6-1 CHAPTER 6: BORROWING ON OPEN ACCOUNT. 6-2 The Basic Concepts of Credit Why Borrow? To smooth...

33

6-1 CHAPTER 6: BORROWING ON OPEN ACCOUNT

-

Upload

sarina-loner -

Category

Documents

-

view

214 -

download

0

Transcript of 6-1 CHAPTER 6: BORROWING ON OPEN ACCOUNT. 6-2 The Basic Concepts of Credit Why Borrow? To smooth...

6-1

CHAPTER 6:

BORROWING ONOPEN ACCOUNT

6-2

The Basic Concepts of Credit

Why Borrow?

To smooth consumption To avoid paying cash for large

purchases (like a car)

To meet financial emergencies

Convenience

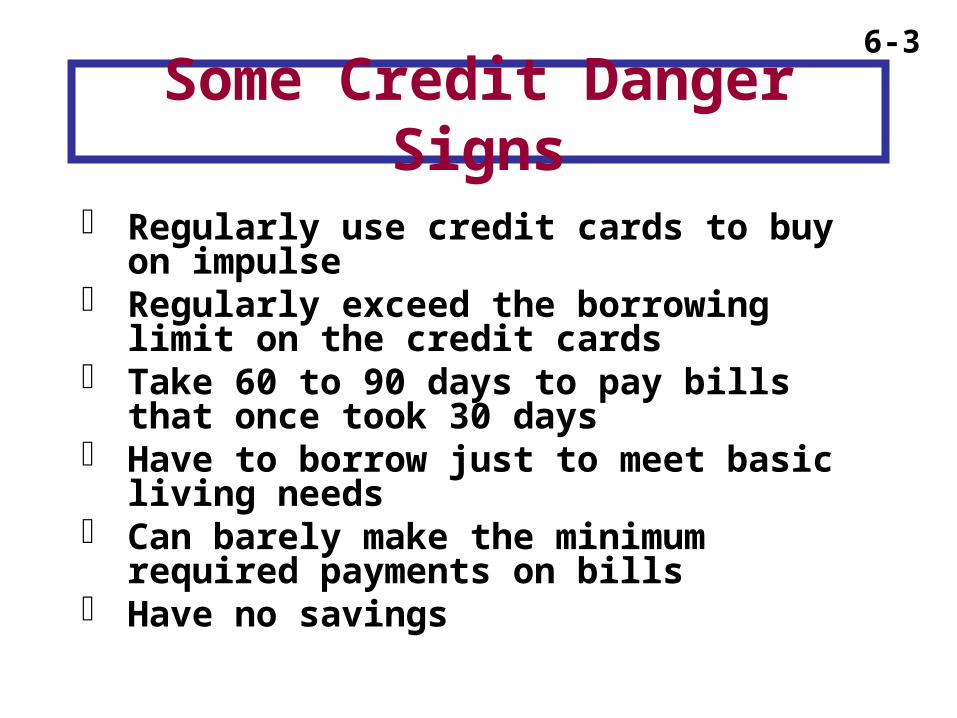

6-3

Some Credit Danger Signs

Regularly use credit cards to buy on impulse

Regularly exceed the borrowing limit on the credit cards

Take 60 to 90 days to pay bills that once took 30 days

Have to borrow just to meet basic living needs

Can barely make the minimum required payments on bills

Have no savings

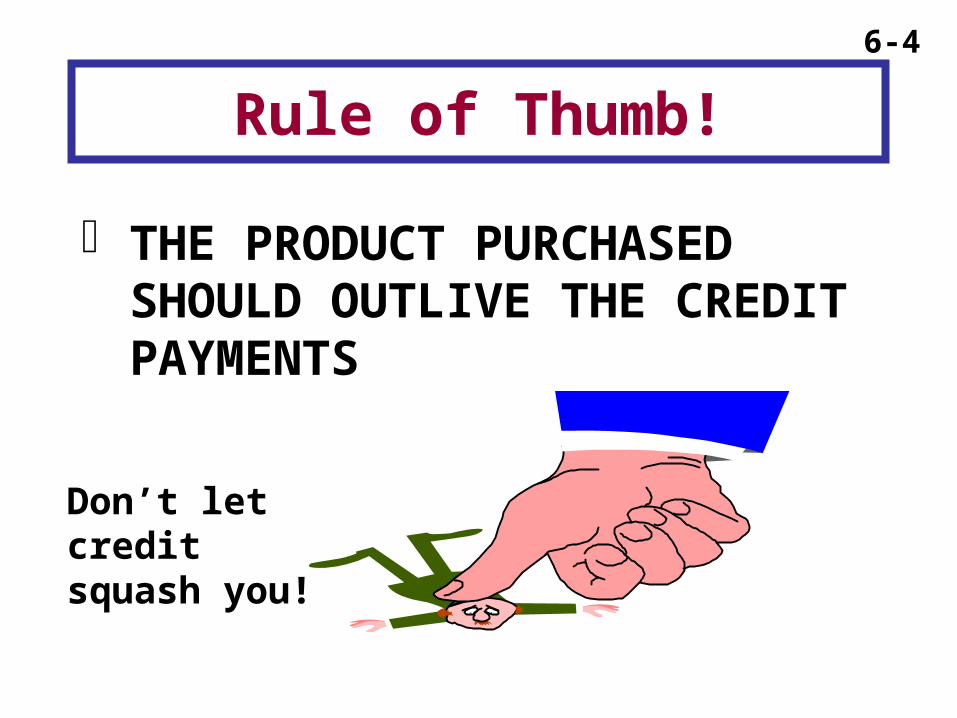

6-4

Rule of Thumb!

THE PRODUCT PURCHASED SHOULD OUTLIVE THE CREDIT PAYMENTS

Don’t letcreditsquash you!

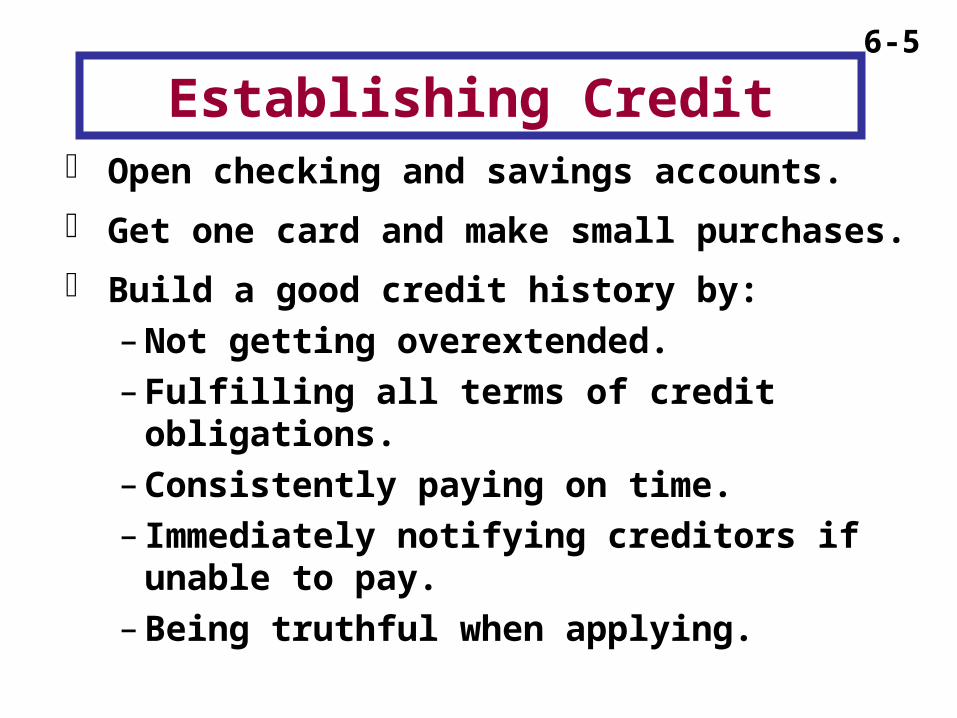

6-5

Establishing Credit Open checking and savings accounts.

Get one card and make small purchases.

Build a good credit history by:

– Not getting overextended.

– Fulfilling all terms of credit obligations.

– Consistently paying on time.

– Immediately notifying creditors if unable to pay.

– Being truthful when applying.

6-6

How much credit can you stand?

Total monthly consumer credit paymentsMonthly take-home pay

Monthly consumer credit payments (excluding mortgage) should not exceed 20% of your

monthly net income.

DEBT SAFETY RATIO =

6-7

Steps for Women in Establishing Credit :

Consistently use your own legal name to build credit history.

Ex: Mary Brown, not Mrs. John Brown

Have information reported to credit bureau in your name as well as your husband’s.

Consider retaining separate credit file when you marry.

6-8

Open Account Credit Credit extended to a consumer in

advance of any transaction.

Consumer can buy/borrow up to a specified amount, the credit limit.

Usually, interest can be avoided by paying balance in full promptly.

6-9

Bank Credit Cards: Issued by financial institutions

Features include:– Line of credit dependent upon

applicant’s financial status and ability to pay

– Cash advances and balance transfers

– Other services or rebates

– Interest rates and fees

6-10Other Credit Cards & Charge Accounts:

Retail charge cards (ex: Sears)

30-day charge accounts

Travel & entertainment cards

Prestige cards

Affinity cards

Secured credit cards

Student credit cards

6-11Debit Card:

Looks like a credit card but works like writing a check—accesses your checking account.

Does not provide line of credit.

Greater liability exposure in event of fraudulent use.

Prepaid card is a debit card with fixed amount available—does not access your checking account.

6-12

When Losing a Credit Card or Debit Card…

Credit card– Card holder not liable

for fraudulent charges if loss is reported before the card is used

– If reported after the card is used, maximum liability is $50

Debit card– If stolen, the thief

could wipe out your checking account!

– Check with your bank regarding policies on lost or stolen cards

6-13

Revolving Credit Lines:

Open account credit offered by banks and other financial institutions.

Usually offer higher credit lines and lower interest rates than credit cards!

Money accessed by writing checks.

6-14

Forms of revolving credit: Overdraft protection lines

– A line of credit linked to a checking account

– Enables a depositor to overdraw the account up to a predetermined limit

– Usually with limits between $500 to $1000

Unsecured personal credit lines– Available on an as-needed basis– Money is accessed by writing checks– Repayment is set up on a monthly

installment basis

6-15

Forms of revolving credit: Home equity credit lines

– Secured by the equity in owner’s home– Interest tax deductible up to $100,000

(if you itemize deductions) – Lenders usually set the maximum

credit line at 75%-80% of the market value of the home

– Example: A couple buys a home for $85,000, ten years later, it’s worth $165,000. Mortgage balance is $45,000. Using 75% loan-to-market value ratio, how much can they borrow?

– Answer: 0.75*165,000-45,000 = $78,750.

6-16

Obtaining and Managing Open Account Credit

Steps in opening an account:

1. Complete and submit application.

2. Lender investigates creditworthiness.

3. Lender obtains credit bureau report.

4. Lender makes credit decision; may use credit scoring.

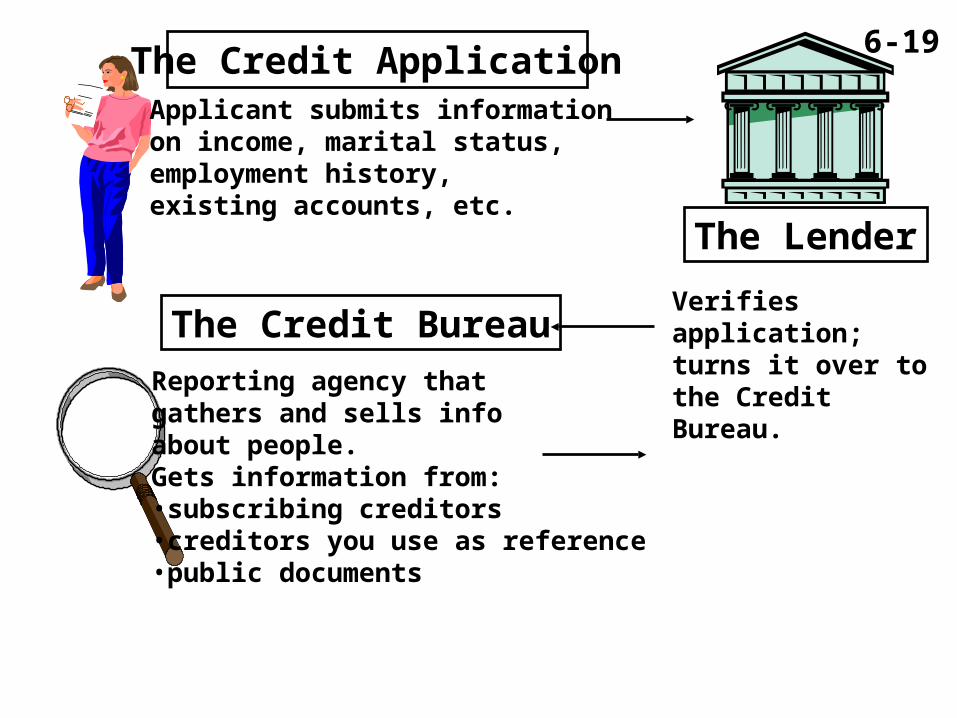

6-17The Credit Application

Applicant submits information on income, marital status, employment history, existing accounts, etc.

6-18The Credit Application

Applicant submits information on income, marital status, employment history, existing accounts, etc.

The Lender

Verifies application;turns it over to the Credit Bureau.

6-19

The Credit Bureau

The Credit ApplicationApplicant submits information on income, marital status, employment history, existing accounts, etc.

The Lender

Verifies application;turns it over to the Credit Bureau.

Reporting agency thatgathers and sells infoabout people.Gets information from:•subscribing creditors•creditors you use as reference•public documents

6-20

The Credit Bureau

The Credit ApplicationApplicant submits information on income, marital status, employment history, existing accounts, etc.

The Lender

Verifies application;turns it over to the Credit Bureau.

Credit Bureau submits report back to lender; lender then makes

Reporting agency thatgathers and sells infoabout people.Gets information from:•subscribing creditors•creditors you use as reference•public documents

The Credit Decision

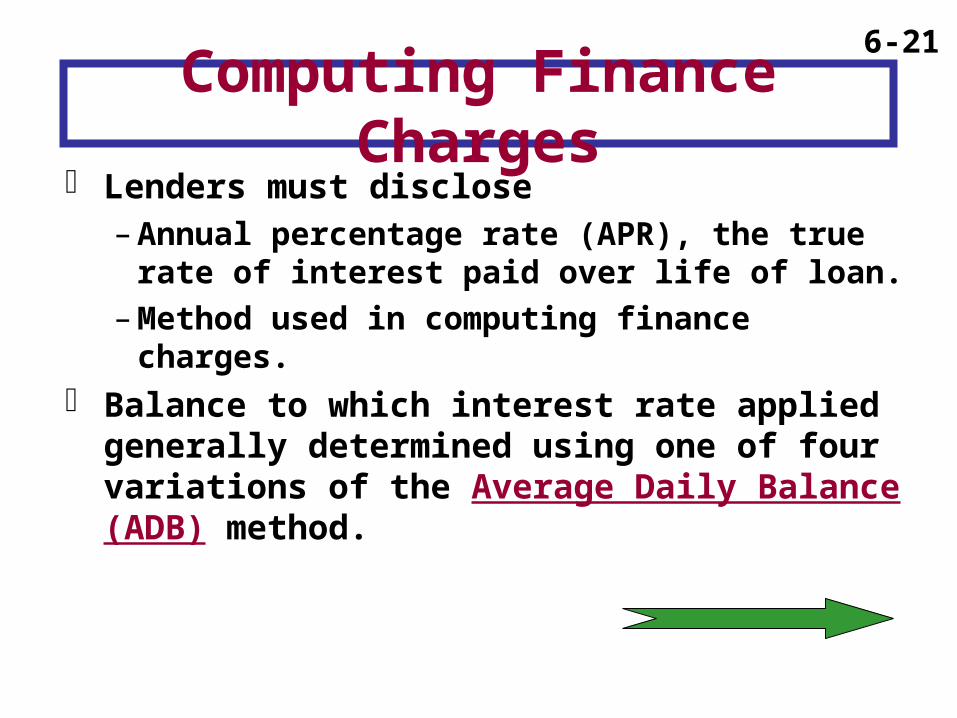

6-21

Computing Finance Charges Lenders must disclose

– Annual percentage rate (APR), the true rate of interest paid over life of loan.

– Method used in computing finance charges. Balance to which interest rate applied

generally determined using one of four variations of the Average Daily Balance (ADB) method.

6-22 ADB excluding new purchases

The most consumer friendly!

ADB including new purchases

Most frequently used—no grace period on new purchases if you carry a balance.

Two-cycle ADB excluding new purchases

Calculated using last 2 billing cycles.

Two-cycle ADB including new purchases

Least consumer friendly method!

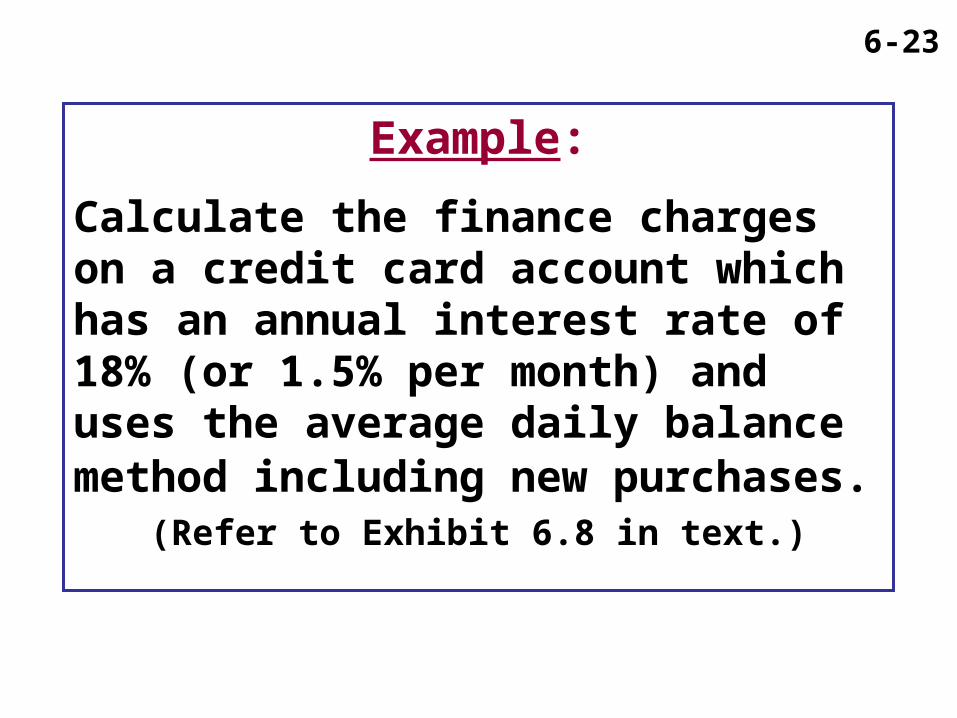

6-23

Example:

Calculate the finance charges on a credit card account which has an annual interest rate of 18% (or 1.5% per month) and uses the average daily balance method including new purchases.

(Refer to Exhibit 6.8 in text.)

6-24

5 $582 $ 2,910

7 932 6,524

15 986 14,790

4 961 3,844

Total: 31 $28,068

ADB = $28,068 31 = $905.42

Monthly APR = .18 12 = .015

Finance charge = $905.42 x .015 = $13.58

ADB Including New Purchases:

# of Days Balance Weighted

(1) (2) Balance (1x2)

6-25Refer to Exhibit 6.7 in text—

What a difference the balance method makes!

Examples shown below all have: Same stated rate of 19.8%Same account activity

Method Finance Charges

ADB including new purchases $132.00

ADB excluding new purchases 66.00Two-cycle ADB

including new purchases 196.20Two-cycle ADB

excluding new purchases 131.20

6-26

Managing Your Credit Cards Review statements promptly each

month and verify each entry.

Pay at least the minimum monthly payment by due date.

Returned merchandise credited to your account.

6-27

Using Credit Wisely

Shop around, comparing:

–Annual fees & other fees

–APR

–Length of grace period

–Balance method

6-28

+Short, interest-free loan

+Simplified record keeping

+Easier resolution to unsatisfactory purchases

+Convenience and emergencies

Disadvantages of Credit Cards–Easy to overspend

–High interest costs

Advantages of Credit Cards

6-29Avoid credit problems by: Using discipline when purchasing. Reducing the number of cards you carry. Being selective in accepting preapproved

credit offers. Not making new charges. Paying more than the minimum. Paying off cards with highest finance charges

first. Transferring balances to card with low

introductory rate and paying off quickly.

6-30

Important Consumer Credit Legislation

Key legislation deals with– Credit discrimination.

– Disclosure of credit information.

– Billing procedures, errors, complaints, and recourse on unsatisfactory purchases.

– Disclosure of finance charges, other fees, credit terms, and loss of credit card.

– Protection against collector harassment.

6-31

Credit Card Fraud Never give account number to someone who

calls you—you must initiate the call. Use only secure Internet sites. Never put credit card info on checks or

personal info on charge slips. Keep your eye on your card! Draw line through blank spaces on slip. Destroy old cards and shred old statements

and slips. Report lost or stolen cards immediately!

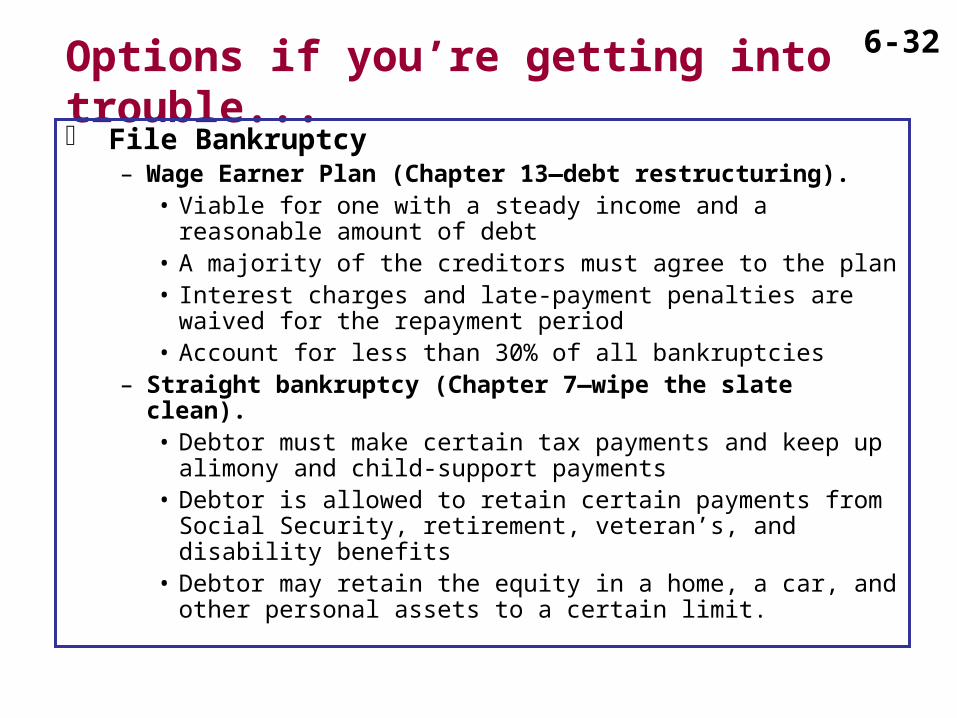

6-32Options if you’re getting into trouble... File Bankruptcy

– Wage Earner Plan (Chapter 13—debt restructuring).• Viable for one with a steady income and a reasonable

amount of debt• A majority of the creditors must agree to the plan• Interest charges and late-payment penalties are waived for

the repayment period• Account for less than 30% of all bankruptcies

– Straight bankruptcy (Chapter 7—wipe the slate clean).• Debtor must make certain tax payments and keep up

alimony and child-support payments• Debtor is allowed to retain certain payments from Social

Security, retirement, veteran’s, and disability benefits• Debtor may retain the equity in a home, a car, and other

personal assets to a certain limit.

6-33Options if you’re getting into trouble... Other bankruptcy options

– Chapter 20: allow individual to wipe out unsecured debt, as per Chapter 7; then use Chapter 13 to restructure their secured debt, including mortgages, home equity loans, and other non-dischargeable debts.

Try credit counselors– Help you prepare a budget and

repayment schedule.– Deal with creditors to possibly reduce

some interest & fees.