Medical board investigations are increasing attorneys claim by Floyd Arthur (PPT)

Upload

truongkhueCategory

view

215download

1

Medical Claim Analysis for a Sustainable Health Portfolio

Aloysius Lim FIAA, CERA, FSAS

Proprietary and Confidential | General Reinsurance AG 1

Agenda

01Understanding Health Business

02Issues affecting Sustainability

03Medical Claim analysis

Proprietary and Confidential | General Reinsurance AG 2

Agenda

02Issues affecting Sustainability

03Medical Claim analysis

01Understanding Health Business

Proprietary and Confidential | General Reinsurance AG 3

Understanding Health Business

• S$200,000 a day for Brunei Royal Family treatment?• “Voluntarily reduced it to S$12.1 million”

Proprietary and Confidential | General Reinsurance AG 4

Understanding Health Business: The Four-Way Game

Healthcare Providers Insured Insurance Company Agents

Proprietary and Confidential | General Reinsurance AG 5

Understanding Health Business:

• Ways of managing Health Business:

• Different from Traditional Life Business

One size fits all approach?

Proprietary and Confidential | General Reinsurance AG 6

Agenda

02Issues affecting Sustainability

03Sustainability Checklists

01Understanding Health Business

Proprietary and Confidential | General Reinsurance AG 7

01Understanding Health Business

02Issues affecting Sustainability

03Medical Claim analysis

Issues with Health Business

Proprietary and Confidential | General Reinsurance AG 8

Example of Issues

Policyholders Product Packaging Agents

Proprietary and Confidential | General Reinsurance AG 9

Example of Issues – Policyholders

Rank Description

1 Typhoid and paratyphoid fevers2 Infectious gastroenteritis and colitis, unspecified3 Dengue hemorrhagic fever

…

6 Motor- or nonmotor-vehicle accident, type of vehicle unspecified

7 Dyspepsia.. …..9 Gastritis and duodenitis

Which conditions may be harder to prove? Signs (Objective) Vs Symptoms (Subjective)

Proprietary and Confidential | General Reinsurance AG 10

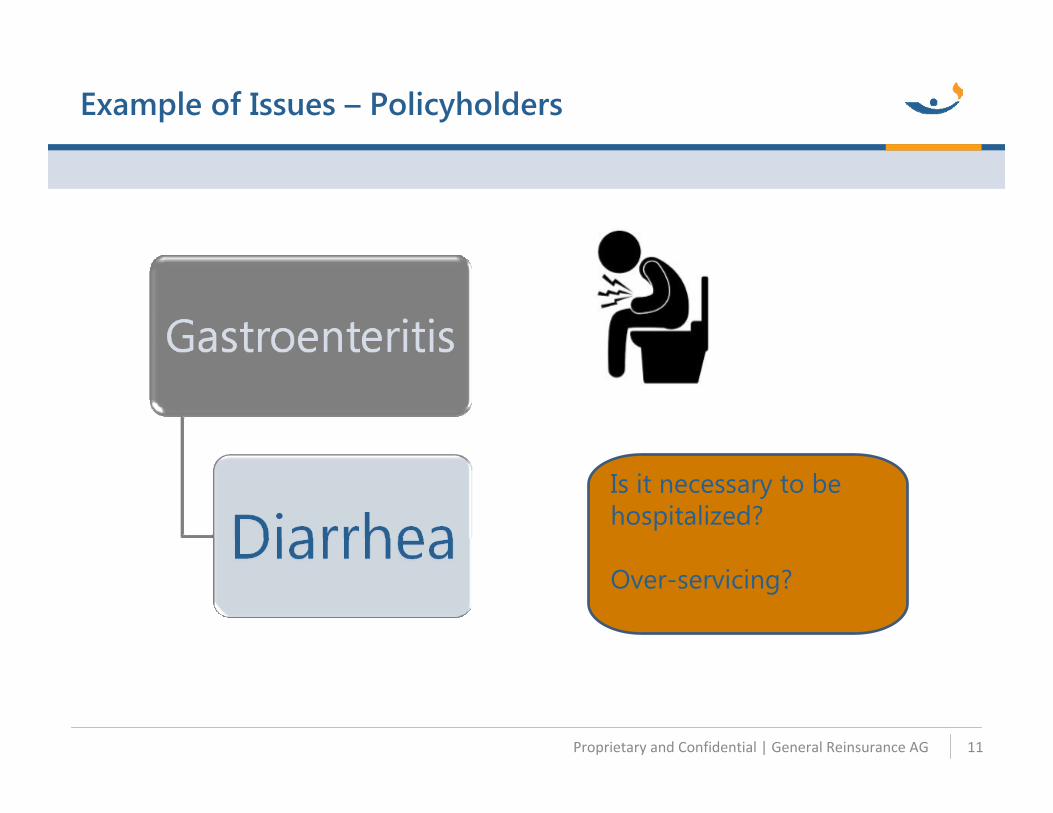

Example of Issues – Policyholders

Is it necessary to be hospitalized?

Over-servicing?

Proprietary and Confidential | General Reinsurance AG 11

Example of Issues – Policyholders

• Top Claim Reasons (Duration 30 – 90 Days)• Consider Duration 30-90 days to consider claims straight after initial waiting

periodDuration 30 – 90 Days Claims:• Claim within 30-90 Days after policy inception• Conditions which may be easier for claim fraud further increase in claim proportion

Why are Claimants behaving this way?

Proprietary and Confidential | General Reinsurance AG 12

Example of Issues – Policyholders

• Is this an issue with Policyholders?• What about:

Proprietary and Confidential | General Reinsurance AG 13

Example of Issues

Policyholders Product Packaging Agents

Proprietary and Confidential | General Reinsurance AG 14

Example of Issues – Product Packaging

Sales Message:Selling these as a bundle

Proprietary and Confidential | General Reinsurance AG 15

Example of Issues – Product Packaging

Proprietary and Confidential | General Reinsurance AG 16

Example of Issues – Product Packaging

Length of stay reasonable?

The list continues…

On month after RCD

Same hospital

Proprietary and Confidential | General Reinsurance AG 17

Product Packaging – Claim

Will the claimant continue to claim?

Proprietary and Confidential | General Reinsurance AG 18

Example of Issues – Product Packaging

• Is this an issue with product packaging?• What about:

Proprietary and Confidential | General Reinsurance AG 19

Example of Issues

Policyholders Product Packaging Agents

Proprietary and Confidential | General Reinsurance AG 20

Example of Issues – Agents

Are these numbers reasonable?

Claims Amount by Agents:

21

2.1% of All Claims

Proprietary and Confidential | General Reinsurance AG

Agent Claim Count % Total Claims

1 170 0.7%

2 150 0.3%

3 120 0.3%

4 110 0.2%

5 100 0.6%

Example of Issues – AgentsExample of Issues – Product Packaging

Proprietary and Confidential | General Reinsurance AG 22

Agenda

02Issues affecting Sustainability

03Medical Claim analysis

01Understanding Health Business

01Understanding Health Business

02Issues affecting Sustainability

03

Proprietary and Confidential | General Reinsurance AG 23

Overall portfolio experience

Portfolio X – Loss Ratio By Accounting Period Portfolio X – Loss Ratio By Incurred period

24Proprietary and Confidential | General Reinsurance AG

Same medical portfolio but different interpretation of profitability: How should we look at it?

Overall portfolio experience

Portfolio A – Loss ratio By Duration Portfolio B – Loss Ratio By Duration

25Proprietary and Confidential | General Reinsurance AG

Which portfolio’s experience are you more concerned about?

Provision for Outstanding Claims

• Why do you need to estimate this? • Estimation of Incurred but not reported claims (IBNR)

- Approach – depends a lot on data quality - Can be determined separately by:

- Product - Region - Other factors that cause the delay pattern to be different – Use

Actuarial Judgment

26Proprietary and Confidential | General Reinsurance AG

• Reasonableness check of whether estimate is sound- Compare estimates with historical

data

• Indicators of reasonableness - Estimates are not biased- Use Actuarial judgment

Provision for Outstanding Claims

Reasonableness Check Example of comparison

27Proprietary and Confidential | General Reinsurance AG

• General analysis based on different factors - Based on understanding of

the issues - Systematic approach - Regular analysis to detect

anomalies promptly• Identify areas of concern

- Deeper analysis

Detailed Claims Analysis

Where should we start? Issues with Health Portfolio

28Proprietary and Confidential | General Reinsurance AG

Detailed Claims Analysis

Abnormally high Loss ratio for region C: - Low exposure?-Fraud? -Hospitals over-charging?- Over-utilisation?-Selective lapse?

Example: Loss ratio by Region

29Proprietary and Confidential | General Reinsurance AG

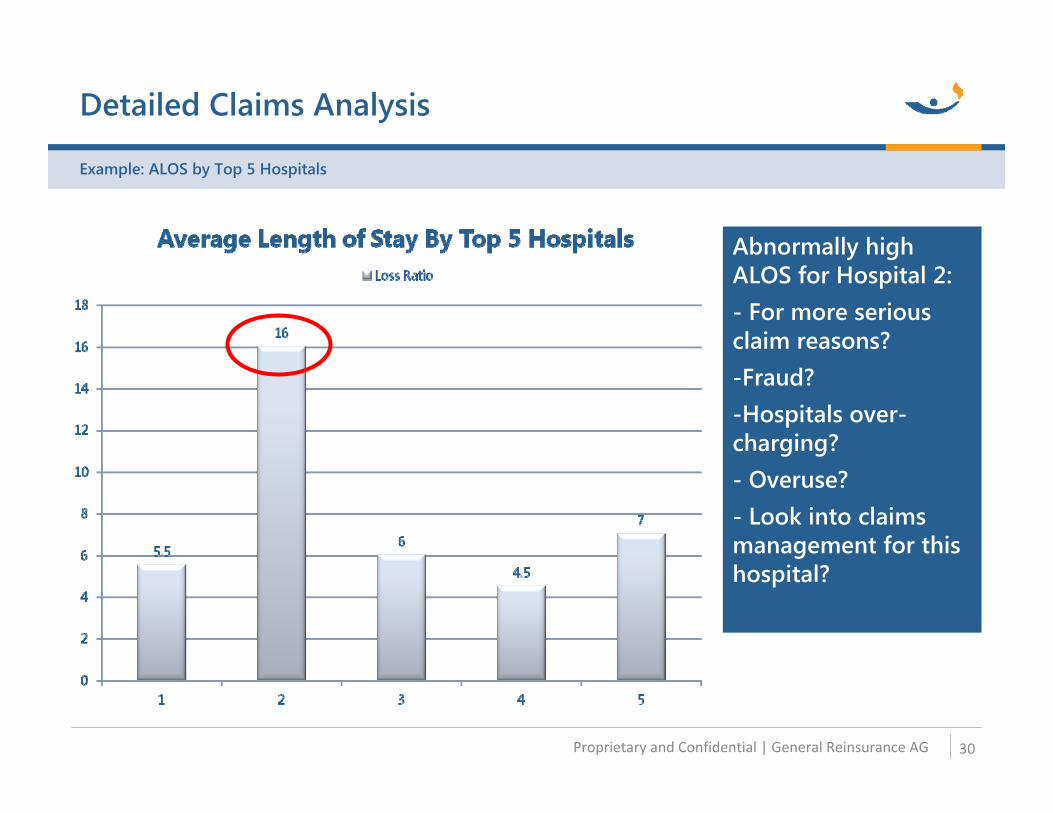

Detailed Claims Analysis

Abnormally high ALOS for Hospital 2: - For more serious claim reasons?-Fraud? -Hospitals over-charging?- Overuse?- Look into claims management for this hospital?

Example: ALOS by Top 5 Hospitals

30Proprietary and Confidential | General Reinsurance AG

Claim Reasons% of Claims < 30

days policy inception

Vehicle accidents 32%

Neoplasm 28%

Hernia 15%

Accidental falls 12%

Accidental drowning 5%

Others 8%

Total 100%

Detailed Claims Analysis

Look into why policyholders claim right after taking out the policy-Anti-selection? -Non-disclosure?-Fraud?- Falls under claim exclusions?- Review claims management process?

Example: Analysis of Claim Reasons for Claims < 30 days since policy inception

31Proprietary and Confidential | General Reinsurance AG

• Big Buzz Words - Big Data - Analytics

• Techniques - Generalized Linear Modelling - Other Techniques

Big Data - Capturing interlinked factors in analysis

Big Data & Analytics Interlinked issues

32Proprietary and Confidential | General Reinsurance AG

• Data collection process - Data System adequate? - What sort of data is collected?

• Understanding how data is collected for proper analysis- Example: Multiple claims for a

single admission

Data – Basic building block of your analysis

Big data? Data quality?

33Proprietary and Confidential | General Reinsurance AG

• Are the data fields standardized?- ICD Codes - Hospital Codes

• Data Checking - Males having pregnancy related

complications?

Ending note - Risk Culture

Describes the values, beliefs, knowledge, attitudes and understanding about risk shared by a group of people with a common interest.

“The way we do things around here”

Proprietary and Confidential | General Reinsurance AG 34

Conclusion

• Understanding health business is important• Managing health business is not as straightforward• Medical Claim Analysis

- provides insights into the experience for active management of health business

- Without good medical claim analysis, you are not able to increase rates.

• Risk culture is important.• Get the right players into the game.

Proprietary and Confidential | General Reinsurance AG 35

Visit genre.com for more info.

Aloysius Lim FIAA, CERA, FSAS

Keep up with the latest industry trends –www.genre.com/perspective

Proprietary and Confidential | General Reinsurance AG 36

Disclaimer

This presentation is protected by copyright. All the information contained in it has been very carefully researched and compiled to the best of our knowledge. Nevertheless, no responsibility is accepted for its accuracy, completeness or currency. In particular, this information does not constitute legal advice and cannot serve as a substitute for such advice. It may not be duplicated or forwarded without the prior consent of the Gen Re.

The content of this presentation is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Proprietary and Confidential | General Reinsurance AG 37