8 September Daily market report

7

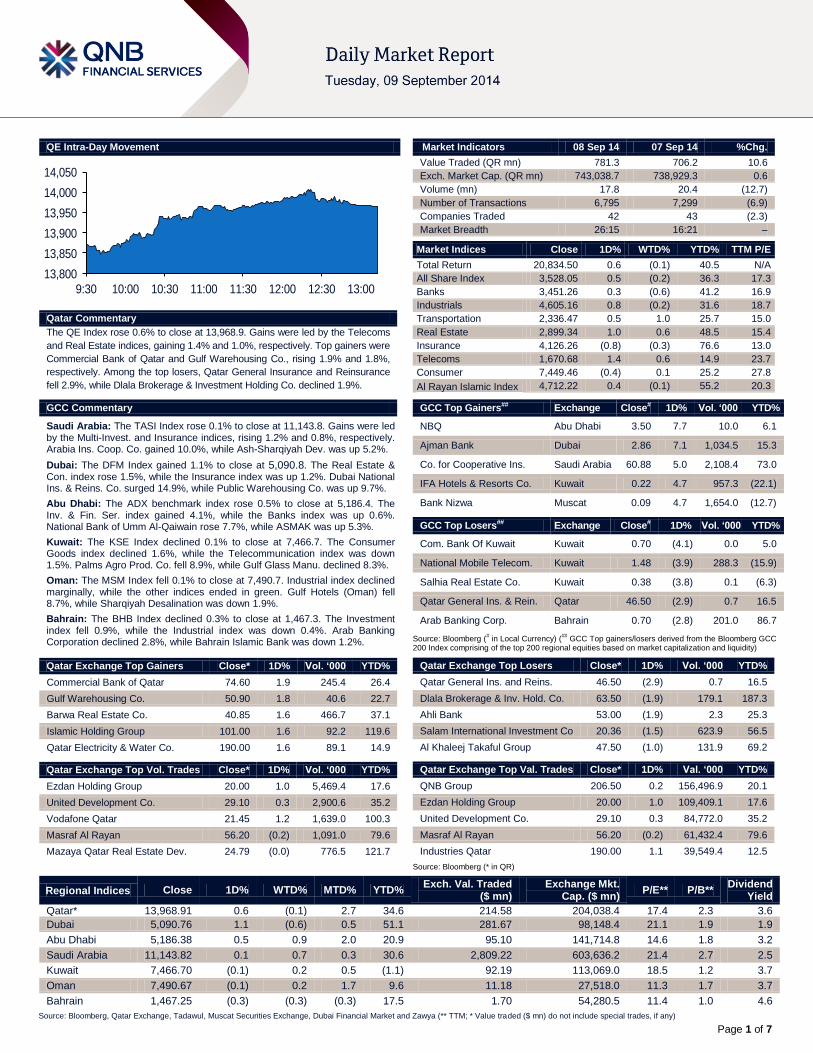

Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE Index rose 0.6% to close at 13,968.9. Gains were led by the Telecoms and Real Estate indices, gaining 1.4% and 1.0%, respectively. Top gainers were Commercial Bank of Qatar and Gulf Warehousing Co., rising 1.9% and 1.8%, respectively. Among the top losers, Qatar General Insurance and Reinsurance fell 2.9%, while Dlala Brokerage & Investment Holding Co. declined 1.9%. GCC Commentary Saudi Arabia: The TASI Index rose 0.1% to close at 11,143.8. Gains were led by the Multi-Invest. and Insurance indices, rising 1.2% and 0.8%, respectively. Arabia Ins. Coop. Co. gained 10.0%, while Ash-Sharqiyah Dev. was up 5.2%. Dubai: The DFM Index gained 1.1% to close at 5,090.8. The Real Estate & Con. index rose 1.5%, while the Insurance index was up 1.2%. Dubai National Ins. & Reins. Co. surged 14.9%, while Public Warehousing Co. was up 9.7%. Abu Dhabi: The ADX benchmark index rose 0.5% to close at 5,186.4. The Inv. & Fin. Ser. index gained 4.1%, while the Banks index was up 0.6%. National Bank of Umm Al-Qaiwain rose 7.7%, while ASMAK was up 5.3%. Kuwait: The KSE Index declined 0.1% to close at 7,466.7. The Consumer Goods index declined 1.6%, while the Telecommunication index was down 1.5%. Palms Agro Prod. Co. fell 8.9%, while Gulf Glass Manu. declined 8.3%. Oman: The MSM Index fell 0.1% to close at 7,490.7. Industrial index declined marginally, while the other indices ended in green. Gulf Hotels (Oman) fell 8.7%, while Sharqiyah Desalination was down 1.9%. Bahrain: The BHB Index declined 0.3% to close at 1,467.3. The Investment index fell 0.9%, while the Industrial index was down 0.4%. Arab Banking Corporation declined 2.8%, while Bahrain Islamic Bank was down 1.2%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Commercial Bank of Qatar 74.60 1.9 245.4 26.4 Gulf Warehousing Co. 50.90 1.8 40.6 22.7 Barwa Real Estate Co. 40.85 1.6 466.7 37.1 Islamic Holding Group 101.00 1.6 92.2 119.6 Qatar Electricity & Water Co. 190.00 1.6 89.1 14.9 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 20.00 1.0 5,469.4 17.6 United Development Co. 29.10 0.3 2,900.6 35.2 Vodafone Qatar 21.45 1.2 1,639.0 100.3 Masraf Al Rayan 56.20 (0.2) 1,091.0 79.6 Mazaya Qatar Real Estate Dev. 24.79 (0.0) 776.5 121.7 Market Indicators 08 Sep 14 07 Sep 14 %Chg. Value Traded (QR mn) 781.3 706.2 10.6 Exch. Market Cap. (QR mn) 743,038.7 738,929.3 0.6 Volume (mn) 17.8 20.4 (12.7) Number of Transactions 6,795 7,299 (6.9) Companies Traded 42 43 (2.3) Market Breadth 26:15 16:21 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 20,834.50 0.6 (0.1) 40.5 N/A All Share Index 3,528.05 0.5 (0.2) 36.3 17.3 Banks 3,451.26 0.3 (0.6) 41.2 16.9 Industrials 4,605.16 0.8 (0.2) 31.6 18.7 Transportation 2,336.47 0.5 1.0 25.7 15.0 Real Estate 2,899.34 1.0 0.6 48.5 15.4 Insurance 4,126.26 (0.8) (0.3) 76.6 13.0 Telecoms 1,670.68 1.4 0.6 14.9 23.7 Consumer 7,449.46 (0.4) 0.1 25.2 27.8 Al Rayan Islamic Index 4,712.22 0.4 (0.1) 55.2 20.3 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% NBQ Abu Dhabi 3.50 7.7 10.0 6.1 Ajman Bank Dubai 2.86 7.1 1,034.5 15.3 Co. for Cooperative Ins. Saudi Arabia 60.88 5.0 2,108.4 73.0 IFA Hotels & Resorts Co. Kuwait 0.22 4.7 957.3 (22.1) Bank Nizwa Muscat 0.09 4.7 1,654.0 (12.7) GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Com. Bank Of Kuwait Kuwait 0.70 (4.1) 0.0 5.0 National Mobile Telecom. Kuwait 1.48 (3.9) 288.3 (15.9) Salhia Real Estate Co. Kuwait 0.38 (3.8) 0.1 (6.3) Qatar General Ins. & Rein. Qatar 46.50 (2.9) 0.7 16.5 Arab Banking Corp. Bahrain 0.70 (2.8) 201.0 86.7 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. and Reins. 46.50 (2.9) 0.7 16.5 Dlala Brokerage & Inv. Hold. Co. 63.50 (1.9) 179.1 187.3 Ahli Bank 53.00 (1.9) 2.3 25.3 Salam International Investment Co 20.36 (1.5) 623.9 56.5 Al Khaleej Takaful Group 47.50 (1.0) 131.9 69.2 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% QNB Group 206.50 0.2 156,496.9 20.1 Ezdan Holding Group 20.00 1.0 109,409.1 17.6 United Development Co. 29.10 0.3 84,772.0 35.2 Masraf Al Rayan 56.20 (0.2) 61,432.4 79.6 Industries Qatar 190.00 1.1 39,549.4 12.5 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 13,968.91 0.6 (0.1) 2.7 34.6 214.58 204,038.4 17.4 2.3 3.6 Dubai 5,090.76 1.1 (0.6) 0.5 51.1 281.67 98,148.4 21.1 1.9 1.9 Abu Dhabi 5,186.38 0.5 0.9 2.0 20.9 95.10 141,714.8 14.6 1.8 3.2 Saudi Arabia 11,143.82 0.1 0.7 0.3 30.6 2,809.22 603,636.2 21.4 2.7 2.5 Kuwait 7,466.70 (0.1) 0.2 0.5 (1.1) 92.19 113,069.0 18.5 1.2 3.7 Oman 7,490.67 (0.1) 0.2 1.7 9.6 11.18 27,518.0 11.3 1.7 3.7 Bahrain 1,467.25 (0.3) (0.3) (0.3) 17.5 1.70 54,280.5 11.4 1.0 4.6 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 13,800 13,850 13,900 13,950 14,000 14,050 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

-

Upload

qnb-group -

Category

Economy & Finance

-

view

264 -

download

5

description

Transcript of 8 September Daily market report

Page 1 of 7

QE Intra-Day Movement

Qatar Commentary

The QE Index rose 0.6% to close at 13,968.9. Gains were led by the Telecoms

and Real Estate indices, gaining 1.4% and 1.0%, respectively. Top gainers were

Commercial Bank of Qatar and Gulf Warehousing Co., rising 1.9% and 1.8%,

respectively. Among the top losers, Qatar General Insurance and Reinsurance

fell 2.9%, while Dlala Brokerage & Investment Holding Co. declined 1.9%.

GCC Commentary

Saudi Arabia: The TASI Index rose 0.1% to close at 11,143.8. Gains were led by the Multi-Invest. and Insurance indices, rising 1.2% and 0.8%, respectively. Arabia Ins. Coop. Co. gained 10.0%, while Ash-Sharqiyah Dev. was up 5.2%.

Dubai: The DFM Index gained 1.1% to close at 5,090.8. The Real Estate & Con. index rose 1.5%, while the Insurance index was up 1.2%. Dubai National Ins. & Reins. Co. surged 14.9%, while Public Warehousing Co. was up 9.7%.

Abu Dhabi: The ADX benchmark index rose 0.5% to close at 5,186.4. The Inv. & Fin. Ser. index gained 4.1%, while the Banks index was up 0.6%. National Bank of Umm Al-Qaiwain rose 7.7%, while ASMAK was up 5.3%.

Kuwait: The KSE Index declined 0.1% to close at 7,466.7. The Consumer Goods index declined 1.6%, while the Telecommunication index was down 1.5%. Palms Agro Prod. Co. fell 8.9%, while Gulf Glass Manu. declined 8.3%.

Oman: The MSM Index fell 0.1% to close at 7,490.7. Industrial index declined marginally, while the other indices ended in green. Gulf Hotels (Oman) fell 8.7%, while Sharqiyah Desalination was down 1.9%.

Bahrain: The BHB Index declined 0.3% to close at 1,467.3. The Investment index fell 0.9%, while the Industrial index was down 0.4%. Arab Banking Corporation declined 2.8%, while Bahrain Islamic Bank was down 1.2%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Commercial Bank of Qatar 74.60 1.9 245.4 26.4

Gulf Warehousing Co. 50.90 1.8 40.6 22.7

Barwa Real Estate Co. 40.85 1.6 466.7 37.1

Islamic Holding Group 101.00 1.6 92.2 119.6

Qatar Electricity & Water Co. 190.00 1.6 89.1 14.9

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 20.00 1.0 5,469.4 17.6

United Development Co. 29.10 0.3 2,900.6 35.2

Vodafone Qatar 21.45 1.2 1,639.0 100.3

Masraf Al Rayan 56.20 (0.2) 1,091.0 79.6

Mazaya Qatar Real Estate Dev. 24.79 (0.0) 776.5 121.7

Market Indicators 08 Sep 14 07 Sep 14 %Chg.

Value Traded (QR mn) 781.3 706.2 10.6

Exch. Market Cap. (QR mn) 743,038.7 738,929.3 0.6

Volume (mn) 17.8 20.4 (12.7)

Number of Transactions 6,795 7,299 (6.9)

Companies Traded 42 43 (2.3)

Market Breadth 26:15 16:21 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 20,834.50 0.6 (0.1) 40.5 N/A

All Share Index 3,528.05 0.5 (0.2) 36.3 17.3

Banks 3,451.26 0.3 (0.6) 41.2 16.9

Industrials 4,605.16 0.8 (0.2) 31.6 18.7

Transportation 2,336.47 0.5 1.0 25.7 15.0

Real Estate 2,899.34 1.0 0.6 48.5 15.4

Insurance 4,126.26 (0.8) (0.3) 76.6 13.0

Telecoms 1,670.68 1.4 0.6 14.9 23.7

Consumer 7,449.46 (0.4) 0.1 25.2 27.8

Al Rayan Islamic Index 4,712.22 0.4 (0.1) 55.2 20.3

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

NBQ Abu Dhabi 3.50 7.7 10.0 6.1

Ajman Bank Dubai 2.86 7.1 1,034.5 15.3

Co. for Cooperative Ins. Saudi Arabia 60.88 5.0 2,108.4 73.0

IFA Hotels & Resorts Co. Kuwait 0.22 4.7 957.3 (22.1)

Bank Nizwa Muscat 0.09 4.7 1,654.0 (12.7)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Com. Bank Of Kuwait Kuwait 0.70 (4.1) 0.0 5.0

National Mobile Telecom. Kuwait 1.48 (3.9) 288.3 (15.9)

Salhia Real Estate Co. Kuwait 0.38 (3.8) 0.1 (6.3)

Qatar General Ins. & Rein. Qatar 46.50 (2.9) 0.7 16.5

Arab Banking Corp. Bahrain 0.70 (2.8) 201.0 86.7

Source: Bloomberg (# in Local Currency) (

## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar General Ins. and Reins. 46.50 (2.9) 0.7 16.5

Dlala Brokerage & Inv. Hold. Co. 63.50 (1.9) 179.1 187.3

Ahli Bank 53.00 (1.9) 2.3 25.3

Salam International Investment Co 20.36 (1.5) 623.9 56.5

Al Khaleej Takaful Group 47.50 (1.0) 131.9 69.2

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

QNB Group 206.50 0.2 156,496.9 20.1

Ezdan Holding Group 20.00 1.0 109,409.1 17.6

United Development Co. 29.10 0.3 84,772.0 35.2

Masraf Al Rayan 56.20 (0.2) 61,432.4 79.6

Industries Qatar 190.00 1.1 39,549.4 12.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded

($ mn) Exchange Mkt.

Cap. ($ mn) P/E** P/B**

Dividend Yield

Qatar* 13,968.91 0.6 (0.1) 2.7 34.6 214.58 204,038.4 17.4 2.3 3.6

Dubai

5,090.76 1.1 (0.6) 0.5 51.1 281.67 98,148.4 21.1 1.9 1.9

Abu Dhabi

5,186.38 0.5 0.9 2.0 20.9 95.10 141,714.8 14.6 1.8 3.2

Saudi Arabia

11,143.82 0.1 0.7 0.3 30.6 2,809.22 603,636.2 21.4 2.7 2.5

Kuwait 7,466.70 (0.1) 0.2 0.5 (1.1) 92.19 113,069.0 18.5 1.2 3.7

Oman 7,490.67 (0.1) 0.2 1.7 9.6 11.18 27,518.0 11.3 1.7 3.7

Bahrain 1,467.25 (0.3) (0.3) (0.3) 17.5 1.70 54,280.5 11.4 1.0 4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,800

13,850

13,900

13,950

14,000

14,050

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

Page 2 of 7

Qatar Market Commentary

The QE Index rose 0.6% to close at 13,968.9. The Telecoms and Real Estate indices led the gains. The index rose on the back of buying support from Qatari shareholders despite selling pressure from non-Qatari shareholders.

Commercial Bank of Qatar and Gulf Warehousing Co. were the top gainers, rising 1.9% and 1.8%, respectively. Among the top losers, Qatar General Insurance and Reinsurance fell 2.9%, while Dlala Brokerage & Investment Holding Co. declined 1.9%.

Volume of shares traded on Monday fell by 12.7% to 17.8mn from 20.4mn on Sunday. However, as compared to the 30-day moving average of 17.4mn, volume for the day was 2.4% higher. Ezdan Holding Group and United Development Co. were the most active stocks, contributing 30.7% and 16.3% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

09/08 US US Treasury 3M High Yield Rate 8-September 0.02% – 0.03%

09/08 US US Treasury 6M High Yield Rate 8-September 0.05% – 0.05%

09/08 US Federal Reserve Consumer Credit July $26.006B $17.350B $18.806B

09/08 EU Sentix Behavioral Ind. Sentix Investor Confidence September -9.8 1.4 2.7

09/08 France Banque De France Bank of France Bus. Sentiment August 97.0 95.0 96.0

09/08 France Ministry of the Economy 3M T-Bill Amount Sold 8-September EU3,896M – EU3,991M

09/08 France Ministry of the Economy 3M T-Bill Average Yield 8-September -0.05% – 0.00%

09/08 France Ministry of the Economy 3M T-Bill Bid/Cover Ratio 8-September 2.7 – 3.0

09/08 France Ministry of the Economy 6M T-Bill Amount Sold 8-September EU1,896M – EU2,093M

09/08 France Ministry of the Economy 6M T-Bill Average Yield 8-September -0.06% – 0.00%

09/08 France Ministry of the Economy 6M T-Bill Bid/Cover Ratio 8-September 4.4 – 4.2

09/08 France Ministry of the Economy 12M T-Bill Amount Sold 8-September EU1,893M – EU2,095M

09/08 France Ministry of the Economy 12M T-Bill Average Yield 8-September -0.06% – 0.00%

09/08 France Ministry of the Economy 12M T-Bill Bid/Cover Ratio 8-September 3.9 – 3.5

09/08 Germany Destatis Trade Balance July 23.4B 16.8B 16.6B

09/08 Germany Destatis Current Account Balance July 21.7B 14.0B 17.2B

09/08 Germany Deutsche Bundesbank 6M Bill Allotment 8-September 1,895M – 1,431M

09/08 Germany Deutsche Bundesbank 6M Bill Average Yield 8-September -0.09% – 0.00%

09/08 Germany Deutsche Bundesbank 6M Bill Bid-Cover 8-September 2.9 – 2.3

09/08 UK Lloyds TSB Halifax House Prices MoM August 0.10% 0.30% 1.20%

09/08 UK Lloyds TSB Halifax House Price 3Mths/Year August 9.70% 10.00% 10.20%

09/08 UK Lloyds Bank Lloyds Employment Confidence August 6.0 – 6.0

09/08 UK London Gold Market Fix. London Gold Market PM Fix 8-September 1,259.0 – 1,266.0

09/08 Spain INE INE House Price Index QoQ 2Q2014 1.70% – -0.30%

09/08 Spain INE INE House Price Index YoY 2Q2014 0.80% – -1.60%

09/08 China Nat. Bureau of Statistics Trade Balance August $49.84B $40.00B $47.30B

09/08 China Nat. Bureau of Statistics Exports YoY August 9.40% 9.00% 14.50%

09/08 China Nat. Bureau of Statistics Imports YoY August -2.40% 3.00% -1.60%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted

Overall Activity Buy %* Sell %* Net (QR)

Qatari 57.49% 54.16% 26,033,355.60

Non-Qatari 42.51% 45.84% (26,033,355.60)

Page 3 of 7

News

Qatar

QNB Group: Qatar project spend set to pick up during 2014-16 – According to a report by QNB Group (QNBK), Qatar’s

investment spending is set to pick up during the 2014-16 period and drive the country’s economic growth. The government has major infrastructure plans for the run-up to the 2022 World Cup and has been implementing those plans. A number of major projects are now underway that have commitments to be completed ahead of the World Cup. QNBK expects project activity to gain momentum during the 2014-2016 period. This includes, for example, the $45.0bn Lusail real estate development project as well as the $40.0bn Qatar Integrated Rail project. Qatar’s development is underpinned by an array of investment projects, which have been crucial toward driving its economic growth in recent years. QNBK said that the infrastructure projects in construction and transport currently account for the largest share of project spending in Qatar. Construction and transport projects make up 78.6% of the projects currently underway. While oil & gas accounted for the bulk of projects during 2000-2011, their share is budgeted to account for only 9.7% over the next decade. This reflects Qatar’s development path, which is now using revenue from the hydrocarbon sector to build up the non-hydrocarbon economy. The bulk of project budgets in construction are for mixed-use real estate developments. Transport spending includes a range of road, rail, sea and air projects. Few new major projects in the gas sector are likely to be initiated in the next few years owing to the North Field moratorium. In the oil sector, projects to boost production at existing fields have been initiated, such as the Bul Hanine redevelopment. (Gulf-Times.com)

Qatar’s gas reserves set to last 156 years – According a

Qatar Economic Insight report by QNB Group (QNBK), Qatar’s gas reserves would last at least another 156 years at current production rates. Qatar had raw gas reserves totaling 872tn cubic feet at end-2013, giving it the third largest proven reserves of natural gas in the world after Russia and Iran. QNBK said that it is therefore likely that Qatar will continue extracting gas well into the 22nd century. Qatar discovered the extent of its natural gas reserves in 1971 when the offshore North Field was discovered. The North Field is now known to be the largest non-associated gas field in the world, accounting for around 99% of Qatar’s gas reserves. Gas production grew on an average 15.4% annually during the 2009-13 period as additional LNG export facilities became operational. Large-scale LNG projects led to major increases in gas production. Qatar is ranked fourth globally for gas production. Around 52.6% of gas production was allocated to LNG exports in 2013, but the expansion program is now complete and LNG production is expected to plateau. Qatar also exports around 11.7% of gas production by pipeline to the UAE. The Barzan project, a $10.3bn North Field gas development, will increase production for domestic use. Initial production is expected in 2015 with incremental growth until 2023. Barzan is an exception to a moratorium on new production from the North Field. As per QNBK, Qatar is likely to benefit from the robust global LNG demand over the next few years. The continued strong Asian demand and slow supply growth are likely to support LNG prices over the medium-term. (Gulf-Times.com)

GDI signs QR5.2bn rig service deals with QP – Gulf Drilling

International (GDI), a subsidiary of Gulf International Services (GISS), has signed contracts worth QR5.2bn with Qatar Petroleum (QP) for the provision of onshore and offshore rigs. These contracts include four new contracts and four contract extensions with QP, each having a term of five years. The new

contracts have been concluded for the provision of two new offshore drilling rigs ‘Dukhan’ and ‘Halul’ and two new land rigs GDI-7 and GDI-8. The contract extensions allow the continuation of services performed by four land rigs GDI-1, GDI-2, GDI-3 and GDI-4. GDI’s CEO Ibrahim J. Al-Othman said that these contracts will impact its revenue growth, which will positively reflect on the company’s profitability for 2014 as well as for the next five years. Further, the addition of a new offshore rig for QP – ‘Halul’ in 2016 will greatly support its long-term revenue growth plans. By mid-2016, GDI will have a total of 18 drilling rigs, in addition to one accommodation jack-up and two liftboats. ‘Halul’ and ‘Dukhan’ rigs are expected to be pressed into service in 4Q2014 and 2Q2016, respectively. These contracts have been previously disclosed to investors. We reiterate out price target of QR136.00 and our OUTPERFORM rating on GISS. (Gulf-Times.com, QNBFS Reserach)

Ashghal launches projects in Al Ruwais – According to

sources, the Public Works Authority (Ashghal) has started executing a number of projects in the Al Ruwais area of Al Shamal. The projects include construction of buildings that will house several government offices, a new general hospital, a new health center, three new schools and two nurseries. Further, Ashghal is continuing with the development of the Al Shamal Road, which is part of the expressway program. This includes the construction of service roads along the Al Shamal Road from the northern part of Doha (at Al Duhail Interchange) up to Al Shamal. The project also includes the construction of new intersections in the Izghawa and Umm Salal Mohamed areas, in addition to other enhancement works. (Gulf-Times.com)

QIMD awards consultancy deal to AEB – Qatar Industrial

Manufacturing Company (QIMD) has awarded the consultancy services for its mixed use tower project to Arab Engineering Bureau (AEB), to be located in the West Bay area. The new project includes three towers, joined at the base, planned for hospitality, commercial and residential use. Drawing on its experience as designer of multitude of high-rises in the West Bay area, AEB’s design is highly effective, both in terms of space planning and energy conservation. The podium that connects three towers is intended for a retail space which perfectly complements the 23-storey grade A office tower, 29-storey hospitality hotel tower and 38-storey residential tower. The QIMD tower will offer ample amount of parking bays located at four basement levels. The project valued at QR1bn, with a total build-up area of 120,000 square meters, is slated for completion in 2018. (Gulf-Times.com)

QA to start non-stop services on Doha-Phuket route – Qatar

Airways (QA) will boost services to Thailand with the introduction of non-stop flights to Phuket, effective from October 26, 2014. The airline currently serves the Doha–Phuket route daily via a linked service through the Malaysian capital Kuala Lumpur. The direct flights to Phuket will be operated with an Airbus A330 in a two class-configuration of 24 seats in business class and 236 in economy class. The new non-stop service from October 26 will facilitate shorter travel times for the growing number of tourists to Phuket and for those heading out of Thailand. (Bloomberg)

International

US consumer credit soars in July with biggest gain since 2001 – US consumer credit soared in July, posting its biggest

jump since November 2001, driven in part by demand for auto loans and student borrowings. The Federal Reserve said total consumer credit increased $26.01bn to $3.24tn in July. June's

Page 4 of 7

consumer credit figure was revised up to show an $18.81bn increase from $17.26bn. Economists polled by Reuters had expected consumer credit to increase $17.35bn in July. According to a Fed spokesman, the previous record was an increase of around $28bn recorded in November 2001. That occurred shortly after the September 11, 2001 attacks when big automakers were offering zero-percent financing and other incentives to lure consumers back to their showrooms. (Reuters)

Oil below $100 tightens OPEC budgets, prompts signs of concern – Oil's slide below $100 a barrel on September 8, 2014

adds to financial worries for OPEC members, prompting some in the producer group to voice concern about too much oil in the market even if they see the current fall as short lived. Top OPEC exporter Saudi Arabia favors oil at $100, which many others in the 12-member group also support. An OPEC delegate said prices were under pressure from too much oil, something some member countries were watching. Estimates from the International Monetary Fund indicate that while current prices are comfortable for OPEC's core Gulf members, they are below levels members including Iran, Algeria and Iraq need in 2014 for their fiscal balance to be zero. (Reuters)

BRC: UK retail sales growth accelerates in August –

According to figures from the British Retail Consortium (BRC), surging clothing and footwear sales helped British retail sales accelerate sharply in August. Total retail spending was 2.7% higher than a year ago, up from 1.3% in July. The BRC said this was the best performance since January, excluding the effects of the timing of Easter holidays. Sales on a like-for-like basis – a measure which strips out changes in floor space and is favored by equity analysts – rose 1.3% on the year, beating expectations of a 0.5% rise and up from a 0.3% decline in July. Clothing and footwear sales rose at the strongest pace since December 2011, helped by back-to-school shopping and fashion retailers changing their seasonal collections. But spending on food declined again, marking its deepest three-month average fall since records began in December 2008. (Reuters)

IMF's Lagarde urges Germany to spend more, aid recovery – International Monetary Fund (IMF) head Christine Lagarde has

urged Germany to increase investments to help spur the Eurozone's flagging economic recovery, adding that the bloc as a whole needed to make more structural reforms. With the Eurozone economy in the doldrums, the European Central Bank announced a series of measures on September 4 to stimulate growth, with its president Mario Draghi expanding on a call for governments to support this process with extra spending. Echoing that sentiment, Lagarde said the process could be aided by Germany, which is borrowing at record-low rates and is on track to record a public sector surplus for the third year running. She said IMF thinks that public or private investments in Germany to finance infrastructure would be welcome, stressing this did not mean making the German economy less competitive. She further added that the International Monetary Fund believes that Germany can go a bit further, that it can do a bit more, in the country's interest. (Reuters)

China's August imports fall unexpectedly but exports buoyant – China's import growth unexpectedly fell for the

second consecutive month in August, posting its worst performance in over a year and stoking speculation about whether the authorities should loosen policy further to revive domestic demand. The General Administration of Customs said imports by China fell 2.4% in August compared with a year ago, missing the Reuters estimate for a 1.7% rise. China's import growth was surprisingly weak for the second straight month, raising concerns that the tepid domestic demand exacerbated by a cooling housing market is increasingly weighing on the

economy. In contrast, China's exports were surprisingly buoyant in August amid stronger global demand as it jumped 9.4% from a year earlier to beat a forecast rise of 8%, although the growth rate slowed from 14.5% in July. That pushed the trade surplus to an unexpected all-time high of $49.8bn, which could put further appreciation pressure on the Yuan currency. (Reuters)

Japan second-quarter GDP shrinks 7.1%, adds to doubt over inflation goal – Japan's economy shrank an annualized

7.1% in April-June from the previous quarter, worse than a preliminary estimate, adding to doubts over whether the central bank can achieve its target of 2% inflation early next year. The contraction was the biggest since 1Q2009, when the global financial crisis hit Japan's exports and factory output, and some analysts now expect the economy to barely grow in the current fiscal year to March 2015. The weak performance following a sales tax hike in April will keep the Bank of Japan and Prime Minister Shinzo Abe's government under pressure to expand the fiscal and monetary stimulus in order to lead the economy out of a long deflationary phase. (Reuters)

Regional

Sadeed Investment acquires 30% equity in BRC Industrial (Saudia) – Sadeed Investment Limited has acquired 30% equity

participation in BRC Industrial (Saudia) Ltd. BRC Industrial is Saudi-based steel products manufacturing and processing company, whose revenues are predicted to exceed SR1bn in 2014. Sadeed is a Swicorp and Partners-owned investment vehicle dedicated to make investments in the steel sector in Saudi Arabia. (GulfBase.com)

IDB picks arrangers for USD Sukuk offer – The Jeddah-

based Islamic Development Bank (IDB) has picked nine banks for a potential US dollar-denominated Islamic bond issue. IDB has mandated CIMB, Deutsche Bank, First Gulf Bank, GIB Capital, HSBC, Maybank, Natixis, National Bank of Abu Dhabi, and Standard Chartered Bank as joint bookrunners to arrange investor meetings in the Middle East, Europe and Asia starting on September 11, 2014. IDB will start its roadshows in Kuala Lumpur on September 11, 2014, followed by Abu Dhabi and Dubai on September 14, 2014, Scandinavia and Germany on September 15, 2014, Switzerland on September 16, 2014 and London on September 17, 2014. (Peninsula Qatar)

Al Khodari Sons to diversify into solar and nuclear power –

Abdullah Abdul Mohsin Al Khodari Sons Company (Al Khodari Sons) said that it would diversify into solar power and nuclear energy. The company’s new activities will include supplying and installing solar energy equipment and systems, along with providing contractor services, maintenance and other operations for nuclear energy. (GulfBase.com)

SRECO recommends SR60mn dividend for 1H2014 – Saudi

Real Estate Company’s (SRECO) board of directors has recommended the distribution of 5% dividend (SR0.5 per share), amounting to SR60mn for 1H2014. Shareholders registered with the Securities Depository Center (Tadawul) on September 9, 2014, will be eligible to receive the dividend. (Tadawul)

PC invites shareholders to attend OGAM – Advanced

Petrochemical Company’s board of directors has invited its shareholders to attend the Ordinary General Assembly Meeting (OGAM) with the agenda to approve issuance of Sukuk in compliance with Shari’ah principles. The company’s BoD seeks approval on the various aspects of Sukuk issuance, as well as to authorize the BoD to take all necessary measures to issue such Sukuk, once the necessary approvals from the relevant authorities have been received. (Tadawul)

Page 5 of 7

Saudi CMA approves ICC’s capital rise – The Saudi Capital

Market Authority’s (Saudi CMA) board of commissioners has approved Itqan Capital Company’s (ICC) request to increase its capital from SR73.42mn to SR173.42mn. (Tadawul)

SKFH receives CMA approval to launch fund – The Saudi

CMA’s board of commissioners issued its resolution providing approval for Saudi Kuwaiti Finance House Company (SKFH) to offer its Baitk AlWaed Saudi Equity Fund. (Tadawul)

AFRE secures $1bn loan for Doha venture – Al Futtaim

Group Real Estate (AFRE) has secured a $1bn loan facility for the Doha Festival City development. Now, AFRE has begun the process to secure funding support for its Riyadh project as well as the major expansion at Dubai Festival City. (Bloomberg)

Vela vessels transferred to Bahri's ownership – The National

Shipping Company of Saudi Arabia (Bahri) announced that ‘Pisces Star’, a VLCC vessel in the Vela fleet, has been transferred to Bahri's ownership on September 8, 2014, and its name was changed to ‘Hilwah’. This marks the completion of transferring the ownership of six vessels from Vela to Bahri. The remaining Vela vessels shall be transferred to Bahri on a staggered basis as per the vessel delivery schedule, which is expected to be completed before the end of 2014. (Tadawul)

UAE credit bureau starts issuing consumer data to banks –

Al Etihad Credit Bureau in United Arab Emirates has begun issuing credit information about consumers to banks and financial institutions in an effort to strengthen the country's banking industry. Until now, banks in the UAE have often been unable to access data on consumers at other financial institutions when making lending decisions. This has allowed borrowers to obtain money from many lenders and run up big debts which sometimes prove impossible to repay. The credit reports include consumers' debt obligations and payment behavior patterns for the past two years. (Reuters)

Etihad Rail signs MoU with GIBCA Crusher – Etihad Rail has

signed a MoU with GIBCA Crushing & Quarry Operations Company (GIBCA Crusher). The agreement will ensure the efficient delivery of raw materials to distribution and export terminals throughout the country. Under the MoU, Etihad Rail will transport stone aggregates for Gibca Crusher from its quarry in Ras Al-Khaimah to distribution terminals in Jebel Ali, ICAD Cities I and IV, Ruwais, Saqr Port, and Fujairah Port. (GulfBase.com)

DEWA shortlists 8 firms for clean coal power plant – The

Dubai Electricity & Water Authority (DEWA) has shortlisted eight companies to build a 1,200 megawatt (MW) clean coal power plant, which is part of a $20bn investment that aims to help in diversifying the Emirate’s energy mix by 2030. Dubai produces very little oil and relies mostly on costly imports of gas to satisfy its growing energy consumption. DEWA has also put out a tender for the construction of a 100-megawatt independent solar power project (IPP). DEWA has shortlisted 24 companies for this solar project and hopes to evaluate bids by the end of October 2014. (GulfBase.com)

Dubai FDI to attract global hospitality players – Dubai

Investment Development Agency (Dubai FDI) in the Department of Economic Development (DED) is making a strong bid to bring more global hospitality operators into the Emirate. With Dubai expecting to attract 20mn tourists by the end of the decade, investment in hospitality infrastructure and services is a top priority for the government. Dubai’s hotels welcomed more than 11mn guests in 2013, an increase of one million on 2012 figures and an indication that Dubai is on track to achieve its 2020 visitor target. (GulfBase.com)

Tebyan, Swarovski partner for Sparkle Towers at Dubai Marina – Dubai-based property developer, Tebyan has signed a

partnership agreement with Austria-based Swarovski to create a unique crystal-inspired Sparkle Towers at Dubai Marina. Branded as ‘Space Marveled by Swarovski’, the ultra-luxurious resort-style residential project is unique due to its exquisite crystal-themed innovations, ranging from the sparkling lighting solutions and crystal interiors. The project consists of two towers with 29 floors and 14 floors, which are connected by a residential podium. (GulfBase.com)

Samsung Group merger not to affect Arabtec’s JV – Arabtec

Holding stated that the merger between Samsung Engineering and Samsung Heavy Industries (Samsung Group) will not affect the joint venture (JV) between Samsung Engineering and Arabtec Holding. Consequently, the merger will not have any impact on Arabtec’s financials or its operations. (DFM)

Dubai to spend $32bn on Al Maktoum airport expansion –

Dubai will spend $32bn on expanding Al Maktoum International Airport to handle over 200mn people annually next decade, roughly triple the current level of passenger traffic. Al Maktoum currently has a capacity of only about 5mn people per year. Dubai Airports stated on September 8, 2014 that Dubai's ruler Sheikh Mohammed bin Rashid al-Maktoum has approved plans to enlarge Al Maktoum, whose expansion would take place in two phases over 6-8 years, and will be developed over an area covering 56 square kilometers. However, Dubai Airport officials have not said how they will fund the project. (Reuters)

ICD to buy $300mn stake in Nigeria's Dangote Cement – The

Investment Corp of Dubai (ICD) has agreed to acquire a $300mn stake in Nigerian cement producer, Dangote Cement. Dangote's current market capitalization is about $23.7bn, which means ICD would take a stake of about 1.3%. (Reuters)

Hill International wins AED186.9mn Dubai Parks contract –

US-based Hill International has received a contract from Meraas Leisure & Entertainment to provide show & ride construction management consultancy services for Phase I of the Dubai Parks development in Dubai. The two-year contract has an estimated value of approximately AED186.9mn. The entire AED9.5bn Dubai Parks development will be a 30mn square-foot leisure complex, which will feature numerous theme parks, hotels, retail, dining and entertainment facilities in the Jebel Ali region of Dubai, as well as an inner-city family entertainment center with retail and dining facilities in the Satwa region of Dubai. (Bloomberg)

OPWP to extend PPAs with existing IPPs – Oman Power &

Water Procurement Company (OPWP) is about to complete the process of extending power purchase agreements (PPAs) with some independent power projects (IPPs), which are going to expire before 2018. The contract extensions, which include Al Kamil Power and Barka 1, are expected to be completed before 2014-end. The extension is subject to regulatory approvals and an agreement on commercial terms. Earlier in 2014, OPWP had initiated discussions with the plant owners at Al Kamil and Barka 1, Ghubrah and Wadi Jizzi for extending contracts until 2020. Apart from extending PPAs with existing IPPs, OPWP authorities also expect additional generation from a Sur IPP and another mega plant. (GulfBase.com)

NCSI: Oman’s inflation stands at 0.63% in July 2014 –

According to a report by the National Centre for Statistics & Information (NCSI), Oman’s annual rate of inflation stood at 0.63% in July 2014, while the rate increased by 0.25% on a MoM basis. The report details price rises in various segments and other commodities & services. Prices in housing & utility rose by 1.39%, education rose by 6.27%, healthcare (5.72%),

Page 6 of 7

communications (0.12%), furniture, household items & regular maintenance (7.28%), restaurants & hotels (0.88%), tobacco (0.34%), culture & leisure (0.41%), and miscellaneous goods & services (0.05%) on a YoY basis. Alternatively, price declines for food & non-alcoholic beverages by 0.03%, while prices for clothes & footwear fell by 0.07%, and transportation costs by 1.17% on a YoY basis. (GulfBase.com)

Glasspoint receives $53mn financing – US-based Glasspoint

Solar, a producer of solar equipment used for enhanced oil recovery, has received $53mn from a group of investors led by Royal Dutch Shell and Oman’s largest sovereign wealth fund. Existing investors Chrysalix Energy Venture Capital, Nth Power and Rockport Capital also contributed to the equity round. These funds will be used to accelerate the deployment of Glasspoint’s solar-steam generators in Oman. (Bloomberg)

Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

[email protected] [email protected] [email protected]

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 [email protected] [email protected] Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*Market closed on 08 September 2014)

80.090.0

100.0110.0120.0130.0140.0150.0160.0170.0180.0190.0200.0210.0

Aug-10 Aug-11 Aug-12 Aug-13 Aug-14

QE Index S&P Pan Arab S&P GCC

0.1%

0.6%

(0.1%)(0.3%)

(0.1%)

0.5%

1.1%

(0.5%)

0.0%

0.5%

1.0%

1.5%

Saud

i Ara

bia

Qata

r

Kuw

ait

Bah

rain

Om

an

Abu D

habi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,255.44 (1.1) (1.1) 4.1 DJ Industrial 17,111.42 (0.2) (0.2) 3.2

Silver/Ounce 19.03 (0.9) (0.9) (2.3) S&P 500 2,001.54 (0.3) (0.3) 8.3

Crude Oil (Brent)/Barrel (FM Future)

100.20 (0.6) (0.6) (9.6) NASDAQ 100 4,592.29 0.2 0.2 10.0

Natural Gas (Henry Hub)/MMBtu

3.85 0.3 0.3 (11.3) STOXX 600 346.09 (0.4) (0.4) 5.4

LPG Propane (Arab Gulf)/Ton 106.38 0.7 0.7 (15.9) DAX 9,758.03 0.1 0.1 2.2

LPG Butane (Arab Gulf)/Ton 125.25 (0.4) (0.4) (7.7) FTSE 100 6,834.77 (0.3) (0.3) 1.3

Euro 1.29 (0.4) (0.4) (6.2) CAC 40 4,474.93 (0.3) (0.3) 4.2

Yen 106.03 0.9 0.9 0.7 Nikkei 15,705.11 0.2 0.2 (3.6)

GBP 1.61 (1.4) (1.4) (2.7) MSCI EM 1,094.99 (0.2) (0.2) 9.2

CHF 1.07 (0.5) (0.5) (4.6) SHANGHAI SE Composite* 2,326.43 0.0 0.0 9.9

AUD 0.93 (1.0) (1.0) 4.1 HANG SENG 25,190.45 (0.2) (0.2) 8.1

USD Index 84.23 0.6 0.6 5.2 BSE SENSEX 27,319.85 1.1 1.1 29.0

RUB 36.96 (0.2) (0.2) 12.4 Bovespa 59,192.75 (2.5) (2.5) 14.9

BRL 0.44 (1.1) (1.1) 4.2 RTS 1,245.53 (0.9) (0.9) (13.7)

200.7

170.0

152.4