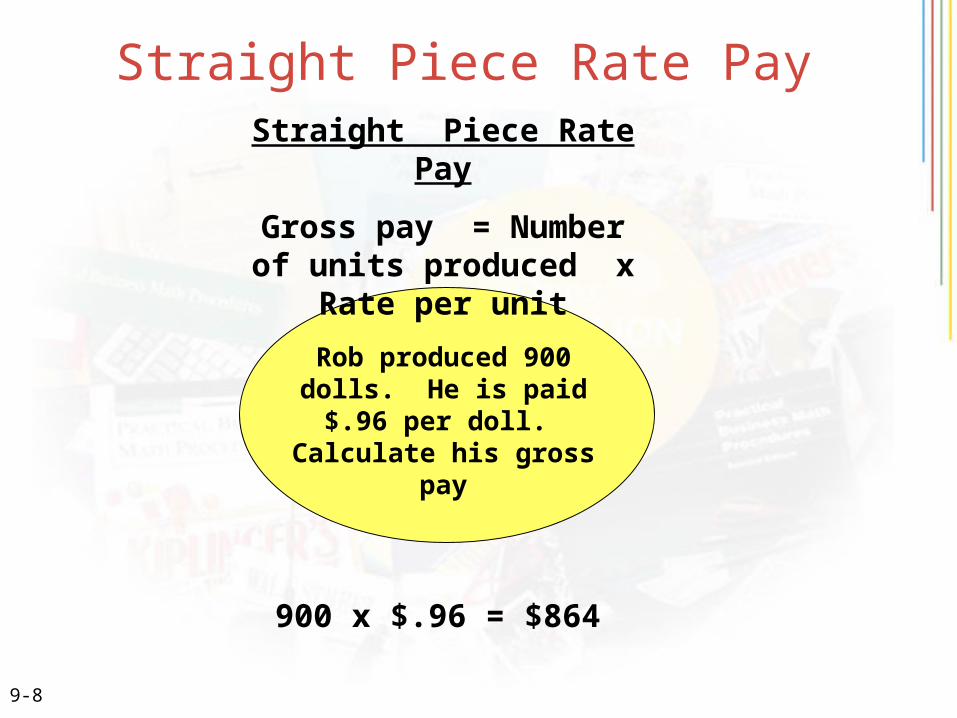

Straight Piece Rate Pay

Straight Piece Rate Pay

Gross pay = Number of units produced x Rate per unit

Rob produced 900 dolls. He is paid $.96 per doll.

Calculate his gross pay

900 x $.96 = $864

9-9

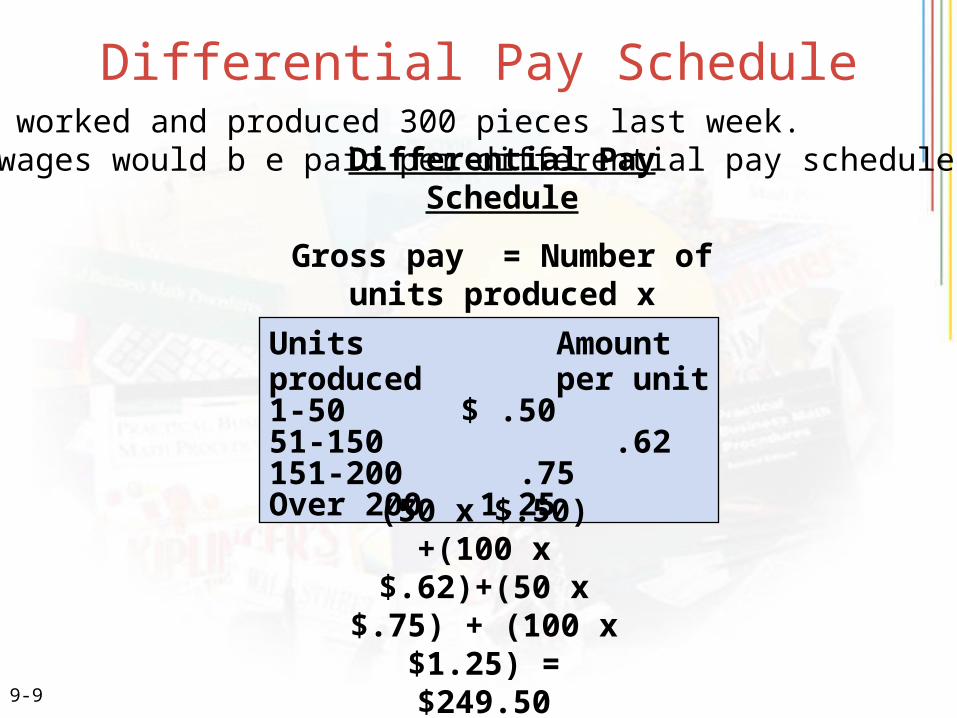

Differential Pay Schedule

Differential Pay Schedule

Gross pay = Number of units produced x Various rates per

unitUnits Amountproduced per unit1-50 $ .5051-150 .62151-200 .75Over 200 1.25

(50 x $.50) +(100 x $.62)+(50 x $.75) +

(100 x $1.25) = $249.50

John worked and produced 300 pieces last week. His wages would b e paid per differential pay schedule.

9-10

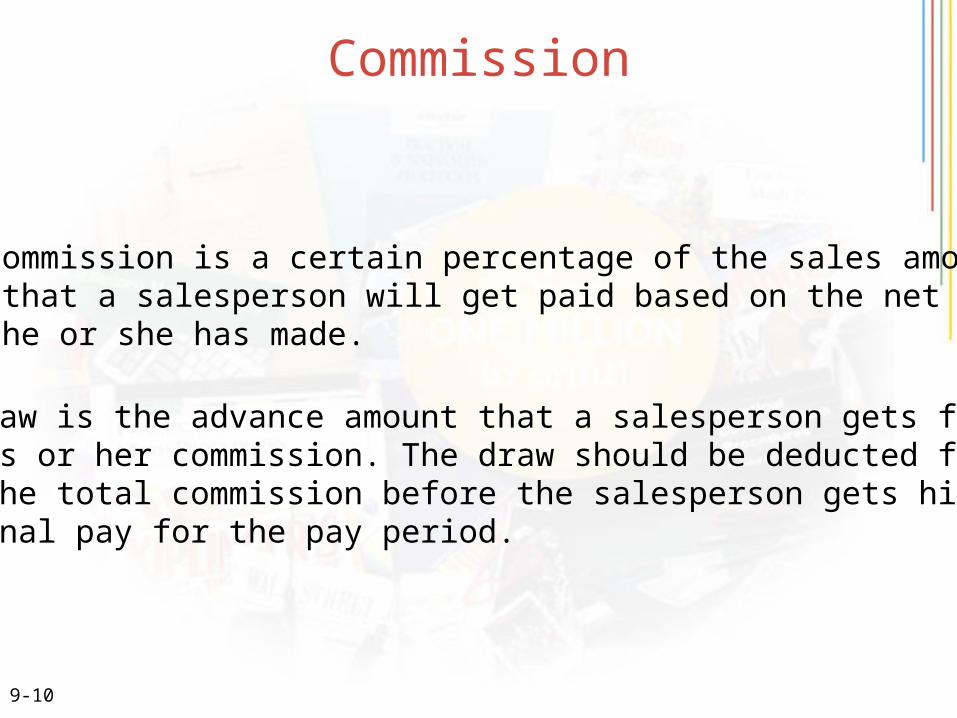

Commission

Commission is a certain percentage of the sales amount that a salesperson will get paid based on the net sales he or she has made.

Draw is the advance amount that a salesperson gets from his or her commission. The draw should be deducted from the total commission before the salesperson gets his or her final pay for the pay period.

9-11

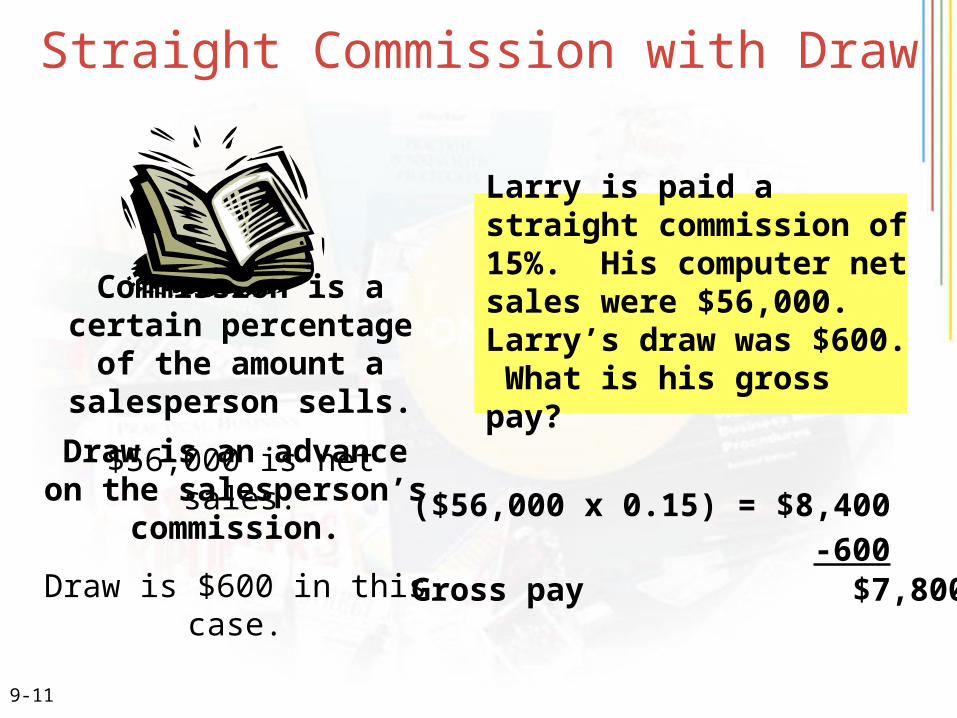

Straight Commission with Draw

Commission is a certain percentage of the amount a

salesperson sells.

$56,000 is net sales.Draw is an advance on the salesperson’s commission.

Draw is $600 in this case.

Larry is paid a straight commission of 15%. His computer net sales were $56,000. Larry’s draw was $600. What is his gross pay?

($56,000 x 0.15) = $8,400

-600Gross pay $7,800

9-12

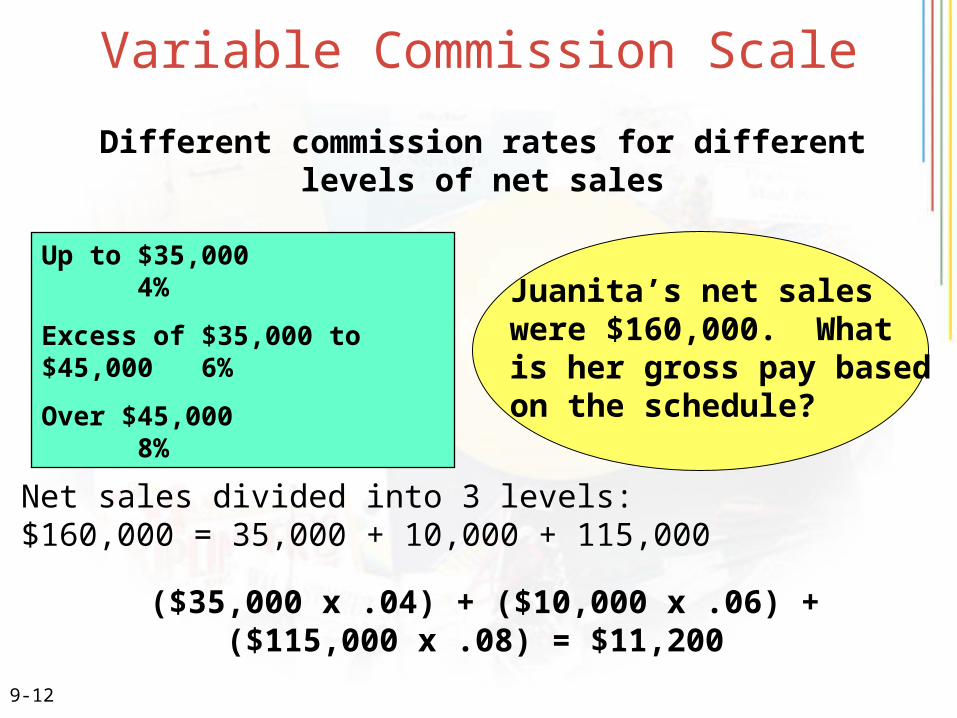

Variable Commission Scale

Different commission rates for different levels of net sales

Up to $35,000 4%

Excess of $35,000 to $45,000 6%

Over $45,000 8%

Juanita’s net sales were $160,000. What is her gross pay based on the schedule?

($35,000 x .04) + ($10,000 x .06) + ($115,000 x .08) = $11,200

Net sales divided into 3 levels:$160,000 = 35,000 + 10,000 + 115,000

9-13

Salary Plus CommissionGross Pay = Salary + Commission

Chung receives a salary of $3,000 per month. He also receives a 4% commission for sales over $20,000. Last month’s sales were $50,000. Calculate Chung’s gross

pay.

$3,000 + ($30,000 x .04) = $4,200

Sales amount over $20,000 with commission:$50,000 – 20,000 = $30,000 This amount would apply 4% commission.

9-14

Payroll Register

Week #41

Allowance& Salary

Employee marital Cum. per Cum. Health NetName status earnings week Reg. Ovt. Gross earnings S.S. Med. S.S. Med. FIT SIT Ins. Pay

Rey, Allice M-2 96,750 2,250 2,250 - 2,250 99,000 750 2,250 46.5 32.63 356 135 100 1,579.91A B C D E F G H I J K L M

GLO COMPANYPayroll Register

Earnings Taxable Earnings FICA

FICADeductions

Rate Base

Social Security 6.20% $97,500

Medicare 1.45 No Base

9-15

Federal Income Tax Withholding (FIT)

1. Percentage Method

9-16

Table 9-3,9-4 Percentage method income tax withholding tables

OneWithholding

Payroll Period AllowanceWeekly $ 65.38Bi weekly 130.77Semimonthly 141.67Monthly 283.33Quarterly 850.00SemiAnnually 1700.00Daily or miscellaneous (each 13.08day of the payroll period)

(b) MARRIED person -if the amount of wages(after subtracting The amount of income taxwithholding allowances) is: to withhold is:Not over $154 $0Over -- But not over -- of excess over --$154 $449 10% $154$449 $1,360 $29.50 plus 15% $449$1,360 $2,573 $166.15 plus 25% $1,360$2,573 $3,907 $469.40 plus 28% $2,573$3,907 $6,865 $842.92 plus 33% $3,907$6,865…… $1819.06 plus 35% $6,865

Partial

9-17

Percentage Method

1) Locate one withholding allowance and multiply by the number of allowances employee claims

2) Subtract step 1 from employees pay

3) In table 9.2 locate appropriate table and compute income tax

$65.38 x 2 = $130.76

$2,250.00 - 130.76$2,119.24

$2,119.24 -1,360.00$ 759.24

Tax $166.15 + .25 ($759.24) $166.15 + 189.81 = $355.96

9-18

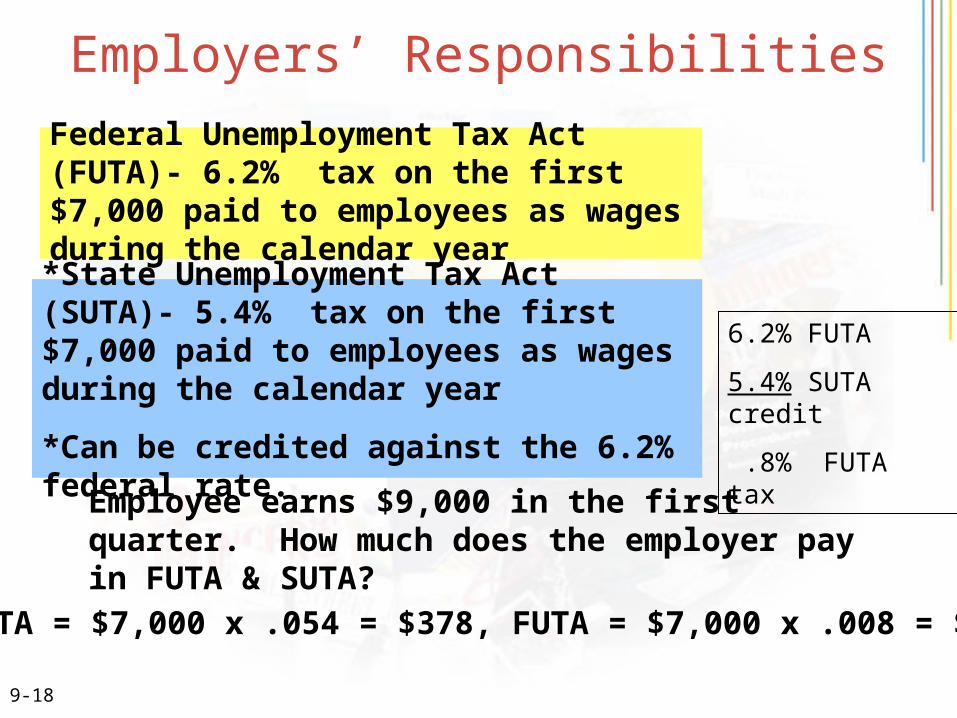

Employers’ Responsibilities

Federal Unemployment Tax Act (FUTA)- 6.2% tax on the first $7,000 paid to employees as wages during the calendar year

*State Unemployment Tax Act (SUTA)- 5.4% tax on the first $7,000 paid to employees as wages during the calendar year

*Can be credited against the 6.2% federal rate.

Employee earns $9,000 in the first quarter. How much does the employer pay in FUTA & SUTA?

SUTA = $7,000 x .054 = $378, FUTA = $7,000 x .008 = $56

6.2% FUTA

5.4% SUTA credit

.8% FUTA tax

9-19

Homework

9-28 and 9-29

9-20

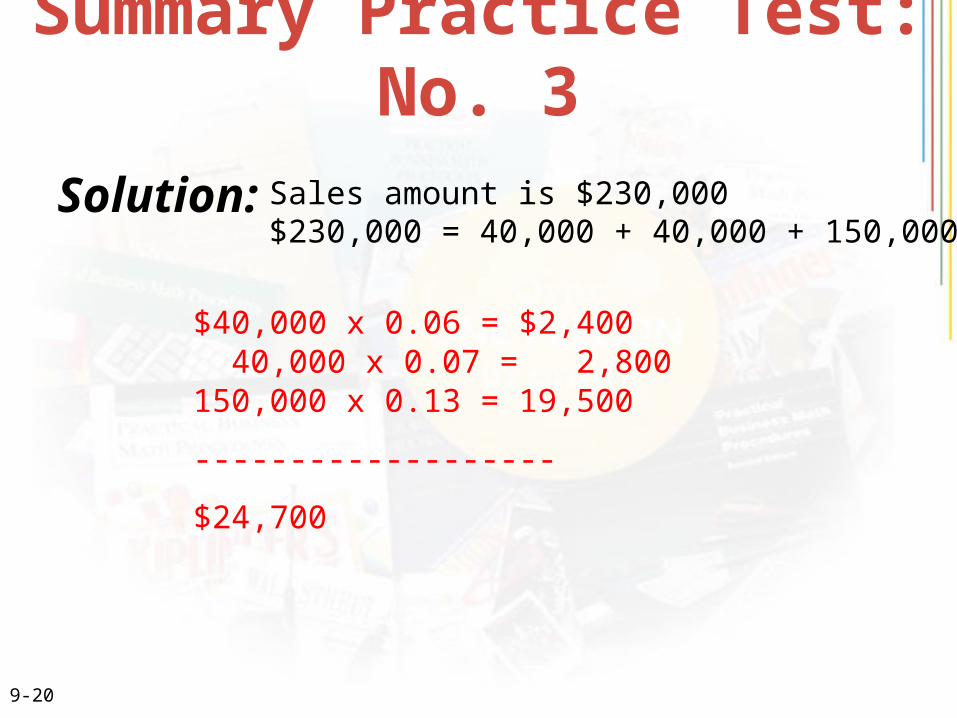

Summary Practice Test: No. 3

Solution:

$40,000 x 0.06 = $2,400 40,000 x 0.07 = 2,800150,000 x 0.13 = 19,500

------------------- $24,700

Sales amount is $230,000$230,000 = 40,000 + 40,000 + 150,000

9-21

Problem 9-26:

Solution:

Social Security: $2,100 x .062 = $130.20 Medicare: $2,100 x .0145 = $30.45

Yes for Social Security: 52 weeks x $2,100 = $109,200 - 97,500 $ 11,700 exempt

9-22

Problem 9-27:

Solution:

Social Security: $1,000 x .062 = $62Medicare: $1,300 x 0.0145 = $18.85

FIT: $1,300.00 - 130.76 ($65.38 x 2) $1,169.24 Base FIT + Additional FIT - 449.00 $29.50 + (0.15) ($720.24) $ 720.24 $29.50 + $108.04 = $137.54

2 is the exemption.$65.38 per exemption.

9-23

Problem 9-30:

Solution:

11 x $400 = $ 4,40011 x $500 = 5,50011 x $700 = 7,700 17,600 - 700 $16,900

State: $16,900 x .056 = $946.40

Federal: $16,900 x .008 = $135.20

$0 for week 30 (At week 30, all 3 employees had over $7,000 in wages in the year).

For the 3rd employee, the employer needs to pay up to the first $7,000. Hence, $700 should be deducted from the total $17,600.