6HSWHPEHU )W /DXGHUGDOH · 2016-06-18 · x"AICPA Experts, Premier Federal Tax Update," AICPA x"Al...

49

Transcript of 6HSWHPEHU )W /DXGHUGDOH · 2016-06-18 · x"AICPA Experts, Premier Federal Tax Update," AICPA x"Al...

RandeeAbramsonJaime AngaritaAlan CampbellBethany Carr

Lynn ClementsRichard Dotson

Lucinda GallagherWendy Johnson

Thomas LongmanJames LuffmanWilliam MaloneyRoger Michels

Christine MorenoMario Nowogrodzki

Pat PattersonRobert RankinRichard Shapiro

Poornima Srinivasan

Albert GrassoOf Counsel/Chuhak & Tecson, P.C.

Christine M. Moreno, CPA, Esq.,JDChristine M Moreno, Attorney, PA

Frederick G. Spoor, CPA/PFSSpoor & Associates, PA

Health Care Reform: Your Questions - My Answers

Albert Grasso

Albert GrassoOf Counsel

Chuhak & Tecson

Albert Grasso, former Chuhak & Tecson president and now in an Of Counsel position with the firm, headed the tax practice and co-chaired the ERISA practice.Al lectures nationally for the American Institute of CPAs and other groups on tax and employee benefits. He is past chairman of the American Management Association's National Conference on Employee Benefits.

Textbooks written by Al are used nationwide by other professionals to understand the constantly changing tax and pension laws, and he is a member of the advisory board for "The Accountant's Business Manual."

Al has been recognized as both a Leading Lawyer in the tax and employee benefits areas and as an Illinois Super Lawyer in tax matters.

"AICPA Experts, Premier Federal Tax Update," AICPA"Al Grasso's Tax Briefs, Tax Planning for Closely Held Businesses," AICPA"Compensation Issues in Not-For-Profit Organizations," AICPA"S Corporation or Limited Liability Company," Journal of Taxation"Tax Reform Act of 1986: Pension and Deferred Compensation Plans," Prentice-Hall"Retirement Planning," Federal Tax Workshops, Inc."Compensating Employees of Tax-Exempt Organizations," Illinois CPA Foundation"Unrelated Business Taxable Income," Illinois CPA Foundation

"Tax Reform Act of 1986," AICPA, 1986"1987/1988 Annual Tax Update," AICPA, 1987"Tax Planning Issues After TRA '86," AICPA, 1987"Partnerships - Taxable Income and Distributive Shares," BNA Tax Management Portfolio 282-2nd, 1982"TAMRA-Technical Corrections Topics," AICPA, 1988"Mastering the Tax Season," AICPA, an annual update, 1988 to 1994"Closely Held Corporations," Practitioners Pub. Co.

There is no PowerPoint presentation for this session.

Estate Tax Update

Christine M. Moreno, CPA, PA

Christine M. MorenoAttorney- CPA

Our presenter, Christine M. Moreno, is both an Attorney and CPA, whose presentation will be on the use of §1031 Exchanges during challenging economic conditions.

Since 1985 Christine has been a frequent presenter in the area of §1031 like-kind exchanges, appearing before the Florida Real Estate Exchangors, Northside Brokers, the FICPA and various local FICPA Chapters. Christine is a Past President and current Board Member of the FICPA Gold Coast Chapter, and looks forward to discussing with fellow CPAs new ideas in structuring real estate transactions.

A native of Florida, schooled in Florida, and living in Florida, Christine has been a practicing attorney and CPA for over 25 years. Although Christine does not prepare tax returns, she does provide tax consultations, and collaborates with various CPAs in providing services to clients in real estate, corporate, and probate matters.

In 1989 Christine was elected and served as Mayor of the City of North Miami. Christine is past president of the Hobe Sound Port Salerno Rotary Club, and Chair of its Literacy Committee. She believes that education is the cornerstone of our profession, and volunteerism is theanchor to our community and our lives.

CHRISTINE M. MORENO ATTORNEY-CPA

TEL: 772/ 288-1020

For Tax Years 2011, 2012 & Beyond

None of the Materials contained herein, and None of the information conveyed orally during this presentation, can be used or relied upon for penalty protection.

Christine M. Moreno, Attorney-CPA, practices law throughout the State of Florida, with her law office in Stuart, Florida.

A graduate of Barry Univ & U of M Law School, and Mayor of North Miami in 1981. Christine was past President of the North Dade South Broward FICPA Chapter and remains a Director. Chris has served as Past Chair of the Accounting Show Committee.

Christine holds a CGMA designation and advises individuals on their business, estate, real estate, probate and tax matters. Her practice does notinclude preparing or filing tax returns.

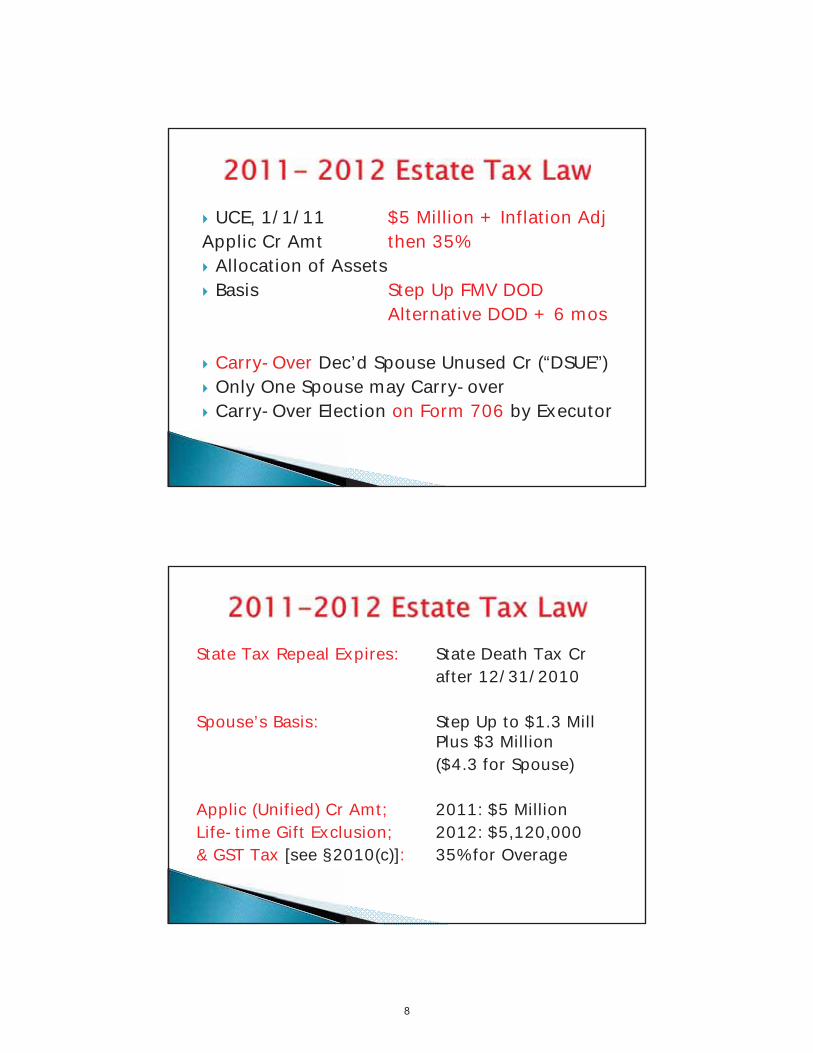

UCE, 1/1/11 $5 Million + Inflation AdjApplic Cr Amt then 35%

Allocation of AssetsBasis Step Up FMV DOD

Alternative DOD + 6 mos

Carry-Over Dec’d Spouse Unused Cr (“DSUE”)Only One Spouse may Carry-overCarry-Over Election on Form 706 by Executor

State Tax Repeal Expires: State Death Tax Crafter 12/31/2010

Spouse’s Basis: Step Up to $1.3 Mill Plus $3 Million($4.3 for Spouse)

Applic (Unified) Cr Amt; 2011: $5 Million Life-time Gift Exclusion; 2012: $5,120,000& GST Tax [see §2010(c)]: 35% for Overage

Rev Proc 2011-41, Section 4.02 et seq.

Sum of General Basis Increase(Aggregate Basis Increase PLUSCarry-Over/Unrealized Losses Increase)ANDSpousal Basis Increase

DeductionsMarital Deduction (Spouse US Citizen by 706

filing date or QDOT, included in Estate and Pass to Spouse)

QDOT TrustDirectly made Educational or Medical Payments Gifts to Charity--For Charitable Use ONLY

Qualified Terminable Interest Property (“QTIP”)Terminable Interest Property w/ POA

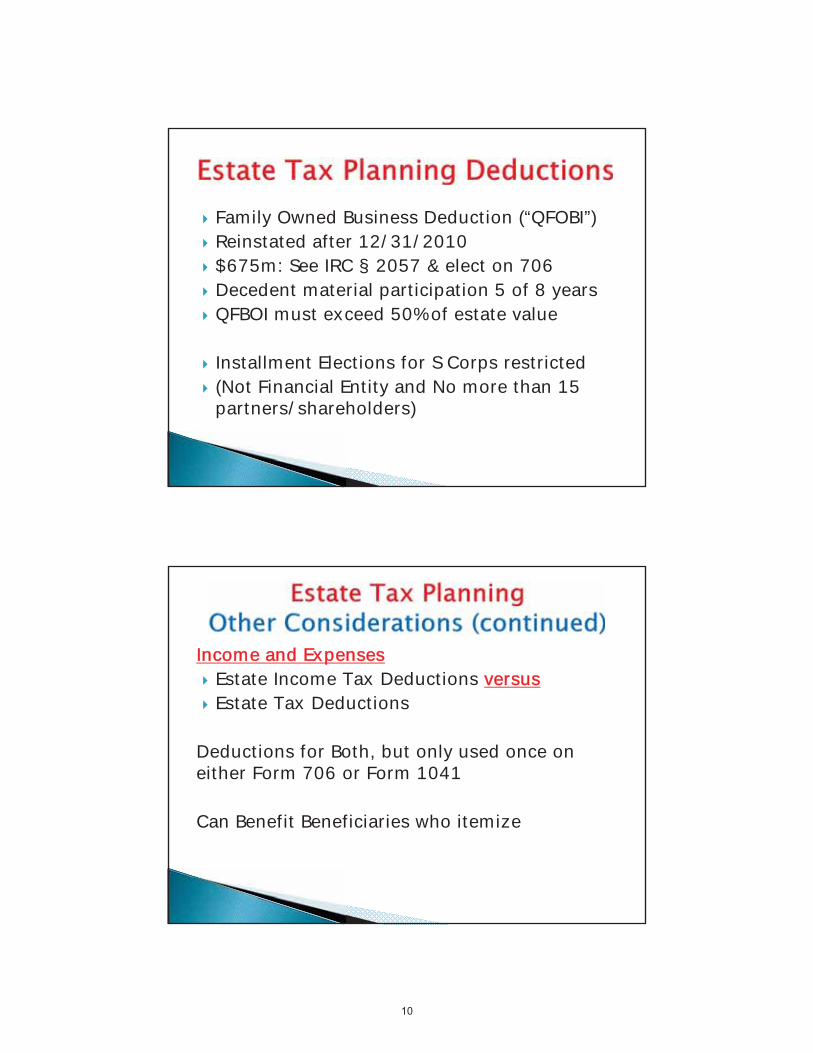

Family Owned Business Deduction (“QFOBI”)Reinstated after 12/31/2010$675m: See IRC § 2057 & elect on 706Decedent material participation 5 of 8 yearsQFBOI must exceed 50% of estate value

Installment Elections for S Corps restricted(Not Financial Entity and No more than 15 partners/shareholders)

Income and ExpensesEstate Income Tax Deductions versusEstate Tax Deductions

Deductions for Both, but only used once on either Form 706 or Form 1041

Can Benefit Beneficiaries who itemize

Portability vs. Credit Shelter Trust

Shield Appreciated AssetsSurviving Spouse RemarriageAsset ProtectionGST Planning

BEWARE of Formula & Power Clauses

Estate Tax Law Sunsets 12/31/2012Economic Growth & Tax Reconcil Act of 2001reinstated if no legislative action prior to 12/31/2012

UCE & Gift Tax Exclusion $1 MillionTax Rates Graduate to 55%No Portability of Spouse’s Estate Tax Exclusion

Good Night, Sweet Prince

Fiduciary Accounting and Tax Update

F. Gordon Spoor, CPA/PFS

F. Gordon Spoor, CPA/ PFSManaging Shareholder

Spoor & Associates

Gordon has practiced public accounting in St. Petersburg, Florida since 1974. He is married to Chris Spoor and they have four children ranging in age from 28 to 33 and five grandchildren. He received his Bachelor of Arts Degree from the University of South Florida and is a member of the American Institute of Certified Public Accountants, the Florida Institute of Certified Public Accountants and the Suncoast Estate Planning Council and holder of a NASD series 65 Registered Investment Advisor Representative license. He is licensed to practice as a CPA in both Florida and Georgia.

He is the managing shareholder of the CPA firm of Spoor & Associates, P.A., and a shareholder in the investment advisory firm of Anderson, Riley & Spoor, P.A. He is active in the Florida Institute of Certified Public Accountants (FICPA) and served on its Board of Governors in 2002-2003, as Chairman of the FICPA State Tax Section for two years, and as a member of the Legislative Policy Committees for one year. He is currently a member of the FICPA Federal Tax Committee, Chairman of the AICPA Trust, Estate & Gift Tax Technical Resource Panel, Chairman of the AICPA Fiduciary Accounting Matters Task Force and served on a joint committee composed of the FICPA, Florida Bar and Florida Bankers Association regarding the rewriting of Florida’s Trust Administration Code and revisions to Florida’s Principal & Income Act. Gordon also serves as an expert witness for the State of Florida Board of Accountancy. Additionally, he serves as a discussion leader for continuing professional education courses and has been awarded an outstanding discussion leader award in every year the award has been given since he became a discussion leader in 1992. He is also the recipient of a 2000-2001 FICPA Presidential Service Award as a result of his efforts on behalf of the FICPA in serving as the lead representative of their Florida Uniform Principal & Income Act task force. He is a frequently published author on subjects relating to estates & trusts as well as the area of general tax practice.

He has published numerous articles covering these topics and others. He is co-author of the FICPA’s “Fiduciary Accounting For Florida” course materials and a contributing author to “Florida Law of Trusts – Fourth Edition” (West Publishing). Much of his time is spent consulting in the area of fiduciary accounting and income tax as well as litigation support in trust matters. He is co-author of “The Fiduciary Accounting Answer Book” (CCH 2009).

F. Gordon Spoor, CPA/PFS

Spoor & Associates, P.A.

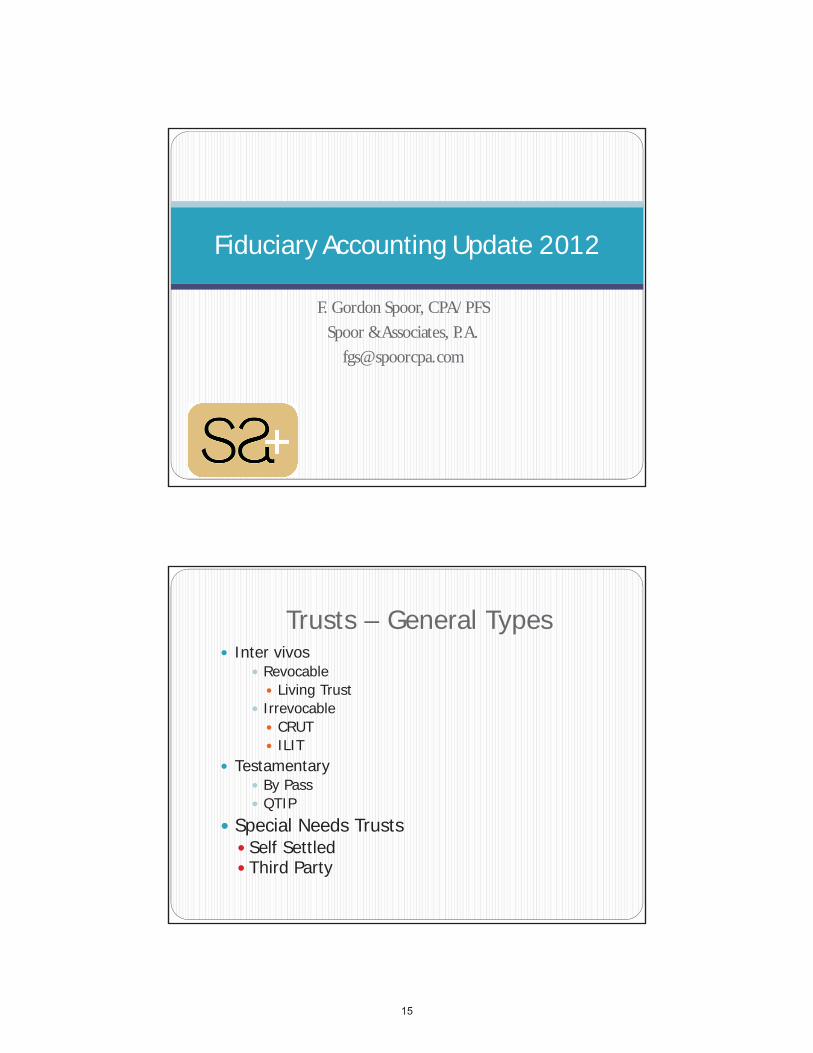

Fiduciary Accounting Update 2012

Trusts – General Types Inter vivos

RevocableLiving Trust

IrrevocableCRUTILIT

TestamentaryBy PassQTIP

Special Needs TrustsSelf SettledThird Party

Simple vs. ComplexSimple

All trust accounting income required to be distributed annuallyNo charitable contributionsNo distributions of corpus

Complex

Grantor TrustsDefinition found in IRC §§671-679

Reversions in excess of 5% of trust (IRC §673)Power to control beneficial interest (IRC §674)Certain Administrative Poweres (IRC §675)Power to Revoke (IRC §676)Income for Benefit of Grantor (IRC §677)Certain Foreign Trusts ( §679)

How is a Trust Taxed?IRC §641(b):

“ The taxable income of an estate or trust shall be computed in the same manner as in the case of an individual, except as otherwise provided in this part. “

Personal ExemptionsMajor differences from individual income taxationPersonal Exemption (IRC §642(b)(3)

Estate $600Simple Trust $300Complex Trust $300 or $100Special Needs Trust – equal to Individual Exemption

The Distribution DeductionEstates and Trusts are entitled to a special deduction

“The distribution deduction.”IRC §651 – Simple Trusts“there shall be allowed as a deduction in computing taxable income….. the amount of the income required to be distributed”

The Distribution DeductionComplex Trusts and EstatesIRC §661 The deduction will be the total of

Amounts required to be paid currently (Tier I)Other amounts paid, credited or permanently set aside. (Tier II)

The Distribution DeductionIn all cases the distribution deduction cannot exceed distributable net income (DNI)

IRC §651(b) & IRC §661(c)

What is “Income”For distribution purposes?

IRC §643(b)“…… the amount of income of the estate or trust for the taxable year determined under the terms of the governing instrument and applicable local law.”

What is “Income”For distribution purposes?

First, READ THE GOVERNING INSTRUMENTSecond, be familiar with your state’s principal and income act.Income computed in accordance with the above will be the “income required to be distributed” of a Simple Trust.

What is DNI?IRC §643(a)

Taxable income before ExemptionDistribution DeductionSpecial DeductionsAdd back:Capital LossesMunicipal Income (Net of allocable Expenses)Subtract:Capital Gains

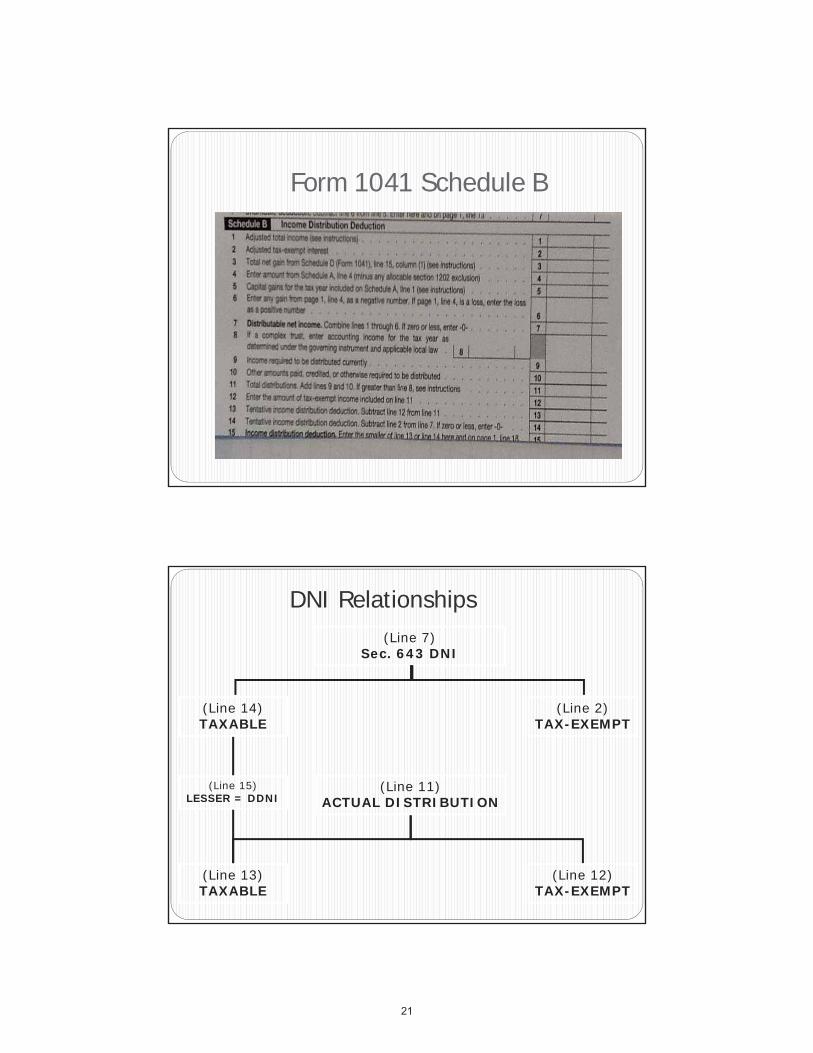

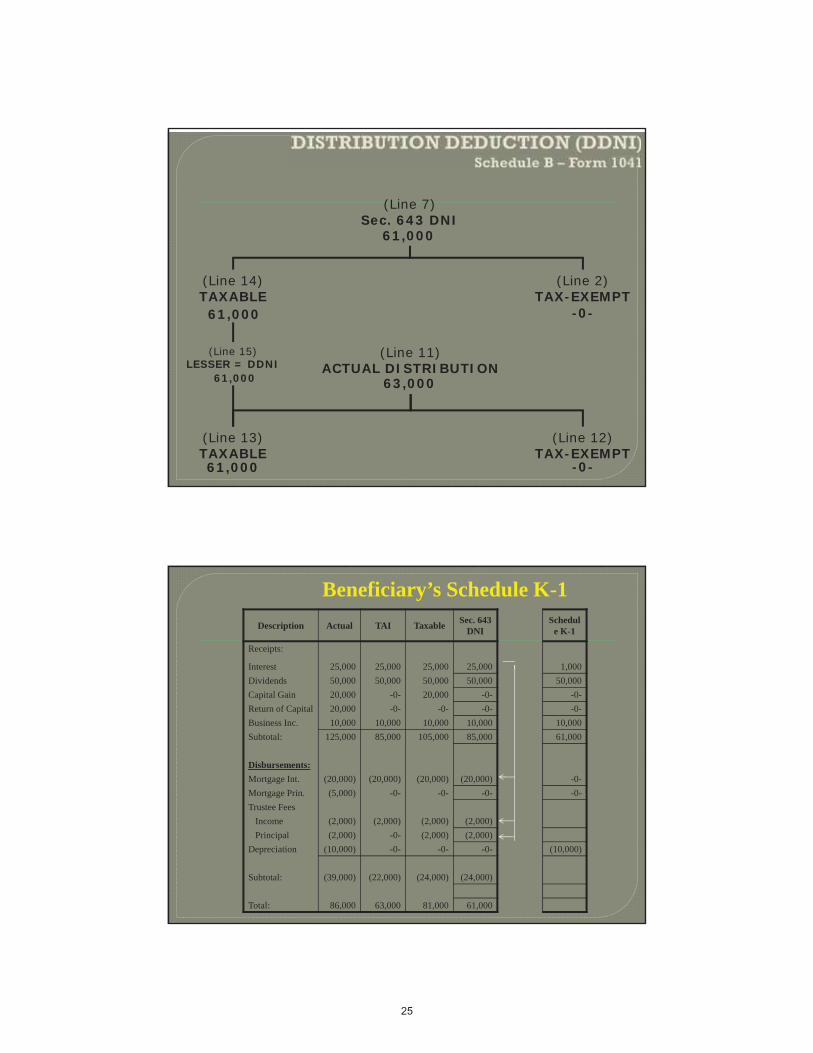

Form 1041 Schedule B

(Line 7)Sec. 643 DNI

(Line 11)ACTUAL DISTRIBUTION

(Line 2)TAX-EXEMPT

(Line 12)TAX-EXEMPT

(Line 13)TAXABLE

(Line 14)TAXABLE

(Line 15)LESSER = DDNI

DNI Relationships

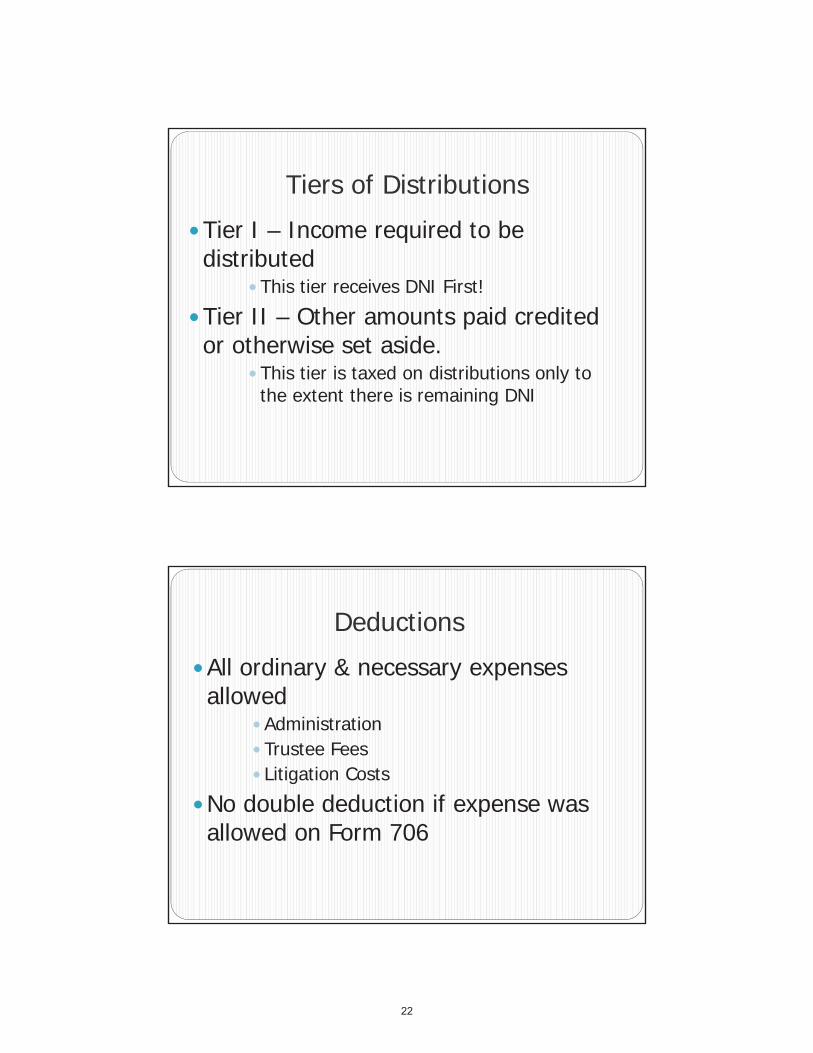

Tiers of Distributions

Tier I – Income required to be distributed

This tier receives DNI First!

Tier II – Other amounts paid credited or otherwise set aside.

This tier is taxed on distributions only to the extent there is remaining DNI

Deductions

All ordinary & necessary expenses allowed

AdministrationTrustee FeesLitigation Costs

No double deduction if expense was allowed on Form 706

Deductions

Exceptions to “double deduction” rule.Deductions “in respect of a decedent” are allowed on both the Form 706 & 1041

Property TaxesAccrued Interest Paid

Deductions subject to 2% limitation

Expenses that were not occasioned by the creation of the estate or trust will not be subject to the 2% “haircut”

IRS is pursuing Investment Advisory Fees as not being unique to trust administration.

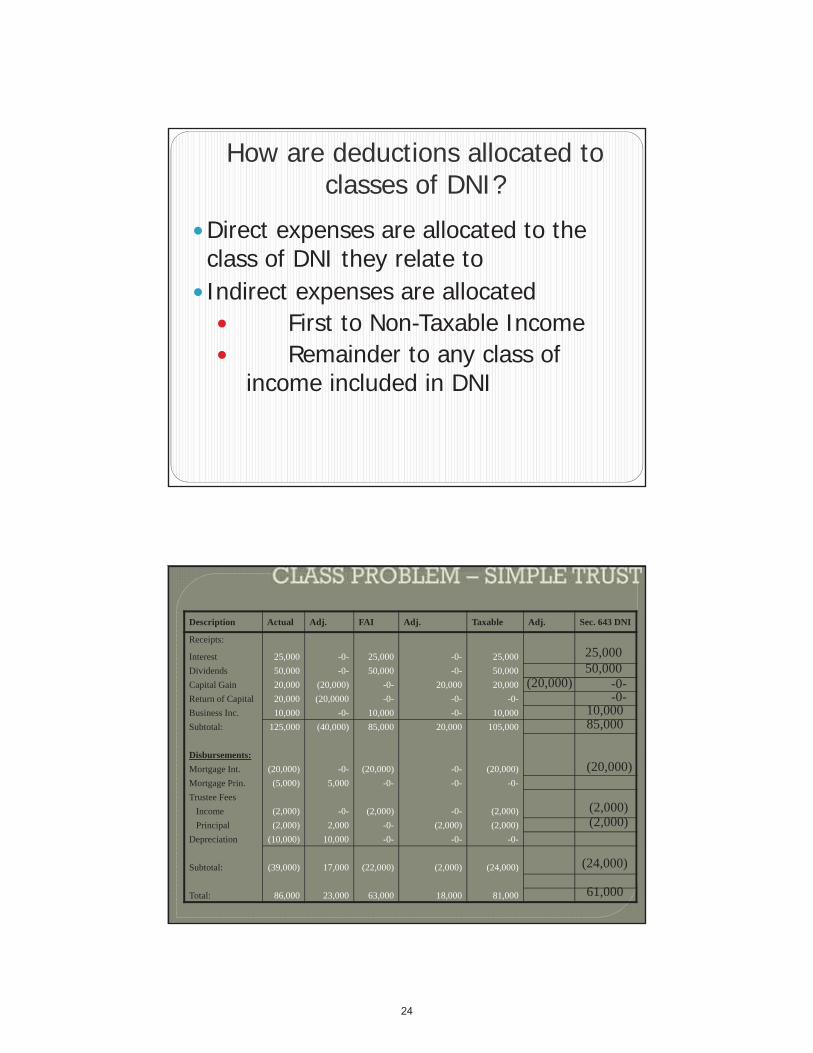

How are deductions allocated to classes of DNI?

Direct expenses are allocated to the class of DNI they relate toIndirect expenses are allocated

First to Non-Taxable IncomeRemainder to any class of

income included in DNI

Description Actual Adj. FAI Adj. Taxable Adj. Sec. 643 DNI

Receipts:

Interest 25,000 -0- 25,000 -0- 25,000Dividends 50,000 -0- 50,000 -0- 50,000Capital Gain 20,000 (20,000) -0- 20,000 20,000Return of Capital 20,000 (20,0000 -0- -0- -0-Business Inc. 10,000 -0- 10,000 -0- 10,000Subtotal: 125,000 (40,000) 85,000 20,000 105,000

Disbursements:Mortgage Int. (20,000) -0- (20,000) -0- (20,000)Mortgage Prin. (5,000) 5,000 -0- -0- -0-Trustee Fees

Income (2,000) -0- (2,000) -0- (2,000)Principal (2,000) 2,000 -0- (2,000) (2,000)

Depreciation (10,000) 10,000 -0- -0- -0-

Subtotal: (39,000) 17,000 (22,000) (2,000) (24,000)

Total: 86,000 23,000 63,000 18,000 81,000

25,00050,000

(20,000)

10,00085,000

(20,000)

61,000

(24,000)

(2,000)(2,000)

-0--0-

(Line 7)Sec. 643 DNI

(Line 11)ACTUAL DISTRIBUTION

(Line 2)TAX-EXEMPT

(Line 12)TAX-EXEMPT

(Line 13)TAXABLE

(Line 14)TAXABLE

(Line 15)LESSER = DDNI

61,000

61,000 -0-

-0-61,000

61,000 63,000

Beneficiary’s Schedule K-1Description Actual TAI Taxable Sec. 643

DNI

Receipts:

Interest 25,000 25,000 25,000 25,000Dividends 50,000 50,000 50,000 50,000Capital Gain 20,000 -0- 20,000 -0-Return of Capital 20,000 -0- -0- -0-Business Inc. 10,000 10,000 10,000 10,000Subtotal: 125,000 85,000 105,000 85,000

Disbursements:Mortgage Int. (20,000) (20,000) (20,000) (20,000)Mortgage Prin. (5,000) -0- -0- -0-Trustee Fees

Income (2,000) (2,000) (2,000) (2,000)Principal (2,000) -0- (2,000) (2,000)

Depreciation (10,000) -0- -0- -0-

Subtotal: (39,000) (22,000) (24,000) (24,000)

Total: 86,000 63,000 81,000 61,000

Schedule K-1

1,00050,000

-0--0-

10,00061,000

-0--0-

(10,000)

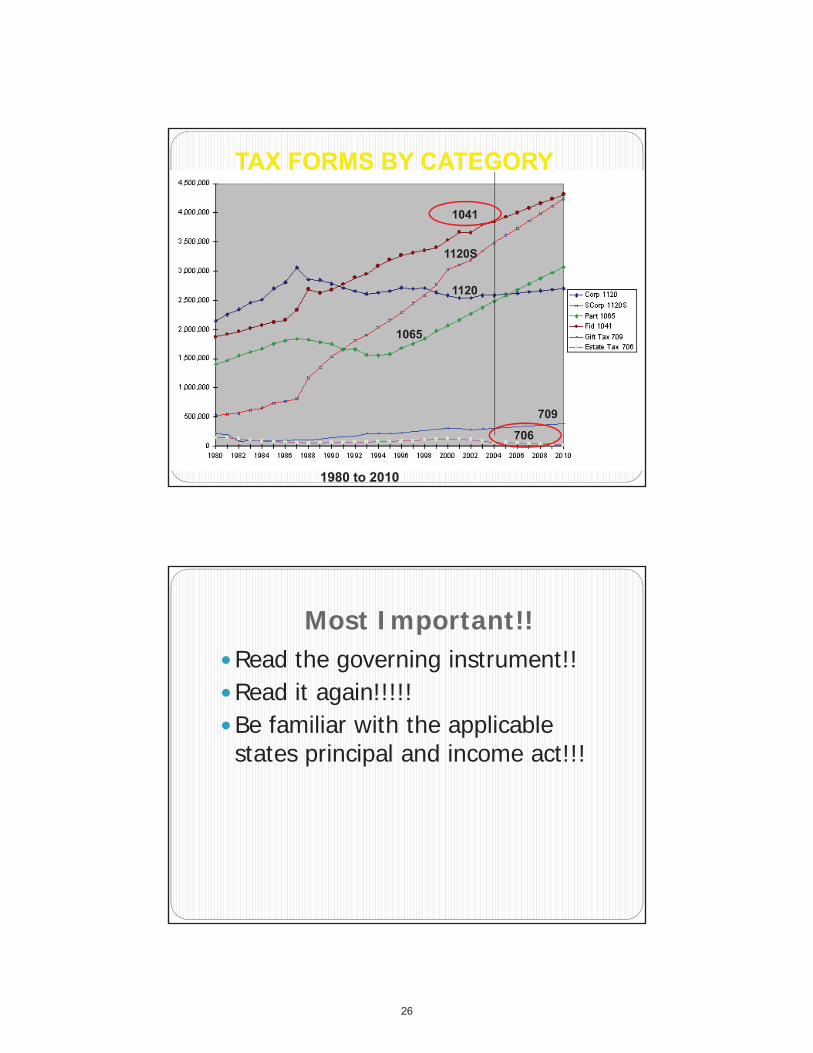

Most Important!!Read the governing instrument!!Read it again!!!!!Be familiar with the applicable states principal and income act!!!

Uniform Principal & Income ActAdopted by NCCUSL in 2000

Adopted in 43 States

Revised 2008Revisions adopted in 5 StatesIntroduced in 11 StatesFlorida wrote their own revisons

F.S. 738.302Examples – Accrued Income

Decedent dies on June 30, 2010. All assets are held in a living trust which will eventually divide into a marital and by-pass trust with all income required to be paid to the surviving spouse. As of that date the Form 706 (assuming there is an estate tax!) listed the following assets:

Accrued interest on a bond which paid interest semi-annually on January 1st and July 1st $10,000Dividend payable to shareholders of record June 28th, payable July 5th $7,500

F.S. 738.302Examples – Accrued Income

When these amounts are received are they principal or income.

Both are IRD for purposes of computing the estate tax deduction.

UPIA §302 provides that a receipt that is periodic and has a due date shall be treated as income if the due date occurs after the date of death and principal if the due date occurs before death.

F.S. 738.302Examples – Accrued Income

A payment is periodic if it is paid at regular intervals

The due date for the interest payment accrued is July 1st

which is after the decedent’s death and it is therefore all income.

The due date for the accrued dividend is the record date which fell before the date of death and it is therefore all principal.

The deduction for estate tax paid will follow the IRD.

F.S. 738.303 Undistributed Income

Computing undistributed income when an income interest ends.

Surviving spouse, who is a spouse by a second marriage, dies 5 years later. At the time of their death their estate is entitled to “undistributed income” from the trust, assuming nothing to the contrary in the actual trust document. How is this computed?

F.S. 738.303 Undistributed Income

UPIA §303 defines undistributed income as net income received before the date on which the income interest ends.

UPIA §301 provides that an income interest ends on the day before an income beneficiary dies.

If the surviving spouse passed away on September 15th their income interest ended on September 14th and “undistributed income” is income received prior to September 14th.

F.S. 738.303 Undistributed Income

The trust was receiving rental income from investment property. One particular tenant chronically pays their rent late. Their rental payment is $15,000 per month. They paid their September rent on September 14th.

Is this undistributed income?What if it was paid on the 13th?

This same principal applies to expenses.Only expenses actually paid through September 13th would be included regardless of amounts payable!

F.S. 738.401Entities

Receipts from entities.

An entity is any form of conducting business except sole proprietorships.

Cash receipts from entities are income unless they are deemed in liquidation and as such would be considered principal.

If an entity distributes more than 20% of its assets, the distribution is deemed to be in liquidation.

F.S. 738.401Entities

The trustee has a large investment portfolio which is invested for growth and generates a great deal of capital gains but very little in dividends and interest.

Capital gains are considered principal while dividends and interest are considered income.

Trustee transfers the entire investment portfolio into a single member LLC, an entity.

Distributions from the entity are all income if they are not deemed to be in liquidation.

F.S. 738.401Entities

This will result in the conversion of capital gains into income reciepts!

The category of income reported on the Schedule K-1 has no impact on fiduciary accounting!

May result in tax free distributions to the income beneficiary because capital gains are not ordinarily included in DNI!

My be a violation of fiduciary duty!

Florida’s 2012 RevisionsThe Florida Uniform Principal and Income Act (the “UPIA” or the “Act”), became effective January 1, 2003. The Florida UPIA has greatly improved the guidance offered to fiduciaries in administering trusts and estates in Florida but experience revealed some shortcomings. Interested industry groups offerred solutions that are included in SB 1050, effective 01/01/13.

Application between Trusts & EstatesConfusion existed as to which sections of the current Act applied to only trustees or personal representatives

Current act defines “fiduciaries” to include both trustees and personal representatives.

F.S. s. 738.102(3)

Some portions of the Act were intended to only apply to trustees.

F.S. ss. 738.105; 738.401(7); 738.1041

Application between Trusts & EstatesApplication to estates was defined F.S. s. 738.201

“A fiduciary of an estate or of a terminating income interest in a trust shall determine the amount of net income and net principal receipts received from property specifically given to a beneficiary under the rules of §738.301-738.706 which apply to trustees……. (s. 738.201(1))

Similar language in s. 738.201(2)

Application between Trusts & EstatesTrustee improperly used currently in

F.S. s. 738.105 F.S. s 738.301 – 303F.S. s. 738.401 – 403F.S. s. 738.501 – 504F.S. s. 738.601 – 608F.S. s. 738.701 – 705

The Solution: “Fiduciary”“which apply to trustees” language removed from F.S. s. 738.201(1) & (2)

Added “fiduciary” to all sections intended to apply to all fiduciaries as defined in F.S. s. 738.102(3)

“Fiduciary” changed to “trustee”

Carrying ValueProbate Code Rule 5.346 requires presentation of carrying value in estate accountings

Only definition is in appendix B of the Rule

F.S. 736.08135 requires presentation of “carrying value” in all trust accountings

Carrying value is referenced in new F.S. ss. 738.202, 738.401(6) & 738.603

But current law does not have a definition of “carrying value”

The SolutionAddition of a definition in F.S. 738.102

Definition is modeled after the Model Fiduciary Accounting Standards adopted by the American Bar, American Bankers and AICPA

Allows for adjustment to carrying value upon a change in trustees.

Carrying Value Defined"Carrying Value" (also known as "Inventory Value" and "Fiduciary Acquisition Value") means the fair market value at the time the assets are received by the fiduciary. For estates of decedents, and trusts described in s. 733.707(3) after the grantor’s death, the assets are considered as received at the date of death. If there is a change in fiduciaries, a majority of the continuing fiduciaries may elect to adjust the carrying values to reflect the fair market value of the assets at the beginning of their administration. If that election is made, it must be reflected on the first accounting filed after the election. For assets acquired during the administration of the estate or trust, the carrying value will be equal to the acquisition cost of the asset.

Scope of Fiduciary DutyF.S. 738.103 “Fiduciary duties; general principles” outlines default duties that apply to all trusts.

As written, it is not clear whether these duties are owed to all trusts that are either administered in this state or under Florida Law

The SolutionF.S. 738.103 now provides that the Act applies to all trusts administered in this state or under Florida law.

Duplicative language in F.S. 738.104(11) regarding application to all trusts has been removed

Modernize UnitrustsF.S. 1041 “Total Return Unitrusts” provides for both the creation of an express unitrust and the conversion of existing trusts to unitrusts

Total Return Unitrusts have experienced wide acceptance

But fluctuation in the stock market may cause material swings in the annual amount of unitrust payments

Some provisions of F.S. 1041 are duplicative

The SolutionThe revised Act provide for the addition of a “smoothing rule” that uses average fair market value of trust assets for the current and preceding two years

Additions to or distributions from principal are accounted for in the new smoothing rule.

Adds definition of “Average Fair Market Value”

Applies to Express Untrusts unless document directs otherwise

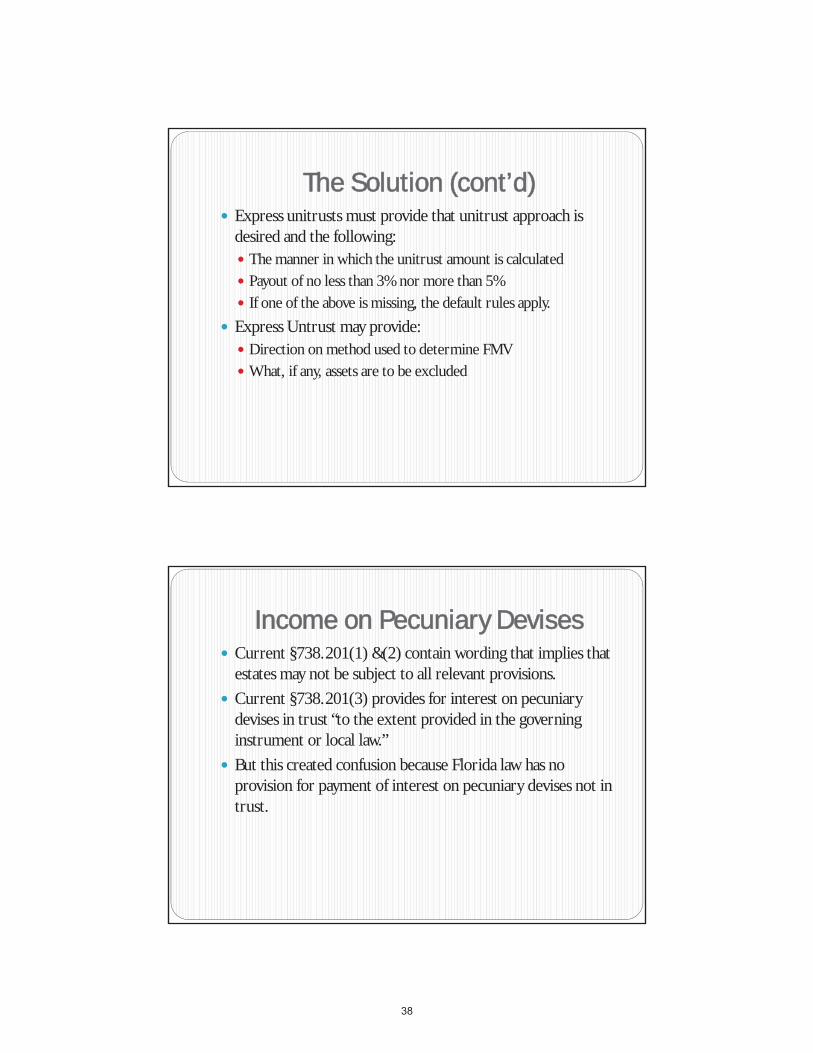

The Solution (cont’d)Express unitrusts must provide that unitrust approach is desired and the following:

The manner in which the unitrust amount is calculatedPayout of no less than 3% nor more than 5%If one of the above is missing, the default rules apply.

Express Untrust may provide:Direction on method used to determine FMVWhat, if any, assets are to be excluded

Income on Pecuniary DevisesCurrent §738.201(1) &(2) contain wording that implies that estates may not be subject to all relevant provisions.

Current §738.201(3) provides for interest on pecuniary devises in trust “to the extent provided in the governing instrument or local law.”

But this created confusion because Florida law has no provision for payment of interest on pecuniary devises not in trust.

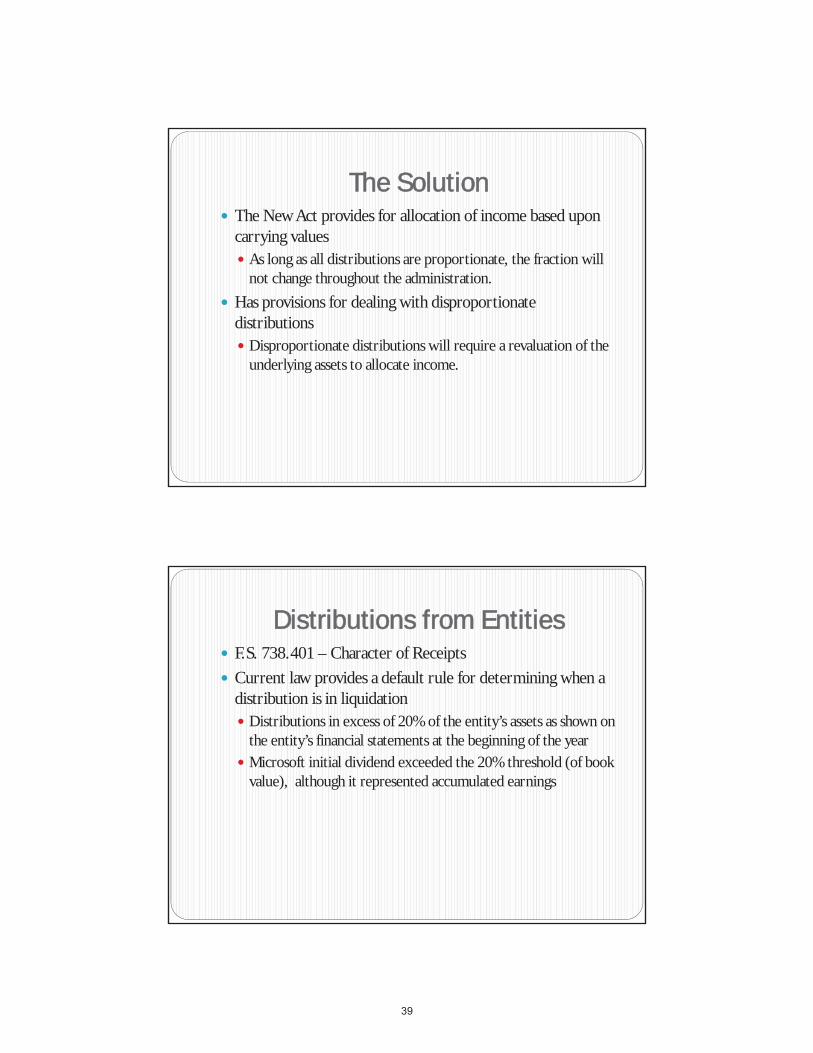

The SolutionThe New Act provides for allocation of income based upon carrying values

As long as all distributions are proportionate, the fraction will not change throughout the administration.

Has provisions for dealing with disproportionate distributions

Disproportionate distributions will require a revaluation of the underlying assets to allocate income.

Distributions from EntitiesF.S. 738.401 – Character of Receipts

Current law provides a default rule for determining when a distribution is in liquidation

Distributions in excess of 20% of the entity’s assets as shown on the entity’s financial statements at the beginning of the yearMicrosoft initial dividend exceeded the 20% threshold (of book value), although it represented accumulated earnings

Distributions from EntitiesCurrent F.S. 738.401(7) applies to private trustees

Targeted Entities & Investment Entities.Classification based upon “undistributed cumulative net income” received during the period the interest is held by the trust.If the Targeted Entity is an Investment Entity, the receipts are treated as if the trust directly held its pro rata share of the assets.

The SolutionF.S. 738.401(5)(b) 20% of book value rule remains intact for non-publicly traded entities but is changed to 10% of fair market value for publicly traded entities, subject to minimum investment returns.

Publicly Traded Securities – allocation to principal reduced to the extent that the cumulative return from the entity while owned by the trust does not equal 3% of entity’s FMVat the beginning of each year

The Solution (cont’d)Non-Publicly Traded entities – allocation to principal is reduced to the extent that the cumulative annual return from the entity does not equal 3% of the entity’s carrying value at the beginning of each year. (plus income taxes computed as if all taxes had been paid by the trust).

Targeted Entities that are not “Investment Entities” are treated as any other entity, so special rules have been eliminated.

The Solution (cont’d)For Private Trustees, special rules still apply for “Investment Entities”, with modifications.

Publicly Traded Partnerships no longer treated as “Investment Entities”

FIFO rule applies to allocations to income in current and preceding two years – (i.e. all distributions are treated as income first)

Character of income remains the same as if the trust owned its pro-rata share of the underlying assets directly (i.e. K-1 classification is used)

Retirement PlansCurrent F.S. 738.602 was amended in 2009 to change the method used to compute the income from deferred comp. plans, annuities and retirement plans as a reaction to an IRS ruling that challenged the UPIA language and the “10% rule applied to IRA accounts. (Rev. Rul. 2006-26)

Allowed for different allocations for marital and non marital trusts

The SolutionF.S. 738.602 amended to treat all plans the same with regards to how income is calculated.

Additionally, beneficiaries of marital trusts may require that all income earned within a retirement plan to be distributed at least annually. (IRC Reg. 20.2056(b)-5(f)(1))

Liquidating AssetsCurrent F.S. 738.603 applies 10% of receipts from liquidating assets to income and the balance to principal

Similar to the 10% rule rejected by the IRS in Rev. Rul. 2006-26

The SolutionAdopted provisions similar to the 1962 Act

Receipts to the extent of 5% of carrying value are income and the balance is principal

Carrying value is reduced for receipts allocated to principal

If carrying value is reduced to zero all receipts become principal

Income Tax AllocationsCurrent F.S. 738.705 has caused some confusion regarding the proper allocation of income taxes to income earned by pass-through entities

The SolutionAmended F.S. 738.705 codifies the formula used by NCCUSL and many commentators to properly allocate income taxes

D = (C-(R*K))/(1-R)

D = Distribution to income beneficiary

C = Cash paid by the entity to the trust

R = tax rate on income

K = entity’s K-1 taxable income

Life EstatesCurrent F.S. 738.801 uses the provisions of F.S. 738.701-705 to allocate expenses between life tenants and remaindermen

Applying trust principles to allocate expenses between life tenants and remaindermen was often confusing

Current law refers to “official mortality tables” but does not address what those are

The SolutionAmended F.S. 738.801 removes reference to F.S. ss. 738.701 – 705 and specifically identifies those expenses allocable to the life tenant and remaindermen.

Any expenses that are not referenced are to be treated under common law

Mortality tables and present value tables are defined by reference to 26 U.S.C. s. 7520

Learn more about membership. | [email protected] | www.ficpa.org(800) 342-3197 (in Florida) | (850) 224-2727

“ I renew because of the invaluable networking opportunities that being a member of the F ICPA provides. From being involved with your local chapter to attending networking events, the F ICPA is an organization that is

known and respected across many industries.”

Monica Ospina, CPA, ABV, CFF Cherry, Bekaert & Holland, LLP

Coral Gables Member since 2007

“ I renew my F ICPA membership because of the signif icant access to education, current events, and the

networking it provides.”

Ray Monteleone, CPA President, Paladin Global Partners

Fort Lauderdale Member since 1979

“ Ibeced

“ I’m renewing my F ICPA membership because it keeps me professionally and socia lly connected to my fellow peers in the profession.”

David White, CPA Carr Riggs & Ingram LLC

Tallahassee Member since 2010

FICPA Membership: Connect, Learn and ThriveProud to be a Member

Keep Your Organization Moving Forward

For more information, please contact the FICPA at [email protected]

or call (800) 342-3197 (in Florida) or (850) 224-2727 extension 412.

The FICPA has partnered with the AICPA and other providers to address the changing needs of business professionals. This partnership now enables us to provide a wide range of courses, instructors, and educational solutions in a variety of formats, including on-site training, seminars, and webcasts.

Topic areas including: • Technical • Strategic and Business Management • Leadership Development • Communication skills • Ethics

Using FICPA on-site training benefits your staff by offering:• Team building opportunities while enhancing their skill set • Smaller class sizes and more interaction with the instructors • Professional development opportunities without the hassle of travel

Meanwhile, employers gain by:• Saving money by eliminating travel expenses • Saving time by scheduling training when it is convenient for you and your staff • Customized, flexible training designed to fit your company’s specific needs

Call or e-mail us today to find out how FICPA has the right training solutions for you!