47376 MLF Cover - IIS Windows Serverlibrary.corporate-ir.net/library/88/884/88490/items/... · ·...

64

MAPLE LEAF FOODS INC. 2005 Annual Report MAPLE LEAF FOODS INC. 2005 ANNUAL REPORT Passionate People Passionate about Food

Transcript of 47376 MLF Cover - IIS Windows Serverlibrary.corporate-ir.net/library/88/884/88490/items/... · ·...

MA

PL

E

LE

AF

F

OO

DS

I

NC

.2

00

5

An

nu

al

R

ep

or

t

MAPLE LEAF FOODS INC. 2005 ANNUAL REPORT

Passionate People Passionate about Food

On the Cover: A historical landmark in Toronto, the

St. Lawrence Market and its many fine purveyors of

fresh meats, cheeses, produce and other food products

has served as the inspiration for food lovers for more

than 100 years. Such markets provide an ideal venue for

our passionate people who are constantly seeking new

ideas for innovative food products for our customers

and consumers.

Pictured left to right are: Jeannie Schmitz (Canada Bread

Fresh Bakery), Glen Gratton (Agribusiness Group),

Andy Persaud (Maple Leaf Consumer Foods) and

Valerie Walton (Maple Leaf Global Foods).

M A P L E L E A F F O O D S I N C .

30 St. Clair Avenue West, Suite 1500

Toronto, Ontario, Canada M4V 3A2

www.mapleleaf.com

Passionate People Passionate about Food

Printed in Canada

47376_MLF_Cover.qxd 3/20/06 4:36 PM Page 1

C O R P O R A T E P R O F I L E

aple Leaf Foods is a Canadian success story with

growing global reach. Our roots in the flour

business date back to a small-town mill in 1836, our

meat processing business back to the 1860s, and our

bakery business to the amalgamation of five separate companies in 1911.

Rich in history, Maple Leaf Foods entered our current growth phase in

1995 when McCain Capital Corporation pooled our expertise in

the food business with the financial resources of Ontario Teachers’

Pension Plan Board. Today, Maple Leaf Foods employs approximately

24,000 people, exports to nearly 80 countries, and operates in Canada,

the United States, the United Kingdom, Europe, Southeast

Asia and Mexico.

Our Meat Products and Agribusiness operations are strategically

linked to produce high quality meat products, minimize underlying

commodity market exposure, and maximize earnings. They include

animal nutrition, hog production, fresh value-added pork and poultry

products, processed meats and home meal solutions, global sales and

trading, and rendering operations.

Our Bakery operations are concentrated in North America and the

United Kingdom. We are the Canadian market leader in

premium nutrition fresh bakery products, such as whole grain and

organic breads. We are also a major North American supplier of

frozen ready-to-bake, par-baked and pre-baked breads, rolls and

specialty bakery items, in addition to fresh pasta and sauces. In the

U.K., we operate three plants, including one of the largest bagel plants

in the world, servicing the fast growing U.K. and European markets.

Our value creation strategy is supported by our flagship brands

which are growing well above industry averages – Maple Leaf® and

Schneiders® in the meat category and Dempster’s® in the bakery

category. They each deliver a promise to consumers: leadership in food

safety, quality and taste, and nutrition. Behind our products and our

many brands are our passionate people, and their passion for food.

M

Table of Contents1 Financial Highlights

2 Operations Overview

3 Segmented Operating Results

5 Letter from the Chairman

6 Letter to Fellow Shareholders

14 Financials

CAPITAL STOCK

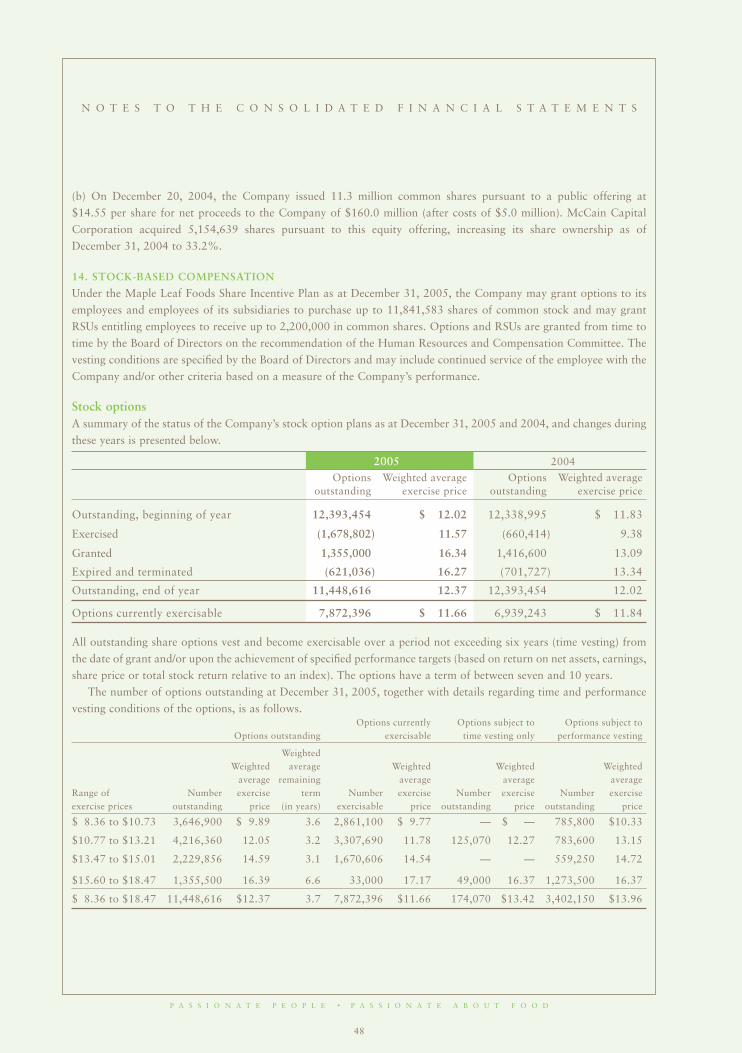

The Company’s authorized capital consists of anunlimited number of voting and an unlimited numberof non-voting common shares. At December 31, 2005,105,704,812 voting shares and 22,000,000 non-votingshares were issued and outstanding, for a total of127,704,812 outstanding shares. There were 1,208shareholders of record of which 1,163 were registeredin Canada, holding 99.4% of the issued voting shares.All of the issued non-voting shares are held by OntarioTeachers’ Pension Plan Board. These non-voting sharesmay be converted into voting shares at any time.

OWNERSHIP

The Company’s major shareholders are McCainCapital Corporation holding 41,518,153 sharesrepresenting 32.5% of the total issued and outstanding shares issued and Ontario Teachers’Pension Plan Board holding 20,728,371 voting sharesand 22,000,000 non-voting shares representing 33.4%of the total issued and outstanding shares. The remainder of the issued and outstanding shares arepublicly held.

CORPORATE OFFICE

Maple Leaf Foods Inc.30 St. Clair Avenue WestSuite 1500Toronto, Ontario, Canada M4V 3A2Tel: (416) 926-2000Fax: (416) 926-2018Website: www.mapleleaf.com

ANNUAL AND GENERAL MEETING

The annual and general meeting of shareholders ofMaple Leaf Foods Inc. will be held on Wednesday, April26, 2006 at 11:00 a.m. at the Glenn Gould Studio,Canadian Broadcasting Centre, 250 Front Street West,Toronto, Canada.

DIVIDENDS

The declaration and payment of quarterly dividends aremade at the discretion of the Board of Directors.Anticipated payment dates in 2006: March 31, June 30,September 29 and December 29.

SHAREHOLDER INQUIRIES

Inquiries regarding dividends, change of address,transfer requirements or lost certificates should bedirected to the Company’s transfer agent:Computershare Investor Services Inc.Stock and Bond Transfer Department100 University Avenue, 9th FloorToronto, Ontario M5J 2Y1Tel: (514) 982-7555or 1-800-564-6253 (toll-free North America)or [email protected]

COMPANY INFORMATION

For public and investment analysis inquiries, pleasecontact our Vice-President, Public & Investor Relationsat (416) 926-2000.

For copies of annual and quarterly reports, annualinformation form and other disclosure documents,please contact our Senior Vice-President, Transactionsand Administration and Corporate Secretary at(416) 926-2000.

TRANSFER AGENT AND REGISTRAR

Computershare Investor Services Inc.100 University Avenue, 9th FloorToronto, Ontario, Canada M5J 2Y1Tel: (514) 982-7555or 1-800-564-6253 (toll-free North America)or [email protected]

AUDITORS

KPMG LLP

Toronto, Ontario

STOCK EXCHANGE LISTINGS AND STOCK

SYMBOL

The Company’s voting common shares are listedon The Toronto Stock Exchange and trade under thesymbol “MFI”.

RAPPORT ANNUEL

Si vous désirez recevoir un exemplaire de la versionfrançaise de ce rapport, veuillez écrire à l’adressesuivante : Secrétaire de la société, Les Aliments MapleLeaf Inc., 30 St. Clair Avenue West, Toronto, OntarioM4V 3A2.

C O R P O R A T E I N F O R M A T I O N

47376_MLF_Cover.qxd 3/20/06 4:36 PM Page 2

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

1

F I N A N C I A L H I G H L I G H T S

• 66.6% Meat Products

• 20.8% Bakery Products

• 12.6% Agribusiness

• 72.9% Domestic

• 13.9% U.S.

• 13.2% Other International

TOTAL ASSETS BYGROUP

• 48.6% Meat Products

• 21.8% Bakery Products

• 20.0% Agribusiness

• 9.6% Non-allocated

• 38.7% Agribusiness

• 38.5% Bakery Products

• 22.8% Meat Products

For years ended December 31(In millions of Canadian dollars, except share information)

2005 2004 2003 2002 2001

Consolidated results

Sales $ 6,463 $ 6,365 $ 5,042 $ 5,076 $ 4,775

Earnings from operations (i) 263 256 152 204 158

Net earnings 94 102 30 80 53

Return on assets employed (ii) 8.2% 8.9% 6.4% 9.2% 7.6%

Financial position

Net assets employed (iii) $ 2,256 $ 2,105 $ 1,561 $ 1,430 $ 1,387

Shareholders’ equity 999 906 654 644 573

Net borrowings 1,063 1,046 785 667 685

Per share

Net earnings $ 0.74 $ 0.90 $ 0.27 $ 0.71 $ 0.55

Dividends 0.16 0.16 0.16 0.16 0.16

Book value 7.82 7.24 5.78 5.70 5.12

Number of shares (millions)

Weighted average 126.8 113.6 113.1 112.5 95.9

Outstanding at December 31 127.7 125.2 113.2 112.9 112.0

(i) Before restructuring costs (2003 and 2005).(ii) After tax, but before interest, calculated on average month-end net assets employed. Before restructuring costs (2003 and 2005).(iii) Total assets, less cash, future tax assets and non-interest bearing liabilities.

DOMESTIC VS.INTERNATIONAL SALES

SALES BY GROUP OPERATING EARNINGS BEFORE

RESTRUCTURING COSTS

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

2

• M A P L E L E A F C O N S U M E R F O O D S

Supported by our flagship brands – Maple Leaf® andSchneiders® – and a family of strong regional brands,Maple Leaf Consumer Foods is Canada’s leading producer of premium quality processed meat and home meal solutions. Products include refrigeratedfully cooked roasts, frozen meat products, bacon, ham,wieners, deli and canned meats, single serve entrées and“hand-held” meat and pastry products.Plants: 24, Distribution Centres: 7

• M A P L E L E A F F R E S H F O O D S

Maple Leaf Fresh Foods is Canada’s leading multi-species fresh meat company, producing premium quality, fresh and frozen value-added pork, chicken,and turkey products. Brands include Maple Leaf ® Prime™

Naturally*, Maple Leaf ® Fresh Grill!, Maple Leaf ®

Fresh Roast!, Maple Leaf ® Prime™ Turkey, Mitchell’sGourmet Foods and Maple Leaf ® Medallion™ Naturally.Plants: 12, Hatcheries: 3

• M A P L E L E A F G L O B A L F O O D S

Canada’s largest exporter of agri-food products, supported by global offices in key markets, includingSoutheast Asia, Europe and Mexico. Operationsinclude the marketing, distribution and trading ofvalue-added protein, bakery and agri-food products,including pork products, seafood, grain and soy products, pre-cooked meat and poultry products,french fries, bakery products and pet food.Plants: 2, Trading Offices: 8

B A K E R Y P R O D U C T S

F R E S H B A K E R Y

The leading Canadian producer and distributor of freshbaked products including breads, rolls, bagels andartisan breads with brands such as Dempster’s®,POM®, Ben’s®, McGavin’s and Healthy Way.Dempster’s® is the national brand leader in highernutrition, whole grain products. The Company alsomanufactures a variety of fresh and filled fresh pastaand sauces under the Olivieri® brand, distributing tocustomers across North America.Plants: 24, Distribution Centres: 12

* Canada’s leading brand of chicken

• E L I T E S W I N E

The Company’s hog management operations are animportant component of Maple Leaf’s quality controland Vertical Co-ordination strategy, supplyingapproximately 20% of Maple Leaf Fresh Foods’pork requirements. With 130,000 sows undermanagement, Elite Swine is the largest hog producerin Canada and the seventh largest production system inNorth America.

• M A P L E L E A F A N I M A L N U T R I T I O N

Canada’s leading animal nutrition organization, supported by leading trusted brands – Shur-Gain inEastern Canada and Landmark Feeds in WesternCanada – and excellence in research and development.The business provides animal nutrition products and services, including swine, dairy and beef cattle, poultry,aquaculture, equine and pet food.Feed Mills: 18, Retail Sales Centres: 13, Hatcheries: 3,

Research Facilities: 3

• R O T H S A Y

Canada’s largest recycler of animal by-products intovalue-added products, including animal feed, aminoacid supplements, biodiesel and other industrial uses.Rothsay provides an essential service for its customers and other Maple Leaf operations by responsibly managing and recapturing the value ofinedible by-products. Plants: 6

F R O Z E N B A K E R Y

A leading North American producer and distributor offrozen unbaked, par-baked and fully baked breads,rolls and bagels and artisan breads for retail and foodservice customers, and a U.K.-based producer ofbagels and specialty breads for the U.K. and Europeanmarkets. Brands include Grace Baking, CaliforniaGoldminer and the Wholesome Harvest line of premiumnutrition products, in addition to the New York Bagelbrand in the U.K. Plants: 12

P R O T E I N V A L U E C H A I N

• Maple LeafAnimal

Nutrition

Feed

• Elite Swine

HogProduction

• Maple Leaf Consumer Foods• Maple Leaf Fresh Foods• Maple Leaf Global Foods

Processing, Marketing & Distribution

• Rothsay

By-Products

O P E R A T I O N S O V E R V I E W

M E A T P R O D U C T S A G R I B U S I N E S S

For detailed information on these operations, visit www.mapleleaf.com.

P R O T E I N V A L U E C H A I N

(In millions of Canadian dollars)

2005 2004 % change

Meat Products Group

Sales $ 4,300 $ 4,127 4 %

Earnings from operations before restructuring costs 60 68 (13)%

Total assets 1,550 1,463 6 %

Agribusiness Group

Sales $ 817 $ 925 (12)%

Earnings from operations before restructuring costs 102 99 3 %

Total assets 640 603 6 %

TOTAL PROTEIN VALUE CHAIN

(In millions of Canadian dollars)

2005 2004 % change

Sales $ 5,117 $ 5,052 1 %

Earnings from operations before restructuring costs 162 167 (3)%

Total assets 2,190 2,066 6 %

The Meat Products Group includes Consumer Foods, Fresh Foods and Global Foods operations.

The Agribusiness Group comprises Animal Nutrition, hog production and rendering operations.

B A K E R Y P R O D U C T S G R O U P

TOTAL BAKERY PRODUCTS GROUP (In millions of Canadian dollars)

2005 2004 % change

Sales $ 1,346 $ 1,313 3 %

Earnings from operations before restructuring costs 101 89 14 %

Total assets 695 702 (1)%

The Bakery Products Group is comprised of Maple Leaf Foods’ 87.5% ownership in Canada Bread Company, Limited,

a leading producer and distributor of fresh and frozen bakery products and fresh pasta and sauces, with operations across

Canada, the United States and the United Kingdom.

S E G M E N T E D O P E R A T I N G R E S U L T S

Our independent directors have had highly successful

careers as leaders in business, academia and public

service. Because of this, they add significant

perspective and oversight into how management

shapes strategy and manages the business.”

From left to right:

Purdy Crawford

Michael McCain

Chaviva Hosek

Jim Hankinson

Scott McCain

Diane McGarry

Bob Stewart

Jeffrey Gandz

Ted Newall

Bob Hiller

Gord Ritchie

Don Loadman

“

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

5

L E T T E R F R O M T H E C H A I R M A N

Delivering long-term shareholder value is seldom a

straight line of profit gains. Implementing the right

strategy to achieve high financial returns in a

diversified global food company means growth

often happens in expansive bursts. It may come in

the form of large acquisitions that expand our

global presence, or exciting new product

innovations that transform the marketplace. Great

companies are premised on such intensity.

The alignment of growth ambitions with

shareholder value involves serious equity

commitments by directors and managers. Our two

largest shareholders – McCain Capital Corporation

and Ontario Teachers’ Pension Plan Board – own

approximately 70 percent of the Company. The 10

independent directors on our 13-member board

have also pledged a substantial amount as an

investment in our future.

An important distinction is that all shareholders

don’t necessarily share the same interests, because

investment horizons are different. Our Board and

management team are managing this Company for

long-term value creation. Shareholders, current and

prospective, should keep this top of mind as you

make investment decisions and measure our success.

We operate in a complex environment with

multiple stakeholders – government, communities,

unions and industry groups to name a few. On this

basis, shareholders need a Board well experienced

in value creation, but also who bring a diversity

of experience to the Company’s management. Our

independent directors have had highly successful

careers as leaders in business, academia and public

service. Because of this, they add significant

perspective and oversight into how management

shapes strategy and manages the business.

We are always looking for ways to better engage

directors in the business and with our people. Last

year, we introduced an innovative new program

called “Board Connect”, where directors spend a

day shadowing a senior operations manager. This

allows them to garner first hand insights into our

business and engage directly with our people. One

director enjoyed a day in the life of a sales executive,

another organizing fresh pork shipments across

the border, while a third participated with the

Consumer Foods’ management team in their annual

budget process. This program will continue in 2006.

Building corporate greatness means dramatic

changes in the next few years as we step with increased

boldness onto the world stage. Your Board will

assess these and all our major business decisions

with a shareholder lens; ensuring long-term value

creation is supported each step of the way.

Sincerely,

G. Wallace F. McCain,Chairman

G. Wallace F. McCainChairman

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

6

L E T T E R T O F E L L O W S H A R E H O L D E R S

We accomplished a great deal in 2005 as we

implemented structural changes throughout the

organization and increased operating earnings by

17% in the first nine months compared with the prior

year. Unfortunately that momentum slowed in the

fourth quarter due to a sharp rise in energy costs,

an unexpected drop in the yen, and higher timing

related advertising and promotion costs. The net result

for 2005 compared with the prior year was as follows:

• Sales increased by 2% to $6.5 billion

• Earnings from operations also increased by 3% to $2631 million

• Earnings per share declined to $0.811 from $0.90

• Cash flow from operating activities increased by

10% to $260 million

• Capital expenditures decreased to $152 million

from $157 million

• Return on net assets declined to 8.2%1 from 8.9%

• Share price closed the year at $15.20, up 1.5%,

outperforming the S&P Food Products Index by 7%

Operating earnings in our Meat Products Group

declined by 13% to $60 million for the year.

The main cause was an industry-wide contraction

in commodity processor margins – approximately

30% in pork and 41% in poultry versus the prior

year. We offset these negative underlying influences

in three ways. First, our Vertical Co-ordination

strategy to minimize commodity influences on our

earnings is working. We effectively own 20% of

our hog supply and this natural hedge against

high hog prices offsets a substantial portion of

the commodity processor margin decline. Second,

we added value to our commodity products

through gains in processing, innovation, and better

sales and marketing execution. Finally, our brand

focused, consumer-oriented, fresh bread and

consumer packaged meats and meals businesses

both performed brilliantly as a result of brand

marketing and sales effectiveness, operational

improvements, and lower raw material costs.

Higher hog prices were the main reason why our

Agribusiness Group’s operating profits increased

by 3% to $102 million. This improvement more

than offset the costs of commissioning a new

high-efficiency feed mill in Atlantic Canada. We

also completed construction of the first commercial

Michael H. McCainPresident and Chief Executive Officer

1 Before restructuring costs (please refer to Management’s Discussion and Analysis)

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

7

biodiesel plant in Canada, employing a proprietary

process developed at Maple Leaf Foods to convert

tallow into a valuable renewable fuel source. The

Agribusiness Group plays a vital role in our value

chain strategy by delivering stable earnings,

providing virtually all animal feed requirements to

our poultry producers and hog production business,

and converting inedible animal by-products into

earnings streams through our rendering operations.

Our Bakery Products Group, which reflects our

87.5% ownership of

Canada Bread, recorded

another very strong

year, capitalizing on

acquisitions and mergers

completed several years

ago. Operating earnings grew by 14% to

$101 million, driven largely by our fresh bakery

operations. The Group faced the challenges of

higher energy and distribution costs and the

start-up costs of a large bagel plant in the U.K. The

portfolio benefit of being in the bakery business

cannot be overstressed as there are excellent

synergies between the protein and bakery businesses.

We like this business very much and will continue

to acquire Canada Bread shares at the right price,

although we have no overt strategy to buy out the

remaining shares.

Maple Leaf continues to be a strong cash generator,

with $260 million in operating cash flow in 2005.

We invested $152 million in capital for the year,

which supported the construction of a high-

efficiency feed mill in Eastern Canada, a biodiesel

plant in Quebec and environmental upgrades in

our rendering business.

We ended the year with

a strong balance sheet,

reflected in a Net

Debt/EBITDA ratio of

2.6x and a commitment

to maintaining investment grade credit quality.

Our long-term compound annual growth rate in

earnings per share since 1995 is 10.4% versus our

goal of 15%, and our return on net assets was

8.2% in 2005, versus our target of 11.5%.

S I M P L I F Y I N G O U R S T R U C T U R E

Much of 2005 was devoted to building a stronger

organization that will support lasting long-term

“ M U C H O F 2 0 0 5 WA S D E V O T E D

T O B U I L D I N G A S T R O N G E R

O R G A N I Z AT I O N T H AT W I L L

C R E AT E L A S T I N G L O N G - T E R M

S H A R E H O L D E R VA L U E . ”

Ear

ning

s Pe

r Sh

are

(1)

RONA

Long-Term Financial Targets:EPS CAGR > 15%RONA 11.5%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

(1) Before restructuring costs

EPS

RONAEPS CAGR: 10.4%

L E T T E R T O F E L L O W S H A R E H O L D E R S

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

8

L E T T E R T O F E L L O W S H A R E H O L D E R S

shareholder value. We began 2005 with 14

independent operating companies, plus several

ancillary business units. We finished the year with

10 streamlined operating companies. All consumer

foods businesses, including Schneider Foods,

Maple Leaf Consumer Foods and Larsen Packers,

were merged as Maple Leaf Consumer Foods. Our

fresh pork and poultry operations were consolidated

as Maple Leaf Fresh Foods. In the Agribusiness

Group, Shur-Gain and Landmark Feeds were

combined as Maple Leaf Animal Nutrition. Our

international trading business was reorganized as

Maple Leaf Global Foods, and is expanding beyond

its core strength in trading to increase geographic

and value-added product diversification.

These types of mergers always put strain on an

organization. Supported by the discipline and

methodology of Six Sigma, they were accomplished

with professionalism and stability, ensuring we

always kept our customers’ needs first. The task of

aligning our core processes and completing very

complex organizational change will continue in

2006. This simpler organizational structure will

deliver operational efficiencies and enable us

to more effectively leverage the competitive

advantages of our national scope, strong brands

and product diversity.

O U R F O U N D A T I O N S

The enduring feature of our Company is our deep

conviction in the long-term benefit of investing in

people and disciplines, specifically our Leadership

Edge and Six Sigma programs. In 2005, we

expanded that commitment by investing over 8,400

person days in leadership values and skills

development through the Maple Leaf Leadership

Academy and Six Sigma training programs. Our team

of 130 Six Sigma Black Belt professionals manage a

portfolio of what is now more than 570 projects.

We know from long experience that safe plants

are well run plants. We are pleased to report that

we recorded our fifth consecutive year of double-

digit improvement in health and safety measures.

In 2005, our lost time accident frequency rate

improved by a remarkable 38%.

F O U R T H Q U A R T E R C H A L L E N G E S

Our fourth quarter results dampened a year of

strong operating performance due to three factors.

First, we faced unprecedented rapid increases in

energy costs, with more than 40% of oil and gas

cost increases occurring in Q4. This is a large cost

From left to right: Wayne Johnson, Brock Furlong, Lynda Kuhn, Doug Dodds

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

9

L E T T E R T O F E L L O W S H A R E H O L D E R S

line that affects each of our business units either

directly in the case of manufacturing and

distribution or indirectly in higher ingredient,

packaging and overhead costs. We are confident

that we will be able to pass these cost increases on

in our pricing, although there is a lag effect,

category by category, as we plug into natural

re-pricing rhythms with our customers.

Second, the yen declined 16% against the

Canadian dollar in the quarter compared to the first

six months of 2005,

causing margin pressure

on our Japanese pork

exports, which are priced

in yen. While this should

normalize over the

medium term, it accounted for a significant portion of

the fourth quarter earnings decline. Japan is

important to our fresh pork strategy and is a great,

though inconsistent market from quarter to quarter.

In Q4 we experienced the downside of this curve,

although our results in Japan for the full year were

satisfactory. Compounding the currency impact, the

Japanese market finished the year with unusually

high frozen pork inventories, as domestic

consumption returned to more normal levels after

two robust years. We believe that both of these

factors are short term. Meanwhile, we have made

headway in diversifying our international markets

for premium quality pork, although there is still

lots of opportunity to better balance our important

Japanese business with other markets.

Third, advertising and promotional costs to

support product launches and brand building were

higher due to timing related costs that are

expected to yield returns

in market share and

brand leadership.

Despite these short-

term challenges, the

foundations of the

business continue to get stronger with each passing

year. We have aggressive growth targets and, as

significant shareholders, take a longer-term view to

wealth creation. The Maple Leaf story will never

be a straight line of rising profits. While we seek

steady earnings growth, we do not manage the

business quarter to quarter. Our commitment to

long-term shareholder value creation is resolute.

“ D E S P I T E T H E S E S H O R T- T E R M

C H A L L E N G E S , T H E F O U N D AT I O N S

O F T H E B U S I N E S S C O N T I N U E

T O G E T S T R O N G E R W I T H

E A C H P A S S I N G Y E A R . ”

From left to right: Rick Young, Rocco Cappuccitti, Kevin Golding, Jerry Vergeer, Bruce Miyashita

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

10

L E T T E R T O F E L L O W S H A R E H O L D E R S

V A L U E C R E A T I O N S T R A T E G I E S

A N D O P P O R T U N I T I E S

The food business provides enormous opportunities

for companies that understand and achieve the

necessary balance between rigorously controlling

costs and growing the top line profitably through

innovation and adding value.

At Maple Leaf Foods, seven strategic elements

form the blueprint for wealth creation and govern all

key business decisions. Each is underpinned with

specific medium-term initiatives:

• Add value for our customers

• Add value to our products

• Invest in leading market shares

• Build our brands

• Innovate

• Drive costs out

• Diversify globally

We are continuously seeking to move our customer

relationships from transactional to strong “enterprise”

partnerships by developing deep insights into their

needs and tailoring our relationship to plug into each

of their unique strategies. Our value-added product

focus spans the Company, from innovation in feed

formulation to new bakery product technology such

as FroBake® in our bakery business. Market share

leadership is critical in this industry to

establish stable market conduct and achieve high

plant efficiencies. We will not compete in a market

that we cannot lead and we have leading market

shares in all our businesses. We are brand equity

builders, and we use innovation as a key brand

building platform. Driving costs out of our business

model is essential to success, supported by Six Sigma

methodology and insights, appropriate capital

investments, consolidation of supply chains into

larger scale facilities, and application of standardized

processes throughout our business structure. We

expect longer-term value creation will be driven by

global diversification, which offers excellent

opportunities in both protein and bakery.

Applying these strategic principles, there are four

major value creation opportunities in the mid-term, in

addition to our many other initiatives. The first is to

complete the merger between Schneider Foods and

Maple Leaf and realize the synergies that result from

having leading brands and market shares in Canadian

packaged consumer meats and meals. The second is

to grow margins in our fresh meat businesses by

adding value to commodity products through service

and value-added processing. The third is harvesting

our investment in the frozen and U.K. bakery

From left to right: Barry McLean, Randy Powell, Michael Detlefsen, Annalisa King

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

11

L E T T E R T O F E L L O W S H A R E H O L D E R S

businesses, where we feel we have significant

opportunity to drive sales volume and earnings

growth. The fourth is to reduce costs in our hog

production operations and restore competitiveness

with the U.S. industry.

M E G A - B R A N D S ; M E G A F U T U R E

The equity in a brand accrues benefits to brand

owners for decades. Very few companies have a

single “mega-brand”. In Canada, we are proud to

have three leading food brands – Schneiders®, Maple

Leaf® and Dempster’s®.

They are among the top

25 brands in the country

and growing well in

excess of the average for

this peer group – a major

accomplishment of our sales and marketing teams. What

keeps these brands fresh, hot and generating better

returns? A time-tested recipe of brand strategy, brand

support and lots of brand innovation.

The Schneiders® brand has penetrated the position

of “Taste The Difference Quality Makes®” deep into

the Canadian awareness. Supported by European

craftsmanship, heritage and top quality ingredients,

the “taste” proposition continues to resonate

with consumers. The Maple Leaf® brand position

of “We Take Care™” gives consumers added

confidence through our commitment to food safety

leadership. In the bakery category, Dempster’s® leads

the premium nutrition whole grain bakery market,

supported by the newly launched brand position

“Nourish Yourself™”. As one of Canada’s leading

national TV advertisers, we support these brands with

continuous and creative breakthrough advertising.

Brands drive market share leadership, and

innovation drives brands. Consumers are always

seeking something “new”

from the brands they

trust. O u r innovation

platform keeps getting

stronger and stronger.

Recent examples include

Maple Leaf® Fully Cooked Roasts, Maple Leaf®

Fresh Grill! and Maple Leaf® Fresh Roast!, all

targeted to meet the needs of time-starved

consumers. In the bakery category, early in 2006

we launched Dempster’s® Smart™, a white bread

made with all the benefits of whole grains and the

first product of its kind in Canada.

T H E N E X T C H A P T E R

The last decade has been transformational. In

many ways, that’s just the end of the first chapter.

“ S C H N E I D E R S ® , M A P L E L E A F ® A N D

D E M P S T E R ’ S ® . . . A R E A M O N G T H E

T O P 2 5 B R A N D S I N T H E C O U N T RY A N D

G R O W I N G W E L L I N E X C E S S O F T H E

AV E R A G E F O R T H I S P E E R G R O U P. ”

From left to right: Rory McAlpine, Peter Smith, Maryanne Chantler, Pat Ressa Absent: Peter Maycock

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

12

L E T T E R T O F E L L O W S H A R E H O L D E R S

Long-term we won’t achieve our ambitious

shareholder return targets solely as a $6.5 billion

Canadian protein and bakery company. We must

take on bigger challenges and more well managed

risks to achieve exceptional returns. We have

defined the agenda for the next decade as follows.

First, we always have and always will begin with

our foundations – Leadership Edge and Six Sigma.

This is our past, our present and our future, but we

are looking at both of these foundations through

new prisms. We need to

take them deeper into the

organization – right to

the front line to engage

100% of our people.

Second, we will take

steps to strengthen “fortress Canada” to ensure it

can profitably grow and sustain any competitive

challenges. This will mean substantial increases in

our capital spending to consolidate operations into

“mega-plants” with world leading technology.

There are opportunities to make such investments in

each segment of our business.

Third, we are stepping up our commitment to

innovation, underpinning the “mega-brands” in our

portfolio. We will do so by enhancing the role of

a “culinary” strategy in our Company, by improving

our new product development processes, by

expanding our leadership in delivering convenience

and nutrition, and by developing greater external

relationships with innovation partners. We are

building a culture that is passionate about food!

Finally, significant investments outside Canada are

imperative to expand our geographic reach in our core

categories and realize our growth and financial

goals. In 2005, our Board reviewed and accepted

broad parameters for such

investments. However,

there must be a visible,

compelling value creation

strategy behind our

investments. We will look

for a convincing path to market/category leadership

that fits well with our existing organization. We also

must be in a state of readiness. We are not there yet,

but we are getting ready. Our balance sheet is in

excellent shape and we expect that by early 2007, the

organizational mergers previously described will be

largely complete. We are taking steps to enhance the

global depth and readiness of our talent and we are

assessing in detail the various market opportunities

available to us.

“ M A P L E L E A F P E O P L E A R E

P A S S I O N AT E , C O M M I T T E D P E O P L E

W H O G E T T H I N G S D O N E , A R E

O U T R A G E O U S LY T E N A C I O U S , A N D W H O

A LWAY S K E E P T H E I R E Y E O N T H E P R I Z E . ”

From left to right: Richard Lan, Scott McCain, Tom Muir, Michael Vels, Michael McCain

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

13

L E T T E R T O F E L L O W S H A R E H O L D E R S

Over the longer-term, we are also proactively

minimizing risk from disease by preparing ourselves

for the potential outbreak of a global influenza

pandemic. We pay close attention to the risk of

avian influenza due to our industry affiliations.

While we are primarily a processor and our business

model is to not own poultry growing operations, we

are taking steps with our employees and producer

partners to reduce risk. The larger concern we all

share is the threat of a pandemic in the human

population. We cannot control this outcome,

although we can take a leadership position in

preparedness, which is exactly what we are doing

– both in our industry and inside our Company.

P A S S I O N A T E P E O P L E ;

P A S S I O N A T E A B O U T F O O D

We continue to nurture and develop the greatest

asset of this organization – our people and their

leadership capabilities, which defines our culture.

Maple Leaf people are passionate, committed

people who get things done, are outrageously

tenacious, and who always keep their eye on the

prize. It’s an amazing place!

Adding to this team are the newest members of

our Executive Council, Annalisa King who leads our

Vertical Co-ordination group, and Maryanne

Chantler who heads up our Purchasing and Supply

Chain group. Both Annalisa and Maryanne have a

strong history in operating and finance roles at

Maple Leaf and they continue to make outstanding

contributions in their new responsibilities. Rory

McAlpine, who has a diverse background in

government and international trade, also recently

joined Maple Leaf’s senior leadership team, to

lead and build our Government and Industry

Relations program.

We are entering 2006 with a great deal of

confidence. Our underlying operating and financial

fundamentals are strong and the talent we have

across the organization, thousands of Maple Leaf

Foods employees, is what will drive value

creation. They are an amazing team, and on that

basis you have invested well.

Michael H. McCain President and

Chief Executive Officer

Richard A. LanPresident and Chief Operating Officer,

Bakery Products Group

J. Scott McCainPresident and Chief Operating Officer,

Agribusiness Group

Tom P. Muir Executive Vice-President andChief Development Officer

Michael H. VelsExecutive Vice-President and

Chief Financial Officer

F I N A N C I A L S

Financial Contents

15 Results of Operations

16 Operating Segments

17 Operating Review

17 Meat Products Group

18 Agribusiness Group

19 Bakery Products Group

20 Acquisitions

21 Capital Resources and Liquidity

23 Derivatives

24 Environment

24 Risk Factors

28 Critical Accounting Estimates

29 Changes in Accounting Policies

30 Recent Accounting Pronouncements

32 Summary of Quarterly Results

32 Forward-Looking Statements

34 Management’s Statement of Responsibility

34 Auditors’ Report to the Shareholders

35 Consolidated Financial Statements

38 Notes to the Consolidated Financial Statements

58 Corporate Governance and Board of Directors

60 Senior Management and Officers

61 Corporate Information

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

15

THE BUSINESS

Maple Leaf Foods Inc. is a leading Canadian food

processing company committed to delivering quality

food products to consumers around the world. Head-

quartered in Toronto, Canada, the Company employs

approximately 24,000 people at its operations across

Canada and in the United States, Europe and Asia.

EFFECT OF RESTRUCTURING AND OTHER ITEMS

Except where noted, operating earnings, net earnings,

earnings per share (“EPS”) and return on net assets

(“RONA”) comparisons for 2005 exclude

$13.2 million before tax ($8.3 million after-tax and

minority interest) in restructuring costs incurred in the

first quarter of 2005. Management believes that this is

the most appropriate basis on which to evaluate

operating results, as restructuring costs are not

representative of continuing operations. Year-over-year

and quarterly comparisons are also affected by the

inclusion of an additional week of operations in the

fourth quarter of 2004, which affect sales and earnings

comparisons in the fourth quarter and full year.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

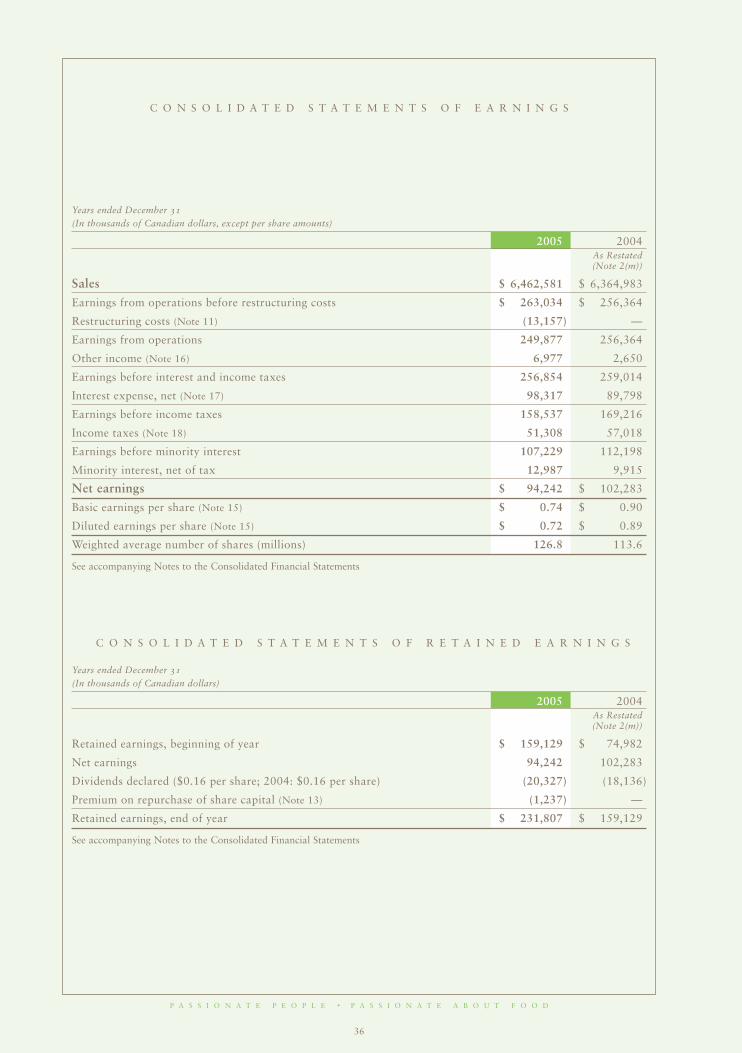

SELECTED FINANCIAL HIGHLIGHTS

The following is a summary of audited financial information for the three years ended December 31, 2005.

(In thousands of dollars except per share information) 2005 2004 2003

Sales $ 6,462,581 $ 6,364,983 $ 5,041,896

Operating earnings before restructuring costs 263,034 256,364 152,428

Net earnings(i) 94,242 102,283 30,217

Net earnings before restructuring costs(i) 102,588 102,283 40,609

Total assets 3,189,780 3,038,133 2,148,721

Net debt 1,062,755 1,046,335 696,678

RONA(ii) 8.2% 8.9% 6.4%

Per share

EPS $ 0.74 $ 0.90 $ 0.27

EPS before restructuring costs $ 0.81 $ 0.90 $ 0.36

Cash dividends $ 0.16 $ 0.16 $ 0.16

(i) 2003 and 2004 restated in accordance with Note 2 to the Consolidated Financial Statements. (ii) This is not a recognized measure under Canadian Generally Accepted Accounting Principles. The calculation of RONA comprises tax-

affected earnings before interest divided by average monthly net assets. Net assets are defined as total assets, less cash, future tax assetsand non-interest bearing liabilities. These calculations and definitions may not be comparable to measures used by other companies.

RESULTS OF OPERATIONS

Operating results for 2005 reflected strong performance

from most businesses and the full year contribution of

Schneider Foods, purchased in April 2004. Earnings for

the full year were affected by weaker results in the

fourth quarter, due to a combination of factors,

including higher energy costs, lower earnings from

exports to Japan and higher advertising and

promotional costs. Management is of the opinion that

these are largely short-term factors which can be

mitigated through price increases. The value-added

businesses, particularly consumer products and fresh

bakery, contributed strongly to earnings through a

combination of new product innovation, operating

improvements and lower raw material costs in the meat

business earlier in the year. The Company also benefited

from portfolio balance across the Protein Value Chain

operations as weaker commodity processing margins

and lower rendering earnings were partly offset by

higher hog profits. Overall, changes in prices of

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

16

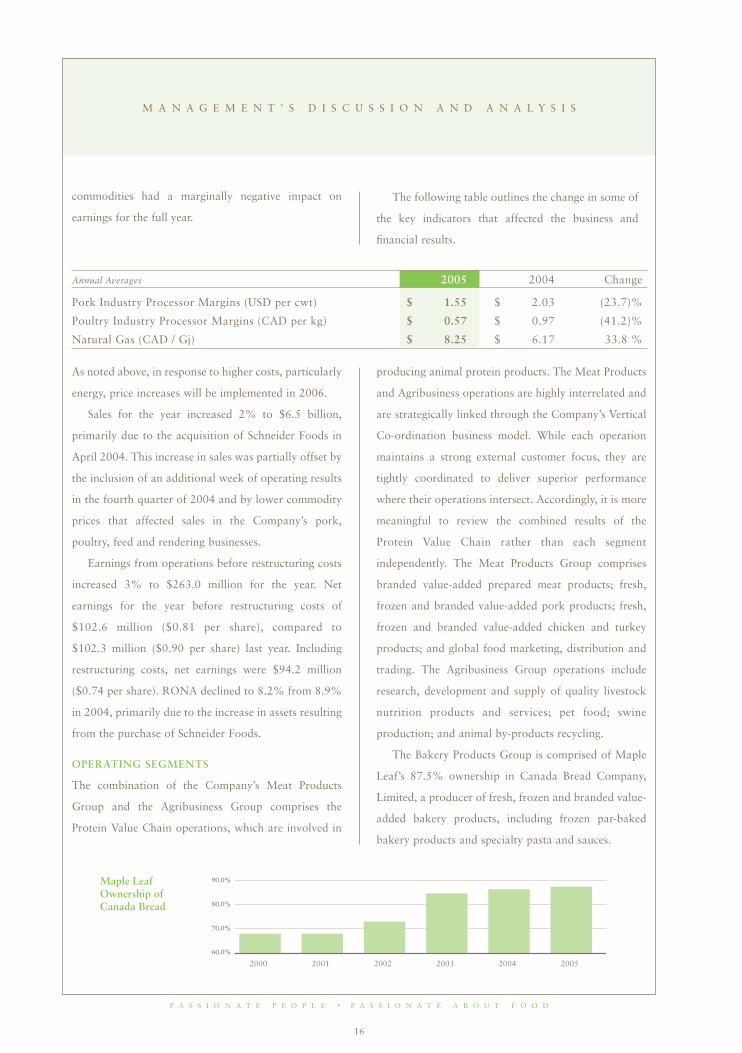

As noted above, in response to higher costs, particularly

energy, price increases will be implemented in 2006.

Sales for the year increased 2% to $6.5 billion,

primarily due to the acquisition of Schneider Foods in

April 2004. This increase in sales was partially offset by

the inclusion of an additional week of operating results

in the fourth quarter of 2004 and by lower commodity

prices that affected sales in the Company’s pork,

poultry, feed and rendering businesses.

Earnings from operations before restructuring costs

increased 3% to $263.0 million for the year. Net

earnings for the year before restructuring costs of

$102.6 million ($0.81 per share), compared to

$102.3 million ($0.90 per share) last year. Including

restructuring costs, net earnings were $94.2 million

($0.74 per share). RONA declined to 8.2% from 8.9%

in 2004, primarily due to the increase in assets resulting

from the purchase of Schneider Foods.

OPERATING SEGMENTS

The combination of the Company’s Meat Products

Group and the Agribusiness Group comprises the

Protein Value Chain operations, which are involved in

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

Annual Averages 2005 2004 Change

Pork Industry Processor Margins (USD per cwt) $ 1.55 $ 2.03 (23.7)%

Poultry Industry Processor Margins (CAD per kg) $ 0.57 $ 0.97 (41.2)%

Natural Gas (CAD / Gj) $ 8.25 $ 6.17 33.8 %

producing animal protein products. The Meat Products

and Agribusiness operations are highly interrelated and

are strategically linked through the Company’s Vertical

Co-ordination business model. While each operation

maintains a strong external customer focus, they are

tightly coordinated to deliver superior performance

where their operations intersect. Accordingly, it is more

meaningful to review the combined results of the

Protein Value Chain rather than each segment

independently. The Meat Products Group comprises

branded value-added prepared meat products; fresh,

frozen and branded value-added pork products; fresh,

frozen and branded value-added chicken and turkey

products; and global food marketing, distribution and

trading. The Agribusiness Group operations include

research, development and supply of quality livestock

nutrition products and services; pet food; swine

production; and animal by-products recycling.

The Bakery Products Group is comprised of Maple

Leaf’s 87.5% ownership in Canada Bread Company,

Limited, a producer of fresh, frozen and branded value-

added bakery products, including frozen par-baked

bakery products and specialty pasta and sauces.

Maple Leaf Ownership of Canada Bread

60.0%

70.0%

80.0%

90.0%

2000 2001 2002 2003 2004 2005

commodities had a marginally negative impact on

earnings for the full year.

The following table outlines the change in some of

the key indicators that affected the business and

financial results.

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

17

Protein Value Chain Operations Protein Value

Chain earnings for the year declined 3% due to

industry-wide decreases in both pork and poultry

processor margins, higher energy costs, higher costs in

the Company’s hog production operations and lower

profits from rendering operations. These factors more

than offset positive contributions from consumer

products and lower feed costs.

Meat Products Group Sales for the year were up

4% to $4.3 billion compared to $4.1 billion last year,

due to the acquisition of Schneider Foods in April 2004.

Offsetting this was the effect of lower commodity prices

that reduced sales values. Earnings from operations for

the year were $59.9 million, down from $68.5 million

last year.

The consumer products business, which is the

combination of the Schneider Foods and the former

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

Maple Leaf Consumer Foods operations, achieved

excellent operating results driven by the full-year

contribution of Schneider Foods, lower raw material

costs and the contribution of higher margin products

such as Maple Leaf Fully Cooked Roasts and

Schneiders lunch kits. These strong results were partly

offset in the fourth quarter by higher energy costs and

timing of advertising and promotional spending to

support brand positioning and new product launches.

This business will implement price increases in 2006 to

offset inflationary costs.

The Schneider Foods merger has met expectations to

date. In 2005, the two organizations were combined

with the majority of systems integration to follow in

2006. This will yield future gains in procurement,

supply chain, working capital and customer service. An

integrated manufacturing strategy will be implemented

OPERATING REVIEW

The following table, which forms the basis of discussion in this document of the Company’s results of operations,

reflects operating earnings by business group before restructuring costs.

Earnings from Operations

($ millions) 2005 2004 Change 2003

Meat Products Group $ 59.9 $ 68.4 (13)% $ 24.3

Agribusiness Group 101.8 98.7 3 % 69.9

Protein Value Chain 161.7 167.2 (3)% 94.2

Bakery Products Group 101.3 89.2 14 % 58.2

$ 263.0 $ 256.4 3 % $ 152.4

Segmented Operating Earnings

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Meat Products Group

Agribusiness Group

Bakery Products Group

0

(50)

50

100

150

200

250

300

Ear

ning

s fr

om O

pera

tion

($

mill

ions

)

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

18

beginning in 2007, although some benefits from

optimizing the manufacturing network will be realized

in 2006. The acquisition of Schneider Foods has given

the Company an effective balance between fresh

primary processing and further processed products,

resulting in a desirable mix of commodity-influenced

and more stable value-added branded businesses. Over

time, in most market conditions, management expects

that this should result in higher margins and less

volatile earnings, particularly when these results are

combined with the counter-cyclical earnings of the

Agribusiness Group.

Earnings from fresh poultry operations declined

sharply in 2005 due to lower industry-wide processor

margins. These margins were at unusually high

levels in 2004 due to a supply shortage related to

avian influenza.

The contribution from primary pork processing

operations was down marginally compared to the prior

year. In 2005, the North American pork processor

spread was lower than 2004 and well below the five-

year average. However, pork processing performance

benefited from an improved value-added sales mix,

increased manufacturing efficiencies and higher

earnings from the Japanese pork market in the first

three quarters of 2005. However, the fourth quarter

was impacted by a 16% depreciation of the Japanese

yen against the Canadian dollar compared to the first

half of 2005, which resulted in a decline in the sales

value and profitability of pork exports to Japan.

In 2005, the Company announced that it will invest

up to $110 million to construct a fresh pork processing

plant in Saskatoon, Saskatchewan. The new plant will

replace a 65-year-old plant in Saskatoon acquired as

part of the purchase of Schneider Foods. The current

facility provides over two-thirds of its production to

other Maple Leaf value-added processing facilities in

Saskatchewan. The new plant will increase production

capacity from the current 17,500 to 20,000 hogs per

week on a single shift, with the capability to process up

to 40,000 on a double shift. Subject to Company and

government approvals, the Province and the City have

committed to infrastructure support that will affect the

ultimate expenditure by the Company. Construction is

expected to commence by mid-to-late 2006 with the

plant commissioned 18 to 24 months later.

Agribusiness Group Sales for the year declined

12% to $816.8 million from $924.9 million last year

due to lower market prices for feed and rendered

products, reflecting lower underlying commodity

prices. Earnings from operations for the year increased

3% to $101.8 million from $98.7 million in 2004.

Contributing to the earnings increase was an

improvement in hog production margins driven

primarily by lower prices for feed grains; however, this

was partially offset by a 4% decline in hog prices

compared to last year. The Company had effective

ownership of 20% of the hogs it processed in the year.

Although hog profits were higher, the Company’s hog

production operations underperformed in the face of a

stronger Canadian dollar and higher operating costs.

The Company has a number of initiatives underway to

improve performance and reduce costs in this business.

Earnings from the rendering operations for the year

declined due to a reduction in export volumes and

lower prices for finished products, compounded by

rapidly rising energy costs. These factors overshadowed

increased operating efficiencies due to a capital

investment in environmental upgrades over the last

number of years. In the fourth quarter, the Company

commissioned a new commercial scale biodiesel plant

in Quebec, which will provide an alternate higher value

market for tallow.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

19

The animal nutrition operations continued to post

steady results for the year.

Bakery Products Group Sales increased by 3% to

$1.3 billion, reflecting higher prices and continued

growth in higher value whole grain and specialty

products. Sales comparisons would have been stronger

if not for the inclusion of an additional week of

operating results in the fourth quarter of 2004.

Earnings from operations for the year increased 14%

to $101.3 million from $89.2 million in 2004 as price

increases and a sales mix that is weighted towards health

and well-being categories contributed to earnings in the

first three quarters. Earnings, particularly in the fourth

quarter, were negatively impacted by higher fuel, energy

and other inflationary costs.

Strong sales of branded whole grain, whole wheat

and specialty fresh bakery products, higher prices, and

Six Sigma driven operating improvements all

contributed to strong earnings growth for the year. This

offset the impact of rising fuel, energy and flour costs

and increased advertising and promotional spending in

the back half of the year.

The Olivieri pasta and sauce business experienced

year over year sales and volume growth reflecting a

decline in the effect of low carbohydrate diets.

The North American frozen business experienced

significant increases in fuel, energy and related costs

which offset the operational improvements in the year

in freight and distribution.

The U.K. bakery operations benefited from sales

growth largely due to overall market growth of

18%. Full year margin growth in 2005 was more than

offset by increased advertising expenditures to support

the New York Bagel brand in the U.K., higher energy

and flour costs and additional costs associated with

commissioning a new bagel plant in Rotherham, England.

Other Income Other income increased to

$7.0 million, up from $2.7 million in 2004. The

increase was due to substantially higher earnings from

equity investments acquired as part of the Schneider

Foods acquisition, insurance proceeds, and gains on

fixed asset disposals that were partially offset by a loss

on conversion of the convertible debenture in the first

quarter of 2005.

Restructuring Costs During the first quarter of

2005, the Company recorded $13.2 million in

restructuring costs ($8.8 million after-tax) in respect of

certain plant closures and operational restructuring for

several of its businesses associated with the integration

of Schneider Foods, the closure of the Company’s

bakery in Peterborough, England, and certain other

operational restructuring items. Of the $13.2 million,

$5.0 million represents the writedown of certain capital

assets that were disposed of or that have become

impaired as a result of restructuring and $8.2 million

relates to provisions for employee terminations, facility

exit costs, and other restructuring costs. Of the

$8.2 million in provisions, $2.9 million was paid

in 2005.

The Company expects to complete the remaining

major components of these restructuring plans in 2006.

Furthermore, management continues to seek out

efficiencies and further optimization opportunities. Any

such rationalization initiatives undertaken in 2006 may

result in charges to earnings and will be recorded in the

quarter in which they occur and disclosed as

restructuring costs.

Interest Expense Interest expense for the year

increased to $98.3 million compared to $89.8 million

last year. In the fourth quarter of 2004, the Company

refinanced a significant portion of its debt, replacing

short-term, lower rate debt with longer-term, fixed rate

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

20

notes that have higher interest rates than short-term

floating debt and therefore contributed to higher

average interest rates of 6.2% paid compared to last

year (2004: 6.0%). A full year impact of the acquisition

of Schneider Foods, partly offset by an equity issue in

December 2004, also contributed to higher interest

expense in the current year. At December 2005, 86% of

indebtedness was not exposed to interest rate

fluctuations.

Income Taxes Income tax expense decreased to

$51.3 million from $57.0 million in 2004. The

Company’s effective tax rate was 32.4% in 2005

compared to 33.7% in 2004. Components of the

changes are provided in Note 18 to the Consolidated

Financial Statements.

ACQUISITIONS

On April 5, 2004, the Company acquired Schneider

Foods for cash consideration of $376.7 million,

including transaction costs of $8.1 million and the

assumption of Schneider Foods’ debt, for a total

purchase price of approximately $500 million.

Schneider Foods is one of Canada’s largest producers

of premium-branded quality food products, specializing

in packaged processed meats, poultry and grocery

products. The Company employs approximately 5,000

people at 20 facilities across Canada.

As at June 30, 2005, the purchase price allocation

(including fair values assigned to intangible assets,

certain fixed assets, legal claims, long-term debt,

pensions, post-retirement benefits and taxes) had been

completed. Other costs of integration that cannot be

allocated to the purchase price were charged to earnings

as incurred. Goodwill resulting from the transaction is

included in the total assets of the Meat Products Group.

The acquisition of Schneider Foods transforms the

Meat Products Group since it significantly increased the

mix of value-added products and management

anticipates this will result in higher margins and more

stable cash flow and earnings. Schneider Foods

and Maple Leaf Consumer Foods have highly

complementary businesses and brands that provide for

significant growth and cost reduction opportunities for

the combined operations.

In May 2005, the Company purchased the

remaining 32% interest in a subsidiary of Schneider

Foods, Cappola Food Inc., for net proceeds of

approximately $3.6 million resulting in additional

goodwill of approximately $1.5 million.

TRANSACTIONS WITH RELATED PARTIES

During 2004 and 2005, the Company completed a

series of market and private agreement purchases of

Canada Bread shares. As a result of these transactions,

the ownership interest in Canada Bread increased from

84.7% at the beginning of 2004 to 87.5% as 225,300

(2004: 490,400) shares were purchased in 2005.

The aggregate value of cash paid and shares issued

to finance these transactions in 2004 and 2005 was

$29.4 million and the allocation of these amounts to

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

160

80

120

)snoillim $( xepa

C

Capital Expenditures

1996

83.2

1995

71.8

1997

114.9

1998

90.8

1999

121.8

2000

108.6

2001

86.8

2002

92.2

2003

132.6

2004

156.8

2005

152.1

Meat Products Group

Agribusiness Group

Bakery Products Group

Depreciation

0

40

140

60

180

100

20

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

21

the underlying assets and liabilities of Canada Bread

resulted in an increase in goodwill of $10.8 million.

On December 20, 2004, the Company issued

11.3 million common shares pursuant to a public

offering at $14.55 per share. McCain Capital

Corporation acquired 5,154,639 shares pursuant to

this equity issue, increasing its share ownership in the

Company to 33.2%.

CAPITAL RESOURCES AND LIQUIDITY

The food industry segments in which the Company

operates are generally characterized by high sales

volume and rapid turnover of inventories and accounts

receivable. In general, accounts receivable and

inventories are readily convertible into cash. An

exception to this is the Agribusiness Group where credit

granted to agricultural customers can have longer

collection terms that are matched to crop and livestock

cycles. Investment in working capital is also affected by

fluctuations in the prices of raw materials, seasonal and

other market-related fluctuations. For example,

although an increase or decrease in pork or grain

commodity prices may not affect margins, they can

have a material effect on investment in working capital,

primarily inventory and accounts receivable.

Due to its diversity of operations, the Company has

in the past consistently generated a strong base level of

operating cash flow, even in periods of higher

commodity prices and restructuring of its operations.

These operating cash flows provide a good base of

underlying liquidity that the Company supplements

with credit facilities to provide longer-term funding and

to finance fluctuations in working capital levels.

Cash Flow from Operations Operating cash flow

for the year of $259.7 million compared to

$235.5 million last year. The increase in cash flow was

largely due to a reduction in long-term receivables and

an improvement in operating working capital, offset by

an increase in future tax assets.

Capital Expenditures Capital spending for the year

decreased to $152.1 million from $156.8 million last

year. The most significant investments in capital in

2005 included the construction of a new feed mill in

Atlantic Canada, a biodiesel plant in Quebec, and

environmental upgrades in the rendering operations in

the early part of the year. During 2005, the Company

completed the construction of a bakery in Rotherham,

England, which was commissioned in the second

quarter of 2005.

Debt Facilities The Company’s strategy related to

liquidity is to reduce reliance on any single source of

credit, maintain sufficient undrawn credit facilities and

to spread debt maturities over time to reduce refinancing

risk. In order to ensure continued access to

competitively priced credit, the Company’s policy is to

maintain its primary credit ratios and leverage at levels

that provide access to investment grade credit. In

circumstances where the Company determines it is

appropriate to reduce leverage, it will use equity or other

forms of liquidity as an additional source of capital.

Immediately following the acquisition of Schneider

Foods in April 2004, the Company commenced a

financial plan to strengthen its balance sheet and

liquidity position. Through a combination of strong

operating cash flows and an equity issue in December

2004, the Company significantly reduced its leverage

ratio, net debt to EBITDA (net debt to earnings

before income taxes, depreciation and amortization),

from a post acquisition high of 3.5x to 2.6x as at

December 31, 2005.

In December 2004, the Company refinanced its

short-term acquisition debt with longer-term debt

sourced in the U.S. and Canadian private placement

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

22

market. The Company’s core revolving bank facility

was increased in size and the term extended for three

years, maturing in December 2007. In January 2005,

the Company redeemed $80 million of its 6%

convertible debentures for cash and the remaining

$11 million were tendered for conversion to common

equity. After completing these transactions, the

Company had extended the average term of its debt

facilities and secured significant un-utilized committed

liquidity. These transactions are explained more fully in

Note 8 to the Consolidated Financial Statements.

At December 31, 2005, the Company had aggregate

credit facilities, including subsidiary debt, of $1.9 billion,

of which $1.2 billion was utilized (including

$77.6 million in respect of letters of credit). Subsidiary

debt facilities available amounted to $159.9 million, of

which $136.3 was utilized (including $8.1 million in

respect of letters of credit) at year end.

To access competitively priced financing, and to

further diversify its funding sources, the Company

operates several accounts receivable financing facilities.

At year end, the Company had $230.1 million (2004:

$209.7 million) outstanding under these facilities.

Where cost effective to do so, the Company may

finance automobiles, heavy equipment, computers and

office equipment with operating lease facilities.

Variable Interest Entities (“VIEs”) In 1999, the

Company entered into agreements, including a

conditional sales agreement, to finance $130.0 million

of the construction cost of a new hog processing facility

in Brandon, Manitoba. This financing provided the

Company with access to well priced funding. The

Company is required to make payments during the term

of the agreement and, at maturity in August 2006, it is

management’s intention to purchase the facility for

$78.0 million. At December 31, 2005, the Company

had outstanding commitments of $87.8 million (2004:

$100.8 million) related to the facility. Recent changes

in Canadian accounting standards required the

re-characterization of this arrangement (see Note 2(m)

to the Consolidated Financial Statements). Therefore,

commencing January 1, 2005, the Company included

the value of the Brandon asset and a related debt

amount of $87.8 million on its balance sheet.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

Contractual Obligations The following table provides information about certain of the Company’s significant

contractual obligations as at December 31, 2005.

Payments due by fiscal year

($ millions) Total 2006 2007 2008 2009 2010 After 2010

Long-term debt $ 1,143.3 $ 110.4 $ 81.7 $ 12.9 $ 175.9 $ 217.2 $ 545.2

Cross-currency swaps related

to long-term debt 98.5 — 23.3 — 5.8 23.3 46.1

Lease obligations 203.2 40.4 31.9 25.9 18.7 16.1 70.2

Total contractual obligations $ 1,445.0 $ 150.8 $ 136.9 $ 38.8 $ 200.4 $ 256.6 $ 661.5

Management is of the opinion that its cash flow and

sources of financing provide the Company with

sufficient resources to finance ongoing business

requirements and its planned capital expenditure

program. Additional details concerning financing are

set out in the Notes to the Consolidated Financial

Statements. As at December 31, 2005, the Company

was in compliance with all debt covenants.

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

23

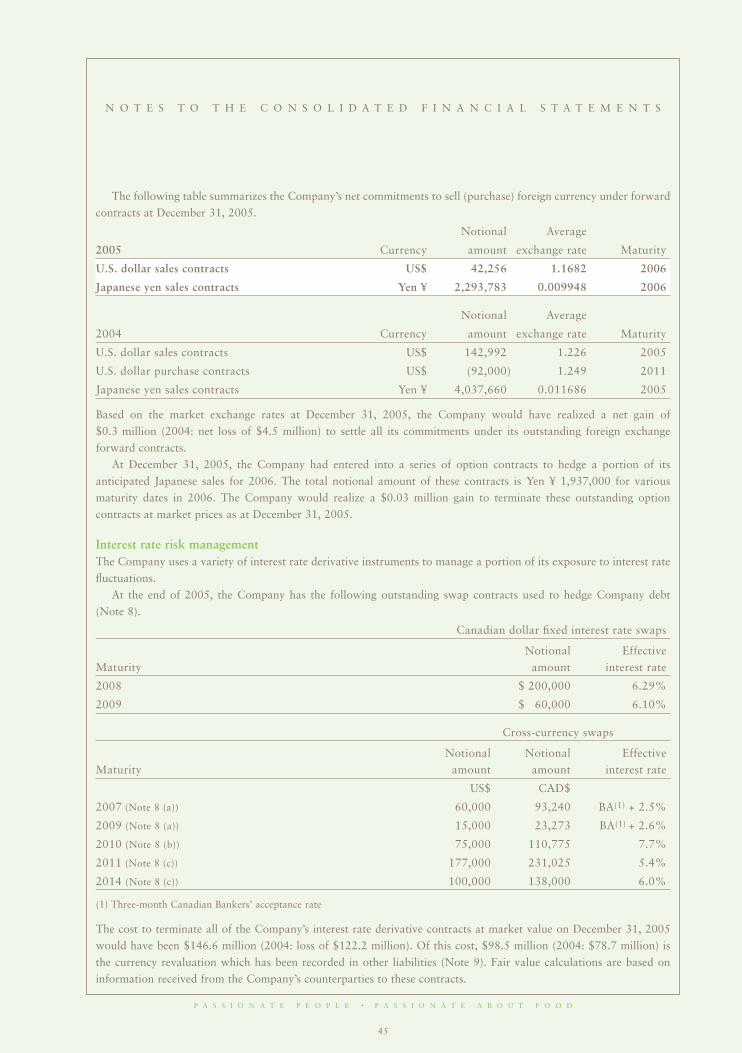

DERIVATIVES

Inherent in the food business is the exposure to market

risks from changes in interest rates, foreign exchange

rates and commodity prices (including wheat, feed

grains and livestock). When considered appropriate,

these exposures may be managed by the use of

derivative financial instruments, including interest rate

swaps, currency contracts, commodity futures and

options. Information on the Company’s material year

end derivative hedge positions is set out in Note 10 to

the Consolidated Financial Statements. If the Company

had not entered into these contracts, operating earnings

for 2005 would have been lower by $9.0 million (2004:

higher by $16.3 million) and interest expense would

have been lower by $19.2 million (2004: lower by

$17.7 million).

Management hedges commodities when it

determines that conditions are appropriate to mitigate

risks and reduce the risk of loss from adverse changes

in commodity prices. The Company attempts to closely

match commodity contract terms with the underlying

hedged exposure and continually measures the

effectiveness of the hedge in place.

The Company either enters into interest rate swaps

or has negotiated fixed interest rates on credit facilities

such that the interest payment on a relatively high

percentage of its outstanding debt is not exposed to

fluctuations in interest rates. Details of the Company’s

outstanding derivative transactions are set out in

Note 10 to the Consolidated Financial Statements. At

December 31, 2005, 86% (2004: 96%) of the

Company’s exposure to interest rate fluctuations was

hedged or fixed.

The Company periodically enters into foreign

exchange hedges to fix certain of its foreign currency

exposure. This involves the use of cross-currency swaps

and foreign currency-denominated debt to hedge the

Company’s balance sheet exposure and the use of spot,

forward and option contracts to manage the

Company’s exposure to foreign currency cash flows.

All hedging and derivative activity is in accordance

with risk management policies that specify both the

type of allowed derivatives, maximum trading

exposures and the definition of allowable hedge

activity. Counterparty risk is monitored and controlled

carefully, and no derivative instruments may be entered

into with a counterparty whose public credit rating is

less than A credit quality.

During 2005, there were no material derivative

gains or losses related to the ineffectiveness of hedges

and no material hedges were discontinued in 2005 as a

result of it becoming probable that a forecasted

transaction would not occur.

SEASONALITY

The Company is sufficiently large and diversified that

seasonal factors within each operation and business tend

to offset each other and in isolation do not have a

material impact on the Company’s consolidated

earnings. For example, pork processing margins tend to

be higher in the back half of the year when hog prices

historically decline, and as a result, earnings from hog

production tend to be lower. Strong demand for grilled

meat products positively affects the fresh and processed

meats operations, while back to school promotions

support increased sales of bakery, sliced meats and lunch

items. Higher demand for turkey and ham products

occurs in the fourth quarter and spring holiday seasons.

SHARE CAPITAL AND DIVIDENDS

During 2005, the Company repurchased 127,000

common shares for cancellation pursuant to a normal

course issuer bid at an average exercise price of $15.66

per share. The excess of the purchase cost over the book

value of the shares was charged to retained earnings.

M A N A G E M E N T ’ S D I S C U S S I O N A N D A N A L Y S I S

P A S S I O N A T E P E O P L E • P A S S I O N A T E A B O U T F O O D

24

In each of the quarters of 2005, the Company

declared and paid cash dividends of $0.04 per common

share. This represents a total dividend of $0.16 per

common share and aggregate dividend payments of

$20 million and $18 million in the prior year.

As at January 31, 2006, there were 127,761,512

common shares of the Company issued and

outstanding.

ENVIRONMENT

Maple Leaf Foods is conscious of its environmental

responsibilities. Each of its businesses operates within

the framework of an environmental policy entitled

“Our Environmental Commitment” that is approved

by the Board of Directors’ Environment, Health and

Safety Committee. The Company’s environmental

program is monitored on a regular basis by the

Committee, including compliance with regulatory

requirements, the use of internal environmental

specialists and independent, external environmental

analyses. The Company continues to invest in

environmental infrastructure related to water, waste

and air emissions to ensure that environmental

standards continue to be met or exceeded, while

implementing procedures to minimize the impact of

operations on the environment. Expenditures related to

current environmental requirements are not expected to

have a material effect on the financial position or

earnings of the Company.

RISK FACTORS

The Company operates in the food processing sector,

and is therefore subject to risks and uncertainties

related to these businesses that may have adverse effects

on the Company’s results of operations and financial

position. Some of these risks and uncertainties are

outlined below. Prospective investors should carefully

review and evaluate the following risk factors together

with all of the other information contained in this

report. The risk factors described below are not the

only risk factors facing the Company. The Company

may be subject to risks and uncertainties not described

below that the Company is not presently aware of or

that the Company may currently deem insignificant.

Food Safety and Consumer Health The Company

is subject to risks that affect the food industry in

general, including risks posed by food spoilage or

contamination, consumer product liability, and the

potential costs and disruptions of a product recall. The

Company actively manages these risks by maintaining

strict and rigorous controls and processes in its

manufacturing facilities and distribution systems. The

Company’s facilities are subject to audit by federal

health agencies in Canada and similar institutions

outside of Canada, and performs its own audits to

ensure compliance with its internal standards, which

are generally at, or higher than, regulatory agency