5. Measurement Cross Cutting Issues

18

International Financial Reporting Standards The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation. © IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org IFRS measurements: cross-cutting issues Joint World Bank and IFRS Foundation ‘train the trainers’ workshop hosted by the ECCB, 30 April to 4 May 2012 K The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

-

Upload

sanath-fernando -

Category

Documents

-

view

10 -

download

1

description

IASB

Transcript of 5. Measurement Cross Cutting Issues

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IFRS measurements: cross-cutting issues

Joint World Bank and IFRS Foundation ‘train the trainers’ workshop hosted by the ECCB,

30 April to 4 May 2012

KThe views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

Myth 1 2

Everyone knows what ‘best

estimate’ means

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

What does ‘best estimate’ mean? 3

Most likely outcome?

Median outcome?< 50% chance of higher cash flows< 50% chance of lower cash flows

Expected value?Average (mean) of range

Whatever amount feels ‘best’?

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Myth 2 4

The IASB prefers fair value

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IASB does not always prefer fair value

• Provisions

• Impairment of property, plant, equipment, intangibles

• Revenue recognition

• Insurance contracts

• Leases

5

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Myth 3 6

The IASB prefers expected value

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Expected value might be best...

• if objective is to measure current value of asset or liability

• if transactions recur frequently

• if users are concerned about extreme outcomes (outliers)

• if expected value is as easy to estimate as other measures

• if the timing of cash flows is uncertain

• you don’t know…

7

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Most likely or median might be better...

• if objective is to predict future cash flows• if transactions do not recur frequently• if outliers are less important or more uncertain than

central outcomes• if expected value is more difficult to measure

8

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Myth 4 9

Expected value needs accurate data about all

outcomes

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

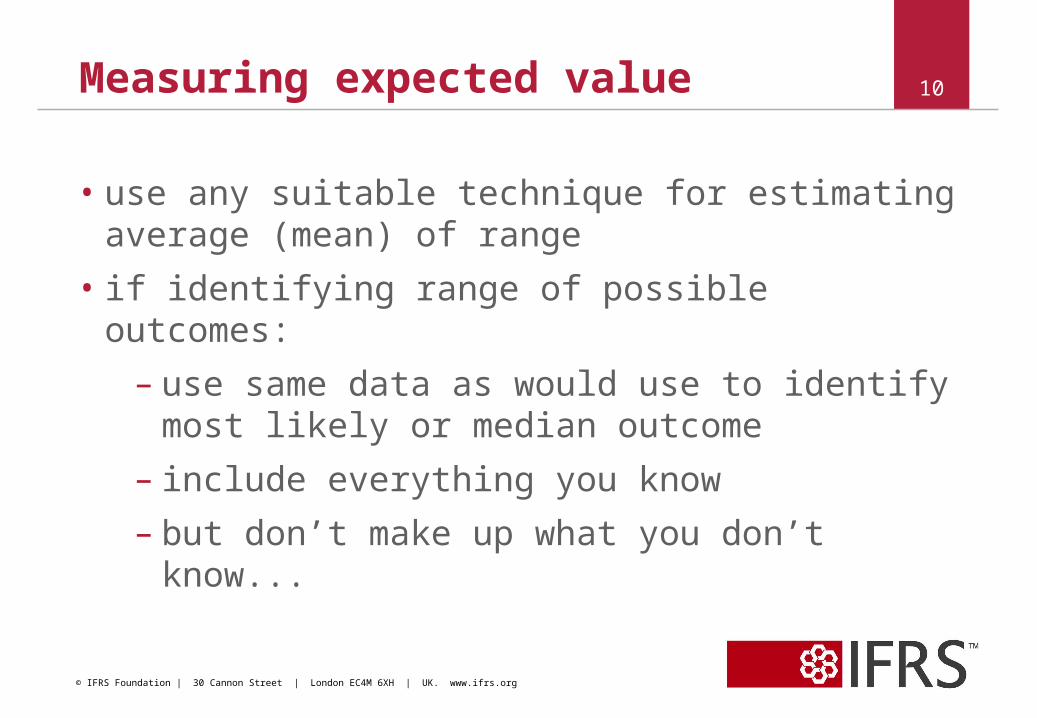

Measuring expected value

• use any suitable technique for estimating average (mean) of range

• if identifying range of possible outcomes:

– use same data as would use to identify most likely or median outcome

– include everything you know

– but don’t make up what you don’t know...

10

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Measuring expected value continued 11

We have evidence that...

Most likely outcome is 100 currency units (CU)

We have no evidence that...

Distribution is other than normal (bell-shaped)

We would estimate expected value to be...

CU 100

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

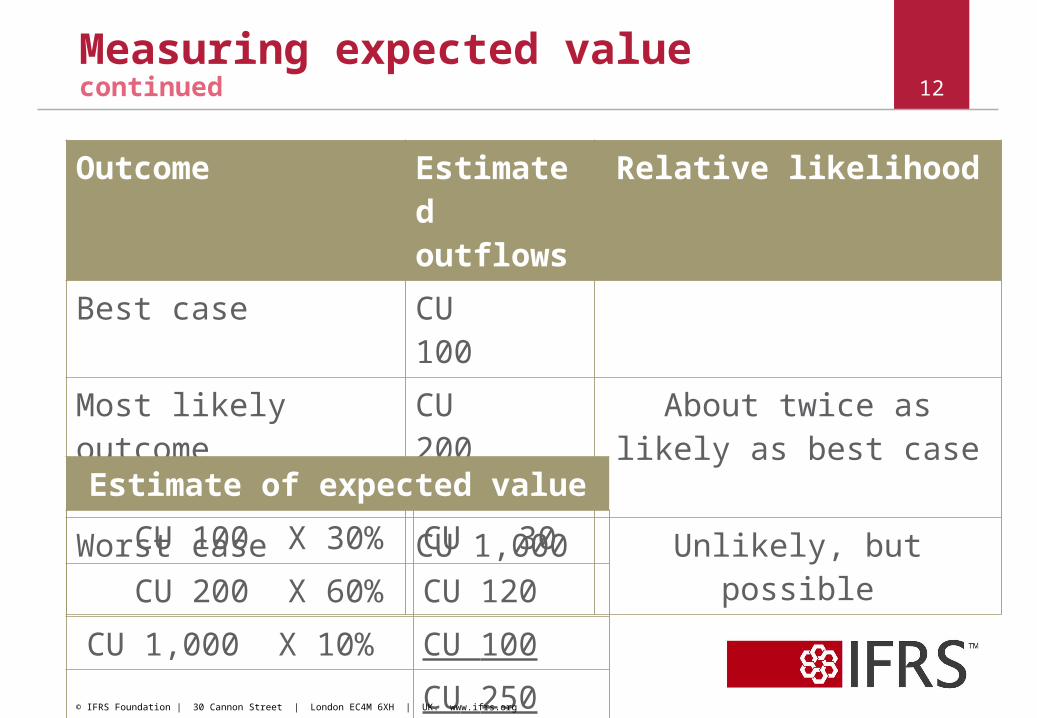

Measuring expected value continued 12

Outcome Estimated outflows

Relative likelihood

Best case CU 100

Most likely outcome CU 200 About twice as likely as best case

Worst case CU 1,000 Unlikely, but possible

Estimate of expected value

CU 100 X 30% CU 30

CU 200 X 60% CU 120

CU 1,000 X 10% CU 100

CU 250© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Myth 5 13

Expected values take

account of risk

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

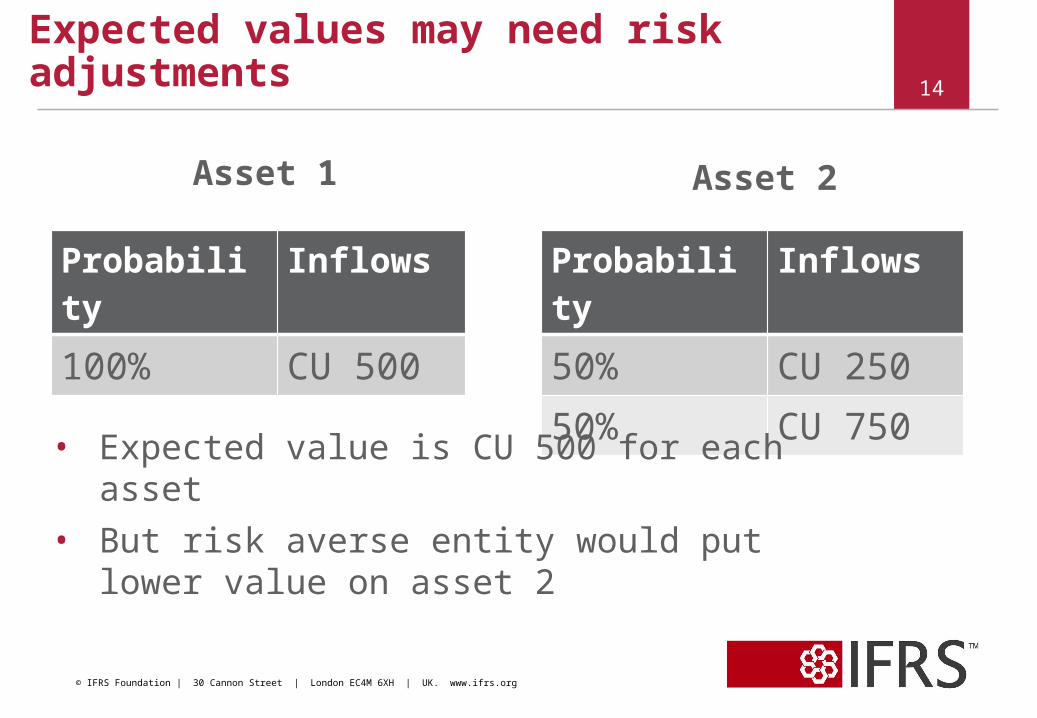

Expected values may need risk adjustments

Asset 1

Probability Inflows

100% CU 500

14

Asset 2

Probability Inflows

50% CU 25050% CU 750

• Expected value is CU 500 for each asset

• But risk averse entity would put lower value on asset 2

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Myth 6 15

Risk always increases

discount rates

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Risk adjustments for liabilities

• risk aversion typically increases transaction prices for uncertain liabilities

• in which case, account for risk by:

1. increasing estimates of cash outflows, or

2. adjusting estimates of probabilities, or

3. reducing rates at which cash outflows are discounted to present value, or

4. adjusting the expected present value

• adjusting discount rate doesn’t always work

16

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Questions or comments?

The IASB encourages its members and staff to express their individual views.

The views expressed in this presentation are those of the presenters.

Official positions of the IASB on accounting matters are determined only after extensive due process and deliberation.

17

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2011 IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

18

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2012 with an effective date after 1 January 2012 but not the IFRSs they will replace.

The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

18

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org