870 Pages in 90 Minutes: What the CFPB Prepaid Proposal ... · PDF file•CFPB issues...

43

© Copyright 2014 by K&L Gates LLP. All rights reserved. 870 Pages in 90 Minutes: What the CFPB Prepaid Proposal Means to Your Business

Transcript of 870 Pages in 90 Minutes: What the CFPB Prepaid Proposal ... · PDF file•CFPB issues...

© Copyright 2014 by K&L Gates LLP. All rights reserved.

870 Pages in 90 Minutes: What the CFPB Prepaid Proposal Means to Your Business

klgates.com

David L. Beam, Partner

K&L Gates LLP1601 K Street NWWashington, D.C. [email protected]

David has a national practice advising companies on federal and state financial laws, with a focus on payments and credit regulation. His practice includes providing compliance and related business advice, interfacing with regulators on behalf of clients, negotiating transactions among parties involved in providing payment services, and defending clients in government investigations and enforcement proceedings.

The laws on which David advises clients include, for example, state money service business (money transmitter) laws; state credit card laws; state gift and prepaid card laws; the federal Electronic Funds Transfer Act and Regulation E; the Credit CARD Act of 2009; Regulation II (the regulation implementing the Durbin amendment); and FinCEN regulations under the Bank Secrecy Act. David’s clients range from startups to some of the world’s largest financial institutions. His practice embraces both traditional payment systems—such as plastic card-based systems—and emerging payment technologies.

Super Lawyers magazine named Mr. Beam a rising star in Washington, D.C., in both 2013 and 2014.

klgates.com 3

Steven M. Kaplan, Partner and Practice Area Leader — Financial Services

K&L Gates LLP1601 K Street NWWashington, D.C. 20006202.778.9204 [email protected]

Steve concentrates his practice in matters related to consumer financial products. His practice includes:

Representing clients in federal and state supervisory matters, investigations and enforcement proceedings;

Advising clients on compliance with federal and state laws governing the licensing and practices of financial institutions, mortgage lenders, consumer finance companies, loan servicers, prepaid card issuers, payment system providers, and secondary market participants;

Acting as regulatory counsel in connection with investments or acquisitions related to consumer loans and other consumer financial products;

Performing specialized regulatory compliance due diligence; Assisting with structuring operations and developing compliance

management systems and due diligence programs; and Assisting in litigation involving regulatory compliance matters.

klgates.com

Kathryn M. Baugher, Associate

K&L Gates LLP1601 K Street NWWashington, D.C. [email protected]

Kathryn represents and counsels a broad range of clients in connection with regulatory compliance matters, including government audits, investigations, and enforcement proceedings. She concentrates on consumer payment systems and federal regulatory enforcement issues, particularly those related to federal mortgage loan insurance/guarantee programs.

With respect to consumer payment systems, Ms. Baugher advises clients on compliance with a wide range of federal and state laws that regulate payment systems, including the Electronic Fund Transfer Act and Regulation E, state money services business (money transmitter) laws, and state gift and prepaid card laws.

Ms. Baugher also counsels clients regarding origination and servicing requirements for FHA-insured, VA-guaranteed, and USDA-guaranteed loans. Prior to joining K&L Gates, Ms. Baugher worked at the U.S. Department of Agriculture, where she advised the Rural Housing Service with respect to its Single Family Housing Guaranteed Loan Program.

klgates.com

Jeremy M. McLaughlin, Associate

K&L Gates LLP4 Embarcadero CenterSuite 1200San Francisco, CA [email protected]

Jeremy’s is a national practice that focuses principally on government enforcement and regulatory compliance for consumer financial products and services. He counsels a broad range of clients in connection with payment systems, credit regulation, data privacy, and consumer and commercial lending.

He focuses on regulatory compliance matters, government investigations, and enforcement proceedings regarding a wide range of federal and state laws, including the Bank Secrecy Act/Anti-Money laundering requirements, Electronic Fund Transfer Act, E-Sign Act, Gramm-Leach-Bliley Act, Fair Credit Reporting Act, and Truth in Lending Act. He also advises financial institutions on federal preemption of state and local laws regulating financial institutions. In addition, Jeremy advises national lenders and servicers on compliance with California state laws governing the financial services industry.

He assists clients in appeals before state and federal courts, including proceedings involving consumer financial laws. He has handled appeals for depository and non-depository financial institutions, among other clients, addressing a broad range of complex issues of law.

klgates.com

Kara M. Ward, Associate

K&L Gates LLP1601 K Street NWWashington, D.C. [email protected]

Kara concentrates her practice on federal policy, focusing on financial services, with an emphasis on the housing finance market, and particular experience with respect to insurance, consumer financial services, payment systems and community economic development.

She provides policy analysis and strategic advice to a variety of financial services companies and trade groups on matters that impact their business. She also engages in advocacy with the Congress and Executive Branch agencies in order to advance her clients’ objectives.

Kara works closely on issues involving the House Financial Services Committee, Senate Banking Committee, as well as the Treasury Department, Consumer Financial Protection Bureau, the Federal Housing Finance Agency, the Department of Housing and Urban Development and the Federal Reserve. Previously, she was an attorney in the Office of the General Counsel at the U.S. Department of the Treasury.

BACKGROUND

klgates.com 7

• Federal Reserve Board amended Regulation E to apply to payroll cards, with a few modifications (“Reg E Lite”)

• Considered, but declined to extend Reg E Lite to all prepaid cards.

• Federal Reserve Board amended Regulation E to apply to payroll cards, with a few modifications (“Reg E Lite”)

• Considered, but declined to extend Reg E Lite to all prepaid cards.2006• The Board adopts gift card rules.• Rules exempt reloadable prepaid products that were not marketed or

labelled as gift cards or gift certificates.

• The Board adopts gift card rules.• Rules exempt reloadable prepaid products that were not marketed or

labelled as gift cards or gift certificates.2010•CFPB issues notice that identifies prepaid cards as one of six markets the CFPB is considering to include as a “larger participant.”

•CFPB issues notice that identifies prepaid cards as one of six markets the CFPB is considering to include as a “larger participant.”2011

•CFPB issues Advance Notice of Proposed Rulemaking (“ANPR”) for GPR cards.•ANPR seeks comment on applying Reg E Lite, creating “Schumer Box”-style disclosures, and restricting credit features.

•CFPB issues Advance Notice of Proposed Rulemaking (“ANPR”) for GPR cards.•ANPR seeks comment on applying Reg E Lite, creating “Schumer Box”-style disclosures, and restricting credit features.2012

• CFPB begins taking complaints about prepaid cards.• CFPB releases proposed rule for prepaid accounts.• CFPB begins taking complaints about prepaid cards.• CFPB releases proposed rule for prepaid accounts.2014

KEY TAKEAWAYS

klgates.com 8

Applies “Reg E Lite” to “prepaid accounts”Applies “Reg E Lite” to “prepaid accounts”

Creates a uniform disclosure regime for prepaid accountsCreates a uniform disclosure regime for prepaid accounts

Restricts credit features associated with prepaid accountsRestricts credit features associated with prepaid accounts

KEY TAKEAWAYS

klgates.com 9

Requires issuers to submit prepaid account agreements to the Bureau for publicationRequires issuers to submit prepaid account agreements to the Bureau for publication

Does not impose restrictions on fees that can be charged for prepaid accountsDoes not impose restrictions on fees that can be charged for prepaid accounts

Does not define “larger participants” in the prepaid account marketDoes not define “larger participants” in the prepaid account market

Authorizes penalties under Dodd-Frank Act (in addition to Reg E/EFTA and Reg Z/TILA)Authorizes penalties under Dodd-Frank Act (in addition to Reg E/EFTA and Reg Z/TILA)

Applies Reg E’s limited liability and error resolution provisions to prepaid accountsApplies Reg E’s limited liability and error resolution provisions to prepaid accounts

TIMELINE Proposed rule posted on November 13, 2014;

CFPB held field hearings on same day. Comments will be due 90 days after publication

in Federal Register. Compliance dates will be based on publication

of final rule (“Final Publication”) Within nine months of Final Publication, disclosures for newly manufactured

prepaid account materials or information delivered to consumer online or by telephone must comply with applicable requirements of Regulation E.

Within twelve months of Final Publication, all prepaid accounts must comply with the requirements of the rule including its disclosure requirements.

klgates.com 10

klgates.com

Scope of the Proposed Rule: What is a “Prepaid Account”?

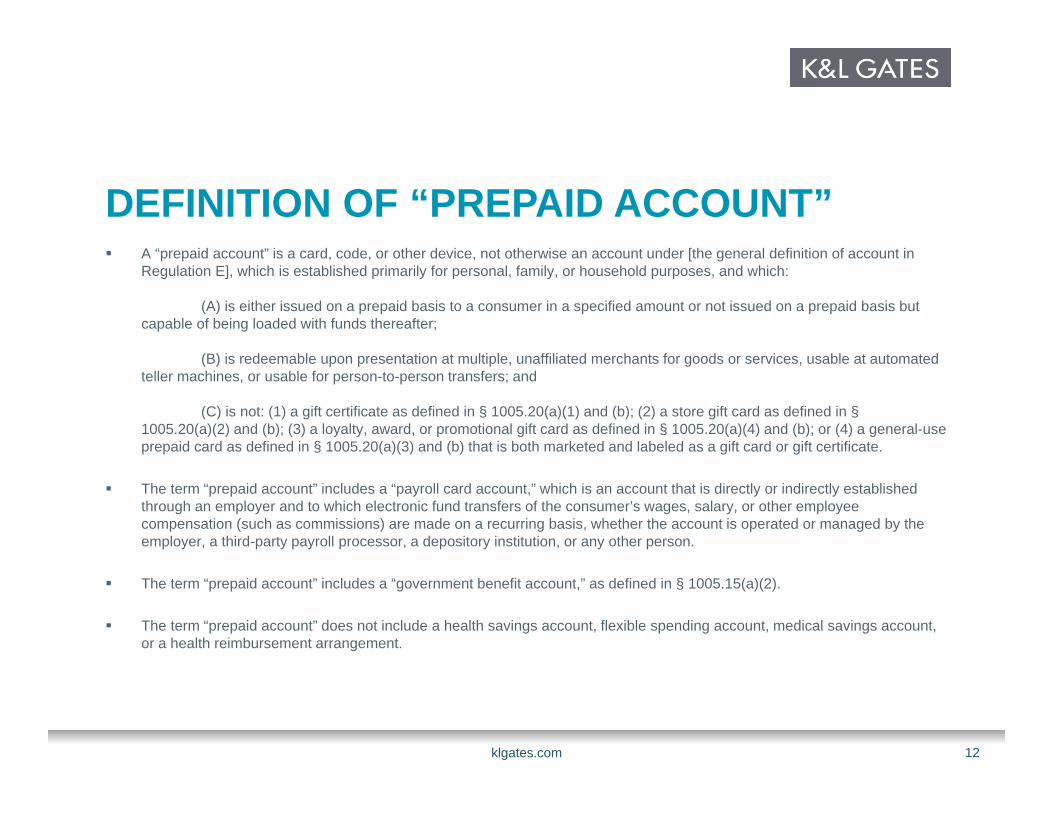

DEFINITION OF “PREPAID ACCOUNT” A “prepaid account” is a card, code, or other device, not otherwise an account under [the general definition of account in

Regulation E], which is established primarily for personal, family, or household purposes, and which:

(A) is either issued on a prepaid basis to a consumer in a specified amount or not issued on a prepaid basis but capable of being loaded with funds thereafter;

(B) is redeemable upon presentation at multiple, unaffiliated merchants for goods or services, usable at automated teller machines, or usable for person-to-person transfers; and

(C) is not: (1) a gift certificate as defined in § 1005.20(a)(1) and (b); (2) a store gift card as defined in §1005.20(a)(2) and (b); (3) a loyalty, award, or promotional gift card as defined in § 1005.20(a)(4) and (b); or (4) a general-use prepaid card as defined in § 1005.20(a)(3) and (b) that is both marketed and labeled as a gift card or gift certificate.

The term “prepaid account” includes a “payroll card account,” which is an account that is directly or indirectly established through an employer and to which electronic fund transfers of the consumer’s wages, salary, or other employee compensation (such as commissions) are made on a recurring basis, whether the account is operated or managed by the employer, a third-party payroll processor, a depository institution, or any other person.

The term “prepaid account” includes a “government benefit account,” as defined in § 1005.15(a)(2).

The term “prepaid account” does not include a health savings account, flexible spending account, medical savings account, or a health reimbursement arrangement.

klgates.com 12

DEFINITION OF “PREPAID ACCOUNT”: CARD, CODE, OR OTHER DEVICE

A prepaid account may be a “a card, code, or other device.”

The definition is not limited to physical cards or devices.

In the preamble to the proposed rule, the Bureau recognizes the existence of what it refers to as “virtual GPR cards” — prepaid products not linked to a physical card or device — that consumers may use “to store and transfer funds via the internet, text, or mobile phone application.”

klgates.com 13

DEFINITION OF “PREPAID ACCOUNT”: NOT OTHERWISE AN ACCOUNT UNDER REGULATION E

The definition of “prepaid account” indicates that if a product is otherwise an account under the general definition of “account” in Regulation E, then the product is not a “prepaid account.”

Existing Regulation E defines “account” as, in general, “a demand deposit (checking), savings, or other consumer asset account (other than an occasional or incidental credit balance in a credit plan) held directly or indirectly by a financial institution and established primarily for personal, family, or household purposes.”

klgates.com 14

RELATIONSHIP TO GIFT CARD RULES The definition of “prepaid account” also excludes “(1) a gift certificate as defined in §

1005.20(a)(1) and (b); (2) a store gift card as defined in § 1005.20(a)(2) and (b); (3) a loyalty, award, or promotional gift card as defined in § 1005.20(a)(4) and (b); [and] (4) a general-use prepaid card as defined in § 1005.20(a)(3) and (b) that is both marketed and labeled as a gift card or gift certificate.” The exemption in the gift card rules (§ 1005.20) for general-use prepaid cards applies to

products that are reloadable and not marketed or labeled as gift cards or gift certificates, whereas the definition of prepaid account would only exclude GPR cards that are both marketed and labeled as a gift card.

This distinction was deliberate. The Bureau did this to ensure that products it intended to include as prepaid accounts would not be excluded due to occasional or incidental marketing activities.

The proposed official interpretations consider the example of “a network-branded general purpose reloadable card that is principally advertised as a less-costly alternative to a bank account but is promoted in a television, radio, newspaper, or internet advertisement, or on signage as ‘the perfect gift’ during the holiday season. For purposes of § 1005.20, such a product would be considered marketed as a gift card or gift certificate because of this occasional holiday marketing activity. For purposes of § 1005.2(b)(3)(i)(C), however, such a product would not be considered to be both marketed and labeled as a gift card or gift certificate and thus would be covered by the definition of prepaid account.”

klgates.com 15

DEFINITION OF “PREPAID ACCOUNT”: ISSUED ON A PREPAID BASIS OR CAPABLE OF BEING LOADED WITH FUNDS The term “prepaid account” includes:

Accounts that are loaded with funds when first provided to a consumer for use; and Accounts that are issued to a consumer with a zero balance to which funds may be loaded

after issuance. A prepaid account must be capable of holding funds, not just acting as a pass-

through vehicle. A product that can never store funds, such as a digital wallet that only holds payment

credentials for other accounts, would not be considered a prepaid account. However, if funds can be transferred to a product and stored before the consumer designates

a destination for the funds, the product would satisfy this prong of the definition. The term “prepaid account” includes accounts that are not reloadable by the

consumer or a third party. The term “funds” is not expressly defined.

The preamble of the proposed rule states that “the proposed rule may have potential application to virtual currency and related products and services,” but that the Bureau’s analysis of these issues “is ongoing.”

klgates.com 16

DEFINITION OF “PREPAID ACCOUNT”: OPEN-LOOP, USABLE AT ATMS, OR USABLE FOR P2P TRANSFERS

A prepaid account must be usable for one or more of the following:

klgates.com 17

Purchases at multiple,

unaffiliated merchants

Person-to-person

transfers

ATM transactions

DEFINITION OF “PREPAID ACCOUNT”: OPEN-LOOP, USABLE AT ATMS, OR USABLE FOR P2P TRANSFERS (CONT’D)

What does it mean to be redeemable at multiple, unaffiliated merchants?

The preamble to the proposed rule paraphrases the requirement by stating that “a prepaid account would be one that is accepted widely at unaffiliated merchants, rather than only a single merchant or specific group of merchants, such as those located on a college campus or within a mall or defined shopping area.”

An account is capable of person-to-person transfers if the account allows a consumer to send funds by electronic fund transfer to another consumer or business. The proposed official interpretations clarify that a transaction involving a store gift card would not be a

person-to-person transfer if the gift card could only be used to make payments to the merchant or affiliated group of merchants on whose behalf the card was issued.

klgates.com 18

The proposed official interpretations cross-reference the existing official interpretations of the gift card rules on this point.

“A card, code, or other device is redeemable upon presentation at multiple, unaffiliated merchants if, for example, such merchants agree to honor the card, code, or device if it bears the mark, logo, or brand of a payment network, pursuant to the rules of the payment network.”

Companies can be “affiliated” if they “agree among themselves, by contract or otherwise, to redeem cards, codes, or other devices bearing the same name, mark, or logo (other than the mark, logo, or brand of a payment network), for the purchase of goods or services solely at such merchants or persons.”

klgates.com

Summary of the Proposed Rule’s Substantive Requirements

DISCLOSURES: GENERALLY Short Form Disclosure Long Form Disclosure Specific Form Requirements Variety of Model Form Disclosures

klgates.com 20

Short Form Disclosure “Static Fees”* Periodic fees, if any Per-purchase fees ATM withdrawal fees Cash reload fees ATM balance inquiry

fees Customer service fees Inactivity fees

Incidence-based Fees** Up to 3 fees not

otherwise disclosed incurred most frequently in prior 12-month period for that prepaid account

This analysis is required each year

klgates.com 21

*If any of the fees can vary, must disclose the highest fee with an explanation that a lower fee may apply**Each variable fee must be evaluated and listed separately

Short Form Disclosure (cont.) Other terms Statement regarding whether credit services and

related fees may apply Statement regarding number of all other fees that

could apply Statement that consumer must register card to protect

funds CFPB’s website for prepaid cards Phone number and website to access the Long Form If applicable, a statement that the product is not FDIC

or NCUSIF insured

klgates.com 22

Short Form Disclosure Model Form• Discloses variable fees exist

with *• No credit products• Discloses additional fees not

listed• Other Model Forms provided

klgates.com 23

Long Form Disclosure Must include all fees associated with prepaid

account and explanation of how they are imposed, waived, or reduced Includes third party fee amounts, to the extent known

Fees must be organized by categories of function, e.g., “Get Started,” “Get Cash,” “Spend Money”

klgates.com 24

Long Form Disclosure Model Form• Categories of fees• Other Model Forms provided

klgates.com 25

Disclosure Timing General Rule: Both provided pre-acquisition

Two exceptions, in which only short form disclosure must be provided pre-acquisition: Telephone exception Retail store exception

klgates.com 26

RETAIL STORE EXCEPTION To qualify for this exception:

The retail store must be a place that the consumer can acquire the account in person;

The consumer must acquire a physical access device at the location.

Retail store does not include: A location operated by the financial institution; A location operated by an agent of the financial institution; or A location that offers “one financial institution’s prepaid account products

exclusively.”

klgates.com 27

CAN’T BE AN AGENT OF THE FINANCIAL INSTITUTION A retail store does not include a location that is an agent of the financial

institution.

Retail stores generally sell prepaid products as the agent of somebody—issuer, program manager, distributor, etc.

Good for Consumers Ensures that funds belong to the principal as soon as they are received by the retailer. Protects funds from claims by retailer’s creditors. Obligates principal to honor funds received by retailer even if retailer does not remit funds.

No Reason to Distinguish It is no easier for a retailer that is the agent of the financial institution to provide the long form

disclosure than for a retailer that is not. Challenges arise from the nature of retail sales, not from relationship with issuer.

klgates.com 28

NOT A "RETAIL STORE" IF YOU SELL ONE FINANCIAL INSTITUTION’S PRODUCTS “EXCLUSIVELY”

What does “exclusively” mean? Does it require that there be an exclusivity agreement? Or is the store automatically considered an “agent” if it

just happens to sell only one prepaid account?

klgates.com 29

Focus is on whether store sells one financial institutions prepaid accounts exclusively. Gift cards

and other excluded prepaid products aren’t considered.

If it just means you sell only one, then . . . .

Retail store that starts selling prepaid accounts will need to

provide long form disclosure for first product on shelf (until it gets a

second product).

If a retail store sells two FI’s products and pulls one from the shelf (say, due to a dispute), the

other FI is required to ensure long form disclosure is provided—even if it didn’t know about the dispute.

FIs will need to require retail stores to rep and warrant that they will at all times sell at least one other FI’s

prepaid products.

INVENTORY CYCLING Because the rule regulates cards and packaging, Bureau recognizes that it needs to

account for inventory replacement cycle. Initial compliance

9 months to comply with respect to all aspects of the rule except retail packaging disclosures. 12 months to ensure that retail inventory complies with the disclosures.

Changes to incidence-based fees If the financial institution determines that the three most commonly imposed fees have changed, then new

inventory printed would need to reflect the update. No requirement to pull old inventory to reflect a change in which fees are most commonly imposed.

Changes to fee amounts

klgates.com 30

“Though the Bureau is not proposing specific package update requirements for the incidence-based fee disclosure, the Bureau notes, however, that financial institutions generally must ensure all other fee types and amounts disclosed pre-acquisition, whether on retail packaging, online, or through other means, are accurate at the time such disclosures are provided. The Bureau, therefore, does not believe that a general disclosure

update requirement is necessary for non-incidence-based fee disclosures provided before a consumer acquires a prepaid account, as a financial institution must continue to honor whatever fee schedule it provides

a consumer.”

REG E LITE: GENERALLY

klgates.com 31

“Full” Reg E v. “Lite”

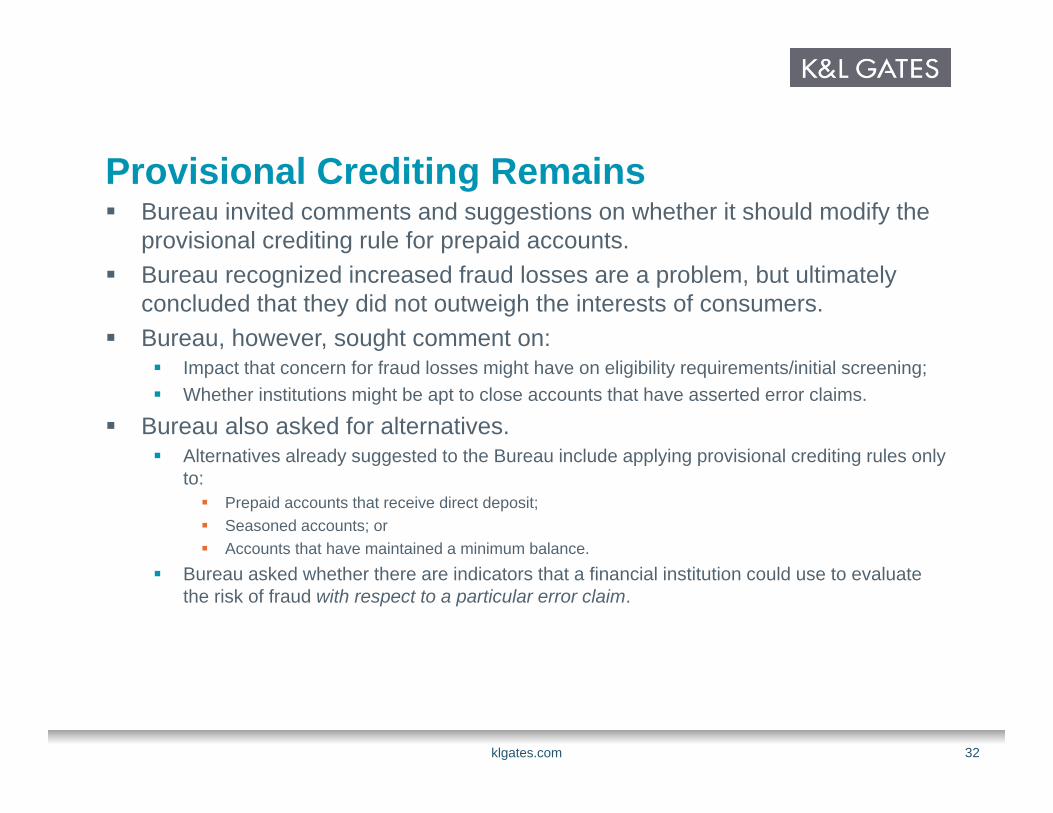

Provisional Crediting Remains Bureau invited comments and suggestions on whether it should modify the

provisional crediting rule for prepaid accounts. Bureau recognized increased fraud losses are a problem, but ultimately

concluded that they did not outweigh the interests of consumers. Bureau, however, sought comment on:

Impact that concern for fraud losses might have on eligibility requirements/initial screening; Whether institutions might be apt to close accounts that have asserted error claims.

Bureau also asked for alternatives. Alternatives already suggested to the Bureau include applying provisional crediting rules only

to: Prepaid accounts that receive direct deposit; Seasoned accounts; or Accounts that have maintained a minimum balance.

Bureau asked whether there are indicators that a financial institution could use to evaluate the risk of fraud with respect to a particular error claim.

klgates.com 32

UNREGISTERED ACCOUNTS For non-payroll and non-EBT

accounts, error resolution and liability limits do not apply if: Consumer hasn’t registered; and FI provides the notice in the sidebar.

Did CFPB intend to require a registration process? Preamble suggests that CFPB

presupposed that all prepaid accounts will be subject to KYC requirements.

But is that the case?

klgates.com 33

It is important to register your prepaid account as soon as possible. Until you

register your account, we are not required to research or resolve errors regarding your account. To register

your account, go to [Internet address] or call us at [telephone number]. We will ask you for identifying information

about yourself (including your full name, address, date of birth, and

[Social Security Number] [government-issued identification number]), so that we can verify your identity. Once we have done so, we will address your complaint or question as set forth

above.

klgates.com

Restrictions on Credit Features

RESTRICTIONS ON OVERDRAFT PROTECTION & OTHER CREDIT PRODUCTS Applies protections from TILA and Reg Z Narrow Exemption

Amends Reg Z definition of “card issuer” to exclude persons that issue a prepaid card that accesses only credit only not subject to any finance charge or fees and not payable in more than 4 installments

BUT: modifies Reg Z definition of “finance charge” to expressly include “any transaction charge” imposed in connection with extending credit, carrying a credit balance, or for credit availability if imposed on a prepaid account—“regardless of whether the creditor imposes the same, greater or lesser charge on the withdrawal of funds from the prepaid account, to have access to the prepaid account, or when credit is not extended.”

klgates.com 35

Credit Restrictions: Extends existing credit card protections from Reg Z Conduct ability to repay analysis Provide monthly periodic statements Provide at least 21 days to pay amounts owed in

connection with credit feature before charging late fee

Total fees cannot be more than 25% of initial credit limit in first year (a few fees excluded)

Cannot increase interest rate unless cardholder has missed two consecutive payments

Provide at least 45-day notice of rate increase

klgates.com 36

Credit Restrictions: Additions to Reg Z

Issuer must wait at least 30 days after consumer registers a prepaid product before opening or soliciting a credit account (note: not “purchases”) Applies even if cardholder has existing credit account

and cardholder registers additional prepaid card Cannot apply different terms and conditions to

prepaid account based on whether linked to credit product

klgates.com 37

Credit Restrictions: Offset (Reg Z) Current general rule: issuer may not offset

cardholder’s indebtedness from credit transaction against funds of cardholder held on account with issuer. Exception: if authorized in writing by cardholder to

periodically deduct all or part of credit debt from deposit account held with issuer

Proposed rule retains general rule, but alters exception such that deduction cannot occur more than once a month

klgates.com 38

Credit Restrictions: Compulsory Use (Reg E) Current law prohibits person from requiring as a

condition for extending credit repayment by preauthorized electronic fund transfers Exception: preauthorized electronic fund transfer

requirement permitted for overdraft protection plans Proposed Rule does not extend the overdraft exception

to prepaid cards, so issuer cannot require repayments of amounts related to a credit feature (such as overdrafts) on a preauthorized, recurring basis using amounts deposited in prepaid account.

klgates.com 39

IS CONGRESS LIKELY TO GET INVOLVED?

Sen. Bob Menendez (D-NJ): “Applauds” CFPB Proposal“Right before consumers swarm to the stores on Black Friday, I’m glad we’re talking about protections for a form of payment that is soaring in use. As the market for prepaid products continues to grow, the need for strong consumer protections and clear guidelines grows as well. Companies should not be able to hide behind the fine print to raise their bottom lines at the expense of responsible consumers. I look forward to reviewing the proposal and continuing to work with the CFPB to make sure consumers are not fooled – regardless of whether they’re paying ahead of time or at the cash register.”

Rep. Maxine Waters (D-CA): Supports CFPB Proposal “Although many lower-income consumers are increasingly turning to prepaid cards to avoid high or

unpredictable bank fees, consumer protections have not kept pace. Today’s announcement ensures that Americans using prepaid cards are treated equally, and afforded the same consumer protections, as credit and debit card holders.”

klgates.com 40

WHAT IS THE CURRENT CLIMATE IN D.C.?

klgates.com 41

Senate Banking Committee

Sen. Richard Shelby (R-AL)

House Financial Services

Rep. Jeb Hensarling (R-TX)

Sen. Sherrod Brown (D-OH)

Rep. Maxine Waters (D-CA)

klgates.com

EFFECT ON STATE LAWS?