7 FAQs about the CFPB's Consumer Complaint Database

12

© 2015 TRUPOINT Partners 7 FAQs about the CFPB’s Complaint Database 1 Quick Answers to Seven of Your Most Common Questions

-

Upload

trupoint-partners -

Category

Economy & Finance

-

view

166 -

download

1

Transcript of 7 FAQs about the CFPB's Consumer Complaint Database

© 2015 TRUPOINT Partners

7 FAQs about the CFPB’s Complaint

Database

1

Quick Answers to Seven of Your Most Common Questions

© 2015 TRUPOINT Partners

1. How is a Complaint Defined?

• Complaint is defined as “a written expression of dissatisfaction with or allegation of wrongdoing by a provider or any financial product or service or any entity subject to regulation or supervision by the Bureau or a Prudential Regulator made by a Consumer (including a representative acting on behalf of a Consumer),” according to a memo of understanding between the CFPB and the OCC.

• N.B. TRUPOINT has reached out to the CFPB to provide clarity on whether complaints must be written, or whether complaints by telephone are also considered. We will update this document with new information when we’ve received it.

• In contrast, “Inquiry” is defined as “a question posed by a Consumer to either of the Parties regarding Federal Consumer Financial Law or a Consumer Financial Product or Service that is not part of a Complaint.”

2

Source: “Memorandum of Understanding By and Between the Consumer Financial Protection Bureau and the Office of the Comptroller of the Currency”; 2011: http://www.bsnlawfirm.com/news/OCC-CFPB-MOU%20on%20complaints.pdf

© 2015 TRUPOINT Partners

2. How Will I Know If There’s a CFPB Complaint About My Organization?

• The Office of Consumer Response, which handles consumer complaints, will screen the complaint for completion and determine if it should be sent to another regulator.

• Screened complaints are forwarded via a secure web portal to the identified company.

• N.B. TRUPOINT has also reached out the CFPB to learn more about the “secure web portal,” as well as who at the financial institution would receive the notification.

• Complaints are only forwarded to companies when they contain the required fields, including the complaint narrative, the consumer’s requested resolution and the consumer’s contact information.

3

Source: “Disclosure of Consumer Complaint Narrative Data”; 2014: http://files.consumerfinance.gov/f/201503_cfpb_disclosure-of-consumer-complaint-narrative-data.pdf

© 2015 TRUPOINT Partners

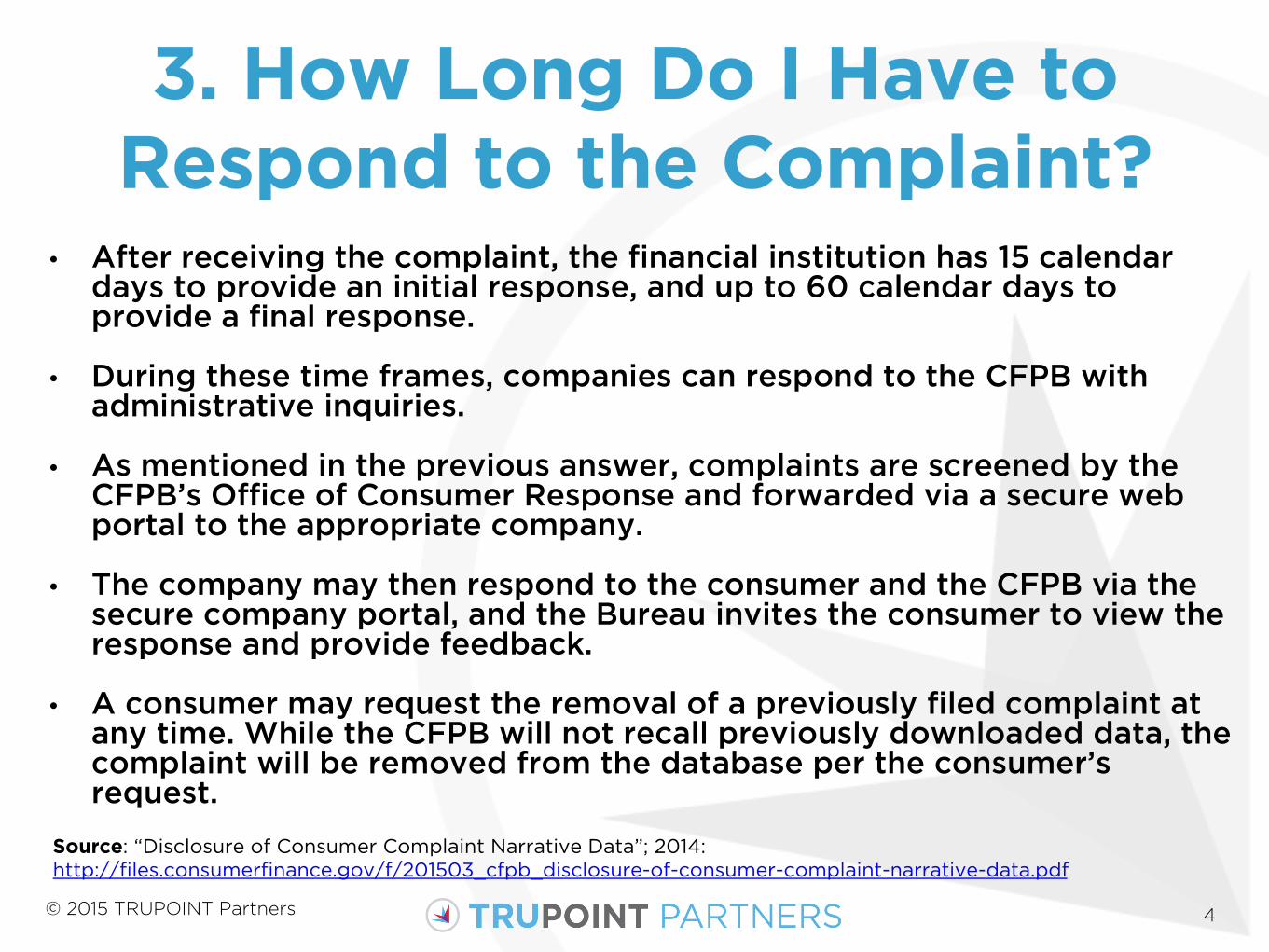

3. How Long Do I Have to Respond to the Complaint?

• After receiving the complaint, the financial institution has 15 calendar days to provide an initial response, and up to 60 calendar days to provide a final response.

• During these time frames, companies can respond to the CFPB with administrative inquiries.

• As mentioned in the previous answer, complaints are screened by the CFPB’s Office of Consumer Response and forwarded via a secure web portal to the appropriate company.

• The company may then respond to the consumer and the CFPB via the secure company portal, and the Bureau invites the consumer to view the response and provide feedback.

• A consumer may request the removal of a previously filed complaint at any time. While the CFPB will not recall previously downloaded data, the complaint will be removed from the database per the consumer’s request.

4

Source: “Disclosure of Consumer Complaint Narrative Data”; 2014: http://files.consumerfinance.gov/f/201503_cfpb_disclosure-of-consumer-complaint-narrative-data.pdf

© 2015 TRUPOINT Partners

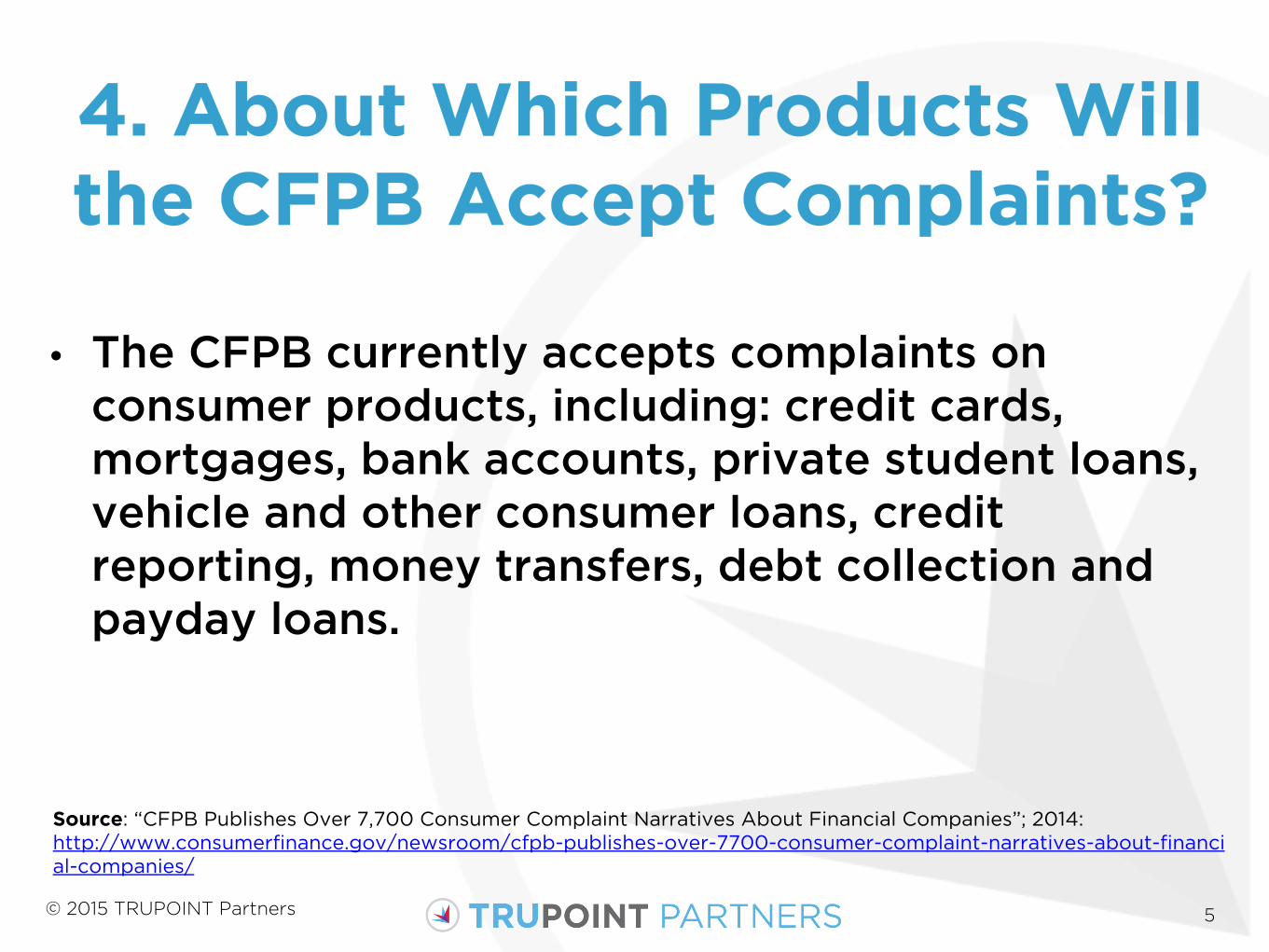

4. About Which Products Will the CFPB Accept Complaints?

• The CFPB currently accepts complaints on consumer products, including: credit cards, mortgages, bank accounts, private student loans, vehicle and other consumer loans, credit reporting, money transfers, debt collection and payday loans.

5

Source: “CFPB Publishes Over 7,700 Consumer Complaint Narratives About Financial Companies”; 2014: http://www.consumerfinance.gov/newsroom/cfpb-publishes-over-7700-consumer-complaint-narratives-about-financial-companies/

© 2015 TRUPOINT Partners

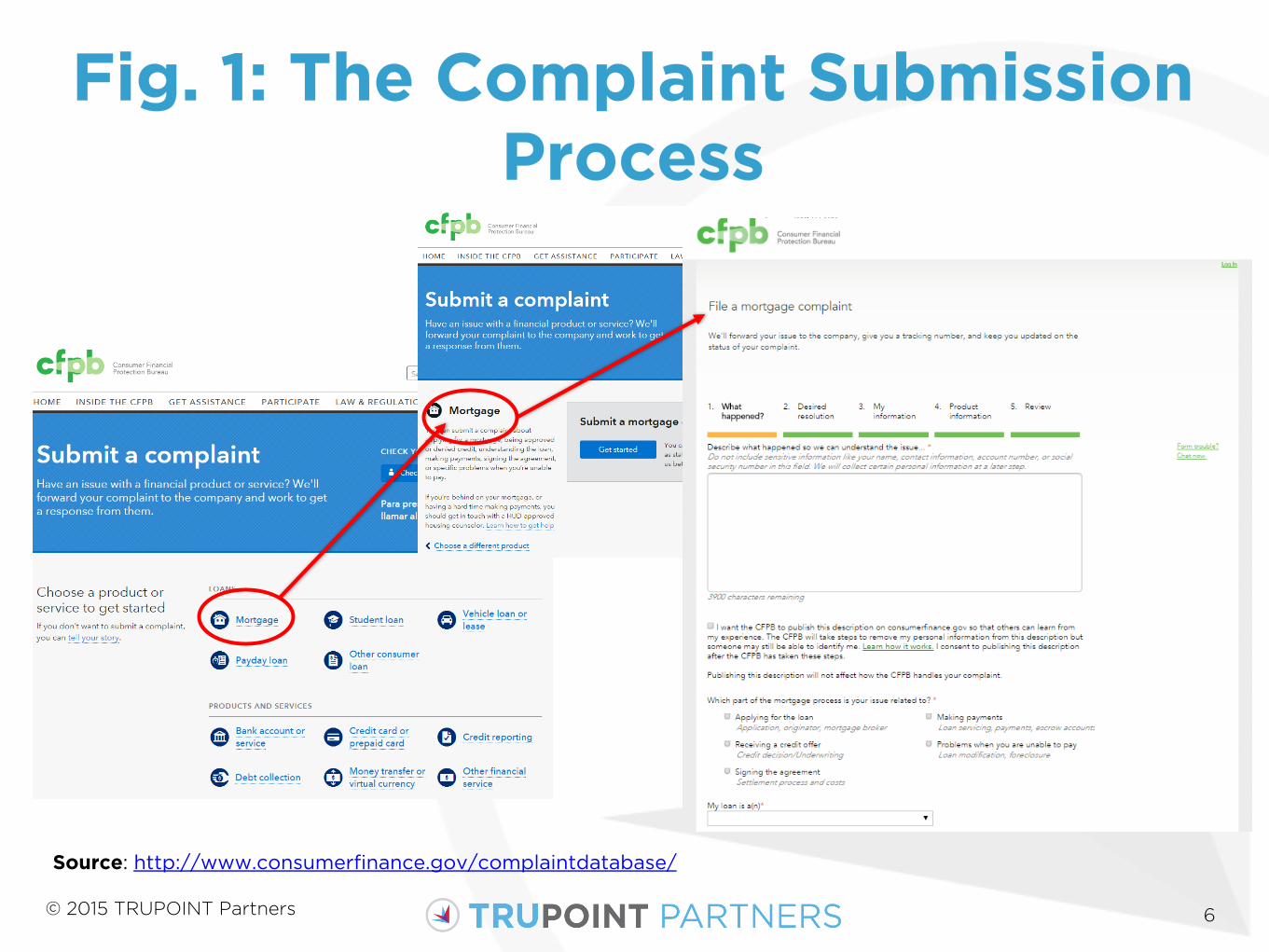

Fig. 1: The Complaint Submission Process

6

Source: http://www.consumerfinance.gov/complaintdatabase/

© 2015 TRUPOINT Partners

5. How Does the CFPB Decide What to Publish?

• First, the Consumer must opt in to having their narrative published publically.

• The CFPB doesn’t verify the accuracy of the facts alleged in the complaints, but they do “take steps” to confirm a commercial relationship between the consumer and the company.

• Complaints are reviewed, or screened, by the Office of Consumer Response to determine if they should be routed to another regulator, or whether each submission is a complaint, inquiry or feedback. Only complaints are forwarded to the identified company for handling as complaints.

• The Bureau also verifies that the complaint is submitted by the identified consumer or his/her authorized representative.

• The complaint is published after the identified company has had the complaint for 15 calendar days, or after they have provided an initial response (whichever comes first).

7

Source: “Disclosure of Consumer Complaint Narrative Data”; 2014: http://files.consumerfinance.gov/f/201503_cfpb_disclosure-of-consumer-complaint-narrative-data.pdf

© 2015 TRUPOINT Partners

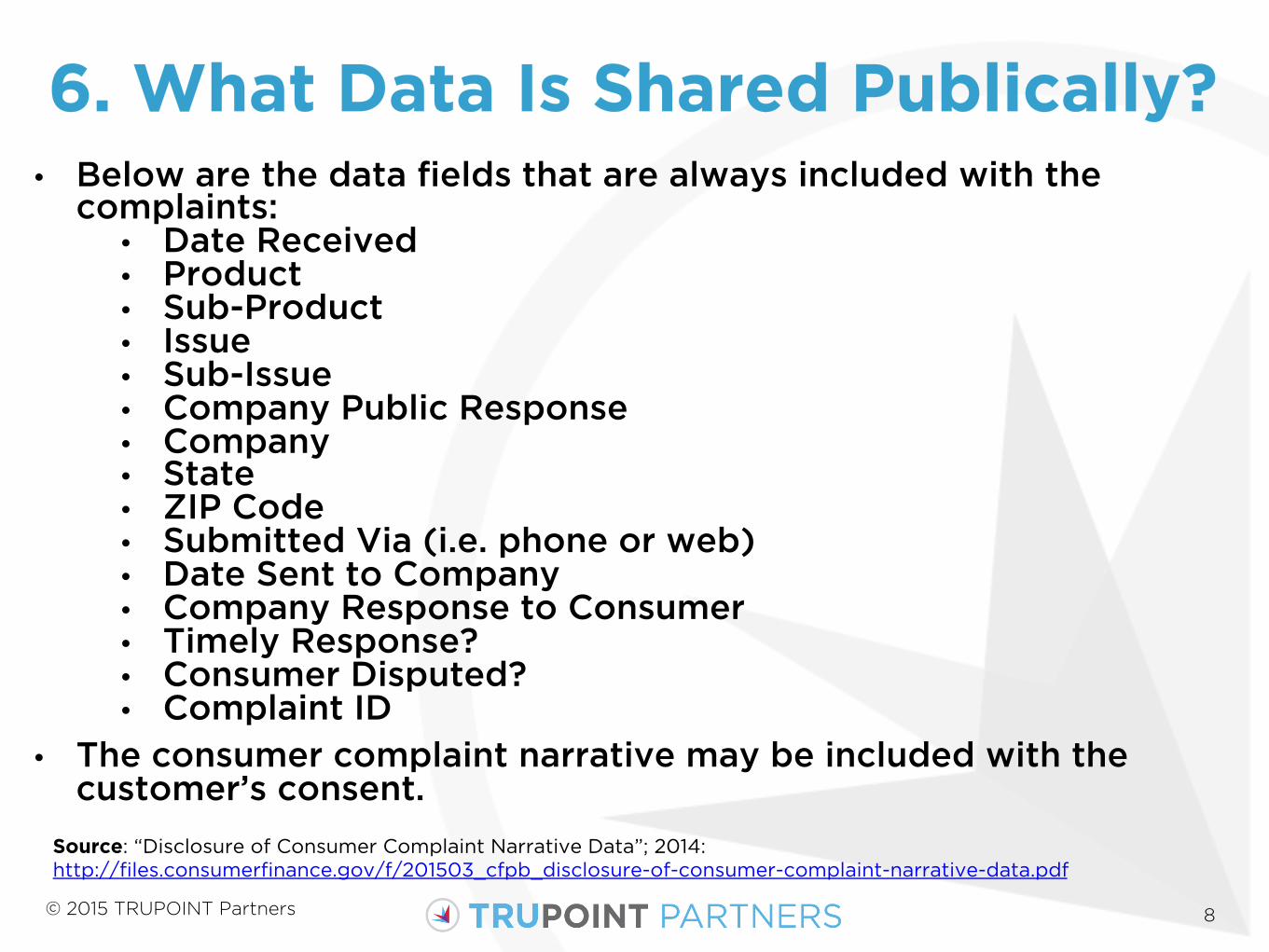

6. What Data Is Shared Publically? • Below are the data fields that are always included with the

complaints: • Date Received • Product • Sub-Product • Issue • Sub-Issue • Company Public Response • Company • State • ZIP Code • Submitted Via (i.e. phone or web) • Date Sent to Company • Company Response to Consumer • Timely Response? • Consumer Disputed? • Complaint ID

• The consumer complaint narrative may be included with the customer’s consent.

8

Source: “Disclosure of Consumer Complaint Narrative Data”; 2014: http://files.consumerfinance.gov/f/201503_cfpb_disclosure-of-consumer-complaint-narrative-data.pdf

© 2015 TRUPOINT Partners

Fig. 2: The Complaint Database

9

Source: http://www.consumerfinance.gov/complaintdatabase/

© 2015 TRUPOINT Partners

7. How Do Companies Respond to Complaints?

• When a Consumer consents to having their narrative published publically, the identified company will have the opportunity to submit a structured response for inclusion with the published narrative.

• The Bureau provides a finite list of optional structured responses from which companies can choose. These structured responses are intended to reduce compliance risk and potential negative interpretations associated with narrative company responses.

• The Bureau notes that although the structured responses are intended to make it easier to respond to consumers while remaining compliant, ultimately, companies are responsible for compliance with all federal regulations regarding consumer privacy, etc.

• Companies will have the opportunity to respond both privately to consumers and publically to the database.

• The CFPB staff may review complaints, company responses and consumers’ feedback to prioritize any complaints for investigation or enforcement action.

10

Source: “Disclosure of Consumer Complaint Narrative Data”; 2014: http://files.consumerfinance.gov/f/201503_cfpb_disclosure-of-consumer-complaint-narrative-data.pdf

© 2015 TRUPOINT Partners

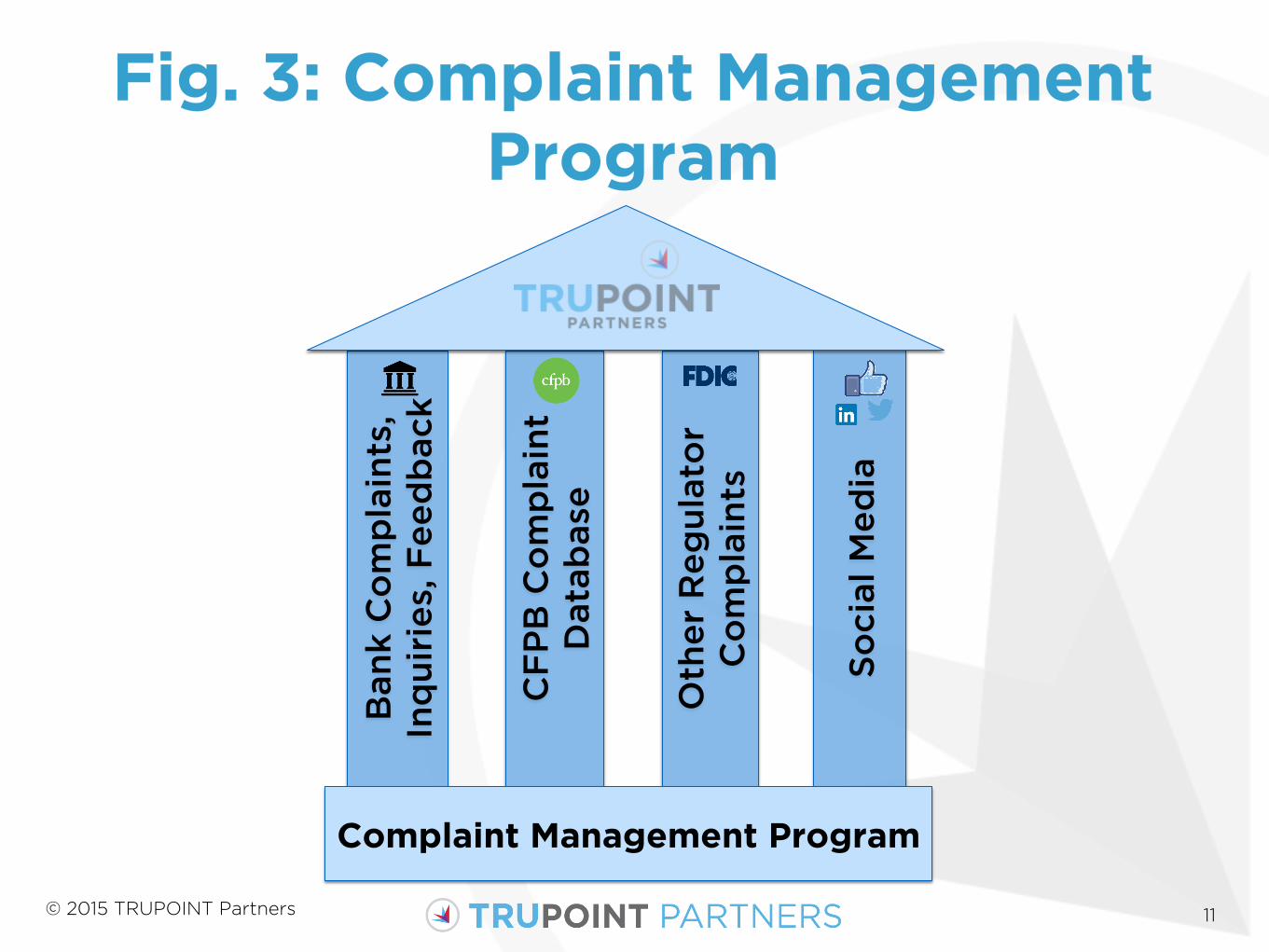

Fig. 3: Complaint Management Program

11

So

cial M

ed

ia

Oth

er

Re

gu

lato

r

Co

mp

lain

ts

C

FP

B C

om

pla

int

Data

base

Ban

k C

om

pla

ints

, In

qu

irie

s, F

ee

db

ack

Complaint Management Program

© 2015 TRUPOINT Partners

TRUPOINT Partners

12

TRUPOINT Partners provides regulatory compliance data analysis and consulting

services to more than 500 financial institutions nationwide. We specialize in Fair Lending /

HMDA, CRA, BSA/AML, and UDAAP.

704.401.1730 www.trupointpartners.com / [email protected]