#5 The Purchase and Risk Management of ICOLI - … Purchase and... · The Purchase and Risk...

49

The Purchase and Risk Management of Insurance Company Owned Life Insurance (ICOLI) September 16, 2016 IASA – Metro NY/NJ & Mid-Atlantic Chapters Fall 2016 Education Conference MMB Consulting, LLC Copyright © 2016 by MMB Consulting, LLC, All Rights Reserved Miles Hopkins, CPA A. Gregory Finkell, JD 3901 Westerre Parkway; Suite 300 Richmond, VA 23233 (804) 762-7036 [email protected] [email protected] Atlantic City, NJ

Transcript of #5 The Purchase and Risk Management of ICOLI - … Purchase and... · The Purchase and Risk...

The Purchase and Risk Management of Insurance Company Owned Life Insurance (ICOLI)

September 16, 2016

IASA – Metro NY/NJ & Mid-Atlantic ChaptersFall 2016 Education Conference

MMB Consulting, LLC

Copyright © 2016 by MMB Consulting, LLC, All Rights Reserved

Miles Hopkins, CPAA. Gregory Finkell, JD

3901 Westerre Parkway; Suite 300Richmond, VA 23233

(804) [email protected]

Atlantic City, NJ

John H. Milne,JD, LLM

John H. Milne received his B.A. degree from Virginia Tech in 1970 and his law degree from theUniversity of Richmond in 1973. He received his Master of Laws in Taxation in 1979 fromGeorgetown University.

John is a member of the Virginia and Tennessee Bar Associations. He is a former member of theClosely-Held Business (Vice-Chairman) and the Employee Benefits Committees of the Tax Sectionof the American Bar Association and the Corporate Counsel Section of the Business Law Section ofthe American Bar Association. He has served as Chairman of both the Tax Section of the VirginiaState Bar and the Virginia Bar Association.

John is located in the Richmond, Virginia office.

Miles J. Hopkins,CPA

Miles graduated from Virginia Tech in 2005 with a Bachelor of Science in Accounting and Information Systems. He is a licensed Certified Public Accountant (CPA) in South Carolina. Previously, Miles worked as a consultant in the financial services and insurance industries and as an auditor with Johnson Lambert LLP, a premier insurance focused audit and tax services firm.

Miles serves on the Board of Directors of the Carolinas Chapter of the Insurance Accounting and Systems Association (IASA). He is an active member of the American Institute of Certified Public Accountants and the South Carolina Association of Certified Public Accountants.

Miles is located in the Charleston, South Carolina office.

A. Gregory Finkell, JD Gregg is a former corporate attorney and served as an associate in the Banking and Credit practicegroup of Simpson Thacher & Bartlett LLP in New York. He is a member of the Central VirginiaEstate Planning Council and is a past member of the New York State and American BarAssociations. Previously, Gregg was a financial analyst at a boutique real estate valuation firm inNew York, where he evaluated income-producing real estate portfolios in connection with bankfinancing and underwriting due diligence.

He received his B.A. from Colgate University and his J.D., magna cum laude, from Brooklyn LawSchool, where he was the Notes and Comments Editor of the Brooklyn Law Review.

Gregg is located in the West Hartford, CT office.

2

3

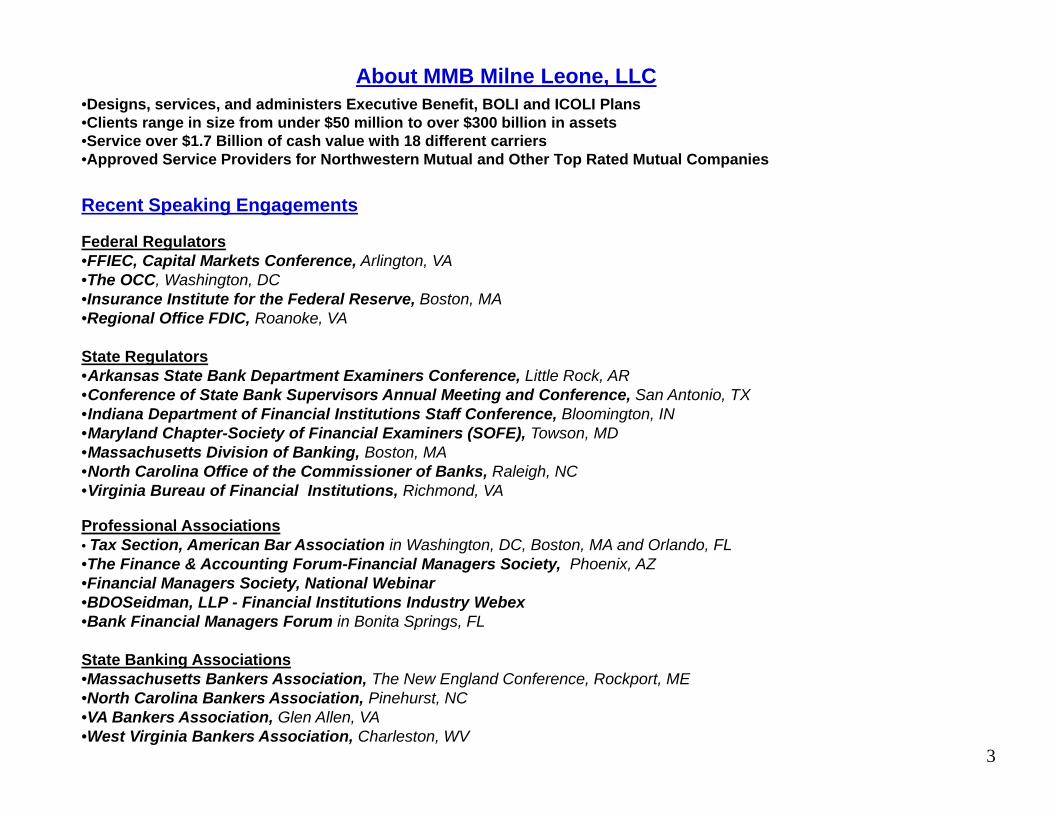

About MMB Milne Leone, LLC•Designs, services, and administers Executive Benefit, BOLI and ICOLI Plans•Clients range in size from under $50 million to over $300 billion in assets•Service over $1.7 Billion of cash value with 18 different carriers•Approved Service Providers for Northwestern Mutual and Other Top Rated Mutual Companies

Recent Speaking Engagements

Federal Regulators•FFIEC, Capital Markets Conference, Arlington, VA •The OCC, Washington, DC•Insurance Institute for the Federal Reserve, Boston, MA •Regional Office FDIC, Roanoke, VA

State Regulators•Arkansas State Bank Department Examiners Conference, Little Rock, AR•Conference of State Bank Supervisors Annual Meeting and Conference, San Antonio, TX •Indiana Department of Financial Institutions Staff Conference, Bloomington, IN •Maryland Chapter-Society of Financial Examiners (SOFE), Towson, MD •Massachusetts Division of Banking, Boston, MA •North Carolina Office of the Commissioner of Banks, Raleigh, NC •Virginia Bureau of Financial Institutions, Richmond, VA

Professional Associations• Tax Section, American Bar Association in Washington, DC, Boston, MA and Orlando, FL •The Finance & Accounting Forum-Financial Managers Society, Phoenix, AZ •Financial Managers Society, National Webinar •BDOSeidman, LLP - Financial Institutions Industry Webex•Bank Financial Managers Forum in Bonita Springs, FL

State Banking Associations•Massachusetts Bankers Association, The New England Conference, Rockport, ME •North Carolina Bankers Association, Pinehurst, NC •VA Bankers Association, Glen Allen, VA •West Virginia Bankers Association, Charleston, WV

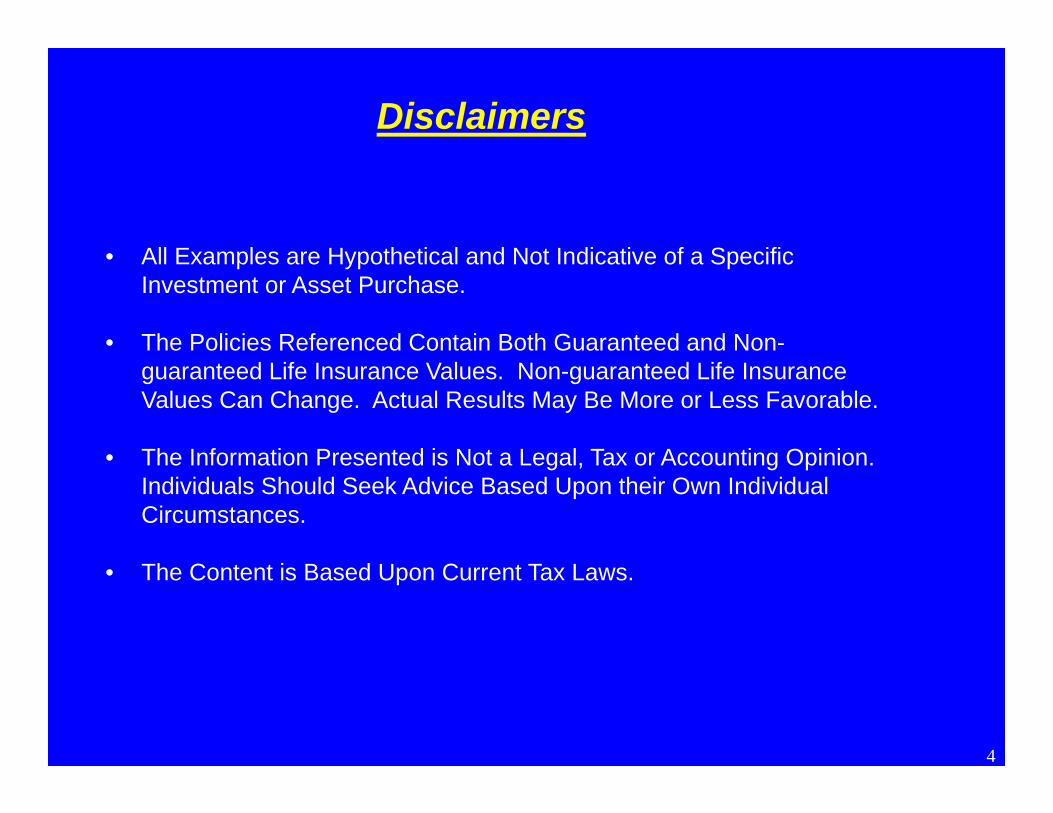

Disclaimers

• All Examples are Hypothetical and Not Indicative of a Specific Investment or Asset Purchase.

• The Policies Referenced Contain Both Guaranteed and Non-guaranteed Life Insurance Values. Non-guaranteed Life Insurance Values Can Change. Actual Results May Be More or Less Favorable.

• The Information Presented is Not a Legal, Tax or Accounting Opinion. Individuals Should Seek Advice Based Upon their Own Individual Circumstances.

• The Content is Based Upon Current Tax Laws.

4

TABLE OF

CONTENTS

MMB Consulting, LLC

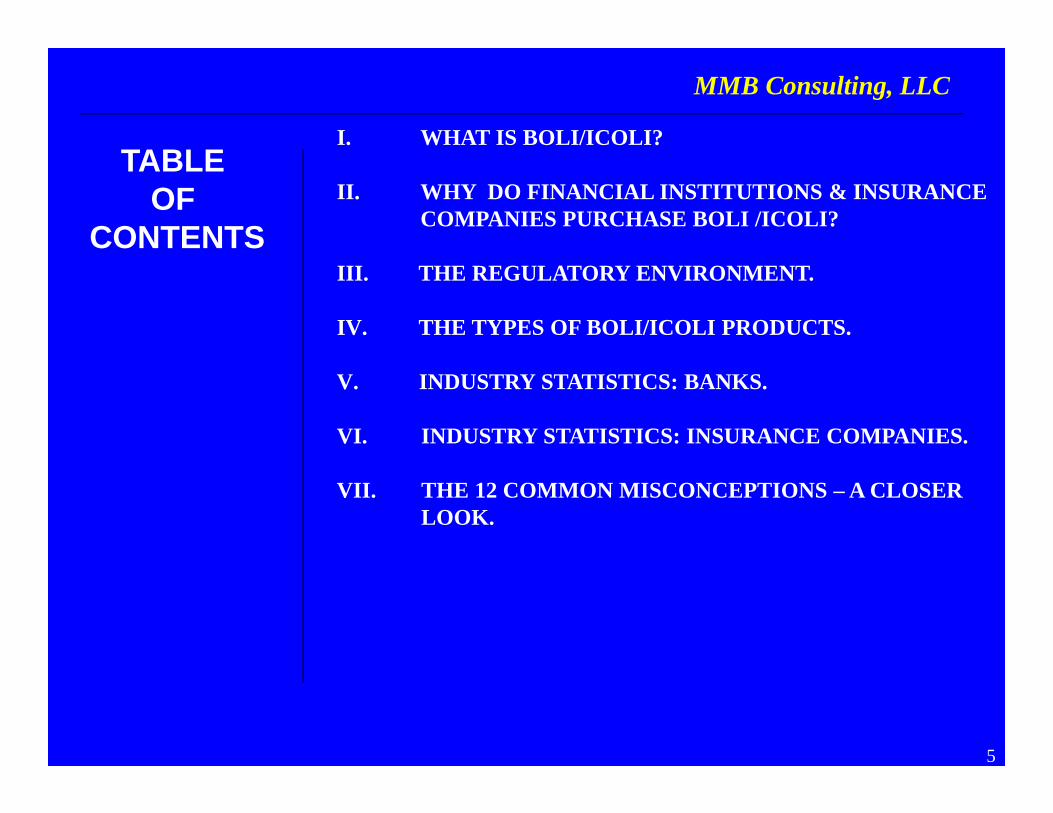

I. WHAT IS BOLI/ICOLI?

II. WHY DO FINANCIAL INSTITUTIONS & INSURANCE COMPANIES PURCHASE BOLI /ICOLI?

III. THE REGULATORY ENVIRONMENT.

IV. THE TYPES OF BOLI/ICOLI PRODUCTS.

V. INDUSTRY STATISTICS: BANKS.

VI. INDUSTRY STATISTICS: INSURANCE COMPANIES.

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK.

5

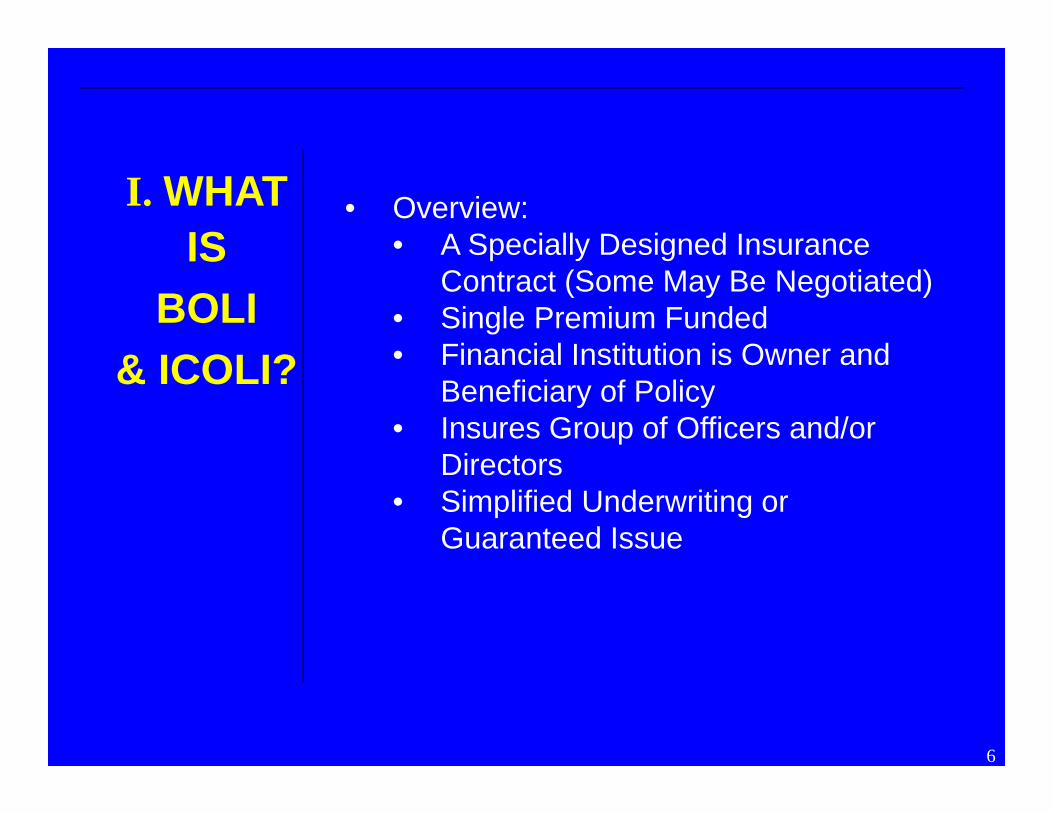

I. WHAT IS

BOLI & ICOLI?

• Overview:• A Specially Designed Insurance

Contract (Some May Be Negotiated)• Single Premium Funded• Financial Institution is Owner and

Beneficiary of Policy• Insures Group of Officers and/or

Directors• Simplified Underwriting or

Guaranteed Issue

6

I. WHAT IS

BOLI & ICOLI?(Continued)

• Regulatory: Bank• Permitted under Interagency Guidelines (OCC-

2004-56)• Must be Funded from an Investment• Business Purpose of the Investment is to

Offset Employee Benefit Costs• Regulatory Guideline is 25% of Tier 1 Capital

in Aggregate and 15% Single Carrier• Document the Pre Purchase Review of Risks

and Rewards• Transaction Risk• Credit Risk• Interest Rate Risk• Liquidity Risk• Compliance/Legal Risk• Price Risk• Reputation Risk

7

I. WHAT IS

BOLI & ICOLI?(Continued)

• Regulatory: Insurance• Generally No Specific Regulations• S&P Limits ICOLI to 25% of

Insurer’s Total Capital & Adjusted Surplus

• 10% Limit for Aggregate Exposure to Single Entity

8

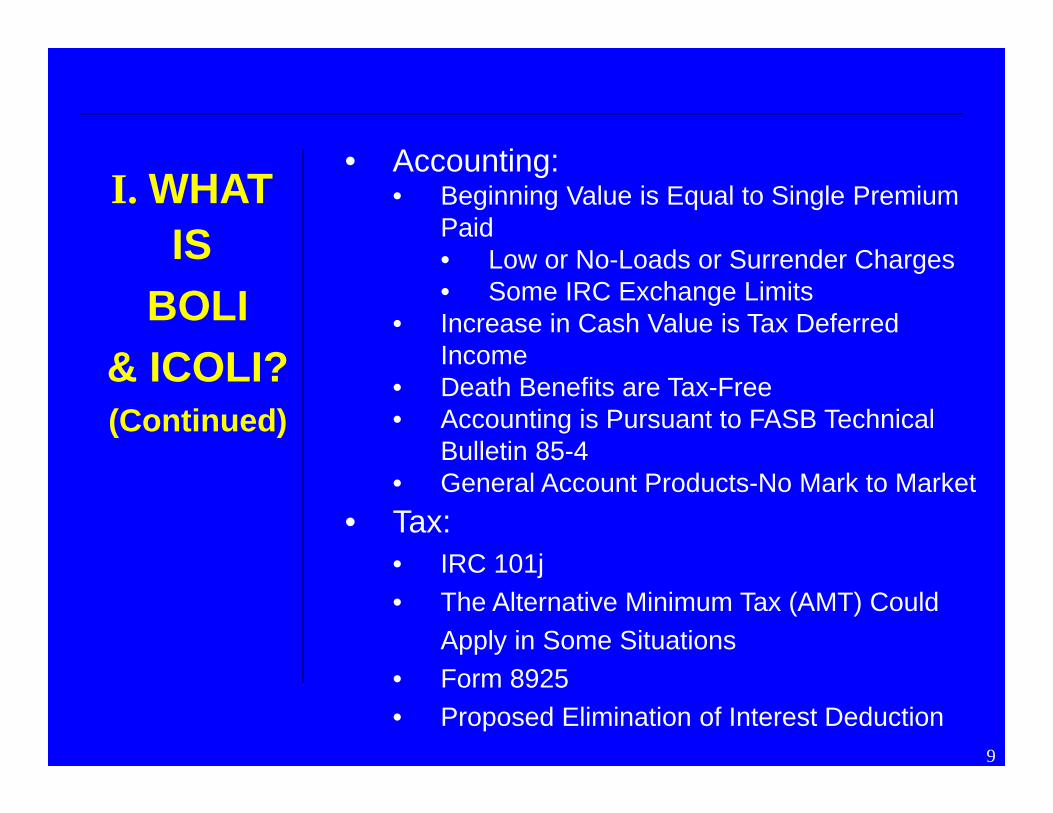

I. WHAT IS

BOLI& ICOLI?(Continued)

• Accounting:• Beginning Value is Equal to Single Premium

Paid• Low or No-Loads or Surrender Charges• Some IRC Exchange Limits

• Increase in Cash Value is Tax Deferred Income

• Death Benefits are Tax-Free• Accounting is Pursuant to FASB Technical

Bulletin 85-4• General Account Products-No Mark to Market

• Tax:• IRC 101j• The Alternative Minimum Tax (AMT) Could

Apply in Some Situations• Form 8925• Proposed Elimination of Interest Deduction

9

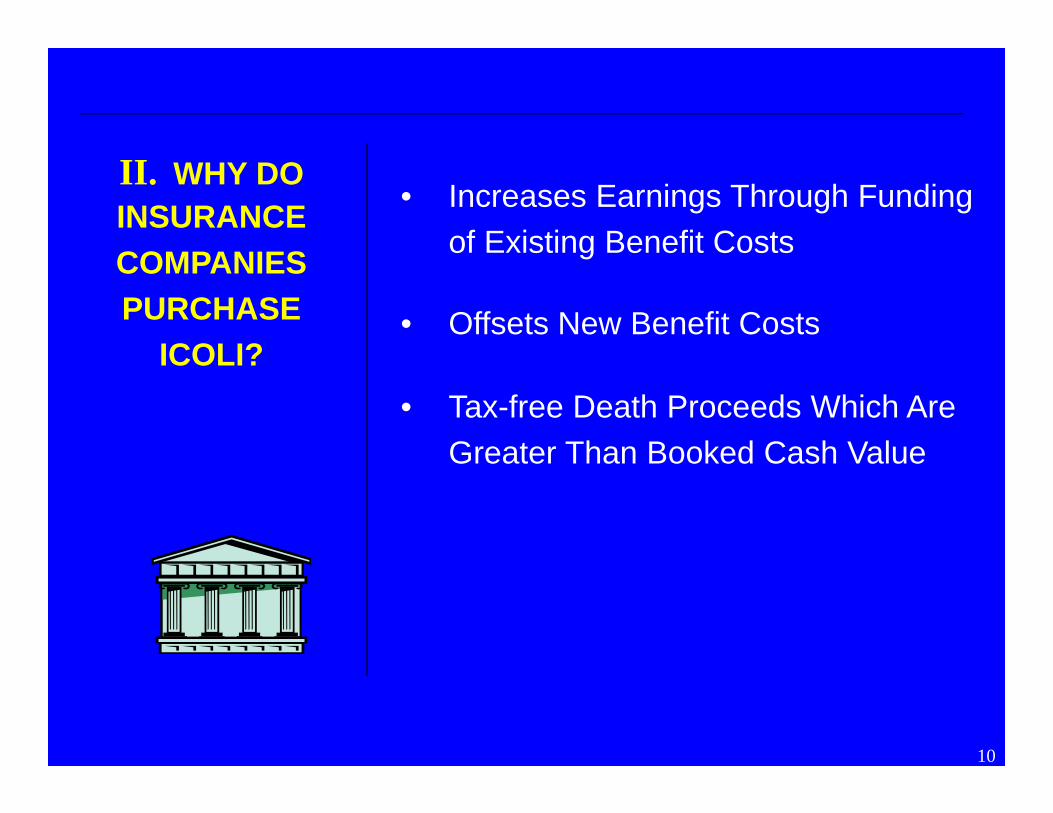

II. WHY DOINSURANCE COMPANIESPURCHASE

ICOLI?

• Increases Earnings Through Funding of Existing Benefit Costs

• Offsets New Benefit Costs

• Tax-free Death Proceeds Which Are Greater Than Booked Cash Value

10

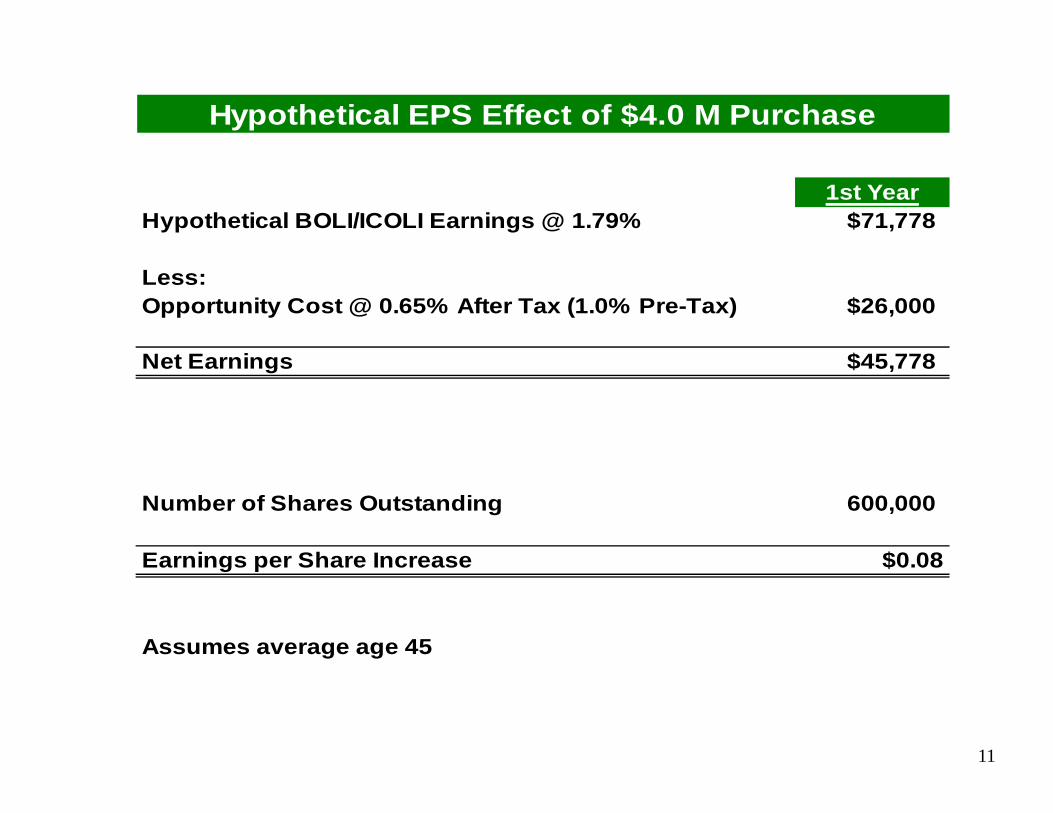

1st YearHypothetical BOLI/ICOLI Earnings @ 1.79% $71,778

Less:Opportunity Cost @ 0.65% After Tax (1.0% Pre-Tax) $26,000

Net Earnings $45,778

Number of Shares Outstanding 600,000

Earnings per Share Increase $0.08

Assumes average age 45

Hypothetical EPS Effect of $4.0 M Purchase

11

Hypothetical Lifetime Financial Effects

Cash Inflows:

Death Proceeds Received @ Age 85 $17,150,366

Cash Outflows:

Premium Paid $4,000,000

Opportunity Cost @ 0.65% After Tax $1,183,357

Net BOLI/ICOLI Income Available To Offset Benefits $11,967,009

IRR on Premiums to Total Death Proceeds 3.71%

Tax Equivalent Return (35% bracket) 5.70%

Number of Shares Outstanding 600,000

Earnings per Share Increase - Lifetime $19.95

12

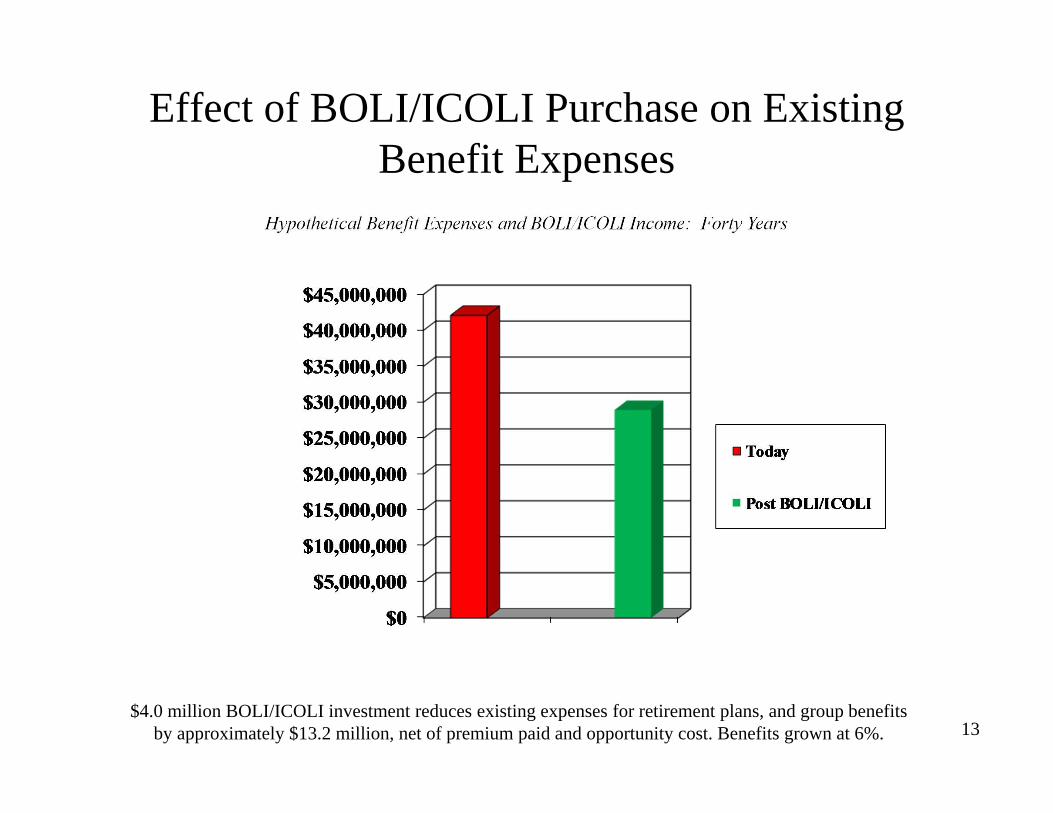

Effect of BOLI/ICOLI Purchase on Existing Benefit Expenses

$4.0 million BOLI/ICOLI investment reduces existing expenses for retirement plans, and group benefits by approximately $13.2 million, net of premium paid and opportunity cost. Benefits grown at 6%.

Hypothetical Benefit Expenses and BOLI/ICOLI Income: Forty Years

13

III. THEREGULATORY

ENVIRONMENT:

• Officer And Board Fiduciary Responsibility/Loyalty and Due Care

• OCC Bulletin 2004-56 & FDIC FIL-127-2004

• Requires Comprehensive Risk Management Process

• Document The Pre Purchase Review

• Investment And Concentration Limits

• Product And Vendor Due Diligence

• SR-12-15

• Ongoing Compliance And Administration Requirements

14

BANKS

INSURANCE COMPANIES

• Officer and Board Fiduciary Responsibility/Loyalty and Due Care

• Generally Unregulated

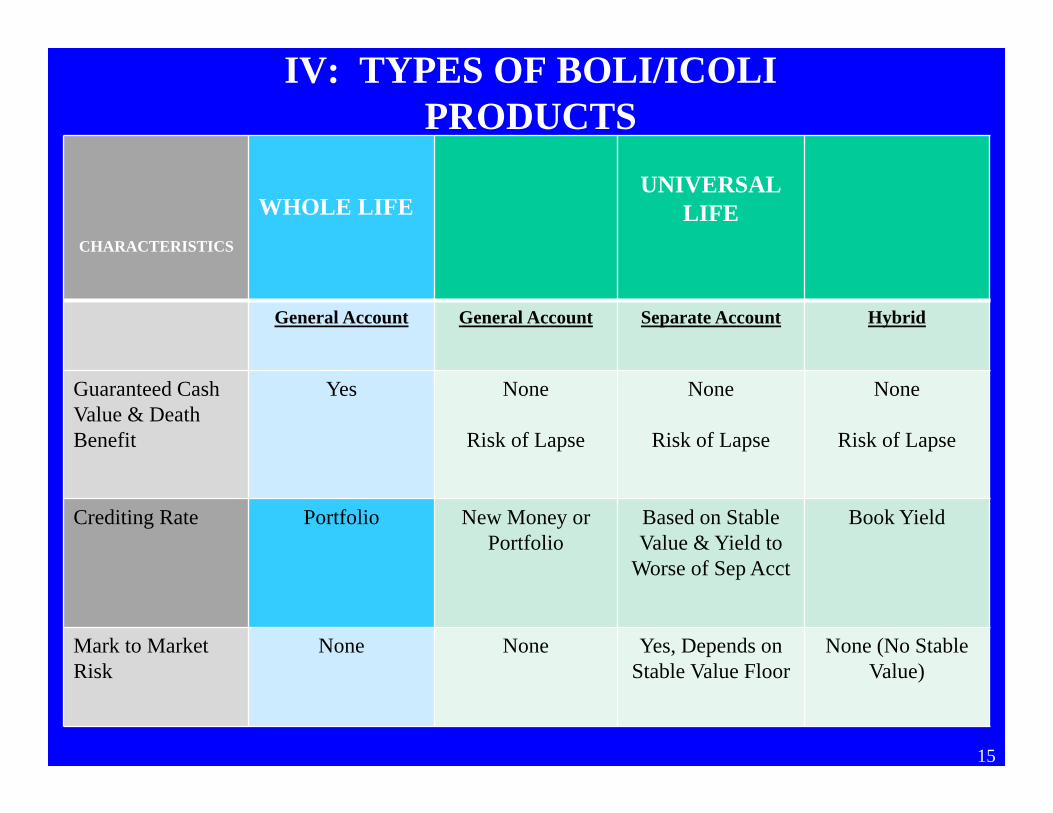

IV: TYPES OF BOLI/ICOLI PRODUCTS

CHARACTERISTICS

WHOLE LIFEUNIVERSAL

LIFE

General Account General Account Separate Account Hybrid

Guaranteed Cash Value & Death Benefit

Yes None

Risk of Lapse

None

Risk of Lapse

None

Risk of Lapse

Crediting Rate Portfolio New Money or Portfolio

Based on Stable Value & Yield to

Worse of Sep Acct

Book Yield

Mark to Market Risk

None None Yes, Depends on Stable Value Floor

None (No Stable Value)

15

IV: TYPES OF BOLI/ICOLI PRODUCTS

CHARACTERISTICS WHOLE LIFEUNIVERSAL

LIFEGeneral Account General Account Separate Account Hybrid

Risk Weighting: Banks

100% 100% 20%/50%/100% Subject to Offsets

20%/50%/100% Subject to Offsets, Not Validated by

Regulators

Investment Choices

None, Carrier General Account

None, Carrier General Account

Several Subject to Stable Value Wrap

Provider

Limited

Bankruptcy Risk Yes Yes Separate AccountMay Be Protected, Matter of State Law, Untested in Courts_______________Death Benefit at Risk

Separate AccountMay Be Protected, Matter of State Law, Untested in Courts_______________Death Benefit at Risk 16

Risk Weighting:Insurance

0.8% Life Cos.5% P&C Cos.

0.8% Life Cos.5% P&C Cos.

Underlying Asset Look-Through

Underlying Asset Look-Through

IV: TYPES OF BOLI/ICOLI PRODUCTS

CHARACTERISTICS

WHOLE LIFEUNIVERSAL

LIFE

General Account General Account Separate Account Hybrid

1035 Exchange Restrictions

Yes Yes Yes, Market Adjustment, Stable

Value Fees

Yes

Cost Disclosures Generally No, Bundled Product

Generally Yes Yes Generally Yes

Mortality Risk Carrier Carrier Carrier or Experience Rating

Carrier but may be limited by

Experience Rating

Complexity Simple Simple Generally requireslegal, accounting,

actuarial and investment advice

& expertise

Maybe(Regulators are Uncertain About

Treatment)

17

V. Industry Statistics: Banks

18

Source: 2014 FFIEC Call Reports19

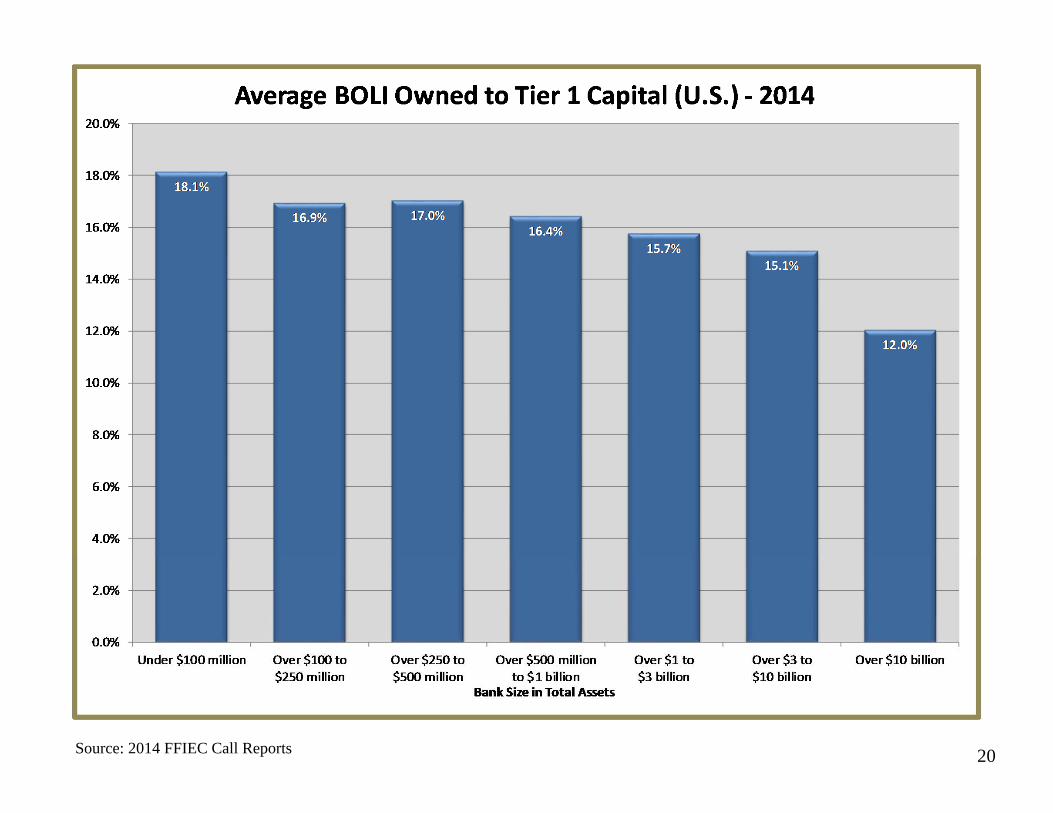

Source: 2014 FFIEC Call Reports 20

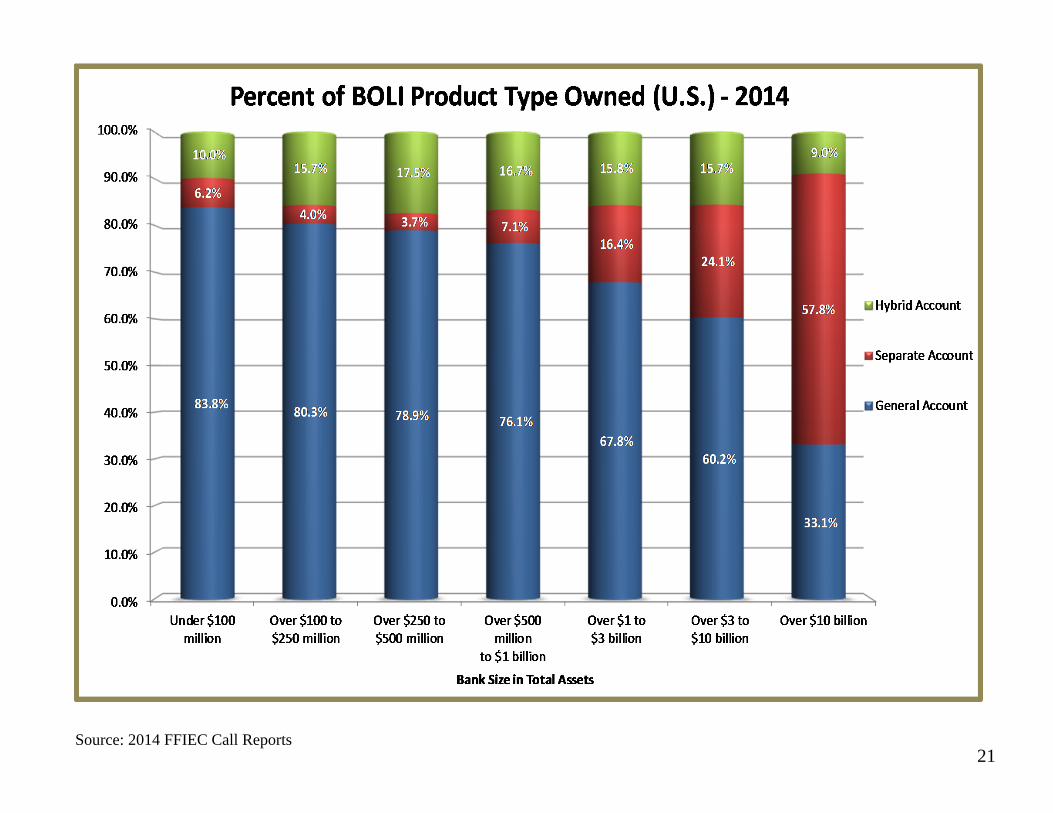

Source: 2014 FFIEC Call Reports21

VI. Industry Statistics: Insurance

Companies

22

*All Statistics are for 2015 unless otherwise noted.

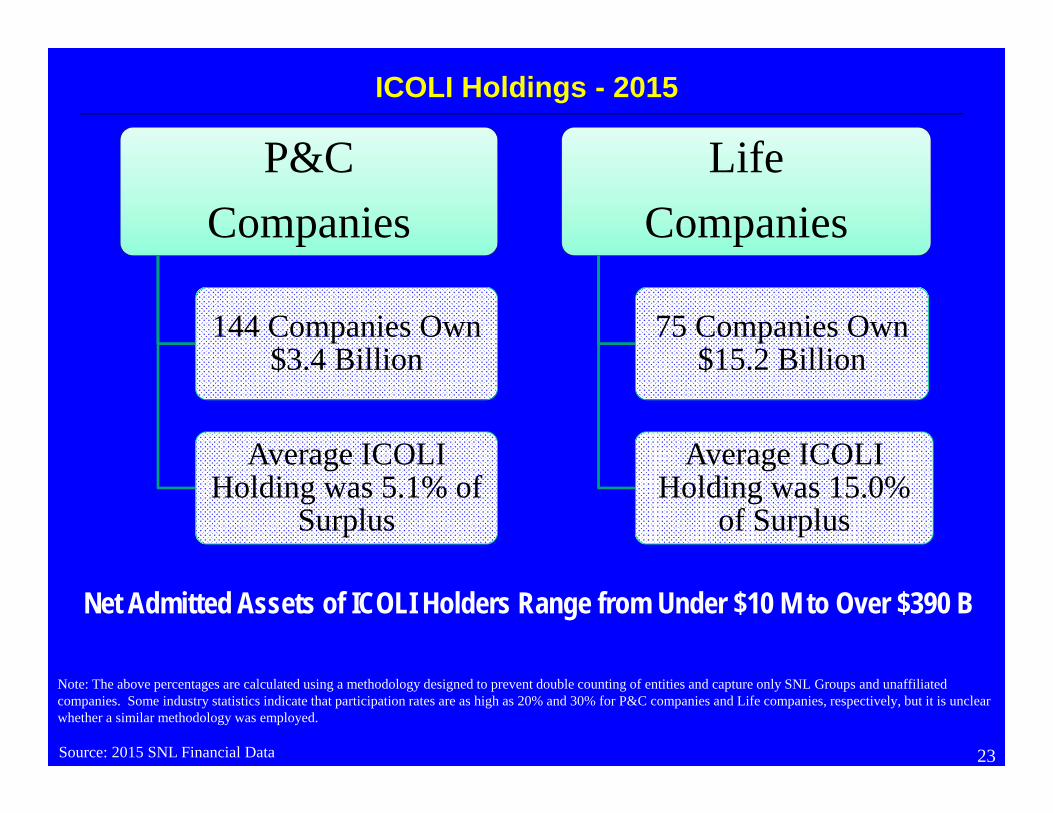

23

P&C Companies

144 Companies Own $3.4 Billion

Average ICOLIHolding was 5.1% of

Surplus

Life Companies

75 Companies Own $15.2 Billion

Average ICOLIHolding was 15.0%

of Surplus

ICOLI Holdings - 2015

Net Admitted Assets of ICOLI Holders Range from Under $10 M to Over $390 B

Source: 2015 SNL Financial Data

Note: The above percentages are calculated using a methodology designed to prevent double counting of entities and capture only SNL Groups and unaffiliated companies. Some industry statistics indicate that participation rates are as high as 20% and 30% for P&C companies and Life companies, respectively, but it is unclear whether a similar methodology was employed.

24

Top 5 ICOLI Holders by Industry - 2015

P&C Companies

•Liberty Mutual - $842.6 M

•Farmers Insurance - $447.8 M

•Hartford Fire - $432.4 M

•MetLife (P&C) - $316.4 M

• Alfa Mutual - $152.9 M

Life Companies

• New York Life - $4.0 B

• MetLife (Life) - $2.5 B

• MassMutual - $1.9 B

• John Hancock - $1.1 B

• AXA - $855.6 M

Source: 2015 SNL Financial Data

Insurance Industry Statistics Relative to BOLI & ICOLI

Total of 1,100+ Life Insurance Carriers Today.

Only 40 +/- Carriers Have Sold a BOLI product.

Only a few carriers sell ICOLI products.

“Half of the stock life companies rated by Moody’s have been downgraded one of more notches since December 31, 2007, with some declining as much as three notches.” 1

“… less than 25% of the mutual companies have been lowered during this period, and none have been downgraded by more than one rating notch.” 1

251Source: Moody’s August 7, 2009 Report, “Revenge of the Mutuals”

1. MISCONCEPTION: “My Vendor Brokers All The Products.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

A number of BOLI carriers have products that are proprietary to one or a limited group of BOLI vendors.

There is no such thing as a true broker in the BOLI business.

Only a limited number of carriers have ICOLI products.• Some ICOLI carriers will sell only to P&C companies.• Other ICOLI carriers will sell only to other life

companies.

26

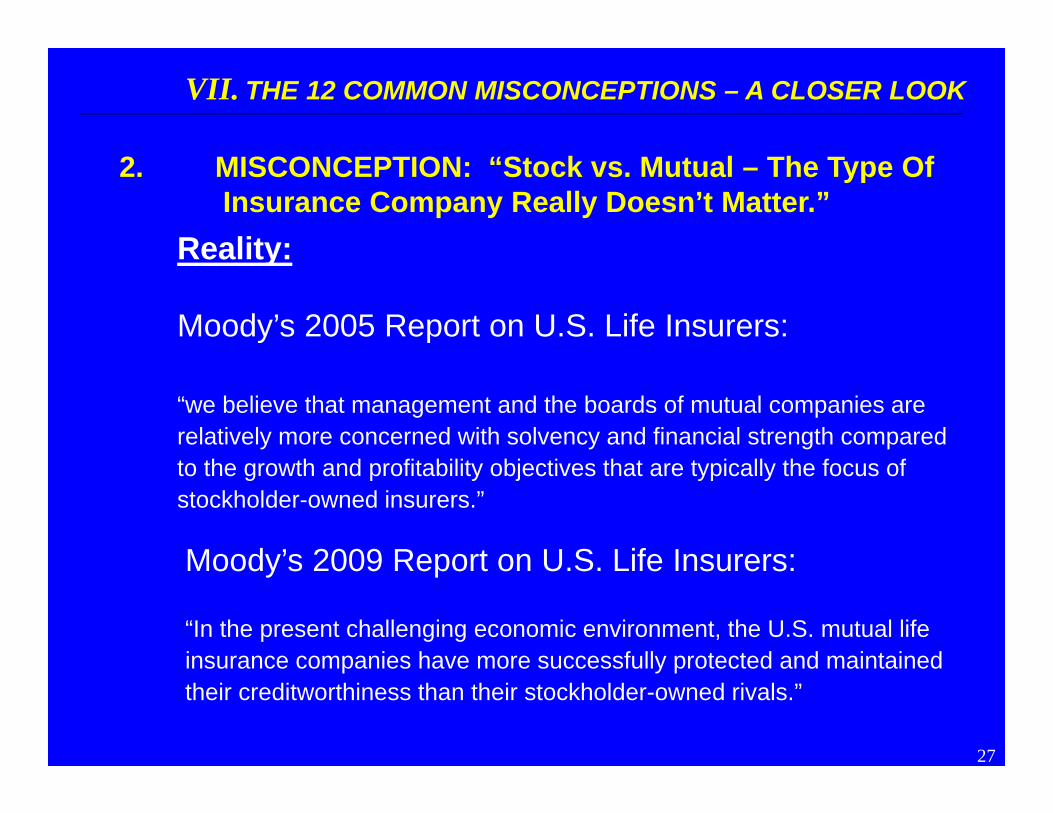

2. MISCONCEPTION: “Stock vs. Mutual – The Type Of Insurance Company Really Doesn’t Matter.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Moody’s 2005 Report on U.S. Life Insurers:

“we believe that management and the boards of mutual companies are relatively more concerned with solvency and financial strength compared to the growth and profitability objectives that are typically the focus of stockholder-owned insurers.”

Moody’s 2009 Report on U.S. Life Insurers:

“In the present challenging economic environment, the U.S. mutual life insurance companies have more successfully protected and maintained their creditworthiness than their stockholder-owned rivals.”

27

3. MISCONCEPTION: “The BOLI/ICOLI Has A Minimum Crediting Rate.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Most products have a minimum guaranteed crediting rate.

Interagency Statement: “before purchasing BOLI, an institution should analyze projected values using multiple illustrations . . .”

Minimum guaranteed crediting rates show only part of the story. Institutions should assess mortality and expenses.

Best analysis includes projections at the contractual guarantees.

28

Sample Carriers &Independent Ratings

Carrier #1 Whole Life

Carrier #2 Universal Life

Carrier #3 Universal Life

29

Cash Value Guarantees - M/E/Interest

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

1 5 10 20 30 40

Carrier #1

Carrier #2

Carrier #3

Years

Guarantees = guaranteed mortality, expenses & interest crediting rate

Sample $1 m Premium: Age 45 Underwritten

Carrier #1 Whole Life

Carrier #2 Universal Life

Carrier #3 Universal Life

30

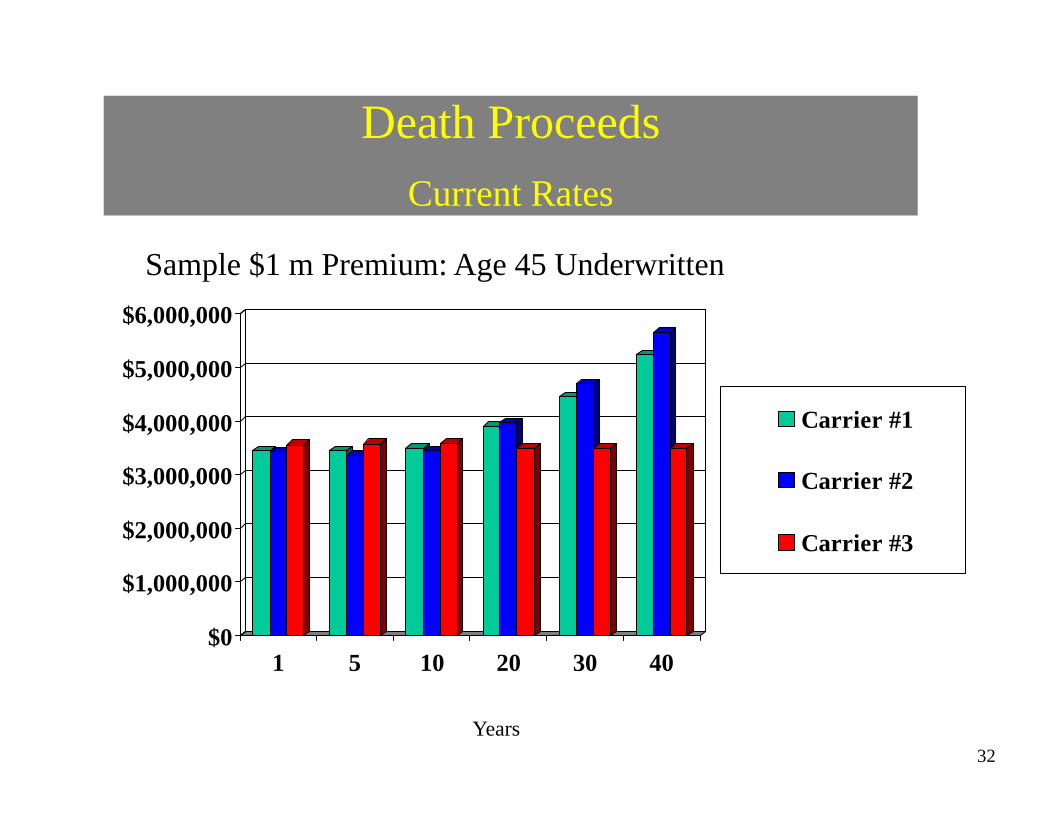

4. MISCONCEPTION: “Death Benefits Are All About The Same.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement: “institutions should analyze projected values (CSV and death benefits) using multiple illustrations . . .”

The ultimate return is the death benefit.

31

Death Proceeds Current Rates

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

1 5 10 20 30 40

Carrier #1

Carrier #2

Carrier #3

Years

Sample $1 m Premium: Age 45 Underwritten

32

5. MISCONCEPTION: “Our Carrier Is Rated ‘A’ Excellent. The Higher The RatingThe Lower The Return.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement:

“Carrier selection is one of the most critical decisions in a BOLI purchase.”

“The credit quality of the insurance company is a key variable.”

An institution should receive a “rate of return . . . comparable to returns on investments of similar maturity and credit risk.”

An American Bar Association publication says, the minimum criteria requires that carriers have at least two ratings from the top two levels and none below investment grade.

Know the carrier’s reputation and historic performance. 33

Rating Chart

Independent Rating Services Financial Strength Ratings The First Three Levels of a Total Five Levels

Moody’s S & P’s Fitch A.M. Best 1 Exceptional

Aaa Extremely

Strong AAA

Highest AAA

Superior A++ A+

2 Excellent Aa1 Aa2 Aa3

Very Strong AA+ AA AA-

Very High AA+ AA AA-

Excellent A A-

3 Good A1 A2 A3

Strong A+ A A-

High A+ A A-

Very Good B++ B+

Top Two LevelsAre

Recommended

34

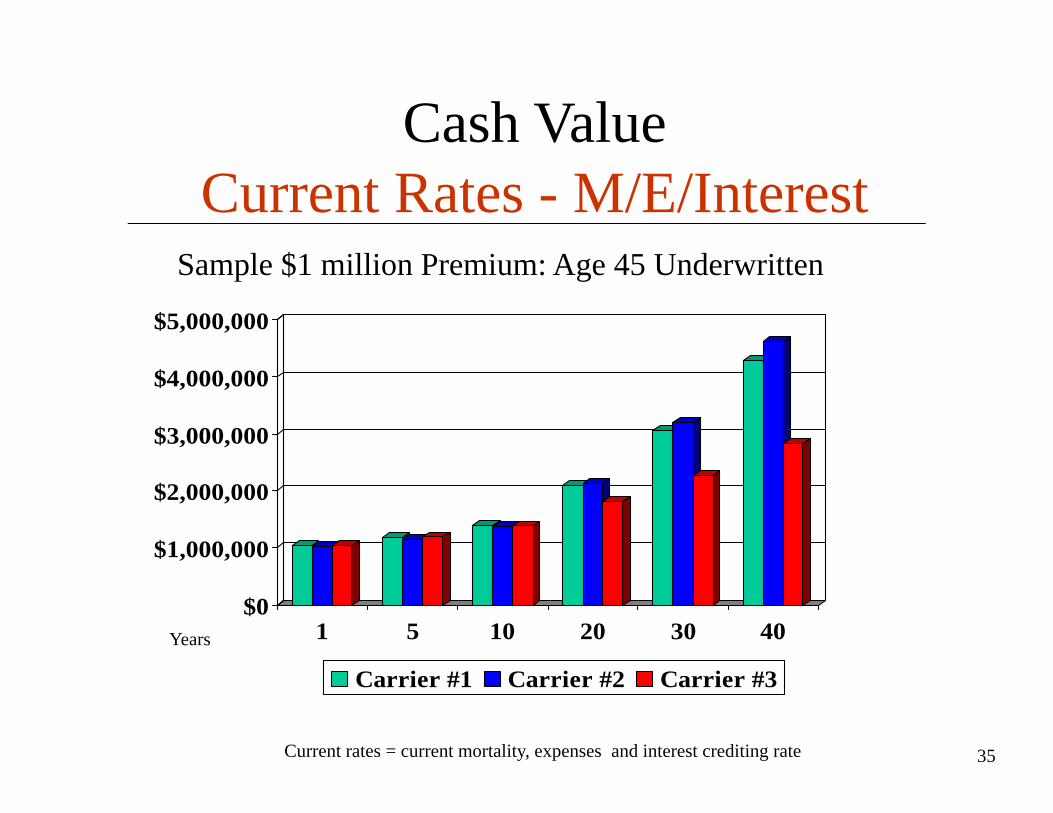

Cash Value Current Rates - M/E/Interest

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

1 5 10 20 30 40

Carrier #1 Carrier #2 Carrier #3

Years

Current rates = current mortality, expenses and interest crediting rate

Sample $1 million Premium: Age 45 Underwritten

35

6. MISCONCEPTION: “If We Have A Problem With Our BOLI/ICOLI,We Can Switch To Another Carrier.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement: “management should inform the board . . . of any other significant risks . . . with BOLI [including] the costs associated with changing carriers . . . and the potential for noncompliance with state . . . and federal law.”

A tax-free exchange of one carrier for another may be effected provided there is still an insurable interest and no material change in health.

BOLI/ICOLI products typically have exchange restrictions and/or charges. 36

37

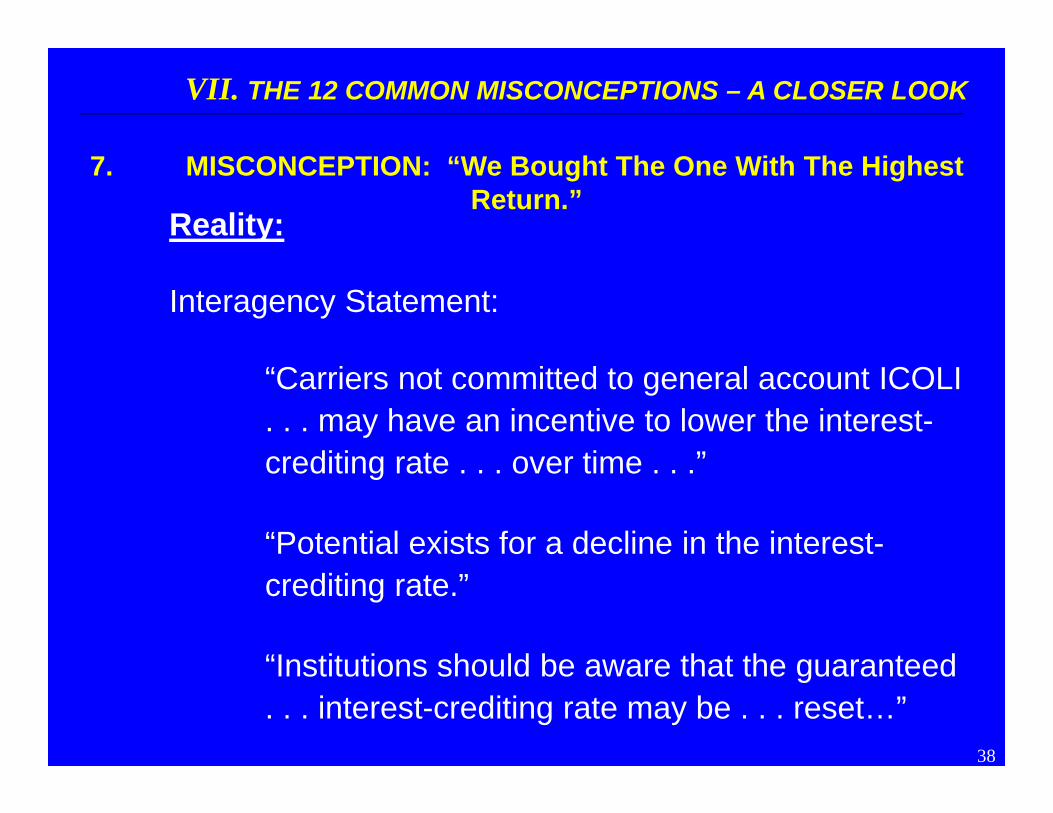

7. MISCONCEPTION: “We Bought The One With The Highest Return.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement:

“Carriers not committed to general account ICOLI . . . may have an incentive to lower the interest-crediting rate . . . over time . . .”

“Potential exists for a decline in the interest-crediting rate.”

“Institutions should be aware that the guaranteed . . . interest-crediting rate may be . . . reset…”

38

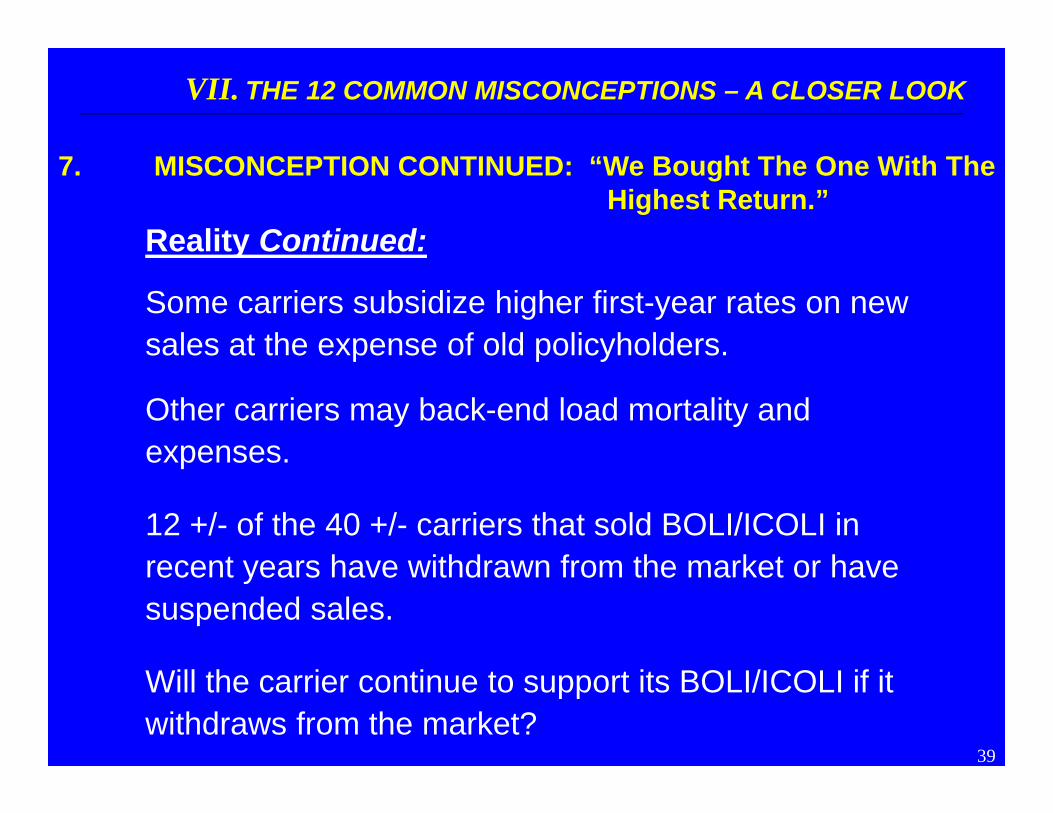

7. MISCONCEPTION CONTINUED: “We Bought The One With The Highest Return.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality Continued:

Some carriers subsidize higher first-year rates on new sales at the expense of old policyholders.

Other carriers may back-end load mortality and expenses.

12 +/- of the 40 +/- carriers that sold BOLI/ICOLI in recent years have withdrawn from the market or have suspended sales.

Will the carrier continue to support its BOLI/ICOLI if it withdraws from the market?

39

Existing BOLI/ICOLI Credited With Lower Interest Rate Than New

BOLI/ICOLI

3.70%3.80%3.90%4.00%4.10%4.20%4.30%4.40%4.50%4.60%4.70%4.80%

1st Qtr 2nd 3rd 4th

NewBOLI/ICOLIExistingBOLI/ICOLI

40

8. MISCONCEPTION: “We Bought A Separate Account BOLI/ICOLI.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement:

“The protected status of separate account assets is generally untested in the courts.”

“Transactional/operational risk may also arise as a result of the variety of negotiable features . . .”

New York recommends that institutions obtain opinions as to creditor protection, qualification as life insurance, and whether there are sufficient assets in the separate account to cover mortality and expenses.

Virginia says community banks may not have the expertise or resources to evaluate and manage separate account products.

41

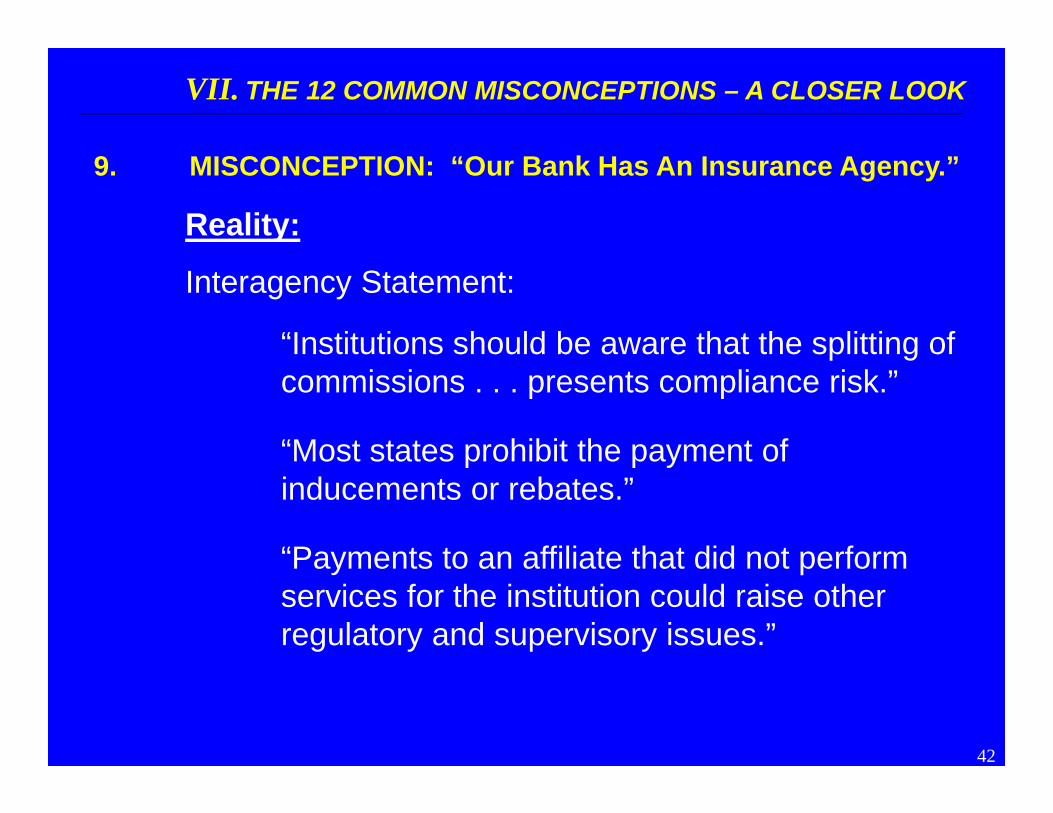

9. MISCONCEPTION: “Our Bank Has An Insurance Agency.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Interagency Statement:

“Institutions should be aware that the splitting of commissions . . . presents compliance risk.”

“Most states prohibit the payment of inducements or rebates.”

“Payments to an affiliate that did not perform services for the institution could raise other regulatory and supervisory issues.”

42

9. MISCONCEPTION CONTINUED: “Our Bank Has An Insurance Agency.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality Continued:

Commissions are subject to income tax.

Several BOLI/ICOLI carriers do not permit vendors to split commissions.

Does the institution’s insurance agency have the expertise and experience to design, service, and administer BOLI/ICOLI?

43

10. MISCONCEPTION: “Our Vendor Is Monitoring The Situation.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:Interagency Statement:

“A prudent risk management process includes . . . effective senior management and board oversight [and] an ongoing system of risk assessment, management, monitoring, and internal control . . .”

“Reliance upon pre-packaged, vendor-supplied compliance information does not demonstrate prudence. . .”

Vendors may have a financial interest to not inform the institution of problems.

44

11. MISCONCEPTION: “I’ll Be Retired Soon, So Why Do I Care About BOLI/ICOLI.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

Actual benefits from BOLI/ICOLI may differ significantly from what was originally projected.

The executive could suffer a loss of benefits, the institution could experience higher benefit costs, or both.

45

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Age45

Age55

Age65

Age75

Age85

Promised Benefit

Net Amount Available(Death Benefit less CashValue)

Shortage

Split Dollar PlansReduced BOLI/ICOLI Growth Squeezes Executive’s Death

Proceeds

46

12. MISCONCEPTION: “I Think Everything Is Fine.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality:

12 +/- out of the 40 +/- BOLI carriers, have left the BOLI business or suspended sales.

23 +/- BOLI carriers have suffered rating downgrades since 2007.

Only limited number of BOLI carriers are in the ICOLI market.

Interest crediting rates have declined.

Stock life insurance carriers are pressed to meet quarterly earnings goals.

47

12. MISCONCEPTION CONTINUED: “I Think Everything Is Fine.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality Continued:

Tax and legal developments could affect BOLI/ICOLI holdings.

Interagency Statement:

“Management . . . should review the performance of the . . . insurance . . . with its board at least annually.”

“More frequent reviews are appropriate if there are significant changes to the BOLI program such as . . .

[D]ecline in the financial condition of the insurance carrier . . .

[C]hange in the tax laws . . . ”48

12. MISCONCEPTION CONTINUED: “I Think Everything Is Fine.”

VII. THE 12 COMMON MISCONCEPTIONS – A CLOSER LOOK

Reality Continued:

Institutions should have a comprehensive investment

policy in place directed at the “Purchase and Risk

Management of BOLI/ICOLI.”

49