50203622-Sharekhan

74

CHAPTER I 1. INTRODUCTION 1.1 INDUSTRY PROFILE Stock market is a market where trading of company stocks, other securities and derivatives takes place. Stock exchanges are corporations or mutual organizations, which are specialized in trading stocks and securities. All sorts of company stocks are enrolled in the stock exchanges. Some of the stock markets in India are listed below: - • Bangalore Stock Exchange • Mumbai (Bombay) Stock Exchange • Calcutta Stock Exchange • Delhi Stock Exchange • Madras Stock Exchange • National Stock Exchange Mumbai (Bombay) stock exchange is India’s first stock exchange. It was founded in 1875 with total number of listed stocks being more than 6,000. In India there are total 22 stock exchanges operating across the country. The National Stock Exchange (NSE) is situated in Mumbai The small and medium sized companies can list their stocks in Over The Counter Exchange of India (OTCEI). The Securities and Exchange Board of India (SEBI) regulates the functioning of capital market and protects the interests of the investors. It is situated in Mumbai. Some functions of SEBI are as follows: - • Regulation of working in stock exchanges and other securities markets. • Registration and regulation of the operation of collective investment plans, including mutual funds. • Inhibition of fallacious and unfair business practices in the securities markets. • Controlling accomplishment of shares and takeover of companies. Stock exchange means any body of individuals, whether incorporated or not, constituted for the purpose of regulating or controlling the business of buying, selling or dealing in securities. 1

-

Upload

nadeem-khan -

Category

Documents

-

view

313 -

download

43

Transcript of 50203622-Sharekhan

CHAPTER I1. INTRODUCTION

1.1 INDUSTRY PROFILEStock market is a market where trading of company stocks, other securities and derivatives

takes place. Stock exchanges are corporations or mutual organizations, which are specialized in

trading stocks and securities. All sorts of company stocks are enrolled in the stock exchanges.

Some of the stock markets in India are listed below: -

• Bangalore Stock Exchange

• Mumbai (Bombay) Stock Exchange

• Calcutta Stock Exchange

• Delhi Stock Exchange

• Madras Stock Exchange

• National Stock Exchange

Mumbai (Bombay) stock exchange is India’s first stock exchange. It was founded in 1875

with total number of listed stocks being more than 6,000. In India there are total 22 stock

exchanges operating across the country. The National Stock Exchange (NSE) is situated in

Mumbai The small and medium sized companies can list their stocks in Over The Counter

Exchange of India (OTCEI).

The Securities and Exchange Board of India (SEBI) regulates the functioning of capital

market and protects the interests of the investors. It is situated in Mumbai. Some functions of

SEBI are as follows: -

• Regulation of working in stock exchanges and other securities markets.

• Registration and regulation of the operation of collective investment plans, including

mutual funds.

• Inhibition of fallacious and unfair business practices in the securities markets.

• Controlling accomplishment of shares and takeover of companies.

Stock exchange means any body of individuals, whether incorporated or not, constituted for

the purpose of regulating or controlling the business of buying, selling or dealing in securities.

1

These securities include:

(i) Shares, scrip, stocks, bonds, debentures stock or other marketable securities of a like nature in

or of any incorporated company or other body corporate;

(ii) Government securities; and

(iii) Rights or interest in securities.

History of stock market in India

The working of stock exchanges in India started in 1875. BSE is the oldest stock market

in India. The history of Indian stock trading starts with 318 persons taking membership in Native

Share and Stock Brokers Association, which we now know by the name Bombay Stock

Exchange or BSE in short. In 1965, BSE got permanent recognition from the Government of

India. National Stock Exchange comes second to BSE in terms of popularity. BSE and NSE

represent themselves as synonyms of Indian stock market. The history of Indian stock market is

almost the same as the history of BSE.

There are 23 recognised stock exchanges in India Bombay Stock Exchange ,National

Stock Exchange, Ahmadabad Stock Exchange, Bangalore Stock Exchange,

Bhubaneswar Stock Exchange, Calcutta Stock Exchange, Delhi Stock Exchange,

Guwahati Stock Exchange, Hyderabad Stock Exchange ,Jaipur Stock Exchange,

Ludhiana Stock Exchange, Cochin Stock Exchange, Coimbatore Stock Exchange,

Madhya Pradesh Stock Exchange, Magadh Stock Exchange, Madras Stock Exchange,

Mangalore Stock Exchange, Meerut Stock Exchange ,OTC Exchange Of India

Pune Stock Exchange, Saurashtra Kutch Stock Exchange, Uttar Pradesh Stock Exchange,

Vadodara Stock Exchange.

1.2. COMPANY PROFILE

Name of the company : Sharekhan ltd.

Year of Establishment : 1925

Admin office : ShareKhan SSKI

2

A-206 Phoenix House 2nd floor,S.B.Marg, Lower Parel Mumbai - Maharashtra, INDIA- 400013

Nature of Business : Service Provider

Services : Depository Services, Online Services and

Technical Research.Core Services :

Equity and Derivatives trading on BSE and NSE

1. Depository Services

2. Online Trading

3. IPO Services

4. Commodity Trading on MCX and NCDEX

5. Port folio Management services.

Number of Employees : Over 3500

Revenue : Data Not Available

Website : www.sharekhan.com Slogan : Your Guide to The Financial Jungle.

1.2.1. Background and inception of the company

Origin and Growth

Sharekhan is a retail broking arm of S.S. Kantilal Ishwarlal Investors Services Pvt. Ltd.,

An organization with more than 8 decades of trust and credibility in the stock market. Sharekhan

Ltd (Formally SSKI Investors Services Pvt Ltd.) was promoted by Mr. Shripal. S Morkharia and

Mr. Shreyas. S Morkhia. It is currently India’s largest broking house. It is a member of the stock

3

exchange, Mumbai. It is a depository participant of the NSDL and CDSL. Its business includes

stock broking, depository services, portfolio management and derivatives.

The company’s core specialty lies in its retail distribution with a large network of

branches i.e. 510 share shops (retail shops) in 170 cities in India and sub-brokers/authorized

persons. Its strengths lies in its investment research capabilities. Its research division has several

analysts continuously monitoring global, national and regional political, economic and social

situations so as to assess their impact on the economy in general, the sectors so as to assess their

impact on the economy in general, the sectors and companies they research which helps them if

offering quality research and advice to clients.

The SSKI Group Comprises of Institutional broking and Corporate Finance. The

Institutional broking division caters to domestic and foreign institutional investors, while the

Corporate Finance Division focuses on niche areas such as infrastructure. Telecom and media.

SSKI has been voted as the Top Domestic Brokerage House in the research category by Euro

Money Survey and by Asia Money Survey.

For the derivates segment, to educate the potential investors towards the share market

they provide a study kit named the ‘Derivative Digest’. And for potential investors wanted to

start the trading in the share market also provided with the study kit ‘First Step to investing in the

share market’, gives them a general understanding about how the share market operates, and it

also gives an idea regarding the role of share brokers in the Capital Market.

These are the wide-raging services offered by the share khan to its customers. And most

importantly. Share Khan is blessed with well-dedicated sales wings, who are looking after the

various needs of the customers in a committed manner and which provide the customers with

tremendous amount of satisfaction and happiness about their investment.

1.2.2. Nature of the Business Carried

Sharekhan is a broking company. The company offers a complete range of pre trade,

trade and post trade service on the BSE (Bombay Stock Exchange) and the NSE (National Stock

Exchange). Whether the client come in to the company’s conventionally located officers and

4

trade in a dedicated ambience or issue instructions over the phone, our highly trained team and

sophisticated equipment ensure smooth transactions and prompt service.\

• Investment Advisory Service

• Facilitation Services to Retail Investors, Corporate.

• Depository Services

• Investment options includes :

i. Online trading (Includes equity, derivatives)

ii. Commodities trading

iii. Mutual Funds

iv. Portfolio management Services

Sharekhan Branches are conceptualized to be place where investors can come in contact

with investment opportunities in an atmosphere of convenience and comfort. Our services are

available through our network of 510 Share Shops spanning 170 major towns and cities in the

country. Professional seeks to educate clients and end their confusion by custom an Investment

Plan according to the needs of clients and is also today a part of company’s induction program

advising employees on how to plan their investments.

1.2.3. VISION, MISSION & QUALITY POLICY

Vision

Sharekhan practices customer centric approach to be leading broking Firm. The Company Vision

is:

i. To be the top most company for providing investment advisory and financial planning

services in India.

ii. To be a leading investment intermediary for transaction through both online and offline

medium.

Mission

5

To educate and empower the individual investor to make better investment decisions through

quality advice and superior service.

a) Educate and empower

i. Research backed advice, which is easy to understand, retail specific, and discipline.

ii. Total equity solutions for the entire investment process.

iii. Relationship management

a) Superior service

i. Integrity

ii. Transparency

iii. Professionalism

iv. Information – product, news, operations

v. Hassle free trading

vi. Enjoyable experience our goals is to accomplish top most position in both online and

offline medium of trade and also to remain a customer centric organization.

Quality objectives

Objectives represent, what needs to be accomplished in order to reach the goals.

• To increase the customer base of investors to invest in all kind of securities.

• Sharekhan has one among the largest network of outlets of the either trading firms with

180 outlets.

• To retain the existing consumers with research backed advice and personalized care the

needs of the consumer.

1.2.4. Products and service profile

The different types of products and services offered by Sharekhan Ltd. are as follows:

• Equity and derivatives trading

• Depository services

6

• Online services

• Commodities trading

• Dial-n-trade

• Portfolio management

• Share shops

• Fundamental research

• Technical research

Types of accounts in Sharekhan ltd.

Sharekhan offers two types of trading account for its clients

➢ Classic Account (which include a feature known as Fast Trade Advanced

Classic Account for the online users) and

➢ Speed Trade Account

7

CLASSIC ACCOUNT

This is a product for the retail investor who is risk-averse and hence prefers to invest in

stocks selectively or who does not trade too frequently. There is no volume commitment on the

part of the client. The features of the products are as follows:

The registration charges are Rs. 750/- that is a one-time payment. With the online

package defaults demat a/c. would be opened with SSKI. For the 1st year no demat charges have

to be paid. It’s free.

The client gets exposure of up to 4 time of the deposit amount. For example if the client

has Rs. 5000/- in his/her account he/she can get the exposure up to Rs. 20,000/-

The brokerage applicable is 0.50% on delivery and 0.1 for intra day trading.

This account comes with the following features:

a. Online trading account for investing in Equities and Derivatives b. Free trading through Phone (Dial-n-Trade)

i. Two dedicated numbers(1800-22-7500 and 39707500) for placing the orders using cell phones or landline phones

ii.Automatic funds transfer with phone banking facilities (for Citibank and HDFC bank customers)

iii.Simple and Secure Interactive Voice Response based system for authentication

iv.get the trusted, professional advice of Sharekhan limited’s Tele Brokers v.After hours order placement facility between 8.00 am and 9.30 am

c. Integration of: Online Trading +Saving Bank + Demat Account.

8

d. Instant cash transfer facility against purchase & sale of shares. e. IPO investments. f. Instant order and trade confirmations by e-mail. g. Single screen interface for cash and derivatives.

SPEED TRADE ACCOUNT

This is an internet-based software application, which enables one to buy and sell in an instant. It is ideal for active traders and jobbers who transact frequently during day’s session to capitalize on intra-day price movement.

The company will be merging speed trade and speed trade plus. There will be a common

exe called speed. Trade which allows customers to trade on both case and F & O. account

opening fee Rs. 1000.

This account comes with the following features:

a. Instant order Execution and Confirmation.

b. Single screen trading terminal for NSE Cash, NSE F&O & BSE.

c. Technical Studies.

d. Multiple Charting.

e. Real-time streaming quotes, tic-by-tic charts.

f. Market summary (Cost traded scrip, highest value etc.)

g. Hot keys similar to broker’s terminal.

h. Alerts and reminders.

i. Back-up facility to place trades on Direct Phone lines.

j. Live market debts.

Charge structure

Fee structure for General Individual:

Charge Classic Account Speed Trade Account

Account Opening Rs. 750/= Rs. 1000/=

Brokerage Intra-day – 0.10 %

Delivery - 0.50 %

Intra-day - 0.10%

Delivery - 0.50%

Depository Charges:

Account Opening Charges Rs. NIL

9

Annual Maintenance ChargesRs. NIL first year Rs. 300/= p.a. from second calendar year onward

SERVICE PROFILE

a. Trading Facilities:

Sharekhan as a member of NSE & BSE provides both offline and online trading facilities

nationwide for trading the securities in secondary market to its clients. The Company’s

wide network of outlets spread across the country facilities to executive the orders in

secondary market.

b. Derivatives: (Futures and Options)

The company also facilitates the trading system for trading in secondary market under

future and options segment of NSE and BSE. The equity dealers in the company will be

eager to give insights into the new sets introduction in the Indian Capital market futures

and options.

c. Depositor Services:

Sharekhan is a Depository participant of National Securities Depository Limited and

Central Depository and securities Limited. Sharekhan will open De-mat accounts, which

will investors to convert physical certificates of shares into electronic balances in an

account maintained.

d. Margin Financing:

In the present rolling settlement scenario, Sharekhan understand investor need for

additional capital availability for daily purchaser shares. It offers unique facility avail

finance, for purchasing shares at very competitive interest rates.

e. IPO’s and Mutual Funds:

Sharekhan offers the change of investing in the potentially lucrative IPO market.

Sharekhan is a distribution house for all mutual funds. This is the new scheme introduced

by the company and it also offers schemes catering to investors with varying risk return

profiles.

10

f. Stock lending and Borrowing:

One can place an order of shares with Sharekhan. It is approved intermediary of the

security or lending scheme. These would be sent out the borrowers, these earnings fees

for all investor’s idle shares. Thus Sharekhan fulfils the investor need for borrowing and

lending of shares.

g. Equity Research:

Sharekhan has a highly rated research using involved in macroeconomic studies, industry

and company specific equity research. The research team’s inputs will be available as

daily trading calls, quarterly investment picks and long term investment picks, based on

the fundamentals of particular company and the industry as whole.

h. Internet Trading:

Investors can also trade their securities through this facility by logging into company’s

website. The virtual world that Sharekhan offers online trading services through.

i. Portfolio Management Services:

Sharekhan securities are a registered portfolio manager with SEBI to manage portfolios

on behalf of clients with discretionary and anon discretionary rights this service is a

provision for those who may not have the right time to manage their stocks investment or

require the service of company’s highly specialized professional team.

j. Online Trading:

Share Khan was amongst the pioneers of online trading in India and has launched

Sharekhan.com in February 2000. Since then, they have been at the forefront in

understanding customer needs, analyzing trends and brining innovation in their offerings.

They have online trading products that are customized to the habits and preferences of

investors as well as traders.

11

Features of Online Trading Products:

i. Live streaming quotes

ii. Instant order execution and conformation

iii. Price alerts

iv. Single Screen for equities and derivatives

v. Multiple market watch windows

vi. Real-time portfolio tacking

a. Other Services:

i. Free access to investment advice, from Sharekhan research team.

ii. Sharekhan “value line “ ( A monthly publication)

iii. Daily research reports and market review.

iv. Daily trading calls based technical analysis

v. Cool trading products. (Daring derivatives and market strategy)

vi. Personalized advice.

vii. Live management information.

viii.Internet based online trading session.

ix. Online BSE and NSE executions through BOLT & NEAT terminals.

Bank Connection:-

Sharekhan has affiliation with 11 banks, which allows its customers to enjoy the facility of instant credit and transfer of funds from his savings bank account to his Sharekhan trading account. The affiliated banks are as follows:

• HDFC BANK • UTI BANK • CITY BANK • ICICI BANK• OBC BANK• UNION BANK • INDUSAND BANK• IDBI BANK• CENTURION BANK• AXIS BANK• YES BANK

1.2.5. Areas of operation:

12

Sharekhan provides a wide range of services nationwide to a substantial and diversified

client base that includes retail clients, high net worth individuals, corporates and financial

institutions.

It has presence in more than 280 cities through its network of longstanding franchisees

and sub brokers.

It has its presence globally i.e in UAE also.

1.2.6. Management team

Dinesh Murikya : Owner of the company

Tarun Shah : CEO of the company

Shankar Vailaya : Director (Operations)

Jaideep Arora : Director (Products & Technology)

Pathik Gandotra : Head of Research

Rishi Kohli : Vice President of Equity Derivatives

Nikhil Vora : Vice President of Researc

1.2.7. Competitors information:

13

Sharekhan is one of the major player in on line Trading. In Mumbai the main

competitors of Sharekhan are ICICI Direct, India bulls, Kotak Securities, HDFC Securities,

Anand Rathi, Motilal Oswal, Religare securities and reliance securities.

Religare Securities:

Religare is a global financial services group with a presence across Asia, Africa,

Middle East, Europe and the Americas. In India, Religare’s largest market, the group offers a

wide array of products and services ranging from insurance, asset management, broking and

lending solutions to investment banking and wealth management. The group has also

pioneered the concept of investments in alternative asset classes such as arts and films .With

10,000 plus employees across multiple geographies, Religare serves over a million clients,

including corporates and institutions, high net worth families and individuals, and retail

investors.

Religare Enterprises Limited is part of a family of companies that fall under the

broader Religare brand, which includes other global businesses such as diagnostics, aviation

and travel, wellness retail, and IT products and solutions. A diversified financial services

group Religare Enterprises Limited (REL) offers a comprehensive suite of customer-focused

financial products and services targeted at retail investors, high net worth individuals and

corporate and institutional clients.

REL, along with its joint venture partners, offers a range of products and services in

India, including asset management, life insurance, wealth management, equity and

commodity broking, investment banking, lending services, private equity and venture capital.

Religare has also ventured into the alternative investments sphere through its holistic arts

initiative and film fund.

Kotak Securities:

Kotak Mahindra is one of India's leading financial conglomerates, offering complete

financial solutions that encompass every sphere of life. From commercial banking, to stock

14

broking, to mutual funds, to life insurance, to investment banking, the group caters to the

financial needs of individuals and corporates.

Kotak Securities Ltd., a 100 % subsidiary of Kotak Mahindra Bank is one of the

oldest and largest broking firms in the industry. Their offerings include stock broking

through the branch and Internet, Investments in IPO, Mutual funds and Portfolio

management service.

Reliance Securities Ltd:

Reliance Securities Limited is a Reliance Capital company and part of the Reliance

Anil Dhirubhai Ambani Group. “Reliance Money” is a brand owned by Reliance Capital

Limited. Reliance Securities with the permission of Reliance Capital Limited uses the

“Reliance Money” brand to market its various services.

Reliance Securities endeavours to change the way investors transact in equities

markets and avails services. It provides customers with access to Equity, Derivatives,

Portfolio Management Services, Investment Banking, Mutual Funds and IPOs. It also offers

secured online share trading platform and investment activities in secure, cost effective and

convenient manner. To enable wider participation, it also provides the convenience of trading

offline through variety of means, including Call & Trade, Branch dealing Desk and its

network of affiliates.

Reliance Money through its pan India presence with 6,233 outlets has more than 3.5

million customers. Reliance Capital is one of India's leading and fastest growing private

sector financial services companies, and ranks among the top 3 private sector financial

services and banking groups, in terms of net worth.

1.2.8. Infrastructural facilities

Sharekhan investment outlets are designed to be places where retail investors can come in

touch with investment opportunities in an atmosphere of convenience and comfort. The look and

15

feel of the offices across India projects a consistent branch image for the company. The features

that enable a unique facility for retailing financial services include among others:

Easily visible branches set up in the commercial spaces of potential investment zones ranging

between 750 sft to 1000 sft.

Most branches are located in the ground floor sporting huge glass frontage promoting

easy accessibility and reflecting our attitude of complete transparency.

The major portion of the branch area dedicated for customer use. The furniture is in CKD

formats to add flexibility in using the branch for investor’s purposes.

Connectivity to NSE for trading facilities.

TV and other electronic mediums to facilitate real time update and dissemination of

information to our customers.

Each branch comprises of trained and qualified investment advisors to take care of the needs of

the customers.

1.2.9. Achievements of Sharekhan

1. Rated among the top 20 wired companies along with Reliance, HUJl, Infosys, etc by

‘Business Today’, January 2004 edition.

2. Awarded ‘Top Domestic Brokerage House’ four times by Euro money and Asia

money.

3. Pioneers of online trading in India amongst the top 3 online trading websites from

India. Most preferred financial destination amongst online broking customers.

4. Winners of “Best Financial Website” award.

5. Voted by CNBC Awaaz as the Most Preferred Stock broker in India in 2005.

1.2.10. Work flow model

At Sharekhan it’s believed that, “The clients are people, not accounts” hence successful

investment management relationship begins with a clear understanding of each client’s specific

needs, concerns and long-term objectives. Sharekhan investment philosophy applies a disciplined

16

approach to building a customized strategy designed to meet customer’s individual financial

goals and tolerance for risk.

1.2.11. Future Plans and prospectus:

i. 2, 00,000 plus retail customers being serviced through centralized call centres /

web solutions.

ii. Branches / Semi branches servicing affluent / aggressive traders through high skill

financial advisor.

iii. 250 independent investment managers/ franchisee servicing 50,000 highly valued

clients

iv. New initiatives Portfolio management Services and commodities trading

CHAPTER II

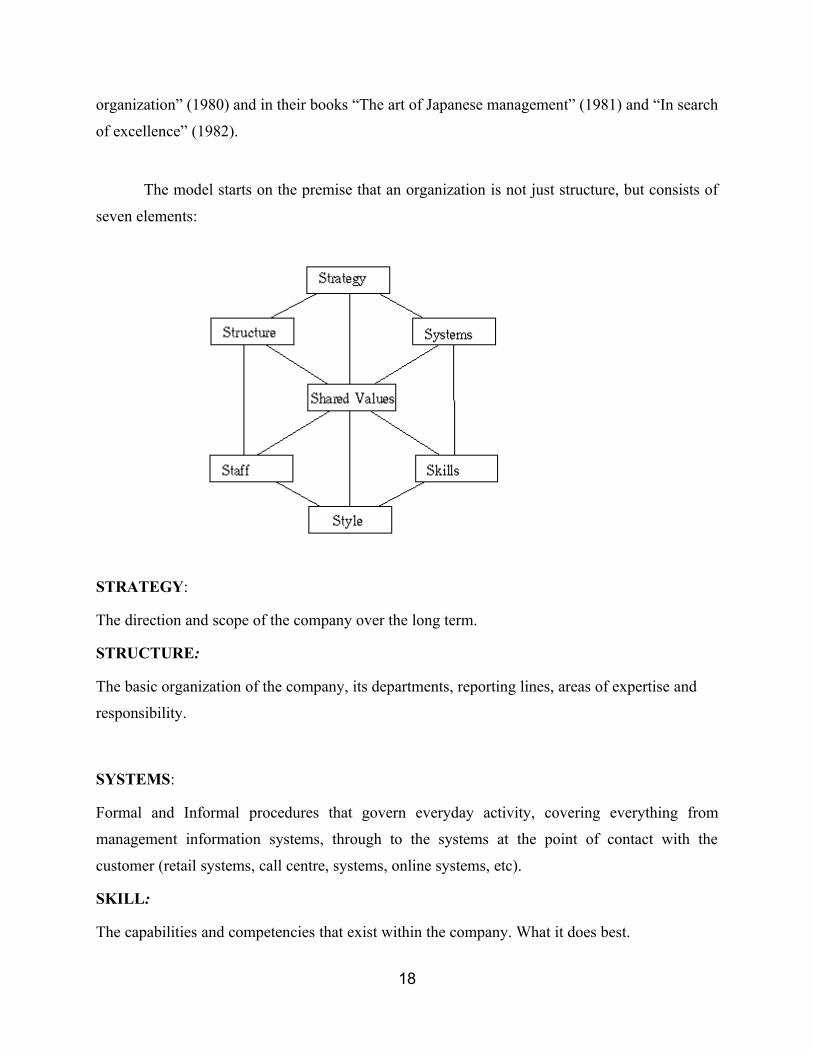

McKinsey 7 s framework with special reference to organisation under study.

The 7-S model is better known as McKinsey 7-S model. This is because the two persons

who developed this model, Tom Peters and Robert Waterman, have been consultants at

McKinsey & co. at that time. They published their 7-S model in their article “Structure is not

17

organization” (1980) and in their books “The art of Japanese management” (1981) and “In search

of excellence” (1982).

The model starts on the premise that an organization is not just structure, but consists of

seven elements:

STRATEGY:

The direction and scope of the company over the long term.

STRUCTURE:

The basic organization of the company, its departments, reporting lines, areas of expertise and

responsibility.

SYSTEMS:

Formal and Informal procedures that govern everyday activity, covering everything from

management information systems, through to the systems at the point of contact with the

customer (retail systems, call centre, systems, online systems, etc).

SKILL:

The capabilities and competencies that exist within the company. What it does best.

18

SHARED VALUES:

The values and beliefs of the company. Ultimately they guide employees towards ‘valued’

behaviour.

STAFF:

The company’s people resources and how they are developed, trained and motivated.

STYLE:

The leadership approach of top management and the company’s overall operating approach.

THE 7S MODEL WITH REFERENCE TO SHAREKHAN:

STRATEGY:

Sets out the vision, mission, objective and major action plans and policies of the

organization. These set out the picture of the organization in the future typically spelling out the

overall corporate strategy, the Strategic business unit strategy and functional Strategies. It can

also be defined as the choice of direction and action that the company adopts to achieve its

objective in a competitive situation. It is the first step that the company has to take in leading its

organization to ladder of success. The major areas of Strategic Goals of Sharekhan are:

Major Description

a. Market Standing Desired share of present and new markets, including areas

in which new products are needed and service goals aimed

at building customer loyalty.

b. Innovation Innovation in products/ services as well as innovation in

skill and activities required to supply them.

c. Human Resources Supply, development and performance of manager’s

employee attitudes.

d. Financial Resources Sources of capital supply and how it will be utilized.

e. Physical Resources Physical facilities and how they will be utilized in

providing services.

19

f. Productivity Efficient use of resources relatives to outcomes.

g. Social Responsibility Responsibilities in such area as concern for community and

ethical behaviour.

STRUCTURE:

Include policies and procedures that govern the way in which the organization acts within

the organization. It provides the frame work for relationship among different parts of the

organization. It sets out formal reporting relationships, mode of communication, their respective

roles and rules and regulation for carrying out different tasks. If it is not properly defined it has a

detrimental effect on the effective and efficient working because motivation and morale is low,

decision are delayed and are of poor quality the expenses rises, orders are lost due to

competition, lack of confidence etc.

Structure of any organization has to answer the following questions-

• What is basic structural form?

• How centralized versus decentralized is the organization?

• What is the relative status and power of the organization?

At sharekhan the structure is clearly defined. Sharekhan has its 620 share shops across

280 cities in India with the headquarters situated at Mumbai. The registered Office is centralized

at residency road, Bangalore. Sharekhan has its operations distributed throughout India. I.e. in

the north and southern regions. The southern region covers areas like Karnataka, Andhra

Pradesh, Kerala and Tamilnadu.These areas are managed by a Regional Branch Head who takes

care of operation in these respective areas. The organization chart for the regional office and its

branches are as follows.

ORGANISATION CHART:

20

HEAD OFFICE Chairman

SYSTEMS:

Systems in their frame work stands for the rules and regulations, procedures and practices that

must be allowed to carry out the tasks in the organization. A good system adds to the efficient

and effective working of the entrepreneur. At Sharekhan in Chintamani the procedure followed is

clear, transparent and not complicated.

The information systems at the various branches of sharekhan are followed by submission of

MIS reports at end of their day to day activities. The activities of the front end operation include:

• Client Advisory Services

• Processing of demat account transactions.

• New issue promotions.

• Portfolio Management of NRI clients.

• Promotions activities for promotions of various funds (New Recommended ones).

• Finally MIS reporting of day to day transactions.

At the back office day to day operations include-

• Processing of various application forms of demat account IPO’s and forwarding the same

to the Head office.

• Providing statement of account to the investors on request.

• Addressing requests for nonpayment of sub broker’s commission.

• MIS reporting of day to day transactions.

21

Regional Heads Zonal Heads

Sr. Regional Jr. Regional

Regional Product Heads

Branch Relationship

Dealers

Sales TeamBack Office

The Total Quality Control System of Sharekhan has created principles about its quality

philosophy-

• Create constancy of purpose and improve services for long range needs rather than short

term profitability.

• Search continually problems in the system and improve processes.

• Encourage effective two way communication and other means to drive fear throughout

the organization and help people to work more productively.

The Electronic Data Processing (EDP) department of Sharekhan takes care of both offline

and online transactions. In the online transactions, online trading takes place using neat software.

It is connected to NSDL, CDSL, NSE and BSE and helps stock brokers to trade online. The

offline is mainly connected for the purpose of conversion of physical form of shares to electronic

form.

STYLE:

Style includes Leadership style of top management and overall operating style of the

organization. Style impacts the norms people follow and they work and interact with each other

and with customers.

• How does the top management make decisions – Participatory Vs Top Down?

• How do managers spend their time in informal meetings, informal conversations, etc?

At sharekhan, they follow a very in effable style of functioning.

• Managers, staff etc are approachable (a perfect blend of formal and informal approaches).

• They follow the system of performance appraisal on 180 degree appraisal model.

Rewards are given according to the performance.

• Personal attention to the project trainees helps in creating a good image in the eyes of the

public.

• Staff has very good informal conversations that develop a sense of loyalist, motivation,

dedication within the employees.

• Emergency meetings are held where top management and employees collectively

participate- targets for the week is set, responsibilities are delegated, suggestions are

invited.

22

• There is a good cordial relation between the management and the employees which

shows a participatory leadership style is observed.

• STAFF:

The staffing procedure mainly includes how the organization has to look into its

people, their backgrounds, and competencies. Staff also includes the organization

approaches to recruitment, selection and specialization. How people developed, how

recruits are trained, socialized and integrated and how their careers are managed?

• At Sharekhan, there are around 3500 employees working across India.

• At Sharekhan, Chintamani branch there are about 10 employees.

• The candidates are recruited from diverse fields of commerce like B. Com’s,

MBA’s, ICWA’s, CA’s and CFA’s great opportunity for fresher’s and post

graduates are available.

• They are involved in all the required meetings and activities.

• The Staff are given freedom to use their innovation and creative skills.

• Get together are held for staff members to socialize.

• Staff grievances are given a listening in a year.

SKILLS:

Include distinctive competencies that reside in the organization. These can be distinctive

competencies people, management practices, systems and technology. What new capabilities the

organization needs to develop, which one does it need to unlearn to compete in future. This can

be learnt through a SWOT Analysis.

The competent skills of the people include good communication and presentation skills,

strong academic record, consistent in the performance levels etc.

SHARED VALUES:

Refers to core/ fundamental values that are widely shared in the organization and serve as

guiding principles that are important. These values have great meaning because they focus

attention and provide a broader sense and purpose. They also give a strong basis for stabilities to

23

the organization, in a rapidly changing environment by providing a basic meaning to people

working in the organization.

• Do people have a shared understanding of why a company exits?

• Do people have a shared understanding of the vision of the company?

• How do people describe the ways in which the company is distinctive?

At Sharekhan, which is primarily a client or investor oriented organization has embedded this

quality among all its member employees. The member’s work today towards the growth and

success of the unit. The employees share responsibility and protect the company’s name and

integrity. There is no sharing of confidential/ important information with the outsiders. There is

collective responsibility and accountability on the part of its members. This can be said as the

shared values of the employees of the organization.

CHAPTER III

SWOT ANALYSIS:

24

A SWOT analysis is a tool, used in management and strategy formulation. It can help to identify

the Strengths, Weaknesses, Opportunities and Threats of a particular company.

Strengths and weaknesses are internal factors that create value or destroy value. They can

include assets, skills, or resources that a company has at its disposal, compared to its

competitors. They can be measured using internal assessments or external benchmarking.

Opportunities and threats are external factors that create value or destroy value. A company

cannot control them. But they emerge from either the competitive dynamics of the

industry/market or from demographic, economic, political, technical, social, legal or cultural

factors.

SWOT MATRIX:

SWOT MatrixINTERNAL

EXTERNAL

(S)

Internal

Strengths

(W)

Internal

Weakness

(O)

External Opportunities

(T)

External

Threats

SO Strategies

Use ‘S’ to take advantage of ‘O ’

WO Strategies

Take advantage of ‘O’ by overcoming

‘W’

ST Strategies

Use ‘S’ to avoid ‘T’

WT Strategies

Minimize ‘W’ and avoid ‘T’

Strengths Global parentage and expertise.

Experience senior management.

World class technology and infrastructure.

Strict risk control systems.

Fundamental and technical research.

25

Multiple products under one roof.

Company with well diversified portfolio.

Weakness Many competitors.

No direct marketing strategy.

Payment services are not good.

No global reach.

Weak brand name.

Opportunities To grab the growing Indian market.

Scope for taking its business overseas and going global.

Scope for increasing its branch network especially in the important financial centres as

well as extending its physical presence in other parts of the country.

Up gradation of the latest technology to give better and faster service to its clients

Threats Global economic slowdown.

The Indian capital market is fluctuating.

The ever increasing and challenging neck-to-neck competition specially with those

established and existing reputed stock broking companies.

Uncertainty of the market and volatility and fluctuations in the stock prices.

Change in customer needs, preferences and taste.

Threat from new entrants into the field of stock broking.

CHAPTER IV

Analysis of balance sheet.

The equity share capital has remained more or less the same. There is 16.6 percentage increases

in Reserves and surplus in 2009 over the previous year. Investments increased by 50 percentage.

CHAPTER V

26

Learning experience.

The opportunity of undergoing an in plant training for one month duration is being capitalized by

me by increasing my knowledge base by working at Sharekhan.

I am privileged to highlight some of the learning experience got from this training.• It helped to link the theories, techniques and practices of management with

different activities of the organization in trading operations

• It increased my conceptual understanding of the entire subject financial derivatives.

• Basically stock market investments are considered to be very risky, but if the scrip’s selected by the investor is favorable according to the market conditions than the investor will be able to generate high profit within a short time span.

CHAPTER VI

INTRODUCTION TO THE CONCEPT

“Derivative is a product whose value is derived from the value of one or more basic

variables called bases (underlying asset, index or reference rate) in a contractual manner”.

Through the use of derivative products, it is possible to partially or fully transfer price

risks by locking-in asset prices.

As instruments of risk management, these generally do not influence the fluctuations in

the underlying asset prices. However by locking-in asset prices, derivative products minimize the

impact of fluctuations in the asset prices on the probability and cash flow situation of risk-averse

investors.

27

The wide array of risks that a business firm is exposed to may be classified into five categories:

Technological risk- arises mostly in the R&D and operations stages of the value chain.

Economic risk- stem from fluctuations in revenues and production costs.

Financial risk- arises from the volatility of interest rates, currency rates, commodity prices, and

stock prices.

Performance risk- arises when the contracting counterparties do not fulfill their obligations.

Legal and regulatory risk- arises from changes in laws and regulations.

WHY TOTAL RISK MATTERS

Modern finance theory regards hedging activities aimed at reducing total corporate as

irrelevant. Under certain plausible condition, the CAPM and Arbitrage pricing theory show that

unsystematic risk has no bearing on the required rate of return. Only systematic risk (or market

risk) is priced and, hence, has an influence on the required rate of return.

Since the price of systematic risk is identical for all the participants in the financial

market, a firm or investor does not benefit by laying it off in the financial market. Thus,

according to this line of reasoning, in an efficient financial market the expected NPV of any risk

hedging activity like taking an insurance cover or buying a forward contract is zero. Other things

being equal, a firm or investor with a high total risk exposure is likely to face financial

difficulties which tend to have a disrupting effect on the profit.

FACTORS DRIVING THE GROWTH OF DERIVATIVES.

• Increased volatility in asset prices.

• Increased integration of national financial markets with the international markets.

• Marked improvement in communication facilities and sharp decline in their costs.

• Development of more sophisticated risk management tools, proving economic agents a

wider choice of risk management strategies and

28

• Innovations in the derivatives markets.

DERIVATIVE PRODUCTS

Forwards: A forward contract is an agreement between two parties to exchange an asset for

cash at a predetermined future date called the settlement date for a price that is specified today.

Futures: A futures contract is a standardized forward contract which can be traded on organized

exchanges. In fact, a future is a standardized form of forward contract. A future is a contract or

an agreement between two parties to exchange an assets / currency or commodity at a certain

future date at an agreed price. The trader who promises to buy is said to be in ‘ long position ‘

and the party who promises to sell said be in ‘short position’.

Options: Inboard sense, an option is a claim without any liability. More specifically, an option is

a contract that gives the holder a right, without any obligation, to buy or sell an asset at an agreed

price on or before a specified period of time.

Warrants: Longer dated options which have expiry date up to one year are called warrants.

Leaps: Long Term Equity Anticipation Securities (LEAPS) are the options having a maturity of

up to 3 years.

Baskets: Baskets are the options on portfolios of underlying Assets.

Swaps: Swaps are private agreements between two parties to exchange cash flows in the future

according to pre-arranged formula.

Swaptions: (Options + Forwards) are the options on a forward Swap.

PARTICIPANTS IN DERIVATIVES MARKET:

Hedgers

Speculators

29

Arbitrageurs

ECONOMIC FUNCTIONS OF THE DERIVATIVE MARKET:

Transfer of risks.

Discovery of future as well as current prices.

Higher trading volumes in financial markets.

Acts as a catalyst for new entrepreneurial activity.

Margining, monitoring and surveillance of the activities of various participants.

A. INTRODUCTION TO FORWARDS:

Forward contracts are perhaps the oldest and simplest tools for managing financial risk. A

forward contract represents an agreement between two parties to exchange an asset for cash at a

predetermined future date called the settlement date for a price that a specified today.

For example, if you agree on Jan 1 to buy 100 bales of cotton on July 1 at a price of Rs-

800/- per bale from a cotton dealer, you have entered into a forward contract with the cotton

dealer. As per this contract, on July 1 you will have to pay Rs-80,000/- and the cotton dealer will

have to supply 100 bales.

According to this agreement, you have bought forward cotton or you are long forward

cotton, whereas the cotton dealer has sold forward cotton or is short forward cotton. No money

or cotton changes hand when the deal is signed. The forward contract only specifies the terms of

a transaction that will occur in future.

Features:

They are bilateral contracts and hence exposed to counter party risk.

30

Each contract is custom designed and hence is unique in terms of contract size, expiration

date and the asset type and quality.

The contract price is generally not available in public domain.

On the expiration date, the contract has to be settled by the delivery of the asset.

If the party wishes to reverse the contract, it has to compulsorily go to the same counter

party, which often results in high prices being charged.

Forward contracts are generally used in real estate, commodities, gold, foreign currency

exchange etc.

B. INTRODUCTION TO FUTURES:

A futures contract is a standardized forward contract which can be traded on organized

exchanges. It is similar to the forward contract in all the respect. In fact, a future is a

standardized form of forward contract. A future is a contract or an agreement between two

parties to exchange an assets / currency or commodity at a certain future date at an agreed price.

The trader who promises to buy is said to be in ‘ long position ‘ and the party who promises to

sell said be in ‘short position’. When a futures contract is first listed for trading by an exchange,

interested parties take long or short positions on the contract. When one trader takes a long

position on the contract for a particular price and another trader takes a short position on the

contract at the same price, it generates a trading volume of one contract. At this point there is one

contract which remains to be performed or settled through delivery of the asset in the future.

Thus, there is one open contract. This is also referred to as open interest, which is the

terminology used to describe the number of open contracts or contracts remaining to be settled in

future on any particular day.

Futures contracts are contracts specifying a standard volume of a particular currency to

be exchanged on a specific settlement date. A future contract is an agreement between a buyer

and a seller. Such a contract confers on the buyer an obligation to buy from the seller, and the

seller an obligation to sell to the buyer a specified quantity of an underlying asset at a fixed price

on or before a fixed day in future. Such a contract can be for delivery of an underlying asset.

31

To eliminate counter party risk and guarantee traders, futures markets use a clearing

house which employs initial margin, daily market to market margin; exposures limits etc. to

ensure contract compliance and guarantee settlement. Standardized futures contracts generate

liquidity, greater transparency, fairness and efficiency. Due to these inherent advantages, futures

markets have been enormously successful in comparison with forward markets all over the

world.

Broadly there are two types of futures:

Commodity futures

(Cocoa, Cotton, Aluminum, Gold, Crude oil, Soya bean etc)

Financial futures

(Index futures, stock futures, debt instruments, foreign currencies, monetary

metals etc)

Features:

Traded on an organized exchange with Notation.

Standardized contract terms are defined by exchange.

Requires margin payment.

They are marked-to-market.

Price is zero and linear payoff.

Both long and short at risk.

The price of a futures contract is determined on the floor of the exchange by forces of demand

and supply. A margin is a deposit to be made to the clearing house by the parties entering into a

futures contract. There are three types of margins:

Initial margin or performance margin

Maintenance margin

32

Variation margin

The difference between forward contract and future is that future is a standardized

contract in terms of quantity, date and delivery. It is traded on organized exchanges, so it has

secondary markets. Future contract is always settled daily, irrespective of the maturity date

which is called marking to the market.

C. INTRODUCTION TO OPTIONS:

Inboard sense, an option is a claim without any liability. More specifically, an option is a

contract that gives the holder a right, without any obligation, to buy or sell an asset at an agreed

price on or before a specified period of time.

Types of options:

1) Call option: - Gives the buyer the right, but not the obligation to buy a specific futures

contract at a predetermined price within a limited period of time.

A call option is a contract, which gives the owner the right to buy an asset for a

certain price on or before a specified date. For example, if you buy a call option on a certain

share of XYZ Company, you have the right to purchase 100 shares (assuming of course, that the

option involves 100 shares).

Suppose current share price (S) of Reliance Industries is Rs-291/-. You expect that price

in a three months period will go up Rs-300/-. But you also fear that the price may also fall below

Rs-291/-. To reduce the chance of risk and at the same time to have the opportunity of making

profit, instead of buying the share, you can buy a 3-month call option on Reliance Industries at

an agreed exercise price (E) of, say, RS-280/-. Ignoring the option premium, taxes, transaction

costs and the time value of money, the decision to exercise your option depends upon the share

price after three months. You will exercise option when the share price after three months is

33

above Rs-280/- and you will not exercise when the share price after three month is below Rs-

240/-.

Thus option should be exercised when:

Share price at expiration > Exercise price = St>E

Do not exercise option when:

Share price at expiration <= Exercise price =St<E

The value of call option at expiration is:

Value of call option at expiration= Maximum [(share price –exercise price), 0]

Ct = Max [(St – E), 0]

The expression above indicates that the value of call option at expiration is the maximum

of the share price minus the exercise price and zero. The call option holder’s opportunity to make

profit is unlimited. It depends on the actual market price of the underlying share when the option

is exercised. Greater the market value of the underlying asset, the larger is the value of the

option. The following figure shows the value of call option.

Value of call option

Unlimited pay off

0 Value of share Out-of-money in the money

Fig. 1.1 Pay-off of a call option buyer

It may be observed from the above figure 1.1 that the possible outcomes can be divided

into two parts: one above the exercise price and other below the exercise price. The outcome

above the exercise price are said to be In-the-money and are beneficial to the option holder but

34

Exercise price

not the outcome below the exercise price. It is the exercise price that divides the good and bad

outcomes.

For the call option writer, he will gain when share price is below the strike price and will

lose when stock price is above the strike price. The call buyer’s gain is call seller’s loss. The

figure 1.2 shows the pay-off of a call option writer.

In –the- money out –of money(Good outcome) (Bad outcome)

0Value of share

Exercise price

Value of call option

Fig. 1.2 Pay –off of a call option writer.

2) Put option: - Gives the buyer the right, but not the obligation, to sell a specific futures

contract at a predetermined price within a limited period of time.

Put option is a contract that gives the holder a right to sell specified shares at an agreed

price on or before a given maturity. Thus, if you buy a put option on shares of XYZ Company,

you have the right to sell 100 shares of this company at the specified price at any time between

today and the specified date.

Suppose the current price (S) of

Reliance Industries is Rs. 291 and you

expect that the price will fall within a

three months. Therefore, you can buy a

3-month put option on Reliance

Industries at an agreed exercise price

35

(E), say, Rs. 295. If the price actually falls to (St) Rs. 280 after three months, you will exercise

your option. You will buy the share for Rs. 280 from the market and deliver it to the put-option

writer to receive Rs. 295. Your gain is Rs.15 ignoring the put option premium, transaction cost

and taxes. You will not exercise if the share price rises above exercise price; the put option is

worthless and its value is zero.

Thus, exercise the put option when

Exercise price >Share price at expiration = E > St

Do not exercise put option when

Exercise price <=Share price at expiration = E<St

The value of put option at expiration will be

Value of put option at expiration= Maximum [(Exercise price –Share price), 0]

Pt = Max [(E-St), 0]

PROFIT

Limited profit

Exercise price

Value of share0

In-the moneyout-of-money

Fig. 1.3 Pay-off for a put option buyer

The figure 1.3 shows that the

value of put option for the put option

holder depends on the value of

underlying asset .The value of put option is zero when it is out of the money. The potential profit

of the put option is limited because share price cannot fall below zero.

36

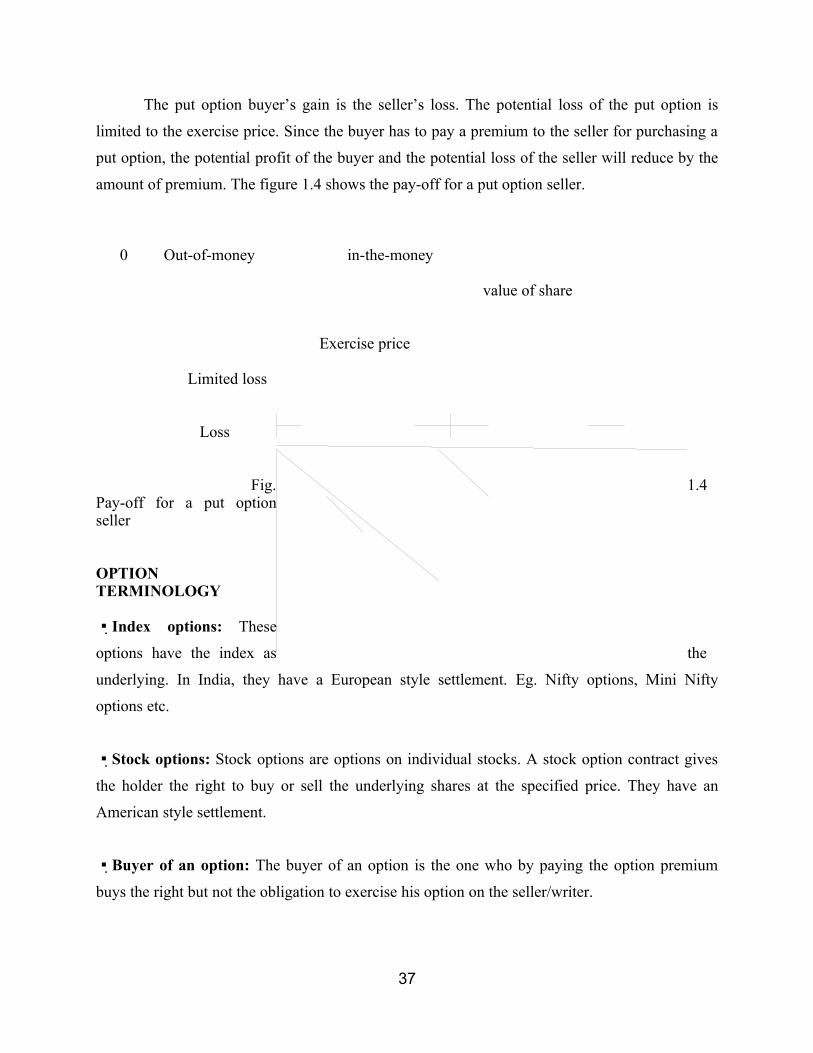

The put option buyer’s gain is the seller’s loss. The potential loss of the put option is

limited to the exercise price. Since the buyer has to pay a premium to the seller for purchasing a

put option, the potential profit of the buyer and the potential loss of the seller will reduce by the

amount of premium. The figure 1.4 shows the pay-off for a put option seller.

0 Out-of-money in-the-money

value of share

Exercise price

Limited loss

Loss

Fig. 1.4 Pay-off for a put option seller

OPTION TERMINOLOGY

Index options: These

options have the index as the

underlying. In India, they have a European style settlement. Eg. Nifty options, Mini Nifty

options etc.

Stock options: Stock options are options on individual stocks. A stock option contract gives

the holder the right to buy or sell the underlying shares at the specified price. They have an

American style settlement.

Buyer of an option: The buyer of an option is the one who by paying the option premium

buys the right but not the obligation to exercise his option on the seller/writer.

37

Writer / seller of an option: The writer / seller of a call/put option is the one who receives the

option premium and is thereby obliged to sell/buy the asset if the buyer exercises on him.

Call option: A call option gives the holder the right but not the obligation to buy an asset by a

certain date for a certain price.

Put option: A put option gives the holder the right but not the obligation to sell an asset by a

certain date for a certain price.

Option price/premium: Option price is the price which the option buyer pays to the option

seller. It is also referred to as the option premium.

Expiration date: The date specified in the options contract is known as the expiration date,

the exercise date, the strike date or the maturity.

Strike price: The price specified in the options contract is known as the strike price or the

exercise price.

• In-the-money option: An in-the-money (ITM) option is an option that would lead to a

positive cashflow to the holder if it were exercised immediately. A call option on the

index is said to be in-the-money when the current index stands at a level higher than the

strike price (i.e. spot price > strike price). If the index is much higher than the strike

price, the call is said to be deep ITM. In the case of a put, the put is ITM if the index is

below the strike price.

• At-the-money option: An at-the-money (ATM) option is an option that would lead to

zero cash flow if it were exercised immediately. An option on the index is at-the-money

when the current index equals the strike price (i.e. spot price = strike price).

• Out-of-the-money option: An out-of-the-money (OTM) option is an option that would

lead to a negative cash flow if it were exercised immediately. A call option on the index

is out-of-the-money when the current index stands at a level which is less than the strike

price (i.e. spot price < strike price). If the index is much lower than the strike price, the

38

call is said to be deep OTM. In the case of a put, the put is OTM if the index is above the

strike price.

• Intrinsic value of an option: The option premium can be broken down into two

components - intrinsic value and time value. The intrinsic value of a call is the amount

the option is ITM, if it is ITM. If the call is OTM, its intrinsic value is zero. Putting it

another way, the intrinsic value of a call is Max[0, (St — K)] which means the intrinsic

value of a call is the greater of 0 or (St — K). Similarly, the intrinsic value of a put is

Max[0, K — St],i.e. the greater of 0 or (K — St). K is the strike price and St is the spot

price.

• Time value of an option: The time value of an option is the difference between its

premium and its intrinsic value. Both calls and puts have time value. An option that is

OTM or ATM has only time value. Usually, the maximum time value exists when the

option is ATM. The longer the time to expiration, the greater is an option's time value, all

else equal. At expiration, an option should have no time value.

European Option: When an option is allowed to exercise only on the maturity date, it is called a

European Option.

American Option: When an option can be exercised any time before its maturity is called an

American Option.

TABLE 1:

Business growth of futures and options market: NSE turnover

(Rs.Cr)

YEAR INDEX

FUTURES

STOCK

FUTURES

INDEX

OPTIONS

STOCK

OPTIONS

TOTAL

TURN

OVER

AVERAGE

DAILY

TURN

OVER

2008-09 2853615 2789329 2672532 164586.4 8480063 46087.32007-08 3820667 7548563 1362111 359136.6 13090478 52153.32006-07 2539574 3830967 791906 193795 7356242 295432005-06 1513755 2791697 338469 180253 4824174 19220

39

2004-05 772147 1484056 121943 168836 2546982 101072003-04 554446 1305939 52816 217207 2130610 83882002-03 43952 286533 9246 100131 439862 17522001-02 21483 51515 3765 25163 101926 4102000-01 2365 - - - 2365 11

Source: www.nseindia.com

TABLE 2:

Derivative instruments available for trade in India (NSE):

PRODUCT

SPECIFICATIONS

INDEX

FUTURES

STOCK

FUTURES

INDEX

OPTIONS

STOCK

OPTIONSUnderlying instrument S&P CNX Nifty Individual securities S&P CNX Nifty Individual securities

Security descriptor N FUTIDX NIFTY N FUTSTK N OPTIDX NIFTY N OPTSTK

Type European American

Contract size Lot size-100 As specified by

exchange

Lot size- 100 As specified by

exchangeExpiry day Last Thursday of the

expiry month

Last Thursday of the

expiry month

Last Thursday of the

expiry month

Last Thursday of the

expiry monthPrice steps Re-0.05 Re-0.05 Re-0.05 Re-0.05

Trading cycle 3 months 3 months 3 months 3 months

Base price-

First day of trading

Previous day closing

Nifty value

Previous day closing

value of underlying

security

Theoretical value

based on Black-

Scholes model

Theoretical value

based on Black-

Scholes modelBase price-

Subsequent

Daily settlement

price

Daily settlement

price

Daily closing price Daily closing price

Price bands Operating ranges are

kept at +10 percent

Operating ranges are

kept at +20 percent

Operating ranges are

kept at 99% of the

base price

Operating ranges are

kept at 99% of the

base priceQuantity freeze 20,000 units or

greater

Lower of 1% of

market wide position

limit stipulated for

open positions or

Rs-5 cr.

20,000 units or

greater

Lower of 1% of

market wide position

limit stipulated for

open positions or

Rs-5 cr.

Settlement basis MTM & final

settlement will be

MTM & final

settlement will be

Cash settlement on

T+1 basis

Daily settlement on

T+1 basis and final

40

cash settled on T+1

Basis

cash settled on T+1

Basis

on T+3 Basis.

Settlement price Closing price for

daily settlement and

closing value on the

expiry day for final

settlement

Closing price for

daily settlement and

closing value on the

expiry day for final

settlement

Premium value for

daily settlement and

the closing value of

index on expiry day

for final settlement

Premium value for

daily settlement and

the closing value on

expiry day for final

settlementBSE also offers similar products in the derivatives segment.

6.1. STATEMENT OF THE PROBLEM:

Through the use of derivative products, it is possible to partially or fully transfer price

risks by locking-in asset prices.

As instruments of risk management, these generally do not influence the fluctuations in

the underlying asset prices. However, by locking in-asset prices, derivative products minimize

the impact of fluctuations in asset prices on the profitability and cash flow situation of risk–

averse investors. Trading in F&O should be well organized approach for the purpose of which

they are being used, be it to hedging or trading for profits. The study analyses the various

strategies that can be used by traders and investors to get maximum returns in the derivatives

market.The problem is to analyze the derivatives that are traded in India with respect to volatility

of market to minimize the risk of the investor in the derivatives market

6.2OBJECTIVES:

• To study financial derivatives as an investment alternative.

• To suggest option strategy to maximize payoff of an investor.

• To analyze various types of financial derivatives used by investors as an effective tools in

managing risk.

41

• To analyse and recommend whether to buy stock at a reasonable price and position

yourself for a big market move.

• To suggest investors in the arena of financial derivatives market for managing risk

especially in the current recession period.

6.3. RESEARCH METHODOLOGY

The type of research is selected on the basis of problems identified. Here the research

type used is descriptive research. Descriptive research includes fact-findings and enquiries of

different kinds. The major purpose of descriptive research is a description of the state of affairs,

as it exists in the present system. In this project an attempt has been made to analyze various

option strategies in the option market and how they help to hedge the risk.

6.3.1. DATA COLLECTION:

Secondary data: is collected through text books, websites, newspapers and company brochure, Nifty Spot Rate for the period of Dec 2008-Jan 2009

6.3.2. SAMPLING TECHNIQUE.

Tools of analysis:The research will be conducted by using the strategies of futures, forwards and options – Bullish, Bearish and Neutral Strategies.

6.3.3. PLAN OF ANALYSIS:

42

The study analyses the financial instruments that can be used by the traders and investors

for hedging the risk involved in buying, holding and selling various kinds of financial assets in

derivatives market with special focus on options.

6.4. LIMITATIONS OF THE STUDY:

The study is limited to investors of Sharekhan and its Employees.

The strategies built are subject to Indian stock market risk and uncertain

conditions.

The findings and suggestions are based on existing trends in the secondary

market.

The strategy does not serve the purpose of suggesting a investor, if the investor

change his risk bearing level.

43

CHAPTER VII

7.1DATA ANALYSIS AND INTERPRETATION:

7.1.1. RISK MANAGEMENT WITH FORWARD CONTRACTS:

Forward contracts are perhaps the oldest and simplest tools for managing financial risk. A

forward contract represents an agreement between two parties to exchange an asset for cash at a

predetermined future date called the settlement date for a price that is specified today.

Illustration with current example:

The depreciation of the Indian rupee and a strong upward movement in international gold

prices pushed the yellow metal to a record high of Rs-15,230/- per 10 grams as on Feb. 18 2009.

As investors are increasingly parking their money in gold because of a melting stock market and

erosion in the value of other financial asset classes, the market price of the gold tend to rise

further. So investor can enter in to forward contract to buy gold at a price close to current market

price say Rs-14,755/- per 10 grams to buy on Mar 2 2009. Now according to this agreement,

investor have bought forward gold or in long forward gold. Whereas the gold dealer has sold

forward gold or in short forward gold. No money or gold changes hand when the deal is signed.

The forward contract only specifies the terms of a transaction that will occur in future.

On Mar 2 2009, the contract will be settled so that investor gets the gold at a price of Rs-

14,755/- per 10 grams. If market price of the gold is higher than the contract price, the investor

gets the profit of the difference between the market and contract price or else undergoes loss if

44

the price is lower than market price. By entering into forward contract the investor can avoid the

downside risk.

Suppose if the market price of the gold touches Rs-15,665/- as projected then investor

gets a profit of Rs-910/- per 10 grams.

Risk management with forward contracts:

7.1.2. RISK MANAGEMENT WITH FUTURE CONTRACTS:

When you buy a security, you have a choice. You can buy it in the spot market and get

immediate delivery or you can buy it in the futures market and obtain deferred delivery on

specified future payment.

These differences between purchases in the spot market and futures market suggest the following

relationship between the spot and futures prices.

45

Futures price . = spot price - PV of interest or dividend

(1+ Risk-free rate of interest) t dividend payments foregone

Broadly there are two types of futures:

Commodity futures

(Cocoa, Cotton, Aluminum, Gold, Crude oil, Soya bean etc)

Financial futures

(Index futures, stock futures, debt instruments, foreign currencies, monetary

Metals etc)

Fig. Risk management with futures contract

The futures contract is entered by a margin deposit which is to be made to the clearing house

by the parties as security of possible default risk in the form of 3 types of margins:

1) Initial margin (performance margin) - 5-25percent.

2) Maintenance margin (app. 75 percent of initial margin)

3) Variation margin (additional fund) - if fall below margin level, exchange issue ‘margin

call’ to deposit variation margin.

46

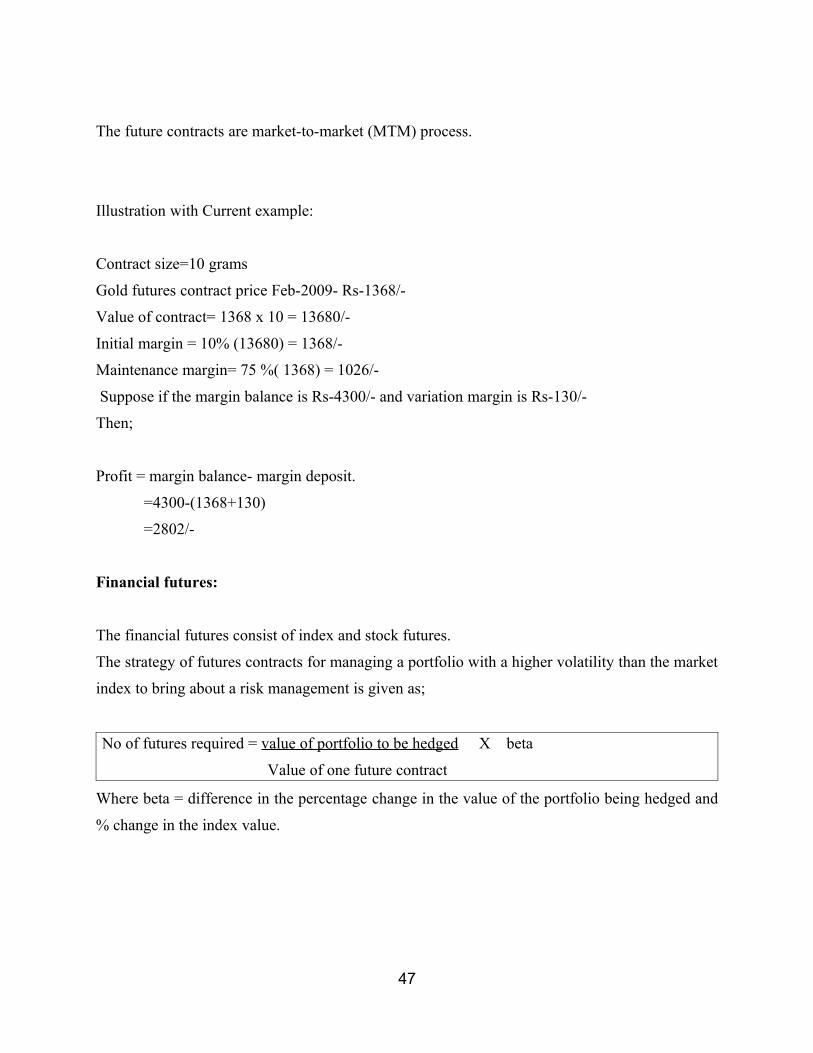

The future contracts are market-to-market (MTM) process.

Illustration with Current example:

Contract size=10 grams

Gold futures contract price Feb-2009- Rs-1368/-

Value of contract= 1368 x 10 = 13680/-

Initial margin = 10% (13680) = 1368/-

Maintenance margin= 75 %( 1368) = 1026/-

Suppose if the margin balance is Rs-4300/- and variation margin is Rs-130/-

Then;

Profit = margin balance- margin deposit.

=4300-(1368+130)

=2802/-

Financial futures:

The financial futures consist of index and stock futures.

The strategy of futures contracts for managing a portfolio with a higher volatility than the market

index to bring about a risk management is given as;

No of futures required = value of portfolio to be hedged X beta

Value of one future contract

Where beta = difference in the percentage change in the value of the portfolio being hedged and

% change in the index value.

47

Illustration with current example;

a) Short position:

Consider the portfolio value is Rs- 60,000/- and nifty is 3046 on Jan 3, 2009.

If the nifty down by 10%, then value of portfolio will be Rs-54,000/- and beta = 1.2

Sell 30 nifty futures @ Rs- 3046 per contract.

Buy 30 nifty futures @ Rs- 2741 per contract.

Gain= 305x30=Rs-9150/-

No. of futures required = 60,000 x 1.2

3046

= 24 no.

b) Long position: (mutual funds)

Investment scheme- Rs-50, 00,000/- and nifty- 3046 on jan3, 2009.

Nifty futures needed= 50, 00,000 = 2500 no.

2000

Conclusion: The strategy is that for managing risk of the portfolio with a higher volatility than

the market index, more futures contracts would be required to bring about a perfect hedge.

48

7.1.3. RISK MANAGEMENT WITH OPTION CONTRACTS:

DATE NIFTY SPOT RATE

16-DEC 2981

17-DEC 3041

18-DEC 2984

19-DEC 3060

20-DEC 3077

23-DEC 3039

24-DEC 2968

25-DEC 2916

28-DEC 2857

30-DEC 2922

31-DEC 2979

01-JAN 2959

02-JAN 3033

03-JAN 3046

06-JAN 3121

07-JAN 3112

08-JAN 2920

10-JAN 2873

13-JAN 2773

15-JAN 2835

16-JAN 2736

17-JAN 2828

49

21-JAN 2796

22-JAN 2706

23-JAN 2713

28-JAN 2771

29-JAN 2849

30-JAN 2823

Table: Nifty Spot Rate for the period of Dec 2008-Jan 2009

The following strategies are analyzed for current market condition and hence forth proper

guidance is given for the investor for managing the risk.

1) LONG CALL:

Where the investor expects the price of the underlying stock to rise, the bought call can

provide leveraged exposure to the price rise. Buying a call also locks in a maximum purchase

price for the life of

the option.

Profits and losses

The maximum loss the investor can suffer is the premium paid for the option, which will

occur if the share price at expiry is below the strike price. The investor breaks even if at expiry

the share price is equal to the strike price of the option plus the premium paid. As the share price

rises beyond this point, the potential profits of the bought call are unlimited.

Current Example:

On 24th Dec 2008, Nifty is quoting at Rs-2968/- and the January- 2950/- (strike price) call

costs Rs-80/- (premium). Buy Nifty call at 80/- Net outlay is Rs-4000/-. If the Nifty index does

go up you can close your position either by selling the option back to the market or exercising

your right to buy the underlying shares at the exercise price.

50

When to use the long call

Market outlook Bullish

Volatility

outlookRising

Possible outcome at expiry

Spot Rate = 3110 Option worth 4000. Closing the position now will produce a net profit of 4000

Spot Rate < 2950 Option expires worthless. The loss is Rs-4000/- (premium)

Spot Rate > 3030 Net profit = intrinsic value of (Break even = 2950+80) option i.e. by whatever amount the share price exceeds 3030/-

Graph 2: Payoff diagram of Long Call

Profit 3110

3030(Break Even)

Loss

2950(Strike Price)

Analysis of Current Example:

Date 24/12/2008 07/01/2009

Spot Price 2968 3012

From Table 1 it is observed that after 7h January market never behaved as per our

expectation. In order to minimize the loss it is better to exercise the option on 7th January, which

will result in loss of (3012-2950-80) × 50 = (900)

Interpretation:

Action 1 If you excise the option 7th January your loss will be 900

Action 2 If you do not excise the option your loss will be 4000

51

Other considerations

Time decay: Time decay works against the buyer of the call. If the expected share price rise

does not take place soon after entering the position, time decay will start to erode the value of the

option.

Strike price: The investor will usually have a choice of strike prices, and must balance the cost

of the option against the rise in share price required for the strategy to be successful. The out-of-

the money option will be the cheapest, but also requires the largest rise in share price. Many

investors regard the at-the-money option as offering the best balance of risk and reward.

Expiry month: A longer-term option allows more time for a rise in the share price to take place,

but will be more expensive than a shorter-term option. The investor needs to form a view of the

time frame over which the share price movement is expected to take place.

Follow-up action

If the share price rise takes place as expected, the call option taker must decide whether

to close out at a profit, or maintain the position in the hope of a further increase in price. The

longer the option position is left open, the greater the effect of time decay.

If the share price does not rise as expected, it is often advisable to close out the position

in order to recover some time value from the position.

If at expiry the option is in-the-money, the investor must choose whether to sell the

option or exercise it. The choice will be determined by whether the investor wants to own the

underlying shares.

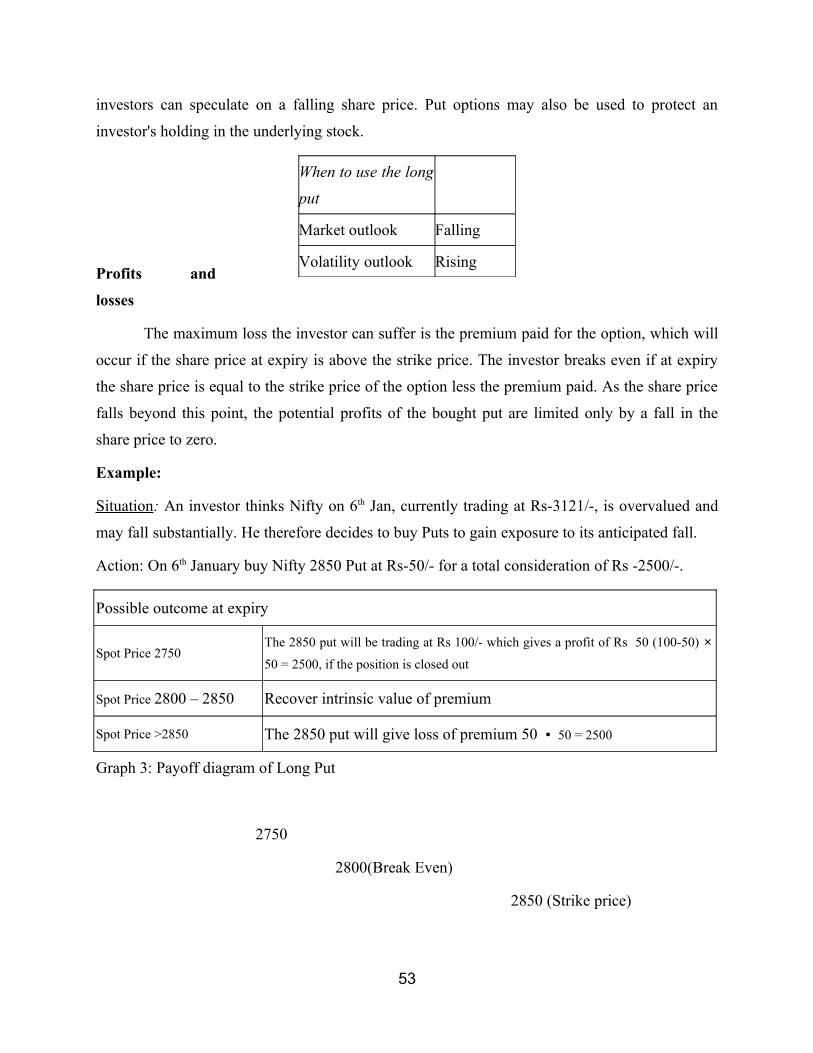

2) LONG PUT:

Where the investor expects the price of the underlying stock to fall, the bought put

provides leveraged exposure to the price fall. Buying a put option is one of the few ways

52

investors can speculate on a falling share price. Put options may also be used to protect an

investor's holding in the underlying stock.

Profits and

losses

The maximum loss the investor can suffer is the premium paid for the option, which will

occur if the share price at expiry is above the strike price. The investor breaks even if at expiry

the share price is equal to the strike price of the option less the premium paid. As the share price

falls beyond this point, the potential profits of the bought put are limited only by a fall in the

share price to zero.

Example:

Situation: An investor thinks Nifty on 6th Jan, currently trading at Rs-3121/-, is overvalued and

may fall substantially. He therefore decides to buy Puts to gain exposure to its anticipated fall.

Action: On 6th January buy Nifty 2850 Put at Rs-50/- for a total consideration of Rs -2500/-.

Possible outcome at expiry