79F64d01

22

Rio Tinto Alcan Financial community site visit 20 September 2009

-

Upload

mythos1976 -

Category

Documents

-

view

218 -

download

0

Transcript of 79F64d01

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 1/22

Rio Tinto AlcanFinancial community site visit

20 September 2009

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 2/22

20 September 2009 2009 North America Financial Community Site Tour 2

Phillip Strachan

Chief Financial Officer, Rio Tinto Alcan

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 3/22

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 4/22

20 September 2009 2009 North America Financial Community Site Tour 4

Cost init iatives

Modelling the business

Synergies and integration

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 5/22

20 September 2009 2009 North America Financial Community Site Tour 5

• Benefits tracking ahead of target, primarily due to procurement savings

• Continue to remain on track to deliver US$1.1 billion in 2010

• Total synergy program one-off capital and operating integration costs have been

significantly reduced at US$130 million and US$191 million compared to targets of US$541 million and US$245 million respectively

• Third-party audit recently completed covered 56% of in-period EBITDA and confirmeda robust process with no material adjustments

H1 2009 in-period net earnings from synergies of

US$483 million exceeded target by 28%

*Synergy Net Earnings include in-period one-time operational expenditures (like severance & relocation costs)

Target

Actual

170

251 252

334

378

483

418

500

600

H1 2008 H2 2008 H1 2009 H2 2009 H1 2010 H2 2010

$1.1 bil lion in 2010

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 6/22

20 September 2009 2009 North America Financial Community Site Tour 6

0

100

200

300

400

500

483

H1 2009

synergies

(14)

Prior

yr adj

(97)

Cost

avoidance

(27)

Exchange

rates

24*

One off

(130)

Rio Tinto Corporate

239**

H1 2009

impact on earnings

US$millions

Rio Tinto Alcan in-period synergies

within underlying earnings

* One-off costs relate to implementation costs which are not included in underlying earnings

** US$73 million of the 2009 savings were first realised in 2008, i.e. they were not incremental

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 7/22

20 September 2009 2009 North America Financial Community Site Tour 7

0 %

5%

10%

15%

2 0 %

2 5%

2008A

H1

2008A

H2

2009A

Q1

2009A

Q2

2009F

Q3

2009F

Q4

GoveWeipa

Gladstone

Mono- Bauxite

Export Bauxite

Weipa/Gove bauxite grade strategy

• Coordinating Gove and Weipa bauxite mining outputs maximises opportunities to lower

caustic usage at Gladstone refineries

• Benefit achieved through optimising output of bauxite from Weipa’s Andoommine

• Synergy result: US$2.2 million EBITDA in period H109, ramped up to US$3.4 million in 2010

Reduced production input costs

Acquisit ion generatesmine plan strategy optimisation

Caustic soda efficiencies

Caustic consumption reductions

% H 1

2 0 0 8

Actual / Forecast

Plan

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 8/22

20 September 2009 2009 North America Financial Community Site Tour 8

• Optimise operating strategy to leverage significant caustic efficiencies

• Focus on improvements to reduce process caustic usage

• Cross refinery initiatives on washers including improved tank turnaround time and process control

• Operational optimisation continues as benchmarking, best practices, procurement and supply chain

benefits are shared with our other north eastern Australian refineries and bauxite mines

• Synergy result: US$3.4 million in period H109, ramping up to US$27 million annually

Gove caustic initiatives

Integrated technical team reviews strategic caustic program andidentifies improvement opportunities at Gove

Caustic consumption

125

130

135

140

145

150

155

160

2008 Q1 Q2 H1 09

K g / t A l

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 9/22

20 September 2009 2009 North America Financial Community Site Tour 9

US$65 million synergies recorded by Primary

Metal in North America by Q2 for 2009

•Re-focusing of synergy efforts to efficiency and productivity has replaced many deferred projects

•Only value considered sustainable beyond the synergy timelines (and market recovery) has beencounted in the quoted benchmarking and productivity synergies

Specif ic measures

US$28 million from benchmarking and productivity improvements

Primary Metal North America2009 Synergy Results

US$ millions • Approximately half of US$100 million

total synergies forecast in 2010 focus on

sustainable productivity improvements

• Structural changes and rapid response to

market conditions leave us better

positioned to capitalise on top-tier growth

opportunities when markets recover

• Gains above original target; a major

contributor to global Primary Metal

synergies

0

10

20

30

40

50

60

70

80

90

100

110

Q1 09 Q2 09 H1 09 H2 09 FY 09

Plan Actual or Forecast

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 10/22

20 September 2009 2009 North America Financial Community Site Tour 10

Cost init iatives

Modelling the business

Synergies and integration

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 11/22

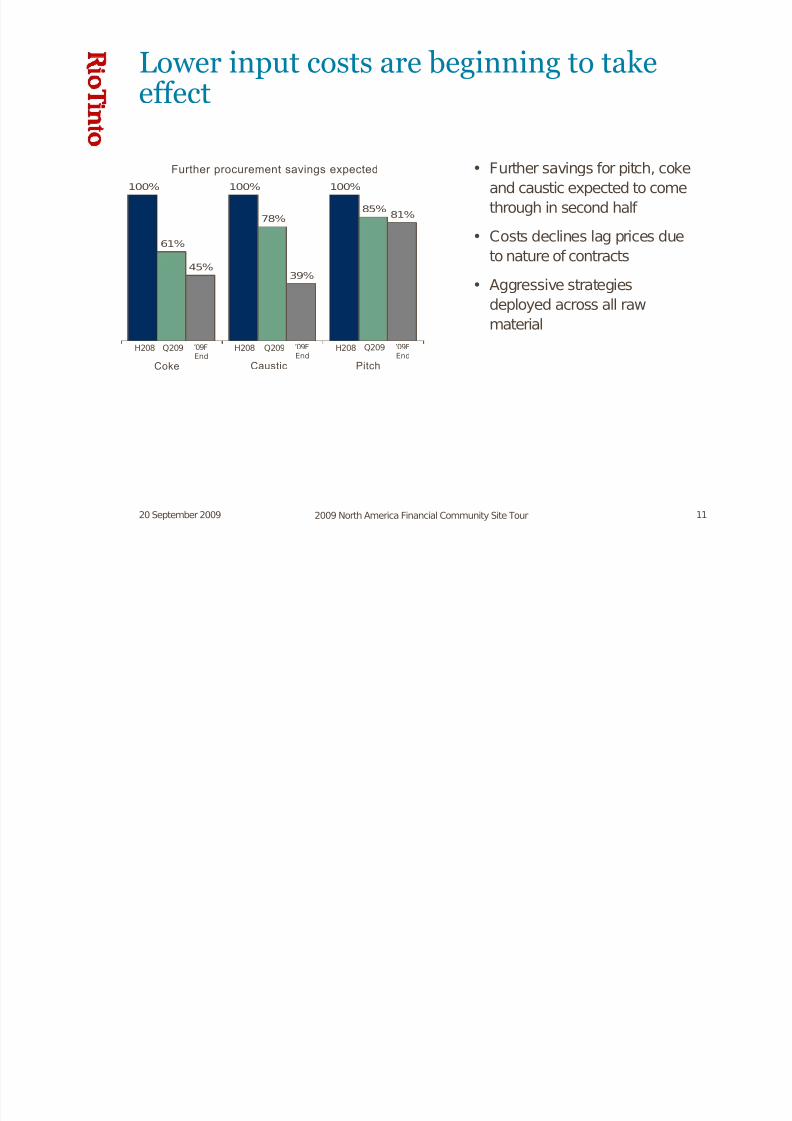

20 September 2009 2009 North America Financial Community Site Tour 11

Lower input costs are beginning to take

effect

• Further savings for pitch, coke

and caustic expected to come

through in second half

• Costs declines lag prices due

to nature of contracts

• Aggressive strategies

deployed across all raw

material

100%100%100%

85%

78%

61%

81%

39%45%

Coke Caustic Pitch

H208 Q209 ’09FEnd

H208 Q209 ’09FEnd

H208 Q209 ’09FEnd

Further procurement savings expected

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 12/22

20 September 2009 2009 North America Financial Community Site Tour 12

Leveraging the operational flexibility of the

business

Total cost equivalent reduction of US$85 per tonne, pre tax

• Energy sales from curtailment

• Sales from carbon products manufacturing

• Technology and infrastructure sales

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 13/22

20 September 2009 2009 North America Financial Community Site Tour 13

Capital initiatives generating significant

savings

2417

586 500

1108

2008 Actual 2009 Forecast 2010 Target

Significant reduct ion in CapitalExpenditures (US$ millions)

GrowthSustaining

• Driving down capex in 2009

• Evaluating growth capex for

2010

• Prioritising use of capital

• Keeping focus on the

reliability of our plants

This does not include 2010 growth capital which remains under evaluation

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 14/22

20 September 2009 2009 North America Financial Community Site Tour 14

80%100%

2008 2009 Forecast

SG&A and capital initiatives generating

significant savings

SG&A down 20% in 2009

2310

(77%)

2530

(85%)

2988(100%)

H1 2008 H2 2008 H1 2009

Trade Working Capital reduction(US$ millions)

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 15/22

20 September 2009 2009 North America Financial Community Site Tour 15

Cost init iatives

Modelling the business

Synergies and integration

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 16/22

20 September 2009 2009 North America Financial Community Site Tour 16

Rio Tinto Alcan’s aluminium pricing

tracking closely to spot prices in 2009

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09

US$/t (lines)

• 2009 first half average LMEprice was US$1,422 per

tonne, a decline of 50% on

H1 2008

• Pricing of aluminium has an

LME price mix on average of

• 55% spot

• 45% one month

Aluminium spot price

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 17/22

20 September 2009 2009 North America Financial Community Site Tour 17

27% 27%29%

43%

51%48%

0%

25%

50%

75%

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09

% of Remelt volume vs. total sales volume (bars) • Percentage of remelt sales nearly

doubled in H1 2009 vs. H1 2008

with premia down almost 30%

• Continuing signs of steady value

added product recovery in North

America and Asia Pacific, withencouraging signs emerging in

Europe

• With market recovery will expect

value added volumes to return to

historical levels

Remelt sales nearly double in H1 2009

versus H1 2008 but volumes are returning

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 18/22

20 September 2009 2009 North America Financial Community Site Tour 18

Premiums are showing signs of recovery

North

America

42%

Europe

24%

Asia Pacific34%

• Includes two components: market premium and product premium

• Market premium varies by region

• Product premium varies by product but on average is about US$180 per tonne

• Overall, net value added premium is around 3.4% above average 2008 LME

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2003 2004 2005 2006 2007 2008 2009

L o c a l M

a r k e t P r e m i u m s ( $

/ t o n n e )

Europe 3M DPPJapanMidwest

Source: Platts Metals Week

Cut in EU dutyto 3% from 6%

Local market premiumsH109 aluminium sales by region

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 19/22

20 September 2009 2009 North America Financial Community Site Tour 19

Key raw material prices have a lag effect

33%

21%

21%

24%14%

32% 32%

23%

0%

20%

40%

60%

80%

100%

Alumina Alumin ium

Other Other

Bauxite Alumina

Energy

Energy

Caustic

Carbon

Aluminium

• Coke and pitch generally have

three to five month lag due tothe pricing (mostly semi-

annual) and days of inventory

• Alumina (two to five month lag)

• 16% of energy LME linked tothree-month

Alumina

• Caustic lag is generally one totwo months

• Fuel oil one to two month lag

Source: CRU

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 20/22

20 September 2009 2009 North America Financial Community Site Tour 20

Sensitivities

71+/-8.3USc83UScCanadian dollar

29+/-1.3USc134UScEuro

107+/-7.1USc71USc Austral ian dollar

399+/- $142/t$1,422/t Aluminium

Effect on Rio Tinto Alcan ful l year

underlying earnings (US$ millions)

10% change

Averageprice/exchange

rate for 2009 firsthalf

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 21/22

20 September 2009 2009 North America Financial Community Site Tour 21

Conclusions

• On track to deliver US$1.1 billion in integration synergies

• Focus on margin improvement

– Hold cost improvements to date

– Further cost compression opportunities

– Market recovery flow through

• Will continue to manage cash into 2010

– Capital, working capital, operations

• Good financial discipline, control and governance

Benefits of actions wi ll continue to flow through in years to come

7/28/2019 79F64d01

http://slidepdf.com/reader/full/79f64d01 22/22

20 September 2009 2009 North America Financial Community Site Tour 22

Questions?