5 slides6.1

22

Double Entry Double Entry System 2 System 2 DR CR

-

Upload

extrakiller -

Category

Education

-

view

43 -

download

0

Transcript of 5 slides6.1

Double EntryDouble Entry

System 2System 2

DR CR

An Overview…

General

Journal

Special

Journals

Ledger Accounts

Trial Balance

Prepare Simple Financial Statements

Adjustments

ObjectivesObjectives

At the end of the lesson, students should be able to :

• know what are Ledger Accounts.

• prepare Ledger Accounts using the ‘T’ format.

• post transactions from the Journals to

the Ledger Accounts.

LEDGER BOOKLEDGER BOOK

AccountAccount AccountAccount

What is an Account ?What is an Account ?

An account is a brief and systematic record of

transactions which are

similar in nature.

DDEBITEBIT CCREDITREDIT

DrDr CrCr NAME OF ACCOUNTNAME OF ACCOUNT

‘ ‘T’ formatT’ format

Left side

Right side

DDEBITEBIT CCREDITREDIT

DrDr CrCr ASSETS ACCOUNTASSETS ACCOUNT

‘ ‘T’ formatT’ format

DDEBITEBIT CCREDITREDIT

DrDr CrCr OWNER’S EQUITY ACCOUNTOWNER’S EQUITY ACCOUNT

‘ ‘T’ formatT’ format

DDEBITEBIT CCREDITREDIT

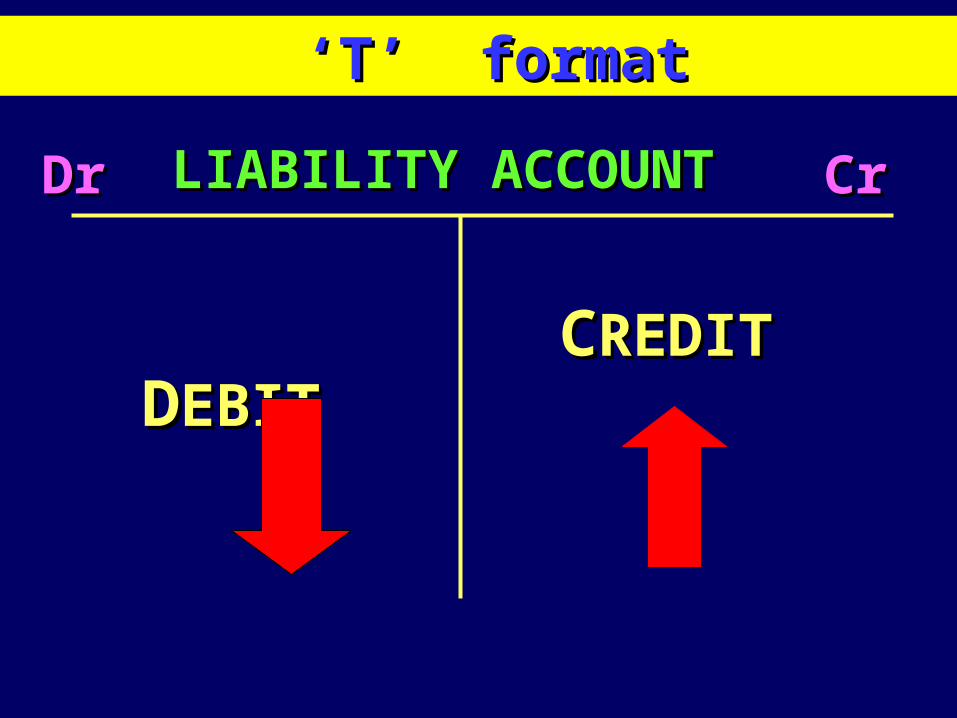

DrDr CrCr LIABILITY ACCOUNTLIABILITY ACCOUNT

‘ ‘T’ formatT’ format

DDOUBLE - OUBLE - EENTRYNTRY ACCOUNTING SYSTEMACCOUNTING SYSTEM

Every business transaction will involve twotwo parties

Each party must give upgive up something (outout) in order toto receive receive something

in return. (inin)

WWhen the business sells its hen the business sells its goods for cash, itgoods for cash, it willwill give upgive up its its goodsgoods to its customer and to its customer and willwill receive cashreceive cash in return.in return.

Cash IN

Goods OUT

Example:

FirmFirm’s goods

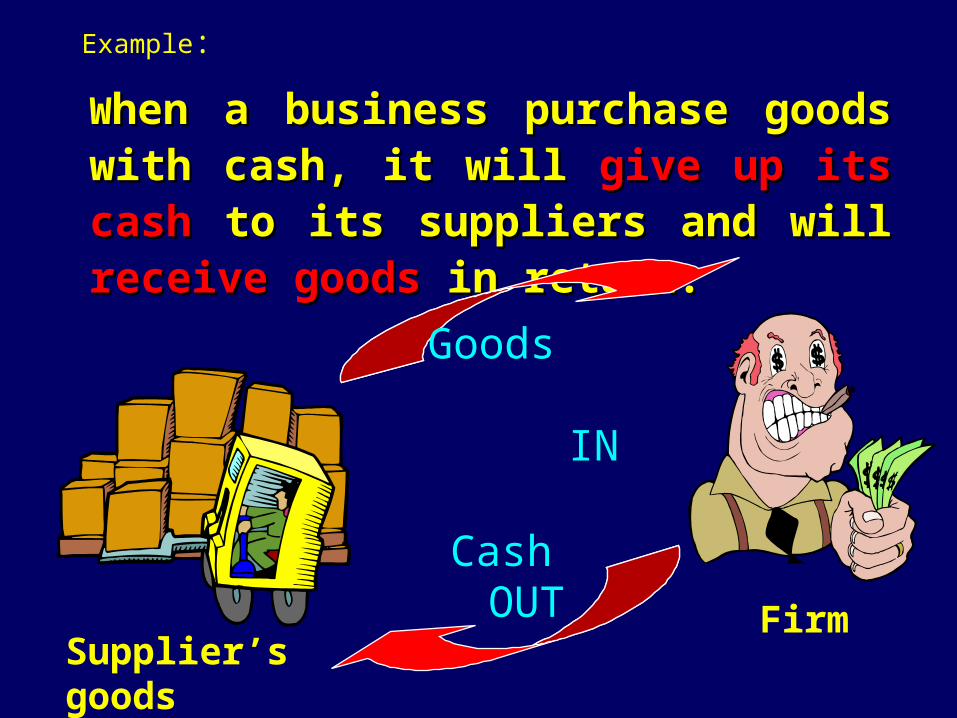

WWhen a business purchase goods hen a business purchase goods with cash, itwith cash, it willwill give upgive up its cashits cash to its suppliers andto its suppliers and willwill receive receive goodsgoods in return.in return.

Goods IN

Cash OUT

Example:

FirmSupplier’s goods

WWhen a business purchase a hen a business purchase a motor vehicle, itmotor vehicle, it willwill give upgive up its its cashcash to the seller and to the seller and willwill receive motor vehiclereceive motor vehicle in return.in return.

Example:

Motor Vehicle IN

Cash OUT

FirmMotor Vehicle

When a debtor pays to the firm, the When a debtor pays to the firm, the firm’s firm’s cash will increasecash will increase and the and the firm’s firm’s debtors will decreasedebtors will decrease. .

Example:

FirmDebtor

Cash

increases

Debtors decreases

When the firm pays to the creditors, When the firm pays to the creditors, the firm’s the firm’s cash will decreasecash will decrease and the and the firm’s firm’s creditors will decreasecreditors will decrease. .

Example:

FirmCreditors

Creditors decreases

Cash

decreases

Hence,

For every business transaction, two accounts will be involved.

One account will have a debit entry and another account will have a

credit entry.

a) Paid $200 for office stationery

Dr CASH a/cCASH a/c Cr

Dr STATIONERYSTATIONERY a/c a/c Cr

$200

$200

StationeryStationery

CashCash

Dr CASH a/cCASH a/c Cr

Dr PURCHASESPURCHASES a/c a/c Cr

$500

$500

PurchasesPurchases

CashCash

b) Bought goods worth $500 using cash

Dr CASH a/cCASH a/c Cr

Dr SALESSALES a/c a/c Cr

$800

$800

SalesSales

CashCash

c) Sold goods for cash $800

Dr STOCK STOCK Cr

Dr TRADINGTRADING a/c a/c Cr

$8000

$8000

TradingTrading

StockStock

d) Closing stock counted is

worth $8000

Dr DRAWINGS a/cDRAWINGS a/c Cr

Dr CASHCASH a/c a/c Cr

$1500

$1500

CashCash

Drawings

e) The owner drew out cash

$1500 for personal use.

Summary - 3 2 1 RULE…

3 things that you have learnt 3 things that you have learnt today…today…

2 questions that you may want 2 questions that you may want to ask…to ask…

1 thing that you still have 1 thing that you still have problem understanding…problem understanding…

![Rachmaninov 3rd Piano Concerto [First Movement] · PDF file53-g e5 = 5 !5 = 5 5 5 5 5 4 5 5 =5 5 = 5e5 5 5 5 5 5 5 5e5 5 5!55 5 5 5 5 5e5 5 5 5 5 5 5! 5 $3e55 5 5: 5 5 5 55 5e 55 5](https://static.fdocuments.us/doc/165x107/5a78944a7f8b9a1f128d15db/rachmaninov-3rd-piano-concerto-first-movement-53-g-e5-5-5-5-5-5-5-5-4-5.jpg)