412 Customer Account Transfer Section, Inc. A Section of SIFMA - 1 ACATS Spring Seminar 2011...

60

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 1 ACATS ACATS Spring Seminar 2011 Spring Seminar 2011 Welcoming Remarks Joseph Zaets – Morgan Stanley President - SIFMA CAT Section

-

Upload

charity-fowler -

Category

Documents

-

view

214 -

download

1

Transcript of 412 Customer Account Transfer Section, Inc. A Section of SIFMA - 1 ACATS Spring Seminar 2011...

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 1

ACATSACATSSpring Seminar 2011Spring Seminar 2011

Welcoming Remarks

Joseph Zaets – Morgan Stanley

President - SIFMA CAT Section

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 2

SIFMAReport

Thomas P. TierneyVice President

Operations, Technology and BCP

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 3

Questions?

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 4

DTCC Update

Louis LeporeLouis LeporeDTCCDTCC

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 5

AgendaAgenda

I.I. Non-CNS ACATS ProposalNon-CNS ACATS Proposal Mutual FundsMutual Funds Other Non-CNS Settling AssetsOther Non-CNS Settling Assets

II.II. ACATS Default PricingACATS Default Pricing

III.III. ACATS Fund Registration (FR) ACATS Fund Registration (FR) ModificationsModifications

IV.IV. ACATS Other ACATS Other

V.V. ACATS StatisticsACATS Statistics

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 6

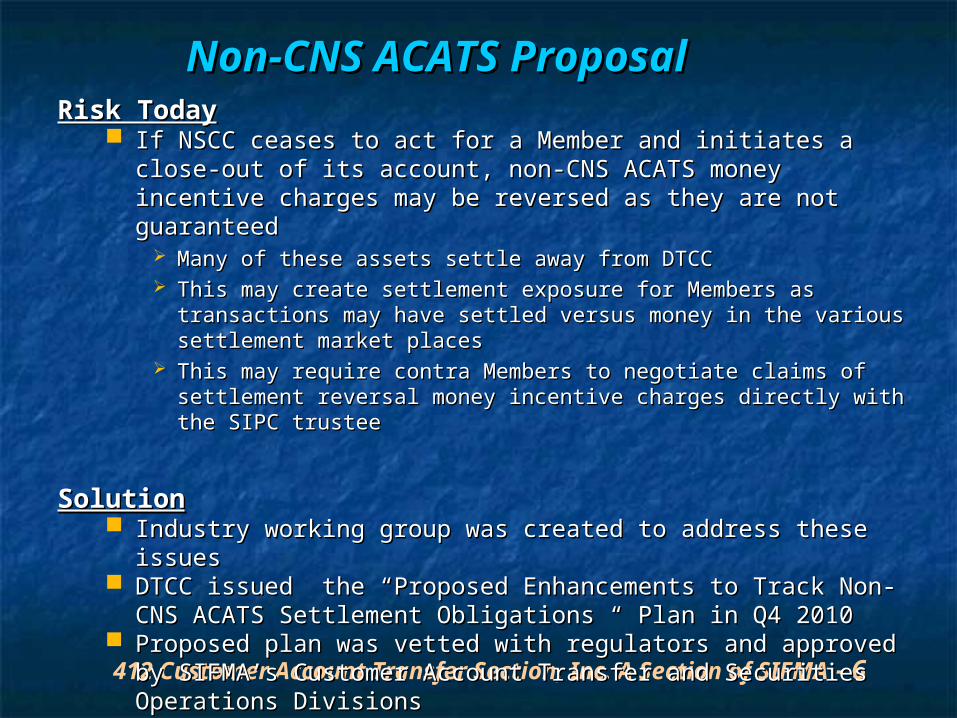

Non-CNS ACATS ProposalNon-CNS ACATS Proposal Risk TodayRisk Today

If NSCC ceases to act for aIf NSCC ceases to act for a Member and initiates a close-out of its Member and initiates a close-out of its account, non-CNS ACATS money incentive charges may be account, non-CNS ACATS money incentive charges may be reversed as they are not guaranteedreversed as they are not guaranteed

Many of these assets settle away from DTCCMany of these assets settle away from DTCC This may create settlement exposure for Members as transactions This may create settlement exposure for Members as transactions

may have settled versus money in the various settlement market may have settled versus money in the various settlement market placesplaces

This may require contra Members to negotiate claims of settlement This may require contra Members to negotiate claims of settlement reversal money incentive charges directly with the SIPC trustee reversal money incentive charges directly with the SIPC trustee

SolutionSolution Industry working group was created to address these issues Industry working group was created to address these issues DTCC issued the “Proposed Enhancements to Track Non-CNS DTCC issued the “Proposed Enhancements to Track Non-CNS

ACATS Settlement Obligations “ Plan in Q4 2010ACATS Settlement Obligations “ Plan in Q4 2010 Proposed plan was vetted with regulators and approved by Proposed plan was vetted with regulators and approved by

SIFMA’s Customer Account Transfer and Securities Operations SIFMA’s Customer Account Transfer and Securities Operations Divisions Divisions

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 7

Mutual Funds Proposal Mutual Funds Proposal Defined Proposed ModificationsDefined Proposed Modifications

1)1) Add Settle-Prep Status 300 to all non standard ACATS transfers Add Settle-Prep Status 300 to all non standard ACATS transfers that contain a mutual fund asset with settlement location 10 that contain a mutual fund asset with settlement location 10 (ACATS- Fund/SERV)(ACATS- Fund/SERV) Ensures ACATS settlement date of transfer always equals last day Ensures ACATS settlement date of transfer always equals last day

Mutual Fund Company can respond to re-registrationMutual Fund Company can respond to re-registration Impacts the following non-standard transfer types:Impacts the following non-standard transfer types:

Partial Transfer Receiver (PTR)Partial Transfer Receiver (PTR) Partial Transfer Deliverer (PTD)Partial Transfer Deliverer (PTD) Residual Credit (RCR)Residual Credit (RCR)

2)2) Segregate all mutual fund transaction activity (settlement Segregate all mutual fund transaction activity (settlement location 10 ACATS- Fund/SERV) within NSCC money settlement location 10 ACATS- Fund/SERV) within NSCC money settlement code 007code 007 Original incentive charges for these assets will be removed from Original incentive charges for these assets will be removed from

NSCC money settlement code 006/008 for consolidation and tracking NSCC money settlement code 006/008 for consolidation and tracking purposespurposes

Acknowledgement reversal charges will continue to be applied Acknowledgement reversal charges will continue to be applied under NSCC money settlement code 007 under NSCC money settlement code 007

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 8

3)3) Create a new MRO Reversal File and/or MRO Comma Delimited Create a new MRO Reversal File and/or MRO Comma Delimited File for reversals resulting from a File for reversals resulting from a Member close-out eventMember close-out event

4)4) Create a new NSCC money settlement code for posting of Create a new NSCC money settlement code for posting of mutual fund asset incentive money reversals resulting from a mutual fund asset incentive money reversals resulting from a Member close-out eventMember close-out event

Next StepsNext Steps Finalize requirements with industry working group - Q1 2011Finalize requirements with industry working group - Q1 2011 Begin development and issue important notices - Q2 2011 Begin development and issue important notices - Q2 2011 Begin testing - Q3 2011Begin testing - Q3 2011 Implementation - Q4 2011Implementation - Q4 2011

Defined Proposed Modifications (continued)

Mutual Funds Proposal Mutual Funds Proposal

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 9

Other Non-CNS ACATS Assets ProposalOther Non-CNS ACATS Assets ProposalConceptual Proposed SolutionConceptual Proposed Solution

For the following non-CNS ACATS assets excluding cash, For the following non-CNS ACATS assets excluding cash, foreign assets and limited partnerships:foreign assets and limited partnerships: Members would settle these assets effectively “free of value” on Members would settle these assets effectively “free of value” on

ACATS settlement dateACATS settlement date NSCC would utilize its Obligation Warehouse (OW) to track the NSCC would utilize its Obligation Warehouse (OW) to track the

settlement status of these ACATS Obligationssettlement status of these ACATS Obligations NSCC would apply incentive charges only on those transactions NSCC would apply incentive charges only on those transactions

which have not completed or failedwhich have not completed or failed Members would receive instructions from NSCC to re-price the Members would receive instructions from NSCC to re-price the

settlement money on these failed transactions to the original settlement money on these failed transactions to the original ACATS market valueACATS market value

Members would subsequently settle these failed transactions Members would subsequently settle these failed transactions versus the original ACATS market value versus the original ACATS market value

Next StepsNext Steps Begin design of this solution with industry working group - Q2 Begin design of this solution with industry working group - Q2

2011 2011 Implementation - Q4 2012 Implementation - Q4 2012

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 10

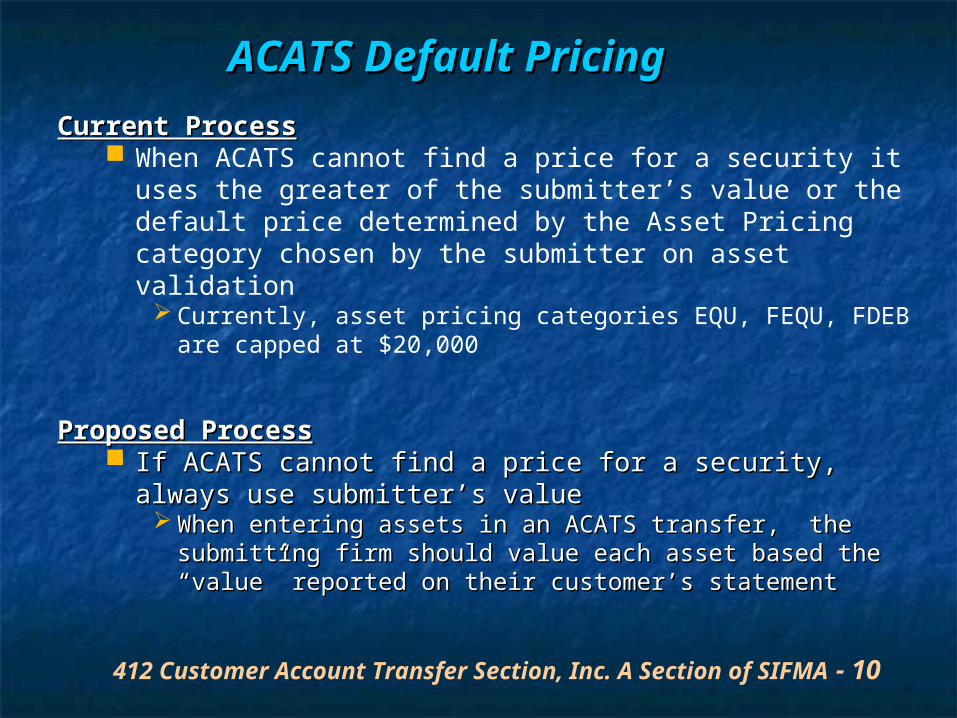

ACATS Default ACATS Default PricingPricingCurrent ProcessCurrent Process

When ACATS cannot find a price for a security it uses the greater of the submitter’s value or the default price determined by the Asset Pricing category chosen by the submitter on asset validation

Currently, asset pricing categories EQU, FEQU, FDEB are capped at $20,000

Proposed ProcessProposed Process If ACATS cannot find a price for a security, always use If ACATS cannot find a price for a security, always use

submitter’s valuesubmitter’s value When entering assets in an ACATS transfer, the submitting When entering assets in an ACATS transfer, the submitting

firm should value each asset based the “value” reported on firm should value each asset based the “value” reported on their customer’s statementtheir customer’s statement

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 11

ACATS Fund Registration (FR) ACATS Fund Registration (FR) ModificationsModifications The following changes will be made to support the passage of The following changes will be made to support the passage of

cost basis on mutual fund transactions and be uniform with cost basis on mutual fund transactions and be uniform with the changes on the Fund/SERV 018 recordthe changes on the Fund/SERV 018 record Add a new social code value 63 – S CorporationAdd a new social code value 63 – S Corporation

Update the values on the “Cost Basis Code” field as follows:Update the values on the “Cost Basis Code” field as follows:

Value Description

0 = Unknown

1 = FIFO (First In First Out)

2 = LIFO (Last In First Out)

3 = High Cost

4 = Low Cost

5 = Average Cost

6 = Select Lot

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 12

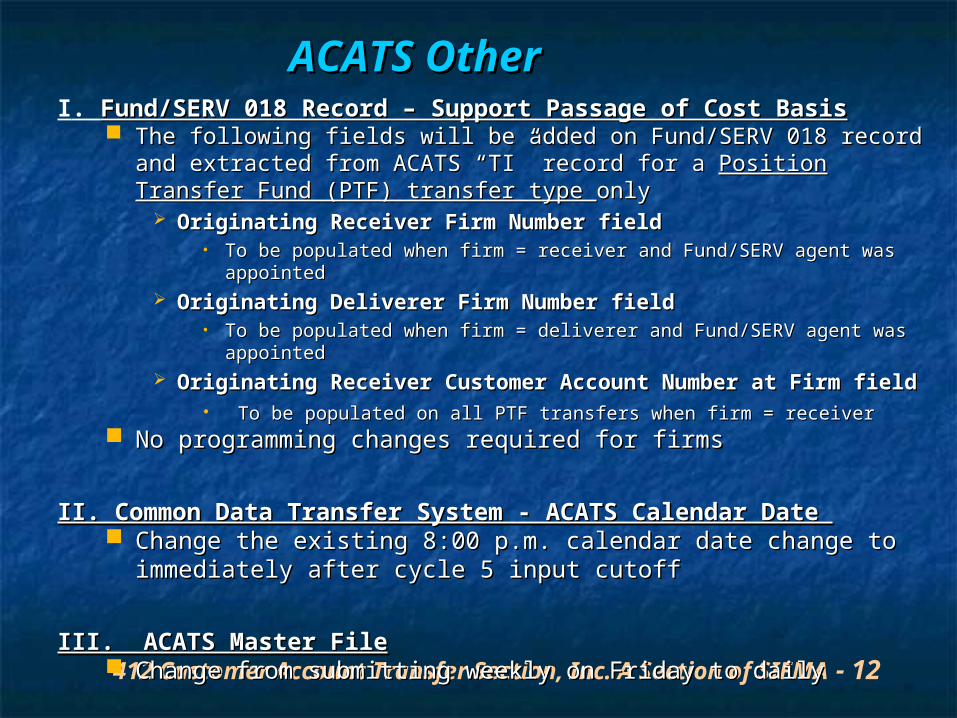

ACATS Other ACATS Other I. Fund/SERV 018 Record – Support Passage of Cost BasisFund/SERV 018 Record – Support Passage of Cost Basis

The following fields will be added on Fund/SERV 018 record and The following fields will be added on Fund/SERV 018 record and extracted from ACATS “TI” record for a extracted from ACATS “TI” record for a Position Transfer Fund (PTF) Position Transfer Fund (PTF) transfer type transfer type onlyonly

Originating Receiver Firm Number fieldOriginating Receiver Firm Number field• To be populated when firm = receiver and Fund/SERV agent was appointedTo be populated when firm = receiver and Fund/SERV agent was appointed

Originating Deliverer Firm Number fieldOriginating Deliverer Firm Number field• To be populated when firm = deliverer and Fund/SERV agent was appointedTo be populated when firm = deliverer and Fund/SERV agent was appointed

Originating Receiver Customer Account Number at Firm fieldOriginating Receiver Customer Account Number at Firm field• To be populated on all PTF transfers when firm = receiverTo be populated on all PTF transfers when firm = receiver

No programming changes required for firmsNo programming changes required for firms

II. Common Data Transfer System - ACATS Calendar Date II. Common Data Transfer System - ACATS Calendar Date Change the existing 8:00 p.m. calendar date change to Change the existing 8:00 p.m. calendar date change to

immediately after cycle 5 input cutoff immediately after cycle 5 input cutoff

III. ACATS Master FileIII. ACATS Master File Change from submitting weekly on Friday to daily Change from submitting weekly on Friday to daily

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 13

ACATS StatisticsACATS Statistics

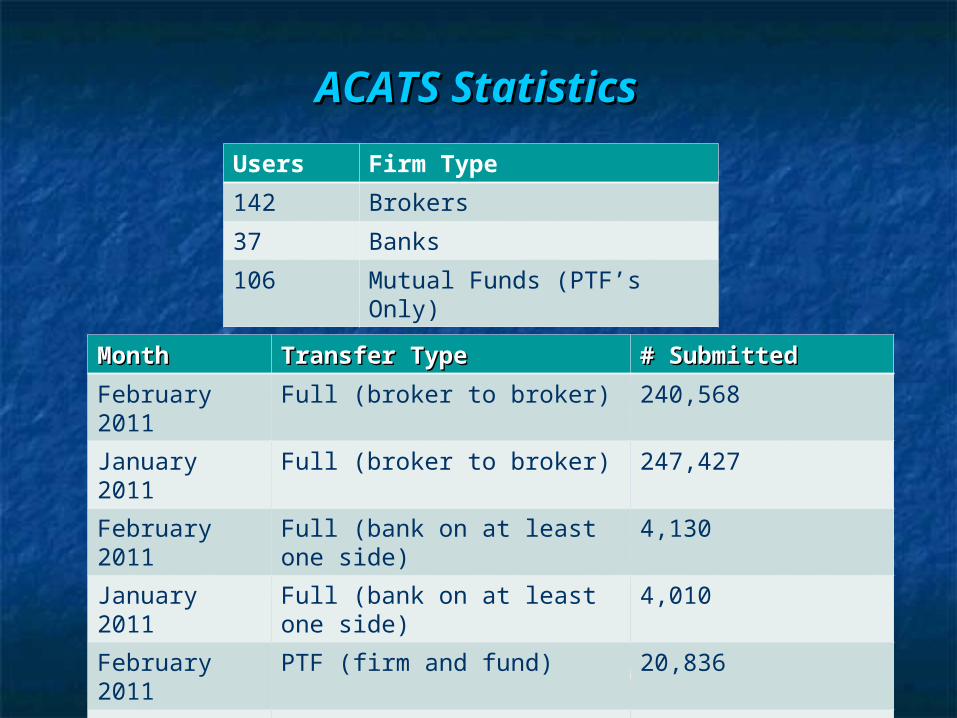

Users Firm Type

142 Brokers

37 Banks

106 Mutual Funds (PTF’s Only)

Month Month Transfer Type Transfer Type # Submitted# Submitted

February 2011

Full (broker to broker) 240,568

January 2011 Full (broker to broker) 247,427

February 2011

Full (bank on at least one side)

4,130

January 2011 Full (bank on at least one side)

4,010

February 2011

PTF (firm and fund) 20,836

January 2011 PTF (firm and fund) 18,892

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 14

Questions?

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 15

Process Service Improvement Process Service Improvement Subcommittee Updates Subcommittee Updates

Scott BradyScott Brady

Merrill LynchMerrill Lynch

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 16

Process Service Process Service Improvement Improvement

Subcommittee UpdateSubcommittee Update Committee meets monthlyCommittee meets monthly Discusses potential enhancements to Discusses potential enhancements to

the ACAT systemthe ACAT system Reviews DTCC changes and updatesReviews DTCC changes and updates We encourage new ideas and We encourage new ideas and

creative thinkingcreative thinking To join contact Scott BradyTo join contact Scott Brady

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 17

2011 Subcommittee 2011 Subcommittee PrioritiesPriorities

Non-ACAT TransfersNon-ACAT Transfers ““Hard to Transfer” assetsHard to Transfer” assets

Transfers with BanksTransfers with Banks Cost BasisCost Basis ACAT Settlement EnhancementsACAT Settlement Enhancements Non-Purpose LoansNon-Purpose Loans Reducing RejectsReducing Rejects

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 18

Current or Recent Initiatives Current or Recent Initiatives

Non-ACAT Working GroupNon-ACAT Working Group Identifying and sharing best practicesIdentifying and sharing best practices Improving Firm to Firm communicationImproving Firm to Firm communication Reducing rejects and DK’ed transfersReducing rejects and DK’ed transfers Improving transfer timeframesImproving transfer timeframes

Transfers with BanksTransfers with Banks Bank ACATSBank ACATS

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 19

Current or Recent Initiatives Current or Recent Initiatives

Cost BasisCost Basis Identifying and sharing best practicesIdentifying and sharing best practices

Non-Purpose LoansNon-Purpose Loans Transfers of Client Collateral AccountsTransfers of Client Collateral Accounts Different ways of doing this across the Different ways of doing this across the

industryindustry

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 20

Reducing RejectsReducing Rejects

Industry Average of 10%Industry Average of 10% Improving Improving We can do betterWe can do better

Rejects Lead to:Rejects Lead to: Re-workRe-work ComplaintsComplaints Unhappy clientsUnhappy clients

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 21

Questions?

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 22

Seminar Break

Seminar will resume in 15 minutes

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 23

Alternative Investments

LeeAnne CalcianoJP Morgan Clearing Corp

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 24

Alternative InvestmentsAlternative Investments

UTILIZING A CENTRALIZED PROCESS

REDUCE COST IMPROVE PRODUCTIVITY

MINIMIZE RISK OF FINES AND PENALTYS

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 25

Broker Dealer Challenges Surrounding Alternative Investments

Standard Process for Alternative Investment One Stop Shopping

Introduction to the DTCC AIP Platform and Related Benefits

OVERVIEWOVERVIEWMoving Forward TogetherMoving Forward Together

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 26

Meeting 15C3-3 Regulatory Requirements

Monthly Balancing with Sponsors

Non-Bank Custodial Responsibilities

Pricing Alternative Investments

Late Tax Filing

Completion of the Entire ACAT Transfer Process

Identification of Adequate Contact Information

Challenges Challenges Daily “Points of Pain” – Adding Daily “Points of Pain” – Adding

ComplexityComplexity

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 27

Benefits of Developing a Standard Practice Across the Broker Dealer Community

Creation of Standardized Agreements For all Broker Dealers

Require Sponsors to Join DTCC AIP Platform

Standard Stream-Lined ProcessStandard Stream-Lined Process Closing LoopholesClosing Loopholes

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 28

Introduction to the DTCC and AIPIntroduction to the DTCC and AIPSafeguarding Our IndustrySafeguarding Our Industry

AIP is Based on Fund/SERV Mutual Fund Model

AIP Platform or Conduit Links Global Market Participants- brokers/dealers, fund managers,

administrators and custodians - provide straight through processing

AIP is Intended to Standardize Industry Communication - security, investor holdings, orders and activities

AIP Provides Scalability and Improved Efficiencies- reduced operational risk and lower costs

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 29

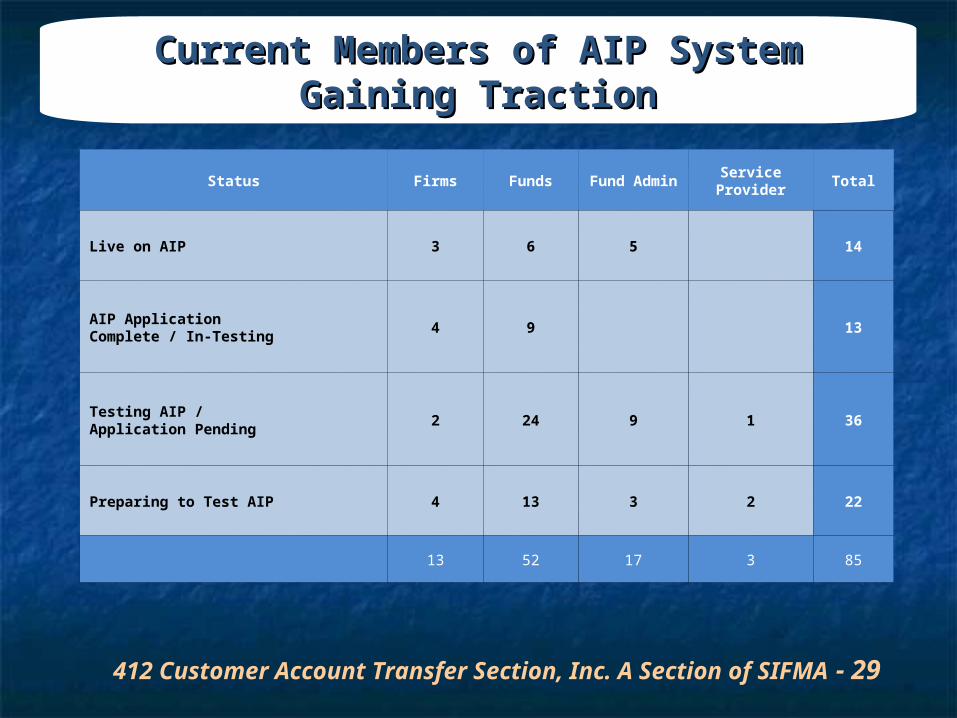

Current Members of AIP SystemCurrent Members of AIP SystemGaining TractionGaining Traction

Status Firms Funds Fund Admin Service Provider Total

Live on AIP 3 6 5 14

AIP Application Complete / In-Testing

4 9 13

Testing AIP / Application Pending

2 24 9 1 36

Preparing to Test AIP 4 13 3 2 22

13 52 17 3 85

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 30

Next StepsNext StepsOpen DiscussionOpen Discussion

Leeanne CalcianoLeeanne Calciano AssociateAssociate 1-347-643-19201-347-643-1920Leeanne.Calciano @JPMorgan.comLeeanne.Calciano @JPMorgan.com

UTILIZING A CENTRALIZED PROCESS

REDUCE COST

IMPROVE PRODUCTIVITY MINIMIZE RISK OF FINES AND PENALTYS

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 31

Questions?

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 32

Cost Basis Working Group Discussions

Ellen Bocina - Fidelity

Kevin McCosker - Pershing

Louis Lepore – DTCC

Derek Yen – Edward Jones

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 33

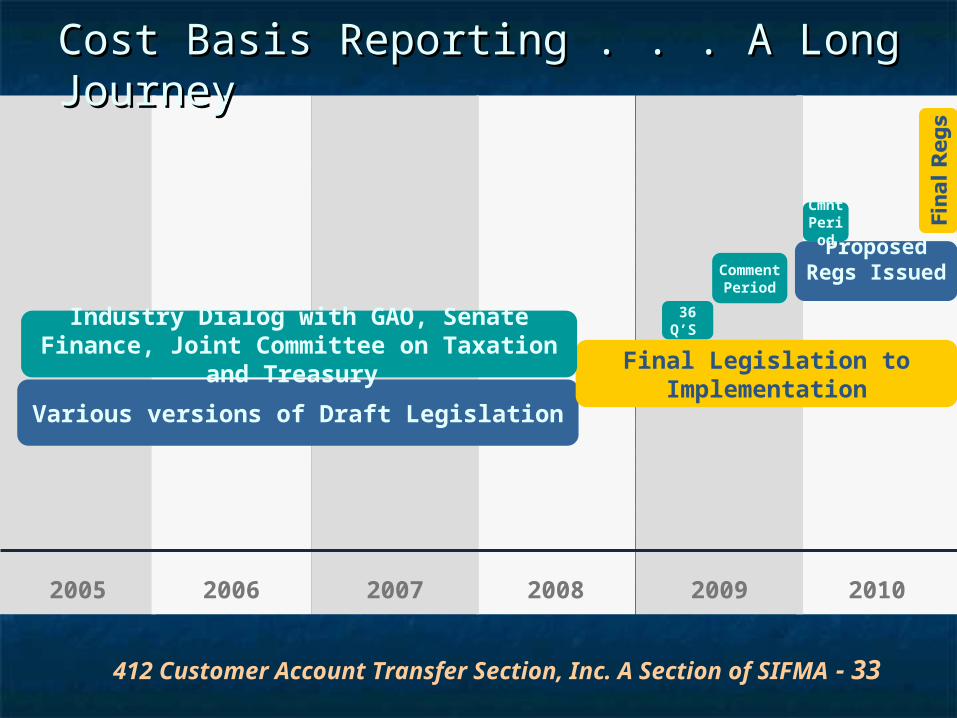

2005 20102009200820072006

Cost Basis Reporting . . . A Long Cost Basis Reporting . . . A Long JourneyJourney

Various versions of Draft Legislation

Comment Period

Final Legislation to Implementation

Proposed Regs Issued

36 Q’S Industry Dialog with GAO, Senate Finance, Joint Committee on Taxation and Treasury

Cmnt Period

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 34

TransfersTransfers

Challenges with Non-ACAT Transfers

Matching

Manual statements

Corrections

Gifted / Inherited

Transfer Reversals

Conversions

Third Party Transfers

Accommodating Mutual Funds

File Changes

Average Cost

Original Cost

Test with Mutual Funds

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 35

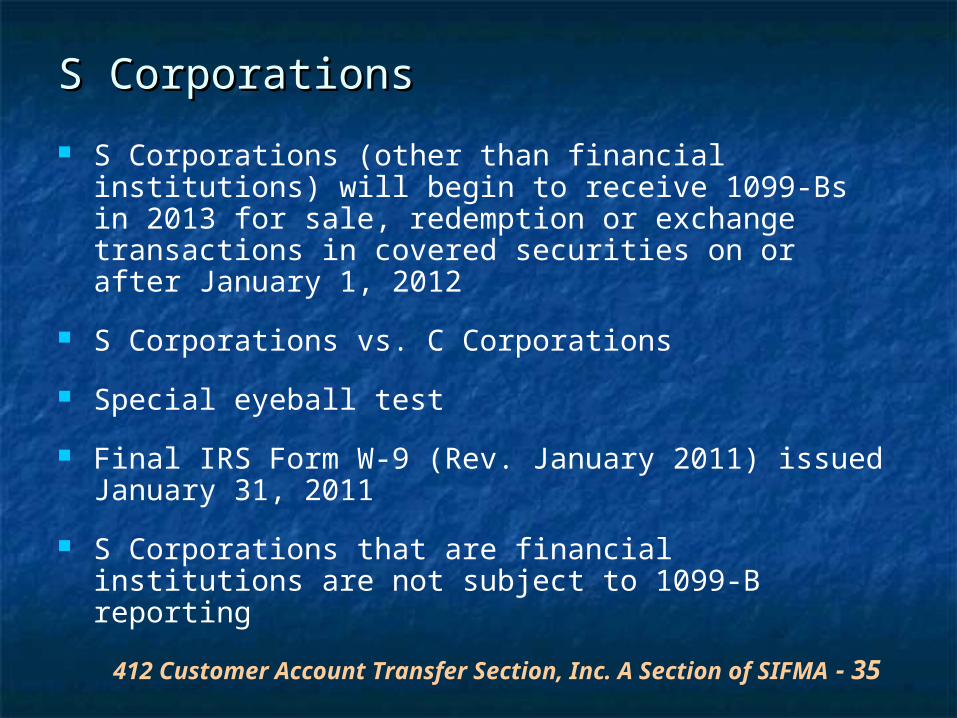

S CorporationsS Corporations

S Corporations (other than financial institutions) will begin to receive 1099-Bs in 2013 for sale, redemption or exchange transactions in covered securities on or after January 1, 2012

S Corporations vs. C Corporations

Special eyeball test

Final IRS Form W-9 (Rev. January 2011) issued January 31, 2011

S Corporations that are financial institutions are not subject to 1099-B reporting

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 36

Changes to IRS 1099 BChanges to IRS 1099 B> \

Box 1b: requires the date of acquisition (allows for combining non-covered, short-term covered and long-term covered lots)

Box 3: requires the reporting of cost or other basis of the security

Box 5: requires the reporting of disallowed wash sale losses

Box 6: requires notification if the security is uncovered

Box 7: requires reporting of the amount of the gain or loss

Box 8: requires identification of the gain or loss as short-term or long-term

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 37

Tax FormsTax Forms

Substitute Forms 1099-B

Include all new required information

Easy for clients to follow

Supplemental Information

Display of dispositions of covered and noncovered securities

Reconciliation with the breakdown of lots on 1099-B

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 38

Education, Communication and Education, Communication and SupportSupport

InternalBranchClient

Educational Tools Policies and

Procedures Training Guides Webinars Round Tables White Papers

Support Needs Phone Calls Service Requests Self Service Tools

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 39

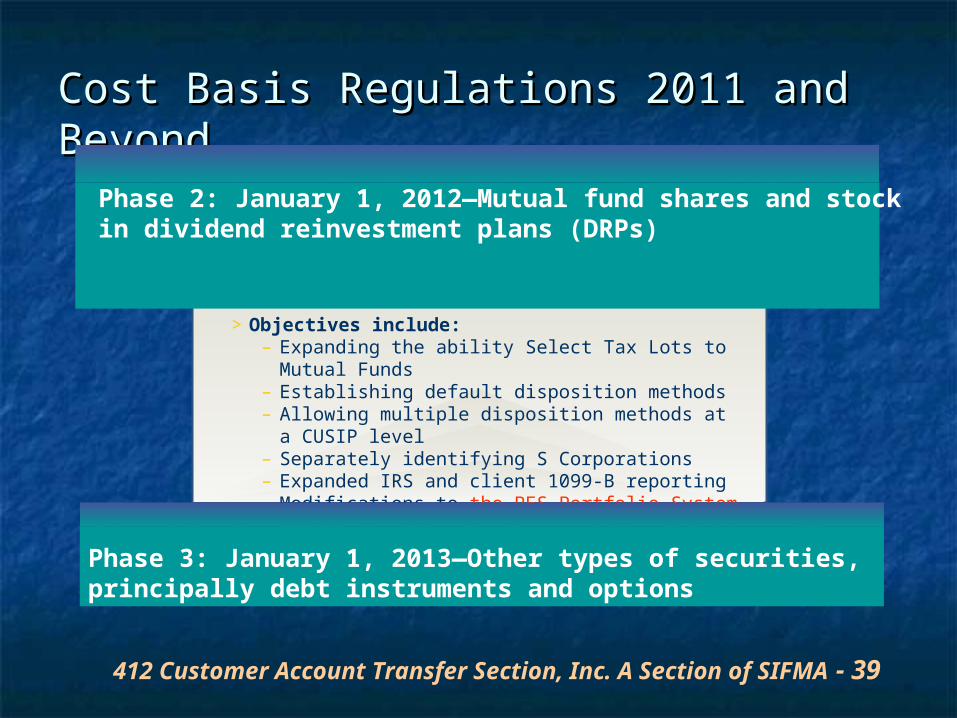

Cost Basis Regulations 2011 and Cost Basis Regulations 2011 and Beyond Beyond

Phase 2: January 1, 2012—Mutual fund shares and stock in dividend reinvestment plans (DRPs)

> Objectives include:– Expanding the ability Select Tax Lots to Mutual

Funds – Establishing default disposition methods – Allowing multiple disposition methods at a

CUSIP level– Separately identifying S Corporations– Expanded IRS and client 1099-B reporting– Modifications to the PES Portfolio System (PORT)

Phase 3: January 1, 2013—Other types of securities, principally debt instruments and options

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 4040

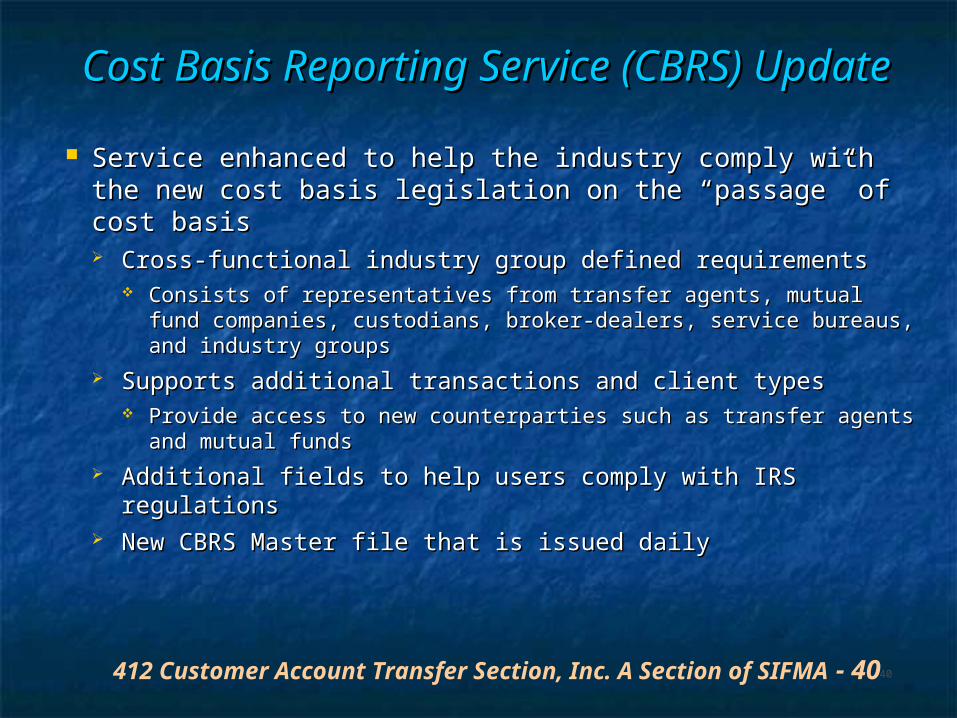

Cost Basis Reporting Service (CBRS) Cost Basis Reporting Service (CBRS) UpdateUpdate

Service enhanced to help the industry comply with the new Service enhanced to help the industry comply with the new cost basis legislation on the “passage” of cost basiscost basis legislation on the “passage” of cost basis Cross-functional industry group defined requirementsCross-functional industry group defined requirements

Consists of representatives from transfer agents, mutual fund Consists of representatives from transfer agents, mutual fund companies, custodians, broker-dealers, service bureaus, and industry companies, custodians, broker-dealers, service bureaus, and industry groupsgroups

Supports additional transactions and client typesSupports additional transactions and client types Provide access to new counterparties such as transfer agents and Provide access to new counterparties such as transfer agents and

mutual fundsmutual funds Additional fields to help users comply with IRS regulationsAdditional fields to help users comply with IRS regulations New CBRS Master file that is issued dailyNew CBRS Master file that is issued daily

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 4141

Cost Basis Reporting Service (CBRS) Cost Basis Reporting Service (CBRS) UpdateUpdate

New system implemented to production on December 10, New system implemented to production on December 10, 20102010

Firms are required to sign documentation to use the new Firms are required to sign documentation to use the new service service Service moved from NSCC to DTCC Solutions to support non-Service moved from NSCC to DTCC Solutions to support non-

traditional DTCC participants/memberstraditional DTCC participants/members CBRS Working Group meets monthly CBRS Working Group meets monthly

Addresses questions/inquires about CBRS serviceAddresses questions/inquires about CBRS service Chaired by Lydia Midwood, Product Manager at DTCCChaired by Lydia Midwood, Product Manager at DTCC

CBRS User guide has been created for best practicesCBRS User guide has been created for best practices Available on CBRS WebsiteAvailable on CBRS Website Working document Working document

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 4242

CBRS – Website LinksCBRS – Website Links

CBRS File Formats and User GuideCBRS File Formats and User Guide http://www.dtcc.com/products/documentation/cs/cbrs.php#layout

s_one

CBRS Frequently Asked Questions (FAQs)CBRS Frequently Asked Questions (FAQs) http://www.dtcc.com/customer/participant/cbrs/index.php

Important NoticesImportant Notices http://www.dtcc.com/legal/imp_notices/dtccsolutions/2010.php http://www.dtcc.com/legal/imp_notices/dtccsolutions/2011.phphttp://www.dtcc.com/legal/imp_notices/dtccsolutions/2011.php

CBRS Customer Support HotlineCBRS Customer Support Hotline (888) 382-2721, Option 6, then 7, then 2(888) 382-2721, Option 6, then 7, then 2

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 43

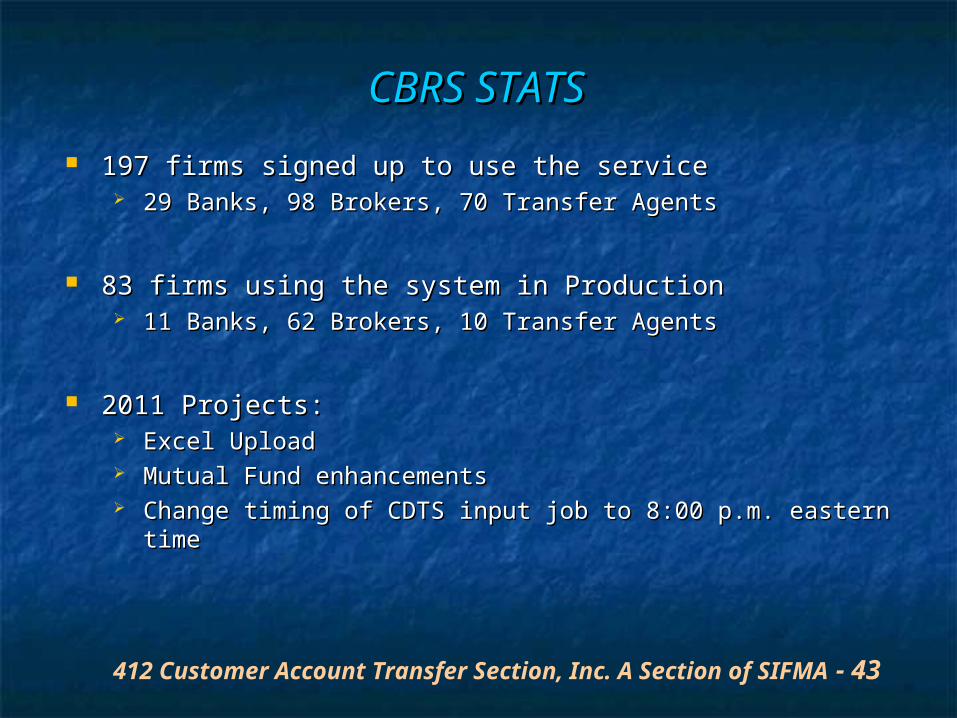

CBRS STATSCBRS STATS

197 firms signed up to use the service197 firms signed up to use the service 29 Banks, 98 Brokers, 70 Transfer Agents29 Banks, 98 Brokers, 70 Transfer Agents

83 firms using the system in Production83 firms using the system in Production 11 Banks, 62 Brokers, 10 Transfer Agents11 Banks, 62 Brokers, 10 Transfer Agents

2011 Projects:2011 Projects: Excel UploadExcel Upload Mutual Fund enhancementsMutual Fund enhancements Change timing of CDTS input job to 8:00 p.m. eastern timeChange timing of CDTS input job to 8:00 p.m. eastern time

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 44

Industry Communication/Participation

SIFMA CAT Cost Basis Sub Committee Various sub groups Contact List

DTCC CBRS Conference Call BDAC Cost Basis Task Force Future collaboration of all 3 groups

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 45

Questions?

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 46

Lunch BreakReminder

Lunch break Seminar will resume in 45 minutes

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 47

Mutual Fund Panel Discussion

Teri Maglio – Charles Schwab

Kelle Hennier – DST Systems

Jeff Naylor – Sungard

Scott Brady – Merrill Lynch

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 48

Mutual Fund TransfersMutual Fund Transfers Mutual Fund Transfer ChallengesMutual Fund Transfer Challenges

Inconsistent Document RequirementsInconsistent Document Requirements Original vs. CopyOriginal vs. Copy Medallion Signature requirement varies Medallion Signature requirement varies

Inconsistent Delivery RequirementsInconsistent Delivery Requirements EmailEmail FaxFax OvernightOvernight

No Dedicated ContactsNo Dedicated Contacts

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 49

Mutual Fund TransfersMutual Fund Transfers Mutual Fund Transfer ChallengesMutual Fund Transfer Challenges

Unable to Obtain Status of TransferUnable to Obtain Status of Transfer Account Mask on Client StatementAccount Mask on Client Statement CUSIP’s not Enrolled for ACATS CUSIP’s not Enrolled for ACATS

Fund/SERVFund/SERV Enforcing Purchase Minimums on Enforcing Purchase Minimums on

TransfersTransfers Inconsistent Processing TimeframesInconsistent Processing Timeframes

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 50

Mutual Fund TransfersMutual Fund Transfers Mutual Fund Best PracticesMutual Fund Best Practices

Dedicated Back Office ContactsDedicated Back Office Contacts Electronic Delivery of Transfer Electronic Delivery of Transfer

Instructions and Supporting DocumentsInstructions and Supporting Documents ACAT Fund/SERV ActivationACAT Fund/SERV Activation PTF ActivationPTF Activation No Minimums to TransfersNo Minimums to Transfers

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 51

PTF TransfersPTF Transfers PTF ChallengesPTF Challenges

IRA FeesIRA Fees Reject codes used inconsistentlyReject codes used inconsistently Unclear Account Mask on Client Unclear Account Mask on Client

StatementStatement Fund CUSIP is not ACATS Fund/SERV Fund CUSIP is not ACATS Fund/SERV

eligibleeligible Purged or No Response from Fund Purged or No Response from Fund

Company or Transfer AgentCompany or Transfer Agent

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 52

PTF TransfersPTF Transfers

PTF Best PracticesPTF Best Practices Consistent use of reject codesConsistent use of reject codes IRA Account Processing IRA Account Processing Dedicated Contacts for PTF TransfersDedicated Contacts for PTF Transfers Fund code excluded as part of fund Fund code excluded as part of fund

account number when initiating transferaccount number when initiating transfer

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 53

PTF TransfersPTF Transfers

Current UsersCurrent Users 17 firms submitted records in February 201117 firms submitted records in February 2011 106 Funds participating as of February 2011106 Funds participating as of February 2011

What can make it easier to pass basis?What can make it easier to pass basis? Increased participation by firms and fundsIncreased participation by firms and funds

CBRS already has transaction types established for PTF transfersCBRS already has transaction types established for PTF transfers Transaction Type 46 – Fund Deliverer/Firm ReceiverTransaction Type 46 – Fund Deliverer/Firm Receiver Transaction Type 51 – Firm Deliverer/Fund ReceiverTransaction Type 51 – Firm Deliverer/Fund Receiver Parties will use Parties will use Fund/SERV Control Number Fund/SERV Control Number from PTF as Transfer from PTF as Transfer

Control NumberControl Number Funds making more of their securities eligible for ACATS-Funds making more of their securities eligible for ACATS-

Fund/SERV Fund/SERV This would reduce manual transfers between firms and firmsThis would reduce manual transfers between firms and firms This would reduce manual transfers between firms and fundsThis would reduce manual transfers between firms and funds

Also eliminate system rejects on PTF transfer submissionAlso eliminate system rejects on PTF transfer submission

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 54

Non-CNS EnhancementsNon-CNS Enhancements

Non-CNS Enhancements - Phase Non-CNS Enhancements - Phase IIII ACATS Fund/SERVACATS Fund/SERV

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 55

Mutual Fund Cost BasisMutual Fund Cost Basis

Investment Company Institute (ICI)Investment Company Institute (ICI) Tax CommitteeTax Committee TA Advisory (TAAC)TA Advisory (TAAC) Broker-Dealer Advisory (BDAC)Broker-Dealer Advisory (BDAC)

BDAC CBR Task Force ActivitiesBDAC CBR Task Force Activities Lot DepletionLot Depletion ACATS-Fund/SERV, Networking, ManualACATS-Fund/SERV, Networking, Manual Best Practices / DocumentationBest Practices / Documentation

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 56

Average Cost ConsiderationsAverage Cost Considerations

Default Elections and Shareholder Default Elections and Shareholder ImpactImpact

Affirmative Election and RevocationAffirmative Election and Revocation TimingTiming ActivitiesActivities

TransfersTransfers During Revocation PeriodDuring Revocation Period After Revocation PeriodAfter Revocation Period

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 57

Mutual Fund Cost BasisMutual Fund Cost Basis

Next StepsNext Steps Fund Default ElectionsFund Default Elections ICI Cost Basis Workshop – Irvine, CAICI Cost Basis Workshop – Irvine, CA CBR for Mutual Funds – DTCC documentCBR for Mutual Funds – DTCC document Fund Onboarding for Mutual FundsFund Onboarding for Mutual Funds

Complete DevelopmentComplete Development TestingTesting

Operational preparations for January, 2012Operational preparations for January, 2012

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 58

BDAC Sharelot Task ForceBDAC Sharelot Task Force

Background and objectivesBackground and objectives ReconciliationReconciliation

Networking enhancementsNetworking enhancements Impact to CBRSImpact to CBRS TimelineTimeline

Future enhancements Future enhancements

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 59

Best Practice Best Practice RecommendationRecommendation

Tax ReportingTax Reporting Firm initiated Fund/SERV redemption Firm initiated Fund/SERV redemption

activity on fund controlled accountsactivity on fund controlled accounts Current practiceCurrent practice Best practice effective January 1, 2012Best practice effective January 1, 2012 JustificationJustification

Maintenance of dealer controlled Maintenance of dealer controlled accountsaccounts

412 Customer Account Transfer Section, Inc. A Section of SIFMA - 60

Questions?